combination of metso minerals and outotec · “intends,” “may,” “plans,” “should,”...

TRANSCRIPT

Combination of Metso

Minerals and Outotec

Metso Flow Control to Become a Separately

Listed Company

2

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Joint Disclaimer / Safe Harbour Statement

Important information

This presentation has been prepared by, and the information contained herein (unless otherwise indicated) has been provided by Metso Corporation (“Metso”) and Outotec Oyj (“Outotec”).

This presentation is for information purposes only. This presentation does not constitute a notice to an EGM or a demerger prospectus and as such, does not constitute or form part of and should not be construed as, an offer to sell, or the solicitation or invitation of any offer to buy,

acquire or subscribe for, any securities or an inducement to enter into investment activity. Any decision with respect to the proposed partial demerger of Metso in which all assets and liabilities of Metso that relate to, or primarily serve, Metso Minerals will transfer without liquidation of

Metso to Outotec should be made solely on the basis of information to be contained in the actual notices to the EGM of Metso and Outotec, as applicable, and the demerger prospectus related to the demerger as well as on an independent analysis of the information contained therein.

You should consult the demerger prospectus for more complete information about Metso Minerals, Outotec, Outotec’s securities and the demerger.

The distribution of this presentation may be restricted by law and persons into whose possession any document or other information referred to herein comes should inform themselves about and observe any such restrictions. The information contained herein is not for publication or

distribution, in whole or in part, directly or indirectly, in or into the United States, Australia, Canada, Hong Kong, Japan, South Africa or any other jurisdiction where such publication or distribution would violate applicable laws or rules or would require additional documents to be

completed or registered or require any measure to be undertaken in addition to the requirements under Finnish law. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such jurisdiction. This presentation is not directed to, and is not

intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or

licensing within such jurisdiction.

The shares referred to in this presentation have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or the securities laws of any state of the United States (as such term is defined in Regulation S under the U.S.

Securities Act), and may not be offered, sold or delivered, directly or indirectly, in or into the United States absent registration, except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the U.S. Securities Act and in compliance with any

applicable state and other securities laws of the United States. This presentation does not constitute an offer to sell or solicitation of an offer to buy any of the shares in the United States.

No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. The information contained in this presentation has not been independently verified. No representation,

warranty or undertaking, expressed or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. Neither Metso nor Outotec, nor any of their respective affiliates, advisors or

representatives or any other person, shall have any liability whatsoever (in negligence or otherwise) for any loss however arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. Each person must rely on their own examination

and analysis of Metso, Outotec, their respective securities and the demerger, including the merits and risks involved. The transaction may have tax consequences for Metso shareholders, who should seek their own tax advice.

This presentation includes “forward-looking statements”. These statements may not be based on historical facts, but are statements about future expectations. When used in this presentation, the words “aims,” “anticipates,” “assumes,” “believes,” “could,” “estimates,” “expects,”

“intends,” “may,” “plans,” “should,” “will,” “would” and similar expressions as they relate to Metso Minerals, Outotec, Neles or the demerger identify certain of these forward-looking statements. Other forward-looking statements can be identified in the context in which the statements are

made. Forward-looking statements are set forth in a number of places in this presentation, including wherever this presentation include information on the future results, plans and expectations with regard to the Combined Company’s or Neles’ business, including their strategic plans

and plans on growth and profitability, and the general economic conditions. These forward-looking statements are based on present plans, estimates, projections and expectations and are not guarantees of future performance. They are based on certain expectations, which may turn

out to be incorrect. Such forward-looking statements are based on assumptions and are subject to various risks and uncertainties. Shareholders should not rely on these forward-looking statements. Numerous factors may cause the actual results of operations or financial condition of

the Combined Company or Neles to differ materially from those expressed or implied in the forward-looking statements. Neither Metso nor Outotec, nor any of their respective affiliates, advisors or representatives or any other person undertakes any obligation to review or confirm or to

release publicly any revisions to any forward-looking statements to reflect events that occur or circumstances that arise after the date of this presentation.

This presentation includes combined financial information presented for illustrative purposes only. The illustrative combined financial information of Metso Outotec are presented assuming the activities were included in the same group from the beginning of each period. The illustrative

combined Sales, Operating profit, EBITDA and Adjusted EBITA have been calculated as a sum of Metso’s and Outotec’s financial information for the year ended December 31, 2018 and for the three months ended March 31, 2019 and aligning the EBITDA and Adjusted EBITA

definitions. The illustrative combined statement of financial position information and net debt illustrate the impact of the demerger and the combination as if the transactions had taken place on March 31, 2019. The illustrative combined financial information presented herein is based on a

hypothetical situation and should not be viewed as pro forma financial information as any transactions between Metso Minerals and Outotec have not been eliminated nor have any purchase consideration, purchase price allocation, differences in accounting principles, adjustments

related to transaction costs, tax impacts and impacts of any refinancing transactions by Metso Outotec been taken into account.

