community association audit process deleon & stang, cpas and advisors allen p. deleon, cpa janet...

TRANSCRIPT

COMMUNITY ASSOCIATION AUDIT PROCESS

DeLeon & Stang, CPAs and Advisors

Allen P. DeLeon, CPA

Janet Gorden, CPA

LUNCH-N-LEARN

Speaker biography – Allen P. DeLeon, CPA

Partner with DeLeon & Stang, CPAs and Advisors

Over 25 years community association auditing experience

Member of the Community Association Institute (CAI)

Chair of the Maryland Association of CPAs

Speaker biography – Janet Gorden, CPA

Senior auditor with DeLeon & Stang Over five years community association

auditing experience Member of the Community Association

Institute (CAI)

Agenda

Introduction Overview of community association audit

process Engagement and audit planning Audit fieldwork Concluding the audit Audit reports Board approval and other issues

WHAT DO YOU THINK AN AUDIT IS?

List your ideas.

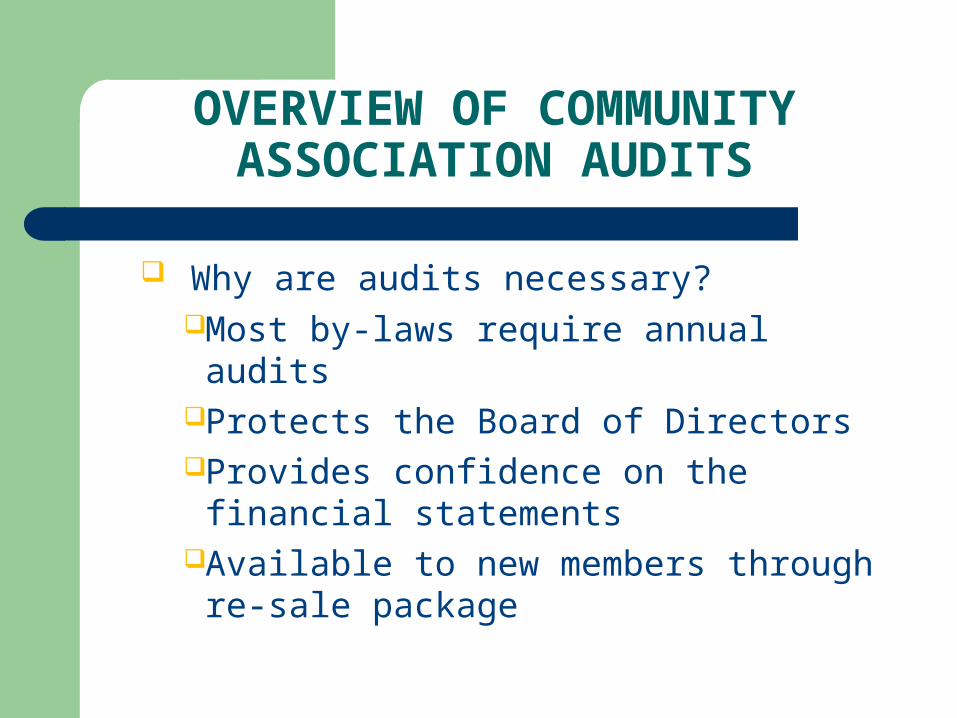

OVERVIEW OF COMMUNITY ASSOCIATION AUDITS

Why are audits necessary?Most by-laws require annual auditsProtects the Board of DirectorsProvides confidence on the financial

