code:pvc13(6) class: iii b.com credits :4 dr. a. samsunisa

TRANSCRIPT

JUSTICE BASHEER AHMED SAYEED COLLEGE FOR WOMEN(Autonomous) Chennai 18.

S.I.E.T.

DEPARTMENT OF COMMERCE

COST ACCOUNTING

Code:PVC13(6) Class: III B.Com

Credits :4

Dr. A. Samsunisa

26

July

20

20

Pre

sen

ter N

am

e

2Course Objectives:

∙ To describe the importance of cost ascertainment, reduction and control.

∙ To interpret the various concepts and elements of cost.

Learning Outcomes:

On successful completion of the course, the students will be able to

∙ Calculate total cost and unit cost of the company, appraise tenders and

quotations.

∙ Reconcile the cost and financial statement of a manufacturing company.

∙ Compute time rate/piece rate for assessing labour cost

26

July

20

20

Pre

sen

ter N

am

e

3

• UNIT I : Introduction 15 Hrs

• Cost – Costing – Cost Accounting – Cost Analysis – Concepts and Classifications – Installation of Costing

Systems – Cost Centre– Cost unit and Responsibility – Goals of Cost Accounting System – Usefulness of

Cost Accounting – Objectives of Costing.

• UNIT II : Unit cost and Reconciliation of Cost 20 Hrs

• Cost Sheets – Tender – Quotations – Reconciliation of Cost and Financial Accounts –

• Memorandum Reconciliation Statement method

• UNIT III : Materials 20 Hrs

• Material Purchase Control – Stores Control – Stores Department- EOQ – Stores records – ABC analysis –

VED analysis – Material Costing – Issue of materials – FIFO – LIFO – HIFO – SAM – WAM (Excluding base

stock method and standard price method)

26

July

20

20

Pre

sen

ter N

am

e

4UNIT IV : Labour 20 Hrs

Labour Cost – Computation and Control – Time Keeping – Methods of wage payment – Time rate and

piece rate system – Taylor–Merrick–Gantt’s Task –Halsey–Rowan – Idle time and over time –Labour

turnover.

UNIT V: Overheads 15 Hrs

Overheads – Classification – Allocation – Apportionment and Absorption – Accounting and control of

overheads – Primary and Secondary distribution – Machine Hour Rate.

The proportion between Theory and Problems shall be 20 :80.

BOOK FOR STUDY:

Reddy and Murthy . A, 2017, Cost accounting, Margham Publications.

BOOKS FOR REFERENCE:

1. Jain and Narang, 2013, Cost Accounting, Kalyani Publishers.

2. Maheswari S.N, 2009, Cost Accounting, Sultan Chand & Sons.

Definition► COST : The term ‘cost ‘ refers to be studied in relation to its purpose and

condition. As per the definition by Institute of Cost and Management Accountants (I.C.M.A), now known as Chartered Institute of Management Accountants (C.I.M.A), London ‘cost ’ is the amount of :

(a) Actual expenditure incurred on a given thing : and

(b) Notional expenditure attributable to a given thing.

► COSTING : The I.C.M.A London has been defined ‘costing’ as ascertainment of costs. It refers to the techniques and process of ascertainment costs and studies the principles and rules concerning the determination of cost of products and services.

Cost ascertainment is done by various methods and techniques such as job costing, unit costing, process costing ,historical or absorption costing, uniform costing, marginal costing, standard costing etc.,

26 July

2020Presenter Name

5

► COST ACCOUNTING : It is the method of accounting for cost. The of process of recording and accounting for all the elements of cost is called ’cost accounting’.

I.C.M.A has defines cost accounting as follows:

“the process of accounting for cost from the point of expenditure is incurred or committed to the establishment of its ultimate relationship with cost centers and cost units. In its widest usage it embraces the preparation of statistical data, the application of cost control methods and the ascertainment of the profitability of activities carried out or planned”.

► COST ACCOUNTANCY: It is an aid of management for decision making.

I.C.M.A. has defined as ’cost accountancy’ as follows:

“ The application of cost accounting and costing principles, methods and techniques to the science, art and practices of cost control and ascertainment of profitability. It includes the presentation of information derived therefore therefrom for the purpose of managerial decision making”. Thus , the term includes costing, cost accounting, budgetary control, cost control and cost audit.

26 July

2020

Presenter Name

6

NEED FOR COST ACCOUNTING:

► Intense competition in the market place has made the

managements of business and industrial units turn to the accounting

departments for accurate and relevant information and regarding

the ‘cost of products or services. Such as cost data is useful in

► (a)Fixation of selling prices;

► (b)Control of cost ; and

► (c)Decision making from alternative choices

26

July

20

20

Pre

sen

ter N

am

e

7

SCOPE AND OBJECTIVES OF COST ACCOUNTING

❖ Scope of Cost Accounting :

❑ The term ‘scope’ refers to field of activity.

❑ Cost accounting is concerned with ascertainment and control of cost.

❑ The information provided to the management is useful for cost control and cost reduction through functions of planning , decision making and control.

❑ Cost accounting confined itself to cost ascertainment and the presentation of same with the main objective of finding the product cost.

❑ With the development of business activity and introduction of large scale production, the scope of cost accounting was broadened and providing information for cost control and cost reduction has consumed equal significance along with finding out cost of production.

❑ The area of application of cost accounting has also widened. Initially, cost accounting was applied in manufacturing activities only.

❑ It is applied in service organisations , government organisations , local authorities , farms , extractive industries etc.,

26

July

20

20

Pre

sen

ter N

am

e

8

OBJECTIVES OF COST ACCOUNTING

► Main objectives or purpose or functions or aim of the cost accounting are;

a) Cost Accounting or Cost Ascertainment

b) Control of Cost

c) Reduction of cost

d) Fixation of selling prize

e) Providing information for framing business policy

26

Ju

ly 2

02

0

Pre

sen

ter N

am

e

9

INSTALLATION OF COSTING SYSTEM

► There is no system or method of costing which can fulfil the requirements of all types of Industries.

► To install most suitable system of costing in a particular organisations, the following should be noted;

a) Requisites of a good costing system

b) Steps necessary to install the system

c) Problems or practical difficulties in installing costing system

d) Steps to be adopted to overcome practical difficulties

26

July

20

20

Pre

sen

ter N

am

e

10

(a)Essentials Requisites of a good costing system

► Simple to Operate

► Flexibity

► Comparability

► Economy

► Timeliness

► Suitability to the enterprise

► Minimum changes in current setup

► Minimum clerical work

► Simplicity of forms and their standardisation

► Effective system to control materials and wages

► Procedure for overheads

► Recognition

► External Factors

► Cost Accountants

26

July

20

20

Pre

sen

ter N

am

e

11

(b)Steps necessary to install the system

► Objectives

► Organisations structure of the business

► Type and the method costing

► Cost records and books

► Technical aspects

► Control System

► Nature of product and business

► Collection of Data

► Cooperation of Staff

► Organising the cost office

► Relationship of cost office to other departments

26

July

20

20

Pre

sen

ter N

am

e

12

(c)Problems or practical difficulties in installing

costing system⮚ Absence of Cost consciousness

⮚ Lack of support from senior executives and Top management

⮚ Suspicion and resistance from workers and emplyees

⮚ Shortage of Trained staff

⮚ Cost of introduction

(d)Steps to be adopted to overcome practical difficulties

⮚ Top Management support

⮚ Employee trust and confidence

⮚ Selection of suitable system and minimising forms

⮚ Training to the staffs

26

July

20

20

Pre

sen

ter N

am

e

13

CLASSIFICATION

OF COST ► Classification is the process of grouping costs according to their common

characteristics. The following are the bases on which costs can be classified;

