company valuation and metrics – top down or bottom up?

TRANSCRIPT

Jeremy Halpern @startupboston Partner, Nutter McClennen & Fish

Paulina Hill @paulinahill Polaris Partners

Christopher Mirabile @cmirabile Launchpad Venture Group

TCN FastTrack – May 2014 Valuing an Early Stage Company

#TCNLive

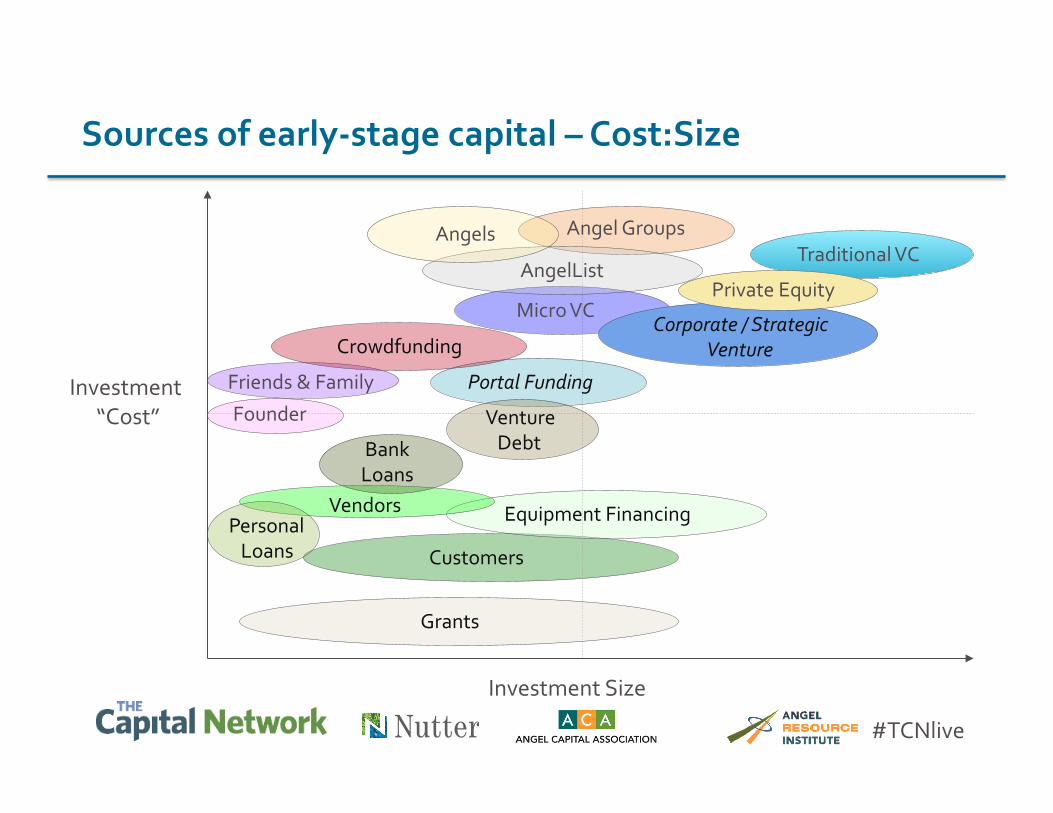

Sources of early-‐stage capital

• Bootstrapping – Founder’s capital and credit cards, bank lines of credit, loans (SBA)

• Equity Financing (Early) – Friends and family, crowdfunding, individual angels, organized angel

groups, early stage venture capitalists

• Equity Financing (Early to Later) – Venture capitalists, corporate venture funds, private equity firms,

hedge funds, and ultimately the public markets

2 #TCNlive

Investment Size

Investment “Cost”

