collapse of enron

TRANSCRIPT

Introduction/Background

Products/Services

Governance Structure

Regulatory Oversight

Key players of Enron’s Scandal

System used in Enron

Rise of Enron

Enron during 1993 to 2001

What went wrong?

Secret Revealed

Whistle blower

Fall of Enron

Reasons of ENEON downfall

Enron Bankruptcy

Reasons of Bankruptcy

End of Enron

Sarbanes-Oxley ACT(SOX) of 2002

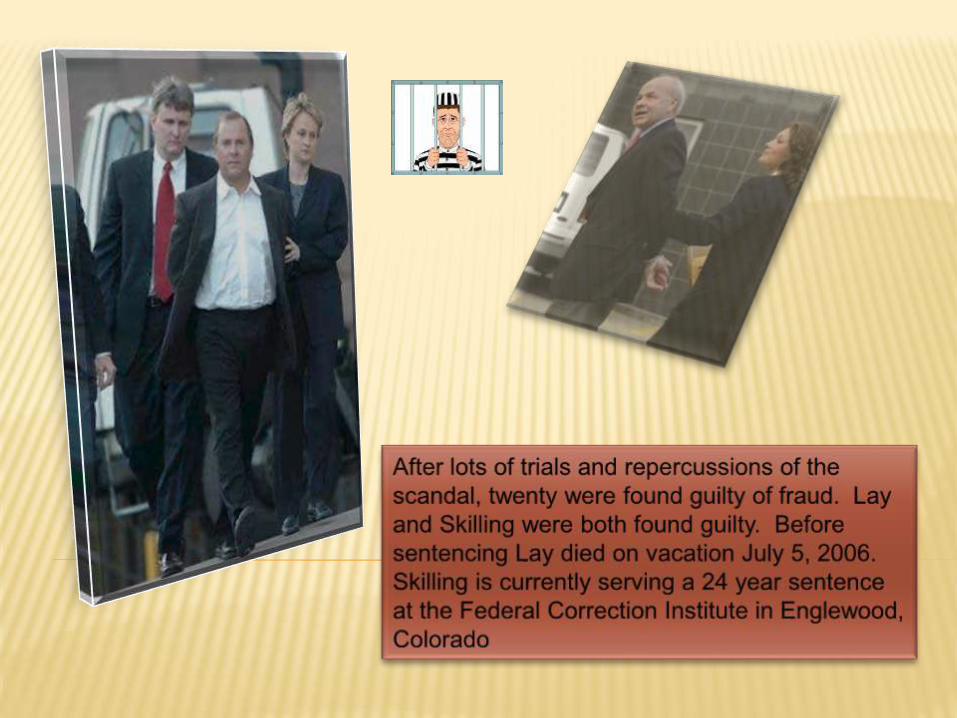

End of Enron looters

Fate of Enron employers and investors

Conclusion

INTRODUCTION/BACKGROUND

OF ENRON

It was formed in 1932, in

Omaha, Nebraska. It was

reorganized in 1979, Inter North.

Houston-based energy and

energy related products trading

and distribution company

Famous for advocacy of energy

deregulation

In just 15 years, climb to be 7th

largest company in US (Fortune

500, 2000), with 21,000 staff

16th largest company in the

worldEnron complex in Downtown

Houston

In 2000, stock has crested at $90 a

share.

Market capitalization: $80 billion

Revenue $139 billion

Arthur Andersen acts as accountant and

consultant

Board of director

14 members, only 2 insiders

Most of the directors owned stock

Employee stock ownership and retirement

planning

Incentive purpose

Enhance company profit

Enron traded in more than 30 different products.

Products traded on EnronOnline include

Petrochemicals

Plastics

Power

Pulp and paper

Steel

Weather Risk Management

Oil and LNG transportation

Broadband

Derivative

Principal investments

Risk management for commodities

Shipping / freight

Streaming media

Water and wastewater

It was also an extensive futures trader including sugar,coffee, grains, hogs, and other meat futures.

