commission of inquiry into the national provident fund

TRANSCRIPT

TRANSCRIPT OF PROCEEDINGS National Judicial Staff ServicesSupreme CourtP O Box 7018BOROKO. NCDPAPUA NEW GUINEA Telephone: (675) 324 5792Facsimile : (675) 325 7732

COMMISSION OF INQUIRY INTO THE NATIONAL PROVIDENT FUND

Mr Tos Barnett, Chairman Mr Donald Manoa, Commissioner(In absentia) Lady Wilhelmina Siaguru, Commissioner

AT WAIGANI, TUESDAY 24 APRIL 2001 AT 1.49 PM.

(Continued from 20 April 2001)

[1:49 pm] THE CHAIRMAN: Yes Mr Reeve? MR REEVE: Thank you Mr Chairman. The business that we have for the commission this afternoon is thefinal part of the opening on tenders procedures and nepotism and we will also be presenting a supplementin relation to the interest calculations on the loan for Eda Ranu. The interest calculations on the PoreporenaFreeway Loan have not been able to be finalised as we had thought and the reason for that is that we aremaking some checks in consultation with the Bank of Hawaii and the Bank of Hawaii changed theiraccounting system so that there is a need for them to retrieve records which are not readily retrievablebefore that aspect can be resolved. The first part of the opening on the topic "Tenders Procedures and Nepotism" which we are presentingtoday relates to the procurement of computer hardware and computer software and the disposal ofcomputer units and I will not attempt to summarise it in any way. It is not a very long opening and itindicates that there was a non compliance with tenders procedures both in relation to the procurement ofcomputer hardware and software and in relation to the disposal of computer equipment and the commissionwill see yet again incidences of assets being disposed of by limited "tendering" to which or in which only theNPF staff were permitted to participate. The second part of that opening deals with the procurement of otherprofessional services and some asset disposals and that opening has been prepared by my learned friendMr Kilepak and I would ask that he present part of this opening. THE CHAIRMAN: Mr Kilepak? MR KILEPAK: Thank you chairman. As usual I intend to give a brief outline on the opening and if I mayhand up the document and seek for direction that it be incorporated into the transcript. OPENING STATEMENT ON PROCUREMENT OF OTHER PROFESSIONAL SERVICES & SOME ASSET

DISPOSALS This opening adopts the Write Ups of the NPF Investigation Findings by Finance Inspectors on "OtherProfessional Fees" as its basis.

It details each payment made and whether such needed further investigation. The Finance InspectorsFindings listed five (5) payments. Two payments were made to the Hay Group Pty Ltd which related to thefollowing services: I. Attend, interview NPF Executives;II. Evaluate NPF jobs and provide feedback;III. Access PNG Salary SurveyIV. Provide report for NPF BoardV. Prepare SCMC Submission and negotiate with SCMCVI. Evaluate and assist with the implementation of the review Although the Board approved for a payment of K23,000.00 a total of K27,711.13 was actually paid. The third payment was made to Freehill Hollingdale & Page for K29,089.64 and although it was advancedprior to the service being actually rendered, the end result was an excellent opinion that had beenadequately discussed on the topic Cue Energy Resources. The fourth payment related to the engagement of Ken Yapane & Associates to refurbish the NPF HeadOffice at a cost of K40,000.00. Although the amount was paid, no work had been done and Mr Yapane had given evidence indicating apayment of K20,000.00 from this amount to Kuntila Company No 35 as per Mr Jimmy Maladina's request.That cheque was originally written to Carter Newell Lawyers but was crossed out and written to KuntilaCompany No 35 Pty Ltd upon Mr Maladina's advice. We are of the view that Mr Herman Leahy is accountable for approving the cheque and being the recipientof the cheque, he would be able to explain why such a payment was made when no work had been done. The opening also details a NPF cash payment of K1600.00 to NEC for its meeting in Vanimo. This paymentwas requested by Hon. Chris Haiveta and authorised by Mr Noel Wright and was to be used to pay singsinggroups who entertained at the meeting. We do not know the outcome of this. This opening clearly shows there is lack of Board deliberations on such payments due to the Board notbeing adequately informed by management. We therefore seek to tender all Tendered Documents referred to in this Opening on the basis a ruling will bedeferred until all affected parties have been afforded an opportunity to object and any objections have beenargued. [1.53pm] THE CHAIRMAN: Okay, thank you. Could you just explain, you said the cheque was crossed outand written to Kuntila Company and in the event Mr Leahy received it, is Mr Leahy and Kuntila, they arerelated, are they? MR KILEPAK: No. THE CHAIRMAN: What do you mean that you said that Herman Leahy is accountable for approving thecheque and being the recipient of the cheque. What does that mean? MR KILEPAK: The NPF vouchers have a section for the recipient of the cheque, a person who receives thecheque from NPF and Mr Herman Leahy was THE CHAIRMAN: You mean he took it into his hand. MR KILEPAK: His signature was down as receiving the cheque, signed THE CHAIRMAN: He signed for the cheque. Okay. Thank you. MR REEVE: He physically did the two. THE CHAIRMAN: Yes. MR REEVE: The third part of the opening and the final part of it deals with the procurement of the stationeryand office supplies. And that opening looks at the tenders procedures and examines whether issues ofnepotism existed at the National Provident Fund in the procurement of stationery and office suppliesbetween 1995 and 1999.

[1.56 pm] As far as we can determine, there were no formal tenders procedures adopted to establish anapproved list of suppliers. It is apparent that management did not involve themselves in the sourcing ofsuppliers and this was left to the discretion of junior staff, and in particular, Mr Simon Wanji. Controls overthe purchases of stationery and office supplies were woefully inadequate, and in this opening, we observethat in 1999, NPF's costs for stationery and office supplies reached an unprecedented level of K513,055compared to an average annual cost in the prior years of K246,568. This opening records the preliminariesof results of our enquiries which are ongoing as follows. The controls in place in the procurement recording and payment of stationery and office supplies were weakand as such, provided the conditions for nepotism and employee fraud to occur and remain undetected.There were inadequate procedures in place in the procurement, recording and payment for stationery andoffice supplies. There is evidence of inadequate management supervision and review where weaknesses incontrols were allowed to prevail. A high risk of employee fraud where there is a complete lack ofsegregation of duties and a weak control environment. There is evidence of fraud as revealed by thefollowing indicators. Firstly, the unexplained increase in stationery and office supplies costs in 1999 where the cost is twice thatof prior years and of year 2000. Secondly, the existence of undisclosed interests of Mr Wanji and Mr Sere Koae, NPF employees, in theprocurement of stationery and office supplies. Thirdly, unusual suppliers were selected. Fourthly, secret commissions were paid by suppliers to Mr Simon Wanji. In our view, the commission will, in response to its terms of reference, be recommending that matters bereferred to the police for investigation in relation to the series of payments made by stationery suppliers toMr Simon Wanji. [2.00 pm] Mr Wanji's dealings with Laiks Printing Limited and Bubia Associated Supplies where he hadownership interest, and Mr Koae's dealings with Bubia Associated Supplies where he had ownershipinterest. In relation to the whole of the balance of this opening we seek to tender the tendered documents which arereferred to in the opening on the usual basis that no ruling will be made until affected parties have beennotified and afforded an opportunity to object and those objections have been ruled upon. And we will benotifying affected parties today and tomorrow, being those parties affected by any part of the totality of thetopic of tenders procedures and nepotism. THE CHAIRMAN: Thank you. I have got here documents headed 'Procurement of Computer Hardware andSoftware'. MR REEVE: Yes. THE CHAIRMAN: It is the totality of the documents or is it just all here? MR REEVE: There are three documents. THE CHAIRMAN: Okay, I have got one headed 11, 'Procurement of Professional Services' and someother MR REEVE: That is correct, that is the next segment. And then the final segment is the THE CHAIRMAN: This one? MR REEVE: Status and Office Supplies. THE CHARIMAN: Thank you. Well, I direct that the documents now handed up relating to ComputerHardware and Software, Other Professional Services and Some Asset Disposals and on Status Supply ofStationery and Office Supplies be accepted and held pending possible objections from parties affected bythis matter, and then to be taken in evidence.

PROCUREMENT OF COMPUTER HARDWARE AND SOFTWARE

Background

The procurement of computer hardware and software has been a significant cost to the Fund and as suchrequires our attention. During the period 1 January 1995 to 31 December 1999 NPF computer systems comprised of the followingcomponents:

Contributions system running on a AS400 system, acquired from Datec and the programoperating the system developed by Datec and in which NPF has a 50% right of ownership.

Computer terminals located in operations area networked to AS400 system.

Other stand alone computers used by the other functions running Microsoft software.

