communicating monetary policy intentions - the case of norges bank amund holmsen 16 may 2009 (with...

TRANSCRIPT

Communicating Monetary Policy Intentions - the Case of Norges Bank

Amund Holmsen16 May 2009

(with Jan F. Qvigstad, Øistein Røisland and Kristin Solberg-Johansen)

Overview

1. What do we communicate?

2. Interest rate forecasts four years on – a review of pros and cons

3. Challenges

Conclusion

It seems to work well in Norway.

Talking about the future…

“…strong vigilance is therefore of the essence...”(Trichet,

August 2007)

“...and anticipates that economic conditions are likely to warrant exceptionally low levels of the federal funds rate for an extended period."

(FED, April 2009)

“...the target overnight rate can be expected to remain at its current level until the end of the second quarter of 2010...”

(BoC, April 2009)

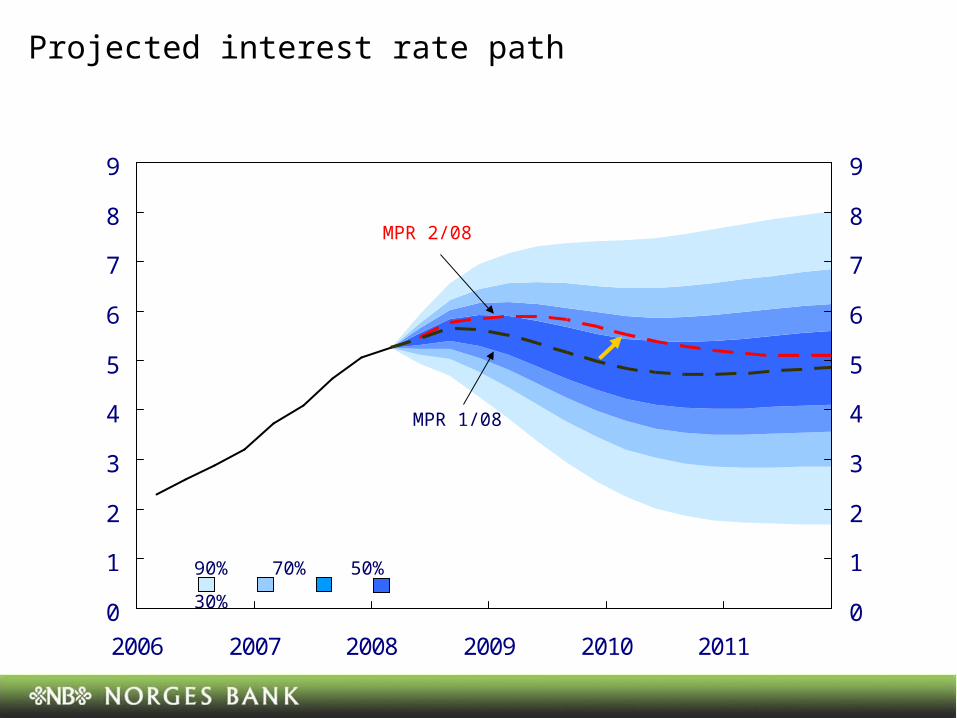

Changes in Norges Bank’s interest rate assumption

2001 - 2002 Constant interest rate

2003 - 2005 Markets’ interest rate expectations …with comments

2005 Our own interest rate forecast

0

1

2

3

4

5

2006 2007 2008 2009 2010 20110

1

2

3

4

5

-3

-2

-1

0

1

2

3

4

5

2006 2007 2008 2009 2010 2011-3

-2

-1

0

1

2

3

4

5

0123456789

2006 2007 2008 2009 2010 20110123456789

0

1

2

3

4

5

6

7

2006 2007 2008 2009 2010 20110

1

2

3

4

5

6

7

90%

70%

50%

30%

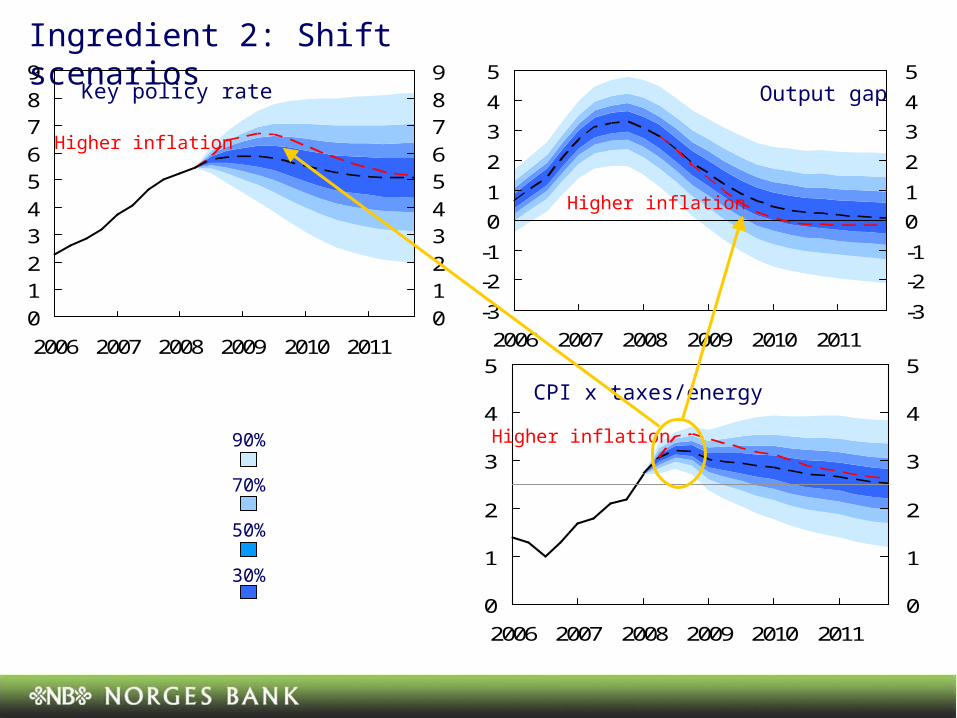

Ingredient 1: Baseline scenario (MPR 2/08) Output gap

CPI excl taxes and energy

CPI

Key policy rate

90%

70%

50%

30%

Ingredient 2: Shift scenarios

0123456789

2006 2007 2008 2009 2010 20110123456789

Key policy rate

-3