This presentation contains financial information regarding the businesses and assets of Metso and Outotec and their consolidated subsidiaries. Such financial information may not have been audited, reviewed or verified by any independent accounting firm. Certain financial data included

in this presentation consists of “alternative performance measures.” These alternative performance measures, as defined by Metso and Outotec, may not be comparable to similarly-titled measures as presented by other companies, nor should they be considered as an alternative to the

historical financial results or other indicators of Metso and Outotec cash flows based on IFRS. Even though the alternative performance measures are used by the management of Metso and Outotec to assess the financial position, financial results and liquidity and these types of

measures are commonly used by investors, they have important limitations as analytical tools and should not be considered in isolation or as substitutes for analysis of Metso’s or Outotec’s financial position or results of operations as reported under IFRS.

This presentation includes estimates relating to the cost and revenue synergy benefits expected to arise from the demerger as well as the related integration costs (which are forward-looking statements), which have been prepared by Metso and Outotec and are based on a number of

assumptions and judgments. Such estimates present the expected future impact of the demerger on the Combined Company’s business, financial condition and results of operations. The assumptions relating to the estimated cost and revenue synergy benefits and related integration

costs are inherently uncertain and are subject to a wide variety of significant business, economic, and competitive risks and uncertainties that could cause the actual cost and revenue synergy benefits from the demerger, if any, and related integration costs to differ materially from the

estimates in this presentation. Further, there can be no certainty that the demerger will be completed in the manner and timeframe described in this presentation, or at all.

Outotec and Metso are Finnish companies. The transaction, including the information distributed in connection with the demerger and the related shareholder votes, is subject to disclosure, timing and procedural requirements applicable in Finland, which are different from those in the

United States. The financial information included in this presentation has been prepared in accordance with accounting standards in Finland, which may not be comparable to the financial statements or financial information applicable in the United States or by U.S. companies.

The new shares in Outotec have not been and will not be listed on a U.S. securities exchange or quoted on any inter‐dealer quotation system in the United States. Neither Outotec nor Metso intends to take any action to facilitate a market in the new shares in Outotec in the United

States.

The new shares in Outotec have not been approved or disapproved by the U.S. Securities and Exchange Commission, any state securities commission in the United States or any other regulatory authority in the United States, nor have any of the foregoing authorities passed comment

upon, or endorsed the merit of, the demerger or the accuracy or the adequacy of this presentation. Any representation to the contrary is a criminal offence in the United States.

It may be difficult for U.S. shareholders of Metso to enforce their rights and any claim they may have arising under U.S. federal or state securities laws, since Outotec and Metso are located in Finland, and all or some of their officers and directors are residents of, non-U.S. jurisdictions.

Judgements of U.S. courts are generally not enforceable in Finland. U.S. shareholders of Metso may not be able to sue Outotec or Metso or their respective officers and directors in a court in Finland for violations of the U.S. laws, including the federal securities laws, or at the least it

may prove to be difficult to evidence such claims. Further, it may be difficult to compel Outotec or Metso and their affiliates to subject themselves to the jurisdiction of a U.S. court. In addition, there is substantial doubt as to the enforceability in Finland in original actions, or in actions for

the enforcement of judgments of U.S. courts, based on the civil liability provisions of the U.S. federal securities laws.

3

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Today’s Presenters

Matti Alahuhta

Chairman

Markku Teräsvasara

President & CEO

Mikael Lilius

Chairman

Pekka Vauramo

President & CEO

4

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Creating Two Leading Companies…

... in Process Technology, Equipment and Services … and in Flow Control

€2.9 billion(1)

2018 Sales

€1.3 billion 2018 Sales

€4.2 billion(1)

2018 Sales

Notes 1. Including €315 million McCloskey estimated calendar year 2018 sales due to September 2018 fiscal year end

Minerals

~€600 million

2018 Sales

Neles

Flow Control

5

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Proposed Metso Outotec Board Composition

Christer

Gardell

Nina

Kopola

Antti

Mäkinen

Kari

Stadigh

Arja

Talma

Mikael Lilius

Chairman

Matti Alahuhta

Vice Chairman

Klaus

Cawén

Hanne

de Mora

Ian W.

Pearce

Current Metso Board

Member

Current Outotec Board

Member

6

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Transaction Summary: All-Share Combination of Metso Minerals and

Outotec, Separate Listing of Metso Flow Control

• Combined Company to be named “Metso Outotec”

• Metso shareholders to receive 4.3 newly issued Outotec shares for 1 Metso share; Metso / Outotec shareholders to own approximately 78.0% / 22.0% of the Combined Company

• Metso to become pure-play flow control business under the name of Neles, separately listed and 100% owned by Metso shareholders

Structure, Exchange

Ratio and Ownership

• Metso Outotec:

− Chairman will be Mikael Lilius and Vice Chairman will be Matti Alahuhta

− Board Composition: 10 directors, with 6 from Metso and 4 from Outotec

− CEO: Pekka Vauramo, Deputy CEO: Markku Teräsvasara, CFO and Deputy CEO: Eeva Sipilä

Governance of Metso

Outotec and Neles

• Metso Outotec(1) combined net debt of €331 million at 31 March 2019

• Neles net cash of €45 million at 31 March 2019

• Dividend policy to be determined by the board of Metso Outotec following completion of the transaction

• Metso Outotec expected to have the capacity for an attractive dividend policy consistent with Metso’s current policy, while maintaining a strong balance sheet and aiming for an investment grade credit rating in line with current Metso rating