To properly put in context the tender procedures or lack of them adopted in the period 1995 – 1999 it is firstnecessary to undertake a brief review of certain background. In early 1993, at the 77th Board of Trustee meeting held 18 February 1993 it is apparent that NPF hadcommissioned KPMG Peat Marwick to assist in the acquisition of a new computer system (CommissionDocument 47 / tendered Document N465). It is apparent from the minutes records at this time that NPF were in the throes of planning for the departureof Niugini Asset Management (NAM) as Managers of NPF. It is relevant to note that the underlying data ofmembers records were held on a NAM operated system. At the 79th Board of Trustee meeting held 16 April 1993, the minutes record that NPF were in discussionwith NAM concerning the purchase of the system's used by NPF (Commission Document 47 / tenderedDocument N466). At the 80th Board of Trustee meeting, the minutes record that NPF's discussions with NAM continued andconsideration given to a proposed software licence and support agreement (Commission Document 47 /tendered Document N467. At the 83rd Board of Trustee meeting held 30 July 1993 it is noted that there were some concerns about the

proprietary rights of McIntosh Securities (PNG) Limited in respect of the software being used by NAM andNPF and consequently the Board resolved to:

"reconsider the agreement to purchase the software and support services but to reserve thatreconsideration until the outcome of the Federal Court Litigation was made known. It was furtherresolved that NPF Management explore any alternatives to the purchase of the software as anadjustment to the Board reconsidering the primary question of the tender by McIntosh Securities(PNG) Limited".

A copy of the Board minute as found in Commission Document 47 will be tendered Document N468. At the 84th Board of Trustee meeting held 30th August 1993, the minutes show that the Board wereadvised by Mr Leahy that management had negotiated a lease arrangement with McIntosh Securities inrespect of the computer hardware and software. A file marked "Datec (PNG) Pty Limited – NPF Software Issues", (Commission Document 1214 tenderedDocument N469) obtained from NPF shows that by 13th September 1993, NPF's Mr Leahy had been indiscussions with a Mr Fuad Ta'eed, the General Manager of Datec (PNG) Pty Ltd concerning that companyassisting NPF identify suitable alternative software packages. The clear inference is that because of concerns about the proprietary rights of McIntosh Securities over the'Securitor Software', NPF sought to review possible alternatives computer systems with the assistance ofDatec (PNG) Pty Ltd. It is not clear as to what, if any, tender procedures were followed in the appointment of Datec as advisors toNPF. However it is apparent that in late 1993, Datec undertook a review of NPF's software requirements. At the 95th Board of Trustees meeting held 29 June 1995, the minutes record that the NPF had cut over tothe new computer system effective 12 May 1995. (Commission Document 47 / Tendered DocumentN470). A file note dated 11 October 1993 prepared by Mr Leahy (Commission Document 1216 / tenderedDocument N471) records that Datec had recommended NPF utilize a AS400 platform and that Datecwould develop software tailored to NPF requirements. It also seems from the minute records that the suitability of this recommendation was not challenged. Itwould be our view that NPF management would not have the requisite skills or knowledge to assess theappropriateness or the risks of the proposal without external assistance. Given that Datec was proposing todevelop software NPF clearly could not rely on their independence and so in our view should have soughtexternal advice. We can we find no mention of NPF management or the Board of Trustees consideringalternative solutions to that proposed by Datec. The proposal put to and adopted by NPF was that following Datec's development of the software, NPFwould be entitled to 50% interest in the proprietary rights. It was also proposed that Datec would thenmarket the software to their clients. The formal acceptance of Datec's proposal to develop software can be found in a letter dated November1993 (Commission Document 1216 / tendered Document N472). The software development cost quoted and agreed to amounted to K217,000 for the initial phase of thedevelopment. It is important to note that a significant implication of this approach was that NPF would be reliant on Datecin relation to future development given that Datec retained an interest in the software as well as becausespecific knowledge of the programme. NPF's Datec correspondence file highlights that the software development project did not run to theanticipated timetable. At the 88th Board of Trustee meeting held, 28 April 1994, NPF Board resolved:

"to continue to pursue Datec (PNG) Pty Ltd to ensure compliance with the timetable for thedevelopment of the software".

A copy of the board minute as found in Commission Document 47 will be Tendered as Document N473.NPF Board minutes record that NPF did not change over from the old McIntosh System to the Datecdeveloped system until May 1995. (Commission Document 47 / Tendered Document 474). By the 97th Board of Trustee meeting held 26 October 1995, it was noted that the development of thesoftware by Datec was continuing to experience difficulties:

"The Managing Director informed the meeting that the operations of the Fund was continuing toexperience difficulties with using the new software designed and installed by Datec (Fiji) Pty Ltd.The trustees noted with concern the unallocated cash figure of over K3 million. It was noted thatal unallocated cash had to be allocated before 1995 year end".

A copy of the Board minute as found in Commission Document 47 will be tendered as Document N475. By the 99th Board of Trustee meeting held 23 February 1996, at minute item 5.11 it seems that theproblems previously experienced had been resolved, the minutes recording: "AS400 – Development of Computer System

The Managing Director informed the meeting that the software was in place and running welland its features were more advanced than the previous software ('securitor', designed and put inplace by Niugini Asset Management Pty Ltd) and phase two would commence in March 1996".

A copy of the Board Minute as found in Commission Document 48 will be Tendered as Document N476. By the 101st Board of Trustee meeting held 28 June 1996 it is clear that phase 2 of the planned softwaredevelopment had not commenced. The minutes record the Board resolved at that meeting thatmanagement prepare a Board paper a setting out what phase 2 involves. At the 102nd Board of Trusteemeeting held 27th August 1996 the minutes record that NPF and Datec had yet to finalise an agreement inrespect of phase 2. (Commission Document 48 / Tendered Document N477). The Datec correspondence files kept by NPF (Commission Documents 1211 – 1218) show that NPF andDatec held regular project meetings to progress the development of the software which continued through1998. There is no indication that NPF management sought the Board's approval or considered the detailedaspects of the project. The Minutes of Board Meetings in 1998 and 1999 record the ongoing progress in fixing bugs in theprogramme and also development of a 'Education Savings' Module (Commission Document 48/49 /Tendered Document N478).

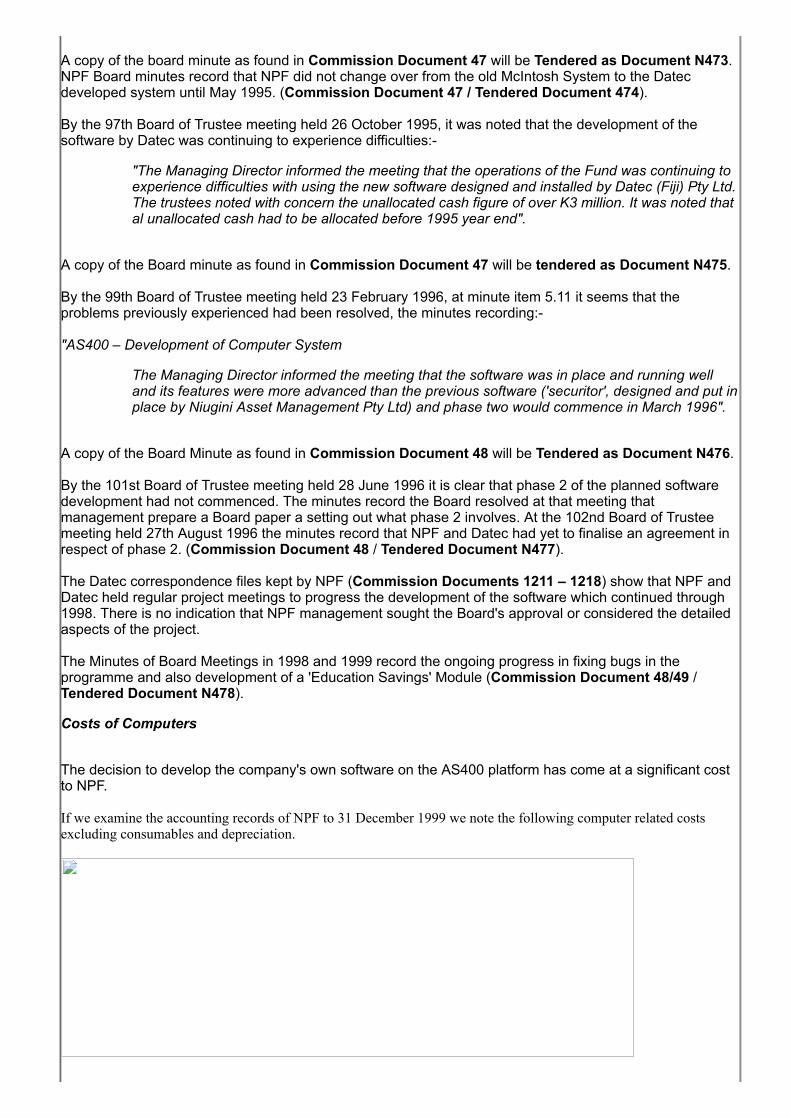

Costs of Computers

The decision to develop the company's own software on the AS400 platform has come at a significant costto NPF. If we examine the accounting records of NPF to 31 December 1999 we note the following computer related costsexcluding consumables and depreciation.