i. According to elements

ii. According to functions

iii. According to nature or behaviour

iv. According to controllability

v. According to normality

vi. According to relevance to decision making and control

26

July

20

20

Pre

sen

ter N

am

e

14

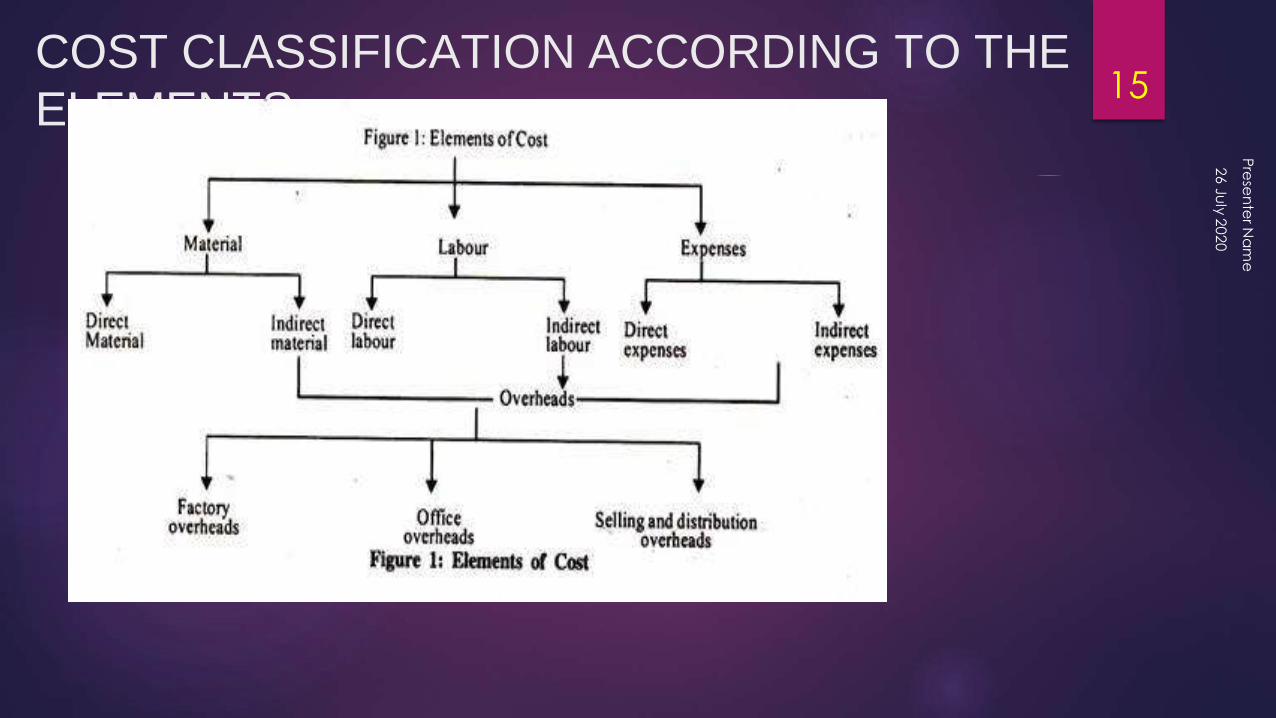

COST CLASSIFICATION ACCORDING TO THE

ELEMENTS

26

July

20

20

Pre

sen

ter N

am

e

15

COST CLASSIFICATION ACCORDING TO THE

functions► The classification is under four major functions of the business:

i. Production cost

ii. Administration cost

iii. Selling cost

iv. Distribution cost

▪ Research Cost

▪ Development Cost

26

July

20

20

Pre

sen

ter N

am

e

16

COST CLASSIFICATION OF ACCORDING NATURE

OF COSTS ► Fixed Cost

► Variable cost

► Semi- fixed or semi – variable cost

COST CLASSIFICATION ACCORDING TO CONTROLABILITY

⮚ Controllable cost

⮚ Uncontrollable cost

COST CLASSIFICATION ACCORDING TO NORMALITYo Normal Cost

o Abnormal Cost

26

July

20

20

Pre

sen

ter N

am

e

17

According to relevance to decision making and

control

► Shut down Cost

► Sunk Cost

► Opportunity cost

► Imputed Cost

► Out-of-pocket Cost

► Replacement Cost

► Conversion cost

► Products cost

▪ Period cost

26

July

20

20

Pre

sen

ter N

am

e

18

SOME OTHER IMPORTANT TERMS► Cost Centre : Cost centre is defined as “a location , person or item

of equipment (group of these) for which costs may be ascertainment

and used for the purpose of cost control” – I.C.M.A.

► Cost Unit : The chartered Institute of Management Accountants

,London, defines a unit of cost as “ a unit of product or service in

relation to which costs are ascertainment.”

❑ Profit Centre : It is a segment of a business responsible for all

activities involved in the production and sales of production and sales

of products . It is created for evaluating performance of a division .

Profit centre has autonomy for decisions concerned with the centre.