Capital Structure and

Dividends

• Unanimously recommended by the boards of both Metso and Outotec

• Irrevocable undertakings from shareholders representing 33.6% of Metso and 24.8% of Outotec shares

Shareholder and

Board Support

• Run-rate annual pre-tax cost synergies of at least €100 million and run-rate annual revenue synergies of at least €150 million

• Run-rate synergies expected to be fully realised by the end of the third year following completion Expected Synergies

• EGMs for Metso and Outotec are expected to be held in October 2019 • Expected closing during Q2 2020, subject to satisfaction of customary closing conditions, including shareholder approval at the EGMs of both Metso and Outotec and regulatory

approvals Timing

Notes 1. Does not include acquisition debt for McCloskey International

• Metso shareholders to receive 2018 dividend of €0.60 per share, payable in November 2019

• Metso board may propose a dividend of up to €221 million in aggregate to be payable in 2020 before closing of the transaction, implying €1.47 dividend per share

• Outotec board may propose a dividend of up to €20 million in aggregate to be payable in 2020 before closing of the transaction, implying €0.11 dividend per share

Pre-Closing

Dividends

• Neles: − CEO: Olli Isotalo

New Combined Company

Metso Outotec

A Leading Company in Process Technology,

Equipment and Services Serving the Minerals,

Metals and Aggregates Industries

8

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Highly Complementary Combination Leveraging the Capabilities of Metso

Minerals and Outotec

Minerals

Creation of a Unique Company in the Industry

Technology

and R&D

Product &

Process

Excellence

Scale

Global

Service

Footprint

9

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Overview of Metso Outotec

Minerals

Process solutions and equipment

for comminution, beneficiation,

pyroprocessing and material

handling

Equipment, spare and wear parts

and services for aggregates

production

Leading manufacturer of recycling

machinery for processing metal

scrap and shredding of waste

Complete portfolio of leading process

solutions and services, as well as full

plant delivery capability

Sustainable solutions for metals

processing, renewable energy

production and industrial water

treatment

Minerals

services

Metals, Energy & Water

Sales: ~€520 million

Recycling

Sales: ~€140 million

Minerals Processing

Sales: ~€1,550 million

Minerals Processing

Sales: ~€760 million

Services Minerals

Equipment

Recycling

Aggregates

Equipment

Metals, Energy &

Water Equipment

2018

Sales

Notes 1. Including €315 million McCloskey estimated calendar year 2018 sales due to September 2018 fiscal year end

52%

19%

19%

9%

1%

Aggregates(1)

Sales: ~€1,200 million(1)

Supported by ~15,600 employees

10

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

4.2 4.2

3.7

2.8

2.6

1.4 1.3

Sandvik (Mining and RockTechnology)

Metso Outotec Epiroc Weir Metso Min. FLSmidth (Minerals) Outotec

Creation of a Leading Company in Process Technology, Equipment and

Services Serving the Minerals, Metals and Aggregates Industries

Key Industry Participants by 2018A Sales (€ billion)(1)

Source: Company filings Notes 1. Financials converted to EUR using 2018 calendar year average FX rates: EUR/DKK 7.4533; EUR/SEK 10.2596; EUR/GBP 0.8847; EUR/CAD 1.5297 2. Represents Sandvik’s Mining and Rock Technology segment sales. Corresponds to 43% of 2018 group sales, as per 2018 Annual Report 3. Including €315 million McCloskey estimated calendar year 2018 sales due to September 2018 fiscal year end 4. Represents 56% of 2018 group sales, as per split between Minerals (56%) and Cement (44%) in the 2018 Annual Report

(2)

(4)

Minerals

(3)

McCloskey Sales( 3)

2.9

GS to align footnotes

format, should be in ( )

See McCloskey

example

11

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Enlarged Installed Base Coupled with Advanced Service Offering to Drive

Significant Benefits

Minerals

Sales Contribution from Services

2018A

• Complementary footprint of service centres enabling closer proximity to customers

• Significant service sales upside

• Potential for cross-selling through combined installed base

Key Combination Benefits

Services 58%

Services 39% Services

52%

(1)

Notes 1. Adjusted for McCloskey services revenue estimate

(1)

12

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Wide Presence Across the Minerals Processing Value Chain

End-to-End Offering in Minerals Processing

Crushing Grinding Tailings

Handling

Dewatering Beneficiation Screening Classification

13

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Leadership in Technology and R&D

Yield maximisation and plant performance optimisation

Metals production from secondary raw materials and tailings

Resource

Efficiency

Energy-efficient process technologies, gas handling and heat

recovery

Solutions for significant reduction in freshwater consumption

Energy and Water

Efficiency

Remote monitoring

Process optimisation

“Digital twin”

Digital to Drive

Productivity

CO2 reduction

Emissions elimination through clean technologies Climate Change

Processes for producing lithium hydroxide for battery industry Battery Raw

Materials

Total R&D expenditure of

~€100 million across Metso

Minerals and Outotec in

2018

Decades of process and

minerals know-how

Unique R&D centres

Pilot plant capabilities

Metso Outotec Capabilities

14

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Sustainability at the Core of Operations

