commentary - rutgers universityraw.rutgers.edu/docs/elliott/17the third wave breaks on the...

TRANSCRIPT

COMMENTARY

Robert K. Elliotton

The Thwd Wave Breaks on theShofe$ of Aooountnig

Information technology (IT) is changingeverjrthing. It represents a new, post-indus-trial paradigm of wealth creation that is re-placing the indxistrial paradigm and is pro-fbiindly changing the way business is done.Becavise of these changes in business, the de-cisions that management must make are verydifferent fix>m former decisions. If the purposeof accounting information is to support busi-ness dedsion-making, and management's deci-sion types are changing, thenit is natural to expect ac-counting to change — bothinternal and external ac-counting. Obviously, if busi-ness, management, and ac-counting change, accountingeducation and research mustchange: the types of studentsrecruited, the curriculum,the set of required capa-bilities of graduates, and theissues investigated.

This article begins bysummarizing the changesbeing driven by IT and theireffect on the needs for ac-coiinting information (sectionI). Then the article summa-rizes the effect of both on needs for changesin internal accounting (section II), external ac-counting, including accounting standard set-ting (section III), pubUc accounting firms (sec-tion IV), accounting education (section V), andaccounting research (section VI). As thebreadth of these issues must signal, the ob-jective is to stimulate further thought and todemonstrate that it is needed.

I. IT IS THE DRIVERAlvin ibfQer's image of the "third wave"

is a good model for considering economic

Figure 1

8000BC 1650 1955

Thr«« fundamentally differentmethods of wealth creation.

For each, a different form of ac-counting informatton is required.

changes. He notes, in his book The ThirdWave, that until about 8000 B.C., the domi-nant mode of life was foraging, fishing, hunt-ing, and herding. You caught what you ate andyou ate what you caught. But, about 10,000years ago, agriculture was developed, and be-came the first m£ijor new weali^-creating tech-nology. Agriculture had momentous implica-tions for civilization, as formerly nomadicpeople became bound to the land they were

cultivating. This led to re-quirements for defense, gov-ernment, and laws. It is ourfirst example of enormoussocial and economicchanges flowing from theintroduction of a newtechnology.

The agricultural para-digm of wealth creation wasdominant for about 10 mil-lennia, until the secondgreat wave of new technol-ogy occurred — industry —exploiting the discoverythat energy could be har-nessed to amplify humanlabor in the factory. Farmore raw material could be

converted to finished goods than with manuallabor alone. Industrialization also had hugeimplications for civilization, as the cities,where the factories were located, became moredensely populated, and marketplaces devel-oped for the exchange of increasingly special-ized products. This is otu* second example ofprofound social and economic changes flow-ing from the introduction of a new technol-ogy.

The industrial paradigm was dominant fora much shorter time, until it began to be re-placed by the third great wave of change —

62 Accounting Horizons I June 1992

the information revolution. This can be datedto the 1950s, with the invention of the tran-sistor and the installation of the first commer-cial computer (although the first computersused vacuum tubes, the happy marriage ofcomputing and semi-conductors was prompt).In the third wave, the engine that drives thesystem is not physical labor, as it is in agri-culture; not machines, as it is in industry; butinformation. As with prior waves of techno-logical change, we can expect important so-cial and economic changes, and we can alreadysee the dim outlines. These include the in-crease in economic power of those countriesthat can make the most effective use of knowl-edge-workers. They also include acceleratingthe demise of the socialist economies, whichcould only hang on during the relativelyslower rates of change in the industrial era.The information age demands the rapid ad-aptation that a free market thrives on, andthe socialist systems were too phlegmatic —govemmentally and managerially—to adapt.

These three great waves of change havecharacteristic technologies in several dimen-sions (Figure 2).

There are character-istic information tech-nologies for each wave.The IT for the first wavewas writing, which wasdeveloped to keep ac-counting records. (If yousent a camel-load of spices to Damascus, youhad to have some way of knowing that thecamel driver was not misappropriating thecargo, so you needed a bill of lading, etc.)

The IT underljdng the second wave wasmovable-type printing, which was developedby Gutenberg around 1450, although the on-set of the industrial age did not occur for sev-eral centuries thereafter. The development ofmovable type was a necessary (although notsufficient) condition for the industrial revolu-tion. For the first time, knowledge could comeout of the monastic libraries, where it hadbeen locked up in unique, handwritten books.With the invention of movable type, bookscould be mass produced. Thus, information

Technology

physical

information

accounting

1at Wave

labor

writing

single-entry

2nd Wave

machinery

printing

double-entry

Figure 2

3rd Wave

semi-conductors

computer

triple-entry(?)

could be widely diffused, permitting the de-velopment of modem science and technology.

The IT for the third wave is the digitalcomputer, making possible fast, inexpensiveinformation storage and processing. Whenharnessed to its full potential (that is, inconjunction with the associated software, databases, and telecommunications), the digitalcomputer permits vast leveraging of knowl-edge-work.

Accountability technologies also changewith the technological waves. In the firstwave, when events unfolded at the stately,annual pace of agriculture, simple account-ability concepts were sufficient. If you livedin ancient Egypt, the one thing you knew wasthat things were always the same. The suncame up every day in the east and went downevery day in the west. The Nile flooded everyyear, in the same season. For millennia, ev-ery year was identical. The idea of progresswas, to the ancient Egyptians, non-existent.If you were the Pharaoh, all you needed toknow was whether there was enough grain inthe storehouses to feed the people during the

annual flood and buildanother pyramid.When your world isthis stable and pre-dictable, you need onlya very simple account-ing technology —single-entry account-

ing; you just count your assets and obligations.When the second wave arrived, however,

single-entry accounting was not sufficient.Things began to move faster. However, double-entry bookkeeping had already been codifiedby Pacioli in 1494. This development precededthe second wave, but double-entry bookkeep-ing was a necessary (although not sufficient)condition for the industrial revolution. Indouble-entry accounting, the debits equal thecredits. The debits represent the benefits tothe company and the credits represent thesacrifices. These debits and credits provide avery convenient way of l^eping track of a largenumber of contracts in various stages of ex-ecution — committed, partially executed, and

Commentary on The Third Wave Breaks on the Shores of Accounting 63

w

w'

w"

fully-executed. A simple accounting entrycould record each stage of the contract. Thus,double-entry bookkeeping enabled an entityto keep track of a large number of contractsin various stages of execution. Abundle of con-tracts is nothing more or less than a corpora-tion, and a corporation is the vehicle requiredto aggregate the capital to build the factoriesand buy the machinery to have an industrialrevolution. Althoughdouble-entry accountingdid not cause the indus-trial revolution, it couldscarcely have occurredwithout the accountingtechnology.

It is reasonahle toassume that the thirdwave will demand a newaccountahility technology. However, it has notyet emerged. Yuji Ijiri has proposed a systemof triple-entry accounting that is original anda major step in the right direction. In thismodel, the fiirst derivative of wealth with re-spect to time is income {w'), and the secondderivative of wealth with respect to time is"thrust" or the rate of change of income {w")Figure 3 summsuizes the notation.

Putting these accounting levels in termsof the three waves of wealth creation: in thefirst wave, there was single-entry accounting— accounting at the w(or wealth) level — andthe prototypical finan-dal statement was a hal-ance sheet. In the secondwave, double-entry ac-counting permitted ar-ticulated statements ofposition and change.Change is at the w' level.The prototypical finan-cial statement for thatwave was the incomestatement, and later thefunds flow statement.

Notation

wealth (as a function of time)

To the extent it measures at the w" level,it is a step in the right direction, hut it maynot go far enough to satisfy third-wave ac-countability needs. The reason is that Ijiri'striple-entry accovmting operates on the sameindustrial-era resources and obligations as areincluded in today's financial statements,whereas the crudal assets for the post-indus-trial firm are very different assets, as dis-

cussed below. In otherwords, a model based onsecond-wave concepts ofassets, liabilities, rev-enue, and expense is notlikely to be suf&dent forthe third wave.

The three waves aresummarized in Figure

Figure 3

first derivative of wealth with respect totime (that is, income)

second derivative of wealth with respect totime (that is, the rate of change in income)

Wealth

' Agricultural era

8000 BC

but they are both at the same level of flow. Soif single entry was good for the first wave anddouble entry for the second wave, is triple en-try good for the third wave?

4. The "s" curves repre-sent the introduction, exploitation, and ma-turity of each wealth-creation paradigm. Aseach wave exhausts its potential, a new wavebegins. Each new cxirve starts a little lowerthan where the last curve left off becausethere's a cost involved in switching firom onetechnology to another, and that cost is thetechnological discontinuity as people try to getoff the old curve and onto the new. Old jobsbecome obsolete, and people scramble to re-train and seek new types of jobs. Educationalrequirements shift, economic forms change,

and, as noted above,there are large socialcosts.

