collaborative promotion optimization - 401k best...

TRANSCRIPT

Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

TPM-TPO-

Collaborat ive

Market ing

is BIGGER

in Dallas!

Collaborat ive Promot ion Opt imizat ion & Cont inuous Improvement Summit

Latest Break Through in Insight-led

Category Optimization

Online consumer intelligence is changing both brand health monitoring and

innovation. As a result, Microtesting can uncover new mass promotions with 20% to

50% better performance. Learn how Big data and Advanced Analytics can maximize

category performance and assortment optimization in regions/store/cluster.

1 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Brian R. Elliott, Ph.D.

CEO and Founding Board Member of Periscope

▪ 17+ years pricing experience in 35+ industries

and 23+ countries

▪ Previously led McKinsey’s Global Consumer Pricing

and Revenue Management Practice for 8 years

▪ Incubated and helped give birth to Periscope as a

wholly owned subsidiary of McKinsey Solutions serving

Retail, Consumer, Travel, Banking, and B2B industries

▪ Still retained as a Global leader in McKinsey’s

Consumer Marketing and Advanced Analytics Center

▪ Led over 12 transformations end-to-end

“My career has

been all about

bringing more

Science to the Art

of sales and

marketing”

2 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

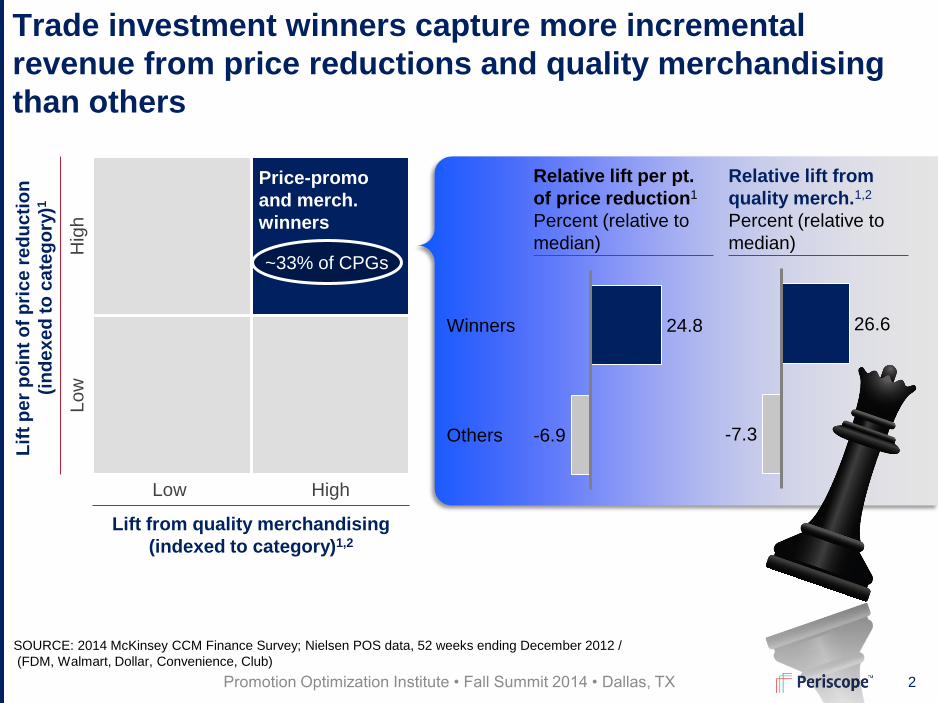

Hig

h

Low High

Low

Lift from quality merchandising

(indexed to category)1,2

Lif

t p

er

po

int

of

pri

ce

re

du

cti

on

(in

de

xe

d t

o c

ate

go

ry)1

Price-promo

and merch.

winners

~33% of CPGs

Trade investment winners capture more incremental

revenue from price reductions and quality merchandising

than others

-6.9 Others

Winners 24.8

-7.3

26.6

Relative lift from

quality merch.1,2

Percent (relative to

median)

Relative lift per pt.

of price reduction1

Percent (relative to

median)

1 Lift from promotion is calculated as difference in sales dollars given the specific promotion compared to baseline sales dollars;

relative lift indexed to category compares company lift by categories against average category lift figures

2 Quality merchandising implies Any Feature or Display on a product

3 Companies cannot exceed category lift by more than 50%

SOURCE: 2014 McKinsey CCM Finance Survey; Nielsen POS data, 52 weeks ending December 2012 /

(FDM, Walmart, Dollar, Convenience, Club)

