“come grow with us” - demerara bank

TRANSCRIPT

ANNUAL REPORT 2012

1 The Logo

2 CorporateObjectives

2 OurMission

2 CorporateInformation

3 NoticeofMeeting

4 ProxyForm

5 FinancialSummary

6 CorporateResponsibility

9 Dr.YesuPersaud,‘An Icon of Sterling Performance’

10 BoardofDirectors

12 ManagementTeam

14 Chairman’sReport

18 ChiefExecutiveOfficer’sReport

23 ReportoftheDirectors

25 Auditors’Report

26 StatementofFinancialPosition

28 StatementofComprehensiveIncome

30 StatementofChangesinEquity

31 StatementofCashFlows

32 NotestoFinancialStatements

59 CorrespondentBanks

60 OurServices

CONTENTS

“Come grow with us”

TheelementsoftheDemeraraBankLogodesignaredrawnfromtheverysourceoftheinspirationthatcreatedsuchanenterprise.

TherelentlessforceofthemightyDemeraraRiver,whichgivestheBankitsname,isdepictedinthesixgoldenstreamsthatflowfromastylishspringin

anupwardmotion.

TheSixstreamsorsixpeople,symbolisethediverserace,andculturesthatmovetogethertowardsacommonGuyanesedestiny.

ThecoloursgoldandgreenhavebeenchosenfortheiraffinitytotheGuyaneselandscapeandtherichesoftheabundantnaturalresourcesforwhichthecountryisfamous.TheDemeraraBankstandsproudandsecure,

reflectingitscommitmenttoGuyanaandconfidenceinthefuture.

The Logo

Tohelpbuildastronger,healthiermorediversebusinesssectorthroughprudentinvestment,attractivedepositplansand

innovativelendingpolicies.

Toprovidethefinancialsupportthatwilldemonstratethebank’scommitmenttobusinessdevelopmentandtoabetterGuyana.

ToprovideadiversifiedrangeofqualityfinancialservicesthroughitsworldwidenetworkofMajorCorrespondentBanks.

Toprovideemployeeswithexcellentopportunitiesforpersonalgrowthanddevelopment.

Toprovideinvestorswithandattractiverateofreturnontheirinvestment.

Tobearesponsiblecorporatecitizen.

DIRECTORSDrYesuPersaud(Chairman)MrPravinchandraDave(ChiefExecutiveOfficer)MrsChandraGajrajMrKomalSamarooDrLeslieChinMrsSheilaGeorgeMrWilliamBarrowMrHemrajKissoon

CORPORATE SECRETARYMrsChandraGajraj

AUDITORSNizam Ali & Company Chartered Accountants215‘C’CampStreet,NorthCummingsburg,Georgetown,Guyana

ATTORNEY AT LAWDe Caires, Fitzpatrick & Karran80CowanStreet,KingstonGeorgetown,Guyana

ATTORNEY AT LAWPersaud and Associates1CroalStreetGeorgetown,Guyana

ATTORNEY AT LAWLuckhoo & LuckhooLot1CroalStreet,Georgetown,Guyana

REGISTRAR & TRANSFER OFFICETrust Company (Guyana) Limited1stFloor,DemeraraBankBuilding230Camp&SouthStreetsGeorgetown,Guyana

REGISTERED OFFICE230Camp&SouthStreetsGeorgetown,GuyanaTelephone:+592-225-0610-9Cable:DEMBANK,GuyanaTelex:6738093(USA)Fax:+592-225-0601Email:[email protected]:www.demerarabank.com

“Toexcelinprovidinginnovativeandsuperiorbankingservicesthroughwelltrained,dedicatedandcourteousstaffintheinterestofourcustomersandshareholdersandtofulfilloursocialresponsibilitiestosocietythroughmeaningfulinvolvementincommunitydevelopment.”

Corporate Objectives

Our Mission

Corporate Information

2

DEMERARA BANK LIMITED

Notice of Meeting

NoticeisherebygiventhattheEighteenthAnnualGeneralMeetingofDemeraraBankLimitedwillbeheldonFriday,21stDecember,2012,at16.30hoursattheDiamondBranch,PlotDBL,Diamond,EastBankDemerarawhenthefollowingbusinesswillbetransacted:

1) ToreceiveandtoconsidertheReportoftheDirectorsandtheAuditedAccountsfortheyearended30thSeptember,2012.

2) Toapprovethedeclarationofadividend.

3) ToelectDirectorsintheplaceofthoseretiringbyrotation.

4) TofixtheremunerationoftheDirectors.

5) ToappointAuditorsandauthorisetheDirectorstofixtheirremuneration.

6) TotransactanyotherbusinessofanAnnualGeneralMeeting.

BYORDEROFTHEBOARD

......................................................

ChandraGajraj(Mrs.)CorporateSecretary

REGISTERED OFFICE230Camp&SouthStreetsGeorgetown,Guyana

November5,2012

PLEASE NOTE:

* OnlyShareholdersortheirdulyappointedproxiesmayattend.

* PleasebringthisnoticetogainentrytotheMeeting.

* Anymemberentitledtoattendandvoteisentitledtoappointaproxytoattendandvoteinsteadofhim/her.

* AproxyneednotbeamemberoftheBank.TheFormofProxymustbedepositedattheRegisteredOfficeoftheBanknotlessthan48hoursbeforethetimeforholdingthemeeting.

* Aproxyformisattachedforuse.

* AnyCorporationwhichisamemberoftheBankmay,byresolutionofitsDirectorsorothergoverningbody,authorisesuchpersonasitthinksfittoactasitsrepresentativeattheMeeting.

* Giftswillbedistributedonlytoshareholderspresentatthemeetingandnotanytimeandplacethereafter.

3

Annual Report 2012

Proxy Form

Demerara Bank Limited230CampandSouthStreetsGeorgetownGuyana

I/We..........................................................................................................................................

of...............................................................................................................................................

beingamember/membersofDEMERARABANKLIMITED,

herebyappoint..........................................................................................................................

of...............................................................................................................................................

orfailinghim/her....................................................................................................................

of...............................................................................................................................................

asmy/ourProxytovoteinmy/ourname(s)andonmy/ourbehalfuponanymatterattheEighteenthAnnualGeneralMeetingoftheBanktobeheldonFriday,21stDecember,2012oranyadjournmentthereofinsuchmannerassuchProxymaythinkproper.

Aswitnessmyhandthis.....................dayof.............................................2012

Signedbythesaid......................................................................................................................

(NameofMember(s))................................................................................................................

(SignatureofMember(s))...........................................................................................................

NOTE:Tobevalid,thisformmustbecompletedanddepositedwiththeSecretaryatleast48hoursbeforethetimeappointedforthemeetingoradjournedmeeting.

4

DEMERARA BANK LIMITED

Financial Summary

Deposits Profit after Taxation

Advances

Assets

Distribution of IncomeAssets

2008 $21 Billion

2008 $750 Million

2008 $7 Billion

2008 $25 Billion

2009 $25 Billion

2009 $818 Million

2009 $9 Billion

2009 $30 Billion

2008 2009 2010 2011 2012 $21.200 $24.893 $28.974 $30.169 $35.048

2008 2009 2010 2011 2012 $749.600 $818.271 $853.396 $983.987 $1043.424

2008 2009 2010 2011 2012 $6.730 $8.708 $9.917 $12.037 $15.392

2008 2009 2010 2011 2012 $25.139 $29.874 $34.464 $36.016 $42.114

2010 $29 Billion 2010

$853 Million

2010 $10 Billion

2010 $34 Billion

2011 $30 Billion

2011 $984 Million

2011 $12 Billion

2011 $36 Billion

2012 $35 Billion

2012 $1,043 Million

Interest Income2008

$1,601 Million

2009 $1,735 Million

2008 2009 2010 2011 2012 $1,601 $1,735 $1,946 $2,152 $2,430

2010 $1,946 Million

2011 $2,152 Million

2012 $2,430 Million

Interest Expense

2008 $784 Million

2009 $910 Million

2008 2009 2010 2011 2012 $784 $910 $1,010 $733 $574

2010 $1,010 Million

2011 $733 Million

2012 $574 Million

2012 $15 Billion

2012 $42 Billion

InterestExpenses 574 30.6%Premises&Equipment 26 1.4%PersonnelExpenses 368 19.6%AdministrativeExpenses 201 10.7%Taxation 456 24.3%Dividends 252 13.4% 1,877

Cash&ShortTermFunds 10,627 25.2%Investments 15,202 36.1%Premises&Equipment 851 2.0%Loans&Advances 15,392 36.6%OtherAssets 28 0.1% 42,100

(G$ Mln) (G$ Mln)

Investments $15,202 Million

Other Assets $28 Million

Premises & Equipment

$851 Million

Loans & Advances $15,392 Million

Cash & Short Term Funds $10,627 Million

Administrative Expenses $201 Million

Personnel Expenses $368 Million

Taxation $456 Million

Dividends $252 Million

Interest Expenses

$574 Million

Premises & Equipment $26 Million

5

Annual Report 2012

Corporate Responsibility

Presentation of Awards to the Branches for their outstanding performance

Corriverton Branch Rose Hall Branch Anna Regina Branch

Building Expo 2012

Demerara Bank Limited participated for the third year in the building exposition, organized and hosted by the Ministry of Housing and Water at the Guyana National Stadium.

Pictures depict a few staff members that were involved in the Expo along with potential credit customers.

Phagwah ( Anna Regina Branch)

Emancipation (Head Office)

Demerara Bank’s staff dressed in traditional outfits to celebrate the festivities

6

DEMERARA BANK LIMITED

Donation made by our Rose Hall Branch to Mayor and Town Council (Waste Management Department) - Rose Hall Town.

Presentation to winners of the “Christmas Cheer Promotion” – Rose Hall Branch.

Demerara Bank Limited launched banking facilities for the first time to the people of the East Coast Corridor.

Chairman, Dr Yesu Persaud, presenting plaque and cash award to top student, Sarah Hakh who topped the country and the Caribbean in CXC this year.

Opening of our Le Ressouvenir Branch in October 2011

Presentation of Gift Certificates to winners of the “Easter Cash Promotion” – Rose Hall Branch.

7

Annual Report 2012

Corporate ResponsibilityBEV Processors – Financing for export oriented Seafood processing plant

Amazon Caribbean – Processing of Heart of Palm in the North West and Berbice Regions for Export.

Housing – Our housing Drive continues

Car Loan – Assisting young professionals in owing their own Motor Vehicle

Dr. Balwant Singh’s Hospital – Modern State of the Art Hospital

Forestry – Contributing to the Development in Forestry Sector

8

DEMERARA BANK LIMITED

Dr. Yesu PersaudChairman, Demerara Bank Limited

Our Chairman Dr. Yesu Persaud was featured in the recent publication – ‘100 Influential Indians in the World’ in

which he was listed under the section of ‘Legends’. Publisher & Editor Mr. A.R. Giri PhD in an article on Dr. Persaud named him ‘An Icon of Sterling Performance’ in which he has dedicated himself towards reshaping the national economy with his pragmatic vision and humanistic consideration. What has made Yesu a rare luminary is his landmark success in providing a progressive direction to the economic development of the entire Caribbean region, besides transforming the economic destiny of the Companies under his control.

“Yesu has been the man behind the formation of the first indigenous Private Sector Bank in Guyana, Demerara Bank Limited.” On November 12, 1994, Yesu established Demerara Bank Limited. Though it was incorporated on January 20, 1992, it was granted a license in March 1994, building of the Bank commenced that very month and on November 12, 1994 it was declared opened by His Excellency, Dr. Cheddi B. Jagan, President of the Cooperative Republic of Guyana as also the first PIO to access this position in that country. On its launching ceremony, Dr. Jagan congratulated Yesu and called him “a dynamic businessman to have turned into gold everything he puts his hands on.”

Dr. Persaud also holds numerous positions of respect in several organizations all of which are working commendable under his esteem leadership. He serves as the Executive Chairman of the Demerara Distillers Limited Group of Companies, these includes:

• Demerara Distillers Limited.