Customer Focus Points

Strong Focus on Sustainability

at Both Companies

Included in the Global

100 Index of most

sustainable companies

in the world seven

consecutive years

(2013-2019)

Minimise

environmental risks

Responsible

procurement and

productivity

Lower water

consumption

Better

environmental

efficiency

R&D projects with

sustainability

targets

Individual HSE

targets

Employee

engagement, culture

and processes

Lost time incidents

In 2018, customers

generated six million

tonnes less of CO2-e

using Outotec’s

technologies

compared to annual

baselines

86% of R&D projects

had sustainability targets

CO2 emissions

reduction in 2018

through

the use of Metso

VertimillTM

technologies

652,000 tCO2

Minerals

Mention Culture and Processes

Change to picture

Metso Truck Body

decreases fuel

consumption per hauled

ton and the rubber lining

decreases noise level by

50% and vibrations as

much as 95%

15

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Based on 2018 Financials

Sales by Segment

Sales by Geography

Sales by Application

Breadth Across Verticals, Geography and Application to Provide Enhanced

Performance

Notes 1. Including €315 million McCloskey estimated calendar year 2018 sales due to September 2018 fiscal year end. Sales by Application excluding Recycling 2. Other includes Non-Ferrous Minerals, Fertilizers, Fuel Minerals, Iron, Zinc and Energy and environmental solutions (incl. water, sulfuric acid and off-gas) 3. Includes Copper, Nickel, Lithium, Cobalt and Tungsten

~20% battery metals(3) ~40% battery metals(3) ~25% battery metals(3)

Minerals(1)

54% 41%

5% Minerals Processing

Aggregates

Recycling

59%

41% Minerals Processing

Metals, Energy & Water

37%

39%

24% EMEA

Americas

APAC

54% 27%

19% EMEA

Americas

APAC

42%

35%

23% EMEA

Americas

APAC

21%

14%

6%

7%

2%

1% 1%

18%

30%

CopperFerrous MetalsIndustrial MineralsPrecious MetalsAluminiumNickelLithiumOtherAggregates

35%

17% 8% 4%

3% 2%

31%

Copper

Precious Metals

Aluminium

Nickel

Lithium

Ferroalloys

Other

14%

19%

9%

2%

12%

44%

Copper

Ferrous Metals

Industrial Minerals

Precious Metals

Other

Aggregates

52%

19%

19%

9%

1% Services

Aggregates Equipment

Minerals Equipment

Metals, Energy & WaterEquipmentRecycling

(2)

(2) (2)

16

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Significant Cost Synergy Opportunities…