3 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Investments in big data, broad data and advanced

analytics means winners are pulling farther ahead

SOURCE: 2012 and 2014 McKinsey Customer and Channel Management (CCM) survey

Engaging in next

generation

collaboration

Placing forward-

looking

strategic bets

Leveraging data

and advanced

analytics

Building

industry-shaping

capabilities

Stronger

financial

results

4 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

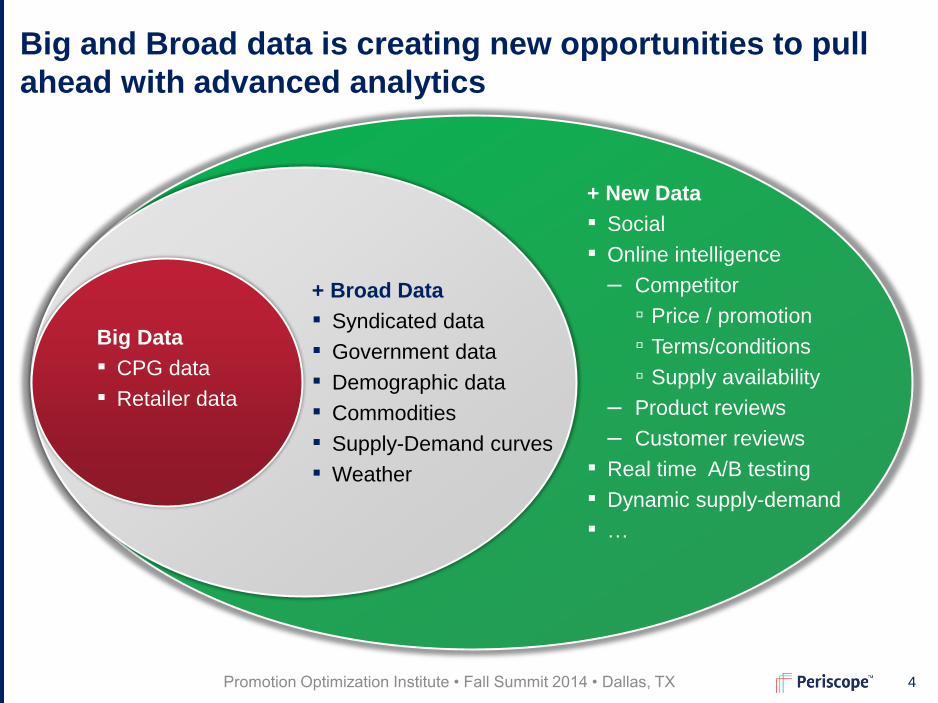

Big and Broad data is creating new opportunities to pull

ahead with advanced analytics

Get the data

warehouse

right

Big Data

▪ CPG data

▪ Retailer data

+ Broad Data

▪ Syndicated data

▪ Government data

▪ Demographic data

▪ Commodities

▪ Supply-Demand curves

▪ Weather

+ New Data

▪ Social

▪ Online intelligence

– Competitor

▫ Price / promotion

▫ Terms/conditions

▫ Supply availability

– Product reviews

– Customer reviews

▪ Real time A/B testing

▪ Dynamic supply-demand

▪ …

5 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

SOURCE: 2014 McKinsey CCM Survey

Data which are table-stakes Percent of respondents

Data winners use Percent of respondents

9

18

18

5

5

5

Conjoint

analysis

Social data

and insights

IT-enabled

Data

collection

from field

Others Winners

36

55

91

90

40

75

Proprietary

Shopper

Research

Data directly

from partner

retailer(s)

Syndicated

scan data Winners

experiment

with new data

sources

Winners are exploring new data sources to support trade

investment decisions

6 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Priorities in assessing trade investment Percent of respondents selecting in Top 3

Looking ahead, winners want a more granular

understanding of what really delivers their strategies

55

64

73

40

35

65

Identifying which

Promotions support

brand strategies

Determining promotions

that win with key

segments

Understanding

incrementality

Others Winners

SOURCE: 2014 McKinsey CCM Survey

7 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Today, let’s highlight how some new sources and