statementsAvailable to new members through re-

sale package

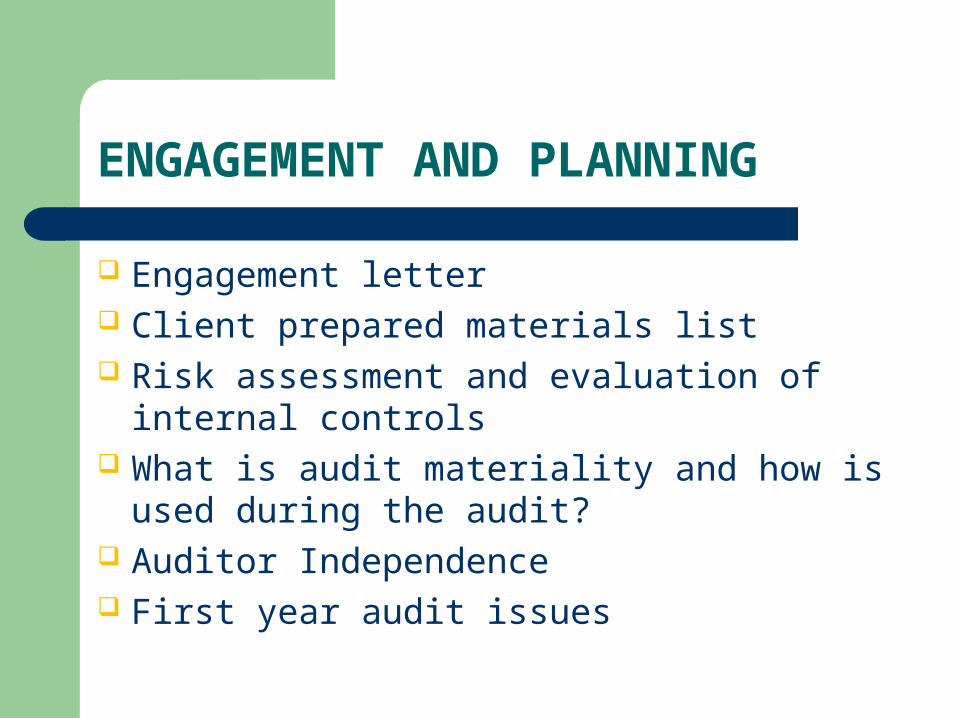

ENGAGEMENT AND PLANNING

Engagement letter Client prepared materials list Risk assessment and evaluation of internal

controls What is audit materiality and how is used

during the audit? Auditor Independence First year audit issues

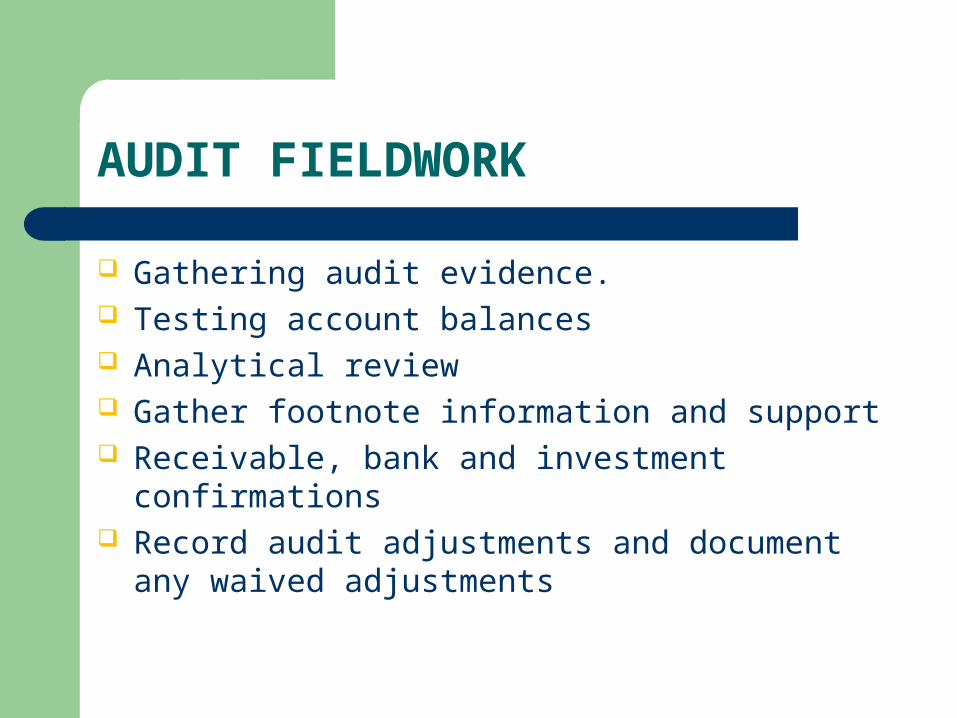

AUDIT FIELDWORK

Gathering audit evidence. Testing account balances Analytical review Gather footnote information and support Receivable, bank and investment confirmations Record audit adjustments and document any waived