Traditional VC

Micro VC

Equipment Financing

Angel Groups Angels

AngelList

Corporate / Strategic Venture

Customers

Portal Funding

Vendors

Founder

Friends & Family

Crowdfunding

Grants

Venture Debt Bank

Loans

Personal Loans

Private Equity

Sources of early-‐stage capital – Cost:Size

#TCNlive

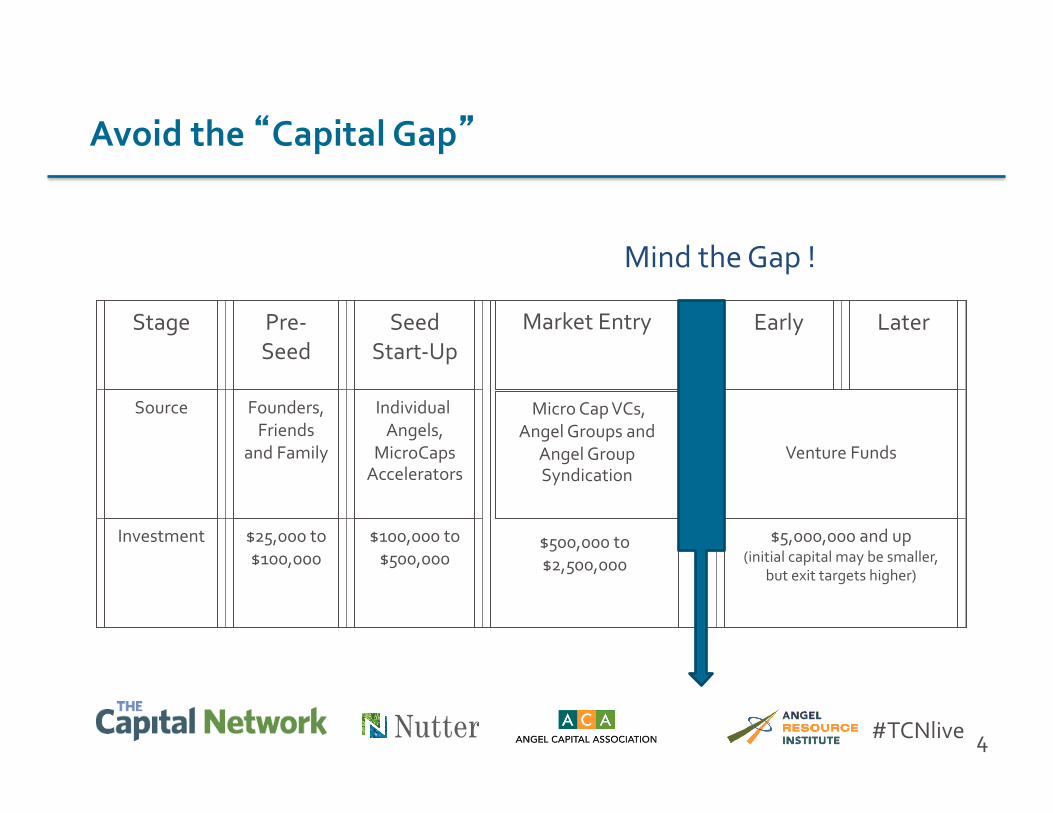

Avoid the “Capital Gap”

Stage Pre-‐Seed

Seed Start-‐Up

$500,000 to $2,500,000

Early Later

Source Founders, Friends

and Family

Individual Angels,

MicroCaps Accelerators

Venture Funds

Investment $25,000 to $100,000

$100,000 to $500,000

$5,000,000 and up (initial capital may be smaller,

but exit targets higher)

Market Entry

Micro Cap VCs, Angel Groups and

Angel Group Syndication

4

Mind the Gap !