At least €100

million run-rate

annual pre-tax

cost synergies

Full realisation

expected by the

end of the third

year following

completion

~60%

of Run-Rate Operations

Procurement

• HQ and administration

• Footprint

• Service utilisation

• IS / IT

• Supply chain optimisation

• Leveraging combined scale

~40%

of Run-Rate

• Implementation costs estimated at ~€100

million to be largely incurred in the first 12-

24 months post-closing

• Well-defined synergy targets

• Integration process to leverage the best

talent from both Metso Minerals and

Outotec businesses

• Implementation to minimise disruption to the

Combined Company's operations and

customers

• Executive oversight with clear priorities

Established Integration Framework

17

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

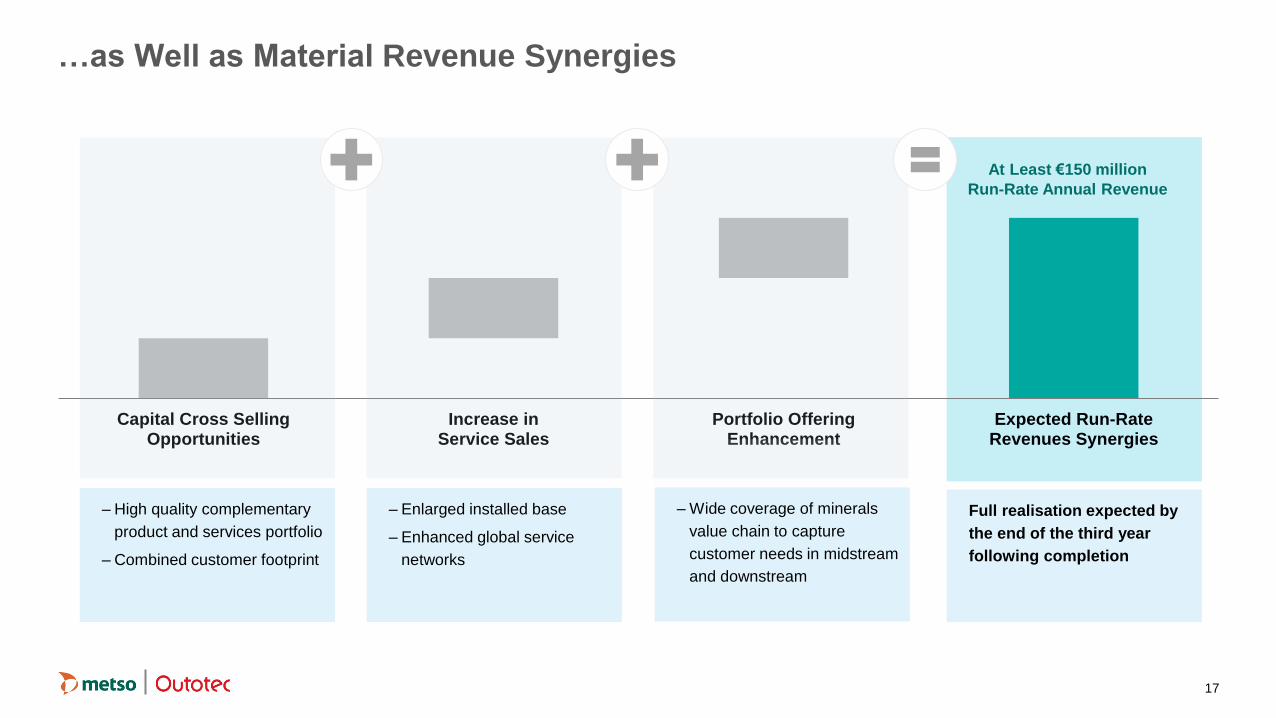

Capital Cross SellingOpportunities

Increase inService Sales

Portfolio OfferingEnhancement

Expected Run-RateRevenues Synergies

…as Well as Material Revenue Synergies

At Least €150 million

Run-Rate Annual Revenue

– High quality complementary

product and services portfolio

– Combined customer footprint

– Enlarged installed base

– Enhanced global service

networks

– Wide coverage of minerals

value chain to capture

customer needs in midstream

and downstream

Full realisation expected by

the end of the third year

following completion

18

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Solid Capital Structure and Attractive Dividend Policy

Notes 1. Does not include acquisition debt for McCloskey International

• Metso Outotec(1) with illustrative combined net debt of €331 million at 31 March 2019

• Metso Outotec to benefit from strong free cash flow, a solid capital structure and will aim for an investment grade credit rating in line with current Metso rating Capital Structure

• Metso to seek certain consents, waivers and amendments in respect of bonds outstanding at the time of the combination

• Bonds to become obligations of Metso Outotec, in accordance with demerger plan

• €1.55 billion backup facilities have been agreed with Nordea Bank Abp for the benefit of Metso and subsequently Metso Outotec in connection with the transaction

Financing

• Dividend policy to be determined by the board of Metso Outotec following completion of the transaction

• Metso Outotec expected to have the capacity for an attractive dividend policy, consistent with Metso’s current policy, while maintaining a strong balance sheet Dividend Policy

• Metso shareholders to receive previously declared 2018 dividend of €0.60 per share, payable in November 2019

• Metso board may propose a dividend of up to €221 million in aggregate to be payable in 2020 before closing of the transaction, implying €1.47 dividends per share

• Outotec board may propose a dividend of up to €20 million in aggregate to be payable in 2020 before closing of the transaction, implying €0.11 dividends per share

Pre-Closing

Dividends

19

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

A Complementary and Compelling Combination for Stakeholders

Scale and

Breadth

• Combination of two highly complementary global businesses with wide presence across the value chain