\

The second period of/^ technological discon-

/Ln«.«on .ra tinuity, between the sec-/ ond and third waves, in-

cludes our entire profes-sional lifetimes. We areliving that technologicaldiscontiniiity, as peopledisplaced fix)m the sec-ond curve desperatelyseek a foothold on thethird curve. A dramatic

Figure 4

Technological Discontinuities

Time

example of this can be seen in Eastern Eu-rope, as the industrial to post-industrial shiftthat the West has had 35 years to assimilateis being crammed into a few months or years.

64 Accounting Horizons I June 1992

Just because we are in a post-industrialeconomy doesn't mean that we can forget thefirst two waves. People still like to eat (theagricultxiral wave), and they still like to drivearound in automobiles (the industrial wave).But the current distribution of the U.S. work-force leaves only two percent of the peoplegrowing food and ten percent actually mak-ing things in factories. Already over sixty per-cent of the workforce is on the third curve,made up of primary and secondary informa-tion sectors. The primary information sectorcomprises entities that are principally con-cerned with the production or use of informa-tion —for example, computer manufacturers,universities, law firms, accounting firms,publishers, and entertainment. The secondaryinformation sector comprises those parts ofnon-information businesses that produce oruse information, such as the engineering andmarketing departments in an industrial firm.Already, modem IT is pervading every aspectof our economy and changing the way we dobusiness.

IT Changes BusinessLeadership businesses — those that can

grasp the business potential of IT — use thetechnology to get closer to their customers. AsIT condenses time and space, it literally closesthe time and space gaps between customers'demands and enterprises' fulfillment. Theyuse IT to improve quality, in fact, to achieveever-improving quality. And they use technol-ogy to "demassify" their products, that is, pro-vide more differenti-ated products or ser-vices for market seg-ments or even indi-vidual customers.

The industrial erarelied upon mass pro-duction to reduceprices. Henry Ford would sell you a Model Tin the color of your choice, as long as it wasblack. Restricted choice is acceptable to cus-tomers only as long as there are no alterna-tives in the marketplace. But today, compa-nies use IT to create a much broader array of

Hierarchical Organization Structure

products. In fact, computer integrated manu-facturing (CIM) permits them to produce "one-off" products.

An example of demaasification through ITcan be seen in home entertainment. Not toolong ago, you had a choice among three net-works: NBC, CBS, and ABC. Tbday, your cablecompany provides 40 to 80 channels. More-over, your VCR expands that to a virtually infi-nite array of programming that can be verytightly tailored to your specific interests.

Yet another feature of IT'S influence is thecapacity it has provided to manage an enter-prise on a global scale — to operate every-where in a coordinated fashion.

Leadership companies use IT to createthese kinds of strategic advantage. Then com-panies not in the leadership class wake up tofind that their customers are abandoningthem, leaving them with only two choices:harness IT themselves to try to catch up tothe leaders or go broke. The followers embarkupon a frantic quest to exploit IT — to im-prove quality, decrease product and produc-tion cycle times, focus on the creation of valuefor the customers, go global themselves, andfill in the gap in their human and technologi-cal resources through such new business formsas partnering and alliances. They're forced todiscover how to make strategic use of IT.

IT Changes ManagementIn this period of technological discontinu-

ity, business managers face a set of issues dif-ferent from those faced by the managers of in-

dustrial enterprises. Wecan contrast the man-agement issues facingsecond-wave vs. third-wave enterprises.

The second-wavemanager operates anenterprise with a hier-

archical organizational structure. Within thatstructure, managers try to achieve some tar-get rate of economic activity.

The hierarchical structure appears like aninverted tree, modeled on the structure of theChurch and the military (Figure 5). The

Commentary on The Third Wave Breaks on the Shores of Accounting 65

Market-ing

Engin-eering

Manufac-turing

advantage of this structure is that a very largenumber of employees can be managed and con-trolled. For example, if each ba3s in a com-pany managed six subordinates, a nine-layerorganization could contain two million em-ployees. But with the size advantage comes adisadvantage: lack of agility.

This can be seen by altering the hierar-chical figure to enclose each of the main func-tional branches in stovepipes (Figure 6). Thesestovepipes impede the horizontal flow of in-formation and facilitate vertical flows. A typi-cal organization hassuch stovepipes as mar-keting, engineering,manufacturing, sales,accounting, and fi-nance.

The stovepiped com-pany may discern thatits competitors have abetter product and real-ize that it must adaptrapidly. So the mar-keting function figures out what basket ofcapabilities would appeal to customers. Theydeliver the requirements to the engineeringfunction, which replies that the product can'tbe designed. So the marketers and engineerstrade ideas for a while until they reach agree-ment on a product that wotdd appeal to cus-tomers and can be designed. They then takeit to the manufiu^turingfunction, which repliesthat it can't make theproduct. After consid-erable additional ex-change of messages,these three agree. Nextthe sales force viewsthe prospective prod-uct and asks how it canbe expected to sell sucha product at the pricenecessary to covercosts. Many more ex-changes later, the finance department blowsthe whistle, because there's no funding avail-able to buy the necessary manufacturingequipment. An all-too-typical result of this

Figure 6

Industry Was "Stovepiped"

CEO

The Networked Organization

type of halting behavior in the stovepiped com-pany is that American automakers require anaverage of six years to bring a new productidea to the showroom floor.

Managers of these hierarchical, second-wave companies at least have a relatively sim-ple job. They receive an endowment of re-sources when they become managers, and theyemploy those resources to convert raw mate-rials into finished goods, assiuning it's a manu-facturing company. Under Frederick Taylor'sprinciples of scientific management, managers

determined the bestway to do things, u^ingsudi tools as time-and-motion studies. The"best way" was thenlocked into the organi-zation to make sure itwould continue to dothings the best way.Control systems weredeveloped to achievethat lock-in. A scien-

tifically managed company had an optimalrate of return, an optimal rate of activity —that is, activity was conceived at the w' level.Such a system even has an optimal, non-zerorate of scrap.

But the management of a third-wave com-pany is different. There is botii a different or-ganizational struct\ire and a different set of

managerial tasks.The organization

Sales Account-ing

Finance

Figure 7

changes from the treestructure to the net-worked form of organi-zation (Figure 7). Thenetwork is enabled byIT—the technology ofwide-area networks—which permits the firmto have any two ormore people cooperateon any specific task asrequired. Messages

can fiow unimpeded in any direction. The net-worked organization rapidly forms and re-forms itself around a rapidly changing set oftasks.

66 Accounting Horizons/June 1992

lb visualize how a networked organizationoperates differently, consider Digital Equip-ment Corporation (DEC). This company hasone of the largest wide-area networks in theworld, with over 80,000employees on the net-work. Every secondyear, DEC holds thelargest single-vendortrade show in the world,called DEC World. DECbudgets over $60 mil-lion and invites morethan fifty thousandpeople to attend the show, which takes placeover a two-week period. DEC designs and pro-duces this show over the wide-area network,obviating the need for persons to be assignedto the task full-time and even the need formeetings. DEC people throughout the worldparticipate in the design and ex^ution of thisenormous project using the medium of an"electronic conference."

When companies are able to break throughthe functional stovepipes, results similar tothose in Figure 8 can be achieved. If Detroittakes six years to get a new car to market andmarket conditions change — say, as a resultof changes in oil prices or consumer prefer-ence for safety — and Honda can get a newcar to market in threeyears, it is easy to pre-dict which will end upwith increased marketshare

Organization formscan be arrayed in a two-dimensional space: sizeand adaptability (Fig-ure 9). In one comer arethe hierarchical organi-zations; they can be aslarge as necessary, butmove like sloths. Theentrepreneurial form inanother comer is much prized for its flexibil-ity and nimbleness in the marketplace; the en-trepreneur can turn the organization on adime. Unfortunately, such an organization iscondemned to remain small. In another cor-

Company

Honda

AT&T

Navistar

H-P

Super-Fast

Product

autos

phones

trucks

printers

Innovators

OUCjflOt

5 years

2 years

5 years

4.5 years

Figure 8

N»wCycl0

3 years

1 year

2.5 years

22 months

Emerging Organizational Form

•low

ner is the networked organization; IT permitsit to possess both large scale and a ^ t y . Ofcourse, the hierarchical oi^amzation form hasnot vanished; most oi^^anizations can still pro-

duce a hierarchicalorganization chart.However, if you lookat the way the orga-nization actuallyoperates, it typicallyhas many networks— formal and infor-mal — superimposedon the hierarchy. The

fully networked firm has not yet emerged, butthe direction of evolution is clear.