It created whole new markets for such oddball"commodities" as broadcast time for advertisers,Internet bandwidth.

Enron Transportation Services:

Oversees Enron's regulated, interstate natural gas pipelines.

Enron had assets spread across :

Central America

Caribbean

South America

Europe

Asia Pacific

ENRON’S GOVERNANCE

STRUCTURE

Management

Lay, Skilling: CEO

Fastow, CFO; Koppers

Causey, CAO; Buy,

CRO

Watkins; Kaminsky;

McMahon

Outside Law Firm

SPEs

Board

Ken Lay: Chair; Co-chair

ZZZ

Audit, Compensation Cees

Company

Policies

Code of Conduct

Internal Audit

ENRON :The regulatory oversight

KEY PLAYERS OF ENRON

SCANDAL1 .Kenneth Lay

Former CEO of Enron, helped

start the company.

Enron extended to him $7.5

million revolving credit line,

which he reportedly used and

repaid with Enron stock 15

times within a period of just

several months

He quit as CEO in February

2001

He returned as CEO in August

2001until he resigned on Jan.

23, 2002

He quit the Enron board

altogether on Feb. 4.

Sherron Watkins said Lay was

"duped" by top executives.

Enron's chief executive in

the first half of 2001

Since joining the

company in 1990, Skilling

helped transform Enron

from a natural-gas pipeline

company into an energy-

trading powerhouse.

Between January and

August 2001 he sold off

about $20 million from

Enron stock

Resigned after the close

of markets on Aug. 14 2001

Charged with conspiracy,

fraud and insider trading.

2. Jeffrey

Skilling

KEY PLAYERS OF ENRON SCANDAL

3. David DuncanEnron's chief auditor

at Anderson

His job was to check

Enron’s accounts.

He is accused of

ordering the shredding

of thousands of Enron-

related documents in

an effort to hide them

from Securities and

Exchange Commission

investigators.

4. Andrew FastowFormer Chief

Financial Officer of

Enron

The mastermind

behind the deceptive

accounting practices

Lea Fastow (his

wife) also plead

guilty to signing and

filing a tax return that

did not include

income the Fastow’s

had received from

Mike Kopper .

3. David DuncanEnron's chief auditor

at Anderson

His job was to check

Enron’s accounts.

He is accused of

ordering the shredding

of thousands of Enron-

related documents in

an effort to hide them

from Securities and

Exchange Commission

investigators.

4. Andrew FastowFormer Chief

Financial Officer of

Enron

The mastermind

behind the deceptive

accounting practices

Lea Fastow (his

wife) also plead

guilty to signing and

filing a tax return that

did not include

income the Fastow’s

had received from

Mike Kopper .

Enron’s Accounting

Firm

The Powers Committee (appointed

by Enron's board to look into the

firm's accounting in October 2001)

came to the following assessment:

"The evidence available to us

suggests that Andersen did not fulfill

its professional responsibilities in

connection with its audits of Enron's

financial statements, or its

obligation to bring to the attention of

Enron's Board (or the Audit and

Compliance Committee) concerns

about Enron's internal contracts

over the related-party transactions”.

- Wikipedia

Key players of ENRON scandal

ENRON’S ACCOUNTING METHOD:

MARKET TO MARKET ACCOUNTING

SYSTEM Mark-to-market accounting requires that once a

long-term contract was signed, income is estimated

as the present value of net future cash flow. Often,

the viability of these contracts and their related costs

were difficult to estimate. Due to the large

discrepancies of attempting to match profits and

cash, investors were typically given false or

misleading reports. While using the method, income

from projects could be recorded, although they

might not have ever received the money, and in turn

increasing financial earnings on the books.

However, in future years, the profits could not be

included, so new and additional income had to be

included from more projects to develop additional

growth to appease investors.