• Enlarged installed base and enhanced services focus

• Strong presence across verticals, geography and applications

Technology

and R&D

• Leverage combined group’s technology and R&D

• Sustainability at the core of Metso Outotec’s customer offering and operations

People and

Governance

• Strong cultural fit, including customer focus and innovation

• Greater scale offers opportunities for industry experts

• Experienced board and management

Attractive

Shareholder

Returns

• Significant revenue and cost synergies

• Strong balance sheet

• Attractive dividend profile

Neles

A Leading Pure-Play

Flow Control Company

21

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

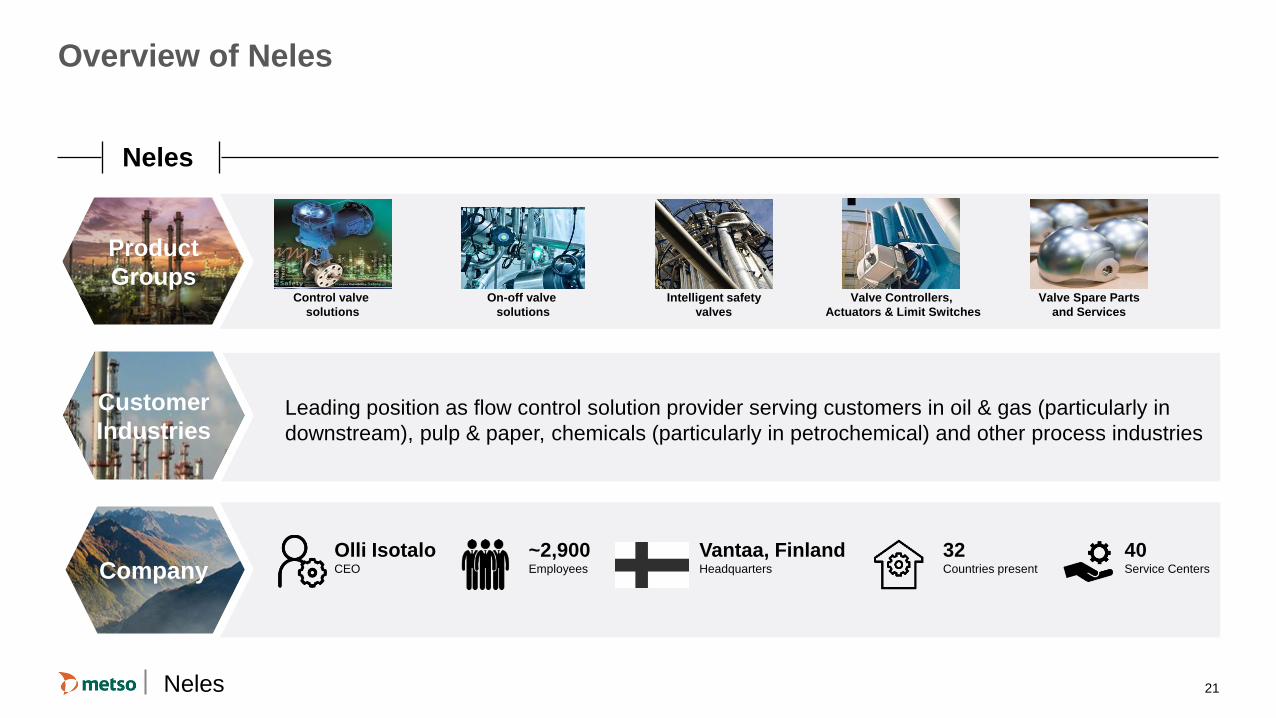

Overview of Neles

Leading position as flow control solution provider serving customers in oil & gas (particularly in

downstream), pulp & paper, chemicals (particularly in petrochemical) and other process industries

Customer

Industries

Company ~2,900 Employees

Vantaa, Finland Headquarters

Olli Isotalo CEO

32 Countries present

40 Service Centers

Neles

Product

Groups Control valve

solutions

On-off valve

solutions

Intelligent safety

valves

Valve Controllers,

Actuators & Limit Switches

Valve Spare Parts

and Services

Neles

22

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

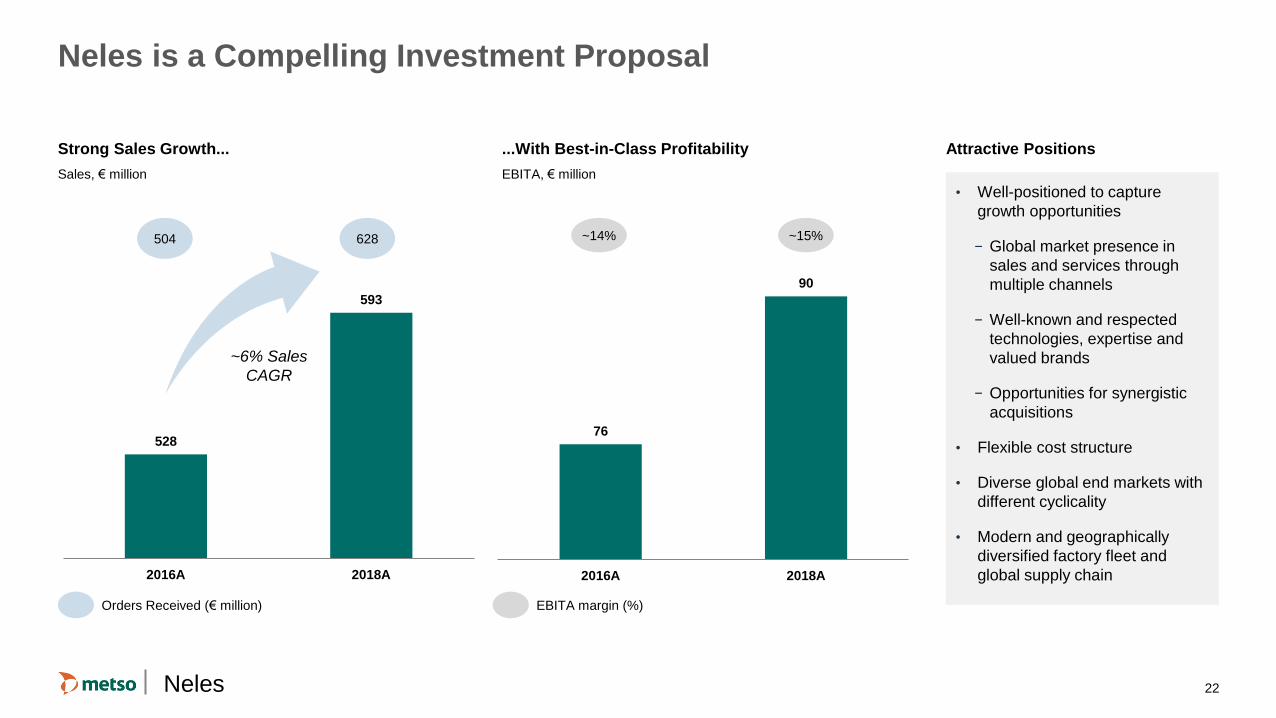

Neles is a Compelling Investment Proposal

• Well-positioned to capture

growth opportunities

− Global market presence in

sales and services through

multiple channels

− Well-known and respected

technologies, expertise and

valued brands

− Opportunities for synergistic

acquisitions

• Flexible cost structure

• Diverse global end markets with

different cyclicality

• Modern and geographically

diversified factory fleet and

global supply chain

528

593

2016A 2018A

~6% Sales

CAGR

504 628

76

90

2016A 2018A

~14% ~15%

Neles

Orders Received (€ million) EBITA margin (%)

Strong Sales Growth...