-2

-1

0

1

2

3

4

5

2006 2007 2008 2009 2010 2011-3

-2

-1

0

1

2

3

4

5Output gap

0

1

2

3

4

5

2006 2007 2008 2009 2010 20110

1

2

3

4

5

CPI x taxes/energy

Higher inflation

Higher inflation

Higher inflation

0

1

2

3

4

5

6

7

8

9

2006 2007 2008 2009 2010 2011

0

1

2

3

4

5

6

7

8

9

MPR 1/08

MPR 2/08

90% 70% 50% 30%

Projected interest rate path

Ingredient 3: Delta accounting of the interest rate path

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

08 Q3 09 Q1 09 Q3 10 Q1 10 Q3 11 Q1 11 Q3

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

Higher demand in NorwayHigher inflation in NorwayHigher interest rates abroadHigher risk premium in the money marketLower growth abroadChanges in the interest rate path

Pros and cons – revisited

Reviewing some counter-arguments

Is conditionality misunderstood?

Are policy makers constrained?

Is it possible to decide on a whole path?

0

1

2

3

4

5

6

7

8

2005 2006 2007 2008 2009 2010 2011 2012

The yield curve moves on economic news

Implied forward rates after previous report

Norges Bank forecast

Key policy rate

Implied forward rates day before reportNorges Bank forecast in the previous report

July 2008

Reviewing some counter-arguments

Is conditionality misunderstood?

Are policy makers constrained?

Is it possible to decide on a whole path?

Interest rate forecasts with fan chart from MPR

3/2008 Percent

90%70%50%30%

Reviewing some counter-arguments

Is conditionality misunderstood?

Are policy makers constrained?

Is it possible to decide on a whole path?

Reviewing some pro-arguments

Is the reaction function better anchored?