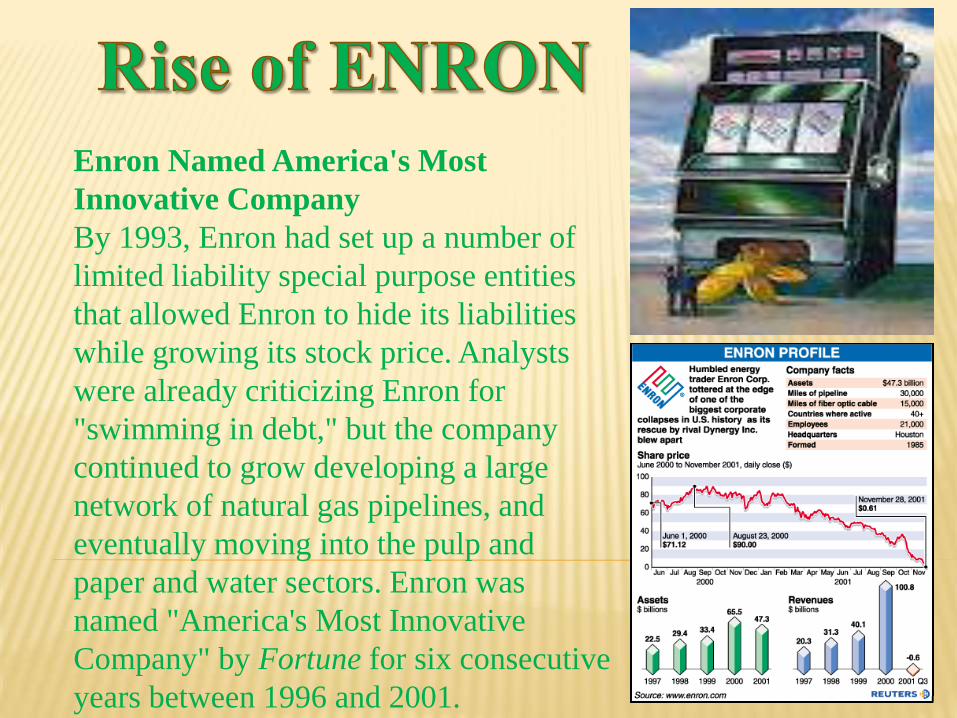

Enron Named America's Most

Innovative Company

By 1993, Enron had set up a number of

limited liability special purpose entities

that allowed Enron to hide its liabilities

while growing its stock price. Analysts

were already criticizing Enron for

"swimming in debt," but the company

continued to grow developing a large

network of natural gas pipelines, and

eventually moving into the pulp and

paper and water sectors. Enron was

named "America's Most Innovative

Company" by Fortune for six consecutive

years between 1996 and 2001.

JEDI & CALPER

In 1993, Enron established a joint venture in

energy investments with CALPERS, the

California state pension fund (organization)

called the Joint Energy Development

Investments (JEDI).

HOW DID THE COLLAPSE

BEGIN?

JEDI

50 %

Interest50 %

Interest

$ 250

Million

in Enron

Stock

High- risk

Asset

ENRON

CALPER1993

CHEWCO

In 1997, Skilling, asked CALPERS to join Enron in a

separate investment. CALPERS was interested in the

idea, but only if it could be terminated as a partner in

JEDI. However, Enron did not want to show any debt

from assuming CalPERS' stake in JEDI on its balance

sheet. Chief Financial Officer (CFO) Fastow

developed the special purpose entity Chewco

Investment Limited Partnership(L.P) which raised

debt guaranteed by Enron and was used to acquire

CALPERS's joint venture stake for $383 million.

Because of Fastow's organization of Chewco, JEDI's

losses were kept off of Enron's balance sheet.

JEDI

$ 383

Million

buyout

$ 383

Million

THIS IS THE PLAN….

