(company’s full name) (company’s address) (telephone · pdf file(company’s...

TRANSCRIPT

Phil SEC 17Q 3Q 2005 1

SEC Number 1177 File Number ____

GLOBE TELECOM, INC. (Company’s Full Name)

5th Floor Globe Telecom Plaza (Pioneer Highlands) Pioneer corner Madison Streets, 1552 Mandaluyong City

(Company’s Address)

(632) 730-2000 (Telephone Numbers)

30 September 2005 (Quarter Ending)

SEC FORM 17-Q (Form Type)

Phil SEC 17Q 3Q 2005 2

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17(2)(b) THEREUNDER

1. For the quarterly period ended 30 September 2005 2. Commission identification number: 1177 3. BIR Tax Identification No. 000-768-480-000 4. Exact name of registrant as specified in its charter: GLOBE TELECOM, INC. 5. Province, country or other jurisdiction of incorporation or organization: PHILIPPINES 7. Address of registrant’s principal office: 5th Floor, Globe Telecom Plaza (Pioneer Highlands) Pioneer corner Madison Streets 1552 Mandaluyong City 8. Registrant’s telephone number, including area code: (632) 730-2000 10. Securities registered pursuant to Sections in Securities Regulation Code Number of shares of stock Title of each class outstanding Common Stock, P50.00 par value 131,899,148 Preferred Stock, P5.00 par value 158,515,021 11. Are any or all of the Securities listed on the Philippine Stock Exchange? Yes 12. Indicate whether the registrant:

a) Has filed all reports required to be filed by Section 17 of the Code and SRC Rule 17 thereunder or Sections 11 of the SRC and SRC Rule 11(a)-1 thereunder, and Sections 26 and 141 of the Corporation Code of the Philippines, during the preceding 12 months (or for such shorter period the registrant was required to file such reports). Yes

b) Has been subject to such filing requirements for the past 90 days. Yes PART I -- FINANCIAL INFORMATION Item 1. Financial Statements. Please refer to Annex A.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

As of and for the period ended 30 September

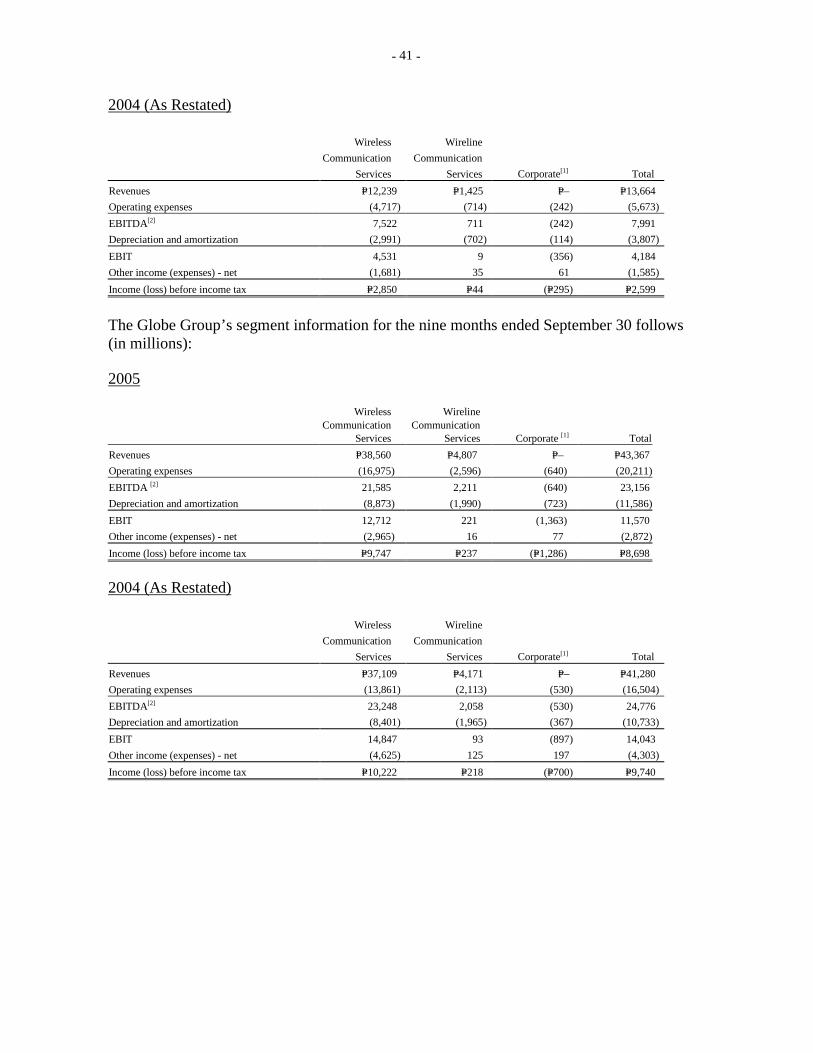

Financial and Operational Highlights (In Million Pesos unless otherwise stated) Globe Consolidated As of and for the nine months ended 30 September (Unaudited) 2005 2004 YoY change (%)

(As restated) 1 Profit & Loss Data Net Operating Revenues ………………………………………………… 43,367 41,280 5%

Service Revenues …………………………………………………… 40,268 39,094 3%

Non-Service Revenues 2 ……………………………………………. 3,099 2,186 42% Costs and Expenses ……………………………………………………. 34,669 31,539 10% Cost of Sales………………………………………………………… 5,034 4,964 1% Operating Expenses 3…………………………………………………. 15,177 11,539 32% Depreciation and Amortization……………………………………… 11,586 10,733 8% Financing…………………………………………………………….. 3,146 4,652 -32% Others - net………………………………………………………… (274) (349) 21% EBITDA4 ………………………………………………………………. 23,156 24,777 -7% EBIT5 …………………………………………………………………… 11,570 14,043 -18% Net Income ………………………………………….…………………. 6,440 8,997 -28% Balance Sheet Data Total Assets ……………………………………………………………. 124,749 127,244 -2% Total Debt ……………………………………………………………… 52,909 52,075 2% Total Stockholders’ Equity ……………………………………………. 47,742 52,080 -8% Financial Ratios (x) Total Debt to EBITDA …………………………………………………. 1.71 1.58 Interest Cover (Gross) ………………………………………………. …. 6.40 7.43 Debt to Equity (Gross) …………………………………………………. 1.11 1.00 Debt to Equity (Net) 6…………………………………………………… 0.90 0.76 Total Debt to Total Capitalization (Book) ……………………………… 0.53 0.50 Total Debt to Total Capitalization (Market) ...…………………………. 0.35 0.25 Other Data Net Cash from Operating Activities ……………………………………. 20,388 19,659 4% Capital Expenditures 7…………………………………………………… 12,095 16,025 -25% Net Receivable Days ……………………………………………………. 54 49 10% Peso/Dollar Exchange Rate (In pesos) ………………………………….. 55.977 56.276 -1% No. of Regular Employees ………………………………………………. 5,071 4,746 7%

_____________________________________________________________ 1 Prior period figures have been restated due to the adoption of various Philippine Accounting Standards (PAS) and Philippine Financial Reporting

Standards (PFRS) on 1 January 2005. (See related discussion in the attached financial statements)

2 Non-Service Revenues include proceeds from sale of handsets, phonekits, accessories, upfront fees/activation fees representing the excess of the selling price of SIM packs over the preloaded airtime. The costs related to the sale of handsets, phonekits, and accessories are shown under Cost of Sales. The difference between non-service revenues and cost of sales is referred to as Subsidy.

3 Operating expenses, among others, include provisions (reversals of provisions) for doubtful accounts, Inventory losses, obsolescence and market decline and losses on property and equipment and other probable losses.

4 EBITDA is defined as earnings before interest, taxes, depreciation, Amortization and other income/expense. EBITDA is calculated by deducting Cost of Sales and Operating Expenses from net operating revenues.

5 EBIT is defined as earnings before interest, other expenses and income taxes. EBIT is calculated by deducting depreciation and amortization from EBITDA.

6 Net debt is calculated by subtracting cash, cash equivalents and short term investments from total debt.

7 Consolidated capital expenditures include property and equipment, acquired as of report date regardless of whether payment has been made or not, but excludes capitalized costs during the period. (See related discussion in Liquidity and Capital Resources Section)

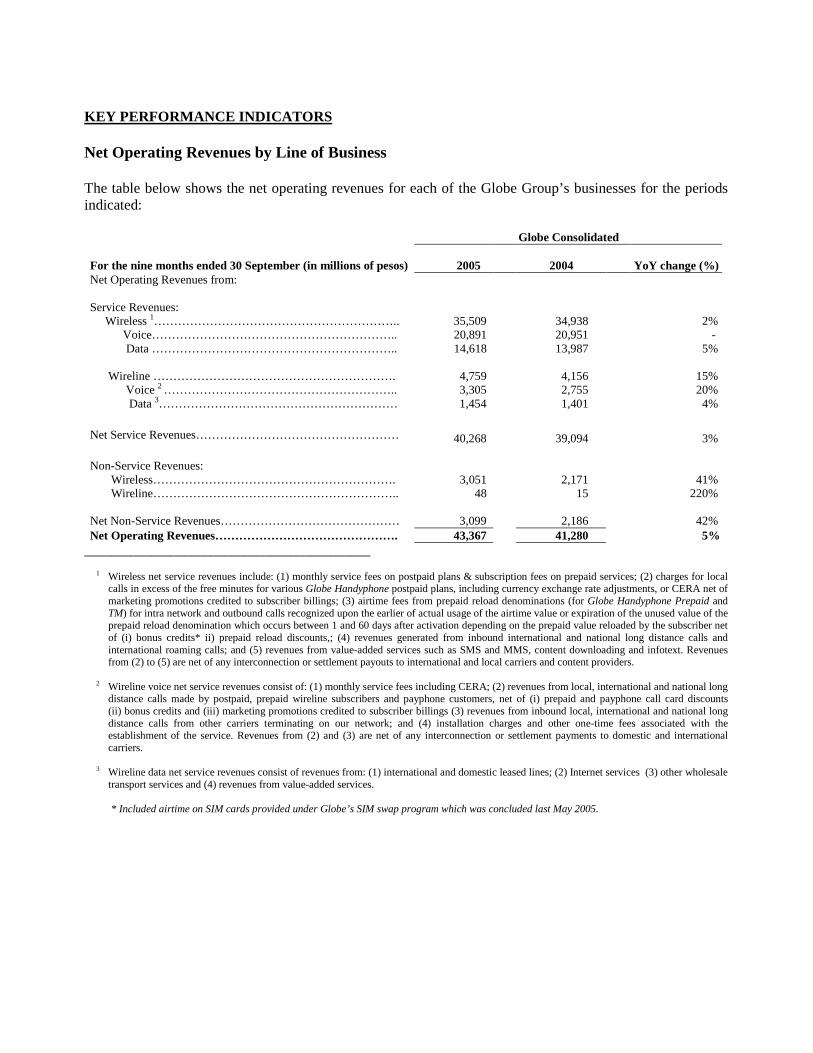

KEY PERFORMANCE INDICATORS Net Operating Revenues by Line of Business The table below shows the net operating revenues for each of the Globe Group’s businesses for the periods indicated: Globe Consolidated For the nine months ended 30 September (in millions of pesos) 2005 2004 YoY change (%) Net Operating Revenues from: Service Revenues: Wireless 1…………………………………………………….. 35,509 34,938 2% Voice…………………………………………………….. 20,891 20,951 - Data …………………………………………………….. 14,618 13,987 5% Wireline ……………………………………………………. 4,759 4,156 15% Voice 2 ………………………………………………….. 3,305 2,755 20% Data 3…………………………………………………… 1,454 1,401 4% Net Service Revenues…………………………………………… 40,268 39,094 3% Non-Service Revenues: Wireless……………………………………………………. 3,051 2,171 41% Wireline…………………………………………………….. 48 15 220% Net Non-Service Revenues……………………………………… 3,099 2,186 42% Net Operating Revenues………………………………………. 43,367 41,280 5%

___________________________________________ 1 Wireless net service revenues include: (1) monthly service fees on postpaid plans & subscription fees on prepaid services; (2) charges for local

calls in excess of the free minutes for various Globe Handyphone postpaid plans, including currency exchange rate adjustments, or CERA net of marketing promotions credited to subscriber billings; (3) airtime fees from prepaid reload denominations (for Globe Handyphone Prepaid and TM) for intra network and outbound calls recognized upon the earlier of actual usage of the airtime value or expiration of the unused value of the prepaid reload denomination which occurs between 1 and 60 days after activation depending on the prepaid value reloaded by the subscriber net of (i) bonus credits* ii) prepaid reload discounts,; (4) revenues generated from inbound international and national long distance calls and international roaming calls; and (5) revenues from value-added services such as SMS and MMS, content downloading and infotext. Revenues from (2) to (5) are net of any interconnection or settlement payouts to international and local carriers and content providers.