integrative analytics can help you leap ahead

Get the data

warehouse

right

Big Data

+ Broad Data

+ New Data

Online intelligence

▪ Competitor

▪ Consumer

▪ Product

Promotion Innovation

Assortment

Promotions

8 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

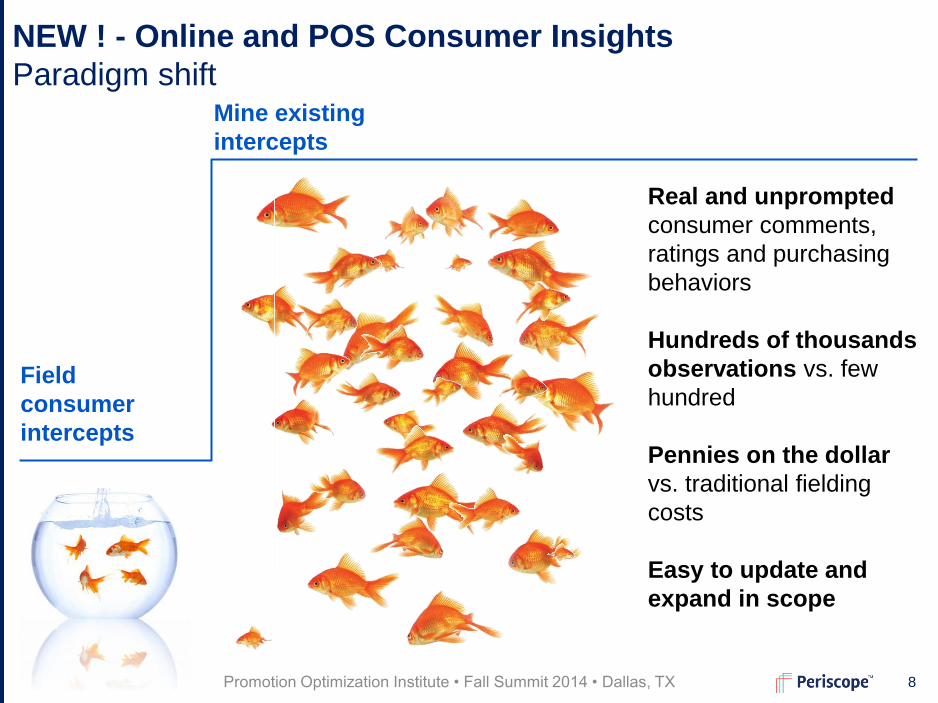

NEW ! - Online and POS Consumer Insights

Paradigm shift

Field

consumer

intercepts

Mine existing

intercepts

Real and unprompted

consumer comments,

ratings and purchasing

behaviors

Hundreds of thousands

observations vs. few

hundred

Pennies on the dollar

vs. traditional fielding

costs

Easy to update and

expand in scope

9 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX 9 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Contents

Active prompting - Promotion Innovation

Passive Listening - Online competitor,

consumer and product intelligence

Integrative use of many sources – Assortment

10 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Consumer Goods and Retailers are facing the greatest

challenge to improve trade promotion effectiveness

11 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Sea of Sameness

12 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

What if you knew precisely which

promotions would work

best before running them?

What if you could be right every time?

13 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Introducing Trade Promotion Innovation (TPI)

Introducing

OFFER

INNOVATION

14 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Find the best

promotions Plan with insight Manage execution

Post Event Evaluation

(TPE/TPO)

Determine the best past

promotions after they

are run

Promotion Planning

(TPP)

Build calendars, simplify

planning for account

managers, forecast

impact, compare

scenarios, and manage

workflow approvals

Build the Ad / Flyer

Managing workflow and

updating forecast

performance for final

execution (e.g.

front/middle/back page,

big/small ad)

How does Promotion Offer Innovation fit in the ecosystem?

Direct Marketing

Use loyalty card to

segment and track

shopper purchasing

behavior and build-up

one-to-one promotion

activities

Promotional "Offer

Innovation"

Test new ideas and

identify the ones that will

perform best, allowing

trade dollars to be spent

more efficiently

Trade Promotion

Management (TPM)

Track trade spend and

ensure proper

accounting, accruals,

and invoicing

15 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Identify the best promotions by micro-testing thousands

Promotion

generation

Generate thousands

of promotions to test

Buy 4 get 1 FREE

Cola

Cola 2L bottles

Buy 4 for $5

Cola

Cola 2L bottles

3 for $3

Cola

Cola 2L bottles

Promotion analytics &

rollout

Identify the highest ROI

promotions to roll-out

nationally in brick & mortar

Buy 4 get 1 FREE

Cola

Cola 2L bottles

Adaptive micro-

testing

Micro-test with small groups of

real shoppers via digital

platforms

With Retailers

Across Retailers

16 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Real Example – SKU X, Channel Y (U.S.)

Micro-testing uncovers offers that tap different behavioral

economics and deliver value to consumers in different ways Real Example – SKU X, Channel Y (U.S.)

Net

Co

ns

um

er

Pri

ce

Volume Sold

No

discount

$5 off

(27%)

$1 off

(6%)

$2 off

(11%)

$3 off

(16%)

$4 off

(22%)

20-50% higher event

sales without

increasing discounts

(or 7-10% higher

price levels without

losing volume)

Tested

Promotions

“Off-the-curve” results

17 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

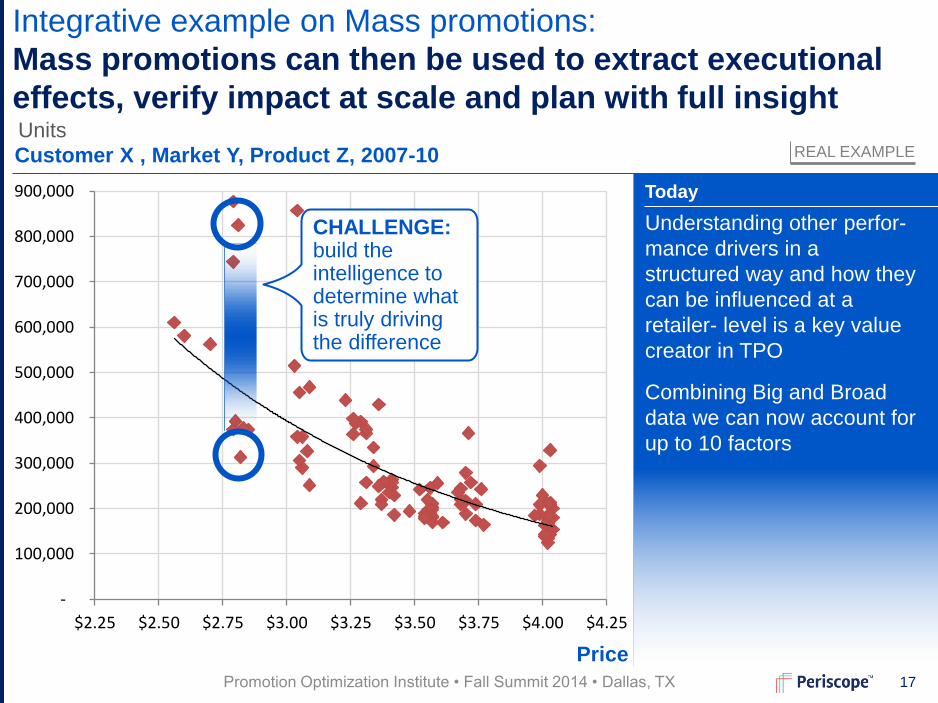

Integrative example on Mass promotions:

Mass promotions can then be used to extract executional

effects, verify impact at scale and plan with full insight Units

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

$2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 $4.00 $4.25

CHALLENGE: build the intelligence to determine what is truly driving the difference

Customer X , Market Y, Product Z, 2007-10

Understanding other perfor-

mance drivers in a

structured way and how they

can be influenced at a

retailer- level is a key value

creator in TPO

Combining Big and Broad

data we can now account for

up to 10 factors

Today

Price

REAL EXAMPLE

18 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

What happened in the over-performing week in the example?

Great week, good package combo, excellent execution Units

Event week

REAL EXAMPLE

Execution

Customer X , Market Y, Product Z, 2007-10

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

$2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 $4.00 $4.25

“DNA of an Event” Over-performance driven by:

Price

Reference price gap

Pantry loading

Cross-Retail

Competition

Weather

+ 50k from execution (50% more cases on display)

Seasonality

impact of the

week

Intra-portfolio

+ 100k from intra-portfolio (very shallow discount on Product Y)

We can do this on purpose with

insight-driven planning

+ 130k from value of the week (July 4)

19 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

What happened in the under-performing week in the example?

Back-to-back deep discounts and bad portfolio interactions

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

$2.25 $2.50 $2.75 $3.00 $3.25 $3.50 $3.75 $4.00 $4.25

-20k from intra-portfolio (very deep Product Y discount)

Customer X , Market Y, Product Z, 2007-10

Execution

“DNA of an Event” Under-performance driven by:

Pantry loading

Intra-portfolio

Reference price gap

Cross-Retail

Competition

Weather

Seasonality

impact of the week

Units

We did this to ourselves without

insight-driven planning

Price

-80k from pantry loading (prior) week deep discount

Event week

REAL EXAMPLE

20 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX 20 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Contents

Active prompting - Promotion Innovation

Passive Listening - Online competitor,

consumer and product intelligence

Integrative use of many sources – Assortment

21 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Online information is exploding, dynamic and can help you

scale and automate your insight generation

Competitor

Intelligence

Consumer

Intelligence

Product

Intelligence

Competitor

Intelligence

Consumer

Intelligence

Product

Intelligence

22 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Advanced competitive intelligence

Best practices

Example: Advanced Automated Product Matching

to adjust complexity and uncover more information

Get ‘Right’ data from

multiple sources

Ability to translate

insights into business

decisions and actions

Real-time, granular

online competitive

pricing, promotion, and

assortment visibility

using artificial intelligence

robots

Mine online consumer

and product ratings,

interactions and

information for consumer

and shopper insights

Exact item match

Slight variations,

to the same offer

Inter-changeable items

across tiers, substitutes

Deg

ree o

f sim

ilari

ty

High

Low

23 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

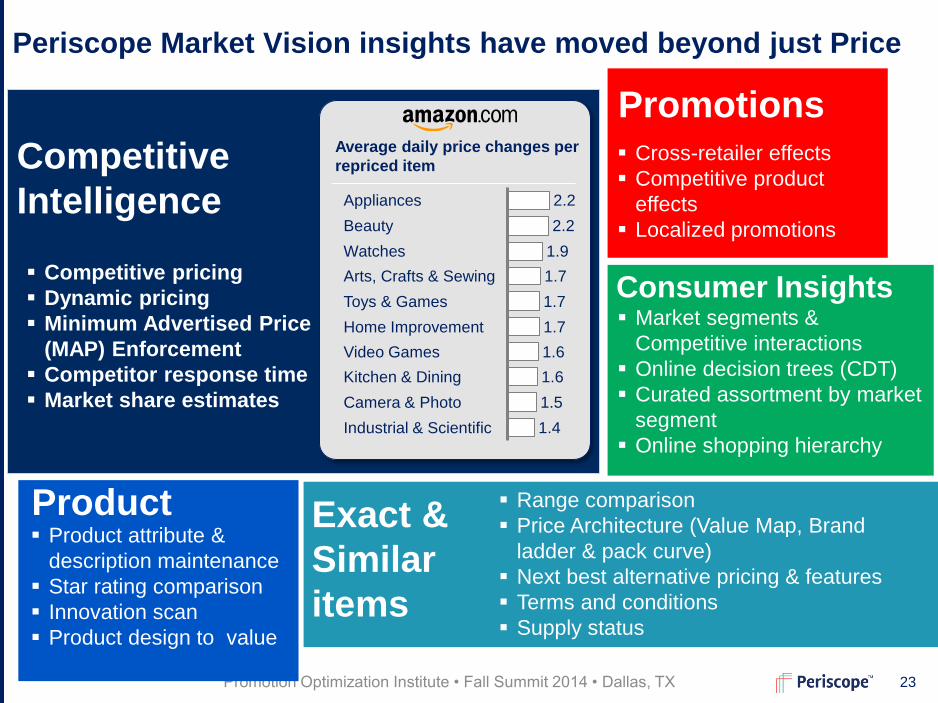

Periscope Market Vision insights have moved beyond just Price

Exact &

Similar

items

Range comparison

Price Architecture (Value Map, Brand

ladder & pack curve)