At no point did NPF Management seek Ministerial approval or Board approval for this expenditure otherthan the original approval for phase 1 of K219,000. It is also noted that at the 88th Board of Trustee Meetingheld 8 October 1993 whilst the Board approved the development of software with features currentlyinstalled in the NPF and upgrade it with additional functionality as required by NPF Management", nofinancial parameters seem to have been set. It would be our view that although Datec's costs were not entirely predictable given the nature of their task,NPF management did not seek to manage these costs as far as we can determine. It would also have beenapparent to management that the cost of the development project would exceed financial delegations andalso the K300,000 (later K500,000) de minimis limit set by the Public Finance Management Act and as suchshould have sought Board and Ministerial approval.

Computer Hardware

Approach adopted

In this section of the opening we examine the tender and purchase procedures adopted by NPF in respectof the procurement of computer hardware and also the procedures adopted by NPF in respect of thedisposal of redundant computer equipment. To undertake this task we have first referred to NPF's FixedAsset Register as found on the Authorised Auditors files then together with the NPF's cash books we havesought to obtain the relevant payment requisitions and supporting invoices. For the financial years 1995,1996 and 1997 NPF management reconciled the general ledger to a Fixed Asset Register and therefore theFixed Asset Register is relied upon to enable us to identify the purchase of computer hardware and anydisposals. For 1998 and 1999 this is not the case and as such it has been necessary to supplement ourapproach with additional inquiries.

1995

According to the fixed asset register found in the authorised auditors files, which can be found inCommission Document 385, at 1 January 1995 NPF had the following computer hardware.

Computer purchases and disposals 1995

The fixed asset register shows that NPF did not purchase any computer hardware in 1995 and also therewas no disposal of equipment in 1995. Examination of NPF's manual cash book confirms that no computer equipment were purchased in 1995.

1996

Computer purchases – 1996

The fixed asset register shows that NPF acquired a computer at a cost of K2,067 and this is described inthe register as a TPG Computer – Fin (D Vagi), indicating that this was a computer purchased for use in theFinance section of NPF. NPF has been unable to locate the relevant payment voucher and therefore wecannot comment any further on this item.

Computer disposals 1996

The fixed asset register shows prime facie that NPF disposed of the following items of equipment. Powermate PC 100Mb on 1 December 1996 (original cost K23,995) Powermate PC 40Mb on 1 December 1996 (original cost K20,598) These items were fully written down to nil in the books of NPF. To date NPF have been unable to determinewhat happened to these two items. It seems that it was the practice of management to treat fullydepreciated assets as having been disposed of even if the physical item of equipment was still in use. NPFstaff inform us that these items of equipment are no longer in use at NPF and staff are uncertain as to whathappened to these items.

1997

The following summary has been extracted from the Fixed Asset Register as found in

Computer purchases 1997

Whilst the Fixed Asset Register records that K15,740 of computer equipment was acquired in 1997 wehave verified K13,373.60 of these costs leaving K2,336.40 unverified. The following payments forcomputers have been identified from NPF cash books.

The difference would appear to relate to a Computer recorded in the Register as a Pentium Computer,reference M Bauai, presumably referring to a computer allocated to Mr Bauai, the Human ResourceManager. With regard to the other acquisitions in 1997 it is noted that whilst these were not significant in cost termsNPF management obtained quotes from various computer suppliers before making a commitment topurchasing the equipment. The supplier providing the lowest quote was then selected as the preferredsupplier. This practice has obvious benefits in that it assists NPF obtain goods at the minimum cost and willassist in preventing nepotism and other corrupt practices. We have found no documentary evidence within any of the NPF accounting records, correspondence files,Managing Director's files and elsewhere that would suggest that NPF management or the Trustees soughtto establish a documented and formal purchase policy in respect of Computer equipment. The purchase ofcomputer equipment particularly at NPF which is dependant on Information Technology required carefulscrutiny by NPF management and the Trustees both in terms of ensuring an appropriate and properfunctioning system but also because of the high level of costs involved. From our review of the pattern and manner of NPF's purchase of computer equipment we have observedthe following matters of note: purchase of computer equipment appears adhoc and not in accordance with annual budgets or specific ITplan no evidence that NPF sought to negotiate better than normal prices with any one supplier from 1998 onwards NPF purchases predominantly from Tanorama Limited and Datec with no documentedattempts to extract better prices from that supplier. Judging by the payment requisition records the purchases from Tanorama Limited and Datec were madewithout reference to any comparison of prices from other suppliers

Computer disposals 1997

The fixed asset register shows prima facie that NPF and again disposed of the following items of equipmentin 1997. Matrix printer, recorded at cost of K4,916 Matrix printer, recorded at cost of K7,910 Memory expansion & disk, recorded at cost of K19,028 UPS, recorded at cost of K3,273 Printer, recorded at cost K11,594 72Mb hard disk, recorded at cost of K2,275 These items were fully written down to nil in the books of NPF. NPF have been unable to determine whathappened to these items but it would appear that these items were classified as having been disposed onlyto effect their removal from the register because these were fully written down to nil value.

1998

There are imperfections in NPF's accounting records for the financial years 1998 and 1999 where the fixedasset register does not seem to reconcile to the general ledger. The Fixed asset register found on theauthorised auditors file in Commission Document 736 shows a brought forward cost as at 1 January 1998for computer equipment of K301,439. The closing balance shown in the Fixed Asset Register on theauthorised auditors file for the 1997 financial year shows a carried forward cost of K315,987. The difference of K14,548 would seem to relate to the following items of computer equipment which"disappear" from the register without explanation: Compliance section PC, recorded at a cost of K2,000 3 IBM PC – MD's office, recorded at a cost of K11,254 UPS – Operations Section, recorded at a cost of K1,292 As with earlier years these items of equipment were fully depreciated in the books of NPF and so had a nilwritten down value, and therefore it is likely that these items were removed from the register for this reason.However no other separate register of assets was maintained as far as we can determine to assist usdetermine what happened to these items. The following summary has been extracted from the Fixed Asset Register as found in

Computer purchases – 1998

The Fixed Asset Register records that K702,356 of computer equipment was acquired in 1998. We haveverified this expense to the underlying vouchers as detailed in the table over the page.

Ref 1 The full invoice value was K42,121.71 but this was paid in 2 instalments because of the need ofTanorama to pay their supplier prior to being able to procure computers to satisfy order from NPF. In ourview the payments to Tanorama required Managing Directors approval and was beyond Mr Wright'sdelegation. Mr Fabila had just joined NPF.Ref 2 – The Board minutes record that the Board approved the purchase of AUD$429,500 – however thefinal invoice price was AUD483,840 – no subsequent board ratification for this amount, although Boardnoted the tabling of a contract for the purchase of a AS400 2175 machine for AUD$483,840.00. Paymentrequisitions will be tendered N484. There are two purchases that require our attention, the purchase of a new AS400 machine and also thepurchase of 16 personal computers from Tanorama Pty Limited.

Purchase of AS400 machine

The purchase of this item of computer hardware would seem to have resulted from concerns about thecapacity and efficiency of NPF's computer system. The 111th Board of Trustee meeting held 28th February1998 records that:

"The Board noted that according to a recent performance analysis conducted by IBM Australia,utilisation of NPF's current system is between 60% and 80% with peaks of 90% and above isexperienced when additional functions are run on the system like "end of day processing". It wasfurther noted that once companies like NPF get involved with hardware and software providerslike Datec, it is an expensive relationship and also involves the regular update of machines. Itwas resolved to approve the expenditure of up to K328,165.00 for the purchase of the upgradeand additional K32,506.00 in annual maintenance charges."

This issue was discussed later at this meeting with a different resolution resulting. At item 6.1 which comesunder the Operations Manager's Report (Mr Leahy) we find the following minute record: "Software issues

The Manager Operations reported on the following software on NPF's system:

(i) Education Savings Module

The Board was informed that completion of the Education Savings Module is expected nextweek. Currently, testing of the module had suffered as a result of the absence of members of thetesting team who were away ill. However, every effort will be made to "cut over" onto the NPF'slive data base next week.

(ii) Outstanding bugs and fixes from phase 1

The Manager operations reported that tangible results had yet to been seen on NPF's currentsystem.