2 Wireline voice net service revenues consist of: (1) monthly service fees including CERA; (2) revenues from local, international and national long

distance calls made by postpaid, prepaid wireline subscribers and payphone customers, net of (i) prepaid and payphone call card discounts (ii) bonus credits and (iii) marketing promotions credited to subscriber billings (3) revenues from inbound local, international and national long distance calls from other carriers terminating on our network; and (4) installation charges and other one-time fees associated with the establishment of the service. Revenues from (2) and (3) are net of any interconnection or settlement payments to domestic and international carriers.

3 Wireline data net service revenues consist of revenues from: (1) international and domestic leased lines; (2) Internet services (3) other wholesale

transport services and (4) revenues from value-added services. * Included airtime on SIM cards provided under Globe’s SIM swap program which was concluded last May 2005.

In the first nine months of 2005, the Globe Group’s (Globe Telecom, Inc., Innove Communications, Inc. and G-Xchange, Inc.) total net operating revenues improved by 5% to P43,367 million from P41,280 million for the same period in 2004 while total net service revenues increased by 3% to P40,268 million in 2005 from P39,094 million in 2004. Wireless service revenues in 2005, which accounted for 88% of net service revenues in 2005, grew by 2% year-on-year. Meanwhile, wireline service revenues added the remaining 12% to net service revenues in 2005 (from 11% for the same period in 2004). The wireline business grew its net service revenues by 15% to P4,759 million from the same period in 2004. Domestically, the Globe Group pays interconnection charges to other carriers for calls originating from its network terminating to other carriers’ networks and hauling charges for calls that pass through Globe’s network terminating in another network. Internationally, the Globe Group also incurs payouts for outbound international calls. These charges are based on a negotiated price per minute. The interconnection expenses paid as a percentage of gross service revenues for the nine months of 2004 and 2005 registered at 20%. The Globe Group also collects termination fees from local and foreign carriers whose calls terminate in Globe Group’s network. Effective 01 January 2004, as part of domestic interconnection agreements concluded in 2002, domestic calls terminating to wireless networks are charged a termination rate of P4.00 per minute (from P4.50 per minute in 2003) while calls terminating to wireline voice networks are charged a termination rate of P3.00 per minute (from P2.50 per minute in 2003). We registered non-service revenues of P3,099 million for the nine months of 2005, a 42% increase from the P2,186 million for the same period last year due mostly to higher year-on-year handset sales contributed by postpaid subscriber acquisitions. Non-service revenues are reported net of discounts on phonekits. The cost related to the sale of handsets and SIM (Subscriber Identification Module) packs are shown under cost of sales. The difference between non-service revenues and cost of sales is referred to as subsidy. Subsidy dropped by 30% in the nine months of 2005 to P1,935 million from P2,778 million for the same period in 2004 in line with the decline in gross subscriber additions following the end of the SIM swap activities last May 2005. Proceeds from the sale of prepaid cards airtime value through electronic load services such as ATM and airtime value through over-the-air (OTA) reloading are treated as deferred or unearned revenues are shown under the liabilities section of the balance sheet since the service has not yet been rendered. Revenue is realized upon actual usage of the airtime value (pre-loaded airtime value of SIM cards and subsequent top-ups) for voice, SMS, MMS, content downloading and infotext services net of free SMS, bonus credits* or the expiration of the unused value, whichever comes earlier. * Included airtime on SIM cards provided under Globe’s SIM swap program which was concluded last May 2005.

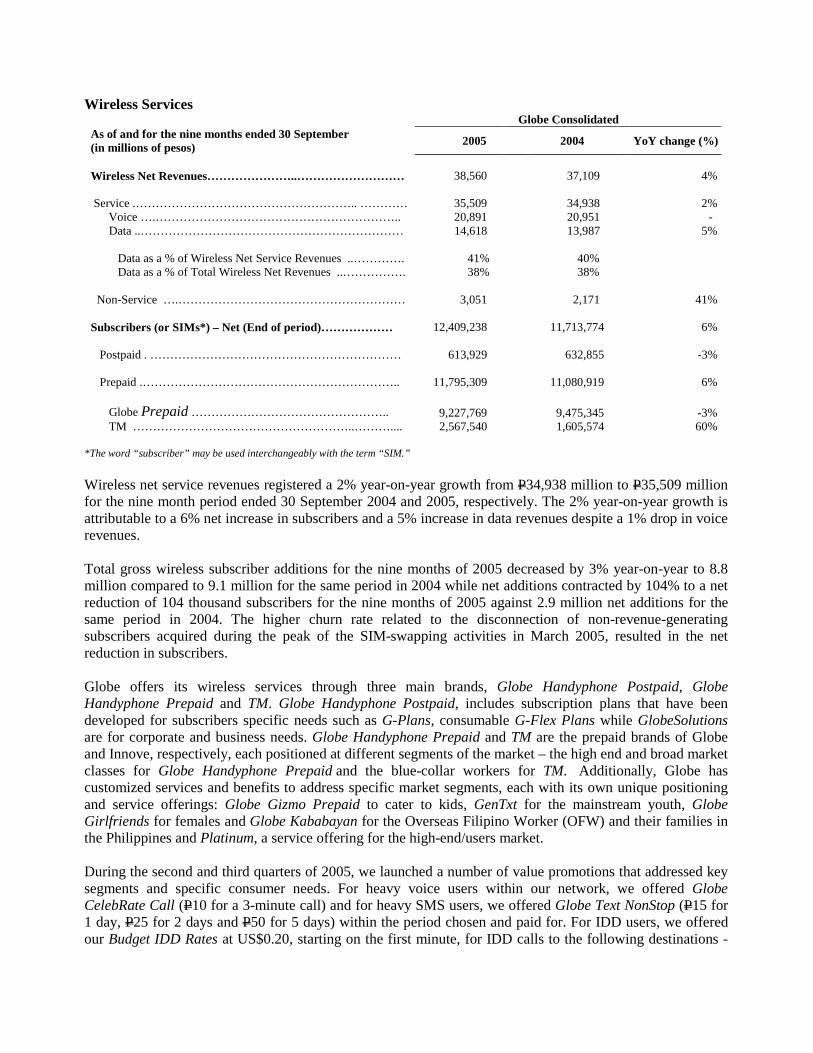

Wireless Services Globe Consolidated As of and for the nine months ended 30 September (in millions of pesos) 2005 2004 YoY change (%)

Wireless Net Revenues…………………..……………………… 38,560 37,109 4% Service .……………………………………………….. ………… 35,509 34,938 2% Voice ….…………………………………………………….. 20,891 20,951 - Data ..………………………………………………………… 14,618 13,987 5% Data as a % of Wireless Net Service Revenues ..…………. 41% 40% Data as a % of Total Wireless Net Revenues ..……………. 38% 38% Non-Service ….………………………………………………… 3,051 2,171 41% Subscribers (or SIMs*) – Net (End of period)……………… 12,409,238 11,713,774 6% Postpaid . ……………………………………………………… 613,929 632,855 -3% Prepaid .……………………………………………………….. 11,795,309 11,080,919 6% Globe Prepaid ………………………………………….. 9,227,769 9,475,345 -3% TM ………………………………………………..……….... 2,567,540 1,605,574 60%

*The word “subscriber” may be used interchangeably with the term “SIM.”

Wireless net service revenues registered a 2% year-on-year growth from P34,938 million to P35,509 million for the nine month period ended 30 September 2004 and 2005, respectively. The 2% year-on-year growth is attributable to a 6% net increase in subscribers and a 5% increase in data revenues despite a 1% drop in voice revenues. Total gross wireless subscriber additions for the nine months of 2005 decreased by 3% year-on-year to 8.8 million compared to 9.1 million for the same period in 2004 while net additions contracted by 104% to a net reduction of 104 thousand subscribers for the nine months of 2005 against 2.9 million net additions for the same period in 2004. The higher churn rate related to the disconnection of non-revenue-generating subscribers acquired during the peak of the SIM-swapping activities in March 2005, resulted in the net reduction in subscribers. Globe offers its wireless services through three main brands, Globe Handyphone Postpaid, Globe Handyphone Prepaid and TM. Globe Handyphone Postpaid, includes subscription plans that have been developed for subscribers specific needs such as G-Plans, consumable G-Flex Plans while GlobeSolutions are for corporate and business needs. Globe Handyphone Prepaid and TM are the prepaid brands of Globe and Innove, respectively, each positioned at different segments of the market – the high end and broad market classes for Globe Handyphone Prepaid and the blue-collar workers for TM. Additionally, Globe has customized services and benefits to address specific market segments, each with its own unique positioning and service offerings: Globe Gizmo Prepaid to cater to kids, GenTxt for the mainstream youth, Globe Girlfriends for females and Globe Kababayan for the Overseas Filipino Worker (OFW) and their families in the Philippines and Platinum, a service offering for the high-end/users market. During the second and third quarters of 2005, we launched a number of value promotions that addressed key segments and specific consumer needs. For heavy voice users within our network, we offered Globe CelebRate Call (P10 for a 3-minute call) and for heavy SMS users, we offered Globe Text NonStop (P15 for 1 day, P25 for 2 days and P50 for 5 days) within the period chosen and paid for. For IDD users, we offered our Budget IDD Rates at US$0.20, starting on the first minute, for IDD calls to the following destinations -