• Demerara Shipping Company Limited

• Distribution Services Limited

• Tropical Orchards Products Company Limited

• Demerara Contractors and Engineers Ltd

• Demerara Distillers (Europe)

• Demerara Distillers (US) Inc.

• Demerara Distillers (St. Kitts) Limited

He is also the Chairman of the following companies/institutions:

• Institute of Private Enterprise Development (IPED)

• Trust Company (Guyana) Limited

• Guyana Unit Trust – A Mutual Fund Institution

• Guyana Youth Business Trust

• Consultative Association of Guyanese Industry Ltd. (CAGI)

After eighteen years Demerara Bank stands strong and has been moving from strength to strength with this year, 2012, being the first in the history of the bank to achieve a billion dollar profit. The bank has established a network of six branches with a branch in each of the county to ensure all class of people have access to suburb and customer friendly banking facilities.

Dr. Persaud remains a strong motivational force for our institution. We are inspired by his grand vision.

9

Annual Report 2012

Board of Directors

STANDING Left to Right:Mr Pravinchandra Dave (C.E.O),

Mr Komal Samaroo, Dr Leslie Chin

and Mr William Barrow

DEMERARA BANK LIMITED

SITTING Left to Right:Mr Hemraj Kissoon, Mrs Chandra Gajraj, Mrs Sheila George

and Dr Yesu Persaud (Chairman)

Annual Report 2012

BACK ROW, Left to RightDebroah A. Sugrim, Assistant Manager (Foreign Trade); John Lee, Manager (Management Information System);

Pravini Ramoutar, Manager, Human Resources & Administration.

FRONT ROW, Left to RightNavita Sahadeo, Chief Internal Auditor; David Ramdeholl, Assistant Manager (Credit Monitoring, Recovery & Legal);

Juanita A. Persico, Manager (Administration & Operations).

Management Team

DEMERARA BANK LIMITED

BACK ROW, Left to Right Mandrekar Khemraj, Branch Manager (Corriverton); Earlene Dawson, Branch Manager (Rose Hall);

Imran Badruddin, Branch Manager (Diamond);

FRONT ROW, Left to RightKhemraj Narine, System Administrator; Serojanie Singh, Branch Manager (Le Ressouvenir Branch).

Deyon D’Oliviera, Branch Manager (Anna Regina).

Annual Report 2012

Chairman’s Report

I extend a warm welcome to the shareholders and all Guyanese. It gives me pleasure in welcoming you to the 18th

Annual General Meeting of the Bank.

OUTLOOK OF ThE GLOBAL ECONOMY

The global economy is still struggling tofindsteadygroundsanddebtoverhanginseveraloftheEuropeancountriescloudstheoutlook.The global economic activities have becomeunevenacrosstheregionsandcountriesandconfidencelevelshaveplunged.Theongoingdebt issues in the European region and thepossiblespill-overeffectsintotheeconomywillaffecttheUnitedStates,emergingmarketsandothercountries. Theyear2012beganwithapositivenotecombined with a marked improvement inmonetaryeasingindevelopedanddevelopingcountries. The world economy is projectedto grow in 2012 by 3.3% and 3.6% in 2013.Thegrowth in theUnitedStates isprojectedat2.2%,whileEuropeanareasmayregisteranegativegrowthof0.4%.China’sGDPgrowthmaybearound7.8%whileIndiamaybeinthevicinityof4.9%to6%.

The outlook for the Caribbean economy isheavilydependentontheWesterneconomiesparticularly the United States and Europeancountries, which are the two major sourcemarketsfortourism,andCaribbeanregions.

TheCaribbeanisprojectedtogrowattherateof3.5%from4.3%in2011.TheslowergrowthintheCaribbeanregionisattributedtoweaker

“...the Bank has been able to achieve a landmark figure of G$1 billion, which is an outstanding achievement for the Bank”.

Dr. Yesu Persaud, Chairman

14

DEMERARA BANK LIMITED

globalexternalenvironment,highoilprices,capacityconstraints in selected economy and a decline incommoditypricesandtourism.

ThE GUYANA ECONOMY

The Guyana economy has been one of the mostresilient in the Caribbean region during the globalfinancialcrisisandeventualeconomicrecession. Infact,overthepastfiveyears,thecountryhasrecordedan average GDP rate of 4.4%. In 2011, Guyana’seconomyexpandedatarobustrateof5.4%,largelysupported by the services sector, followed by themanufacturing,agriculturalandminingsectors.

Theeconomyislikelytogrowatarateof3.8%to4%during2012.Guyana’sgoodperformancerelativetotheCaribbeanneighboursisonaccountofadiverseeconomy. It isprojectedthattheGuyanaeconomywillcontinuetogrowifGovernmentpaysundividedattention to the development of infrastructure,maintaining law and order situations and creatinginvestment-friendly environment for local andoverseasinvestors.

Caribbean countries need to increase their shareof market. Guyana and other countries shouldimplementregionalintegrationthroughtheCaricomSingleMarketandEconomy(CSME),harmonizationof regulations, reductionofbarriers to the regionalmovementoflabourandliberalizationofairtransportservices.

PERFORMANCE OF ThE BANK

It givesme pleasure to report to the shareholdersontheoutstandingperformanceoftheBankduring2011-2012.

The Bank has performed exceedingly well duringtheyear.WehaveachievedthehighestprofitinthehistoryoftheBank,recordingaNetProfitAfterTaxtothetuneofG$1.043billionagainstG$983millionintheprecedingyear,whichreflectsariseof6.1%overthepreviousyear.

Demerara Bank Limited is only eighteen years oldbuthasmaderapidstrides in the last tenyears. Itis remarkable that,within such a short period, the

BankhasbeenabletoachievealandmarkfigureofG$1billion,whichisanoutstandingachievementfortheBank. Duringtheyear,wehaveopenedtheLeRessouvenir,EastCoastDemeraraBranch.Atpresent,theBankishavinganetworkofsixBranches,includingHeadOfficelocationandwehaveplanstoexpandournetwork,includingaspaciousHeadOfficepremisesin2012-2013.

DEPOSITS

TotalDepositsoftheBankhaveincreasedfromG$30billion toG$35 billion,which shows an increase of16.7% over the previous year. Deposit growth inthe banking sector in Guyana increased by 13.3%for the period under review. The performance oftheBankindepositmobilizationareaissatisfactory.ItisnoteworthythattheBrancheshavesignificantlycontributed to the growth of deposits. We havebeen able to enhance our Savings Bank Depositsconsiderably.

Duringtheyear,thecostofourfundshasgonedownand theshareof institutionaldepositshas reducedsignificantly.TheBankwillcontinuetopayattentiontoimprovingtherangeofproductsandservicesfordepositorsinthecomingyears.

LOANS AND ADvANCES

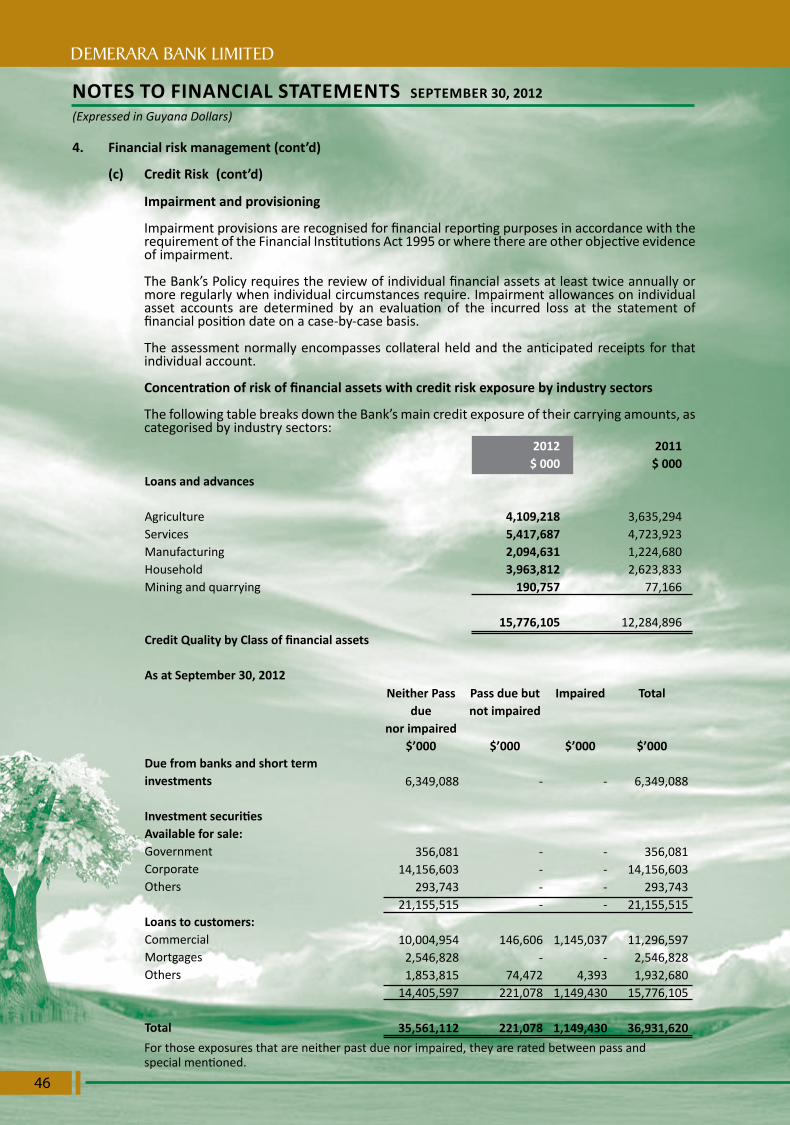

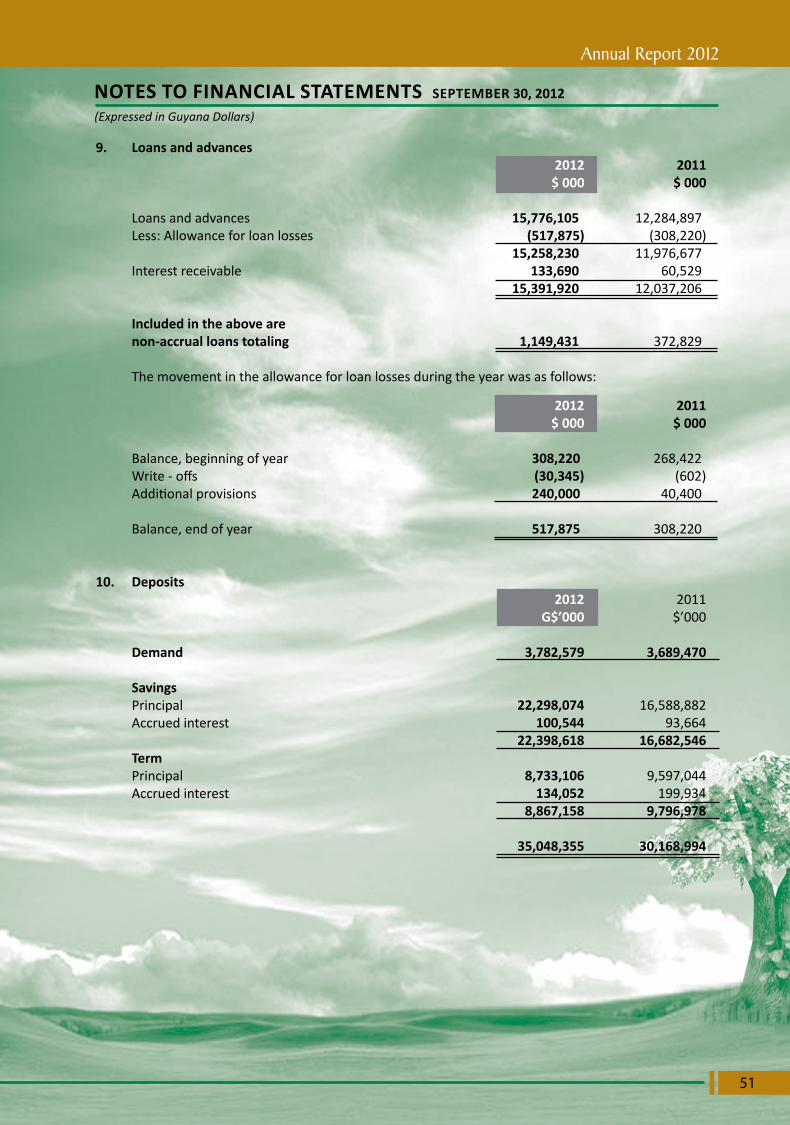

OurLoansandAdvanceshaveincreasedfromG$12billiontoG$15billion,reflectinganincreaseof25%overthepreviousyear.ThecreditdepositratiooftheBankhasremainedinthevicinityof43%.Weplanto increase our Advances significantly during thenextthreetofouryearswiththemajorfocusonthedistribution,agriculture,miningandforestrysectors.WehaveawelldiversifiedAdvancesportfoliowhichcanbeseenfromthefollowingfigures:-