In addition to working in a newly emerg-ing organizational structure, third-wave man-agers face a new — and more diffictilt — setof managerial demands. Unlike the typicalsecond-wave managers, who received an en-dowment of assets to operate and turn over totheir successors unimpaired, third-wave man-agers haplessly inherit an obsolescent basketof resources. They get the keys to a local firmthat must go global, an oversized firm thatmust be downsized, an electro-mechanicalfirm that must go solid-state. One ofthe hard-est tasks is the conversion of the human re-source base from the old model (white collar-

blue collar) to the newmodel (knowledge-workers). The white-collar workers werethe brains who toldthe blue-collar work-ers (the brawn) whatto do. The accountingsystems measuredwhether the brawndid what they weretold so that they couldbe disciplined.

But the third-wave organization

seeks and thrives on change—innovation andimproving quality — and to achieve that, ev-eryone in the organization, right down to theshop floor, must participate. Those we oftenstill think of as blue-collar workers become

Figure 9

lwg«

Commentary on The Third Wave Breaks on the Shores of Amounting 67

knowledge-workers in the third-wave firm. Agasoline truck driver now drives up to thetanks and opens the valves. This is not a sec-ond-wave truck — it has an on-board com-puter that tells the driver where to go next£ind how to optimize the route. Every job isbeconung a km)wledge-work job. Consider thatshop-floor workers in a Japanese automobilefactory spend 20 percent of their time ineducational activities; management envisagesthem not as the hrawn that is just supposedto do what it is told, but as a part of the ag-gregate brainpower of the organization; theyare supposed to help figure out how to improvequality, speed production, and contrihute tocustomer satisfaction.

Moreover, it is not sufficient for manage-ment merely to change all the resources of theorganization; it must also change all the pro-duction processes. It must, for example, shrinkproduct-design and production cycles. Thiscan't be done simply by doing everything faster

("turning up the RPMs"). Management mustredesign hoth products and production pro-cesses. They must reorient the entire organi-zation &om facing inward to the product tofacing outward to the customer.

Most important, management must strivefor quality producte and services — not justgood or excellent quality, but ever-improvingquality. There is never a time when you can'tfigure out some way to improve. So quality tar-gets are adjusted upwards over time. For ex-ample, the automobile you would have con-sidered high quality in the 1930s would notrate your second glance today. Nostalgically,we like to say that cars were better in the olddays, but it is not true. In the old days, afteryou drove an automobile 50,000 miles, youjunked it. Tbday you drive it 50,000 miles andchange the oil. There has been a huge im-provement in quality, hut the job is never fin-ished.

Once a company masters fits, finishes, anddurahility, it proceeds to more abstract quali-

Figure 10Managerial Challenges

I

I

Blue collar/White ooHar

Longevity & seniority

Functional hierarchy

Scale

Knowledge mmwr |

DAHMardm Br^^^^^ Performance

Structure

| 0 S ^ Flexible

./' Control

Multinational

Mergers & acquisitions' T l f ^^''IJS

Paper -. commun

Plana

StrategicalKances

Electronic

Customersatisfaction

Coordination

>dilobal

information t e c h n o t o ^ ^ ^ Enabling

1960

Induatrial economy

1975 1980

_ Tranaltional economy

1995 2010

Informatlon/aervice economy

Period of "creative deatruction"

68 Accounting Horizons/June 1992

100%

Percent^eLate

Deliveries

10%

Target1%

ties, such as the intuitive feel of the product.At length, you begin to realize that there isnever any product or service that is so goodthat it can't be made better.

Management must create the (organizationthat is inexorably biased toward process andproduct improvement.

The kinds of chal-lenges facing manage-ment making thetransition to the thirdwave are summed upgraphically in Figure10. It depicts thosechallenges for a hypo-thetical company be-ing transformed toadapt to the post-in-dustrial era. Compa-nies would encounterthe challenges at dif-ferent times, but management would need in-formation to assess progress and make deci-sions for each of the transforming arrows.They would therefore have accounting needsdifferent firom those of second-wave manag-ers. The next section contrasts the two sets ofaccounting issues.

IL CHANGES IN BUSINESSREQUIRE CHANGES IN INTERNAL

ACCOUNTING INFORMATION

Internal accounting information is deci-sion-support information developed for usewithin the entity. In the second wave, this wasknown as "managerial accounting informa-tion," a term that conveys that the informa-tion is for the purpose of managing andcontrolling the organization. Applied to athird-wave company, the term would be im-precise, because every worker is a knowledge-worker expected to advance the interests ofthe firm. Information is intended to empowerall workers, not just managers.

Remember that the second-wave, indus-trial-era accountant is measuring assets,liabilities, income, and expense: s/he is mea-suring at the w' level. Second-wave account-

Figure 11

On-Time Customer ServiceDivisionA B

ing systems lock in the Taylor model. Theyimpound a strong assumption: there is a bestway to do things, and once it is determined,we lock it into the orgamzaticm; oi» of t l^ toolswe use to lock it in is cost aoonmtii^. For ex-ample, standard cost systems produce vari-

ances, which are sys-tematically driven tozero. In other words, wedrive the second deriva-tive (the rate of chaisein processes) to zero.Typical measurementsin a second-wave sys-tem are at the w' level— the rate of activitylevel.

Figure 11 shows atypical w' measure, thisone a quality measure.The measure is on-time

customer service, and the figure plots monthlylate deliveries for three divisions. The targetis no more than 5 percent late deliveries. Thetarget is a rate of activity that is consideredsatisfactory — at the u?' level. Division C ap-pears to be the best division because it alwaysmeets the target for on-time delivery. DivisionB appears to be the worst division because ithas never yet met the target. (We will recon-sider this analysis later when we discuss theway these results would be analyzed in athird-wave accounting system.)

Another characteristic of a second-waveaccounting system is that it focuses on tan-gible assets, that is, the assets of the indus-trial revolution. These include inventory andfixed assets: for example, coal, iron, and steamengines. And these assets are stated at cost.Accordingly, we focvis on costs, which is theproduction side, rather than the value created,which is the customer side.

Second-wave accounting has a simplifyingconvention: we originate no accounting in-formation until there is a transaction with anoutside party. Only then will information berecorded and then journalized, posted, sum-marized, and reported. In this way theaccounting is based on events and it is fo-cussed on the past.

Commentary on The Third Wave Breaks on the Shores of Accounting 69

a/c 2 4 8 9 5 3

Finally, the second-wave accovinting sys-tem maps the hierarchical organization. Thegeneral ledger coding structure is a virtualmap of the hierarchy (Figure 12). The mostsignificant digits represent the majorbranches high in theorganization chart,and the least signifi-cant digits representthe "shop-floor" activi-ties at the bottom ofthe organization chart.Ib obtain consolidatedfinancial statements,we sort on the left dig-its, and to obtain activ-ity statements, we sorton the right digits.

The account codingstructure locks the tree structure into theorganization. The organization that tries to be-come networked and tries to break throughthe stovepipes is "snapped back" to the hier-archy by the accounting structure. Even if itforms interdisciplinary task forces to solvebusiness problems and those task forces de-velop business-wide solutions, the budgetaryprocess thwarts inter&mctional cooperation.It has no way to deal ef-fectively with sharedcosts and benefits, thussuppressing cross-func-tional behavior. In effect,the account structure isa powerfully conserva-tive force trapping the or-ganization in the secondwave.

In summary, second-wave accounting systemsoperate at the w' level,consider only tangibleassets, focus inwardly onproducts, wait for eventsto occur before originating accounting entries,and lock in the hierarchical organizationalform.

Recently, I was speaking with the founderand CEO of a highly successful software com-pany. He told me that "trying to run my orga-

Figure 12

The General Ledger Maps the Hierarchy

,—subsidiary

— department

I— fur\ction

I— cost center

n

nization with the output ofoai accounting de-partment is like trying to fly an airplane thathas only one dial — a dial that shows the sumof airspeed and altitude. If it's low, Fm introuble, but I don't even know why." This view

is all too typical ofCEOs' views of thevalue of their second-wave accounting sys-tems.

Now we can contrastthis to the third-waveaccounting system. Thisnecessarily is somewhatspeculative, becausethese systems have notyet emerged. But I ven-ture the following pre-dictions about third-

typeI— activity

Figure 13

On-Time Customer Service

DivisionA B

100%

PercentageLate

Deliveries

10%

wave accounting systems.First, they will focus on changes in re-

sources and processes. Because the third-wavemanager must transform the organization —both its resources and processes — account-ing should provide measures of transforma-tion, including rates of change in resourcesand processes. In other words it must moveup from the w and u;' levels to the u;' and ly"

levels. It must re-pudiate the Taylormodel, which sup-presses all change,including improve-ment. In a third-wave accounting sys-tem, the typical mea-surement would beat the I/;" level.