US, Canada, China, Malaysia, Hong Kong, Singapore, Thailand, South Korea, Taiwan and Australia. Additionally, our TM brand continued its Todo Tawag 15/15 promotion (P15 for a 15 minute call) for heavy voice users and the Todo Text promotion (P10 unlimited text usage for 1 day) for SMS-heavy users. The following sections discuss the various key performance indicators of the wireless business on a per-brand basis, such as subscriber figures, gross and net ARPU (Average Revenue Per Unit), SAC (Subscriber Acquisition Costs) and churn, among others. Wireless Services - Postpaid Globe offers postpaid services through its brand Globe Handyphone. Globe’s postpaid subscriber base registered at 613,929 as of 30 September 2005, 3% lower compared to 632,855 posted in the same period last year as more than half of total terminations were company-initiated mostly on credit issues. Gross additions for the first nine months of 2005 registered at 163,795 subscribers, higher by 41% than the 116,234 generated for the same period in 2004 due mainly to subscriber acquisition campaigns and promotions. The average monthly churn rate for Globe’s postpaid subscribers is defined as total disconnections net of reconnections divided by the average postpaid subscribers, divided by the number of months in the period. Globe’s postpaid churn rate averaged 3.2% per month for the nine months of 2005 compared to 2.8% for the same period in 2004 while quarter-on-quarter, it went up to 4.4% in the third quarter from 3.2% in the second quarter of 2005. For postpaid subscribers, permanent disconnections are made after a series of collection steps following non-payment. Such permanent disconnections generally occur within a predetermined number of days from statement date. Net postpaid reductions of 16,566 for the nine months of 2005 improved compared to the 52,171 net disconnections in the same period in 2004. Globe’s postpaid ARPU on a gross basis averaged P=2,187 for the nine months of 2005 from P=2,169 in the same period in 2004. On a quarterly basis, third quarter postpaid gross ARPU improved by 2% to P2,199 from P2,159 in the second quarter on account of fewer subscribers but higher voice traffic. Gross ARPU is computed by dividing recurring wireless postpaid gross service revenues for the period by the average number of postpaid wireless subscribers and then dividing the quotient by the number of months in the period. Net ARPU per Globe postpaid wireless subscriber for the nine months of 2005 registered at P=1,589, a 3% decline from P=1,641 for the same period in 2004 due to both lower voice and data usage for the period. Quarter-on-quarter, Globe postpaid net ARPU reached P1,588 for the third quarter from P1,550 in the second quarter. Net ARPU is computed by dividing recurring wireless postpaid net operating service revenues for the period (net of interconnection charges to external carriers and discounts) by the average number of postpaid wireless subscribers and then dividing the quotient by the number of months in the period. Globe’s postpaid SAC of P=7,490 for the nine months of 2005 is 28% lower than the P=10,462 registered for the same period last year as we lowered both handset subsidies and advertising costs. On a quarterly basis, postpaid SAC for the third quarter only reached P5,462 compared to P9,068 for the second quarter also due to lower handset subsidies and advertising costs. For the first nine months of 2005, handset and SIM subsidies accounted for 87% of acquisition cost while advertising/promotional expenses totaled 13%. These compared to 96% and 13%, respectively, in the comparable period in 2004.

Wireless Services - Prepaid Consolidated prepaid subscribers grew by 6% to 11,795,309 as of 30 September 2005 from 11,080,919 for the same period in 2004. Globe offers prepaid services through its Globe Handyphone Prepaid brand, while Innove offers prepaid services through its TM brand. Globe Handyphone Prepaid and TM subscribers can reload airtime value or credits from Globe Business Centers, accredited dealers/retailers, automated teller machines and via SMS using their mobile phones. Globe AutoloadMAX, an OTA reload channel offers the most affordable and flexible load credits from P10 to P150 in P1 increments for TM subscribers and P25 to P150 in P1 increments for Globe Handyphone Prepaid subscribers. Subscribers can also purchase Globe Prepaid Call and Text cards in P100, P300 and P500 denominations while TM Call and Text cards are available in P50, P100 and P300. A consumer to consumer top up facility, Share A Load, is also available which allows Globe Handyphone Prepaid and TM subscribers to share prepaid load credits among themselves in denominations of P1 to P150 (in P1 increment). Globe Handyphone Postpaid subscribers can also Share A Load to Globe Handyphone Prepaid and TM subscribers in P300 and P500 values in addition to the P1 to P150 denominations. During the first quarter of the year, Globe also launched G-Cash Load where subscribers can use G-Cash to load one’s phone or another Globe Handyphone or TM subscriber’s phone anytime by sending an SMS instruction. G-Cash registered users can likewise convert their G-Cash to prepaid load credits in denominations of P25 to P150 in P25 increments, P300 and P500. In February 2004, Globe launched a nationwide Free SIM-Swap program that allowed subscribers of another mobile network to switch to Globe by exchanging their active SIM cards for Globe Handyphone Prepaid or TM SIMs. Prior to the third quarter of 2004, a prepaid subscriber was recognized upon the activation and use of a new SIM card. The subscriber was provided with 60 days (first expiry) to utilize the preloaded airtime value. If the subscriber did not reload prepaid credits within the first expiry period, the subscriber retained the use of the wireless number, but was entitled only to receive incoming voice calls and text messages for another 120 days (second expiry), except for the first reload of SIM-swappers that was required within only 30 days from the first expiry. However, if the subscriber did not reload prepaid credits within the second expiry period, the account would be permanently disconnected and considered part of churn. The first expiry periods of reloads vary depending on the denominations, ranging from 1 day for P10 to 60 days for P300 to P1,000 reloads. The second expiry is 120 days from the date of the first expiry. The first expiry is reset based on the longest expiry period among current and previous reloads. Under this policy, subscribers are included in the subscriber count until churned. Acknowledging the changing dynamics of the industry, Globe updated its policy in recognizing a subscriber in its total count based on the subscriber intent to use the service. Starting the third quarter of 2004, a SIM-swapper was only considered a subscriber upon making the first reload. Non-SIM swap subscribers or regular subscribers are recognized upon activation and use of a new SIM. Accordingly, subscribers not considered in the subscriber count were not considered as part of churn. The nationwide SIM-swap program was concluded last May 2005.

Globe Handyphone Prepaid Globe Handyphone Prepaid subscriber base for the nine months of 2005 declined by 3% to 9,227,769 from 9,475,345 from the same period in 2004. Gross additions for the nine months of 2005 were lower by 19% at 5,650,810 compared to 6,990,063 in 2004. Churn was also higher at 7.6% vs. 5.8%, which more than offset the gross additions for the period resulting in a net reduction of 957,385 subscribers for the nine months of 2005 compared to 2,802,332 net additions for the same period in 2004. (See related discussion below). Globe’s prepaid gross ARPU averaged P=368 for the nine months of 2005 compared to P=428 for the same period in 2004. On a quarterly basis, prepaid gross ARPU improved to P351 in the third quarter of 2005 from P340 during the second quarter on account of a lower subscriber base and slightly higher voice traffic. Gross ARPU is computed by dividing recurring wireless prepaid gross service revenues for the period by the average number of prepaid wireless subscribers and then dividing the quotient by the number of months in the period.

The net ARPU for Globe Handyphone Prepaid registered a year-on-year decrease of 17% to P=259 for the first nine months of 2005 from P=311 for the same period in 2004. On a quarterly basis, net ARPU was P255 in the third quarter compared to P232 in the second quarter. Net ARPU is computed by dividing recurring wireless prepaid net operating service revenues for the period (net of discounts and interconnection charges to external carriers) by the average number of prepaid wireless subscribers and then dividing the quotient by the number of months in the period. The average monthly churn rate for Globe Handyphone Prepaid subscribers registered at 7.6% for the first nine months of 2005, higher than the 5.8% posted for the nine months of 2004. The higher churn for the year was due to the termination of non-revenue subscribers. Non-revenue subscribers for Globe Handyphone Prepaid relates to subscribers acquired during SIM-swapping activities that were subsequently churned out after their second expiry. In addition, there were also non-revenue subscribers related to “trade scooping,” where large volumes of SIMs are purchased in order to take advantage of SIM-swap activities in the market. During the third quarter, 50% of Globe Handyphone Prepaid churn was contributed by the expiry of these non-revenue SIMs, 32% of which came from disconnections related to previous SIM-swap offers while the remaining 68% came from trade scooping activities. Another 4% was related to the immediate disconnection of ISR SIMs captured in our fraud monitoring system. As such, only 46% of the total churn for the quarter related to “normal churn.” Normal monthly churn rate for Globe Handyphone Prepaid was at 3.8%. The high churn rate is expected to continue until the end of the year as the non-revenue SIMs are disconnected after the lapse of their second expiry period, consistent with the Company’s churn policy. Despite continuous efforts to keep these SIMs in the network and encouraging them to reload, we estimate that another one million non-revenue SIMs may be disconnected from our network through the rest of the year. SAC for Globe Handyphone Prepaid remained at almost the same level of P=260 for the first nine months of 2005 from P=259 for the same period in 2004. Handset and SIM subsidies accounted for 41% (63% in 2004) of SAC while discounts and advertising costs comprised the balance of 59% (37% in 2004). Quarter-on-quarter, SAC increased to P301 in the third quarter from P285 in the second quarter due to higher commissions and subsidies from sales of discounted phonekits.

TM We relaunched TM in the first quarter of 2005 and as of 30 September 2005, TM contributed 21% to the total wireless subscriber base of the Globe group compared to 14% for the same period in 2004. Innove’s TM subscribers increased by 60% to 2,567,540 subscribers as of 30 September 2005 compared to 1,605,574 subscribers for the same period last year. Gross additions, for the first nine months of 2005, increased by 54% to 3,029,345 from 1,972,644 for the same period in 2004. These accounted for 34% of total wireless gross additions for the year versus a 22% contribution the previous year. Net additions were almost eight times higher, from 103,730 for the first nine months of 2004 to 869,216 for the same period this year. The improved subscriber net additions resulted mainly from the relaunch of the TM brand and the success of its acquisition and usage campaigns. The average monthly churn rate for TM registered at 11.3% for the first nine months of 2005 against 13.4% for the same period last year. TM’s churn in 2005 was affected by Globe-initiated terminations of TM SIMs found engaging in International Simple Resale (ISR) activities which are illegal in the Philippines. During the first nine months of 2005, terminations due to ISR activities accounted for 30% of total year-to-date churn. Excluding terminations due to ISR activities, the average monthly churn rate for the nine months of 2005 would be 7.9%. Because of early detection of this illegal usage and the immediate SIM disconnection, the impact to the Company’s financial performance was minimized. (See related discussion on ISR on pages 12 and 13) Year-on-year gross ARPU was likewise higher at P=346 for the nine months of 2005 compared to P=280 for the same period in 2004. On a quarterly basis, gross ARPU registered at P281 in the third quarter from P366 in the second quarter on account of the successful availment of the brand’s Todo Text and Todo Tawag promotions which lowered ARPU because of the lower bulk pricing rate but increased traffic significantly. In addition, the objective of increasing blue-collar worker consumer segment penetration was achieved as evidenced by the strong subscriber take-up. The net ARPU for TM for the nine months of 2005 was P=211 or 17% higher than the P=181 registered for the same period in 2004 driven largely by the increase in usage after the relaunch of the brand early this year. On a quarterly basis, net TM ARPU was P182 in the third quarter compared to P221 in the second quarter due to the temporary removal of P10 to P19 Autoload Max denominations while technical upgrades in the billing system were being undertaken. SAC per TM subscriber decreased by 36% year-on-year to P=101 for the nine months of 2005 compared to P=158 for the same period last year due to a reduction in SIM subsidies. Quarter-on-quarter, SAC per TM subscriber totalled P144 for the third quarter from P86 during the second quarter as a result of higher advertising costs during the period. Of the total acquisition cost for the nine months of 2005, handset and SIM subsidies accounted for 40% (80% in 2004), while discounts and advertising costs made up the balance of 60% (20% in 2004). G-Cash As of 30 September 2005, there were over 1,000,000 registered users of G-Cash generating more than P3 million in total daily transactions. These users can now use G-Cash to buy merchandise from 239 partner establishments with over 4,000 outlets nationwide including more than 200 international partner outlets in 15 countries.