26

July

20

20

Pre

sen

ter N

am

e

19

UNIT -2COST SHEET & TENDER

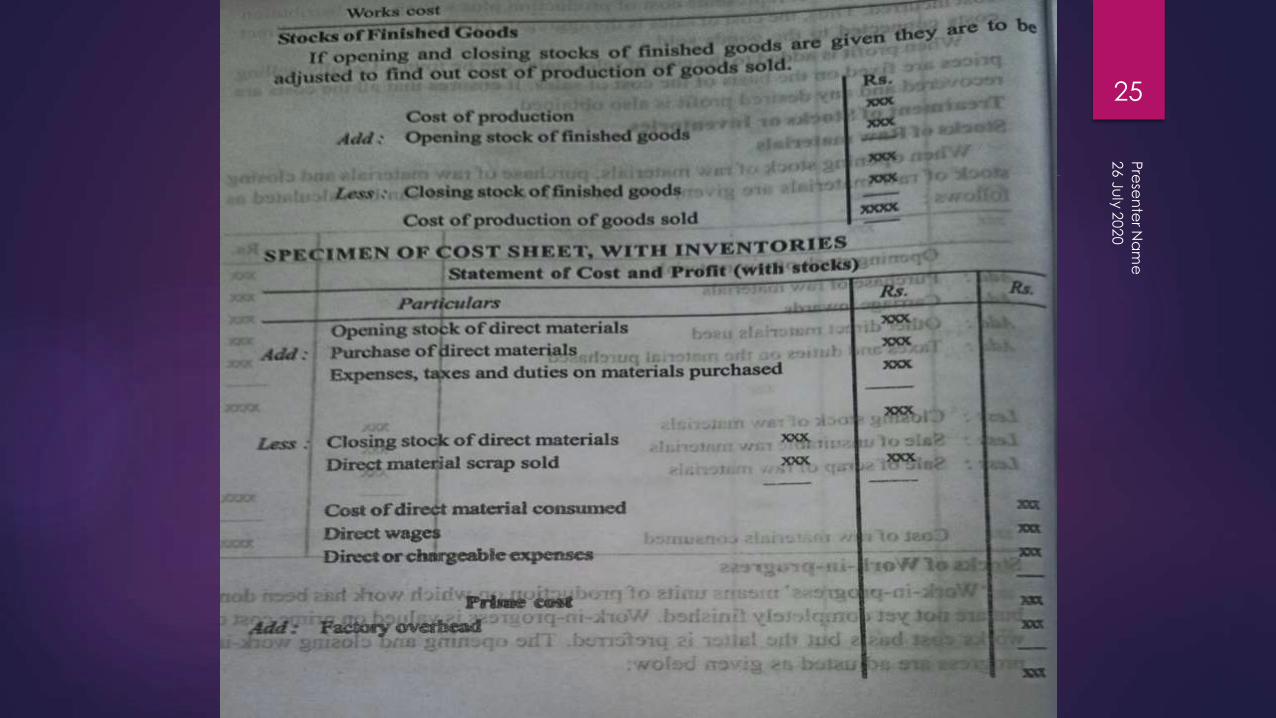

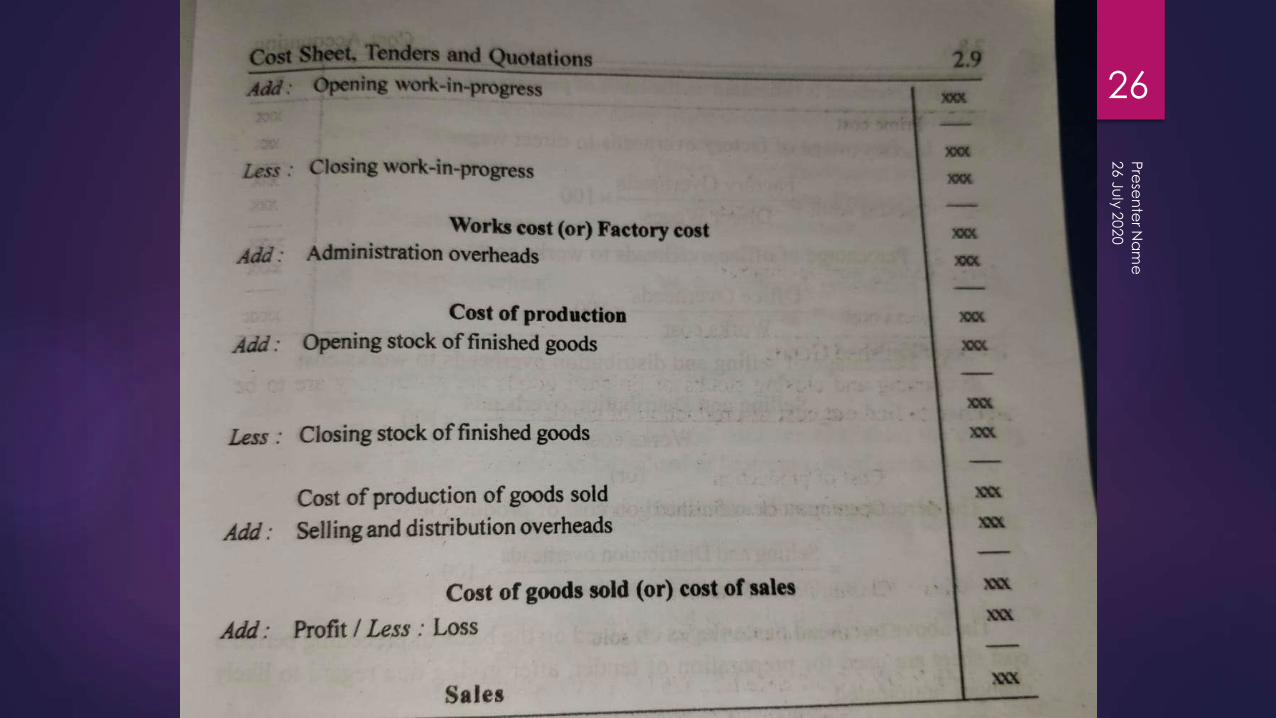

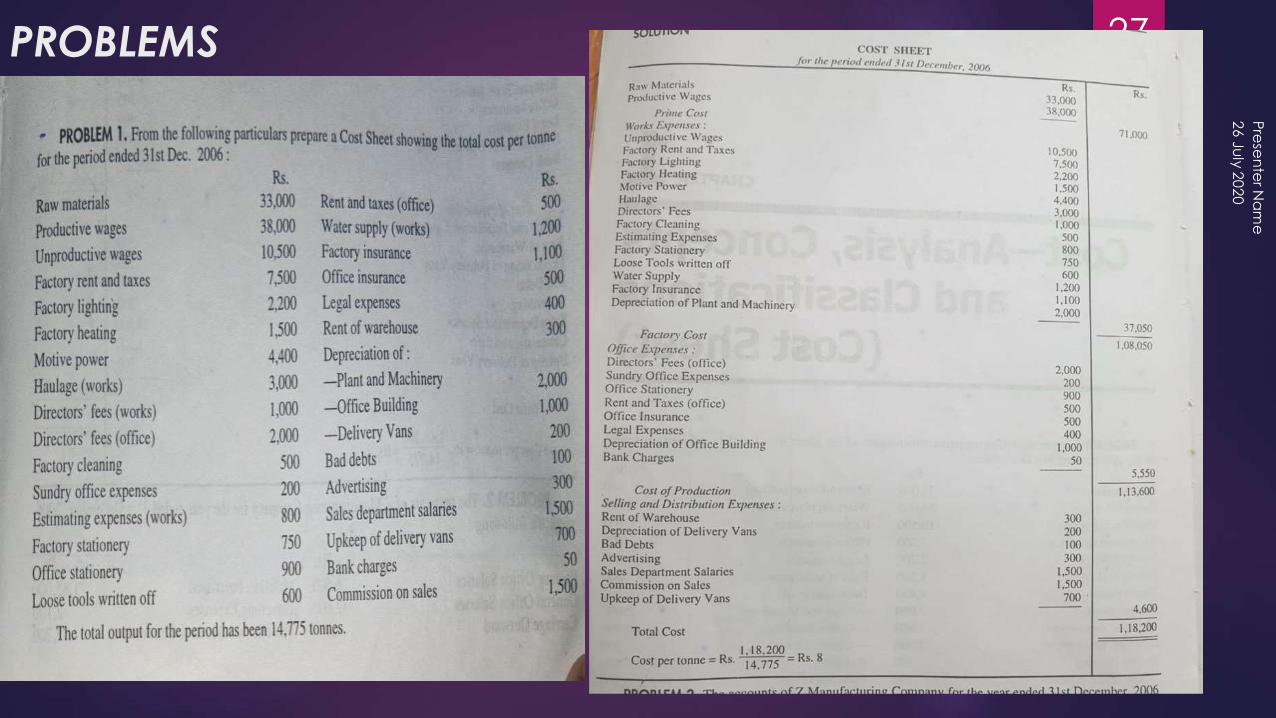

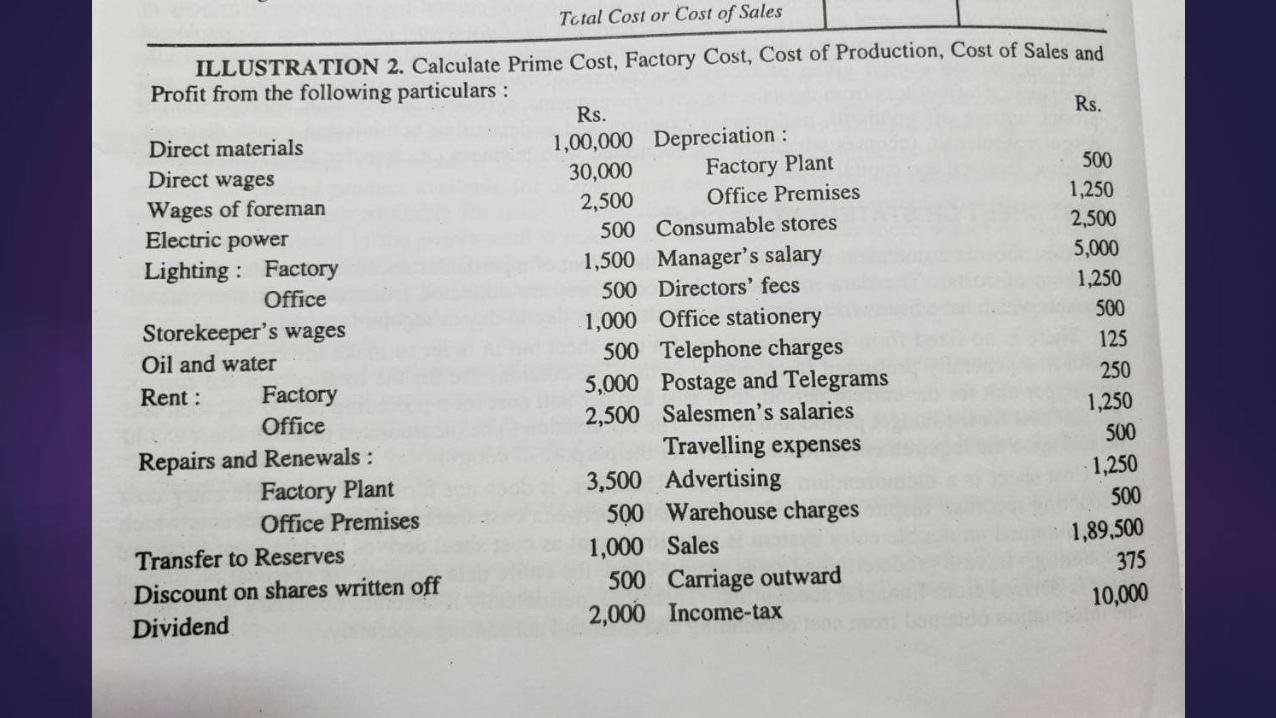

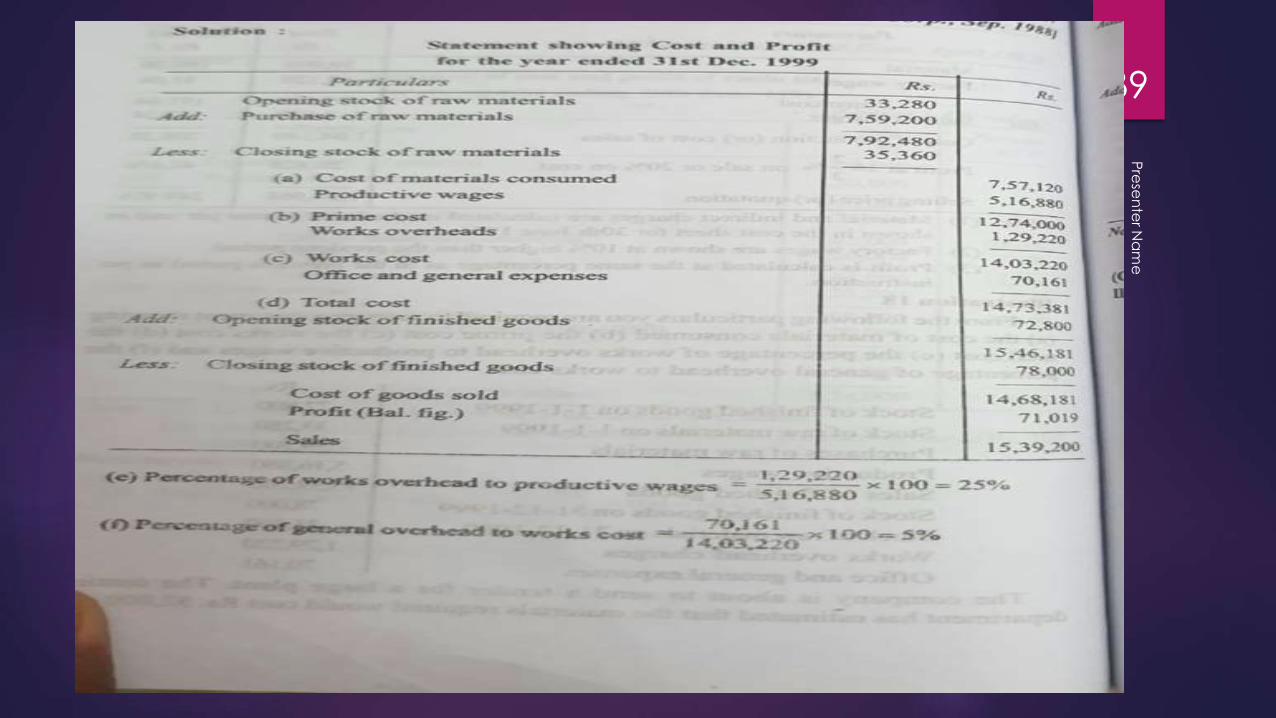

► COST SHEET OR STATEMENT OF COST: The expenses of a product are analysed under different heads in the form of statement . This statement is called cost sheet. Walter & Bigg define, Cost sheet as follows;

“The expenditure which has been incurred upon production for a period is extracted from the financial books and stores records, and set out in a memorandum or a statement . I f this statement confined to the disclosure of the cost units produced during the period , it is termed as a cost sheet”. In other words cost sheet is a statement showing the total cost under proper classifications in a logical order.

⮚ IMPORTANCE,OBJECTIVES,ADVANTAGES OR PURPOSE OF COST SHEET

❑ It provides details to total cost under logical classification.

❑ It provides cost per unit in different stages.

❑ It helps in comparison and cost of control.

❑ Cost sheet is helpful in estimation of cost of preparation of tenders and quotations.

❑ It acts as basics for fixation of selling price.