1. Agriculture 26.05%2. Mining&Quarrying 1.21%3. Manufacturing 9.59%4. Construction&Engineering 3.68%5. Commercial/Trading/Distribution18.64%6. RealEstate 16.14%7. Services 15.71%8. Consumption 8.98%

15

Annual Report 2012

The banks are flushed with funds and in Guyanathere are limited opportunities for investments,resulting in Advances remaining the major assetdeployment segment. We have a good networkofBranchesandourfocuswillbeonincreasingourAdvancesthroughtheBranches.Theprioritysectorforlendingwillbeagriculture,housingandconsumerloans at the Branches. We are creating a pool ofspecializedOfficerstoexplorethecreditpotentialofourbranches.

PROFITABILITY OF ThE BANK

TheNetAssetsof theBankhasmoved fromG$36billion to G$42 billion, registering a rise of 16.7%over the previous year. The Return on AverageAssets is2.67%comparedto2.81%inthepreviousyear. There was significant improvement in theShareholders’Fundsinthelastfiveyears.TheReturnonShareholders’Fundswas19.23%duringtheperiodunderreview.TheNetworthoftheBankhasimprovedfromG$4.4billiontoG$5.7billion,registeringariseof29.5%overthepreviousyear.Almost24%oftheBank’sassetsareinLiquidAssets,givinganexcellentliquiditypositionoftheBank.

EARNINGS PER ShARE

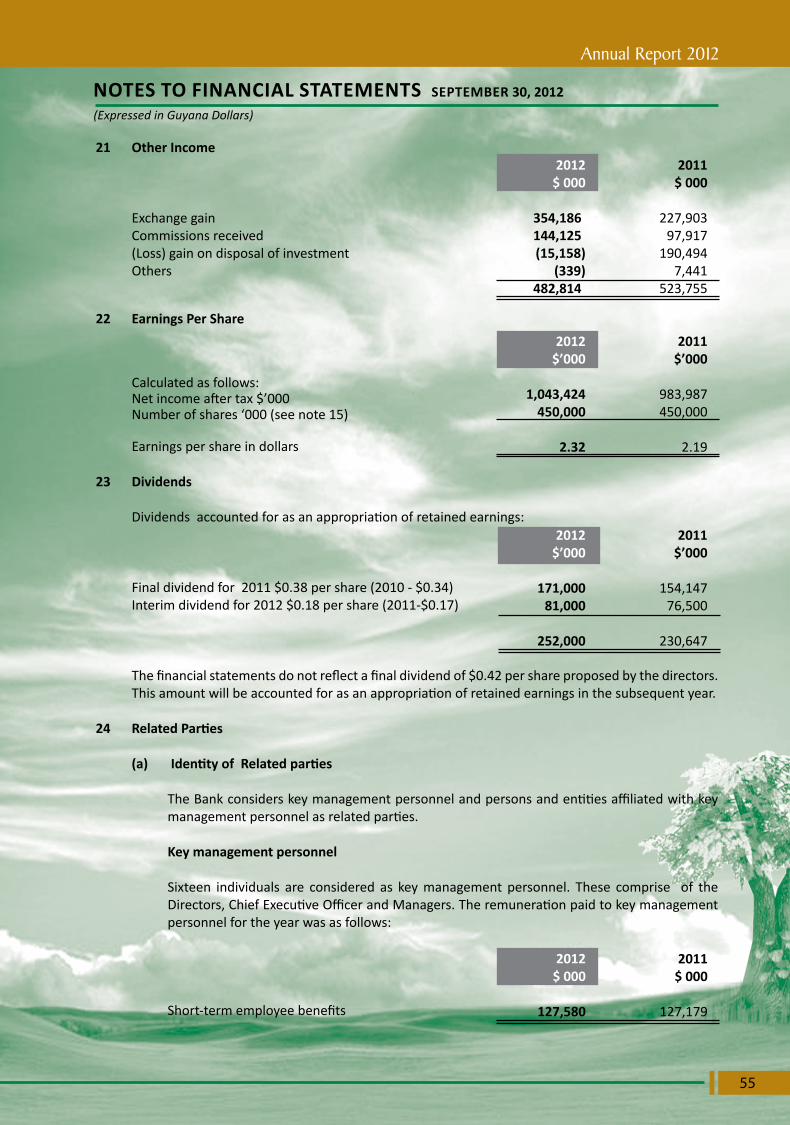

EarningsPerSharehasimprovedto2.32%pershare,whichreflectsariseof5.9%overthepreviousyear.TheBankhasbeenabletoachievecontinuousgrowthintheareasof improving itsprofitandprofitability.TheShareholdershavebeenamplyrewardedinthelasttenyearsnotonlybyhealthydividendsbutalsofromrisingmarketcapitalizationofourBank’sshares.The share of the Bank which was traded aroundG$1.00 toG$2.00at the inceptionof thebankhasgoneuptoG$25.00toG$30.00asattheendofthefinancialyear.

DIvIDENDS

The Bank has paid an interim dividend of 18%duringtheyear.TheBoardofDirectorsishappytorecommendafinaldividendof42%.Thefinaldividend

will be subject to approval of the shareholders attheAnnualGeneralMeeting. This brings the totaldividendofsharespaidbytheBanktoG$0.60onaG$1.00share.ThisreflectsthehighestdividendpaidinthehistoryoftheBank.

Inthelowinterestrateenvironment,wherereturnonfixeddepositsislow,theinvestmentinequitywiththeappreciationofcapitalisagoodoptionforthegeneralpublicandInstitutions.TheBankshalltrytoimproveourperformance in the future tomake investmentin our Bankmore rewarding for our shareholders.It isnoteworthythatmostoftheshareholderswhosubscribed inourBank’s shares to the InitialPublicOfferin1994haveremainedloyaltotheBank.WearegratefultotheshareholdersfortheirloyaltyandconfidencetotheBank.

INFORMATION TEChNOLOGY

ThisyearwasayearofconsolidationforInformationTechnology. TheperformanceofthenewsoftwarefortheATMandPOSsystemswasexaminedindetailwiththeintentionofcompletelyunderstandinghowthesystemsworksothatwecouldbeindependentof our overseas consultants for the resolution ofthe majority of issues. We have reviewed our ITsecurity systems and various improvements weremadethroughupgradesandtheimplementationofnewequipment. Alsoreviewed,wereourbusinessintelligence systems which assist Managers andSupervisorsintheirdecisionmakingprocesses.

MANAGEMENT AND STAFF

Our accomplishments in recent years would nothave been possible without the right people andmanagementinplacetoexecutetheplans.Talentisthebackdropofourstrategyandwestronglybelievethat,inaserviceindustrylikeourBank,wewillonlyexcelbyofferinginnovativeproductsandservicestoourcustomers.TheBankbelievesthatinachangingbanking environment, continuous introduction ofskillsistherequirementoftheday.Ourstaffhasdoneexceedinglywellinachievingoutstandingresultsfor

Chairman’s Report (cont’d)

16

DEMERARA BANK LIMITED

theBankduringthelasteighteenyears.

The Bank has a pool of talented, young staff. Weshallcontinuetoimprovetheirknowledge,skillsandaptitudeforbetterresultsinthefuture.Iwouldliketothankmanagementandstaffatalllevelsfortheirdedicationandperformancetowardstheirduties.

BOARD OF DIRECTORS

IwishtoplaceonrecordmysincereappreciationforthevaluableguidanceandcontributionmadebyallDirectorsduringtheyearthroughactiveparticipationnotonlyinmonthlyBoardMeetingsbutalsoLoans,Marketing,AuditandInvestmentMeetings.

PROSPECTS

The global world faces serious problems of debts,deficits,unemploymentandslowgrowth.Guyanaisboomingpartiallyonaccountofgoldminingandricemillingwhereassugarisstilllaggingbehind.

ThereareexcellentprospectsofdevelopmentintheminingandforestrysectorsinGuyana.Weneedtomaximize our value-added products and services.Thecompetentauthoritywillhavetoworkoutalongtermdevelopmentandstrategicplanfortherevivalof

thesugarindustrysothattheindustrycancontinueto

playadynamicroleintheeconomy.

Our knowledge of the customer and passion for

improvingourvaluableservicesatalllevelsofbanking

willcontinueintothefuture. Theexpansionofthe

Bank’s network and the focus on improving value-

added services and products, with our pragmatic

bankingapproach,willcarryustothenewheights.

Ourobjectivesfor2012aswellas2013aretocontinue

afinanciallysoundbankwithabusinessmoduleto

developcoreareasofbanking.TheBankwillcontinue

todevelopskillsinouremployeestomanagetherisks

inanappropriateandresponsiblemanner.

ACKNOWLEDGEMENT

The Bank has received continued support and

patronage from customers, shareholders and well-

wishersinGuyanaandabroad.Wearegratefulfor

the valuable support and guidance of the Bank of

Guyana and other Agencies. We are also thankful

forthecontinuedpartnershipandsupportofother

financial institutions and correspondent banks in

Guyanaandabroad.

Diamond Branch

17

Annual Report 2012

Chief Executive Officer’s Report I extend my greetings and best wishes to all shareholders and the Guyanese public.

Theyear2012hasbeenadifficultandchallengingyear, internationally and locally. The developedeconomiesof theworldhave remained sluggishafter the recession of 2008-2009. The impactof slowdown in the United States andWesterneconomy has affected developing countries ina negative way until the last quarter of 2011.The United States economy continues to faceproblemsofhighdebtandunsustainabledeficit.TheUnitedStatesfacesdangerofafiscalcliff inDecember, 2012. There is no definitive plan inEurope to solvedebt issuesofGreece, ItalyandSpain. In China, economic reforms have beenstalled. It is evident that growth in China andIndia isalsoslowingdown. Indiamayachieveagrowthof 4.9%andChina’s growthmay remainwithinthevicinityof7%to9%.

Caribbean economies continue to face an uphillbattle in the aftermath of the global recession,withmutedeconomicactivitiesin2011and2012.MajorCaribbeancountrieswiththeexceptionofGuyanaandTrinidad&Tobagoaredependentontourismandotherlimitedeconomicactivities.

GUYANA’S ECONOMY

Guyana’seconomicgrowthwas2.8%inthefirstsixmonthsof2012comparedto5.9%in2011.Thegrowth was mainly driven by mining, quarryingand services sectors. Bauxite and gold outputwasbetterwhile the sugarand forest industriesrecorded poor performance. There was amarginaldeclineinthemanufacturingsector.Theinflationwasinthevicinityof2%andwasmainlydrivenbyhighfuelandfoodprices.Theeconomyisprojectedtogrowby3.8%attheendof2012.

The agricultural sector is expected to reboundleadby sugar,fishingand livestock. Theminingsectorwillcontinuetobenefitfromhigheroutput

Mr. Pravinchandra S. Dave, CEO

18

DEMERARA BANK LIMITED

in gold production and better prices. Inflationmayremaininthevicinityof3%to5%.