Next best alternative pricing & features

Terms and conditions

Supply status

Competitive

Intelligence

Competitive pricing

Dynamic pricing

Minimum Advertised Price

(MAP) Enforcement

Competitor response time

Market share estimates

Promotions Cross-retailer effects

Competitive product

effects

Localized promotions

Consumer Insights Market segments &

Competitive interactions

Online decision trees (CDT)

Curated assortment by market

segment

Online shopping hierarchy

Average daily price changes per

repriced item

Camera & Photo 1.5

1.4 Industrial & Scientific

Kitchen & Dining 1.6

Video Games 1.6

Home Improvement 1.7

Toys & Games 1.7

Arts, Crafts & Sewing 1.7

Watches 1.9

Beauty 2.2

Appliances 2.2

Product Product attribute &

description maintenance

Star rating comparison

Innovation scan

Product design to value

24 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

800

600

Jul 2013 May 2013 Mar 2013 Jan 2013 Nov 2012

2,200

2,000

1,600

1,400

1,200

1,000

3,000

2,800

1,800

2,600

2,400

Reference SKU

Lenovo S30(754GE)

Lenovo S30(734GE)

HP Z420(445ET)

HP Z420(434EA)

Lenovo S30(735GE)

HP Z420(448ET)

Lenovo S30(416GE)

HP Z420(454EA)

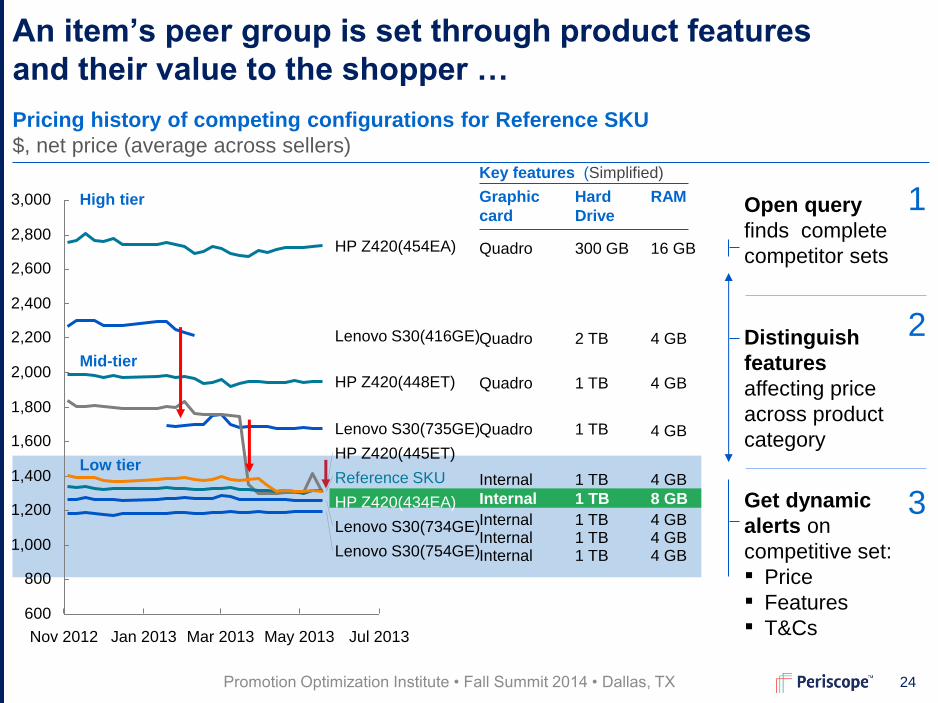

Pricing history of competing configurations for Reference SKU

$, net price (average across sellers)

Quadro

An item’s peer group is set through product features

and their value to the shopper …

Graphic

card

Key features (Simplified)

High tier

Mid-tier

Low tier

Quadro

Quadro

Quadro

Internal

16 GB

4 GB

8 GB

RAM

4 GB

4 GB

4 GB

4 GB 4 GB 4 GB

Open query

finds complete

competitor sets

Distinguish

features

affecting price

across product

category

Get dynamic

alerts on

competitive set:

▪ Price

▪ Features

▪ T&Cs

Internal

Internal Internal Internal

300 GB

2 TB

Hard

Drive

1 TB

1 TB

1 TB

1 TB

1 TB 1 TB 1 TB

1

2

3

25 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Capture longitudinal

data to understand

competitor

behavior:

▪ Frequency/policies

▪ Response time

▪ Follow / lead

1,600

1,500

1,400

1,300

1,200

1,100

1,000

900

May 2013 Apr 2013 Mar 2013 Feb 2013 Jan 2013

... which allows for competitor price monitoring

across identical and similar items over time

0

15

30

Number of competitive offers found

Exact item

Similar

item

Pricing history of competing offers for Reference SKU EUR, Net price, selected peer group SKUs

HP Z420

Reference SKU

Max

Avg.