#TCNlive

• Common Equity – Typical for Founders – Not typical for new, sophisticated investors – Restricted stock and Options

• Debt and Convertible Notes – Often used by early stage companies to avoid valuation – Not the best mechanism for aligning Founders and investors

• Preferred Equity – Primary mechanism for sophisticated angels, angel groups and VCs

5

Equity Investment Vehicles

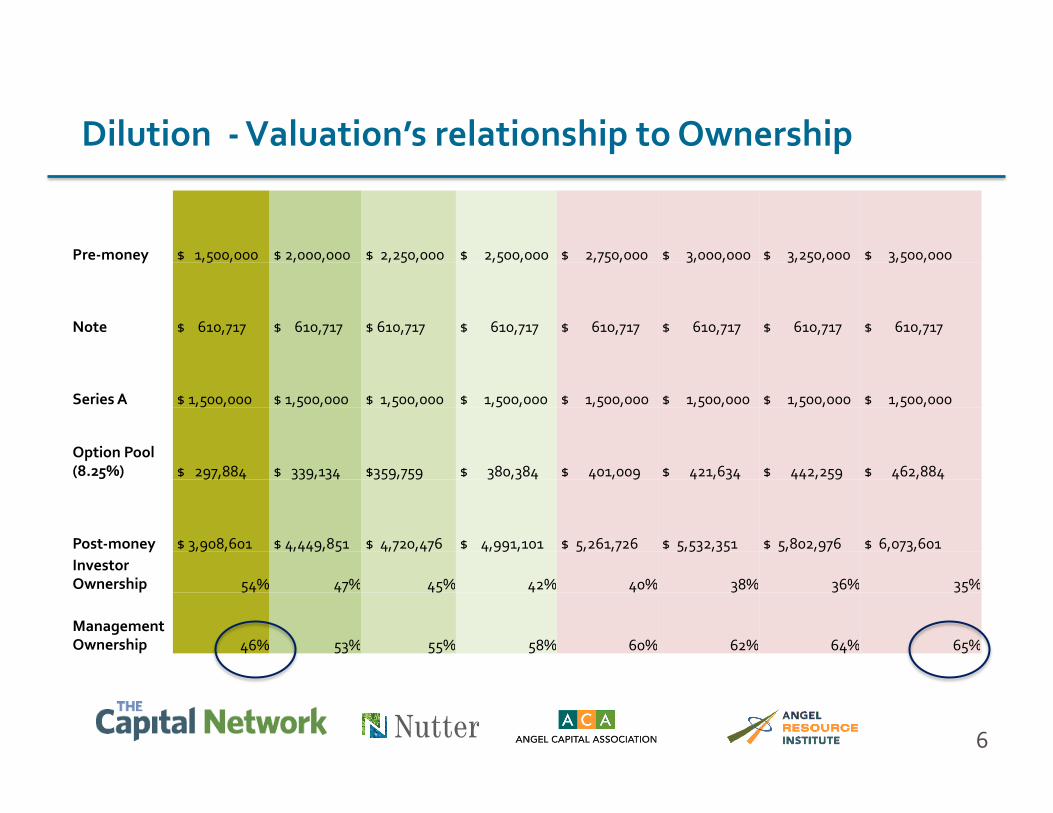

Pre-‐money $ 1,500,000 $ 2,000,000 $ 2,250,000 $ 2,500,000 $ 2,750,000 $ 3,000,000 $ 3,250,000 $ 3,500,000

Note $ 610,717 $ 610,717 $ 610,717 $ 610,717 $ 610,717 $ 610,717 $ 610,717 $ 610,717

Series A $ 1,500,000 $ 1,500,000 $ 1,500,000 $ 1,500,000 $ 1,500,000 $ 1,500,000 $ 1,500,000 $ 1,500,000

Option Pool (8.25%) $ 297,884 $ 339,134 $359,759 $ 380,384 $ 401,009 $ 421,634 $ 442,259 $ 462,884

Post-‐money $ 3,908,601 $ 4,449,851 $ 4,720,476 $ 4,991,101 $ 5,261,726 $ 5,532,351 $ 5,802,976 $ 6,073,601 Investor Ownership 54% 47% 45% 42% 40% 38% 36% 35%

Management Ownership 46% 53% 55% 58% 60% 62% 64% 65%

6

Dilution -‐ Valuation’s relationship to Ownership

Capital Needs

Time

High Risk

Low Risk

Crystallize Ideas

Demonstrate Product

Early Scaling Growth

Sustained Growth

Market Entry

• Raising money takes place over and over again because different lenders and investors match the current capital

amounts and risk profile

Risk vs. Return

#TCNlive

• Understand the capital needed today, and the total capital needed to get to milestones (e.g. exit!) – Type of business (e.g. SaaS, Medical Equipment)? – Cost of getting to market? – Cost of ramping and running the business?