BANKING TRENDS

Thedepositsofthecommercialbankscontinuetoexpand in linewith thegrowth in theeconomy.Depositsincreasedby6.5%inthefirsthalfof2012.Outof commercialbanks’deposits, around77%was private sector deposits. The net domesticcreditbythebankingsystemincreasedby15.2%in

thefirstsixmonthsof 2012. Bankingsector depositswere G$266.5billion at the endof September,2011, which hasincreased toG$301.9 billionas at the end ofSeptember, 2012;registering a riseof 13.3% duringthe period. TheAdvances topublic andprivatesectors by bankswere aroundG$12.5 billion asat September,2011, which hasgrown to G$15.1billion as at theendofSeptember,2012; registeringa rise of 20.8%

duringthetwelvemonths.Theliquiditypositionof Bank’s was very comfortable. The BanksmaintainedexcessfundswiththeBankofGuyana,reflectinganexcessliquidityposition.Duringtheyear, funds continued to flow in GovernmentTreasuryBills,whichwasreflectedbyahighlevelofexcessbiddinginGovernmentTreasuryBills.

Interest rates of the commercial banks haveshownadownwardtrendwithsmallSavingsBankratedecliningfrom1.99%to1.75%asattheendofJune,2012,whileaverageSavingsBankratefor2012continuedtobeinthevicinityof1.56%.91-days’TreasuryBillsratecamedownfrom2.35%attheendofDecember,2011to1.82%asattheendof June, 2012. The lending rate of commercialbankswasinthevicinityof11%to12%,reflecting

comfortable spread for commercial banks.Guyana’sexchangeratehasremainedremarkablystableduring2011to2012inspiteoftheturmoilintheglobalcurrencymarket.

ThestableexchangeratewhichhasmovedaroundG$203toG$205isgreatlyhelpfulinmaintainingthe lower level of inflation and stability of foodprices. Guyana’seconomyisdifferentandmoreresilientcomparedtootherCaribbeaneconomies,whicharedependentononeortwosectors.Theprospects of oil exploration and continuationof high gold prices may result in higher grossdomesticproductforGuyanain2012-2013.

PERFORMANCE OF ThE BANK

Our Bank has shown excellent performanceduringtheyearandhighlightsofourperformanceareashereunder:-

3 DepositsoftheBankhaveincreasedfromG$30billiontoG$35billion,registeringariseof16.7%overthepreviousyear.

3 TheGross Profit of the BankwasG$1.4billion last year, which has increased toG$1.5 billion – a rise of 7.1% over thepreviousyear.

3 NetProfitoftheBankwasG$983millionwhich has increased to G$1.043 billion,registeringariseof6.1%overthepreviousyear.

3 TheBank’sAdvanceshaveimprovedfromG$12 billion to G$15 billion, showing ariseof25%overthepreviousyear.

3 Investments of the Bank were G$12.5billion as at September 30, 2011,whichhas increased toG$15.2 billion in 2012,showingariseof21.6%overthepreviousyear. Investment re-valuation reserveswere negative at G$246 million as atSeptember30,2011,whichhasimprovedtoapositiveG$283million.

3 Earnings Per Share has improved from2.19%to2.32%pershare,showingariseof5.9%overthepreviousyear.

3 ReturnonAverageAssetshasdecreasedslightly but is still above the industryaverage.

“The Net Profit of the Bank has improved from G$983 million to G$1.043 billion, showing a rise of 6.1% over the previous year. It is noteworthy that the Bank’s Profit was G$107 million in 2001, which has gone up above the G$1 billion mark in 2012”

19

Annual Report 2012

3 Return on Shareholders’ Funds was19.23%; a marginal decline over thepreviousyear.

3 TotalNetworthoftheBankhasimprovedfrom G$4.4 billion to G$5.7 billion,registering a rise of 29.5% over thepreviousyear.

DEPOSIT MOBILIzATION

OurDepositshaveincreasedfromG$30billiontoG$35billionduring the year. Themostnotablefeature of our deposit mobilization was theincrease in our Savings Bank Deposits. Duringtherecentpast,wehaveexpandedthenetworkof our branches to six. Our main objective isto increase the number of deposit holders byproviding excellent technology, good bankingproducts and competitive rates of interest ondeposits. Wehave introduced special incentiveschemesforourbranchestomobilizemaximumnumberofaccountduringtheyear.Incidentally,allourbrancheshadpromotionalactivitiesduringtheyearorganizing‘specialweeks’andrewardingcustomerswithprizesandincentives.

Our Bank was the first to initiate internetbanking in Guyana. Our deposit mix was notveryfavourableintheinitialyears,havingahighlevelofTermDeposits.WehavemadesustainedeffortstoreduceourTermDepositsandincreaseourshareofSavingsandDemandDeposits.

Atpresent,theshareofourSavingsBankDepositsand Demand Deposits is approximately 75% ofourtotalDeposits. Withthedecreasinginterestratescenario,interestonSavingsBankDepositsinGuyanahasshownadownwardtrend.WeshallintroducecustomersegmentspecificproductstofurtherenhanceourSavingsBankDeposits.

AdvAnces And non-Performing Assets

OurAdvances have increased fromG$12 billiontoG$15billionasatSeptember30,2012,whichshowsariseof25%overthepreviousyear.ItshouldbenotedthatthetotalbankingsectorAdvanceshasincreasedfromG$87billiontoG$108billionfromSeptember,2011toSeptember,2012.

InGuyana,theratioofcredittoGDPisverylow

comparedtoothercountries.Duringtheyear,thenationalaverageofthecreditdepositratiowasinthevicinityof29%to35%,whileourBank’screditdepositratiowas36%to44%duringtheyear.

InGuyana,thedemandforbankableprojectshasremained low, resulting in high liquidity for ourBankaswellasotherbanks.

The activities in the mining sector have growntremendously over the last three years. Thepriceofgoldcontinuedtoshowanupwardtrendduring the year. The number of Licences andMiningPermitshasincreasedinthelastyear.Theforestrysectorhasalsoexpandedduringtheyear.We are exploring the possibilities of extendingmore credit to themining and forestry sectors.The major area of concern in financing thesesectorsisthenon-availabilityofcollateralandtosomeextent,non-availabilityofauditedFinancialStatements.

We had obtained a Line of Credit from theInter-American Investment Corporation (IIC) forprovidinglongtermcredittoourexport-orientedentrepreneurs. The rate of interest on suchborrowingwasbelow5%.

OurNon-Performing Loans have increased fromG$372 million to G$1.1 billion during the year.This is amainareaof concern forus. We shalldevelopplansfortherecoveryofourduesfromNon-PerformingAccounts. OurNon-PerformingLoans are fully backed by assets and we haveadequate provision for providing for Losses inNon-PerformingLoans.Weshallcontinuetopayundividedattentiontothequalityofappraisalforadvancesinthecomingyears.

INvESTMENT

OurInvestmentwasG$12.5billionasonSeptember30,2011,whichhas increasedtoG$15.2billion,showinga riseof 21.6%over theprevious year.In Guyana, we do not have much Investmentoptions. The banking system is having highliquidityand lowcreditdeposit ratio. Hopefullyin the coming years, the Government will takesomestepsfortheestablishmentofmutualandmoneymarket funds. It is noteworthy thatourInvestment Re-valuation Reserve was negativeG$246 million as at September 30, 2011, has

Chief Executive Officer’s Report (cont’d)

20

DEMERARA BANK LIMITED

movedtoapositiveG$283millionduringtheyear.

INCOME AND ExPENSES

The Net Profit of the Bank has improved fromG$983million toG$1.043billion,showingariseof6.1%overthepreviousyear. It isnoteworthythattheBank’sProfitwasG$107millionin2001,which has gone up above the G$1 billionmarkin 2012. We have been able to achieve profitgrowthconsistentlyinthelastelevenyears.Thisisonaccountofourprudentassetsandliabilitiesmanagement. Interest IncomeonAdvanceshasincreased from G$1.2 billion to G$1.3 billion,showingariseof8.3%overthepreviousyear.

Our Interest Income on Investment was G$974millionlastyearwhichhasmovedtoG$1.1billionthisyear,showingariseof17.5%overthepreviousyear.Our Interest Expensehas gonedown fromG$732 million as at September 30, 2011 toG$574million, which is a remarkable reductionof interest expenses during the year in view ofthefactthatourdepositshavegoneupbynearly17%duringtheyear.OurNetInterestIncomewasG$1.4billionasatSeptember30,2011,whichhasincreasedtoG$1.9billion,showingariseof35.7%overthepreviousyear.TheimprovementofourNet Interest Income was partially due to theincreaseinourAdvancesandInvestmentIncomeandmainlydue to the reductionofour interestexpensesondeposits. Theexchange incomeofthe bank has increased from G$228 million in2011toG$354millionin2012,registeringariseof55.3%overthepreviousyear.

However,ourcommissionandotherincomehavegone down by nearly G$100 million during theyear. We shall examine the areas of improvingourprofitandprofitabilitytomaximizeourprofitsinthecomingyears. ThestaffcostsoftheBankhave increase from G$329 million to G$368million,showingariseof11.9%overthepreviousyear, while our non-staff administrative costshave increased from G$184 million to G$233million,whichshowsan increaseof26.6%. Ourexpanding network of branches has increasedthecostofconsumableitemsandourstaffcostshave increasedmainly on account of additionalmanpoweratthebranches.

We have appointed a Procurement Committeein the Bank to examine and analyze differentsegments of expenditure. The Committee willfocus on controllable expenses and improve

the procurement methodology and system toincrease our income and reduce our expenses.The independent working of a ProcurementCommittee facilitates transparency andaccountability.

RISK MANAGEMENT AND CAPITAL ADEqUACY

Risk is inherent in banking business which ismainly concerned with the mobilization anddeploymentofmoney.BanksinGuyanaoperatein a regulated but full operational autonomyand freedom to evolve their own policies andprocedures. Risks in commercial banks haveenhanced on account of rapid technologicaldevelopments and a general decline in publicmoral values. Wewill ensure that we are abletodefine,identifyandmeasurerisksinourbankandevolvesoundriskmanagementpracticesandpolicieswhich canprovideearlywarning signalsto initiateprompt, correctiveactions suitingourrequirements.Infuture,weshallsetupaseparateRiskManagementDepartmentwithqualifiedandexperienced staff. At present, risks are beingmonitoredbyanindividualdepartmentundertheoverallsupervisionoftheChiefExecutiveOfficerandtheBoardofDirectors.

Maintaining adequate capital as regulatorynormsandforfuturedevelopmentisverycriticalfor a commercial bank. Regulatory authoritiesin Guyana and international banks, after thefinancial crisis of 2008, have prescribed capitaltobeinlinewithBaslenorms.BanksinGuyanaarerequiredtomaintainaminimumcorecapitalof 8% of the total risk-weighted assets. UnderBasleIII,Banksneedtomaintainanexcesscapitalof 2.5%, in addition to 8%of base capital. OurBank’s capital adequacy ratio as at September30,2012was31.73%comparedto30.29%asatSeptember 30, 2011. The main improvementin the capital adequacy ratiowasonaccountofsignificant improvement in our mark-to-marketinvestmentvalue.Theexcellentcapitaladequacyratioprovidestheplatformforenhancedlendingandsoundnessofthebank.

STAFF TRAINING

Staff training is a continuous process. Wehavedevisedanelaboratetrainingplanforclassroomandon-the-job training for our employees. Wehave already started on-the-job training in thecreditareaforemployeesofourBerbiceandEastCoastBranches.TheBankplanstoimpartspecial

21

Annual Report 2012

training to its employees in the areas of credit,investmentandforeignexchange.