Min

Range

of offers

“Lazy”

pricers

Or

testing

higher

prices?

Monitor competitive

offerings of exact

match and similar

featured items

▪ Number of offerings

▪ Price ranges

▪ Regional

segmentation

3 weeks lag

to adjust

reference

SKU price

26 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX SOURCE: Periscope Market Vision

At-scale understanding of competitive dynamics

Coffee machine online competitive mapping

Size

Strength of

association

27 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX SOURCE: Periscope Market Vision

…and consumer segments

Stove Top

Barista

Capsule

Mass Market

Rocket Ship

Coffee machine online competitive mapping

Expert analysis:

▪ Five distinct market

segments are apparent

– Mass Market

– Capsule

– Barista

– Rocket Ship

– Stove Top

▪ Capsule segment plays a

key role to links Mass

Market with higher-end

espresso makers

▪ Nespresso brand appears

strong: mostly competing

with Delonghi clone

machines

Size

Strength of

association

28 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Working Gloves (206 SKUs / 20 Brands)

Sm.Brands (10%)

Brand die-hards (30% of SKUs)

Mechanix (57%)

Wells

Lamont (43%)

Big Brands (60% of SKUs)

Women

Garden (12%)

Carpenter (13%)

Cold/ Snow (12%)

General use (42%)

Contractor (21%)

Men Hvy -

Duty (44%)

Men Cut/

Abrasion (32%)

Women (24%)

Leather (38%)

Synthetic (62%)

… as well as price ranges per segment

$40-45

$35-40

$30-35

$25-30

$20-25

$15-20

$10-15

$5-10

$0-5

Price

range

% offers

3%

3% 5% 7% 16%

8% 10% 40%

43% 27% 20% 5%

8% 4% 18% 10% 13% 19% 5%

30% 32% 18% 8% 30% 50% 44% 27% 33% 32%

5% 32% 32% 19% 83% 30% 38% 25% 21%

32% 25% 8% 10% 13% 33% 16%

56% 10% 40% 5%

Range

Average

$11-42 $6-24

$25 $13

$11-37

$21

$1-12

$5

$10-15

$13

$3-30

$16

$11-24

$16

$7-23

$16

$2-18

$8

$16-36

$27

$1-38

$18

29 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

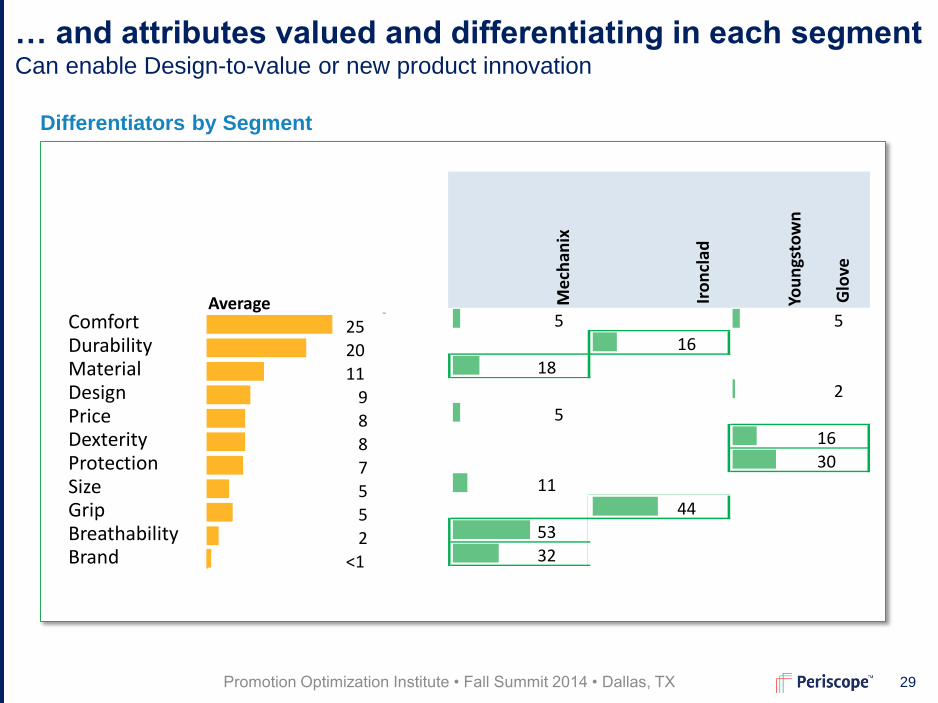

… and attributes valued and differentiating in each segment Can enable Design-to-value or new product innovation

Comfort Durability Material Design Price Dexterity Protection Size Grip Breathability Brand