Test 1: Are market rates reasonably aligned with our forecast?

Test 2: Are there smaller jumps in market rates around policy announcements?

a) November 2005

012345678

2006 2007 2008 2009012345678

012345678

2006 2007 2008 2009012345678

012345678

2006 2007 2008 2009 2010012345678

Baseline scenario

Forward rates

b) June 2006

012345678

2007 2008 2009012345678

c) June 2007 d) March 2008

Baseline scenario

Forward rates

Baseline scenario

Forward rates

Baseline scenario

Forward rates

0

10

20

30

40

50

60

70

4.4.01 27.2.02 22.1.03 28.1.04 15.12.04 2.11.05 27.9.06 15.8.07 25.6.08

Change in 12-month LIBOR krone rate from the day of a policy announcement to the following day, and averages for the two periods. Basis points.

Market rates as exogenous assumptions

Interest rate forecasts

Fewer misunderstandings

Easier to talk about the future Exit strategy as integrated part of the

communication

Credible interest rate forecast vs quantitative easing

Reviewing some more pro-arguments

Challenges

Modelling optimal monetary policy

Consistency Over time and accross states of the

economy

Alternative approaches

Simple interest rate rule

rt = rt-1 + (1-)[1(Ett+k-*)+2yt +3yt]

Optimal policy: Minimizing a loss function

L = (π - π*)2 + λy2 + δ(r - r-1)2

Simple rule

rt = rt-1 + (1-)[1(Ett+k-*)+2yt +3yt]

Two approaches Coefficients optimized over unconditional loss Coefficients optimized over conditional loss

We faced the “rules vs discretion” issue and had to take a stand!

-2

-1

0

1

2

3

2006 2007 2008 2009

-2

-1

0

1

2

3

Forward looking Taylor rule vs Timeless

0

1

2

3

4

5

6

7

2006 2007 2008 2009

0

1

2

3

4

5

6

7

0

1

2

3

2006 2007 2008 2009

0

1

2

3Inflation Output gap

Interest rate

Timeless

Timeless Timeless

MPR 2/2006

2k * 2 2t t k t k t k t k 1k 0

L E 0.3y 0.2(i i )

MPR 2/2006

MPR 2/2006

In 2006 we were able to reproduce our forward-

looking Taylor-rule forecast with optimal policy

under timeless perspective with the loss

function:

-2

-1

0

1

2

3

2006 2007 2008 2009 2010

-2

-1

0

1

2

3

Ramsey and Timeless (baseline scenario)

0

1

2

3

4

5

6

7

2006 2007 2008 2009 2010

0

1

2

3

4

5

6

7

0

1

2

3

2006 2007 2008 2009 2010

0

1

2

3

Ramsey

Timeless

RamseyRamsey

Output gap

Key policy rate

Timeless

Timeless

Inflation

-2

-1

0

1

2

3

2006 2007 2008 2009 2010

-2

-1

0

1

2

3

0

1

2

3

4

5

6

7

2006 2007 2008 2009 2010

0

1

2

3

4

5

6

7

0

1

2

3

2006 2007 2008 2009 2010

0

1

2

3

Timeless and Ramsey:- λ=0.30- Weight change in interest rate=0.2

Inflation Output gap

Key policy rateTimeless with different λ’s

λ=0.20

λ=0.20 λ=0.20

Baseline scenario

Baseline scenario

Baseline scenario

λ=0.40

λ=0.40λ=0.40

Current approach: Forecasts, alternative scenarios and ”interest rate account”

Publish loss function (Svensson)

Interest rate rule

Target criterion (Woodford&Giannoni) (π - π*) + θ(y-y-1)=0

Alternative approaches to commitment

The experience is good

The conditionality and the uncertainty in the forecast seem well understood

Monetary policy appears to have become more predictable

The policy discussion is brought closer to the research frontier

Still early. If nothing else – better economists

Conclusions

Communicating Monetary Policy Intentions - the Case of Norges Bank

Amund Holmsen16 May 2009

(with Jan F. Qvigstad, Øistein Røisland and Kristin Solberg-Johansen)