UPhOLDING vALUES AND SOCIAL WORK

As one of our core values, we are an equalopportunity employer. Our policies are non-discriminatory as we continue to strive to offerthebestservicestoallourcustomers,irrespectiveofethnicity, culturalbackgrounds,and religion /belief.TheBankcontinuestoplayaninstrumentalroleasacorporatecitizen.

In accordance with our Mission Statement,the Bank takes pride in fulfilling its socialresponsibilities throughmeaningful involvementincommunitydevelopment.TheBankhasbeenaproudsponsorofvarioussportingandeducationaleventsespeciallyinareaswhereourbranchesarelocated.

Duringourlastfinancialyear,thebankhasgivena number of donations to various organizationsand has supported several meaningful events.Wehaverewardedanumberofstudentsfortheiroutstanding performance in their examinationsalong with recognizing the country’s top CSEC2012 student, re-painted pedestrian crossingsin different areas in close proximity to schoolsas well as contributed to various constructionprojects such as the restoring and rebuilding ofthe St. JosephMercy Hospital and a shelter forvictimsofabuseinBerbice.

In addition, the Bank has on-going programmesfor food distribution, school supplies as wellas financial assistance to various organizationsincluding theHelp&Shelter, LifelineCounselingServices and Avon Community Help Fund forsupportingbreastcancereducation&awareness.

Webelieve thatour contributionshaveandwillcontinue to make positive impacts on the livesof the future generation in Guyana. We shallcontinuetoseeknewmeasurestohelpconservethe usageof our natural resources aswe try torestructure our policies and procedures with a“go-green”initiativeinmind.

ACKNOWLEDGEMENT

We have received good support from our

customers, shareholders and employees.Without the support of our customers, wewould not have achieved good financial results.We also acknowledge and place on record, ourappreciationforthecontributionofallemployeesandmembersofthemanagementteamwhohaveplayedasignificantroleinthesuccessoftheBank.

FUTURE PROSPECTS

The Guyana economy and major economies oftheworld,includingtheUnitedStatesarepassingthroughdifficulttimes.SlowdownoftheUnitedStates and the European economy will have amajor impact on developing countries. Politicalstability will be amajor precondition for futuregrowthandinvestmentinGuyana.

Ourmajorobjectivesinthecomingyearswouldbetoconsolidatefinancialgainsofthelastfewyearsand broaden the customer base by aggressivemarketing and pragmatic approach to problemsofourcustomers.

Weshallfocusonthereductionofnon-performingloansandcontrolourexpenditureandincreasingour non-fund based income to further improveprofitability. We have a committed pool ofhuman resources. Motivation and training willhelp to build a strong Institution. Improvingcustomers’satisfaction,employees’performanceand productivity are the basic requirements forlong-termgrowthandstability. Oursuccesswilldepend on our ability to adapt, engineer bothtechnical and non-technical solutions to ourgrowingcustomerdemandsandexpectations.

We have vision and the infrastructure todevelop a common corporate language forour employees to build a stronger and viablefinancial institution in service of the Guyanesepeople. During challenging times, DemeraraBank has demonstrated exceptional strength.We are entering into a phase of bankingwhichischaracterizedbyhighliquidityandlowinterestrates,with tough competition. We shall alwaysendeavour to offer valuable contribution tothe progress and prosperity of our clients,shareholders, employees and the society as awhole.

Chief Executive Officer’s Report (cont’d)

22

DEMERARA BANK LIMITED

Report of the DirectorsTheDirectorshavepleasureinsubmittingthisReportandAuditedFinancialStatementsfortheyearendedSeptember30,2012.

PRINCIPAL ACTIvITIES:

TheBankprovidesacomprehensiverangeofbankingservicesoutofourmainofficeatCamp&SouthStreets,GeorgetownandBranchesinRoseHall&Corriverton,Berbice,AnnaRegina,Essequibo,Diamond,EastBankDemeraraandLeRessouvenir,EastCoastDemerara.

FINANCIAL RESULTS: (In Thousands of Guyana Dollars)

TheresultsfortheyearendedSeptember30,2012areasfollows:

2012 2011ProfitBeforeTax $1,499,178 $1,389,852Taxation $455,754 $405,865ProfitAfterTax $1,043,424 $983,987

APPROPRIATIONSDividendsPaid $252,000 $230,647RetainedEarnings $791,424 $753,340

DIvIDEND:

TheDirectorsrecommendadividendof$0.60pershare,including$0.18interimpaidinMay2012.

RESERvES AND RETAINED EARNINGS:

TheBankhas reached its statutory reserve limit andno furtherprovision is required. Thebalanceof$791,424 isplacedonRetainedEarningswhichnowstandsat$4,523,425. Theproposeddividendof$189MwillbepaidoutofRetainedEarnings.

DIRECTORS:

InaccordancewithArticle97oftheBank’sArticlesofAssociation,theDirectorsretiringforthetimebeingareMr.KomalR.Samaroo,Mrs.ChandraGajraj,Mrs.SheilaGeorgeandMr.WilliamH.Barrow,andbeingeligible,offerthemselvesforre-election.

AUDITORS:

TheAuditorsNizamAli&Company,beingeligible,offerthemselvesforre-appointment.

DIRECTORS’ EMOLUMENTS:

Dr.YesuPersaud 1,800,000Mr.HemrajKissoon 1,020,000Mr.KomalR.Samaroo 1,020,000Mr.WilliamH.Barrow 1,020,000Mrs.SheilaGeorge 1,020,000Dr.LeslieChin 1,020,000Mrs.ChandraGajraj 1,020,000Mr.PravinchandraDave 360,000

23

Annual Report 2012

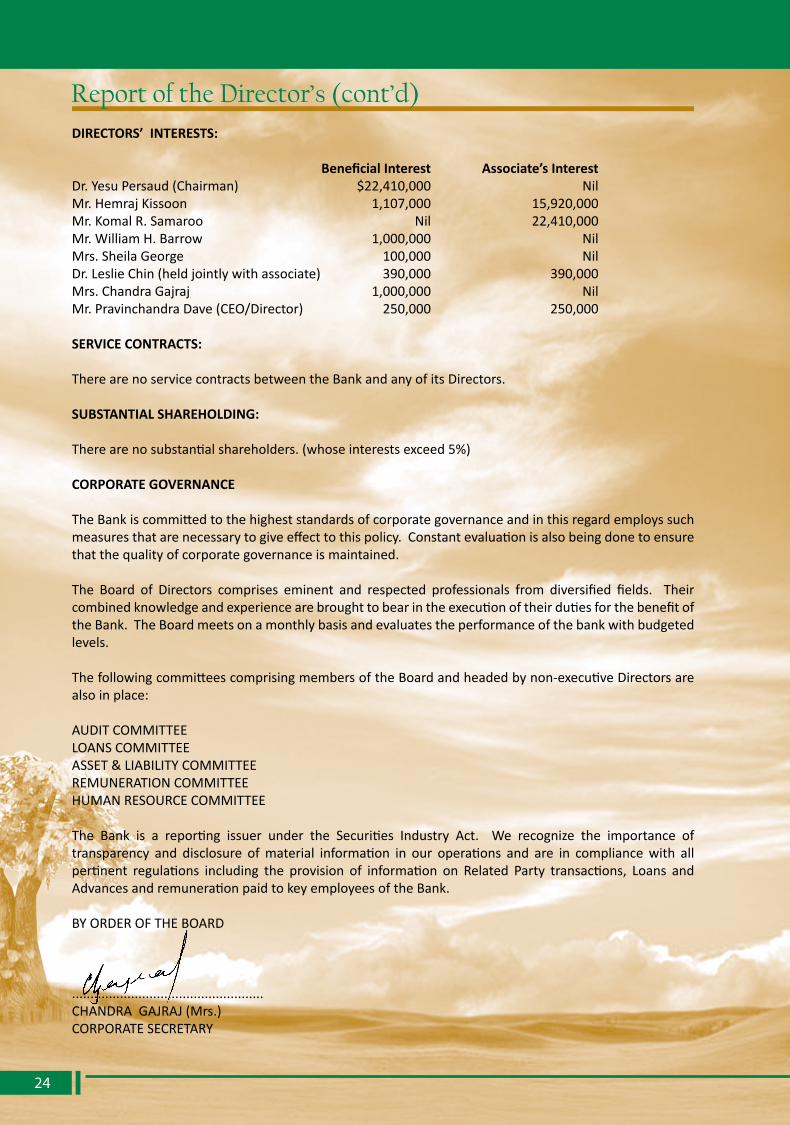

DIRECTORS’ INTERESTS:

Beneficial interest Associate’s interestDr.YesuPersaud(Chairman) $22,410,000 NilMr.HemrajKissoon 1,107,000 15,920,000Mr.KomalR.Samaroo Nil 22,410,000 Mr.WilliamH.Barrow 1,000,000 NilMrs.SheilaGeorge 100,000 NilDr.LeslieChin(heldjointlywithassociate) 390,000 390,000Mrs.ChandraGajraj 1,000,000 NilMr.PravinchandraDave(CEO/Director) 250,000 250,000

SERvICE CONTRACTS:

TherearenoservicecontractsbetweentheBankandanyofitsDirectors.

SUBSTANTIAL ShAREhOLDING:

Therearenosubstantialshareholders.(whoseinterestsexceed5%)

CORPORATE GOvERNANCE

TheBankiscommittedtothehigheststandardsofcorporategovernanceandinthisregardemployssuchmeasuresthatarenecessarytogiveeffecttothispolicy.Constantevaluationisalsobeingdonetoensurethatthequalityofcorporategovernanceismaintained.

The Board of Directors comprises eminent and respected professionals from diversified fields. TheircombinedknowledgeandexperiencearebroughttobearintheexecutionoftheirdutiesforthebenefitoftheBank.TheBoardmeetsonamonthlybasisandevaluatestheperformanceofthebankwithbudgetedlevels.

ThefollowingcommitteescomprisingmembersoftheBoardandheadedbynon-executiveDirectorsarealsoinplace:

AUDITCOMMITTEELOANSCOMMITTEEASSET&LIABILITYCOMMITTEEREMUNERATIONCOMMITTEEHUMANRESOURCECOMMITTEE

The Bank is a reporting issuer under the Securities Industry Act. We recognize the importance oftransparency and disclosure ofmaterial information in our operations and are in compliancewith allpertinent regulations including the provision of information on Related Party transactions, Loans andAdvancesandremunerationpaidtokeyemployeesoftheBank.

BYORDEROFTHEBOARD

....................................................CHANDRAGAJRAJ(Mrs.)CORPORATESECRETARY

Report of the Director’s (cont’d)

24

DEMERARA BANK LIMITED

AUDITORS’ REPORT To the Shareholders of Demerara Bank Limited

We have audited the accompanying financial statements of Demerara Bank Limited; which comprise the statement of financial position as at September 30, 2012 and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of the Bank as of September 30, 2012 and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards and comply with the requirements of the Financial Institutions Act 1995 and Companies Act 1991.