(iii) Member Savings Bonus

The Manager Operations reported that tangible results had yet to be seen on NPF's currentsystem.

(iv) Unpresented cheque listing

The Manager Operations informed the meeting that work on the unpresented cheque listingwas progressing.

(v) AS400 Model 2175

The Managing Director tabled a report from Datec (PNG) Pty Ltd which quoted the results of arecent performance analysis conducted by IBM Australia on NPF's current central processingunit ("CPU"). It was noted that current utilisation of the CPU was 90% and above. This peakutilisation was experienced when the system ran additional functions like "end of dayprocessing". Two (2) quotations had been received from Datec. The preferred quote inAustralian dollars came to the following.

Hardware and software totals AUD$429,500 Annual Maintenance AUD$ 60,589AUD$490,089(AUD$ to Kina .8071) PNGK607,222

It was resolved to approve of the purchase subject to the approval of the Minister for Financeunder the 61 of the Public Finances (Management) Act 1995."

The relevant Board paper referred to in this minute can be found in Commission Document 24 and will betendered Document N485 and a copy of the Board Minutes as found in Commission Document 50 willbe Tendered N486. It is noted that this board paper quoted AUD$380,671 (inclusive of AUD$52,506maintenance) for the AS400 2175 and AUD$306,609 (inclusive of AUD$ 42,291 maintenance) for AS400model 2135. The minute record is clearly confusing where on the one hand at item 5.8 the approved expenditure up toK328,165 for the purchase of the AS400 machine upgrade and which would appear to be consistent withone of the quotes included in Mr Leahy's Board paper (although there is inconsistency in the currencystated, the minute in Kina and the board paper in Australian dollars) but then later at item 6.1 a much higherfigure was approved by the Board (AUD$490,089). This second higher figure does not tally with the quotedprices from Datec as stated in the Board Paper. The actual Datec invoice raised for the AS400 machine excluding maintenance was a total of AUD483,840(being AUD463,860 for the machine and AUD19,980 for the installation). We will return to this anomaly in a moment.

Ministerial approval – S61 Public Finances Management Act 1995

Following the apparent approval of the Board to purchase the new AS400 through Datec, NPFmanagement sought the approval of the Minister for Finance by way of the following submission dated 9March 1998: "A. PURPOSE

To seek your approval under Section 61 of the Public Finances (Management) Act 1995 for thepurchase of hardware and software for NPF's operating system. The equipment recommendedfor purchase is an AS400 model 2175 risk based system.

B. FACTS AND CONSIDERATIONS

NPF has been involved with Datec (PNG) Pty Ltd since 1993. Datec is retained exclusively byNPF, and we suspect many other organisations in Papua New Guinea, to provide software andhardware support services.

Given the nature of the computer age, utilisation of computers and the efficiency they bring intoany business environment involves, to a very large degree, reliance on the supplier's expertisein the area. Whilst our reliance on Datec is unavoidable at this stage, it is important that we atleast attempt to reduce our reliance on Datec's expertise in the area. With this purchase we aimto reduce our reliance on Datec by developing independence in terms of the requirement forsoftware fixes, modifications and future enhancement developments.

Apart from the strategic objectives of this purchase, NPF's current operating system is incapableof sustaining its peak interactive workload. In fact, NPF's current operating system, recentlyunderwent a performance analysis conducted by IMB Australia. The results showed that NPF'scurrent system averages between 60% and 80% utilisation of the Central Processing Unit("CPU") with peak utilisation of 90% and above. Utilisation of the CPU of 90% and above isexperienced when additional functions are run on the system like "end of day processing". Thisprocess involves the updating and posting of all transactions conducted during the day. Thisprocess is "run" overnight which also includes the backing up of data onto a separate disk forstorage outside of NPF. It was made known to us that the industry average of recorded CPUutilisation is 60% and below.

With the purchase of the new system, NPF's current system will be used as a developmentmachine. NPF's software programmer, Mr Joseph Mapai will be able to apply and test anysoftware changes that are requested from time to time. At the present time, there are some 19bugs and fixes outstanding from NPF's phase I developments. These are currently being workedon by Datec. Further, there are some 30 items for developments for the Fund. Thesedevelopmental items will enhance the functionality of the current system. However, it is a veryexpensive exercise for the Fund with Datec continually attending to the matters mentionedabove. In the last 8 months NPF has spent K150,000.00 on software development items. There are a number of special tasks yet to be fully thought out and documented fordevelopment. Currently, the education savings module has been prioritised for completionshortly. This module involves the quarantine of additional contributions paid in by the member forpurposes of education. The new system will be Year 2000 compliant. By way of explanation, there are two aspects tothe concept of Year 2000 compliant. These two aspects are the system itself and the softwareapplication on the system. The AS400 model 2175 will contain features that, at the turn of thecentury, will allow it to differentiate between the last two digits of the year. So that rather thanassume that the last two digits of the year will change the date of the system to 1 January 1900,it will identify the new year as January 1 2000. Tis will not necessarily apply to NPF's softwareapplications. However, having a system which is Year 2000 compliant will assist Datec to makethe necessary changes to NPF's software application such that it is Year 2000 compliant. The option of simply upgrading NPF's current system has been considered. It has beenestimated at around AUD$200,000 to upgrade the current operating system. In the event NPFchose this course, it will not have a development system which will mean that its aim, in terms ofreducing its reliance on Datec will not be achievable. This is not a desirable situation and in themanagement and the Board's view, should be avoided.

C. FINANCIAL IMPLICATIONSThis purchase is a significant purchase for the Fund which has been budgeted for in 1998. D. STAFFING IMPLICATIONS

The efficiency this new system will bring to the Fund will reduce the need foradditional staff.

E. POLITICAL IMPLICATIONSNon envisaged. F. LEGISLATIVE IMPLICATIONS

This purchase requires the approval of the Minister under Section 61 of the PublicFinances (Management) Act 1995.

G. OTHER IMPLIATIONSNon envisaged".

A copy of this submission as found in Commission Document 50 will be Tendered as Document N487. The glaring omission in this brief is any sort of support or reference to an "expert" analysis of the investmentdecision by someone with the requisite technical knowledge and independence. It is apparent that NPFrelied on the recommendations of Datec both in terms of the decision to upgrade and with regard to thepurchase of the AS400 through Datec. There is no indication whatsoever that NPF sought a second opinionon the proposal by an appropriate independent computer consultant. Clearly Datec could not be classed asan independent advisor where NPF would be purchasing equipment through Datec and also where therewas an existing relationship between NPF and Datec where Datec had developed software utilised by NPF. Also on the same date, the 9 March 1998 we find Mr Leahy provided the following clarification given to theSecretary for Finance, Mr Morea Vele. "I refer to the above purchase.

On preparing the minutes for our last meeting, I note that some clarification is needed withregard to the purchase price of the Equipment. This note is by way of information only since wealready have the resolution of the Board to proceed with the purchase. In any event, Ministerialapproval under Section 61 of the Public Finance (Management) Act 1995 is required.In the course of settling the terms of the hardware purchase contract with Datec, figures for thepurchase were finalised and those appear below:

· Hardware and software totals AUD$429,500.00· Annual maintenance (separate contract) AUD$ 60,589.00· Data conversion AUD$ 18,500.00

AUD$508,589.00

(kina to AUD$ 0.871) PNGK630,143.72

By way of clarification, the Managing Director by oversight referred to the purchase amounts inhis reporting of the proposed purchase as Kina amounts rather than Australian dollar amounts. Ifyou examine the quote from Datec, which appears as one of the annexures in the ManagingDirector's report, you will note that it clearly states on the front page, "prices in Australiandollars" whereas the Managing Director referred to kina figures in his report. Nonetheless, wenote we have approval from the Board to purchase the Equipment and have prepared asubmission to go to the Minister."

A copy of this letter as found in Commission Document 5d will be Tendered as Document N488. It is apparent that the Board minute in question (111th Board meeting) examined previously was whollyinaccurate but even though Mr Leahy was according to this letter aware of the inaccuracies there was nocorrection of the anomaly at subsequent Board Meetings.

On the 23rd March 1998 Mr Leahy responding to enquiries from the Department of Finance advised theDepartment of the following concerning the NPF's proposed acquisition of the AS400:

"I refer to our telephone conversation this morning. You raised two queries in relation to the above purchase. (i) Purpose

This new piece of hardware is being purchased to upgrade the software support theNPF requires in terms of its administrative and management information functions.These systems are continually outdated with the rapid progress in software andhardware development. To keep up with improved performance of the currentsystem, you need to purchase the additional upgrades.NPF's current operating system is now outdated and will no longer be supported byIBM for spare parts.As mentioned in our submission, NPF's current operating system is now over utilisedin terms of the Central Processing Unit, Disk Capacity and Memory. This new pieceof hardware will address these problems.

