com542a course plan

DESCRIPTION

For BComTRANSCRIPT

CHRISTUNIVERSITY, BENGALURU - 29DEPARTMENT OF COMMERCE

COURSE PLANJUNE 2016 – SEPTEMBER 2016

Programme/Semester

BCom – 5th semester

Subject/Code Advanced financial accounting -COM 542ATotal hours 60 Hours

Planned date

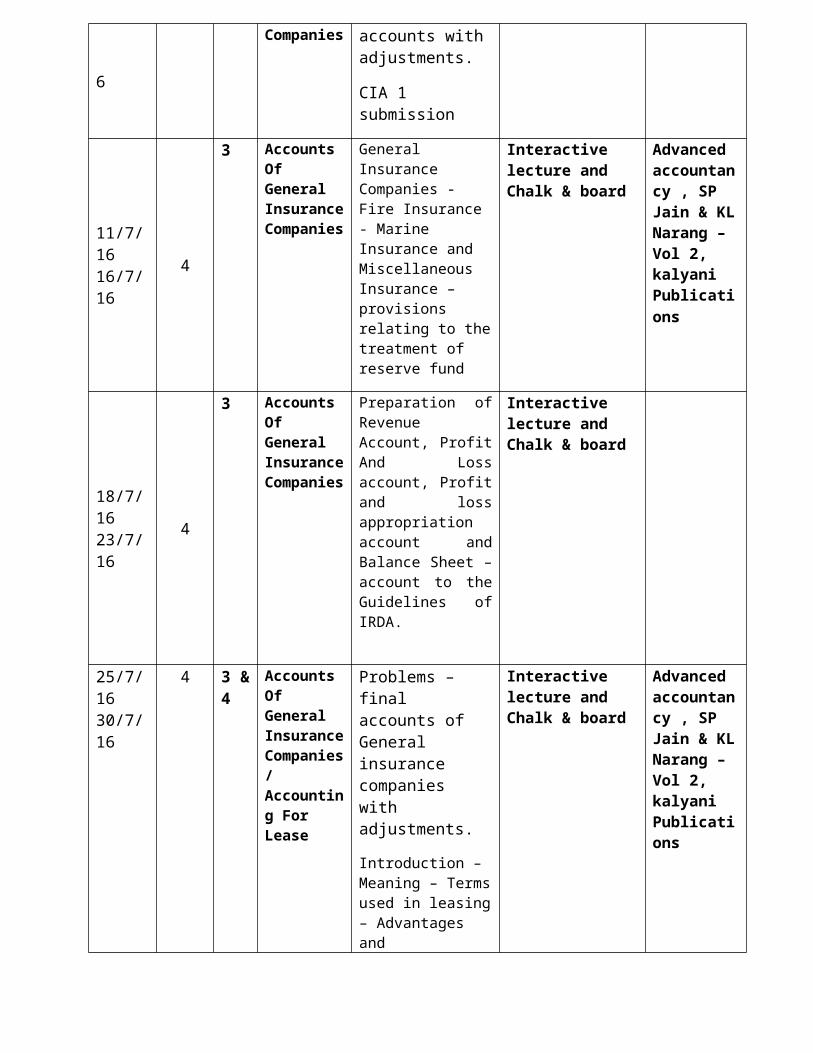

No of hours Unit Heading Details Method Reading/Ref

1/6/164/6/16 2 1

Accounts Of Banking

Companies

Introduction and Meaning - Books of

accounts to be maintained by

Banking Companies - Special features of Bank Accounting -

Items requiring special attention in

Preparing Final Accounts

Interactive lecture and Chalk & board

Advanced accountancy , SP Jain &

KL Narang – Vol 2,

kalyani Publications

6/6/1611/6/16 4 1

Accounts Of Banking

Companies

Rebate on Bills Discounted –

Statutory Reserves – Statutory Liquidity

Ratio – Cash Reserve Ratio – Income from

Non-Performing Assets – Basis of Treating a Credit Facility as NPA

Interactive lecture and Chalk & board

13/6/1618/6/16 4

1 Accounts Of Banking Companies

Assets Classification and Provisions – Preparation of Final Accounts according to the Guidelines of RBI and Banking Regulation Act of 1949

Interactive lecture and Chalk & board

20/6/1625/6/16

4 1&2 Accounts Of Banking Companies/ Accounts Of Life Insurance Companies

Problems – final accounts of banking companies.

Meaning – Type of Insurance – Life Insurance – General Insurance – Accounts of Life Insurance Business – Statutory

Interactive lecture and Chalk & board

Advanced accountancy , SP Jain & KL Narang – Vol 2, kalyani Publications

& Subsidiary Books

27/6/162/7/16 4

2 Accounts Of Life Insurance Companies

Determination of Net Liability and Amount due to policy holders – Preparation of Revenue Accounts and Balance sheet according to IRDA guidelines

Interactive lecture and Chalk & board

4/7/169/7/16 4

2 Accounts Of Life Insurance Companies

Problems – Insurance company final accounts with adjustments.