Chartered Accountants Georgetown, Guyana October 17, 2012

Nizam Ali & CompanyChartered Accountants215 ‘C’ Camp StreetNorth CummingsburgGeorgetown

Tel: (592) 227-8825Tel/Fax: (592) 225-7085E-mail: [email protected]

Partners: Nizam Ali - FCCA, CTA; Leslie Verasammy - FCCA

25

STATEMENT OF FINANCIAL POSITION AS AT SEPTEMBER 30, 2012

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

2011$ 000

6,807,0533,784,666

10,591,719

12,527,888

15,000

12,037,206

808,81835,493

844,311

36,016,124

ASSETS Cash and Short Term Funds Cashandcashequivalents StatutorydepositwithBankofGuyana Investments Availableforsale Assets classified as held for sale Loans and Advances Other Property,plantandequipment Otherassets

ThesefinancialstatementswereapprovedbytheBoardofDirectorsonOctober17,2012andsignedonitsbehalfby:

….............………………….....……Mr. Pravinchandra S. Dave

ChiefExecutiveOfficer/Director

….............………………….....……Mr. hemraj Kissoon

Director

Notes

7

8

14

9

1112

2012$ 000

6,452,3644,174,352

10,626,716

15,202,281

15,000

15,391,920

850,51327,747

878,260

42,114,177

26

DEMERARA BANK LIMITED

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

STATEMENT OF FINANCIAL POSITION AsatSeptember30,2012

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

2011$ 000

3,689,470

16,682,5469,796,978

30,168,994

1,461,756

450,000450,000

(246,627)3,732,0014,385,374

36,016,124

Liabilities and shareholders’ equity DepositsDemand Savings Term

other Liabilities shareholders’ equity Sharecapital Statutoryreserve Investmentrevaluationreserve Retainedearnings

Notes

10

13

1516 (i)

16 (ii)

2012$ 000

3,782,579

22,398,6188,867,158

35,048,355

1,359,193

450,000450,000283,204

4,523,4255,706,629

42,114,177

27

Annual Report 2012

STATEMENT OF COMPREhENSIvE INCOME FOR ThE YEAR ENDED SEPTEMBER 30, 2012

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

2011$ 000

1,177,625 974,235 2,151,860

333,419 389,893 9,572 732,884

1,418,976(40,400)

1,378,576 523,755

1,902,331

512,479

1,389,852

405,865 983,987

2.19

Interest incomeLoansandadvancesInvestments Interest expense Savingsdeposits Termdeposits Others Net interest income Loanlossesnetofrecoveries Netinterestincomeafterloan Lossesnetofrecoveries Otherincome Net interest and other income Non-interest expenses Incomebeforetaxation Taxation net income for the year Earnings per share in dollars

Notes

9

21

18

2017

22

2012$ 000

1,285,993 1,144,481 2,430,474 315,325 250,497 7,750 573,572 1,856,902

(240,000) 1,616,902 482,814 2,099,716 600,538 1,499,178 455,754 1,043,424 2.32

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

28

DEMERARA BANK LIMITED

STATEMENT OF COMPREhENSIvE INCOME FOR ThE YEAR ENDED SEPTEMBER 30, 2012

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

2011$ 000

983,987

(492,100)

(208,317)

(700,417)

283,570

net income for the year Other Comprehensive Income

Netchangeinfairvalueofavailable-for-salefinancialassets.

Netchangeinfairvalueofavailable-for-salefinancialassetstransferredtoincomestatement.

Totalothercomprehensiveincome(loss)fortheperiod. Totalcomprehensiveincomefortheyear.

2012$ 000

1,043,424

490,781

39,050

529,831

1,573,255

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

29

Annual Report 2012

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

STATEMENT OF ChANGES IN EqUITY FOR ThE YEAR ENDED SEPTEMBER 30, 2012

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

Total

$’000

4,332,451

983,987

(230,647)

(700,417)

4,385,374

1,043,424

(252,000)

529,831

5,706,629

Statutoryreserves

$’000

450,000 - -

-

450,000

-

-

-

450,000

Retainedearnings

$’000

2,978,661

983,987

(230,647)

-

3,732,001

1,043,424

(252,000)

-

4,523,425

Sharecapital

$’000

450,000

-

-

-

450,000

-

-

-

450,000

Balance at October 1, 2010 ProfitfortheyearSeptember30,2011 Dividend(note23) Netchangeinfairvalueofavailableforsaleinvestment Balance at September 30, 2011 ProfitfortheyearSeptember30,2012 Dividend(note23) Netchangeinfairvalueofavailableforsaleinvestment Balance at September 30, 2012

Investment revaluation

reserve$’000

453,790

-

-

(700,417)

(246,627)

-

-

529,831

283,204

30

DEMERARA BANK LIMITED

STATEMENT OF CASh FLOWS FOR ThE YEAR ENDED SEPTEMBER 30, 2012

WithcomparativefiguresforSeptember30,2011(Expressed in Guyana Dollars)

2011$ 000

1,389,852(2,151,860)

732,885

34,464 - 2,152,985

(877,141)(146,274)

3,801 1,338,933 336,508

(437,725) 2,376,428

(2,615,936)

(700,417)(2,122,828)

-(235,384)

(5,674,565)

(230,647)(230,647)

(3,528,784) 10,335,837

6,807,053

cash flows from operating activities

Netincomebeforetaxation Interestincome Interestexpense Adjustmentsfor: DepreciationLossondisposalofplantandequipmentInterestreceived Interestpaid IncreaseinstatutorydepositwithBankofGuyanaDecreaseinprepaymentsandothers Increaseindeposits Decreaseinotherliabilities TaxespaidNet cash from operating activities cash flows from investing activities Increaseininvestments Netchangeinfairvalueofavailableforsaleinvestmentrecogniseddirectlyinequity IncreaseinloansandadvancesProceedsfromsaleofpropertyplantandequipmentPurchaseofproperty,plantandequipmentNet cash used in investing activities cash flows from financing activities DividendsNet cash used in financing activities net decrease in cash and cash equivalents cash and cash equivalents, beginning of year Cashandcashequivalents,endofyear(note7)

2012$ 000

1,499,178(2,430,474)

573,572

55,744 3,330 2,299,387

(632,573) (389,686)

7,747 4,938,362

(95,298) (463,018)

5,366,271

(2,616,467) 529,831 (3,281,554) 2,710

(103,480) (5,468,960)

(252,000) (252,000)

(354,689) 6,807,053

6,452,364

“Theaccompanyingnotesformanintegralpartofthesefinancialstatements”

31

Annual Report 2012

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

1. incorporation and Business Activities

DemeraraBankLimitedwasincorporatedonJanuary20,1992asaprivatelimitedliabilitycompanyundertheprovisionsoftheCompaniesAct,Chapter89:01andwaslicensedtocarryonthebusinessofBankingonOctober31,1994.TheBankobtainedCertificateofContinuanceonApril2,1997inaccordancewiththeCompaniesAct1991.

TheBankoffersacompleterangeofbankingandfinancialservicesandoperatesundertheprovisionsoftheFinancialInstitutionsAct(Act1of1995).

TheBankwasregisteredasareportingissuerundertheSecuritiesIndustriesAct1998onSeptember02,2003.OnSeptember02,2003theBankwasdesignatedanapprovedmortgagefinancecompanybytheMinisterofFinanceinaccordancewithsection15oftheIncomeTaxAct.Theincomeearnedfrommortgagesgrantedbyanapprovedmortgagefinancecompanyisexemptfromthepaymentofcorporationtaxes,providedthatthesemortgagescomplywiththestipulatedregulations.

2. new standards and interpretations not yet adopted

Current year Revised standardsand interpretationswhichbecameeffectiveduring the current yearandwere

adopteddidnothaveanyimpactontheaccountingpolicies,financialperformanceorpositionoftheBank.

not yet effective Anumberofnewstandards,amendments to standardsand interpretationsarenotyeteffective

for theyearendedSeptember30,2012,andhavenotbeenapplied inpreparing thesefinancialstatements.Discussedbelowarethosestandardsthatwillhaveanimpactonthefinancialstatementsofthebank.

IFRS 9 - Financial Instruments IFRS 9 requires all recognised financial assets that are within the scope of IAS 39 Financial

Instruments: Recognition and Measurementtobesubsequentlymeasuredatamortisedcostorfairvalue.Specifically,debt investments thatareheldwithinabusinessmodelwhoseobjective is tocollectthecontractualcashflows,andthathavecontractualcashflowsthataresolelypaymentsofprincipalandinterestontheprincipaloutstandingaregenerallymeasuredatamortisedcostattheendofsubsequentaccountingperiods.Allotherdebtinvestmentsandequityinvestmentsaremeasuredattheirfairvaluesattheendofsubsequentaccountingperiods.

IFRS9iseffectiveforannualperiodsbeginningonorafter1January2013,withearlierapplicationpermitted.

IFRS 13 - Fair value Measurement IFRS13establishesasinglesourceofguidanceforfairvaluemeasurementsanddisclosuresabout

fairvaluemeasurements.TheStandarddefinesfairvalue,establishesaframeworkformeasuringfairvalue,andrequiresdisclosuresaboutfairvaluemeasurements.ThescopeofIFRS13isbroad;itappliestobothfinancialinstrumentitemsandnon-financialinstrumentitemsforwhichotherIFRSsrequireorpermitfairvaluemeasurementsanddisclosuresaboutfairvaluemeasurements,exceptin

32

DEMERARA BANK LIMITED

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

2. new standards and interpretations not yet adopted (cont’d) IFRS 13 - Fair value Measurement (cont’d)

specifiedcircumstances.Ingeneral,thedisclosurerequirementsinIFRS13aremoreextensivethanthoserequiredinthecurrentstandards.Forexample,quantitativeandqualitativedisclosuresbasedonthethree-levelfairvaluehierarchycurrentlyrequiredforfinancialinstrumentsonlyunderIFRS7FinancialInstruments:DisclosureswillbeextendedbyIFRS13tocoverallassetsandliabilitieswithinitsscope.

IFRS13iseffectiveforannualperiodsbeginningonorafter1January2013,withearlierapplication

permitted.

Amendments to iAs 1- Presentation of items of other comprehensive income

The amendments to IAS 1 retain the option to present profit or loss and other comprehensiveincomeineitherasinglestatementorintwoseparatebutconsecutivestatements.However,theamendmentstoIAS1requireadditionaldisclosurestobemadeintheothercomprehensiveincomesectionsuchthatitemsofothercomprehensiveincomearegroupedintotwocategories:(a)itemsthatwill notbe reclassified subsequently toprofitor loss; and (b) items thatwill be reclassifiedsubsequently to profit or loss when specific conditions are met. Income tax on items of othercomprehensiveincomeisrequiredtobeallocatedonthesamebasis.

TheamendmentstoIAS1areeffectiveforannualperiodsbeginningonorafter1July2012.

3. summary of significant Accounting Policies

Theprincipalaccountingpoliciesappliedinthepreparationofthesefinancialstatementsaresetoutbelow.Thesepolicieshavebeenconsistentlyappliedtothepreviousyear. 3.1 Basis of preparation

3.1.1 statement of compliance ThefinancialstatementsarepreparedinGuyanaDollarsinaccordancewithInternational

Financial Reporting Standards. They have been prepared under the historical costconventionasmodifiedbythevaluationoffinancialassetsavailableforsaleandfinancialassetsatfairvaluethroughtheprofitorloss.

The preparation of these financial statements in conformity with IFRS requiresmanagementtomakeestimatesandassumptionsthataffectthereportedamountofassets,liabilities,contingentassetsandcontingentliabilitiesatthedateofthefinancialstatementsandincomeandexpensesduringtheperiod.Actualresultscoulddifferfromtheseestimates.Theareas involvingahigherdegreeof judgementor complexity,orareaswhereassumptionsandestimatesaresignificanttothefinancialstatementsaredisclosedinnote5.

ThefinancialstatementswereauthorisedforissuebytheBoardofDirectorsonOctober

17,2012.

33

Annual Report 2012

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

3.2 foreign currency translation (a) functional and presentation currency

Items included in the financial statements are measured using the currency of the

primaryeconomicenvironmentinwhichtheentityoperates.ThefinancialstatementsarepresentedinGuyanaDollarswhichisthefunctionalandpresentationcurrency.

(b) transactions and balances

Transactions inforeigncurrenciesaretranslatedattherateofexchangerulingatthetransactiondate.Foreigncurrencymonetaryassetsandliabilitiesaretranslatedattherateofexchangerulingatthestatementoffinancialpositiondate,exceptasotherwisestated. Foreign exchange positions are valued daily at prevailing rates. Resultingtranslationdifferencesandprofitsandlossesfromtradingactivitiesareincludedinthestatementofcomprehensiveincome.

3.3 Property, plant and equipment

Property,plantandequipmentarestatedgenerallyathistoricalcost,exceptforthosemeasuredatfairvalue,whentheyaretestedforimpairment.Historicalcostincludesexpendituredirectlyattributabletotheacquisitionoftheitems.