adjustments

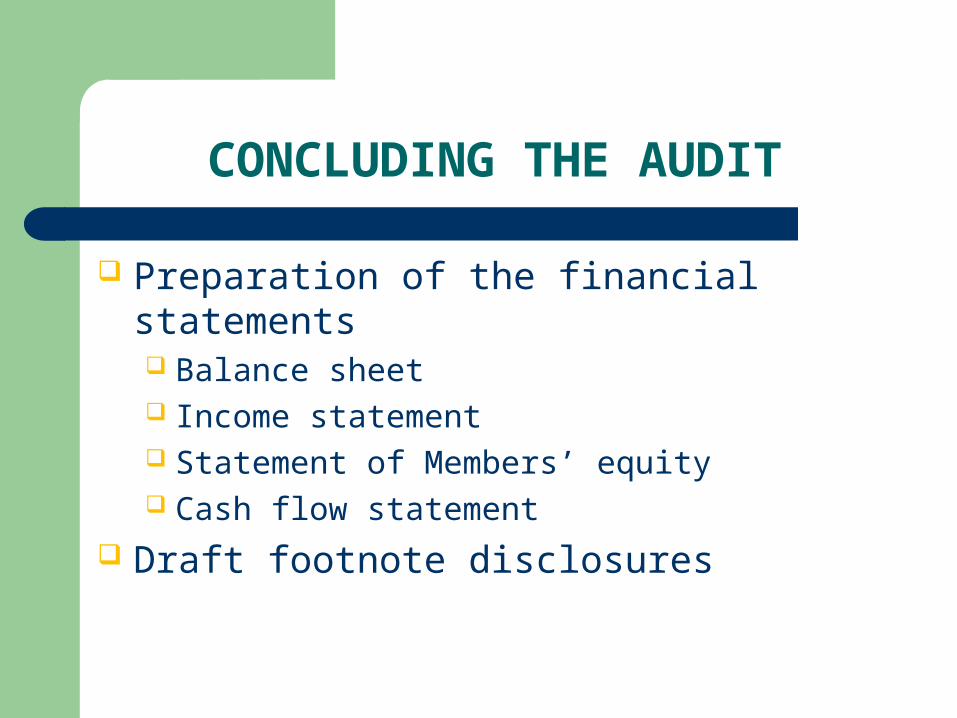

CONCLUDING THE AUDIT

Preparation of the financial statements Balance sheet Income statement Statement of Members’ equity Cash flow statement

Draft footnote disclosures

CONCLUDING THE AUDIT(continued)

Supplementary statements Replacement reserve fund Reserve study Budget to actual reports Commitments and contingencies Related party transactions Subsequent events

AUDIT REPORTS

Auditors’ Opinion & Financial statements SAS No. 115 letter with management

comments SAS No. 114 – communication from the

auditor Representation letter

AUDIT REPORTS (continued)

Different types of audit opinionsUnqualifiedExceptionDisclaimer

ADVICE TO BOARDS

Review the draft audit report and ask questions

Pay attention to the SAS No. 115 letter for significant control deficiencies or material weaknesses

Review audit adjustments and make sure they are recorded by management company

Sign representation letter within 60 days

RECENT AUDIT TRENDS

Allowance for bad debts and delinquent assessments receivable

Going concern Borrowing from replacement reserve fund Out of date replacement reserve studies Inadequate budgeting – resulting in operating

fund losses

RECENT AUDIT TRENDS (continued)

Books kept on cash basis Filing incorrect tax returns – 1120 vs. 1120H Not recording prior year audit adjustments Lack of fidelity insurance Not recording all year end accruals Not recording insurance claims

FUTURE ACCOUNTING AND AUDITING STANDARDS

Clarity project Going concern Private company accounting standards OCBOA accounting standards Review or compliation IFRS – merging US and International

accounting standards

QUESTIONS