26

July

20

20

Pre

sen

ter N

am

e

20

26

July

20

20

Pre

sen

ter N

am

e

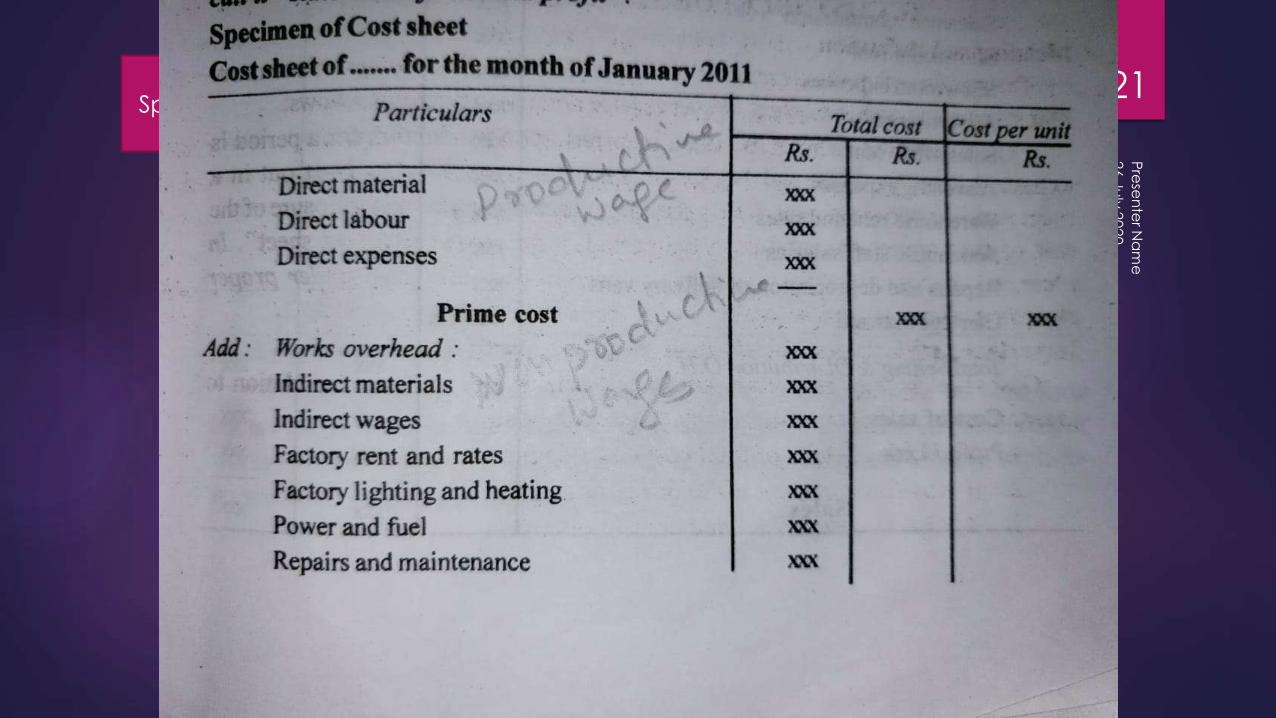

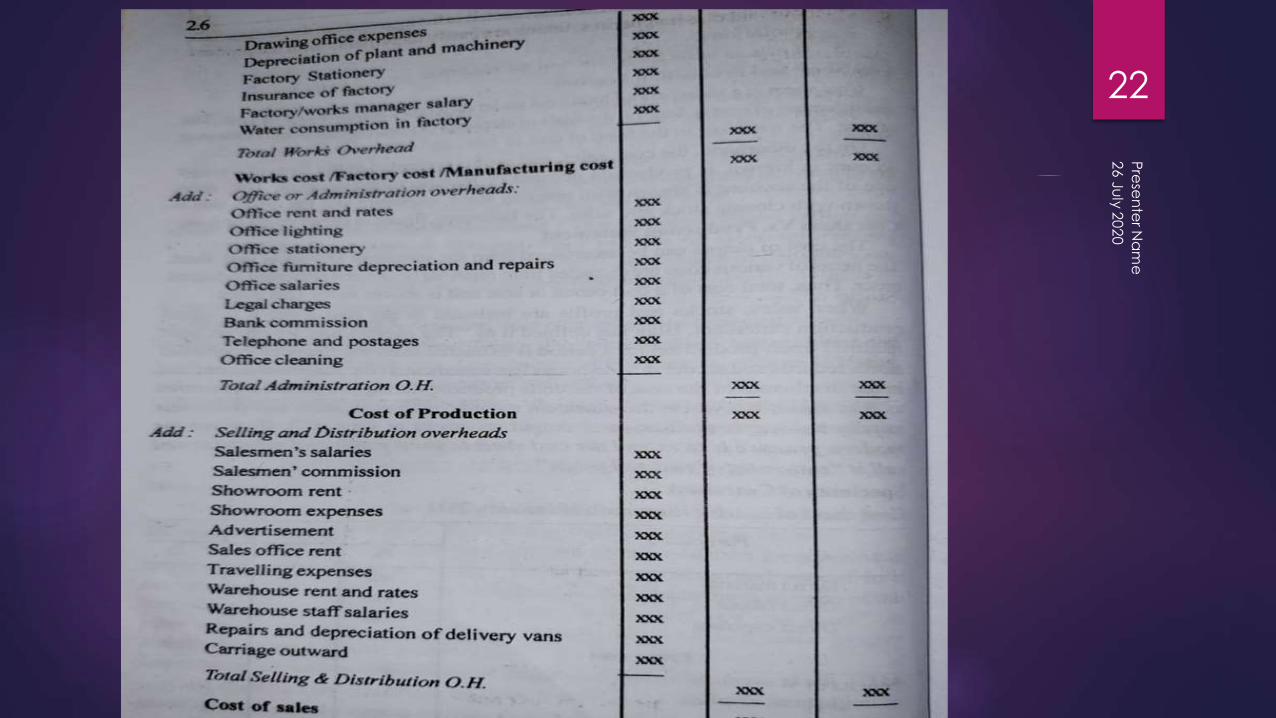

21Specimen Cost Sheet

26

July

20

20

Pre

sen

ter N

am

e

22

26

Ju

ly 2

02

0

Pre

sen

ter N

am

e

23

26

July

20

20

Pre

sen

ter N

am

e

24

26

July

20

20

Pre

sen

ter N

am

e

25

26

July

20

20

Pre

sen

ter N

am

e

26

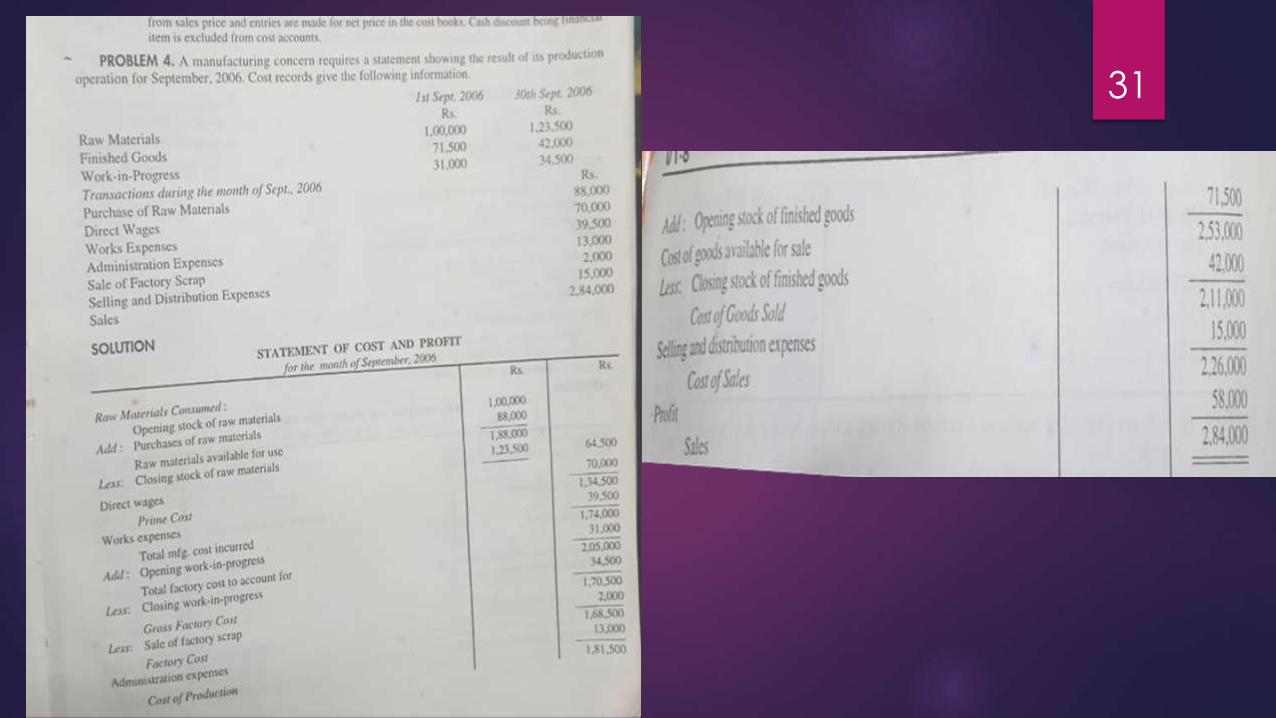

PROBLEMS2

6 Ju

ly 2

02

0

Pre

sen

ter N

am

e

27