Property,plantandequipmentistestedforimpairmentwheneverthereisobjectiveevidencethat the carrying amount of the asset may exceed its recoverable amount. Any resultingimpairmentlossisrecognisedimmediatelyinthestatementofcomprehensiveincome.

Subsequentcostsareincludedintheasset’scarryingvalueorrecognisedasaseparateasset,asappropriate,onlywhen it isprobablethatfutureeconomicbenefitsassociatedwiththeitemwillflowtotheBankandthecostof the itemcanbemeasuredreliably.Thecarryingamountofthereplacedpartisderecognised.Alltheirrepairsandmaintenancearechargedto the statement of comprehensive income during the financial period in which they areincurred.

Depreciation of property, plant and equipment excluding land, is provided for, over the

estimatedusefullivesoftherespectiveassetsusingthestraight-linemethod.

Thefollowingannualdepreciationratesareapplicablefortherespectiveassetcategories.

Building 2% Furnitureandequipment 10% Motorvehicles 20% Thegainorlossarisingondisposalorretirementofanitemofproperty,plantandequipment

isdeterminedasthedifferencebetweenthesalesproceedsandthecarryingamountoftheassetandisrecognisedinthestatementofcomprehensiveincome.

3.4 non- current assets held for sale

Anon-currentassetisclassifiedasheldforsalewhen:itscarryingamountwillberecovered

3. summary of significant Accounting Policies (cont’d)

34

DEMERARA BANK LIMITED

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

principallythroughasaletransaction;theassetisavailableforimmediatesaleinitspresentcondition;anditssaleishighlyprobable.Assetsclassifiedasheldforsalearenotdepreciatedoramortisedandarecarriedatthelowerofcarryingamountandfairvaluelesscoststosell.

3.5 financial assets and liabilities

3.5.1 classification

The Bank classifies its financial assets in the following categories: financial assets,at fair value throughprofitor loss, loans and receivables andavailable for sale. Theclassification depends on the purpose forwhich the financial assetswere acquired.Financial liabilitiesareclassified in thefollowingcategories:financial liabilitiesat fairvaluethroughprofitorlossandotherfinancialliabilities.Managementdeterminestheclassificationofitsfinancialassetsandliabilitiesatinitialrecognition.

(a) financial assets at fair value through profit or loss

Financialassetsatfairvaluethroughprofitorlossarefinancialassetsheldfortrading.Afinancialassetisclassifiedinthiscategoryifacquiredprincipallyforthepurposeofsellingintheshortterm.

(b) Available for sale financial assets

Available-for-saleassetsarefinancialassets thatarenotfinancialassetsat fairvalue

throughprofitandlossorloansandreceivablesoriginatedbytheBank.Available-for-saleinstrumentsincludecertaindebtandequityinvestments.

(c) Loans and receivables Loans and receivables are financial assetswith determinable payments that are not

quotedinanactivemarket.

3.5.2 recognition The Bank recognises financial assets on the date it commits to purchasing the assets or

ondisbursement of loans and advances.All other financial assets or liabilities are initiallyrecognisedonsettlementdate.

3.5.3 Measurement Oninitialrecognition,financialassetsandliabilitiesaremeasuredatfairvalueplus,incase

ofafinancialassetorliabilitynotatfairvaluethroughprofitorloss,transactioncostthataredirectlyattributabletotheacquisitionorissueofthefinancialassetorliability.

Subsequentto initial recognitionallfinancialassetsat fairvaluethroughprofitor lossandavailable-for-saleassetsaremeasuredatfairvalue.Wheretheseassetsaretradedonanactivemarket,thequotedmarketpriceisusedtomeasurefairvalue.Wheretheseinstrumentsare

3. summary of significant Accounting Policies (cont’d)

3.4 non- current assets held for sale (cont’d)

35

Annual Report 2012

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

3. summary of significant Accounting Policies (cont’d)

3.5.3 Measurement (cont’d)

notquotedonanactivemarketfairvalueisdeterminedusingdiscountedcashflowanalysis.Estimated future cash flows are based onmanagement’s best estimates and the discountrateisamarketrelatedrateatthestatementoffinancialpositiondateforaninstrumentwithsimilartermsandconditions.

Anyavailable-for-saleassetthatdoesnothaveaquotedmarketpriceinanactivemarketand

wherefairvaluecannotbereliablymeasured,isstatedatcost,includingtransactioncost,lessimpairmentloss.

Gainsand lossesarising fromthechange in the fairvalueofavailable-for-sale investments

subsequenttoinitialrecognitionareaccountedforinthestatementofcomprehensiveincomeasotherrecognisedgains.

Gainsandlosses,bothrealisedandunrealised,arisingfromthechangeinthefinancialassets

andliabilitiesatfairvaluethroughprofitorlossarereportedinotherincome.

All non-trading financial liabilities, loans and receivables and held-to-maturity assets aremeasured at amortised cost less impairment losses. Amortised cost is calculated on theeffectiveinterestratemethod.

3.6 Loans and advances LoansandadvancestocustomerscompriseofloansandadvancesoriginatedbytheBankand

areclassifiedasfinancialassetsatamortisedcost.

All loans and advances are recognised when cash is advanced to borrowers and arederecognisedwhenborrowersrepaytheirobligationorwhentheloaniswrittenoff.Loansarewrittenoffafterallnecessarylegalprocedureshavebeencompletedandtheamountofthelossisfinallydetermined.

Uponclassificationofaloantonon-accrualstatus,interestceasetoaccrueandallpreviouslyaccruedandunpaidinterestisreversedinthecurrentperiod.Interestisonlyrecognisedinsubsequentperiods,totheextentthatpaymentofsuchinterestarereceived.

Loansandadvancesaregenerally returned toaccrual statuswhenthetimelycollectionofboth principal and interest is reasonably assured and all delinquent principal and interestpaymentsarebroughtcurrent.

Impairment TheBankcarriesoutadetailedreviewofitsloanportfoliotwiceyearly.

Specificprovisionsareestablishedasaresultofthesedetailedreviewsofindividualloansand

advancesandreflectanamountwhichinmanagement’sjudgement,providesadequatelyforestimatedlosses.Factorsconsideredinsuchanalysesinclude:

(i) Delinquencyincontractualpaymentsofprincipalorinterest

36

DEMERARA BANK LIMITED

3. summary of significant Accounting Policies (cont’d)

3.6 Loans and advances (cont’d)

Impairment (cont’d)

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

(ii) Cashflowdifficultiesexperiencedbytheborrower (iii)Breachofloancovenantsorconditions (iv) Initiationofbankruptcyproceedings (v) Deteriorationinthevalueofcollateral

TheBank’spolicyforprovisioningconformwiththerequirementoftheFinancialInstitutionsAct(FIA)1995.

UndertheprovisioningrequirementoftheFIA1995,uponreviewoftheloanportfolio,loans

areclassifiedinoneoffivecategories:pass,specialmention,sub-standard,doubtfulandloss.Provisionsarethenmadebasedonclassificationoftheloan.

GeneralprovisionisestablishedwhereprudentassessmentbytheBankofpastexperienceandexistingeconomicandportfolioconditions indicatethat it isprobablethat losseshaveoccurred,butwheresuchlossescannotbedeterminedonanitem-by-itembasis.

Doubtfulloansarewrittenoffafterallnecessarylegalprocedureshavebeencompletedandtheamountofthelossisfinallydetermined.

Theprovisionfortheyear,lessrecoveriesofamountspreviouslywrittenoffandthereversalofprovisionnolongerrequired,isdisclosedinthestatementofcomprehensiveincomeasloanlossesnetofrecovery.

3.7 Provisions Provisions are recognisedwhen theBankhas a present legal or constructiveobligation as

aresultofpastevents, it isprobablethatanoutflowembodyingeconomicbenefitswillberequiredtosettletheobligation,andareliableestimateoftheamountoftheobligationcanbemade.

3.8 Dividend on ordinary shares

Dividend that are proposed and declared during the period are accounted for as an

appropriationofretainedearningsinthestatementofchangesinequity.

Dividendthatareproposedanddeclaredafterthestatementoffinancialpositiondatearenotshownasaliabilityonthestatementoffinancialpositionbutaredisclosedasanotetothefinancialstatements.

3.9 revenue recognition

Loans and investments Interestincomeisaccountedforontheaccrualbasisforinvestmentsandforallloans

other than non-accrual loans using the effective interest ratemethod.When a loanis classified as non- accrual, any previously accrued but unpaid interest thereon isreversedagainstincomeofthecurrentperiod.Thereafter,interestincomeisrecognised

37

Annual Report 2012

3. summary of significant Accounting Policies (cont’d)

3.9 revenue recognition (cont’d)

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

onlyaftertheloanrevertstoperformingstatus.

Fees and commission income Feesandcommissionarenotincludedinthecalculationofeffectiveinterestrate.These

feesarerecognisedinincomewhenabindingobligationhasbeenestablished.Wheresuchobligationsarecontinuing,incomeisrecognisedoverthedurationofthefacility.

3.10 Pension TheBankparticipatesinamulti-employerplanwithcertainothercompanies,theassetsof

whichareheld intrustee-administeredfundswhichareseparatefromtheBank’sfinances.Theplan is generally fundedby payments fromparticipating companies taking account ofrecommendationsofindependentqualifiedactuaries.

3.11 cash and cash equivalents Cashandcashequivalentscompriseofcashonhandandshorttermhighlyliquidinvestments

thatarebothreadilyconvertible intoknownamountsofcashandsoneartomaturitythattheypresentinsignificantriskofchangesinvalueduetochanginginterestrates.

3.12 Acceptances, guarantees and letters of credit

The Bank’s commitments under acceptances, guarantees and letters of credit have beenexcluded from these financial statements because they do not meet the criteria forrecognition. These commitments as at September 30, 2012 amounted to $1,293,663,417(2011-$1,009,386,459).Intheeventofacallonthesecommitments,theBankhasequalandoffsettingclaimsagainstitscustomers.

3.13 taxation Tax expense for the period comprises current and deferred tax. Tax is recognised in the

statementofcomprehensiveincome,excepttotheextentthatitrelatestoitemsrecogniseddirectlyinequity.Inthiscasethetaxisalsorecognisedinequity.

Current tax Thecurrentincometaxiscalculatedonthebasisofthetaxlawsenactedatthestatementof

financialpositiondate.Managementperiodicallyevaluatespositionstakenintaxreturnswithrespecttosituationsinwhichapplicabletaxregulationissubjecttointerpretation.

Deferred tax Deferredincometaxisrecognised,usingtheliabilitymethod,ontemporarydifferencesarising

between the tax base of assets and liabilities and their carrying amounts in the financialstatements.

Thetaxbaseofassetsandliabilitiesarenotmateriallydifferentfromtheircarryingamounts,

consequently,noprovisionisrecognisedinthesefinancialstatementsfordeferredtaxassetorliability.

38

DEMERARA BANK LIMITED

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

3.14 Leases Leaseinwhichasignificantportionoftherisksandrewardsofownershipareretainedbythe

lessorareclassifiedasoperatingleases.Paymentsmadeunderoperatingleasesarechargedtothestatementofcomprehensiveincomeonastraight-linebasisovertheperiodofthelease.AllleasingarrangementstowhichtheBankisapartyareconsideredoperatinglease.

3.15 segment reporting Abusiness segment isa componentofanentity that isengaged inprovidingproductsor

servicesthataresubjecttorisksandreturnsthataredifferentfromthoseofotherbusinesssegments. A geographical segment is engaged in providing products or serviceswithin aparticulareconomicenvironmentthataresubjecttorisksandreturnsthataredifferentfromthoseofsegmentsoperatinginothereconomicenvironments.

3.16 comparatives Certaincomparativeswererestatedtoconformwiththepresentationofthecurrentyear.