(ii) What is it?

The AS400 is a box the size of a stand along PC. This box will replace NPF's soldoperating system which is the size of a 4 draw cabinet. The box contains softwarecomponents which will operate NPF's current administrative and managementinformation functions. For your further assistance I enclose brief notes on the AS400system.Please note that due to the delay in obtaining Ministerial approval the quote ofAUD$448,000.00 has been increased by 8% (AUD$35,840.00). In view of thefluctuating Kina, I suggest you provide a ceiling on the price in Australian dollarsabove which NPF will be required to seek further approval."

A copy of this letter as found in Commission Document 5d will be Tendered s Document N489. On the 25 March 1998 Mr Mete Kahano from the Department of Finance responded as follows:

"Reference is made to your letter dated 9 March 1998 seeking Minister's approval on thepurchase of the AS400 Model 2275 ("the equipment"). Whilst I understand the need for the procurement of the equipment by the Fund, there are alsoestablished procedures in which Public Institutions such as NPF should comply with especiallywhen such purchases involve large sums of money. The reasons given as basis for the Fund notto tender for the purchase of this equipment are not in line with these procedures. I suggest you state your reasons as to why the Fund cannot go on tender and request for anissuance of a Certificate of Inexpediency (COI) by the Minister for the purchase of theequipment."

A copy of Mr Kahona's response as found in Commission Document 5d will be Tendered as DocumentsN490.On the 26th March 1998, Mr Leahy wrote to Mr Vele Iamo, Deputy Secretary in response to the request byMr Kahano. The letter reads as follows:

"Department of Finance are considering our submission to the Minister with regard to the abovepurchase. They have queried us on whether we have complied with the tender procedures set forth in thePublic Finance (Management) Act 1995. I have provided the following reasons to the Department as to why the purchase of the hardwarewas not put out to tender:

1. NPF owns 50% of the intellectual property rights in the software developed on the AS400 riskbased system. The other 50% is owned by Datec (PNG) Pty Ltd. The software currently in useon the system has been developed specifically for the particular hardware NPF is purchasing. 2. Datec is the only distributor of this hardware in PNG. 3. NPF is a 33% shareholder in Steamships Pty Ltd which in turn is a 50% shareholder of Datec(PNG) Pty Ltd. It is Board policy to source business from companies in which NPF is ashareholder so that the Funds member eventually benefit from the increase in profitability ofthose business. The Department of Finance have now requested that the NPF Board certify that the inviting oftenders is impracticable or inexpedience. Please certify below that the calling of tenders with regard to the above purchase isinexpedient".

A copy of Mr Leahy's letter as found in Commission Document 5d will be Tendered as Document 491. The reasons stated in favour of the request for a Certificate of Inexpediency saw favour with theDepartment of Finance because an internal memorandum Dated 31 March 1998 from Mr Kahona to DeputySecretary Policy, the Acting Secretary and the Minister recommended that a Section 61 approval begranted to NPF for a total purchase price of AUD515,000 for the AS400 hardware and related software. A copy of the memo as found in Commission Document 5D will be tendered as Documents N492. A further copy of the same memo was found but dated 13th May 1998 and this is then followed by a letterdated 25th May 1998 to Mr Fabila at NPF from Sir Mekere Morauta, MP as Acting Minister granting NPFthe relevant approval as follows: "I refer to your predecessor's letter of 9th March 1998 on the above.

In accordance with Section 61 of the Public Finances (Management) Act 1995, I hereby give myapproval for the National Provident Fund to purchase the AS400 Model 2175 ("the equipment")from Datec at a total purchase price of up to K638,086.98 (AUD$515,000). My approval on the estimated price ceiling of up to K638,086.98 (AUD$515,000) is inclusive ofthe initial purchase price of K630,143.72 (AUD$508,589) plus the fall in the Kina value. Anyvariation in the price above should seek my prior approval."

A copy of the approval as found in Commission Document 5D will be tendered as Document N493. The AS400 as detailed in the table earlier was paid for in two instalments, K64,129.97 being 10% as adeposit in June 1998 on the date the contract was signed with Datec (Commission Document 25 /tendered Document N494) and the balance of K587,737.07 in September 1998. The total cost thereforebeing K651,867.04 (AUD483,840). This was within the approved amount provided by the Minister forFinance's approval but was significantly greater than the earlier quotes provided by Datec to NPF on whichthe Board provided their approval. It would appear from the minuted record of events that NPFmanagement exceeded its authority where the minutes for the 112th meeting record that the Boardapproved of an upgrade at minute item 5.8 of K328,165 and then at 6.1 AUD429,500.00.The signed contract for AUD483,840 was according to the minutes of the 113th Board meeting tabled to theBoard. No mention is made in the minutes either by management or the Trustees acknowledging that thispayment was greater than the relevant Board resolution or ratifying managements execution of theagreement. It is our view that this increase in costs probably requires our further attention and request theCommissioners direction before pursuing.

Purchase of 18 PC's from Tanorama Pty Limited

In 1998, NPF's other major purchase of computer equipment was through Tanorama Pty Limited whereNPF purchased 18 PC's. As far as we can determine these PC's were acquired for use in Operations

section (11) and the remainder in Finance and Accounts (7). The decision to purchase computer equipment from Tanorama Pty Limited is not documented in the BoardPapers or in Board minutes. We are told by the current accounts payable and operations staff that thereason for purchasing was related to the fact that a Mr David Moang was employed by Tanorama as acomputer consultant. We are further told that Mr Moang was formerly with Datec and NPF staff thoughtNPF received good service from Mr Moang and therefore staff preferred to purchase from Tanorama PtyLimited (Commission Document 1246 / tendered Document N495). It is clear that NPF management approving the purchase of the computers from Tanorama allowed this formof favouritism to occur because Mr Wright and Ms Dopeke approved these purchases without insisting oncomparable quotes from other suppliers. The market for computer sales in PNG is relatively small but thereare a number of suppliers and as such the market can be seen as competitive, although it is noted that inthe supply of personal computers the industry margins are known to be modest and thereby providing forminimal opportunities for cost savings. In the case of Tanorama Pty Limited's invoices to NPF in 1998 it is noted that the invoices included a 5%procurement charge, presumably representing that company's profit margin. It is our view that where NPFfailed to 'shop around' it is likely that NPF did not obtain the best possible prices. It is also noted that in relation to this order for 16 PC's made in March 1998, NPF was requested byTanorama Pty Limited to settle an advance payment of K21,060.86 being 50% of the invoice value toenable that company to obtain the relevant computers ordered from their suppliers. Mr Maong explainedthis as follows:

"Due to our current situation with our suppliers, they have requested that we give them 50%payment before they release the computers to us. This is why we have included on the quote toNellie that we require 50% of the payment of the total price we quoted….."

A copy of the fax from Tanorama as found in Commission Document 1241 will be tendered as DocumentN496. The payment request of K21,060.86 was paid by NPF cheque 19892 as requested and this was approvedby Mr Wright. The balance of K21,060.86 was paid by NPF cheque 20252 dated 27th May 1998 and againthis was approved by Mr Wright. In our view Mr Wright acted in excess of his delegated authority inapproving these two payments because the full invoice was for K42,121.72 and Mr Wright's financialdelegation was limited to K25,000. These payments should have been approved by Mr Kaul (Marchpayment ) and then Mr Fabila (May payment) or the Board of Trustees.

Computer disposals 1998

Other than the items of computer equipment noted earlier in this section as having "disappeared" from theFixed Asset register, there is no record of any items of equipment being disposed of in 1998.

1999

As we have earlier mentioned there are imperfections in NPF's accounting records for the financial years1998 and 1999. This is again apparent in respect of the Fixed Asset register for 1999. This is found on theauthorised auditors file (Commission Document 737 tendered Document 497) and shows a broughtforward cost as at 1 January 1999 for computer equipment of K720,161. The closing balance shown in theFixed Asset Register on the authorised auditors file for the 1998 financial year shows a carried forward costof K1,003,797. The difference of K283,636 relates to the following items of computer equipment which "disappear" from theregister without explanation: Datec Computers recorded at a cost of K282,568 Hewlett Colour printer K1,066 As with earlier years these items of equipment were fully depreciated in the books of NPF and so had a nilwritten down value, and therefore it is possible that these items were removed from the register for thisreason. However no other separate register of assets was maintained as far as we can determine to assistus determine what happened to these items. The following summary has been extracted from the Fixed Asset Register as found in

Computer purchases – 1999

The Fixed Asset Register records that K55,578 of computer equipment was acquired in 1999, we haveverified this expense to the underlying vouchers as detailed in the table over the page.