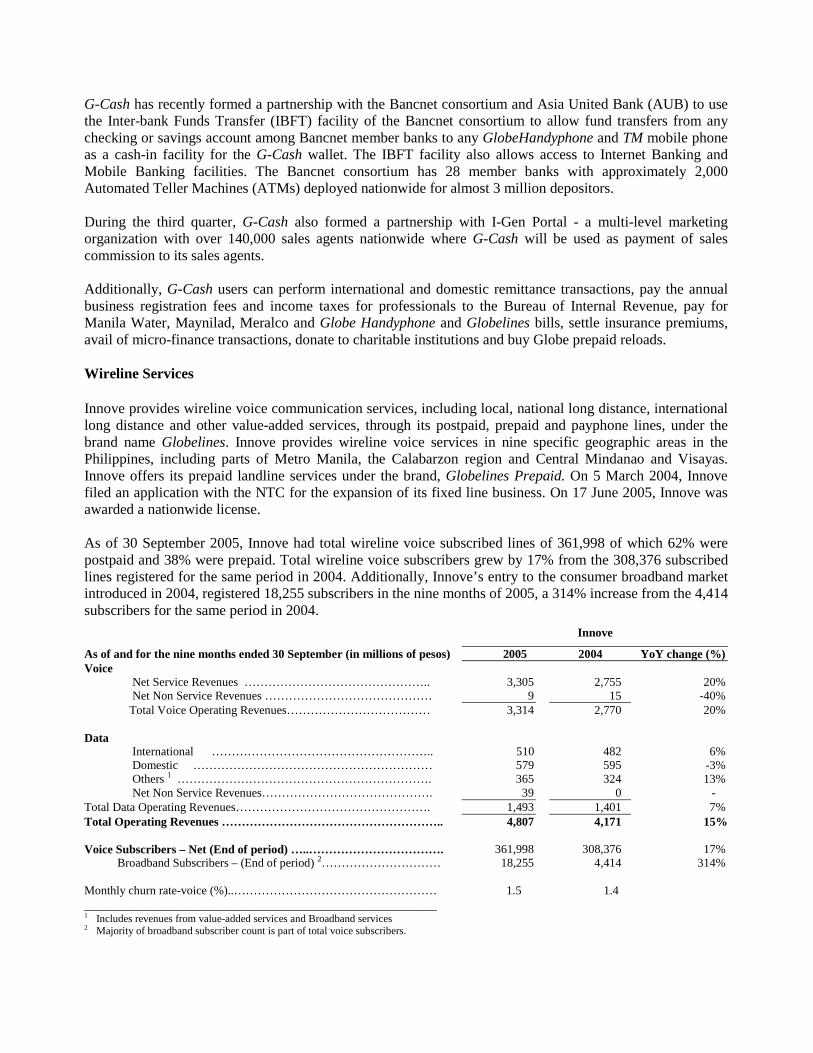

G-Cash has recently formed a partnership with the Bancnet consortium and Asia United Bank (AUB) to use the Inter-bank Funds Transfer (IBFT) facility of the Bancnet consortium to allow fund transfers from any checking or savings account among Bancnet member banks to any GlobeHandyphone and TM mobile phone as a cash-in facility for the G-Cash wallet. The IBFT facility also allows access to Internet Banking and Mobile Banking facilities. The Bancnet consortium has 28 member banks with approximately 2,000 Automated Teller Machines (ATMs) deployed nationwide for almost 3 million depositors. During the third quarter, G-Cash also formed a partnership with I-Gen Portal - a multi-level marketing organization with over 140,000 sales agents nationwide where G-Cash will be used as payment of sales commission to its sales agents. Additionally, G-Cash users can perform international and domestic remittance transactions, pay the annual business registration fees and income taxes for professionals to the Bureau of Internal Revenue, pay for Manila Water, Maynilad, Meralco and Globe Handyphone and Globelines bills, settle insurance premiums, avail of micro-finance transactions, donate to charitable institutions and buy Globe prepaid reloads. Wireline Services Innove provides wireline voice communication services, including local, national long distance, international long distance and other value-added services, through its postpaid, prepaid and payphone lines, under the brand name Globelines. Innove provides wireline voice services in nine specific geographic areas in the Philippines, including parts of Metro Manila, the Calabarzon region and Central Mindanao and Visayas. Innove offers its prepaid landline services under the brand, Globelines Prepaid. On 5 March 2004, Innove filed an application with the NTC for the expansion of its fixed line business. On 17 June 2005, Innove was awarded a nationwide license. As of 30 September 2005, Innove had total wireline voice subscribed lines of 361,998 of which 62% were postpaid and 38% were prepaid. Total wireline voice subscribers grew by 17% from the 308,376 subscribed lines registered for the same period in 2004. Additionally, Innove’s entry to the consumer broadband market introduced in 2004, registered 18,255 subscribers in the nine months of 2005, a 314% increase from the 4,414 subscribers for the same period in 2004. Innove

As of and for the nine months ended 30 September (in millions of pesos) 2005 2004 YoY change (%) Voice Net Service Revenues ……………………………………….. 3,305 2,755 20% Net Non Service Revenues …………………………………… 9 15 -40% Total Voice Operating Revenues……………………………… 3,314 2,770 20% Data International ……………………………………………….. 510 482 6% Domestic …………………………………………………… 579 595 -3% Others 1 ………………………………………………………. 365 324 13% Net Non Service Revenues……………………………………. 39 0 - Total Data Operating Revenues…………………………………………. 1,493 1,401 7% Total Operating Revenues ……………………………………………….. 4,807 4,171 15% Voice Subscribers – Net (End of period) …..……………………………. 361,998 308,376 17% Broadband Subscribers – (End of period) 2………………………… 18,255 4,414 314% Monthly churn rate-voice (%)..…………………………………………… 1.5 1.4 _____________________________________________________ 1 Includes revenues from value-added services and Broadband services 2 Majority of broadband subscriber count is part of total voice subscribers.

Innove’s gross wireline voice ARPU averaged P=1,226 for the nine months of 2005 compared to P=1,269 for the same period in 2004. Gross ARPU is computed by dividing recurring wireline voice gross service revenues for the period by the average number of wireline voice subscribers and then dividing the quotient by the number of months in the period. Innove’s net wireline voice ARPU for the nine months of 2005 declined by 2% to P1,080 from P1,104 for the same period in 2004. Net ARPU is computed by dividing recurring wireline voice net operating service revenues for all service areas for the period (net of discounts and interconnection charges to external carriers) by the average number of wireline voice subscribers and then dividing the quotient by the number of months in the period. The average monthly churn rate for Globelines was 1.5% for the nine months of 2005 compared to 1.4% for the same period in 2004. Innove’s GlobeQuest brand offers wireline data services, including international and domestic lease lines, internet, data center support services and wholesale transport services. Businesses and individuals can subscribe to GlobeQuest’s Private Networks for their international and domestic lease line requirements. Internet users can apply for Broadband Internet or Broadband Access for commercial turnkey internet business solutions to access Innove’s advanced broadband network infrastructure or high-speed fiber optic network. Additionally, GlobeQuest DataCenters provide businesses with advanced infrastructure and technology to support data hosting applications. Wireline data net operating revenues, which principally consist of billings for these services increased by 7% to P=1,493 million for the nine months of 2005 from P=1,401 million for the same period in 2004. The higher growth was mainly due to higher broadband revenues as broadband subscribers increased by 314% from 2004. International Long Distance (ILD) Services Globe and Innove both offer ILD services. ILD services are offered between the Philippines and over 200 countries. This service generates revenues from both inbound and outbound international call traffic with pricing based on agreed international termination rates for inbound traffic revenues and NTC-approved ILD rates for outbound traffic revenues. Globe Consolidated For the nine months ended 30 September 2005 2004 YoY change (%) Total ILD Minutes (in million minutes) 1…………………………. 1,046 952 10% Inbound………………………………………………………… 887 809 10% Outbound.……………………………………………………… 159 143 11% ILD Inbound / Outbound Ratio (x) …………………………… 5.6 5.7 ________________________________________________________________________________________________

1 ILD minutes originating from and terminating to Globe and Innove networks.

On 1 June 2005, Globe started its CelebRate IDD promo for its postpaid subscribers that offered US$0.20 for IDD calls after the first 4 minutes aimed at heavy IDD users. The first 4 minutes were charged at the prevailing rate of US$0.40 per minute for selected destinations. This promotion ended on 27 September 2005. On 28 September 2005, Globe Budget IDD promotion was launched to all wireless subscribers with a flat rate of US$0.20 per minute, starting on the first minute, for IDD calls to the US, Canada, China, Malaysia, Hong Kong, Singapore, Thailand, South Korea, Taiwan and Australia. The promo ended last 27 October 2005 but was extended until 26 November 2005. On 14 September 2005, Globelines launched its Lowest IDD rates promotion for its Globelines subscribers, Globe1 card users and Globelines Broadband subscribers. Globelines postpaid subscribers were charged US$0.20 per minute for IDD calls to selected

countries while Globe1 card users could make IDD calls for US$0.10 per minute from Globelines postpaid and prepaid lines including payphones nationwide. Additionally, Globelines Broadband subscribers could make Voice Over Internet Protocol (VOIP) calls for only US$0.05 per minute to 51 international destinations. Year–on-year, total ILD volumes increased by 10% in 2005. On a consolidated basis, ILD revenues, from the Wireless and Wireline services, increased by 3% to P=9,856 million for the first nine months of 2005, translating to 25% consolidated net service revenues for this period (compared to P=9,537 million and 24% respectively, for the same period in 2004). Inbound ILD volume and correspondingly, ILD revenues have been affected by ISR operations. An ISR operation is a method of terminating inbound international calls without passing through the normal IGF. ISR operations involve routing inbound international calls through private leased lines or IP data lines, and then terminated to the called party through a local cellular or fixed line number. As the ISR operators terminate an inbound IDD call as a local call, they are able to offer lower rates to foreign carriers than current termination rates. As a result, Globe is not able to realize the full inbound international revenue and instead earns only from charges from local or national calls or access charges from other carriers and normal domestic termination charges for local or NDD calls which are lower than international termination rates. To reduce ISR activities, Globe initiated increased detection and blocking procedures including closer coordination of detected ISR lines with other industry players. The Company also implemented arrangements with international carriers to reduce arbitrage opportunities for ISR operators. The Company further tightened its fraud and risk evaluation process for corporate and individual accounts and is implementing legal, commercial and technical solutions to the ISR concern such as the immediate termination of SIMs detected as being used for ISR operations including the suspension of AutoLoad Max retailers identified as having significant loading transactions to ISR SIMs. The Company has also coordinated with the NTC and other government agencies in addressing this concern. Because of these ongoing efforts, ISR losses have significantly decreased compared to last year. Results of Operations Globe Consolidated