Differentiators by Segment

Me

chan

ix

Iro

ncl

ad

You

ngs

tow

n

Glo

ve

5 5

16

18

2

5

16

30

11

44

53

32

Average

25

20

11

9

8

8

7

5

5

2

<1

30 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

At-Scale insight requires automation

Online Market

Canvasing and

Monitoring

Advanced Data

Cleaning & Matching

Insight extraction

Source: Periscope Market Vision

– but also enables insight-

driven retailing at scale

across categories

Complements existing

research for CPG and

scales across markets…

31 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX 31 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Contents

Active prompting - Promotion Innovation

Passive Listening - Online competitor, consumer

and product intelligence

Integrative use of many sources – Assortment

32 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

No substitution

of SKUs considered

Limited granularity

Generic allocation

of limited shelf space

SKUs ranked by sales

The traditional approach

33 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Sometimes they are quite indifferent –

even between two ‘mega skus’

… And sometimes there is just one

SKU that fits there bill – even if it’s a

relatively lower volume one

When shoppers come into a category they have different

degrees of ‘loyalty’ to different SKUs

34 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Traditional optimisation approaches frustrates our “just-

one-SKU” shopper and reducing net category spend

SKU Pareto

Cumulative revenue

95

% o

f R

eve

nu

e –

22

6 ite

ms

# of weighted Items

% cumulative revenue

Optimisation

opportunity

The lower

revenue

ginger

SKU

All the

lemon and

lime SKUs

Unproductive

SKUs

Keep Delete

Walk-rate !

35 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Multi-year transaction data

Loyalty card data

Consumer panel data

Fully granular data

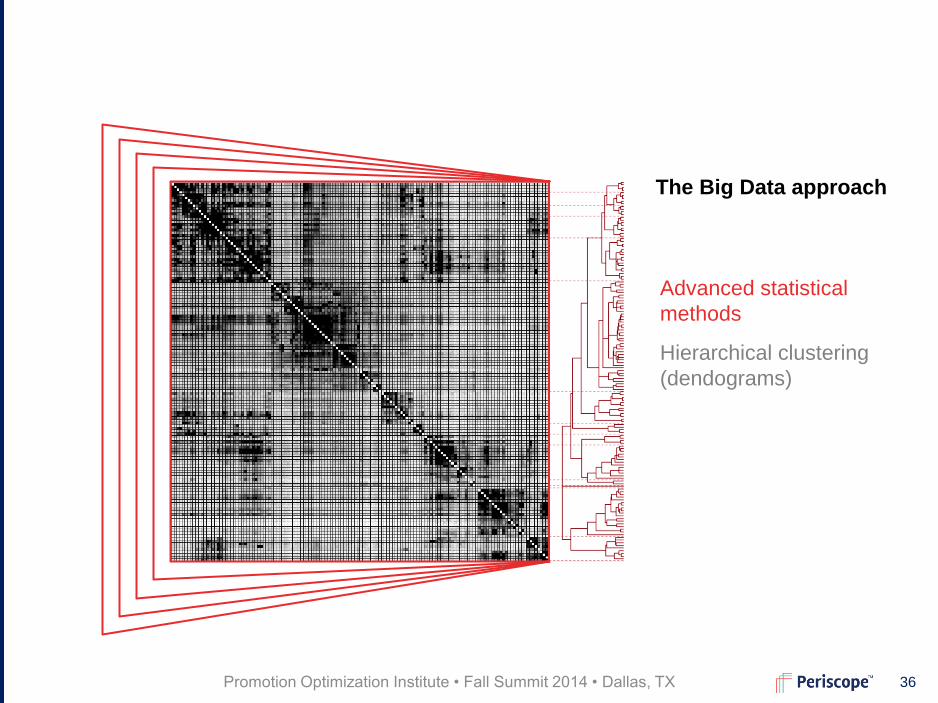

The Big Data approach

36 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Hierarchical clustering

(dendograms)

Advanced statistical

methods

The Big Data approach

37 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Hierarchical clustering

(dendograms)

Multidimensional scaling

(consumer decision tree)

Advanced statistical

methods

Market

Segment 1 Segment 2

Brand A Brand B

Type 1 Type 2 Type 1 Type 2

Flavor 1 Flavor 2

Size 1 Size 2

The Big Data approach

38 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Advanced statistical

methods

Market

Segment 1 Segment 2

Brand A Brand B

Type 1 Type 2 Type 1 Type 2

Flavor 1 Flavor 2

Size 1 Size 2

Entropy based

switching

Brand B Brand A

Consumer Loyalty

Less polarized, Less loyal

Share of Requirements

With multi-dimensional switching barriers

Hierarchical clustering

(dendograms)

Multidimensional scaling

(consumer decision tree)

Stochastic switching model

(entropy calculations)

The Big Data approach

39 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Actual behaviour

(switching, walk rates)