Sales, € million

...With Best-in-Class Profitability

EBITA, € million

Attractive Positions

23

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Overview of Neles’ End Markets

Neles

Notes 1. Maintenance, repairs and operations

Recent

Development

Oil & Gas 37%

Chemicals 22%

Pulp & Paper 27%

Other Industries

14%

Sales Split by End Markets

Global Market

Drivers

Oil and gas upstream, midstream and downstream Opex and

Capex

Pulp & paper and bioproducts Opex and Capex

Petrochemicals and Other Chemicals Opex and Capex

Flow Control End Markets Have Strong Long-Term Growth Potential

Strong Long-Term Market Drivers

2018A

Overall process industry Opex and Capex

24

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

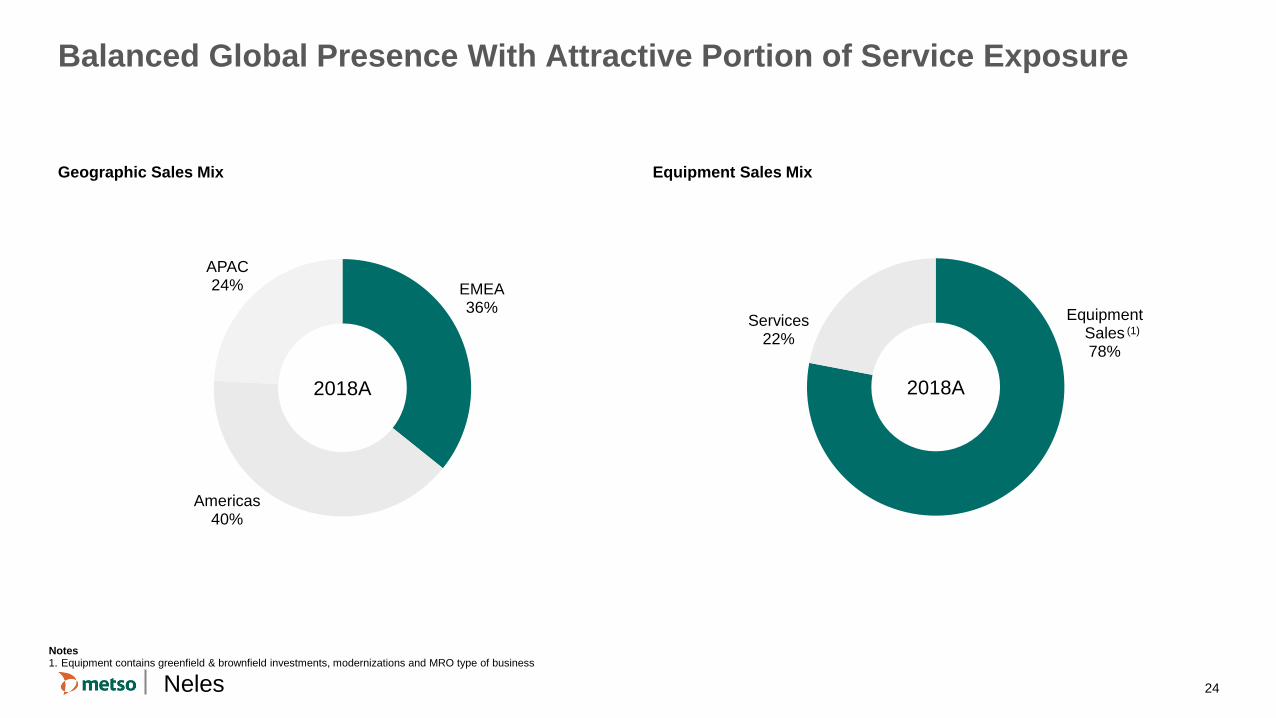

Balanced Global Presence With Attractive Portion of Service Exposure

Geographic Sales Mix Equipment Sales Mix

Neles

EMEA 36%

Americas 40%

APAC 24%

2018A

Equipment Sales 78%

Services 22%

2018A

(1)

Notes 1. Equipment contains greenfield & brownfield investments, modernizations and MRO type of business

25

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

11.8x

23.9x

17.0x

15.1x 14.3x

12.6x 12.4x 11.7x

11.1x

Enterprise Value / EBIT(1)

2020E

Notes 1. Source: Capital IQ as of 2 July 2019

Crystalising Value Potential Through Re-rating Compared to

Flow Control Peers

Neles

26

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Neles: A Highly Attractive Investment Opportunity

Leading position as a flow control solution provider with market leadership across pulp & paper valves and down stream oil & gas control valves

Continued outperformance of market growth with best-in-class profitability and proven resilience through the cycle

Solid balance sheet and financial position

Diversified sales mix both by region and industry

A fully focused, dedicated management to deliver shareholder value and leverage further growth opportunities