4. Financial risk management

TheBank’sactivitiesexposeittoavarietyoffinancialrisks:marketrisk(includingpricerisk,interestrateriskandcurrencyrisk),liquidityriskandcreditrisk.TheBank’soverallriskmanagementprogramfocusesontheunpredictabilityoffinancialmarketsandseekstominimisepotentialadverseeffectsontheBank’sperformance.

TheBoardofDirectorsisresponsiblefortheoverallriskmanagementapproachandforapprovingtheriskstrategiesandprinciples.

TheBank’smanagementmonitor’sandmanagesthefinancialrisksrelatingtotheoperationsoftheBankthroughinternalriskreportswhichanalyseexposuresbydegreeandmagnitudeofrisks.

TheBank’srisksaremeasuredusingmethodswhichreflecttheexpectedlosslikelytoariseinnormalcircumstances.

Monitoringandcontrolling risks isprimarilyperformedbasedon limitsestablishedby theBank.

TheselimitsreflectthebusinessstrategyandmarketenvironmentoftheBankaswellasthelevelofriskthattheBankiswillingtoaccept.

TheBankactivelyusescollateraltorescueitscreditrisks. (a) Market risk TheBank’sactivitiesexposeittofinancialrisksofchangesinforeigncurrencyexchangerates

andinterestrates.TheBankusesgapanalysis,interestratesensitivityandexposurelimitstofinancialinstrumentstomanageitsexposuretointerestandforeigncurrencyrisk.

3. summary of significant Accounting Policies (cont’d)

39

Annual Report 2012

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

4. Financial risk management (cont’d)

(a) Market risk (cont’d)

i) Price Risk

Priceriskistheriskthatthevalueoffinancialinstrumentswillfluctuateasaresultofchangesinmarketpriceswhetherthosechangesarecausedbyfactorsspecifictotheindividualsecurityofits issuerorfactorsaffectingallsecuritiestradedinthemarket.Managementcontinuallyidentifiestheriskanddiversifiestheportfoliotominimisetherisk.

TheBankdoesnotactivelytradeinequityinstruments.TheBank’sexposuretoequity

pricerisksarisingfromequityinvestmentsisnotmaterialtothefinancialstatements.

(ii) Interest rate risk TheBankisexposedtointerestrateriskbuttheBank’ssensitivitytointerestisimmaterial

asitsfinancialinstrumentsaresubstantiallyatfixedrates.TheBanksexposuretointerestrateriskonfinancialassetsandfinancialliabilitiesaredisclosedonpages40and41.

Total

$’000

10,626,71615,391,92015,202,281

893,26042,114,177

35,048,3551,359,1935,706,629

42,114,177

-

Over 5 years

$’000

-4,166,609

14,354,021-

18,520,630

----

18,520,630

1-5 years

$’000

-3,764,562754,516

-4,519,078

8,867,158--

8,867,158

(4,348,080)

Within 1year

$’000

6,349,0886,321,741

93,744-

12,764,573

22,396,943142,270

-22,539,213

(9,774,640)

Average Interest

rate

%

1.2511.027.80

2.002.25

Maturing 2012

Assets CashresourcesNetloanstocustomersInvestmentsOthers Liabilities and shareholders’ equity CustomersdepositsOtherliabilitiesShareholders’equity interest sensitivity gap

Non- interestbearing$’000

4,277,628

1,139,008-

893,2606,309,896

3,784,2541,216,9235,706,629

10,707,806

(4,397,910)

40

DEMERARA BANK LIMITED

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

Total

$’000

10,591,71912,037,20612,527,888

859,31136,016,124

30,168,9941,461,7564,385,374

36,016,124

-

Over 5 years

$’000

-3,232,5447,619,716

-10,852,260

---

10,852,260

1-5 years

$’000

-2,738,086

20,149-

2,758,235

9,796,978141,576

-9,938,554

(7,180,319)

Within 1year

$’000

5,628,9915,693,7464,888,023

16,210,760

16,686,56181,600

-16,768,161

(557,401)

Average Interest

rate

%

1.2510.417.96

2.462.25

Maturing 2011

Assets CashresourcesNetloanstocustomersInvestmentsOthers Liabilities and shareholders’ equity CustomersdepositsOtherliabilitiesShareholders’equity interest sensitivity gap

Non- interestbearing$’000

4,962,728 372,830 - 859,311 6,194,869

3,685,455 1,238,580 4,385,374 9,309,409

(3,114,539)

4. Financial risk management (cont’d)

(a) Market risk (cont’d)

(ii) Interest rate risk (cont’d)

41

Annual Report 2012

NOTES TO FINANCIAL STATEMENTS SEPTEMBER 30, 2012

(Expressed in Guyana Dollars)

4. Financial risk management (cont’d)

(a) Market risk (cont’d)

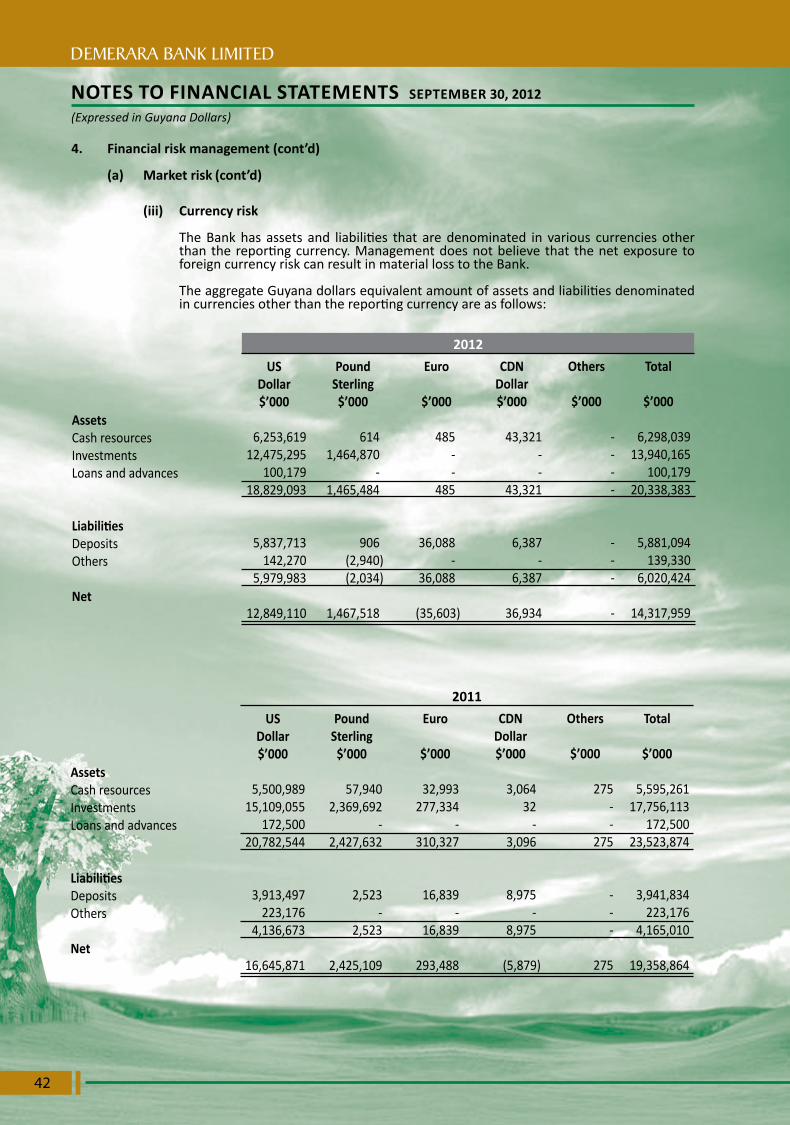

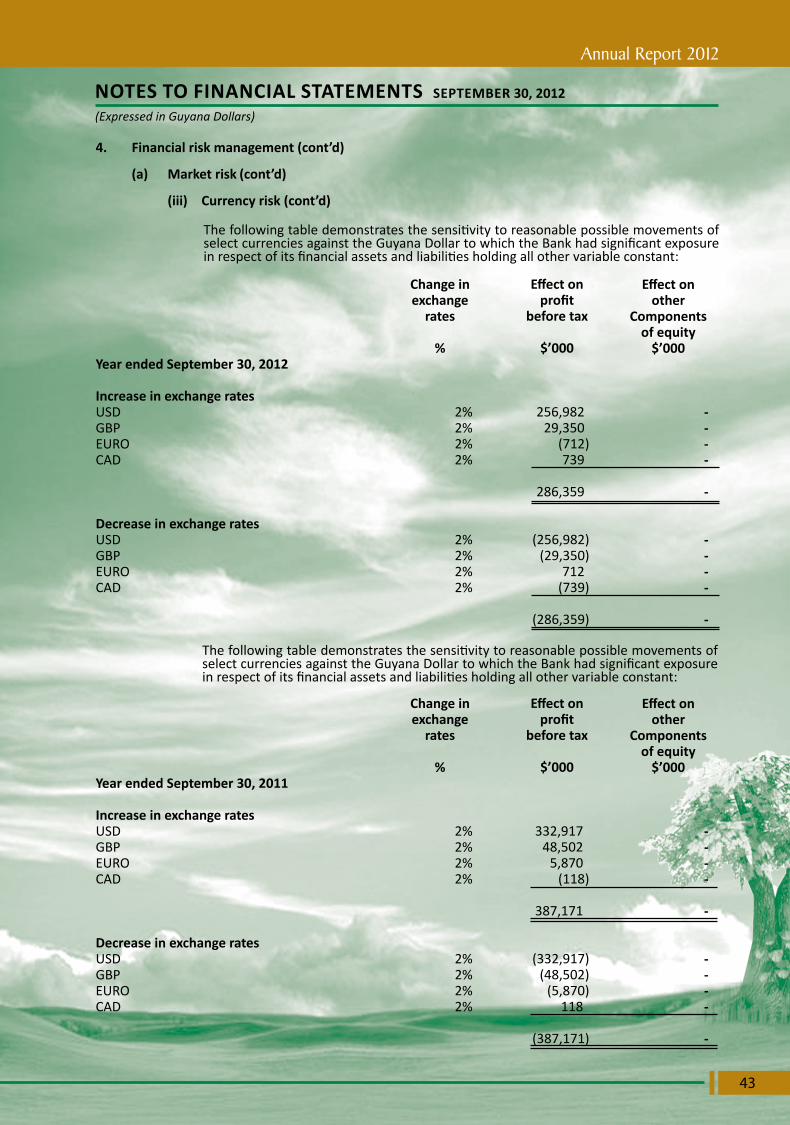

(iii) Currency risk

TheBankhas assets and liabilities that aredenominated in various currenciesotherthanthereportingcurrency.Managementdoesnotbelievethat thenetexposuretoforeigncurrencyriskcanresultinmateriallosstotheBank.

TheaggregateGuyanadollarsequivalentamountofassetsandliabilitiesdenominatedincurrenciesotherthanthereportingcurrencyareasfollows:

Total

$’000

6,298,03913,940,165

100,17920,338,383

5,881,094139,330

6,020,424

14,317,959

CDNDollar$’000

43,321--

43,321

6,387

-6,387

36,934

Euro

$’000

485 - - 485

36,088 - 36,088 (35,603)

PoundSterling$’000

6141,464,870 -1,465,484

906(2,940)(2,034)

1,467,518

US Dollar$’000

6,253,61912,475,295

100,17918,829,093

5,837,713142,270

5,979,983

12,849,110

2012

Assets CashresourcesInvestmentsLoansandadvances Liabilities DepositsOthers Net

Others

$’000

----

---

-

Total

$’000

5,595,26117,756,113

172,50023,523,874

3,941,834223,176

4,165,010

19,358,864

CDNDollar$’000

3,064 32 - 3,096

8,975 - 8,975

(5,879)

Euro

$’000

32,993277,334

-310,327

16,839-

16,839

293,488

PoundSterling$’000

57,9402,369,692

-2,427,632

2,523-

2,523

2,425,109

US Dollar$’000

5,500,98915,109,055

172,50020,782,544

3,913,497223,176

4,136,673