• Compensate the management for getting to this point – What do they need for future motivation? – How many more senior people will be hired w/ options?

• Look at comparable exits to understand likely exit multiple – Don’t forget to account for invested capital!

• Is this a business investors can afford to invest in?

8

The Long View – Total Capital Requirements

#TCNlive

• Valuation Based on Measuring…. – Sales (Multiple of revenue –P/R) – Net Income (P/E) – Cash Flow (EBITDA or Free Cash Flow) – Discounted Cash Flow (DCF) – Discounted Future Earnings – Net Worth or Book Value – Real Options, Black Scholes, etc.

• NONE OF THESE APPLY TO STARTUPS!

9

Quantitative Methods – Valuing Mature Companies

#TCNlive

Valuation Issues

• Market Test & the Power of Auction: Leverage • Round size • Source (Angel, VC, Strategic etc.) • Total Capital Requirements • Terms vs. Pre-‐Money Price • Impact of Option Plans • Price less important than relationship • Positioning for future • Impact of Convertible Debt from F&F • On the “Promise” or the “Numbers” but not both!

Qualitative & Quantitative Factors

• COMPARABLES – Valuation of deals recently

completed in a similar space

• KEY ASSETS OF THE COMPANY – Management: Commitment

Knowledge & Experience – Intellectual Property &

Defensibility – Financials & Time to Profit – Milestones Achieved – Revenue – Customers and Feedback – Barriers to Entry

• FINANCING HISTORY / NEEDS – Funding to Date – Future Funding Needs – Last Round Post-‐Money Valuation – When was last round completed – Is the stock option pool sufficient

• SIZE AND GROWTH OF MARKET – Current Size & Targeted Market

• NOT the Total Available Market – Growth -‐ CAGR

11 #TCNlive

Early Stage Company Valuation Methodologies

• Venture Capital Method (used also by many angels) – Future revenue x industry multiple x pro rata percentage x IRR = current value

• Discounted Hypothetical Cash Flow / Net Present Value – Based on fiction

• Chicago (DCF x probability tiers) – Same issue as above

• Berkus (finger in the air) – Maximums per attribute (max $2.5m)

• OTA/Payne – Comparison to average x weight – Helpful for biotech/cleantech

• Risk Factor Method – Highly subjective – a more detailed version of Berkus Method

• Opportunity Cost / Contribution Model – Based on sweat and lost alternative revenue

• 1/3 Max rule – Treats angels like co-‐founders and weight cash versus sweat

• Transaction Comparables – Hard to find like deals; general market trends may apply