Crystallisation of attractive sector trading multiples

Neles

Conclusion

Neles

28

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Indicative Key Transaction Milestones

• Initiation of regulatory review

• Publication of demerger prospectus

• Metso and Outotec EGMs

• Metso and Outotec 2019 dividend payment

• Expected closing

Q3 2019

October 2019

March 2020

Q2 2020

29

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Creating Two Leading Companies…

... in Process Technology, Equipment and Services … and in Flow Control

€2.9 billion(1)

2018 Sales

€1.3 billion 2018 Sales

€4.2 billion(1)

2018 Sales

Notes 1. Including €315 million McCloskey estimated calendar year 2018 sales due to September 2018 fiscal year end

Minerals

~€600 million

2018 Sales

Neles

Flow Control

30

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

Appendix

31

Content

(Top Alignment)

Subtitles

(bottom alignment)

Page Titles

(bottom alignment

Page Content

Left Alignment Page Content

Right Alignment

Content

(Bottom Alignment)

Footnotes

(Top Alignment)

224/101/44

205/220/233

127/127/127

255/255/255

0/0/0

230/230/230

Chart 7

Chart 8

Chart 9

Chart 1

Chart 2

Chart 3

Chart 4

Chart 5

Chart 6

0/0/0

22/155/214

207/207/207

235/241/246

192/192/202

Body Text

Background

Message Box

Table Highlights

Titles

235/235/235

135/135/135

252/238/224

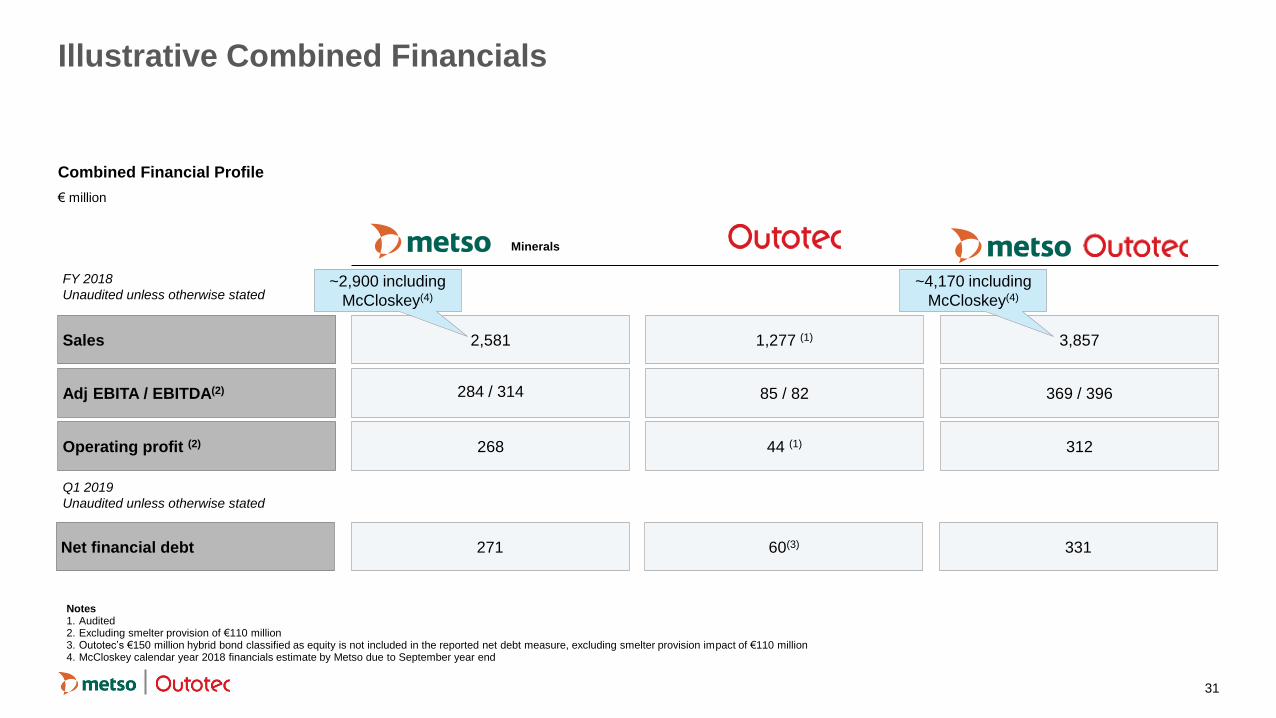

Illustrative Combined Financials

Combined Financial Profile

€ million

Notes 1. Audited 2. Excluding smelter provision of €110 million 3. Outotec’s €150 million hybrid bond classified as equity is not included in the reported net debt measure, excluding smelter provision impact of €110 million 4. McCloskey calendar year 2018 financials estimate by Metso due to September year end

FY 2018

Unaudited unless otherwise stated

Sales 2,581 1,277 (1) 3,857

Adj EBITA / EBITDA(2) 284 / 314 85 / 82 369 / 396

Operating profit (2) 268 44 (1) 312

Minerals

~2,900 including

McCloskey(4)

~4,170 including

McCloskey(4)

Net financial debt 271 60(3) 331

Q1 2019

Unaudited unless otherwise stated