ENRON CALPER

CHEWCO

Short term loans

1997

CALPERENRON

Kop

per Chewco: An entity

supposedly independent of

Enron

125

383

JEDIEnron

sole

partner

Big River

Little River

11.4

----

132

Barclay’s Bank--

----

240 Enron

guarantee 6.6

11.4

Enron

aide

2001

PROGRESS OF ENRON

Growth for Enron was rapid in 2000, the company's annual revenue reached$100 billion US. It ranked as the seventh-largest company on the Fortune 500 and the sixth-largest energy company in the world. The company's stock price peaked at $90 US.

Enron build many SPE(Special Purpose Entities) to get the investment for the Enron while showing to the investors that these SPE were independent from Enron but in fact these SPE raised the debt, investment and projects for the Enron. These SPE gave the guaranty for the Enron which increased the trust of the investors.

Enron stock exchange increased to the highest from the companies existed between 1997 -2001.

In just 15 years, climb to be 7th largest company in US(Fortune 500, 2000), with 21,000 staff and 16th largest company in the world.

Market capitalization increased to $80 billion with revenue $139 billion.

MAIN REASON OF ENRON FRAUD

FUZZY NUMBERS

POLITICAL SUPPORT TO

ENRON BY BUSH GOVT.

Skilling and Kenneth contributed in Bush government for the political support from Bush to make money and many unethical laws.

Skilling's boss, the late Kenneth "Kenny Boy" Lay, gave $531,800 to the campaigns of George W. Bush, and Bush appointed two justices to the Supreme Court --John Roberts and Samuel Alito --who may now have the power to return the favor to one of Lay's key lieutenants to help them in fraud.

ENRON

What Went Wrong?

SECRET REVEALED

In autumn 2001, CALPERS and

Enron's arrangement was

discovered, which required the

discontinuation of Enron's prior

accounting method for Chewco and

JEDI. This disqualification

revealed that Enron's reported

earnings from 1997 to mid-2001

would need to be reduced by $405

million and that the company's

indebtedness would increase by

$628 million.

Against Watkins letter Lay, the CEO ,arranged to

have a ENRON’S Law Firm Vinson and Elkins

that looked after all questionable deals.

Watkins continued to do her work and sold stock

of 30000 dollar in August,2001 and some in late

September.

In February 2002,she revealed the various facts

regarding ENRON partnerships and finally

resigned in November. But Watkins Revealed all

the facts only after ENRON filed for bankruptcy.

FALL OF ENRON :1

In 2001 October 2001 : Securities And Exchange Act Launches

A Formal Investigation Into Its “Related Party

Transactions”

November 8,2001 : Enron Restates Its Earning For

First Three Quarters Of 2001

December 2, 2001 : Enron Files For Protection From

Creditors In New York Bankruptcy Court

December 3, 2001 : Lays Off Five Thousand

Employees

FALL OF ENRON:2

In 2002 January 9 : The Justice Department

Announces That It Is Pursuing A

Criminal Investigation Of Enron

January 24 : The Hearings On Enron

Begin

February 4 : Improper Financial

Transactions And Self Dealing

October 31 : The CFO , Fastow Is

Indicted Of Being The Mastermind

Behind The Scandal .

FALL OF ENRON:3

In 2003

February 3: The Creditors Sue Lay And His Wife To Recover $70 Million In Transfers

July 11 : It Settled Its Allegations Of SEC Paying $300 Million .

January 14, 2004 : Fastow Agrees To Serve 10 Years In Prison .

July 8 : Lay Surrenders After Being Indicted .

REASONS OF ENRON DOWNFALL

Bad investments in “new economy” ventures

Off-balance-sheet entities created to eliminate losses from the ventures

Rather than face the write-offs, they tried to hide them with accounting

Many off-balance-sheet loans collateralized by Enron stock

Opaque reporting encouraged short sellers Form over substance in reporting Self –dealing as CFO trading with the

company in troubled assets Corporate ego overwhelmed control

systems Restatements, corrections and new

disclosures Collapse of confidence in reporting and

integrity of management “Run on the bank”

ENRON’S BANKRUPTCY

Major reason of bankruptcy?