Reviewing these purchases in 1999 we have a number of observations, as follows:

1. There are several instances where Management approval of purchases but which they wereto benefit from, albeit in the form of a new and better computers.

Examples include:Bloomberg Screen – January 1999

Mr Wright purchasing of a Bloomberg Screen at great expense and which wouldappear to be unnecessary. A Bloomberg Screen allows the user to obtain live sharequotes throughout the world. Given NPF's portfolio this was in our view anextravagant waste of money.

The purchase benefited Mr Wright (in his work role and not personally) but Mr Wrightapproved the purchase.

Think Pad – March 1999

Mr :Leahy approval of a new portable IBM think pad computer is another example,again this purchase was approved by Mr Leahy and for his use.

It is noted that in September 1999, NPF introduced a new system of approvalsdesigned to prevent such conflict situations. (Commission Document 1254 /tendered Document N498).

2. All purchases were made with Datec (PNG) Pty Ltd.

It should be noted that no comparable quotes from other suppliers were obtained tocheck that NPF was obtaining value for money.

3. Bloomberg Screen

This item of equipment cost NPF K41,515.03 and was approved for purchase by MrWright. Mr Wright's financial delegation limit was K25,000 and as such Mr Wright hasclearly exceeded his authority. Mr Wright is in our view potentially liable for anylosses associated with this purchase.

The Bloomberg Screen is not used by NPF, and has been packed and placed instorage. It is not entirely clear as to what rights of ownership NPF has in respect ofthe Bloomberg Screen but we are informed by NPF's Acting Managing Director, MrMitchell considers that the screen belongs to Bloomberg and NPF's payment waseffectively a right of use.

1999 – Disposal of Computer Equipment

According to the Fixed Asset Register, NPF did not dispose of any equipment in 1999. However, inquiries with NPF staff have revealed that NPF did dispose of old Y2K noncompliant computersand other ancillary equipment by way of a tender to staff. We are told by NPF that these items of equipment were fully written down to nil in the books of NPF. A memo dated 5 August 1999 issued by Mrs Shirley Marjen to all staff records the results of the tender asfollows: "We refer to a memo by Kaspa Kula dated 27th July 1999.

We received tremendous response from staff members of the Fund in respect to the tendernotice.

The tender officially closed on Wednesday 4th August 1999 and the tender box was opened by Ms SalomeDopeke and myself and the successful bidders were declared on 5th August 1999.

You are all required to pay the amount owing in full (strictly cash only) to the Accounts Officer,present your official receipt to Mr Kula and collect your item(s).

All items MUST be collected with seven (7) days as of the date of this memo".

A copy of the memo as found in Commission Document 1256 will be Tendered N500. The tendering of computers to staff only can be criticised as a form of Nepotism and in our view NPF did notobtain market value for these items of computer equipment. In our view, NPF management were remiss in their duties in failing to maximise on the sale proceeds of thetender process. A memo issued by Mr Kasper Kula, Manager of Management Information systems to MrLeahy recommended that the old computers be sold by staff tender (Commission Document 1258 /tendered Document N502). A hand written note on the memo under the initials of Mr Leahy approved ofMr Kula's recommendation. "KasperPlease proceed with tender to staff" We also note that in June 1999, Mr Fabila approved the donation of an old IBM computer to the BaptistBible Church at six mile. A copy of the memo as found in Commission Document 1257 will be Tenderedas Document N501. Again whilst this was no doubt for a worthy cause, Mr Fabila's duty as we have stated in an earlier hearing,was to the members of the Fund and as such in our view was required to maximise proceeds from anydisposal of NPF assets. This mindset seems to have been absent at NPF. 11. PROCUREMENT OF OTHER PROFESSIONAL SERVICES & SOME ASSET DISPOSALS

A. OTHER PROFESSIONAL SERVICES

In Commission Document 4A which is the WriteUps of the NPF Investigation Findings by FinanceInspectors, is a Report on Administrative and Operating Expenditures incurred by NPF during the period 1January 1999 to 31 August 1999. The specific expenditure items covered in that Report included among others, "Other Professional Fees". For our purposes, a copy of the cover letter and the Report on "Other Professional Fees", which will beTendered Document OP1 to OP4 details five payments made in that period (01/01/99 to 31/08/99).

These were: Hay Group Pty Ltd (two payments); Freehill Hollingdale and Page; Ken Yapane & Associates;and ETS Group. 1. HAY GROUP PTY LTD

A total payment of K27,711.13 being Cheque # 21784 dated 07/01/99 for K23,158.52 andCheque # 22975 dated 12/07/99 for K4,552.61.

The amount was paid for the following services rendered to NPF: attend, interview NPF Executives Evaluate NPF jobs and provide feedback Access PNG Salary Survey Provide report for NPF Board Preparation of SCMC submission and negotiation with SCMC Evaluation of review Assist with Implementation of Review

The Finance Inspectors were of the view that the payments were in order. However, it should also be noted that at the 115th Board Meeting held 6 November 1998, item10.3 records that the Hay Consultants Group completed their project and the Board resolved toapprove the unbudgeted amount of K23,000.00 for that project.

An extract of the minute, taken from Commission Document 50, will be Tendered DocumentOP 5.

Although the payments were made in 1999, we are unable to locate any mention of this item inthe 1999 Board Minutes.

2. FREEHILL HOLLINGDALE & PAGE

A payment of K29,089.64 by Cheque # 2314 dated 09/02/99 was made in advance prior to theservices being actually rendered.

This was so the above company could enquire into Cue Energy Resources Ltd of which NPFinvested A$11,726,094.00 during the period 17/07/97, to 04/12/97 while Mr Copland was thechairman of the NPF Board of Trustees.

The payment was authorized by the Managing Director Mr Henry Fabila.

This payment, as noted by the Finance Inspectors was paid in advance before the services wereactually rendered.

However, as stated in our opening on Tenders Procedures and Nepotism, (at transcript page7597), Freehill Hollingdale & Page provided an excellent opinion on Cue Energy Resources andthe liability of NPF Board members, which the Commission has seen when we dealt with thetopic Cue Energy Resources.

Relevant copies of the NPF vouchers and a letter of instruction by Mr Fabila are located inCommission Document 1197. Part D and will be Tendered Documents OP 5A to OP 5G.

We are satisfied that this matter does not warrant any further investigation.

3. KEN YAPANE & ASSOCIATES

A Cheque No 22150 dated 26/02/99 for K40,000.00 was paid in advance. It was to be for theNPF Head Office Refurbishment that included:

Drawing up plans for furniture layout to ground floor, Prepare documentation for tendering purposes, Calling of tenders, awarding of contract, Supervision of Contractor during actual fitout stage,

Certifying of contractors invoices for payments. It should be noted that at the time of the investigation by the Finance Inspectors, no work had been done. Furthermore, the Corporate Secretary Mr Leahy instructed the OIC Accounts Mr Simon Wanji to processthe vouchers / cheque and that such authorisation for this improper and highly questionable payment wasgiven by Mr Leahy. Mr Leahy was also the recipient of the cheque while Mr Wanji witnessed. We would interpose that copies of documents evidencing the above, taken from Commission Document690 will be Tendered Document OP 6 and OP 7. Further, on 2 October 2000, Mr Yapane appeared before the Commission of Inquiry and stated at transcriptpage 2502 that he provided the quote, the invoice and the drawings. At that hearing, he was shown two documents taken from Commission Document 690. The first document was a letter dated 16 October 1998, a copy to be Tendered Document OP 8 and OP 9that submitted a lump sum of K50,000.00 as its professional fee as per discussions between Mr Yapane, MrLeahy and Ms Andoiye. The letter further reads: "The fee proposal covers for:

* Measure up and drawing up of existing premises and preparation of indicative plans withfurniture layouts,

* Prepare detail documentation which includes final furniture layout and detailed scope of worksfor tendering purposes.

* Calling of tender and screening of tenders and recommending to client for awarding ofcontract.

* Supervision of contractor during actual fitout stage. * Certifying of Contractors invoices for payments". On that letter is an handwritten note by Mr Herman Leahy dated 26 February 1999 that reads: "Ranu/Simon,Please process a cheque for my approval". The second document was an invoice dated 18 January 1999 described as NPF01. Although it statedK50,000.00 as the total fees quoted, only K40,000.00 was invoiced. A copy of the invoice will be Tendered Document OP 10. The invoice may have been attached to a letter by Mr Yapane to Mr Fabila dated 18 January 1999 asevidenced by Mr Fabila's response in a letter dated 1 February 1999. Mr Fabila's letter is addressed to Ken Yapane & Associates and reads: "Dear Ken, RE: NPF OFFICE REFURBISHMENT – GROUND FLOOR Thank you for your letter of 18 January 1999.