CIA 1 submission

Interactive lecture and Chalk & board

11/7/1616/7/16 4

3 Accounts Of General Insurance Companies

General Insurance Companies - Fire Insurance - Marine Insurance and Miscellaneous Insurance – provisions relating to the treatment of reserve fund

Interactive lecture and Chalk & board

Advanced accountancy , SP Jain & KL Narang – Vol 2, kalyani Publications

18/7/1623/7/16 4

3 Accounts Of General Insurance Companies

Preparation of Revenue Account, Profit And Loss account, Profit and loss appropriation account and Balance Sheet – account to the Guidelines of IRDA.

Interactive lecture and Chalk & board

25/7/1630/7/16 4

3 & 4

Accounts Of General Insurance Companies/ Accounting For Lease

Problems – final accounts of General insurance companies with adjustments.

Introduction – Meaning – Terms used in leasing – Advantages and disadvantages of leasing – Classification

Interactive lecture and Chalk & board

Advanced accountancy , SP Jain & KL Narang – Vol 2, kalyani Publications

1/8/166/8/16

4 4 Accounting For Lease

Differences between operating and financial lease –

Interactive lecture and Chalk & board

Accounting treatment in the books of lessee and lessor

8/8/1613/8/16 -- - -- CIA 2 MSE

16/8/1620/8/16 4

4 Accounting For Lease

Practical Problems in lease – in the books of lessor and lessee

Interactive lecture and Chalk & board

22/8/1627/8/16 4

5 Recent Trends in Accounting

Human Resource Accounting: Need for HRA – Reasons for HRA – Development of HRA – Meaning (Concept) of HRA – Objectives of HRA – Valuation of Human Resources – Historical Cost Approach – Replacement Cost Approach – Opportunity Cost – Standard Cost approach – Present Value Approach – Recording and Disclosure in Financial Statements – Benefits of HRA – Problems and limitations of HRA – Position of HRA in India

Interactive lecture and Chalk & board

Advanced accountancy , SP Jain & KL Narang – Vol 2, kalyani Publications

29/8/163/9/16

4 5 Recent Trends in Accounting

Social Responsibility Accounting:

Social Responsibility of Business – Meaning of social accounting – Approaches to social accounting – Measurement of Social Cost benefit – ProblemsEnvironmental Accounting: Introduction – Environmental challenges – An

Interactive lecture and Chalk & board.

overview – Business response to environmental issues – International accounting requirements for environmental issues – Legal framework of environmental accounting in India.

6/9/1610/9/16 4

5 Recent Trends in Accounting

CIA 3 submission

Inflation Accounting (Accounting for price level changes)

Introduction to inflation accounting – Introduction- meaning –objective

Interactive lecture and Chalk & board,

13/9/1617/9/16 4

5 Recent Trends in Accounting

Problems in inflation accounting – Current cost accounting method

Interactive lecture and Chalk & board

19/9/1624/9/16 4 Revision Interactive lecture

CIA I Details (Component 1) Theory to application assignments :

The students must write a critical review of the performance of two banking companies comparing their financial statements.

Learning Objective To enhance the ability of the student to critically analyse the financial statements of banking companies

Develop cohesive thinking Enhance writing skills Encourage library usage and referencing Stimulate research culture

Evaluation rubrics:

Criteria

Excellent

4 -3

Yes

Good

3 - 2

Yes, but

Satisfactory

2 -1

No, but

Unsatisfactory

1 - 0

No

Content

Conceptual understanding, Latest developments, relevance, facts, examples,

All the points are covered

Any four points are covered

Any three points are covered

Any two points are covered.

Organization

Introduction

Supporting literature

Inferences

Conclusion

All points are covered.

Any three points are covered.

Any two points are covered.

Any one point is covered.