We saw (in Fig-ure 11) a u;' measureof on-time customerservice. Figure 13 de-picts the same com-pany with the same

data. This figure is the same as the one aboveexcept that the 5 percent target for late deliv-eries is gone. Instead, the time required foreach division to cut its rate of fiEiilure in halfis computed (the half-life in months). The newtarget is to minimize the half-life. On the ba-

9 5Half-Life in Months

60

70 Accounting Horizons/June 1992

sis of this new target, division B appears tobe the best (rather than worst) division, anddivision C appears to be the worst (rather thanbest). With the same company and the samedata, the u;" (or third-wave) view yieldsquite a different pic-ture than the w' (orsecond-wave) view.

Businesses are be-ginning to generateinternal informationat the w " level. More-over, they are begin-ning to write contracts on this basis as well.The second-wave procurement contract de-mands a defect rate of less than x parts perthousand. The third-wave procurement con-tract demands a defect rate of less than x partsper 1,000 this quarter, x parts per 10,000 nextquarter, and x parts per 100,0(X) the follow-ing quarter.

The resources and obligations measuredin a third-wave accounting system must alsochange. The resources that drive the third-wave company are information-based assets,such as R&D, human assets, knowledge, data,and capacity for innovation. These assets don'teven appear on second-wave balance sheets.We cannot leave themout of the account-ability set and expectmanagers and inves-tors to reach sound de-

Company

GE

Motorola

H-P

Brunswick

Super-Fast Producers

Product

circuit breai^ers

pagers

testers

fishing reels

OMCych

3 weeks

3 weeks

4 weeks

3 weeks

Figure 14

NuwCyeh

3 days

2 hours

5 days

1 week

asions.Because the third-

wave organization is fo-cussed outward on cus-tomers, its accountingsystem must be con-cerned with measuringthe values created forcustomers.

The third-wave ac-counting system must enable the networkrather than lock in the hierarchy.

Finally, the third-wave accounting systemmust provide real-time dials on the businessrather than waiting for events to occur beforerecording them, thus providing only a retro-

Comparison of 2ncl and 3rdWave Accounting Systems

Industrial 0ra

resources (w) and rates of change in resourcesprocesses (w') (w') and processes (w")

tangibles

products

events

maps hierarchy

spective look at the enterprise. As a practicalmatter, more and m(u% businesses, throughuse (^computer integrated manufacturing, re-semble continuous-process activities. It is in-

creasingly unusual tosee work-in-process sit-ting ax the shop floor forweeks and months.What we see is com-pletely redesigned pro-duction processes thatminimize the non-value-added time.

Figure 14 illustratesthe order-of-magnitude improvements pos-sible with process redesign through IT. Theproduction cycle times represent the elapsedtime from order to finished goods, ^ t h suchvirtually continuous processes, it is possibleto think about "process-dials" in real time onthe business.

As noted, this third-wave accounting sys-tem is a set of predictions, because there aren'tany such systems yet. But these predictions(see Figure 15) embody a focus shift from thew and w' levels to the w' and w " levels, fromtangibles to intangibles, from products to cus-tomers, from events to real-time dials on theprocesses, and from mailing the hierarchy to

enabling the network.We can take these

speculations further byfociising on the kinds ofinformation man-agement actually usesto run the business, in-stead of on the catego-ries of traditional ac-counting.

At the highest stra-tegic level, running thebusiness means deter-mining the "indus-try (ies)" in which the

company wants to participate and thefundamental approach to succeeding in theindustry(ies) the company already par-ticipates in. However, the information neededfor such purposes is broader than what ac-counting systems can systematically collect

Figure 15

Mormatkm era

intangibles

customers

processes

enables network

Commentary on The Third Wave Breaks on the Shores of Accounting 71

and generate. For example, strategic think-ing at this level involves considering social,technological, and political trends, and no ac-counting s^tem is likely to be designed to dothat. Ib get a better fix on what kind of infor-mation might be feasible to include, we canuse Michael Porter's model of the elements ofindustry structure (see Figure 23). Accordingto the model, the key elements are (1) thethreat of new entrants, (2) the threat of substi-tutes, (3) bargaining power vs. suppliers, (4)bargaining power vs. customers, and (5) theintensity of rivalry of the present competitors.

No accovmting system is likely to reportsystematically on the threats of substituteproducts and new competitors entering themarket, even though such information wouldbe helpful whenever it was obtained. However,there is a lot of relevant information in thethree remaining categories that can be col-lected and reported systematically to assistmanagement in its strategic and tactical deci-sion making. Selected examples of such in-formation are presented below for each indiis-try in which the company has a strategic busi-ness unit ("SBU"):

Competitive position ofSBU (forcompany and its principal competitors)• Percent of sales from products developed

in lasix months (excluding product-line ex-tensions).

• Average time to bring a new product ideato the marketplace.

• Market's perception of quality of productsvs. competition.

• Market's perception of quality of servicevs. competition.

Bargaining power vs. customers• Percent (number) of customers accounting

for c percent of total sales.• Customers' industry concentration.Bargaining power vs. suppliers• Percent (number) of suppliers accounting

for X percent of total purchases.• Suppliers' industry concentration.

The sources of these types of data vary byindustry and may include public data bases.

competitor intelligence systems, and thecompany's own transaddcm systems. Each typewould be useful, but customer data is perhapsthe most important for a third-wave company.Without a focus on the customer, a companyhas little chance of success in the third-waveeconomy. For this reason, we shall explore theissue of accounting for customer satisfactionmore closely.

Bargaining Power vs. Customers

Customer satisfaction is closely related tocustomers' perceptions of the quality of prod-ucts and services they receive firom a vendor.There may be as many definitions of qualityas there are customers. But, in general, thecloser the fit between customer desires andproduct attributes, the higher the customeris likely to assess quality. An apparently highquality product (measiired, say, by fit, finish,and durability) that poorly fulfills the cus-tomer's desires is not likely to be rated as highquality.

Customers' standards for judging qualityare not fixed, but change over time. Many pro-ducts considered high quality fifty years agowouldn't rate second glances in today's mar-ketplace, because standards have risen —spectacularly for some products: think of air-planes, stereos, and business equipment. Inother areas, standards haven't changed asmuch: a good loaf of bread fifty years agowould still be a good loaf of bread today.

The fact that perceptions of quality changeover time suggests that quality is a relativeconcept. There's no measure that objectivelystates the quality of a product or service forall time. All we can say is that consumers cancompare the quality of two products or ser-vices and say which is better quality. Similarly,a consumer could consider a particular prod-uct or service and specify what would make ithigher quality. For these reasons, surveys ofcustomers' perceptions of quality are irreplace-able. Nevertheless, data on the characteris-tics of products that lead to customer satis-faction are just as important, ^thout this linkto the design and productive processes, therewould be no path to improvement.

72 Accounting Horizons/June 1992

Other factors equal, consumers wouldprobably rate a product higher in quality if it:• had more utility,• were cheaper, or• were available sooner.

Each of these would have to be studiedclosely. For example, if we could read the cus-tomer's mind, we might find that:• utility encompasses durability, reliability,

performance, and maintainability,• cost includes not only purchase cost, but

total life-cycle cost of ownership, and• timeliness embraces shorter product de-

sign and manufacturing cycles and evenan element of innovation (the innovatorhaving more timely products than thereplicator).Some of these components are monitored

today by most manufactoirers (for example,cost, outgoing quality levels, and on-time de-liveries), though often the customer's defini-tions of acceptable quality and on-time deliv-ery differ Grom the company's. Other indicatorsof quality can be teased out of information al-ready contained in, or easily added to, accovint-ing records. The computing capacity inexpen-sively available today permits far more thor-ough analysis of accounting data to infer keycomponents of customer satisfaction. Forexample:• Durability. If sales documentation were ex-

panded to include the age of imits beingreplaced, measures of durability imder ac-tual customer conditions could be devel-oped.

• Reliability. Analysis of parts and servicerecords could yield up-time ratios andmean-time-to-failure figures under actualuse conditions.

• Performance. Customer reorder rates andtrends would indicate satisfaction withperformance.

• Innovation. Percentage of revenue fromproducts that did not exist two years agowould indicate the level and trend of inno-vation. (The ability to sell new products tocustomers is a more valid measure of inno-

vation than, say, the number of patents ob-tained.)

• Product-design cycle. Elapsed time fromproduct conception to firat commercialsale. For longer-term projects, milestonescan be tracked.

* Manufacturing cycle. Elapsed time fi*omraw materials to finished goods. A closerelative is the ratio of work-in-process in-ventory to sales.Technology will open more possibilities for

the future. For example, when caller identi-fication becomes available, the information ina company's telephone switch (which is, afterall, just a part of the company's computer sys-tem) will permit monitoring of customer-satisfaction issues from call patterns. A burstof calls from customers' maintenance shops tothe company's engineering department couldsignal deteriorating maintainability. A re-ciprocal burst could signify that engineerswere not able to diagnose problems in realtime, but had to investigate and call back later.