26

July

20

20

Pre

sen

ter N

am

e

28

26

July

20

20

Pre

sen

ter N

am

e

29

26

July

20

20

Pre

sen

ter N

am

e

30

26

July

20

20

Pre

sen

ter N

am

e

31

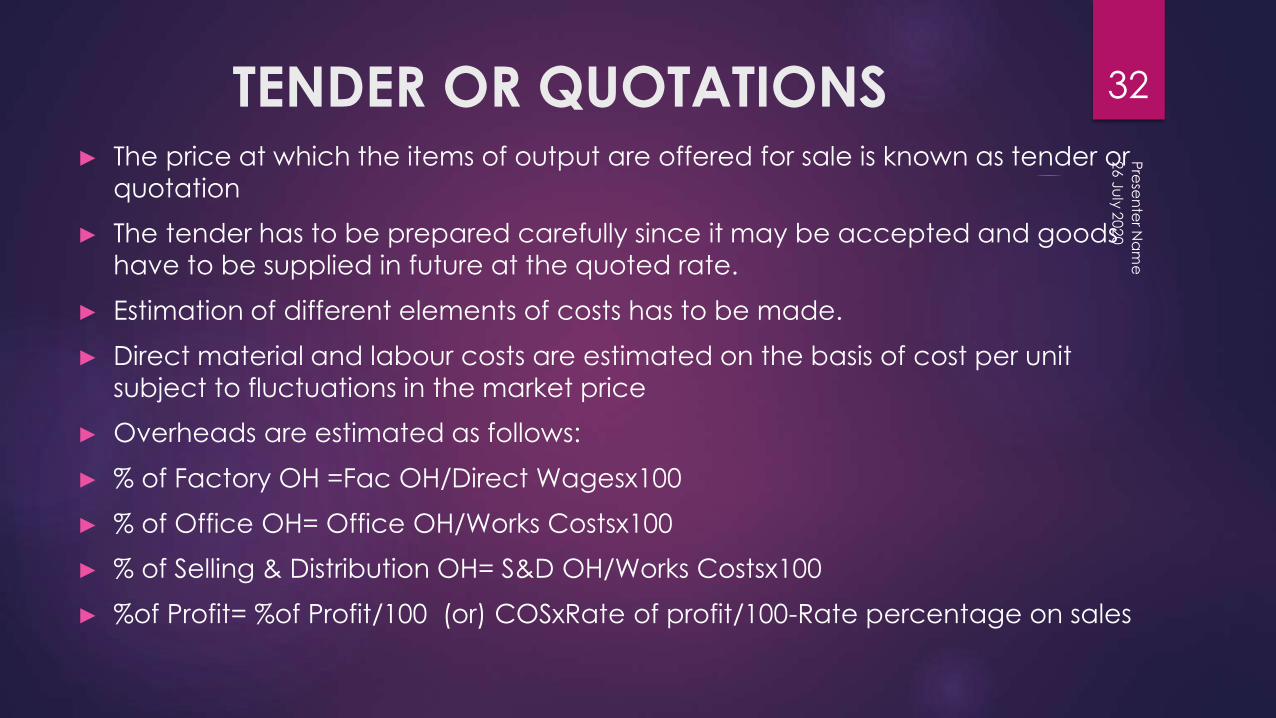

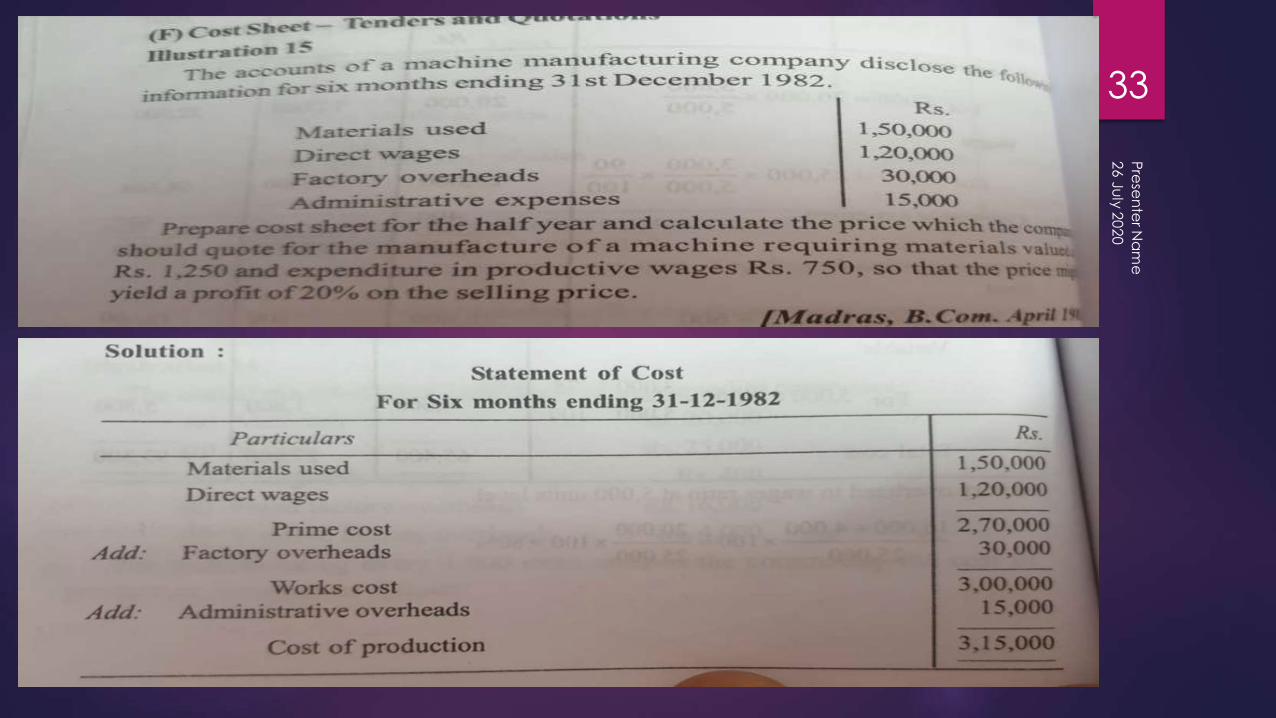

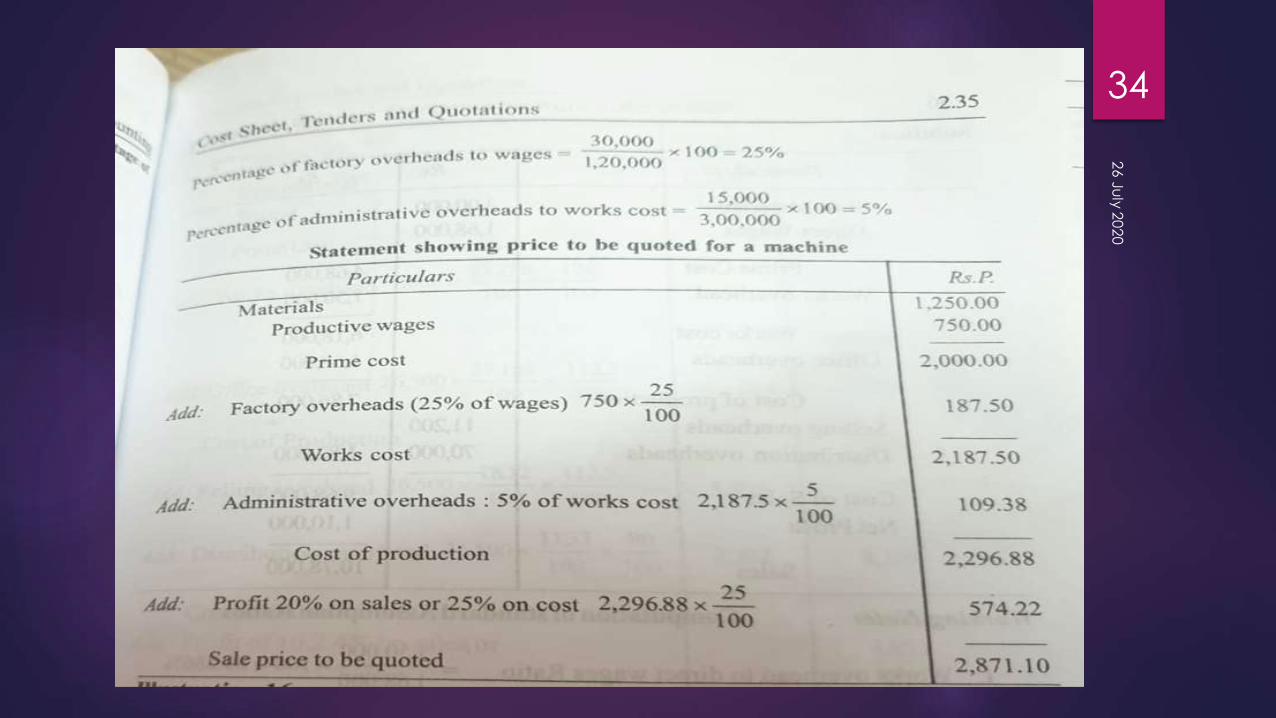

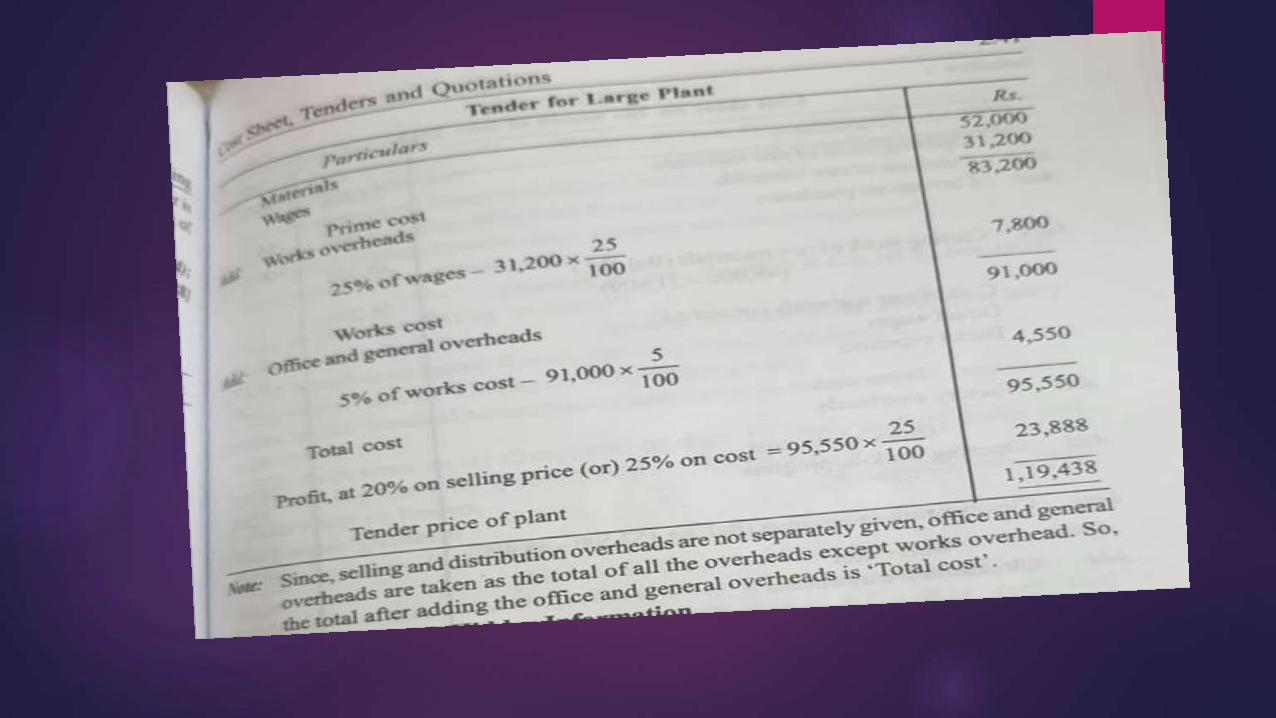

TENDER OR QUOTATIONS► The price at which the items of output are offered for sale is known as tender or

quotation

► The tender has to be prepared carefully since it may be accepted and goods

have to be supplied in future at the quoted rate.

► Estimation of different elements of costs has to be made.

► Direct material and labour costs are estimated on the basis of cost per unit

subject to fluctuations in the market price

► Overheads are estimated as follows:

► % of Factory OH =Fac OH/Direct Wagesx100

► % of Office OH= Office OH/Works Costsx100

► % of Selling & Distribution OH= S&D OH/Works Costsx100

► %of Profit= %of Profit/100 (or) COSxRate of profit/100-Rate percentage on sales