Statistically relevant

Optimal SKU selection

per store

Predictive sales forecast

Advanced statistical

methods

Market

Segment 1 Segment 2

Brand A Brand B

Type 1 Type 2 Type 1 Type 2

Flavor 1 Flavor 2

Size 1 Size 2

Entropy based

switching

Brand B Brand A

Consumer Loyalty

Less polarized, Less loyal

Share of Requirements

With multi-dimensional switching barriers

The Big Data approach

40 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Revenue growth

more than double

the category growth

in the market

AND

Saves 40% of Category

management time

Impact

41 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

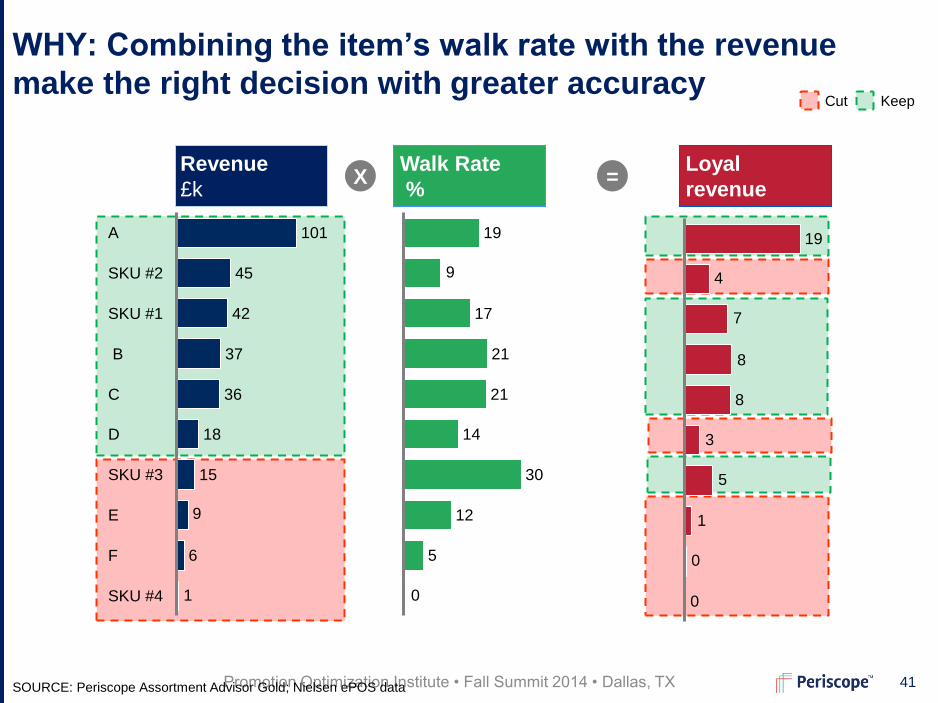

WHY: Combining the item’s walk rate with the revenue

make the right decision with greater accuracy

SOURCE: Periscope Assortment Advisor Gold; Nielsen ePOS data

Cut Keep

X = Loyal

revenue

Walk Rate

%

Revenue

£k

8

0

0

1

5

3

8

7

4

19

0

5

9

12

30

14

21

21

17

19

1

6

9E

SKU #3 15

D

42

SKU #2 45

A 101

SKU #4

F

18

C 36

B 37

SKU #1

42 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

AO results vary with the quality of consumer insights

Simple Pareto

Dendogram

Purchase

structure

Consumer

Decision Tree Level 1

Level 2

Level 4

Level 5

Level 3

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

Cash contribution margin Percent

SKU count Percent

Market map

Spices

Premium Non Premium

Core &

Gourmet

Brand B &

Other CoreMain-

streamValue

Core Gourm.Brand

BOther Prem. MS $ Store Grocery

Pepper A/O A/O BlendSalt Grill A/O

Brand Brand Brand BrandBrand Brand Brand Brand

Size 1

Size 2

Size 1

Size 2

Size 1

Size 2

Size 1

Size 2

Flavor Preference

Salt Preference

Brand Preference

+ Level 6

▪What

drives their

decision?

(reported)

▪How

closely do

current

SKUs

interact?

▪Who is loyal

to what

attributes

and why

with more

precision,

depth, and

non-linear

connections

▪Who is

loyal to

what on

each

occasion

and Why?

Up-converted

Dendogram

▪How loyal

are

shoppers

to different

groups of

SKUs?

Market

Segment 1 Segment 2

Brand A Brand B

Type 1 Type 2 Type 1 Type 2

Flavor 1 Flavor 2

Size 1 Size 2

43 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Simple Pareto

Multiple

Criteria

Flexible sub-

segments

Facings and

Listings

Rigid sub-

segments

Level 1

+ Level 2

+ Level 4

+ Level 5

+ Level 3

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

Cash contribution margin Percent

SKU count Percent

Localized

Shopper mix

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100

Cash contribution margin Percent

SKU count Percent

$Sales

%Margin

+ →

+ Level 6 … And also with the quality of the optimization

▪Analytically

cluster

stores

▪Tailor

assortment

to a

particular

customer

profile,

shopping

mission,

store

catchment

and format

▪Product

dimensions

▪Timing of

replenishment

▪Space elasticity

simultaneously

with

substitutability

▪Simplify

distribution

center (DC) using

Russian doll

▪Attribute

based

substitution

▪Predict “walk

rates”

▪New product

performance

▪Each

“subcategory”

is

individually

optimized

▪More

balanced

view (e.g.

Revenue

velocity, Profit

velocity,

loyalty, etc.).

▪Delist the

weakest

items

44 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Are you ready to take the leap? All sustainable sources of competitive advantage are hard to copy

45 Promotion Optimization Institute • Fall Summit 2014 • Dallas, TX

Any questions or comments?

45