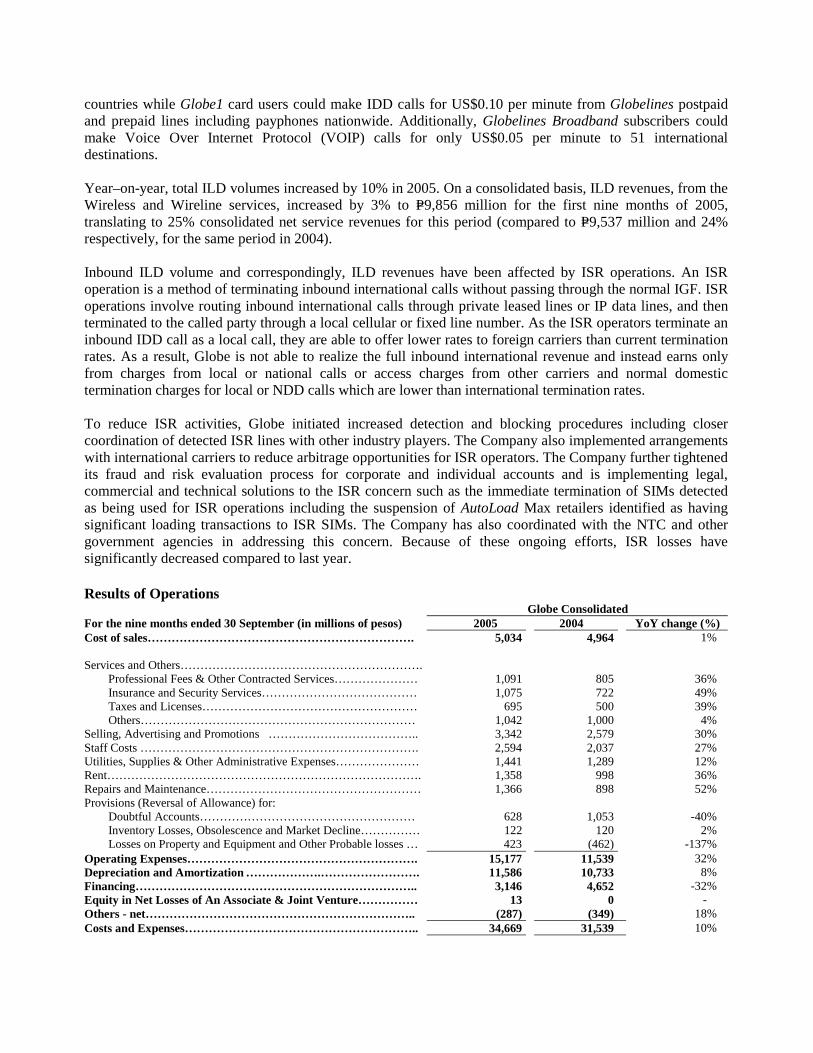

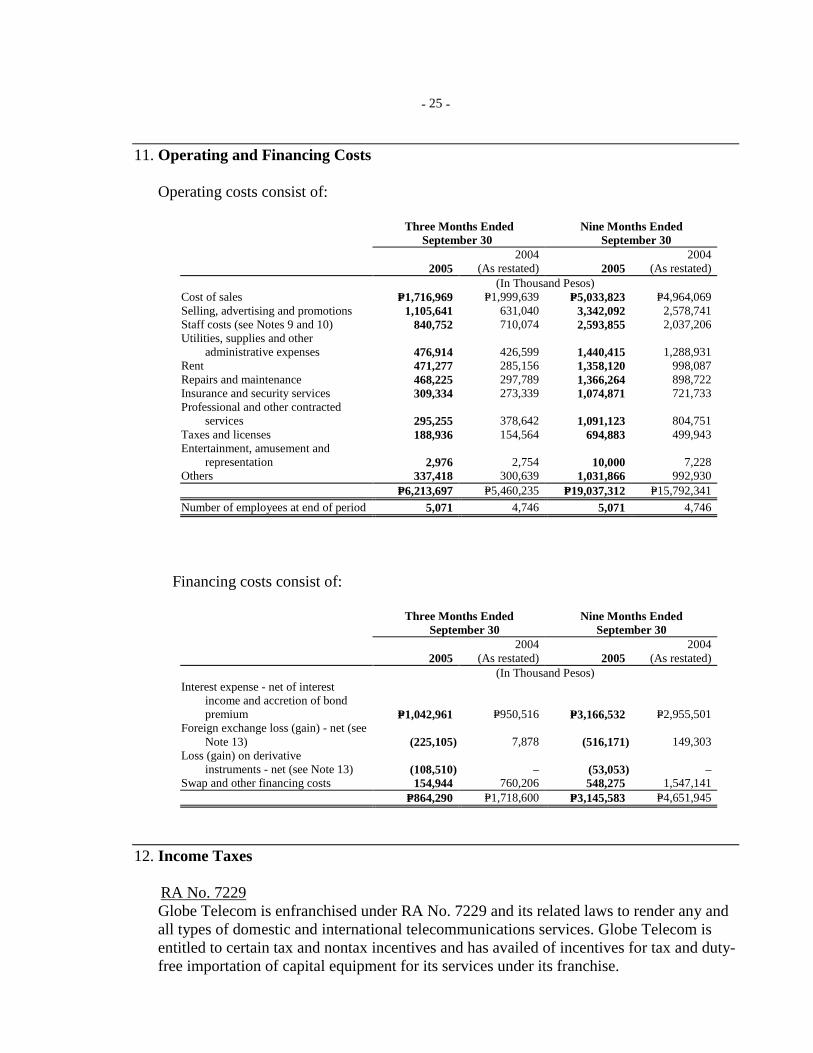

For the nine months ended 30 September (in millions of pesos) 2005 2004 YoY change (%) Cost of sales…………………………………………………………. 5,034 4,964 1% Services and Others……………………………………………………. Professional Fees & Other Contracted Services………………… 1,091 805 36% Insurance and Security Services………………………………… 1,075 722 49% Taxes and Licenses……………………………………………… 695 500 39% Others…………………………………………………………… 1,042 1,000 4% Selling, Advertising and Promotions ……………………………….. 3,342 2,579 30% Staff Costs ……………………………………………………………. 2,594 2,037 27% Utilities, Supplies & Other Administrative Expenses………………… 1,441 1,289 12% Rent……………………………………………………………………. 1,358 998 36% Repairs and Maintenance……………………………………………… 1,366 898 52% Provisions (Reversal of Allowance) for: Doubtful Accounts……………………………………………… 628 1,053 -40% Inventory Losses, Obsolescence and Market Decline…………… 122 120 2% Losses on Property and Equipment and Other Probable losses … 423 (462) -137% Operating Expenses…………………………………………………. 15,177 11,539 32% Depreciation and Amortization ……………….……………………. 11,586 10,733 8% Financing…………………………………………………………….. 3,146 4,652 -32% Equity in Net Losses of An Associate & Joint Venture…………… 13 0 - Others - net………………………………………………………….. (287) (349) 18% Costs and Expenses………………………………………………….. 34,669 31,539 10%

For the nine months of 2005, the Globe Group’s operating expenses increased by 32% to P=15,177 million from P=11,539 million for the same period in 2004 as Globe launched various marketing initiatives and shouldered increased network operating costs related to its aggressive expansion in the past year. This network expansion also resulted in depreciation and amortization growth of 8% year-on-year to P11,586 million. However, quarter-on-quarter, operating expenses (including cost of sales) have declined to P6,730 million in the third quarter from P6,855 million in the second quarter due to cost-reduction initiatives as well as reduced contracted services from the conclusion of the SIM-swap promo, lower staff costs from outsourcing initiatives and lower insurance expenses. Services and Others increased by 29% to P3,903 million for the first nine months of the year as a result of increased marketing and network-related expenses for the period. The Professional fees and Other Contracted Services account increased by 36% to P1,091 million for the nine months of 2005 due mainly to higher charges on contracted services incurred by the marketing and distribution groups for various subscriber acquisition activities (including related freight, courier and clerical services and consultancy fees). Taxes and licenses increased by 39% to P695 million due to higher NTC fees and real property taxes related to the increased number of cellsites. Meanwhile, Insurance and Security Services expenses increased by 49% to P1,075 million brought about by higher insurance premiums and security costs due to the larger number of cellsites and network facilities. Selling, Advertising and Promotions expenses increased by 30% to P3,342 million for the first nine months of 2005 due mostly to increased marketing and promotional activities related to the acquisition and implementation of usage and loyalty campaigns for subscribers including promotion activities related to the relaunch of the TM brand. Staff costs grew by 27% to P2,594 million on account of a 7% year-on-year increase in headcount which grew by 325 personnel, from 4,746 to 5,071 in the first nine months of 2005. These additional headcount were deployed mainly in the Wireless Group, given the expected growth of its subscriber base amidst increasing competition and continuing expansion of the network. Utilities, Supplies and Other Administrative expenses registered a 12% year-on-year increase due mainly to higher power and utilities charges to support the Globe Group’s expanded network facilities in 2005. Rent expenses increased by 36% to P=1,358 million because of increases in charges for cellsites, warehouse and interconnection facilities in support of the Globe Group’s continued network expansion. Repairs and Maintenance expenses likewise increased by 52% year on year to P1,366 million for the first nine months of 2005 due to additional technical service agreements necessary for the repair and maintenance of the Globe Group’s expanded network facilities and equipment. Provisions for trade receivables decreased by 37% to P547 million for the fist nine months of 2005 compared to P873 million for the same period in 2004 due to credit and system improvements made to address subscriber delinquency issues. Provisions for doubtful accounts for traffic receivables registered at P80 million compared to P181 million due to subsequent settlement and collection of traffic receivables previously provided with allowance. As a result, total provisions for doubtful accounts, including provisions for non-trade accounts, amounted to P=628 million for the first nine months of 2005 against P=1,053 million for the same period in 2004. Net subscriber receivable days was 54 for the first nine months of 2005 compared to 49 for the same period last year due to higher receivables from the wireline business.

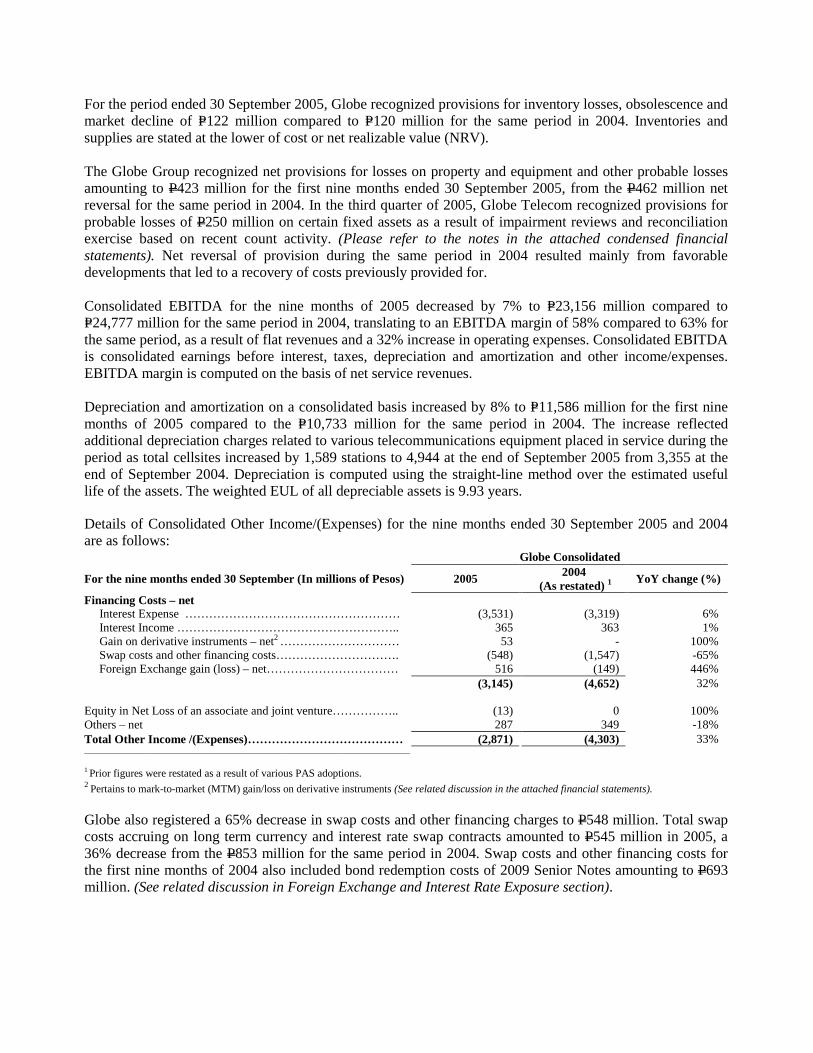

For the period ended 30 September 2005, Globe recognized provisions for inventory losses, obsolescence and market decline of P=122 million compared to P=120 million for the same period in 2004. Inventories and supplies are stated at the lower of cost or net realizable value (NRV). The Globe Group recognized net provisions for losses on property and equipment and other probable losses amounting to P423 million for the first nine months ended 30 September 2005, from the P462 million net reversal for the same period in 2004. In the third quarter of 2005, Globe Telecom recognized provisions for probable losses of P250 million on certain fixed assets as a result of impairment reviews and reconciliation exercise based on recent count activity. (Please refer to the notes in the attached condensed financial statements). Net reversal of provision during the same period in 2004 resulted mainly from favorable developments that led to a recovery of costs previously provided for. Consolidated EBITDA for the nine months of 2005 decreased by 7% to P=23,156 million compared to P=24,777 million for the same period in 2004, translating to an EBITDA margin of 58% compared to 63% for the same period, as a result of flat revenues and a 32% increase in operating expenses. Consolidated EBITDA is consolidated earnings before interest, taxes, depreciation and amortization and other income/expenses. EBITDA margin is computed on the basis of net service revenues. Depreciation and amortization on a consolidated basis increased by 8% to P=11,586 million for the first nine months of 2005 compared to the P=10,733 million for the same period in 2004. The increase reflected additional depreciation charges related to various telecommunications equipment placed in service during the period as total cellsites increased by 1,589 stations to 4,944 at the end of September 2005 from 3,355 at the end of September 2004. Depreciation is computed using the straight-line method over the estimated useful life of the assets. The weighted EUL of all depreciable assets is 9.93 years. Details of Consolidated Other Income/(Expenses) for the nine months ended 30 September 2005 and 2004 are as follows: Globe Consolidated