I acknowledge receipt of the architectural drawings and a bound copy of the specificationsenclosed with your letter.

The matter will now be referred to our Board for formal approval". A copy of the letter, taken from the Managing Director's Running Fine – Commission Document 324 willbe Tendered Document OP 11. What should also be noted was that the matter was not discussed at Board level. The subsequent Board

Meeting on 8 February 1999 only resolved to delegate an amount of K50,000.00 to the Managing Directorand the Corporate Secretary. Any amounts in excess of K50,000.00 would need to be approved by theChairman (Mr Maladina) and signed for by at least one other Trustee. Thus, Mr Herman Leahy's authorising of Mr Simon Wanji to process the cheque of K40,000.00. An extract of the minute, taken from Commission Document 51 will be Tendered Document OP 12. A Cheque No 22150 for K40,000.00 and dated 26 February 1999 was made payable to Ken Yapane &Associates. The cheque is located in Commission Document 690 and a copy will be TenderedDocument OP 13. Further at transcript page 2514 to 2516, Mr Yapane admitted depositing the K40,000.00 into his companyaccount with PNGBC on 1 March 1999. The next day Mr Yapane drew a cheque for K20,000.00 and on 12 March a further K20,000.00 was drawn.Mr Yapane said that one cheque was made payable to Peddle Thorp and the other was invested into JRCreative Network (Money Rain). The money invested with Money Rain was later credited into the accountaccording to Mr Yapane. On 11 October 1999 Mr Yapane appeared again before the Commission of Inquiry and when crossexamined further, stated at transcript pages 2719 to 2721 that only K8,000.00 was paid to Peddle Thorpwith an outstanding of K2,000.00 Mr Yapane agreed that Peddle Thorp did the architectural design and the specification for tender and all hedid was to coordinate everything although there was nothing to coordinate as the project was shelved. Peddle Thorp's file which is Commission Document 710 contains all the necessary documentation and itshows that, the agreed lump sum fee was K13,568.75 and at the stage of the project being out for tender,the cost claimed was K10,176.56 (ie, 75% of the agreed fee of K13,568.75). As of 21 September 1999, the outstanding amount to be paid to Peddle Thorp was K2,176.56. A copy of a letter dated 21/09/99 detailing the above will be Tendered Document OP 14. At transcript page 4471, when dealing with the Tower Opening, we discussed the Bank Statement for KenYapane & Associates for the period 28/02/99 to 31/03/99 (which was Tendered Document T462) andadvised of the K40,000.00 being credited to that account on 1 March 1999 and three debits of K20,000.00each on 2 March 1999, 10 March 1999 and 12 March 1999. We stated then that we would discuss this later. On 1 November 2000, Mr Yapane made a Statement which was incorporated into the transcript at pages3246 to 3251. The K40,000.00 NPF Office Refurbishment is at transcript page 3250. Mr Yapane stated that Mr Maladina was not involved in securing the contract for him. He could not recallwho had told him about this contract but remembered telephoning Ms Andoiye who referred him to MrLeahy. He wrote a letter dated 16 October 1998 which had been discussed earlier. Peddle Thorp was engaged and by 18 October 1998, he submitted his invoice. The statement further reads:

"I went to Mr. Maladina's office, (I cannot recall what I went to see him about). He asked how thecontract with NPF was coming on. I asked, "What contract". He replied, "The fitout". I wassurprised. I said, "We are about to finish". He asked how much my fees were. I replied,"K50,000.00". He asked, "Can you give me K20,000. I need some money and I'll pay you back".I said, "OK".

On 1st March, 1998 I received payment and arranged express clearance. I went and paidK20,000 to Mr. Maladina by way of a cheque payable to Kuntila No. 35. He has not paid me

back yet. In April, 1998 I paid Peddle Thorp's fee of K8,000 as agreed".

When crossexamined at transcript pages 3262 to 3268 the following was revealed. The first debit of K20,000.00 on 2 March 1999 was originally written to Carter Newell Lawyers but wascrossed out and written to Kuntila Company No 35 Pty Ltd. We have discussed this at transcript page 3263 whereby Mr Yapane advised that it was Mr Maladina whoauthorized him to make the change. A copy of the cheque, taken from Commission Document 694 will be Tendered Document OP 15. Mr Yapane had maintained that the payment to Kuntila Company No 35 (although shown as a consultancyfee in his cash books) was a loan to Mr Maladina. His answer as to the difference remains unsatisfactory. The same approach was also made in relation to the other two lots of K20,000.00, whereby one was paid toJR Creative Network and credited back into the account two weeks later. A copy of the cheque, taken from Commission Document 694 will be Tendered Document OP 16. The other lot of K20,000.00 was paid to a J. Louia, whom Mr Yapane said was his cousin brother. Thecheque was cashed. A copy of the cheque, taken from Commission Document 694 will be TenderedDocument OP 17. Mr Yapane had maintained that it was a loan, and not a consultancy fee as shown in the cash book. We would interpose that whether it was a loan or a consultancy fee, the fact is that money was paid by NPFprior to any refurbishment being done by Ken Yapane and Associates and that such money was later paidto recipients who had no relationship in regard to the NPF office refurbishment. It is also no coincidence that Mr Herman Leahy authorised this improper payment as he was onlydelegated an amount of K50,000.00 by the Board eighteen (18) days prior to his authorisation. It would beinteresting to find out who were the movers of such a Board resolution at the board meeting. It is our view that Mr Herman Leahy should be held accountable for this improper payment of K40,000.00where no work had been done. 4. ETS GROUP

A Cheque # 2349 dated 12/04/99 for K29,900.00 was paid to ETS Group for drawing up a DueDiligence report of Steamships Super Market at Waigani, in February 1999. Based on thatReport, NPF decided not to buy the said property.

The Finance Inspectors have concluded that the payment was in order and we do not intend toinvestigate any further.

5. MINAO SURVEYORS PTY LTD A total amount of K19,617.81 was paid to Minao Surveyors Pty Ltd with the particulars as follows:

The information is taken from Commission Document 1224 and copies of the documents willbe Tendered Document OP 18 to OP 22

6. SOGU WORKS PTY LTD A total amount of K9,858.40 was paid to Sogu Works Pty Ltd with the particulars as follows:

The information is taken from Commission Document 1225 and copies of the documents willbe Tendered Document OP 23 to OP 24.

7. NEC SECRETARIATE

On 2 September 1996, Hon. Chris Haiveta wrote to Mr Robert Kaul and requested a donationtowards payment of Singsing Groups who will be performing at an NEC Meeting in Vanimo.

A letter dated 6 September 1996 was faxed to Mr Kaul by a Paul Sosori, the Personal Assistantof the Office of Deputy Prime Minister and Minister for Finance Hon. Chris Haiveta.

The letter attached a list of Cultural/Singsing Groups as follows: 1. Schotiaho BankI. Yako VillageII. Waromo Catholic MamaIII. Lido VillageIV. Wesdeco Cultural GroupV. Palai GroupVI. Ningil GroupVII. Mushu VillageVIII. NGIIX. AmanabX. Green RiverXI. LimiXII. NukuXIII. AitapeXIV. TelefominXV. Wutung Mr Noel Wright, authorised the payment of K1,600.00 as per his handwritten note to the letter which reads:

"Please arrange a cash cheque (NEC Secretariate) for K1,600 and deliver to Paul Sosori –Vulupindi Haus".

It is signed by Mr Wright and dated 6/9/96. Ms Salome Dopeke then instructed Mr Simon Wanji to process the Cheque A.S.A.P and have it dropped offsame day as per her notation on the letter. That note also advised of the amount to be "charged toentertainment". The Cheque Requisition Form advised of a cheque in favour of NEC Secretariate as payment of donation toNEC members meeting to be held in Vanimo. A Cheque # 015472 dated 06/09/96 for K1,600.00 was signed by Mr Noel Wright and Ms Julie Sema. Mr Paul Sosori was the recipient of the cheque as evidenced by his signature. The above information is taken from Commission Document 1130 and copies of the documents will beTendered Document OP 25 to OP 29 respectively. B. DISPOSABLES 1. Kwila Table in Managing Director's Office.

A Kwila table was bought by NPF for the Managing Director's office in 1996 at a costof K2,122.00

The Capital Expenditure Report for the period ending 31 August 1996 which wasAppendix 2 of the Finance Report located in Commission Document 16 advised ofthe above.

A copy of Appendix 2 will be Tendered Document OP 30.

The Kwila table was put on tender as noted in Ms Salome Dopeke's memo to theManaging Director dated 23 September 1998.

The memo reads:

"I understand this table was put on tender sometime ago. To date we stillhave it sitting on the asset register.

Could you please inform us of the outcome so necessary adjustmentscan be made. For your action. Kind Regards."