Reconceiving the ExchangeTransaction

Even though most of the information onquality discussed above is "nontraditional" inaccounting systems, it could be processed firomdata in today's records. However, the im-portance of information on customer interac-tions suggests that basic exchange account-ing could be rethought in order to capturemore of that kind of information.

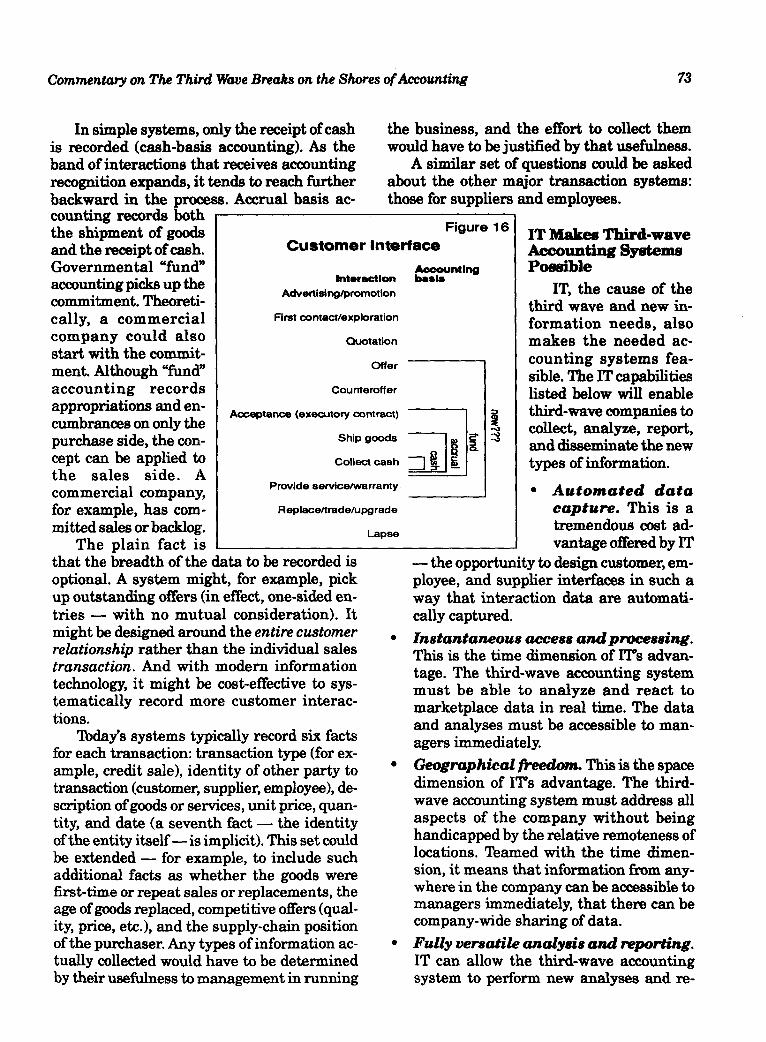

As I have noted, the traditional system isbased on initiating accounting informationonly when events are transacted with outsideparties. This has obvious virtue. Companieswill always need to keep track of transactionswith customers, suppliers, and employees;otherwise, they wouldn't know the status oftheir many outstanding rights and dbligations.Nevertheless, events with (mtside parties thatare recorded under the traditional accountingmodel are only a segment in a series of inter-actions, and those other interactions arepotentially useful in evaluating customer sat-isfaction. The interactions are depicted morefully in Figure 16.

Commentary on The Third Wave Breaks on the Shores of Accounting 73

In simple systems, only the receipt of cashis recorded (cash-basis accounting). As theband of interactions that receives accountingrecognition expands, it tends to reach furtherbackward in the process. Accrual basis ac-counting records boththe shipment of goodsand the receipt of cash.Governmental "fund"accoimting picks up thecommitment. Theoreti-cally, a commercialcompany could alsostart with the commit-ment. Although "fund"accounting recordsappropriations and en-cumbrances on only thepurchase side, the con-cept can be applied tothe sales side. Acommercial company,for example, has com-mitted sales or backlog.

The plain fact is

the business, and the effort to collect themwould have to be justified by that usefulness.

A similar set of questions could be askedabout the other m^or transaction systems:those for suppliers and employees.

Figure 16Customer interface

taitoraetion

Advertising^omotion

First contact/expioration

Quotation

Offer

Courtteroffer

Acceptance (executory contract)

Ship goods

Collect cash |

Provide service/warranty

Repiace/trade/upgrade

Lapse

Accountingbaste

IT Makes Third-waveAccountiiig SystemsPossible

IT, the cause of thethird wave and new in-formation needs, alsomakes the needed ac-counting systems fea-sible. The IT capabilitieslisted below will enablethird-wave companies tocollect, analyze, report,and disseminate the newtypes of information.

that the breadth of the data to be recorded isoptional. A system might, for example, pickup outstanding offers (in effect, one-sided en-tries — with no mutual consideration). Itmight be designed around the eritire customerrelationship rather than the individual salestransaction. And with modem informationtechnology, it might be cost-effective to sys-tematically record more customer interac-tions.

Tbday's systems typically record six factsfor each transaction: transaction type (for ex-ample, credit sale), identity of other party totransaction (customer, supplier, employee), de-scription of goods or services, unit price, quan-tity, and date (a seventh fact — the identityof the entity itself— is implicit). This set couldbe extended — for example, to include suchadditional facts as whether the goods werefirst-time or repeat sales or replacements, theage of goods replaced, competitive offers (qual-ity, price, etc.), and the supply-chain positionof the purchaser. Any types of information ac-tually collected would have to be determinedby tiieir usefulness to management in running

• Automated datacapture. This is atremendous cost ad-vantage offered by IT

— the opportunity to design customer, em-ployee, and suppKer interfaces in such away that interaction data are automati-cally captured.Instantaneous access and processing.This is the time dimension of IT's advan-tage. The third-wave accounting systemmust be able to analyze and react tomarketplace data in real time. The dataand analyses must be accessible to man-agers immediately.Geographical freedom. This is the spacedimension of IT's advantage. The third-wave accounting system must address allaspects of the company without beinghandicapped by the relative remoteness oflocations. Teamed with the time dimen-sion, it means that information from any-where in the company can be accessible tomanagers immediately, that there can becompany-wide sharing of data.Fully versatile analysis cutd reporting.IT can allow the third-wave accountingsystem to perform new analyses and re-

74 Accounting Horizons/June 1992

port in new formats as needed. The man-ager of the third-wave company must beable to have data reported in the mannerdesired, even if the report has never beendemanded before.

* Capacity for additional data types. ITcan allow the manager to add new infor-mation types to the accounting systemwithout redesigning its entire structureand while retaining the other advantagesalready described.

• Acce88 to external data bases. IT canallow the third-wave accounting system totap external data bases. Much of the in-formation needed for the third-wave ac-counting system is about competitors andother marketplace features. Such informa-tion would be available from public databases and could be marshalled on demandfor managers.The characteristics just described are

those of the wide area network and the rela-tional data base.

A wide area network is more than a set ofwires. It is also the intelligence (embedded insoftware) to navigate through the network tofind and take adv£uitage of information. Infor-mation does not exist in a vacuum — it WEIScreated by someone. So the ability to find in-formation is also the ability to find expertise— the person who created the information.This is a crucial aspect of the nimble, adap-tive company, opening the way for productiveinteractions as well as additional sharing.Some have concluded that the key resource ofthe modern enterprise is its aggregatebrainpower, but that this is useless \inless itcan be marshalled on demand. The wide areanetwork is essential to finding and marshal-ling corporate brainpower.

The relationsil data base concept providesthat data can be added along any dimension.New t3rpes of data — for example, informa-tion about suppliers, ctistomers, and competi-tors — can be added to existing systems with-out altering existing uses and functions. Oncethe new data are added and their relationshipsto the existing data are specified, they can beused with the old data types to create newt j ^ s of reports and analyses.

These reports and analyses are not lim-ited. The same relational data base can be"viewed" firom many angles. The traditionalangles (or Views") are personnel, sales, credit,production, etc. However, it is also possible toadopt the following angles (assuming only thatrelevant data have been captured): strategicplanner, market analyst, customer, supplier,and competitor.

The wide area network is extensible. It isnot bounded by the struct\ire of the organiza-tion. For example, it can connect to public databases, to customers, and to suppliers. Thesesources can supply much of the external in-formation discussed above. They can also re-ceive information firom the company. Manage-ment can permit suppliers and customers re-stricted views into the company. One form ofthis sharing is EDI — electronic data inter-change.