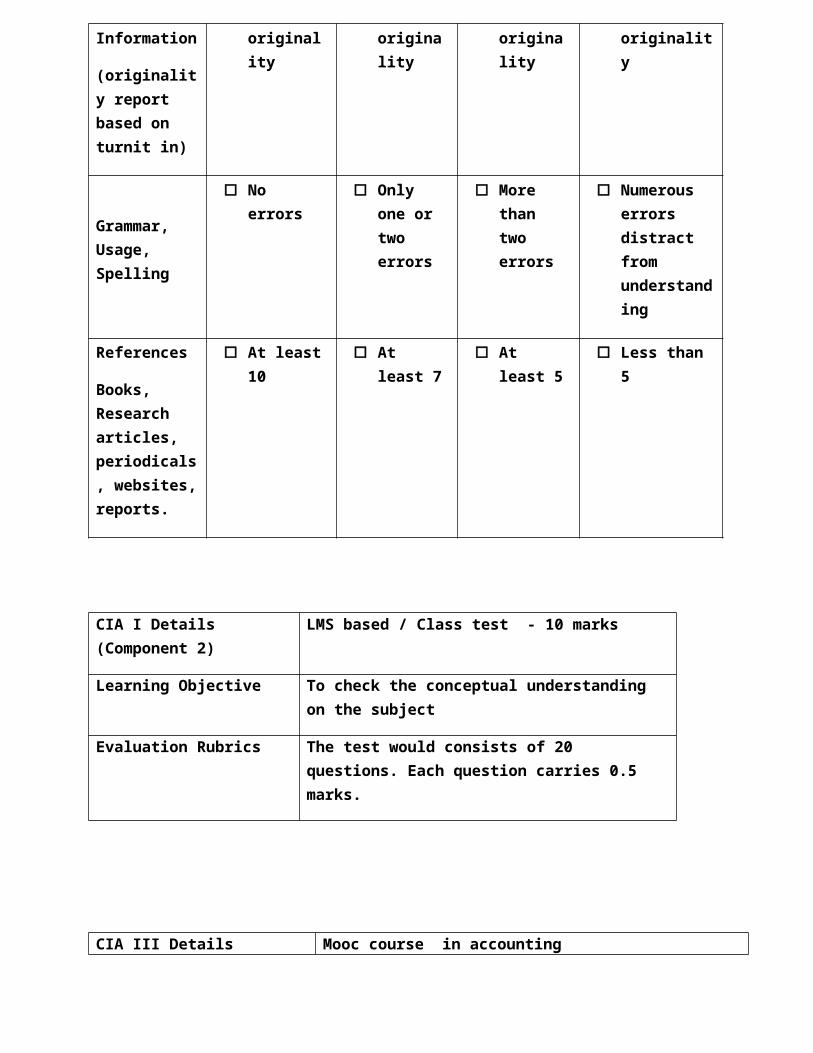

Quality of Information

(originality report based on turnit in)

75-100% originality

50-75% originality

25-50% originality

Below 25% originality

Grammar, Usage, Spelling

No errors Only one or two errors

More than two errors

Numerous errors distract from understanding

References

Books, Research articles,

At least 10 At least 7 At least 5 Less than 5

periodicals, websites, reports.

CIA I Details (Component 2) LMS based / Class test - 10 marks

Learning Objective To check the conceptual understanding on the subject

Evaluation Rubrics The test would consists of 20 questions. Each question carries 0.5 marks.

CIA III Details (Component 1) Mooc course in accounting

Learning Objective To give the students an international exposure in the field of accounting

Evaluation Rubrics The mooc scores (percentages) would be converted to 10 Marks

CIA III Details (Component 2) This is a Group presentation and each group is formed based on the class strength. The students are expected to make a presentation on the assigned/chosen topic. The students shall be evaluated individually based on the following rubric

Learning Objective Ability to work as a team

Develop comprehension ability amongst students

Articulate and present thoughts coherently

Enhance public speaking and presentation skills

Rubrics for Oral Presentation

Criteria Excellent

16-20

Very good

12-15

Satisfactory

8-11

Need to Improve

Below 8

Content The presentation demonstrates clear purpose and subject; cites at least four pertinent examples supported with facts and/or statistics and convincing arguments and concludes with conviction.

The presentation demonstrates clear purpose and subject; cites at least two pertinent examples supported with facts and/or statistics and concludes with conviction.

The presentation demonstrates the purpose and subject; cites at least two pertinent examples but does not support with adequate facts and/or statistics. Conclusion is not convincing.

The presentation demonstrates the purpose and subject; but does not give relevant examples or adequate facts and/or statistics. Conclusion is not convincing.

Delivery Holds attention of entire audience with the use of direct eye contact, seldom looking at notes

Speaks with Modulation in volume and maintains audience interest and emphasize key points

Consistent use of direct eye contact with audience, but still returns to notes

Speaks with satisfactory variation of volume and maintains reasonable interest of the audience.

Displays minimal eye contact with audience, while reading mostly from the notes

Speaks in uneven volume with little or no maintenance of interest by the audience

Holds no eye contact with audience, as entire report is read from notes

Speaks in low volume and/ or monotonous tone, which causes audience to disengage

Organization Able to sequence information accurately

Average accuracy with information sequencing

Displays minimal accuracy of information sequencing

Displays no accuracy in information sequencing

Enthusiasm (Based on evaluator’s

Demonstrates strong

Moderate enthusiastic

Shows little enthusiasm

Shows no interest in topic

Observation) enthusiasm about topic during entire presentation

feelings about topic

about the topic being presented

presented

Q& A session Demonstrates full knowledge by answering all class questions with explanations and elaboration

Is at ease with expected answers to all questions, without elaboration

Is uncomfortable with information and is able to answer only rudimentary questions

Does not have grasp of information and cannot answer questions about subject