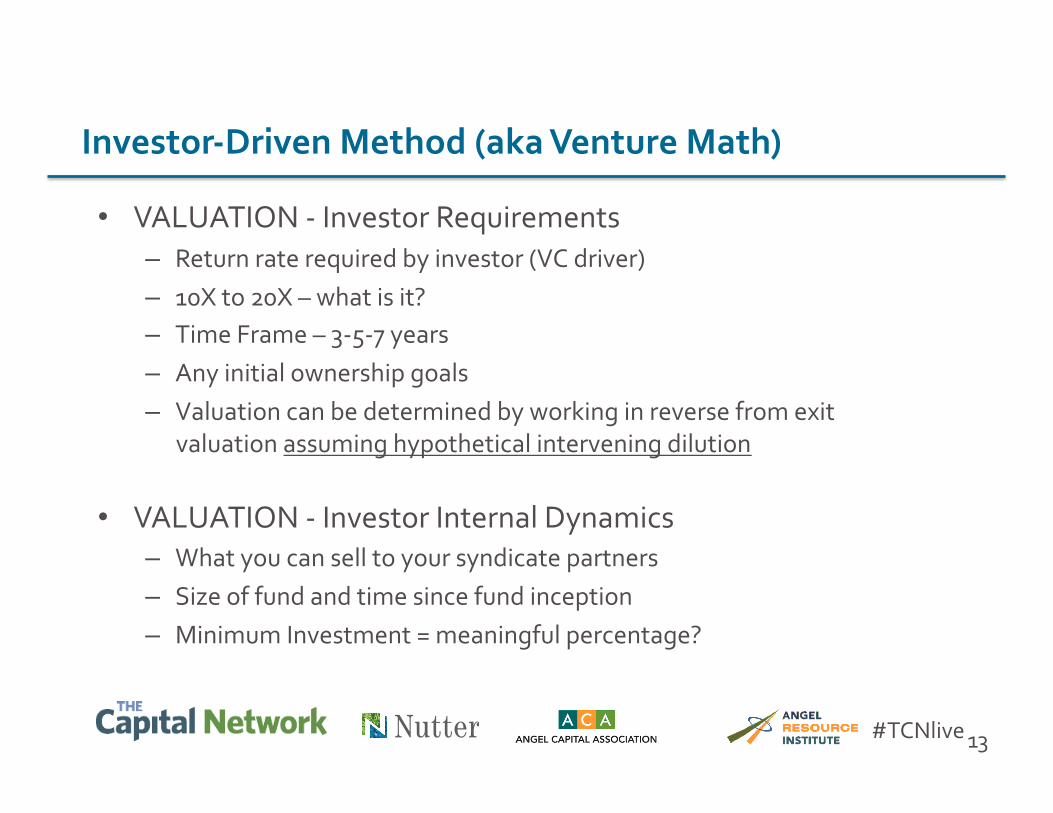

Investor-‐Driven Method (aka Venture Math)

• VALUATION -‐ Investor Requirements – Return rate required by investor (VC driver) – 10X to 20X – what is it? – Time Frame – 3-‐5-‐7 years – Any initial ownership goals – Valuation can be determined by working in reverse from exit

valuation assuming hypothetical intervening dilution

• VALUATION -‐ Investor Internal Dynamics – What you can sell to your syndicate partners – Size of fund and time since fund inception – Minimum Investment = meaningful percentage?

13 #TCNlive

Dave Berkus Method

If it exists, then Add to Company value Sound idea $500k Prototype $500k Quality Team $500k Quality Board $500k Initial Sale $500k Valuation Range = $0 -‐ $2.5 million

14 #TCNlive

Bill Payne Method

Factor Weight Rating (100% basis) Comment Management 30 125 On board, ex sales Size of Opportunity 25 115 Could be huge Product/Service 10 110 Disruptive platform Sales Channels 10 70 All foreign Stage of Business 10 125 Prototype works Other 15 80 All revs outside US

100%

Weighted Average Rating = 1.0875 Pre-‐revenue Multiplier = $1.75 million

Valuation = 1.0875 x $1.75 million = $1,903,125

15 #TCNlive

Risk Factor Summation Method (same company) Baseline $1.75 million Risk Factor Adjustment (-‐$500k to +$500k) Comment Management +$500k Done it before Stage +$250k Prototype works Funding Risk -‐$250k Int’l mkts tough Regulatory 0 Unregulated mkt Manufacturing +250k Nothing new Sales & Mktg -‐$500k Int’l mkts Competition +$250k Few in target mkt

Technology +$250k Off shelf parts Litigation 0 None expected International -‐$500k All revs Int’l Reputational -‐$250k Int’l issues Exit +$250k Likely early

$250k Valuation = $2.0 million

16 #TCNlive

Structure to allow value growth over time

• Underlying Assumption – All business is a risk adjusted cash flow – Structuring a deal is “guessing” what the exit valuation will be

• Valuation is a “Black Art” – Goal is to quantify a qualitative assessment, and then…. – Negotiate the deal so that everyone feels just a bit unhappy