Many companies have wide area networksand relational data bases, but are not full-fledged third-wave companies. The technolo-gies are necessary but not sufficient in them-selves to create a third-wave accounting sys-tem. The systems must be designed to servethe company's needs, must reflect thecompany's vision and managerial strategy, andmust be integral to its structure, style, andpurpose. Then the capabilities must be man-aged effectively, prompting behavioral changesamong personnel that harness the technolo-gies for competitive advantage.

III. CHANGES IN BUSINESS ANDNEW ACCOUNTING NEEDS

REQUIRE CHANGES IN EXTERNALACCOUNTING

like "management accounting," "financialaccounting" is a second-wave term. It limitsthe reporting entity's accountability to finan-cial information, and third-wave entities haveexternal accountabilities that go beyond finan-cial information. These accountabilities repre-sent accounting needs that call in question theefficacy of GAAP.

Much of what users want to know aboutthe company is nonfinandal. The same rea-soning makes "financial" a constraint that lim-its the usefulness of GAAP. For example, us-

Commentary on The Third Wave Breaks on the Shores ofAccounting 75

ers want to know the company's mission andgoals, its strategy, the industries ia which thecompany participates, the competitive positionof the company within those indiistries, therelative levels of quality and customer satis-faction of the company and its competitors,progress in product-design and productioncycle-time reduction and productivity, and de-velopment of the company's human assets.None of these can easily be reduced to fi-nancial numbers.

Besides being limited by the concept of fi-nancial information, today's GAAP present ia-vestors with periodic, historical, cost-basisstatements. Each of the four italicized wordsrepresents an additional second-wave limita-tion on external reporting.

Periodic financial statements follow theannual agricultiiral (first wave!) cycle, laterexpanded to quarterly in the United States(but not eversrwhere). However, the volatilityof today's markets suggests that more fi^quentreporting of some sort would be beneficial, andIT permits it.

GAAFs insistence on historical informa-tion is another limitation. We know that us-ers wish to estimate the magnitude, timing,and uncertainty o{future cash flows, and theFASB's concepts statements recognize it. Inaddition, the third wave increases the speedof change to such an extent that straight-lineextrapolations from the past are no longergood predictors of the future. This conditionand users' purposes suggest that forecastinformation should be supplied.

GAAP also favors cost-basis information,despite the fact that assets and liabilities aresubject to increasingly rapid shifts in value.The call for mark-to-market accounting for fi-nancial entities is evidence ofthe strain third-wave economics has put on GAAP.

And finally, GAAP presents information instatements — physical aggregations of datapresented in a standardized form on paper —whereas IT opens the possibility of present-ing data in different forms. IT makes possiblethe real-time release of salient facts as theyoccur. IT also makes it possible to deliver ana-lytical models over wide-area networks. Forexample, instead of (or in addition to) present-

ing physical external statements to investors,users might log onto the company's system andmanipulate the companjr's spreadsheet to ana-lyze and reanalyze the company's data alongdimensions different from those reported orchange management's assumptions andreanalyze the data.

GAAP has several ofthe limitations of tra-ditional internal accounting. It focuses ontransaction-based financial information, looksinward at the product instead of outward atthe customer, and measiires at the resourcesand process levels {w and w') instead of thechanges in resources and changes in processeslevels iw' and w"). It favors tangible assetswith balance-sheet expression, while disfa-voring intangible assets (such as human as-sets, information assets, and R&D) by treat-ing them as expenses.

Discounting even half of the limitationscited in this section, the case for a reconsidera-tion of GAAP is still powerful. But the FASBis not free simply to figure out a better GAAPmodel and impose it. The Board works in apolitical environment. Its pronouncementsaffect the creation and distribution of wealth,and those affected naturally lobby for theirinterests. Kenneth Arrow taught that for mak-ing decisions that affect people's welfare, thereis no "scientific" method that is both rationaland fair — that the only alternative is politi-cal.

The FASB, then, is qtiite properly a quasi-political body, constituted to consider the de-sires of the parties with a stake in the out-come when fulfilling its mission — and theyare diverse constituencies that seldom agree.One ofthe few things that finandal statementpreparers agree upon is that the scoring rulesshould not be changed in the middle of thegame. Thus there is a powerful constituencyin favor of the status quo. Add the attesters— who are dissuaded from change by un-known, but probably unbearable, legal liabili-ties — and you have an implacably conser-vative environment. The same managementsthat complain that they can't run the businesswith today's accounting information are theones who make pilgrimages to Norwalk tolobby against changes.

76 Accounting Horizons I June 1992

The academician's natural retort is, "OK,we can't change external accounting. But wecan change internal accounting, because it canbe anything management wants it to be in or-der to run their business. So, that's where ourtarget should be."

There are three problems with this an-swer: (1) the impediments to change withinthe company are far greater than commonlyrecognized, (2) there are serious risks if wepermit internal and external accounting todiverge, and (3) the decisions of investors andmanagers are fundamentally similar.

In the first place, every entity has its ownmicrocosm of the political misalignment thatprevents consensus for change at the GAAPlevel. In all likelihood, the internal loserswould be the advantaged constituencies —those with the highest propensity and stron-gest clout to resist change — for example,functional vice presidents, who lose powerwhen stovepipes are abolished. Thus the po-litical drama played out in public in Norwalkis played out in private in numerous corpo-rate offices.

In the second place, we run a big risk ifwe permit internal and external aax)untingto get out of sync with each other. If they mea-sxire conceptually diflFerent outcomes, a ten-sion will arise between internal and externalaccounting that may lead man-agement to do things that theyknow are sub-optimal. For ex-ample, in a bad quarter, theymay be motivated to window-dress the external accounts bydoing things that they know notto be rational from a managerialstandpoint — like firing people,the third-wave human assets, who may bemore important to future success than rela-tively obsolete plant and equipment. It is of-ten stated that American managers sufferfrom a short-term orientation caused, presum-ably, by quarterly reporting. However, theproblem is not quarterly reporting, it is thedifference between external accounting andeconomic reality (ideally reflected in internalaccounting) that gives rise to such acts. IfGAAP were a good model of economic success,

Figure 17

A Simple Exchange

Seller

Goods

MoneyBuyer

there woiild be no harm in managers tryingto maximize alcmg a GAAP measurement scaleas often as possible. 'The problem is tiiat GAAPis not a good measurement of the creation ofreal values. Ib avoid the creation of motiva-tions for uneconomic behavior, external andinternal accounting systems (mght to be "con-sistent." Consistent, in this sense, permitsdifferent 'Views," but into the same underlyingreality.

An analogy: If you're in New York andwant to go to Bostm, you need a map. Thetype of map depends on how you're going toget there. For hiking, you need a top<^^phi-cal map so you can avoid mountains. For driv-ing, you need a road map. For going by boat,you need a marine navigation map. For fiy-ing, you need a map that shows the locationsof t£dl buildings, and so forth. Though each ofthose views is different, depending on the useto which it is put, the underlying reality isconsistent: New York and Boston remain thesame distance from each other, the same di-rection, and so forth. In the same sense, busi-ness requires consistency between the exter-nal and internal accounting systems.

In the third place, the tasks of investorsand managers are essentially similar, thoughperformed at different levels. Each is inter-ested in selecting among competing invest-

ment alternatives so as to maxi-mize the present value of futurecash flows. Accordingly, the deci-sion information used by eachmay be different in degree of de-tail (fineness) but should be, asnoted above, "consistent."

If standard setters are tobreak out of the second-wave

paradigm, they will have to think of new mod-els that are not grounded on the simple trans-action. The typical second-wave transactionis depicted in Figure 17, which shows the ex-change of goods (or services) for money (or apromise to pay money in the very near future).

The current GAAP model impounds thefollowing assumptions:• Nothing accountable happens until there

is an exchange.• Exchanges are bargained at arm's length.

Commentary on The Third Wave Breaks on the Shores of Accounting 77

• Exchanges are simple (cash for goods orservices).

• One side of each exchange is cash virtu-ally now.It is the simple equivalence of the values

of the cash (or virtual cash) and noncash com-ponents of tile simple exchange, bargained atarm's length, that makes double-entry book-keeping work.

However, IT permits personsdoing business to engage inmuch more elaborate exchangesand keep track of them. Figure18 shows a more complex(though not the most complexpossible) exchange that invali-dates an assumption vmderljdngGAAP accounting, because thereis no way to allocate the value of"money now" (the only directlymeasuirable component of the ex-change) to the five noncash com-

Figure 18

A Complex ExchangeGoocto

Seller

IV. CHANGES IN BUSINESS ANDNEW ACCOUNTING NEEDS

REQUIRE CHANGES IN PUBLICACCOUNTING FIRMS

Public accounting firms have not adjustedto the third wave. The biggest challenge theyface is that a very laige part of their practices is

tied—loosely or ti^tly—to his-torical cost-basis finaiidal state-ments that are losing their util-ity. Most accounting, auditing,and tax work and perhaps half ofconsulting work is related to his-torical cost-basis financial state-ments or accounting systems. Yet,imlike other enterprises whoseproduct is dediningin utility, pub-lic accoimting firms cannot unilat-erally redesign the product, be-cause GAAP and tax laws are de-termined externally.