Mr Fabila responded by his handwritten note dated 23/9 on the memo. It reads:

"This table was bought by Corp. Sec. After tender and he is presentlypaying it off in instalments. Therefore, it should be taken off the assetregister".

The memo is located in Commission Document 368 which is the NPF File onMemos In & Out 1997/1998 and a copy will be Tendered Document OP 31. The Fixed Asset Register as at 31 August 1998 showed that the Coffee table wasresold at K2000.00. A copy of page 3 of the Fixed Asset Register which shows the above and taken fromCommission Document 1243 will be Tendered Document OP 32 Mr Herman Leahy sought a Salary Advance of K2000.00 on 30 September 1998which was used to purchase the Kwila Table. The Salary Advance File and the 1998 Journal File showed that as of 31 August1998, the Kwila table had depreciated to the value of K334.00 and that there was aprofit of K212.00 on the eventual purchase by Mr Leahy. Copies of the relevant pages of the Salary Advance File and the 1998 Journal Filetaken from Commission Document 1243 will be Tendered OP 33 and OP 34.

Nothing is mentioned in the 1996 – 1999 Board Minutes. 2. RAFFLE OF TELEVISION AND VIDEO DECK

On 23 October 1998, the Managing Director, Mr Henry Fabila wrote a memo to allstaff regarding the raffling of the Television and video deck located in the NPF BoardRoom.

The letter reads:"RAFFLE OF TELEVISION AND VIDEO DECK

Please be informed that the TV and the Video Deck in the Board Roomwill be raffled to all the staff and the management.

The raffle tickets will be selling at K2.00 per ticket. The money made willgo towards the XMas party at the end of the year.The duration of selling of the raffle tickets will commence from 26 October1998 and the closing date will be 11 December. Drawing of the luckyticket will take place at the Staff Christmas party.

Accounts Section Staff – Simon and Ranu will be in charge of obtainingand selling the tickets and accounting for proceeds of sale.

There will be only one winner for the TV and the Video Deck.

Please observe the conditions of entry:

1. The prize must be taken as offered and is not redeemable.

2. Any ticket may be judged void if reported stolen, illegible, mutilated,altered, misprinted or defective in any manner. Liability for void tickets, ifay, is limited to replacement of ticket. No prize will be given for a voidticket.

3. Members of the public are not eligible to participate in this raffle andticket sold to any person other than a NPF employee is void.

4. The prize must be collected within 21 days from the date the winningticket is drawn otherwise it will be forfeited.5. In the event of any dispute the decision of the NPF Managing Directorwill be final and no correspondence will be entered into. All entriesbecome the property of the Fund.

Thank you".

The memo is located in Commission Document 355 (which is the ManagingDirector's Running File 1998/1999), and a copy will be Tendered Document OP 35.

We are unable to locate any records that could show how much was raised andwhether such proceeds were banked or not.

It would therefore seem that proceeds from the raffle of the TV and Video deck wereused for the said Christmas Party.

12. Procurement of stationery and office supplies Commission of Inquiry Opening Address Tenders / Nepotism

Introduction

This opening looks at the tender procedures and examines whether issues of nepotism exists atthe National Provident Fund of Papua New Guinea's ("NPF") in the procurement of stationeryand office supplies. In particular this opening seeks to identify whether there was any failure tocomply with tender procedures and whether such failure benefited any person and whetherthere was any conflict of interest in the procurement of these services.

Delegations

It is important to state what financial delegation limits were set by the Trustees in the management of thefinances of the Fund. The Commission will recall how we have referred to these in earlier hearings, but atthis point it is relevant to restate briefly what these delegations were as recorded by the minutes. In the Managing Directors report for June 1993 which is found in Commission Document 370, Mr Kaulprovided the following regarding financial delegation:"It is apparent that there exists no financial delegation authority for management members. This delegation would beimportant in order to limit and control management use of finances of the Fund. It is recommended that the Boardapproved the attached schedule setting out the financial delegation levels.

This report has been tendered as Document H3.On 30 July 1993 at the 83rd Board Meeting (Commission Document 47) minutes record that the Boardresolved to accept the Managing Directors recommendation. These limits applied up until 8 February 1999.At the 117th Board meeting minutes held on 8 February 1999, which can be found in CommissionDocument 51 and has been tendered as document OS9, the Trustees resolved:

"…to delegate an amount of K50,000 to the Managing Director and the Corporate Secretaryrespectively. Any amounts in excess of K50,000 must be approved by the Chairman and signedfor by at least one other Trustee. No other members of management were delegated anyfinancial powers".

On 8 March 1999 a Special Board Meeting was held where the minutes record:

" The Managing Director was asked to comment on his request to increase the limit on hisfinancial delegation from the previously resolved K50,000 limit to K350,000.It was resolved to increase the limit on the Managing Director's financial delegation fromK50,000 to K100,000. It was further resolved that the Managing Director use his discretion toutilise his powers under section 18A (Delegation by the Managing Director) of the NPF Act todelegate to his subordinates any or all his powers and functions relating to this financialdelegation".

A copy of the minutes for this meeting can be found in Commission Document 51 and has been tenderedas Document OS10.

The Managing Director is empowered by the NPF Act and Rules to delegate his power.

Amounts recorded as per the financial statements

The financial statements of NPF record the following costs for stationery and office supplies for the years 1995 to2000:

As we can see in the period 1995 to 1998 the costs were reasonably constant but in 1999 there was aquantum leap in the cost incurred by the Fund. NPF have been unable to offer any specific explanation.There does not appear to be any obvious misallocation errors or charges to explain the increase. It is alsopertinent to note that stationery costs have returned to 'normal' levels in year 2000.We have reviewed the NPF Board papers and management reports to identify whether any reasons have

been put forward by the management to explain the increase in cost for the year ended 31 December 1999.Whilst we would expect an increase attributed to the general increase in costs in the country due to fallingexchange rate during 1999, the increase in stationery and office supplies costs can not be fully explained bysuch factors. This is clearly supported by the stationery and office supplies cost for the year 2000 where thecost has reduced to the expected level.The detailed break down of the expense are shown by the detailed profit and loss accounts found in theabove noted Commission Documents will be tendered as document NS1.

Summary of Suppliers used between 1 January 1995 to 31 December 1999

We have obtained a list of the payments made by NPF between 1 January 1995 and 31 December 1999 inrespect of purchase of stationery and office supplies. This list is found in Commission Document 1233and will be tendered as document NS2. The total paid to these supplies over this period is as follows:

It is worthy of note that of the top ten (10) suppliers listed according to total amount paid shown above, onlyfour (4) are commonly recognised suppliers. These four are Moore Business Systems, Remington, Oceania(PNG) Limited and Huon Litho Press P/L.

Accounting and Controls over stationery and office supply expenditure

The special investigation performed by the Finance Department Inspectors included an audit of the processover procurement, recording and payment of operational and administrative expenses. A copy of theFinance Department Inspectors' report is found in Commission Document 4A. The report uncoverednumerous procedural irregularities and weaknesses. The same was also found by the Auditor General inhis audit of the financial statements of the Fund for the years ended 31 December 1998 and 1999.These reports highlight the existence of a weak internal control environment. In such a weak environmentvoid of proper checks and balances, the risk of fraud, theft and error increases, particularly with respect tothose perpetuated by management or staff.Whilst we do not wish to reperform the work performed by the Auditor General and the Finance Inspectors,there are sufficient concerns about the high level of stationery costs in 1999 to require us to examinespecific payments to selected suppliers and summarise our findings. In order to do this we have used thetwo reports mentioned and isolated payments made to certain suppliers biased to those where we notethere are matters of concern. Namely changes in buying patterns, and the purchases of stationery fromrelated entities. In choosing the payments to review we have also considered other factors such asrelationship of the supplier to employees of the Fund.Details of work done and our findings are as follows:

Staff / Qualification

The accounting staff of NPF in the accounts payable section during the period 1 January 1995 to 31 December 1999and their relevant educational qualification and experience are as follows:

Officer In Charge of NPF Accounting Department, Mrs Dili Tarua (Commission Document 1229 to betendered as document NS3). As Finance Manager Mr Wright was ultimately responsible for the establishment and monitoring of properprocedures and controls in the area of procurement, recording and payment of stationery and officesupplies. From his resignation on 7 January 1999, Ms Dopeke took over the responsibility of FinanceManager until her termination in February 2000. Mr Wanji's promotion to officer in charge of the accounts payable section occurred before 1995. In theperiod under review, Mr Wanji and Mrs Tamarua were the only staff in the accounts payable section until inJune 1999 where Mrs Ure replaced Mrs Tamarua.

The State of controls over procurement, recording and payments – 1995 to 1999