For the nine months ended 30 September (In millions of Pesos) 2005 2004 (As restated) 1 YoY change (%)

Financing Costs – net Interest Expense ……………………………………………… (3,531) (3,319) 6% Interest Income ……………………………………………….. 365 363 1% Gain on derivative instruments – net2 ………………………… 53 - 100% Swap costs and other financing costs…………………………. (548) (1,547) -65% Foreign Exchange gain (loss) – net…………………………… 516 (149) 446% (3,145) (4,652) 32% Equity in Net Loss of an associate and joint venture…………….. (13) 0 100% Others – net 287 349 -18% Total Other Income /(Expenses)………………………………… (2,871) (4,303) 33% ______________________________________________________________________

1 Prior figures were restated as a result of various PAS adoptions. 2 Pertains to mark-to-market (MTM) gain/loss on derivative instruments (See related discussion in the attached financial statements).

Globe also registered a 65% decrease in swap costs and other financing charges to P548 million. Total swap costs accruing on long term currency and interest rate swap contracts amounted to P545 million in 2005, a 36% decrease from the P853 million for the same period in 2004. Swap costs and other financing costs for the first nine months of 2004 also included bond redemption costs of 2009 Senior Notes amounting to P693 million. (See related discussion in Foreign Exchange and Interest Rate Exposure section).