Buyer

ponents of the exchange. GAAP must come toterms with this more complex world if it is toretain its relevance.

Following are some implications for stan-dard setters entering the third wave. Theyshould:• Study the behavior of users, not just their

stated preferences or their comments onGAAP. If they use non-GAAP informationin attempting to predict future cash flows,assume it is useful.

• Study IT era internal information needs.• Focus on third-wave value drivers (infor-

mation-based assets andpeople).

• Focus on continuous ratherthan periodic informationflows.

• Focus on measurementsthat signal change in therate of change (that is, w ").

• Provide continuing service(consultation, education,software) to constituencies.

• Educate managements and users as to thethird-wave accounting paradigm.

Account-ing andauditing

Tax

CPA firms are also organized the way sec-ond-wave entities are organized. They are"stovepiped," as depicted in Figure 19, insteadof networked, divided instead of teamed Tlieymust break through these stovepipes in orderto better serve their cHents.

CPA firms have two separate, though re-lated, product lines: attest services and consult-ing services (which, broadly defined, subsumetax services). Each of these will be dealt with inturn.

The third wave creates two separate oppor-timities for attest service: it produces vast newstreams of information that demand attestation,

and it provides the means to au-tomate much of the attest process.

Historically, CPAs have at-tested to finandal statements, butthese statements contain a declin-ing share of the information usedby investors. In a survey I didabout ten years ago, I alreadyfound more than 400 examples ofattestation to information otherthan the financial statements.These included attestatioQ to fore-

casts, projections, feasibility studies, EDP soft-ware, internal controls, utility rate applica-

Figure 19

CPA Firms are"Stovepiped"

CEO

Manage-Tient con-

suiting

78 Accounting Horizons / June 1992

revenue -- costs —

a

Firm infrastructure

Human resource

Procuremsnt

Inboundlogistks

Opera-tions

Out-boundlogistics

tions, contract costs (cost-plus-fixed-fee con-tracts), regulatory filings, lease contingencies,royalties (coal, oil, motion pictures, etc.), com-pliance with regulations, occupancy statistics,enrollment statistics, attendance statistics,political contributions, labor negotiationsdata, third-party reimbursement claims, andmany others. The more new data streams, themore attestation opportunities arise.

The development ofnew data streamsmust be seen in termsof the conditions foreconomic demand forattestation services.Whenever (1) usersneed the information,(2) there is a conflict ofinterest between thepreparer and the userof the information, (3)the information is"auditable," and (4)there is a favorablecost-benefit ratio forattestation, the condi-tions for economic demand of attest servicesare in place. Taken together with the newstreams of information being generated, theopportunities are promising.

At the same time these opportunities aredeveloping, IT ischanging the produc-tion technology of au-diting, providing moreefficient and differentmeans of attestation.These include moreand cheaper comput-ing power, wide-areanetworks, and theemergence of "intelli-gent" software. In com-bination, these re-sources permit rede-signing the audit topiggy-back the cUent's systems in real time,producing attestation on demand.

Now we turn to the nonattest services ofCPA firms. It is helpful to consider these ser-

Generic Value ArrowFigure 20

Technology develcpinent

Market-ing & sales Service

Primary activities

CPA Firm Value Arrow

(0.2%

Firm Infrastructure

Human resource management

Techmlogy support

Administrative support

Recruit andmanage

personnel

Productdevelop-

ment

Practicedevelop-

mant

Primary activities

vices by appljdng Michael Porter's value-chainanalysis.

In value-chain analysis, all the activitiesof the firm are mapped into a value arrow (seeFigure 20). The overall length of the arrowrepresents total value created by the organi-zation: in a competitive market, that is whatcustomers are willing to pay — that is, rev-

enue. In order to createthose values, costs areincurred, which isrepresented by theshorter (unshaded)length of the arrow.The difference betweenrevenue and cost (theshaded area) is mar-gin. In order to in-crease margin, the en-terprise can, for exam-ple, increase value tocustomers or decreasecosts. The activities ofthe firm are mappedinto the various cells inthe arrow, repre-

senting two basic groups: those that createvalue for customers (primary activities) andthose that don't, but are required in order tosustain the entity (supporting activities).Gienerically, the primary activities aire inbound

logristics, operations,outbound logistics,marketing and sales,and continmng service.For Ford, operations isbuilding the car. Butbuilding and deliveringit are not enough: Fordmust help the customerkeep the car on the road— continmng service.

A value arrow foran accounting firm isdepicted in Figure 21. Ifaccovinting firms are to

prosper, they must make their clients betteroff. They cannot make their clients better offthrough selling them raw materials at lowerprices or lending them money at lower rates.

Source: Michael Porter

Figure 21

Performservice

Continuingciient

servioe

Commentary on The Third Wave Breaks on the Shores of Accounting 79

So how can CPA firms make their clients bet-ter off? What is their special value to clients?What can they do for clients swimming inpools of new information? One formulation isthat CPAs can attempt to make their clientsbetter off through the use of information andinformation systems. This is because clientsare all interested in the strategic use of thegrowing sources of infoirmation available tothem, and CPAs are information specialists.

Figure 22 shows the CPA firm as one ofthe client's suppliers. The CPA firm's goal isto make its clients better off— to maximizetotal value along the value chain. The way todo that is to help the client make its custom-ers better off.

Figure 22

CPA Firm Value Chain

CPA Firm

SuppNar Client

If we look at the traditional products ofCPA firms — audits and tax compliance, wesee that they are directed to the support activi-ties of client firms (the upper arrow from theCPA firm to the client in Figure 22). Theseservices provide value by lowering the cost ofcapital and by minimizing tax expense. Nev-ertheless, these services are not directed atthe dients'primary value-adding activities. Inorder for the CPA firm to flourish, it must fo-cus on services directed to the strategic use ofinformation to facilitate the primary value-adding functions in its clients' organizations.

First steps necessary to achieve this in-clude the following:• Develop a fundamental understanding of

the strategic value of information systems.

• Understand how the client's primaryvalue-adding activities create value.

• Figure out how the client csui create morevalue through the use of information andinformation systems.

• Identify, coordinate, and develop the re-sources in the firm to make it happen.Only then are CPA firms likely to flourish

in the long term.

V. CHANGES IN BUSINESS ANDNEW ACCOUNTING NEEDSREQUIRE CHANGES IN

ACCOUNTING EDUCATIONThe changes discussed to this point have

important implicationsfor education. Graduatesare no longer enteringsecond-wave companies.Even those companiesthat appear to be proto-typical industrial compa-nies are in the process oftransformation. They arebecoming richer in theuse of information andIT. In many cases, eventheir products containmore information; for ex-ample, today's Ford con-tains thirteen computers(to manage lighting,

carburetion, braking, entertainment, etc.).Graduates need to be able to function in theseemei ging third-wave companies, and the cur-riculum must be changed to give them the ca-pabilities.

The American Accounting Association rec-ognized many of these needs in its Bedford Re-port (1986). Although the report focused onchanges in the profession and what was nec-essary to prepare students to function in the newprofessional environment, it also recognized thatthe challenge to the capabilities of graduatingaccountants derived fiiom econcnnic change: "Theaccounting profession...is in a state of fiux, re-flecting massive changes taking place in tech-nology and social values, and in social, govern-ment, and business institutions."

Cuatonwr

80 Accounting Horizons/June 1992

The Bedford report rightly held that "Thefiindamental challenge to accounting educa-tors...is how to identify an appropriate balancehetween a broad fundamental education anda suffident accounting education in spedalfields." Breadth meant strengthening the gen-eral-education component of students' expe-rience and revising accounting a)urses to treatthe disdpline as an information developmentand distribution function for economic ded-sion making.

A similar stance was taken by the leadersof the largest accounting firms in a signed pa-per issued in 1989 (Perspectives on Education:Capabilities for Success in the Accounting Pro-fession). The paper called for educationalbreadth and stressed the need for students todevelop analytical and conceptual thinkingabout accounting as opposed to memorizingthe voluminous and rapidly expanding rulesaccountants must apply in their everydaywork.

Considering the prindple of comparativeadvantage, higher education clearly can dobetter than employers at general education:for example, communications, language,analytical abilities, economics, and quantita-tive methods. But prac-tice firms are at nodisadvantage withtechnical content: forexample, computer au-diting, statistical sam-pling, and FASB 96. Tomaximize comparativeadvantage, employerslook to colleges andimiversities to deliverthe components of gen-eral education.