A substantial fraction of Enron’s reported profits over a 4

year period (1996-2000) had been the result of

accounting manipulations

--- investigation by special committee of the Enron board

Reported profit Actual profit

Bankruptcy Filing Came After Series Of

Revelations' That Giant Energy Trader Had

Been Using Special Purpose Entities

Company’s CFO In 2001 Stated That

Enron Has Established SPEs To Move Assets

And Debt Off Its Balance Sheet And To

Increase Cash Flow.

According To John, a University Law

Professor ,Once SPE Is Formed By Enron, It

Will Then Borrow Debt From Banks And

Enron Would Guarantee That Debt .

REASON FOR BANKRUPTCY (1)

Accounting gimmickry:Unable to spot bad accounting practices and company’s overstatement of profits

Conflict of auditor:The multiple conflicting roles of auditor

Automatic renewal of auditing contracts

Affecting the independence of auditor

Accounting and staff policy failure:Although a professor of accounting and a dean for monitoring the company, but they all fail in their profession

Disastrous loss in employees’ retirement fund, but the ex-CEO has cashed his own stock much earlier.

Political confusion:

Ironical relationship between governmental

monitoring parties and political parties.

REASON FOR BANKRUPTCY (2)Managerialism

Managers tend to build up their own empires and scarify the profits/benefits of the organization

Conflict of the board

Enron’s board of directors fail to control and oversee the management

The board had been benefited in various relationship with the company

Lack of independence of the board

END OF ENRON

After all the red flags that indicated Enron was up to no good, it was later discovered that Enron recorded assets as profits inflated, or even fraudulent and nonexistent. Offshore accounts were used to cover debts and losses and were excluded from the firm’s financial statements. Enron also hired public accountants to find loopholes. This chart shows the stock price dramatically drop when the corruption was discovered.

SARBANES-OXLEY ACT(SOX) OF

2002

Sarbanes-Oxley ACT(SOX) of 2002 is a United States federal law as a reaction to a number of major corporate and accounting scandals.

The act contains that companies must “enlist and track performance of their material risk and associated control procedures”.

CEOs are require to vouch for the financial of their companies.

Board of Directors must have audit Committees whose members are independent of company senior management.

Companies can no longer make loans to a company director.

In addition, penalties for fraudulent financial activity made much more severe.

END OF LOOTERS OF ENRON

Arthur Anderson: The company

surrendered its CPA license on August 31,

2002, and 85,000 employees lost their jobs.

Jeffrey Skilling: He was sentenced to 24

years and 4 months in prison.

Kenneth Lay: He was sentenced of 10-

years jailed with millions of fine.

Fastow and Lea: Fastow and Lea

both pleaded guilty to two charges of

conspiracy and was sentenced to ten

years.

David Duncan: He pleaded giulty

with the maximum sentence for his

crimes is ten years.

END OF ENRON'S EMPLOYEES

The day after filing for bankruptcy, Enron fired

5,000 workers, one quarter of its 21,000

employees and they have lost their health care

and life savings.

Laid-off workers received a mere $4,500

severance payment.

More than 20,000 of Enron's former employees won a

suit of $85 million for compensation of $2 billion that

was lost from their pensions.

$7.2-billion settlement from a $40-billion lawsuit,

was reached on behalf of the shareholders.

Workers had received one week’s pay for each

year of work and one week’s pay for each $10,000

a year in salary.

Enron paid $55 million in retention bonuses to

about 500 top executives.

ENRON’s employees Retirement System lost $24

million and smaller retirement investment funds

lost another $3.3 million.

CONCLUSION

Enron was a remarkable and innovative company in the world, Its success cannot be neglected.

But there is a interest question for Enron’s bankruptcy: Is there a company can get success without ethics?

To see from the facts, the answer is “no.”

Whether Enron or Anderson, they finally pay for their fault on ethics.

We see ethic problem would bring a fatal strike to a company, no matter how it was successful.

There is something money cannot buy, integrity is one of them.

NO QUESTION, THEN;

Thank You

!