• Setting Deal Structure – MUST understand total capital requirements and likely capital sources – Need to understand option pool needs – Other economic terms include: liquidation preference, dividends, anti-‐

dilution adjustment and vesting of founder’s stock and option pool

GOAL: Founders, Management, Early Investors and Later Investors all have great risk adjusted returns

17 #TCNlive

Angel Round Sizes Remain Steady Over Three-‐Year Period

$0.00

$0.50

$1.00

2011 2012 2013

Median Round Size Mean Round Size

*Angel rounds include angels & angel groups only

$950K $857K $931K

$610K $600K $600K

$M

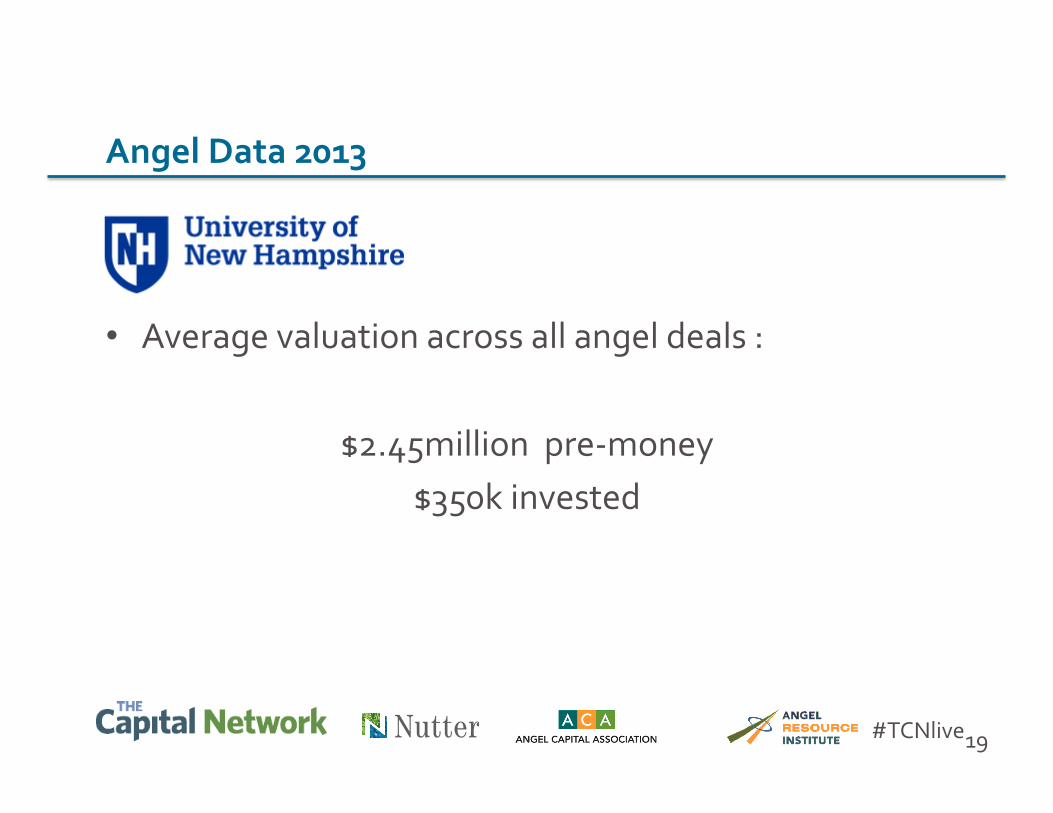

• Average valuation across all angel deals :

$2.45million pre-‐money $350k invested

19

Angel Data 2013

#TCNlive

20

The average pre-‐money valuation for a pre-‐revenue company across the US is $2.1 million

Average Valuations -‐ Wisdom of the Angel Crowd

#TCNlive

TCN FastTrack

May 2014 Valuing an Early Stage Company

Jeremy Halpern Nutter McClennen & Fish @startupboston [email protected] 617.439.2943

Paulina Hill Polaris Partners @paulinahill

Christopher Mirabile Launchpad Venture Group @cmirabile