The new curricu-lum must integrate technology. Merely givingstudents PCs and having them learn word-processor and spread-sheet programs is insuf-fident to prepare them to enter third-wavecompanies. They need to learn how orga-nizations can enhance the value they deliverto customers through networking. They needthe experience of participating in a network.

The new curriculum should also be ori-

Elemertts of Industry Structure

InduXryconpetHorso

Intensityof rivalry

ented to give students an appredation andsome understanding of the various aspects ofglobalism. Accreditation standards alreadymention an "international" reqixirament, buttoo often this has been satisfied with an op-tional half-course in intematiimal accounting.That approach cannot, for example, allow thestudent to appredate the ways in which ev-ery business today faces global issues. Everyenterprise, no matter how local it appears tobe — even if it appears to be bolted to theground in Oklahoma with all of its customerswithin five miles — is affected by nonlocalevents and conditions. We can pursue thisbriefly by positing the Tulsa General Hospi-tal and asking whether its claim to beingstrictly local is valid.

First let's look at the organization in thecontext of Michael Porter's "S-box" analysis ofthe competitive situation (Figure 23). Considerthe suppliers: the medical imaging and diag-nostic hardware comes from Germany andSweden, and the new resiiknts come fromSaudi Arabia, Pakistan, and India. Even if thecustomers are local, whether that customerbase stays put in Tulsa is profoundly affectedby what happens to the world price of oil,

which is largely deter-mined in the MiddleEast. Hien there's thethreat of new competi-tion — say a large,multi-national healtii-care organization thatenters the TVilsa marketor simply buys thel^ilsa General Hospital.And finally, there's thethreat of product substi-tution, as, for example,new medical and surgi-

cal equipment—invented overseas—changesin-patient services to out-patient proceduresthat can be performed in doctors' offices.

To get across the message that all enter-prises face global issues, a global perspectiveshould be built into all elements of the cur-riculum. To package that perspective in a half-course in international accounting is to un-derstate its pervasiveness.

Figure 23

Source:Michael Porter

Commentary on The Third Wave Breaks on the Shores of Accounting 81

Finally, since the renovated curriculummust prepare graduates to enter third-wavecompanies, it must teach an accoimting modelsuitable to third-wave circumstances. This isa demanding chal-lenge, but the need isclear.

Figure 24

University Value Arrow

Lbraries

Dormitoriee

Recruitstudents

Curric-ulum

design

Educatestudents

A StrategicPlanning Model forHigher Education

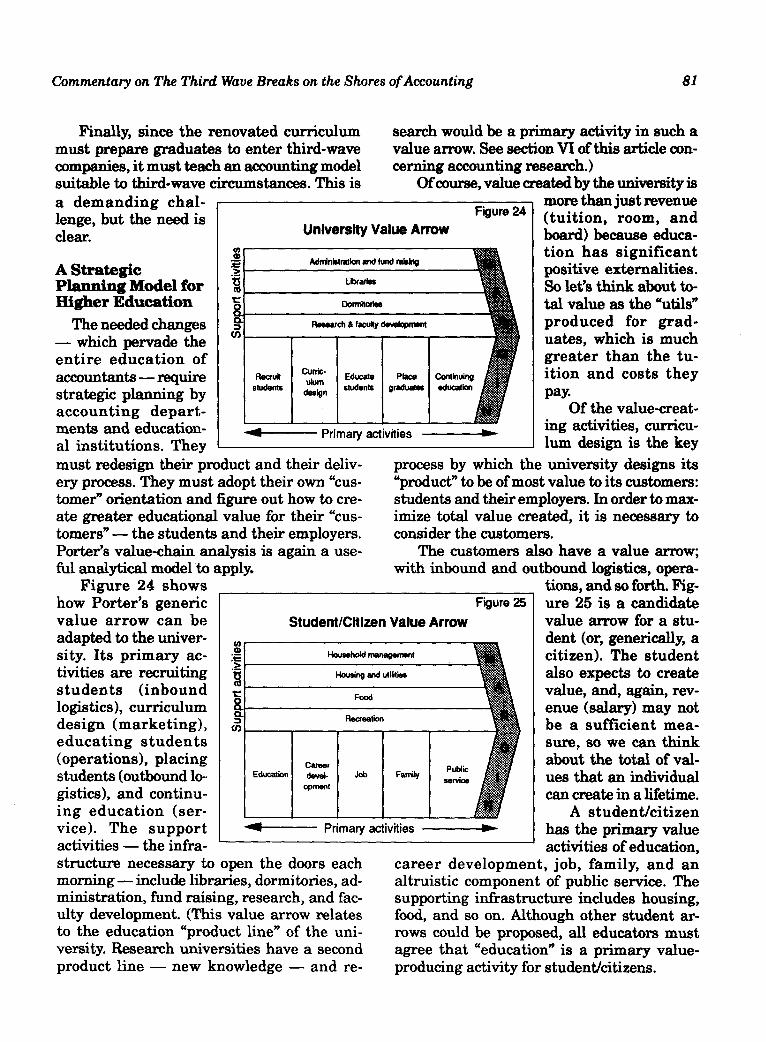

The needed changes— which pervade theentire education ofaccountants—requirestrategic planning byaccounting depart-ments and education-al institutions. Theymust redesign their product and their deliv-ery process. They must adopt their own "cus-tomer" orientation and figure out how to cre-ate greater educational value for their "cus-tomers" — the students and their employers.Porter's value-chain analysis is again a use-fiil analj^ical model to apply.

Figure 24 showshow Porter's genericvalue arrow can beadapted to the univer-sity. Its primary ac-tivities are recruitingstudents (inboundlogistics), curriculumdesign (marketing),educating students(operations), placingstudents (outbovmd lo-gistics), and continu-ing education (ser-vice). The supportactivities — the infra-structure necessary to open the doors eachmorning — include libraries, dormitories, ad-ministration, fund raising, research, and fac-ulty development. (This value arrow relatesto the education "product line" of the uni-versity. Research universities have a secondproduct line — new knowledge — and re-

AdmlnWration and fund raising

Resaarcfi & faculty developnient

Placegraduates

Continuingeducation

Primary activities

Student/Citizen Value Arrow

1•c8.

CO

Household management

Housing and utiiities

Food

Recreation

EducationCareerdevel-

opmentjob

Primary activities

search would be a primary activity in such avalue arrow. See section VI of this article con-cerning accounting research.)

Of course, valtie created by the university ismore than just revenue(tuition, room, andboard) because educa-tion has significantpositive extemsdities.So let's think about to-tal value as the "utHs"produced for grad-uates, which is muchgreater than the tu-ition and costs theypay.

Of the value-creat-ing activities, curricu-lum design is the key

process by which the university designs its"product" to be of most value to its customers:students and their employers. In order to max-imize total value created, it is necessary toconsider the customers.

The customers also have a value arrow;with inbound and outbound logistics, opera-

tions, and so forth. Fig-ure 25 is a candidatevalue arrow for a stu-dent (or, generically, acitizen). The studentalso expects to createvalue, and, again, rev-enue (salary) may notbe a sufficient mea-sure, so we can thinkabout the total of val-ues that an individualcan create in a lifetime.

A student/citizenhas the primary valueactivities of education,

career development, job, family, and analtruistic component of public service. Thesupporting infrastructure includes housing,food, and so on. Although other student ar-rows could be proposed, all educators mustagree that "education" is a primary value-producing activity for student/citizens.

Figure 25

FamilyPublic

service

82 Accounting Horizons/June 1992

After developing these individual arrows,the interesting part is concatenating them intoa value chain. This permits analysis of valuecreated across the entire chain, including theuniversity's component. The value chain in

institutions that supply new assistant profes-sors.

The other main input to higher educationis the students — that is, recruits from sec-ondary education. Universities frequently

University Value Chain

Faculty

Figure 26

Students Employers

Recruits

Figure 26 includes the university, its suppli-ers (faculty and recruits), its customers (stu-dents), and their customers (employers). Themodel permits analysis of the curriculum interms of how the university can create valuefor both students and employers, all the waydown the value chain. In the value chain, notethat the needs of students and employers arerelated—not identical, but related—because,although education aspires to create broadervalues (for example, capadties for enlighteneddtizenship and cultxiral appredation), it mustalso create employability.

Value-chain analysis need not look onlyforward in the value chain, but can also lookbackward as Figure 26 shows; the universityis not the beginning — other value activitiesprecede it. These include the primeuy inputsto higher education: facility and students. Thevalue chain has implications for these sourcesof value.

Figure 26 implies that faculty should beselected for their ability to serve the univer-sity's value creating activities, particularly itscustomer satisfaction activities. That wouldmean selecting faculty with regard for theirability to teach. And it would mean demand-ing evidence of ability to teach from suppliersof faculty — that is, the doctoral granting