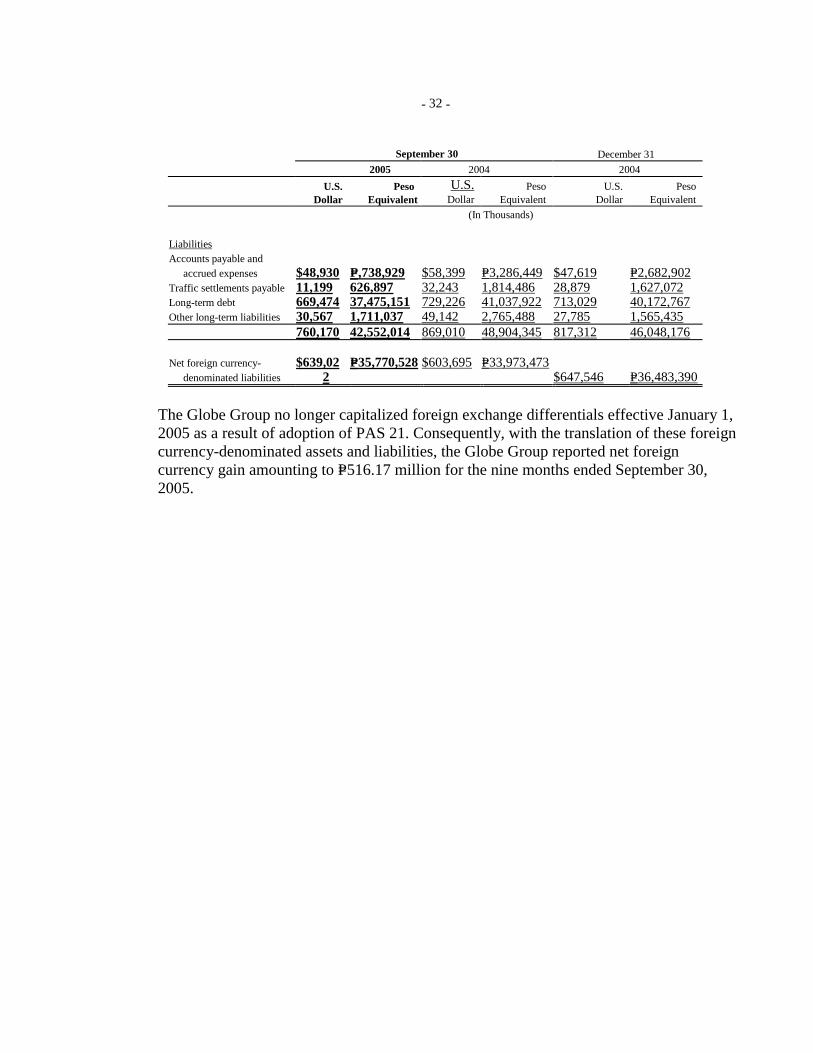

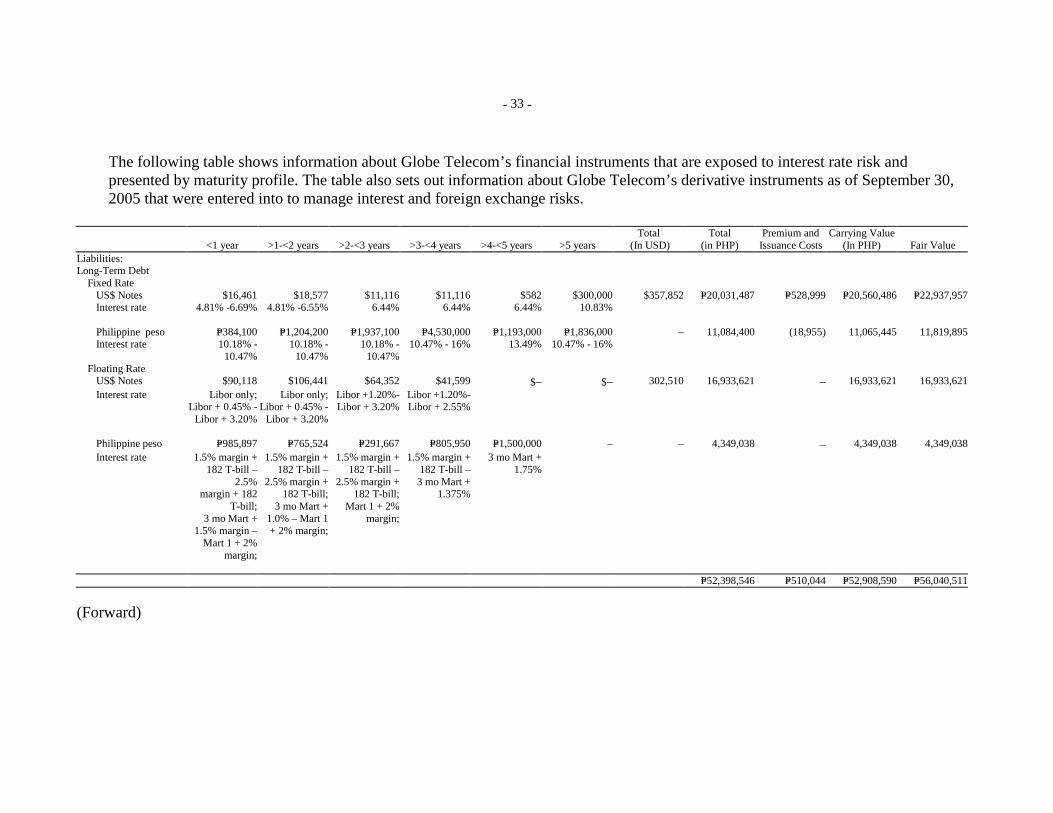

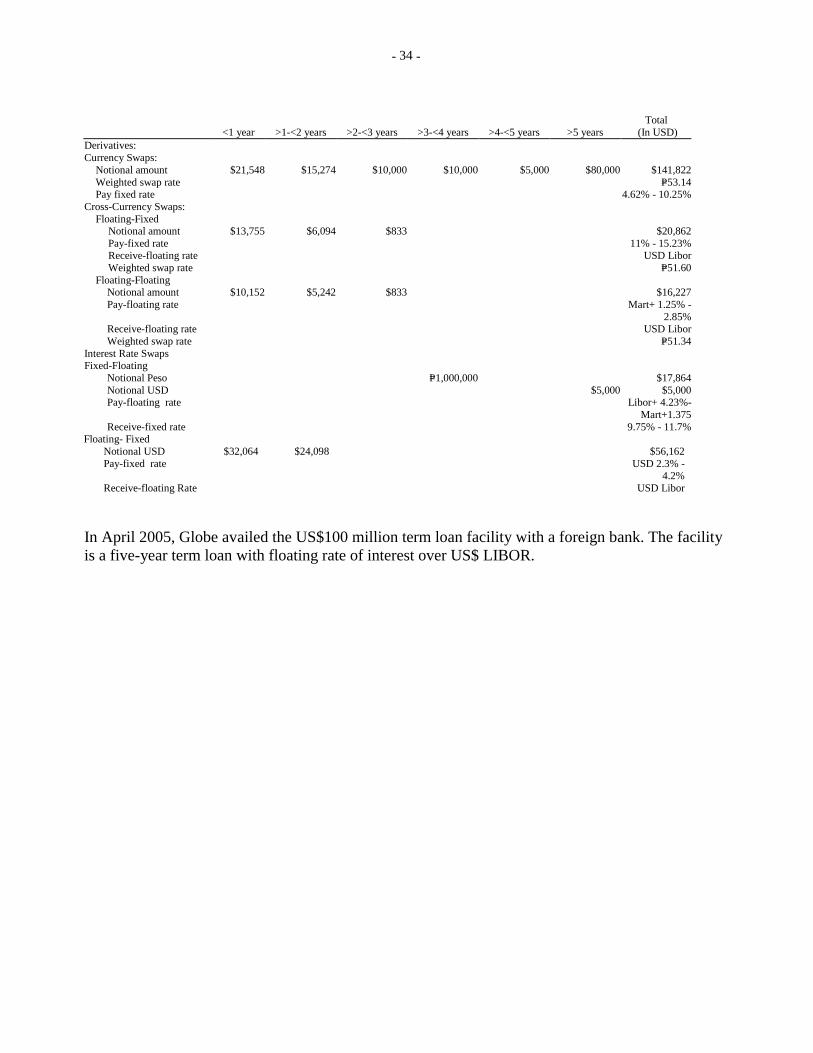

During the first nine months of 2005, the Globe Group registered net foreign exchange gains of P516 million compared to a net foreign exchange loss of P149 million for the same period last year due to higher debt denominated in dollar during the same period in 2004. Also in 2005, the Globe Group adopted PAS 21 which prohibits capitalization of forex gains and losses. (See related discussion on page 16 under Foreign Exchange and Interest Rate Exposure section) Consolidated EBIT or earnings before interest, other expenses (income) and taxes decreased by 18% to P=11,570 million for the nine months of 2005 compared to P=14,043 million for the same period in 2004. For the period ended 30 September 2005, Globe’s consolidated provision for current and deferred income tax increased by 204% to P2,258 million from P743 million for the same period in 2004 mainly as a result of the expiry of the income tax holiday incentive of Globe on 31 March 2005 and Innove’s turning into a taxable income position subject to the regular corporate tax rates in 2005. As a result, Globe’s consolidated effective income tax rate was 26% in the nine months of 2005 vs. 8% for the same period in 2004. The Globe Group’s deferred tax assets and liabilities as of 30 September 2005 were computed using the tax rate of 32%. Republic Act (RA) 9337 which will become effective on 01 November 2005 increases the tax rate to 35% and then reduces the rate to 30% on 01 January 2009. The Group will reflect the effects of the change in the tax rate in the fourth quarter financial statements. Consolidated net income decreased by 28% year-on-year to P=6,440 million from the P=8,997 million posted for the same period in 2004. Accordingly, consolidated basic earnings per common share were P47.65 and P63.92 (as restated) for the first nine months of 2005 and 2004, respectively. Consolidated diluted earnings per common share were P47.62 and P63.79 (as restated) for the first nine months of 2005 and 2004, respectively. Foreign Exchange and Interest Rate Exposure Starting 1 January 2005, the Globe Group adopted PAS 21, The Effects of Changes in Foreign Exchange Rates, which eliminates the capitalization of foreign exchange differentials related to the acquisition of property and equipment. Previously, the foreign currency-denominated liabilities used to finance the acquisition and installation of Globe and Innove’s property and equipment were capitalized. These foreign exchange differentials were added to or deducted from the cost of the appropriate property and equipment accounts. The adoption of PAS 21 decreased our beginning retained earnings by P2,444 million. (Please see related discussion in the attached condensed financial statements) The Philippine Peso closed at P=55.977 as of 30 September 2005 from P=56.276 as of the same date last year. The foreign exchange differentials arising from remeasurement of foreign currency-denominated accounts are charged/credited to current operations. Globe Group’s net foreign exchange gains/(loss) credited/(charged) to current operations amounted to P516 million gain and P149 million loss for the nine months ended 30 September 2005 and 2004, respectively. To mitigate foreign exchange risk, Globe enters into short-term foreign currency forwards and long-term foreign currency swap contracts. Short-term forward contracts are used to manage Globe’s foreign exchange exposure related to foreign currency-denominated monetary assets and liabilities. For certain long term foreign currency denominated loans, Globe enters into long term foreign currency and interest rate swap contracts to manage its foreign exchange and interest rate exposures.

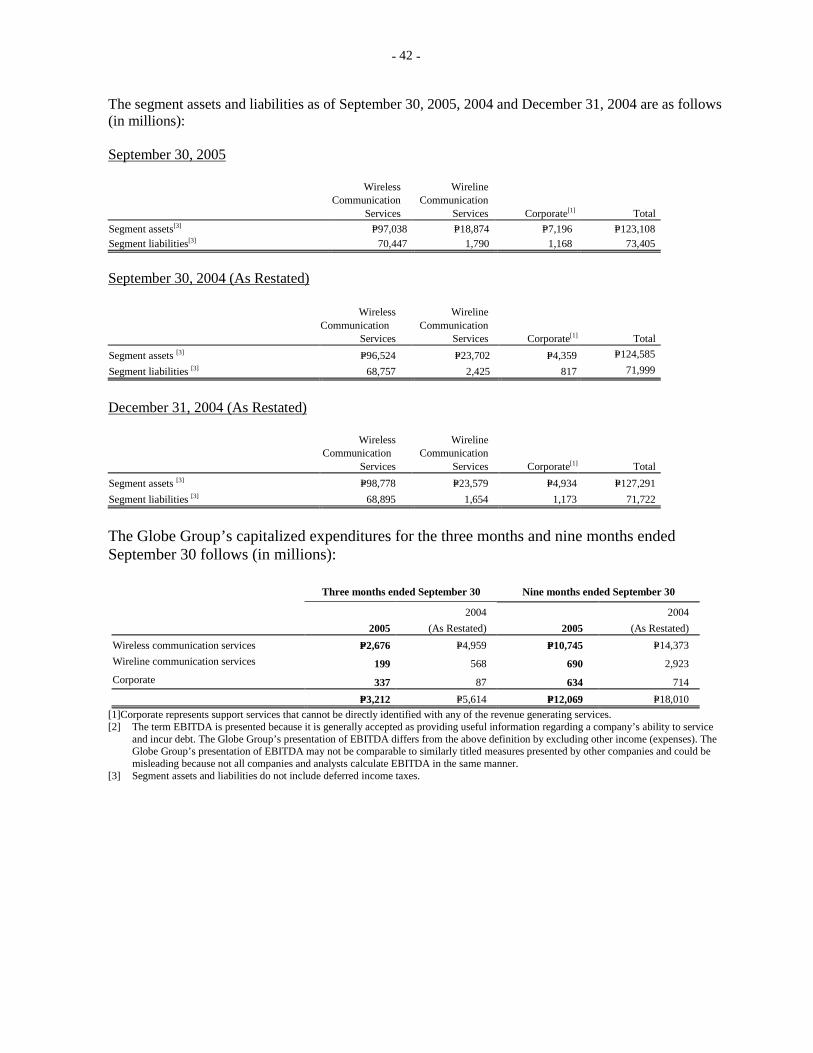

As of 30 September 2005, Globe had US$179 million in outstanding foreign currency swap agreements, some of which have option features. The Company also sold covered currency options with total notional amount of US$28 million with maturities ranging from March 2006 to March 2007. Globe uses interest rate swaps to manage the Company’s interest rate risk in a cost-efficient manner. As of 30 September 2005, Globe had US$56 million in notional amount of US$ swaps under which it effectively swapped some of its floating rate US$ denominated loans into fixed rate, with semi-annual payment intervals up to August 2007. The Company also has US$5 million in notional amount of US$ swaps under which it effectively swapped 9.75% fixed coupon of its 2012 Senior Notes to a floating rate based on LIBOR, subject to a cap. The performance of the swap is linked to the 10-year and 30-year US$ Constant Maturity Swap Rates. Globe also has a fixed to floating interest rate swap contract with a notional amount of P1 billion, in which it effectively swaps a fixed rate Philippine peso denominated bond into floating rate with quarterly payment intervals up to February 2009. Globe Telecom also has outstanding short term non-deliverable currency forward contracts with a total notional amount of US$3 million to fix the peso cash flows from coupon and redemption of dollar-linked peso notes. The Group also has embedded forwards and options in certain financial and non-financial contracts with total notional amount of US$51 million. Globe’s 2012 Senior Notes also contain embedded call options which give Globe the right to prepay the Notes at a certain call price per year. Gains on derivative instruments represent the net mark-to-market (MTM) gains on derivative instruments. Beginning 2005, MTM values have to be booked as required by PAS 39. The estimated unrealized mark-to-market gain on the outstanding derivatives of Globe amounted to US$18 million based on valuation as of 30 September 2005. US$1 million of the increase is reflected in the consolidated statements of income for the nine months ended 30 September 2005. (See related discussion under Results of Operations) Consolidated foreign currency-linked revenues were 28% of total net revenues for the periods ended 30 September 2005 and 2004. Foreign currency linked revenues include those that are: (1) billed in foreign currency and settled in foreign currency, or (2) billed in Pesos at rates linked to a foreign currency tariff and settled in Pesos, or (3) wireline monthly service fees and the corresponding application of the Currency Exchange Rate Adjustment or CERA mechanism, under which Globe has the ability to pass the effects of local currency depreciation to its subscribers. These revenues serve as a natural hedge to our foreign exchange exposure. Liquidity and Capital Resources Consolidated assets as of 30 September 2005 amounted to P=124,749 million compared to P=127,244 million in 30 September 2004. As of 30 September 2005, current ratio on a consolidated basis was 0.73:1 compared to 0.80:1 for the same period in 2004. Consolidated cash, cash equivalents and short term investments was at P=9,807 million at the end of the nine months of 2005, 20% lower than the P12,292 million for the same period in 2004 due to dividend payments and the buyback of shares in March 2005. For the nine months of 2005, gross debt to equity ratio was 1.11:1 on a consolidated basis and remains well within the 2:1 debt to equity limit dictated by certain debt covenants while net debt to equity ratio was 0.90:1.

The financial tests under Globe’s loan agreements include compliance with the following ratios:

• Total debt to equity not exceeding 2:1; • Total debt to EBITDA of 3:1; • Debt service coverage exceeding 1.3 times (except for refinancing of the 2009 bond which the

lenders consented to exclude from the computation); • Secured debt ratio not exceeding 0.2 times.

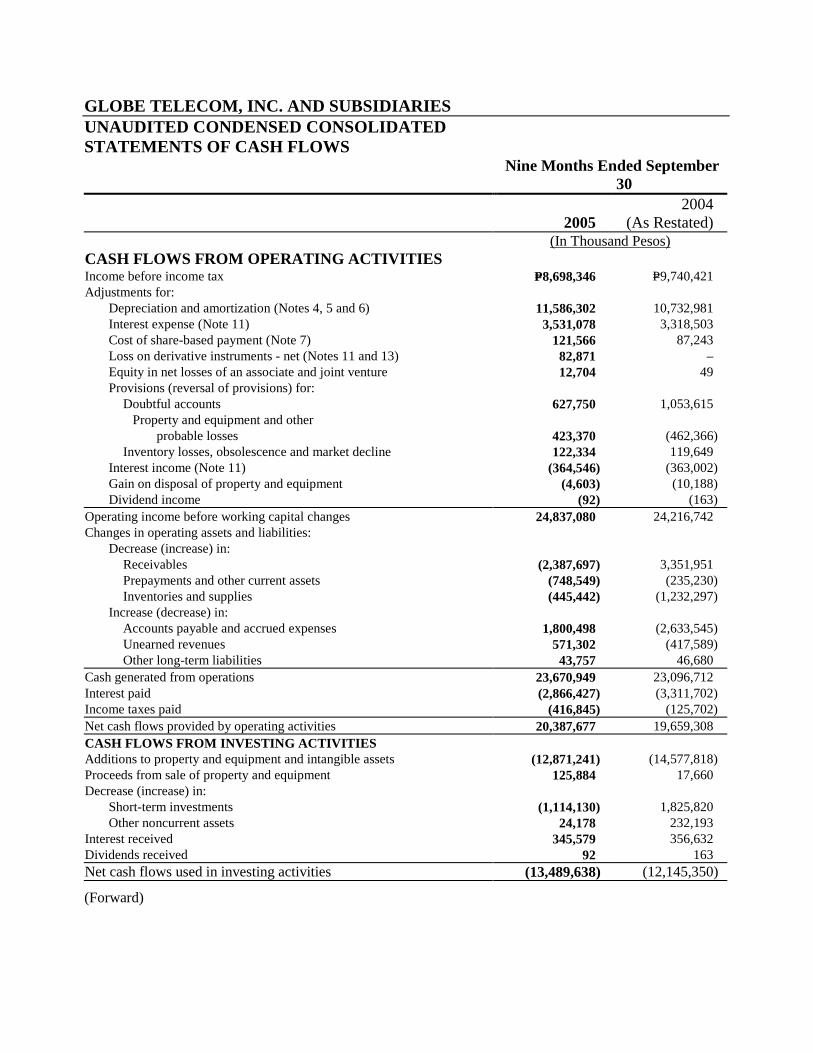

Consolidated net cash flow from operations amounted to P=20,388 million for the period ended 30 September 2005, a 4% increase from P=19,659 million for the same period in 2004. Globe Consolidated

As of and for the nine months ended 30 September (in millions of pesos) 2005 2004 YoY change Capital Expenditures (Cash) ………………………………. ………… 12,871 14,578 -12% Increase (Decrease) in Liabilities related to Acquisition of PPE ………. (776) 1,447 -154% Total Capital Expenditures ………………………………………….…. 12,095 16,025 -25%