26

July

20

20

Pre

sen

ter N

am

e

32

26

July

20

20

Pre

sen

ter N

am

e

33

26

July

20

20

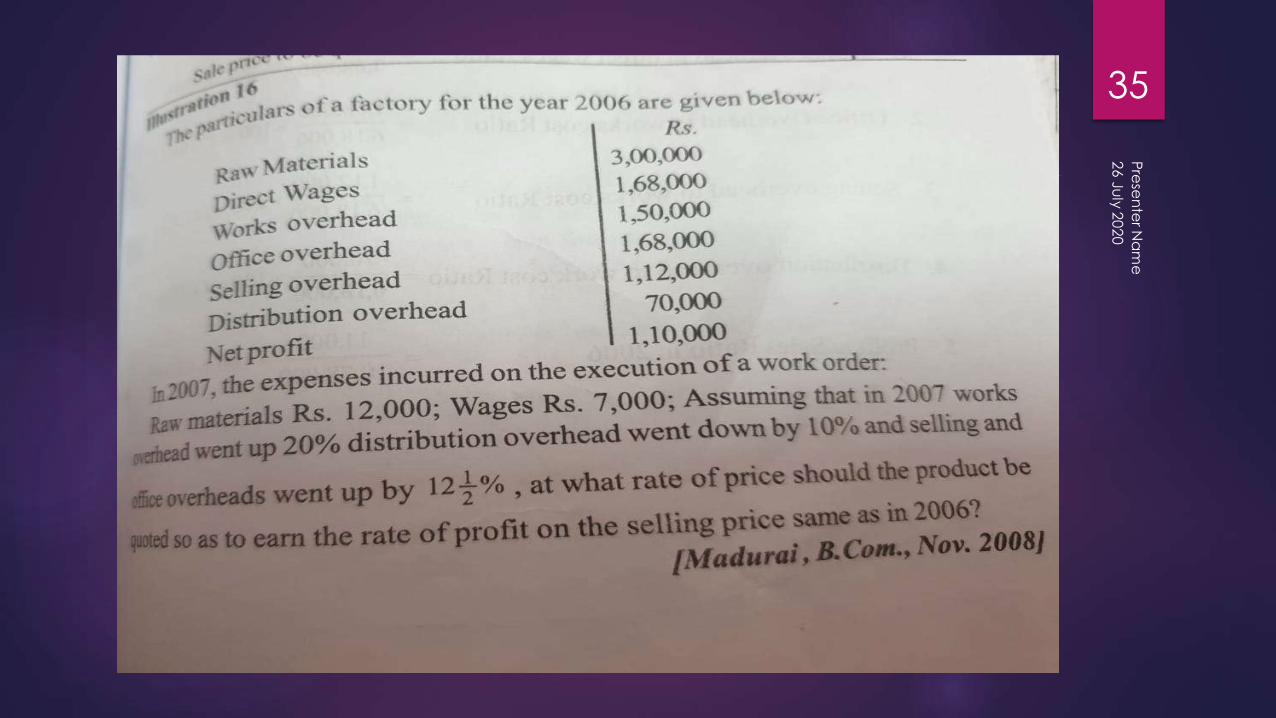

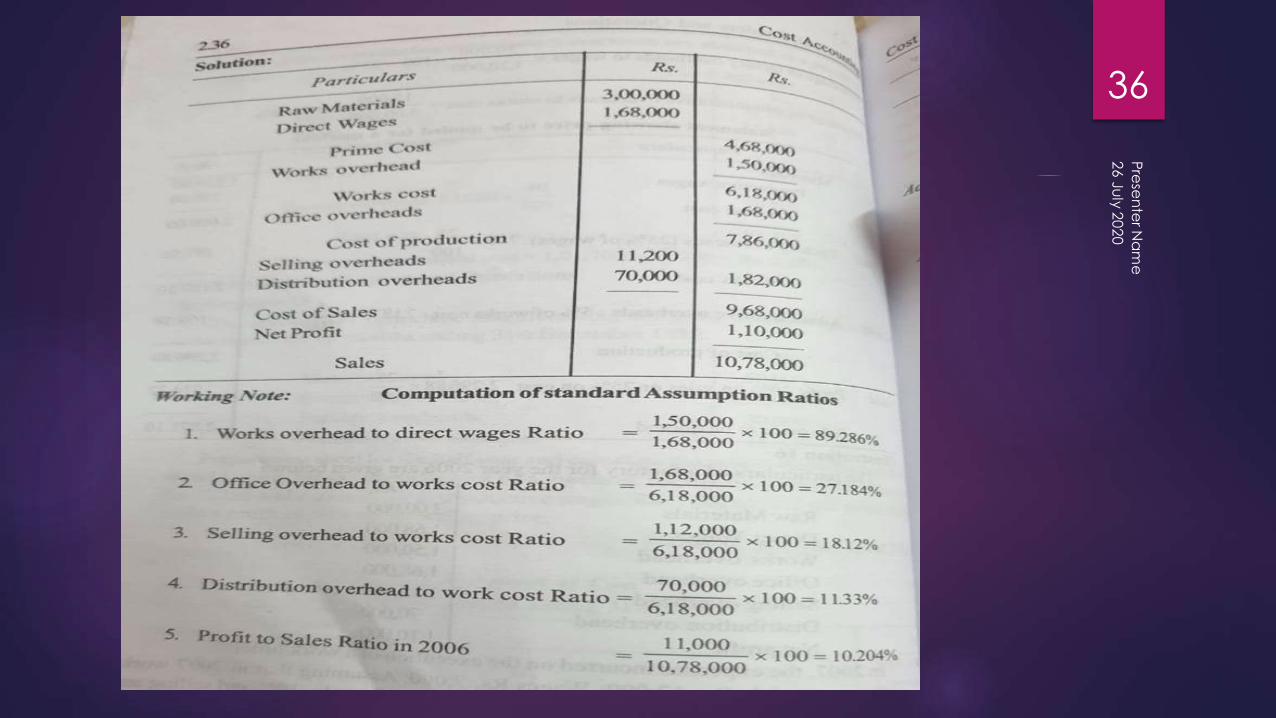

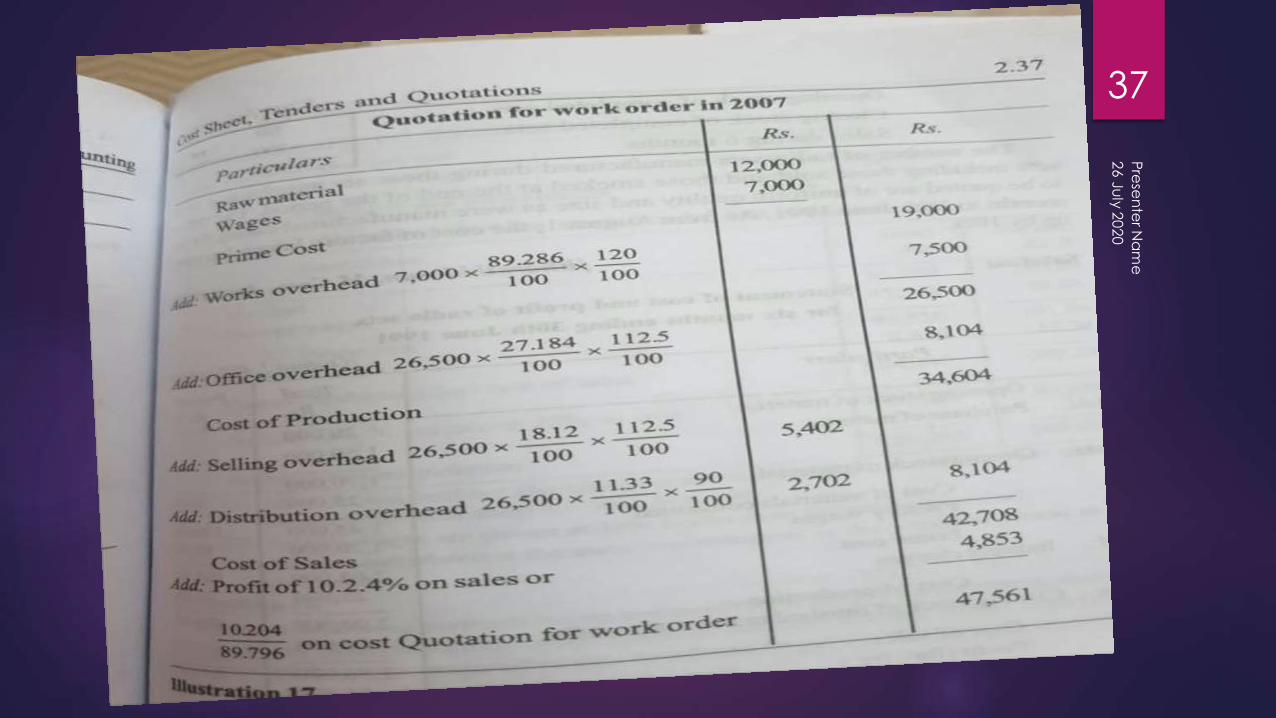

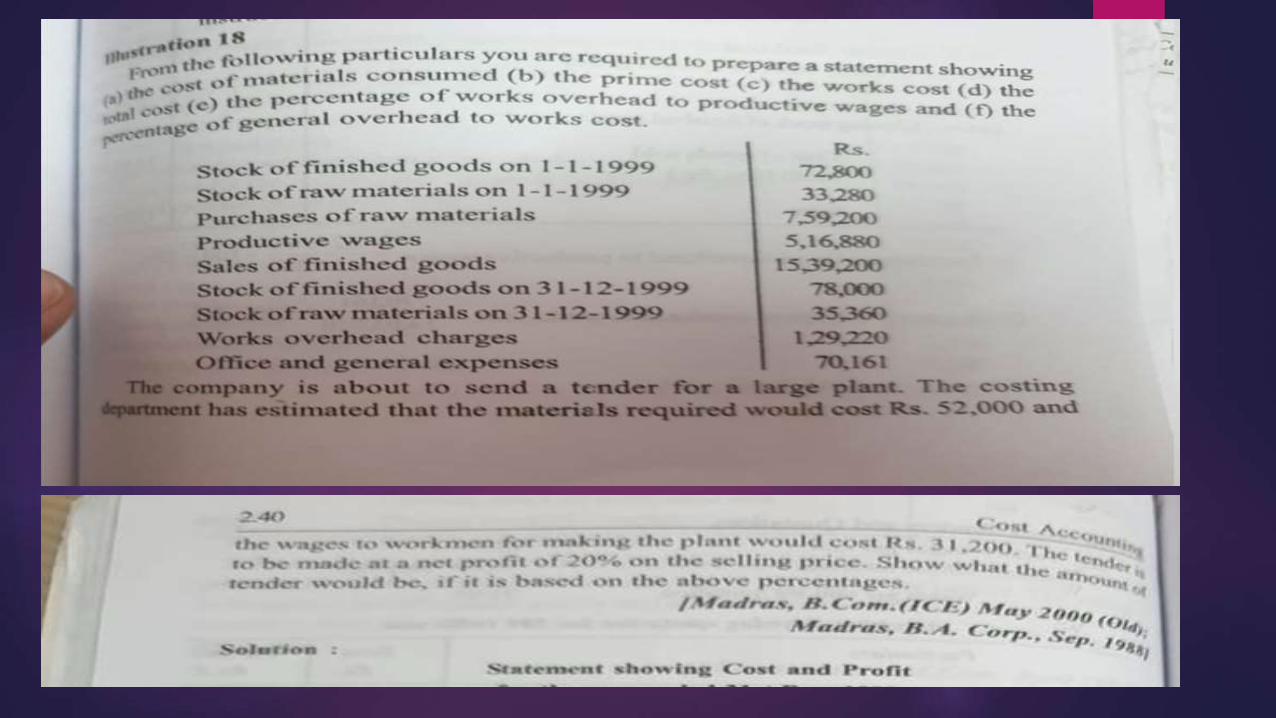

34

26

July

20

20

Pre

sen

ter N

am

e

35

26

July

20

20

Pre

sen

ter N

am

e

36

26

July

20

20

Pre

sen

ter N

am

e

37

26

July

20

20

Pre

sen

ter N

am

e

38

26

July

20

20

Pre

sen

ter N

am

e

39

26

July

20

20

Pre

sen

ter N

am

e

40