Total Capital Expenditures / Service Revenues (%)………………… 30 41

Consolidated net cash used in investing activities amounted to P=13,490 million for the first nine months of 2005, an 11% increase from the P=12,145 million for the same period in 2004. Consolidated capital expenditures for the nine months of 2005 amounted to P=12,095 million. For 2005, Globe has earmarked around P17 billion for capital expenditures that were spent primarily on expanding its wireless network and enhancing the necessary transmission facilities in areas where traffic is expected to surge. The 2005 capital expenditure program is funded through internally-generated cash and debt financing. Consolidated net cash used in financing activities for the nine months of 2005 amounted to P=12,500 million, a 40% increase compared to P=8,947 million for the same period in 2004. Consolidated total debt as of 30 September 2005 amounted to P=52,909 million, a 2% increase from the P=52,075 million for the same period in 2004. Loan repayments of Globe for the nine months of 2005 amounted to P=9,250 million (US$165 million) compared to the P=17,393 million (US$311 million) paid for the same period in 2004. Globe prepaid US$41 million of its long term loans in addition to US$161 million of maturing loans. As of 30 September 2005, gross debt reached P=53 billion, 71% of which are denominated in US$. Of the 71%, 27% has been swapped to pesos. As a result, the amount of US$ debt swapped into pesos and peso-denominated debt accounts for approximately 48% of consolidated loans as of 30 September 2005. Below is the schedule of debt maturities for Globe for the years stated below based on total outstanding debt as of 30 September 2005: Year Due Principal (US$ millions) 2005 …………………………………………………………………………............................... 20 2006 ……………………………………………………………………………………………… 171 2007 ……………………………………………………………………………………………… 148 2008………………………………………………………………………………………………. 115 2009 through 2012 ………………………………………………………………………………. 490 Total 944 Stockholders’ equity was P=47,742 million as of 30 September 2005 or an 8% decline from the P=52,080 million for the same period in 2004. As a result of the adoption of new accounting standards, the Globe Group took a one-time charge to its beginning of the year retained earnings amounting to P2,670 million

representing the net of tax effect of various accounting standards discussed in the attached notes to the financial statements. A substantial portion of this one-time charge is due to the adoption of PAS 21 which no longer allows the capitalization of foreign exchange losses to assets.

On 1 February 2005, the Board of Directors (BOD) of Globe Telecom approved an offer to purchase one share for every fifteen shares of the outstanding common stock of Globe from all shareholders of record as of 10 February 2005, at a price of P950 per share. The approval allowed Globe to purchase up to 9 million shares representing 6.7% of its outstanding common shares. Each shareholder was entitled to tender a proportionate number of shares owned at the 1:15 ratio, referred to as the Tender Ratio, for purchase by Globe upon and subject to the terms and conditions of the tender offer. On 3 February 2005, Globe commenced the tender offer which expired on 3 March 2005 after a one-day extension. Also, on 1 February 2005, the BOD approved the retirement of the purchased shares and the existing 12 million treasury shares acquired in 2003 from DeTeAsia. On 8 March 2005, Globe announced that it had accepted 8 million common shares that were tendered by the stockholders. The accepted shares represented 86% of shares eligible for tender. The value of the tendered shares totaled P7.66 billion. The accepted shares were eventually crossed at the exchange on 15 March 2005 and payment was made on 16 March 2005. (Please refer to page 23 for the shareholder structure as of 30 September 2005) As of 30 September 2005, Globe’s capital stock consists of:

1. Preferred stock Series “A” at a par value of P5 per share of which 158 million shares are outstanding out of a total authorized of 250 million shares. Preferred stock “Series A” has the following features: (a) Convertible to one common share after 10 years from issue date at a price which shall not be less

than the prevailing market price of the common stock less the par value of the preferred shares; (b) Cumulative and non-participating; (c) Floating rate dividend (set at MART 1 plus 2% average for a 12-month period); (d) Issued at P=5 par; (e) Voting rights; (f) Globe has the right to redeem the preferred shares at par plus accrued dividends at any time after

5 years from date of issuance; and (g) Preferences as to dividend in the event of liquidation.

On 15 December 2004 the Board of Directors (BOD) approved the declaration of cash dividends to preferred shareholders as of record date 31 December 2004 amounting to P75 million and was paid on 15 March 2005.

2. Common shares at par value of P=50 per share of which 152 million shares have been issued and 132

million are outstanding out of a total authorized of 200 million shares. In the last annual stockholders meeting on 4 April 2005, Globe’s stockholders authorized the cancellation of its treasury shares and the reduction in the authorized capital stock of the Company. On October 28, 2005, the Securities and Exchange Commission approved the reduction in capital stock. After the reduction, total authorized common shares are now 179,934,373, of which 131,899,148 are outstanding.

On 1 February 2005, the BOD declared the first semi-annual cash dividend in 2005 of P20 per common share with a record date of 18 February 2005 and payment was made on 15 March 2005. On 2 August 2005, the Board of Directors declared the second semi-annual cash dividend for 2005 amounting to P20 per common share outstanding as of record date 19 August 2005, and payment was

on 14 September 2005. This is consistent with our cash dividend policy of distributing 50% of prior year’s net income and represents an increase of 11% over the previous year.

Consolidated Return on Average Equity (ROE) for the period ended 30 September 2005 stood at 16%. On 1 July 2004, Globe Telecom granted additional stock options to key executives and senior management personnel of the Globe Group under the Executive Stock Option Plan 2. It required the grantees to pay a nonrefundable option purchase price of P1,000. The agreement provides for an exercise price of P840.75 per share. 50% of the options become exercisable from 1 July 2006 to 30 June 2014, while the remaining 50% become exercisable from 1 July 2007 to 30 June 2014. As of 30 September 2005, there were a total net outstanding stock options of 1,286,850 granted to key executives and senior management personnel. In order to avail of the privilege, the grantees must remain with Globe Telecom or its affiliates from grant date up to the beginning of the exercise period of the corresponding shares. RECENT DEVELOPMENTS Globe is an intervenor in and Innove is a party to Civil Case No. Q-00-42221 entitled "Isla Communications Co., Inc. et. al., versus National Telecommunications Commission (‘NTC’) et al.," before the Regional Trial Court (‘RTC’) of Quezon City by virtue of which Globe and Innove, together with other cellular operators, sought and obtained a preliminary injunction against the implementation of NTC Memorandum Circular (‘MC’) No. 13-6-2000 from the RTC of Quezon City. NTC MC 13-6-2000 prescribed new billing requirements for cellular service providers. The NTC appealed the issuance of the injunction to the Court of Appeals. On 25 October 2001, we received a copy of the decision of the Court of Appeals ordering the dismissal of the case before the RTC for lack of jurisdiction, but without prejudice to the wireless companies’ seeking relief before the NTC, which the Court of Appeals claims had jurisdiction over the matter. On 22 February 2002, we filed a Petition for Review with the Supreme Court (‘SC’) to annul and reverse the decision of the Court of Appeals. The Supreme Court (‘SC’), on 2 September 2003, overturned the CA’s earlier dismissal of the petitions filed by SMART and Globe. In its 13-page decision, the SC said that the Quezon City trial court could hear and decide the case, contrary to NTC’s argument. The SC has also since denied the NTC’s motion for reconsideration. We are currently awaiting resumption of the proceedings before the RTC of Quezon City. On 17 July 2005, TM launched its Emergency Text service that allows TM subscribers to send an emergency text message even with zero prepaid credit balance. The recipient of the "Please send me load" message may send prepaid load credits via Share-A-Load (SAL) by simply replying to the Emergency Text received. On 7 August 2005, Globe improved on its Hong Kong Share-A-Load service by offering its G-Cash remittance service to OFW SmarTone subscribers in Hong Kong. Globe Handyphone and TM subscribers in the Philippines can now receive G-Cash in P500, P1,000, P3,000 and P5,000 denominations which will be charged to the OFW’s SmarTone subscriptions. These denominations will be charged in Hong Kong dollars and will have a corresponding transaction fee. On 12 August 2005, Globe announced that it had completed the first video call over its 3G trial network. 3G is third generation technology that allows high speed data transmission enabling users to enjoy features that require speed such as video on-demand and video call conference. Following 2G or GSM and 2.5G network or GPRS, 3G network is the next generation of telecommunications technologies and services. Globe Telecom was the first Philippine operator to be given a 3G trial permit and frequencies from the National Telecommunications Commission (NTC). On 14 September 2005 Globelines announced that its postpaid subscribers can call 10 countries for only US$0.20 per minute until 27 October 2005. Subscribers who have activated their IDD can already avail of the

budget IDD rate when calling Australia, Canada, China, Hong Kong, Malaysia, Singapore, South Korea, Taiwan, Thailand and USA. Additionally, with the Globe1 Card, Innove’s PIN-based prepaid call card, consumers can call these countries at US$0.10 per minute using a Globelines postpaid, prepaid landline or payphone until 13 November 2005. Starting 20 September 2005, Globelines Broadband subscribers can call 51 countries for only US$0.05 per minute using Voice Over Internet Protocol (VoIP) technology. The 51 countries are Argentina, Australia, Austria, Belgium, Brazil, Bulgaria, Canada, Chile, China, Colombia, Czech Republic, Denmark, Estonia, Finland, France, Germany, Gibraltar, Greece, Hong Kong, Hungary, Iceland, Ireland, Israel, Italy, Japan, South Korea, Luxembourg, Malaysia, Mexico, Monaco, Mongolia, Netherlands, New Zealand, Norway, Peru, Poland, Portugal, Puerto Rico, Russia, Saudi Arabia, Singapore, Slovenia, Spain, Sweden, Switzerland, Taiwan, Thailand, Turkey, United Kingdom, USA and Venezuela. On 15 September 2005, Innove launched its G-POS (Point of Sale) Service at the Stores Asia Expo 2005 Retail Suppliers Exhibition held concurrently with the National Retailers Conference at the Edsa Shangri-La Hotel. G-POS will allow stores to use their existing POS system instead of using a cellular phone to handle G-Cash transactions such as merchant payments, bills payments, cash and m-currency conversions and AutoLoadMax reloads through GlobeQuest Store Express. GlobeQuest Store Express is a solution specifically designed to address the various connectivity requirements of the retail industry and to meet both the network and information technology requirements of retail companies, regardless of size and retail format. On 20 September 2005, Globe introduced its 3G Roaming service for subscribers traveling abroad in Asia-Pacific countries with 3G networks. With the 3G Roaming service, subscribers traveling abroad have the benefits of faster data access and soon, advanced connectivity with video calling. The 3G technology will allow subscribers to access and download heavy data files such as music tracks and videos from the Internet. It also enables video sharing, through which users can send and save video clips with overall faster access of GPRS. These services are on top of regular voice, SMS and MMS roaming services. Globe international roaming subscribers can now roam in 3G networks of three countries using the following operator networks and 3G-enabled phones - NTT DoCoMo and Vodafone in Japan, Sunday in Hong Kong, and SingTel in Singapore. On 28 September 2005, Globe Handyphone and TM offered its postpaid and prepaid subscribers the CelebRate Budget IDD promotion. Subscribers can make IDD calls to United States, Canada, China, Malaysia, Hong Kong, Singapore, South Korea, Thailand, Taiwan, and Australia for US$0.20 per minute starting on the first minute. The promo will end on 26 November 2005. The following Globe Prepaid CelebRate offerings have also been extended to 26 November 2005.

1. The TXTNONSTOP promotion for Globe-to-Globe unlimited text for only P15 for 24 hours, P25 for two days, or P50 for 5 days.

2. The P10-per-3 minute call promotion for Globe-to-Globe calls. Subscribers can dial 235 + the 10-digit Globe number to avail of the service.

The TXTNONSTOP and P10-per-3-minute call promos are open to all Globe prepaid subscribers, including those with Globe Gizmo, Kapamilya, Globe Kababayan and Traveler's SIMs. The TM Todo Tawag 15/15 promotion (launched on 19 August 2005) was likewise extended to 18 November 2005 and allows TM subscribers to make 15 minute TM-to-TM voice calls for only P15. Subscribers can dial

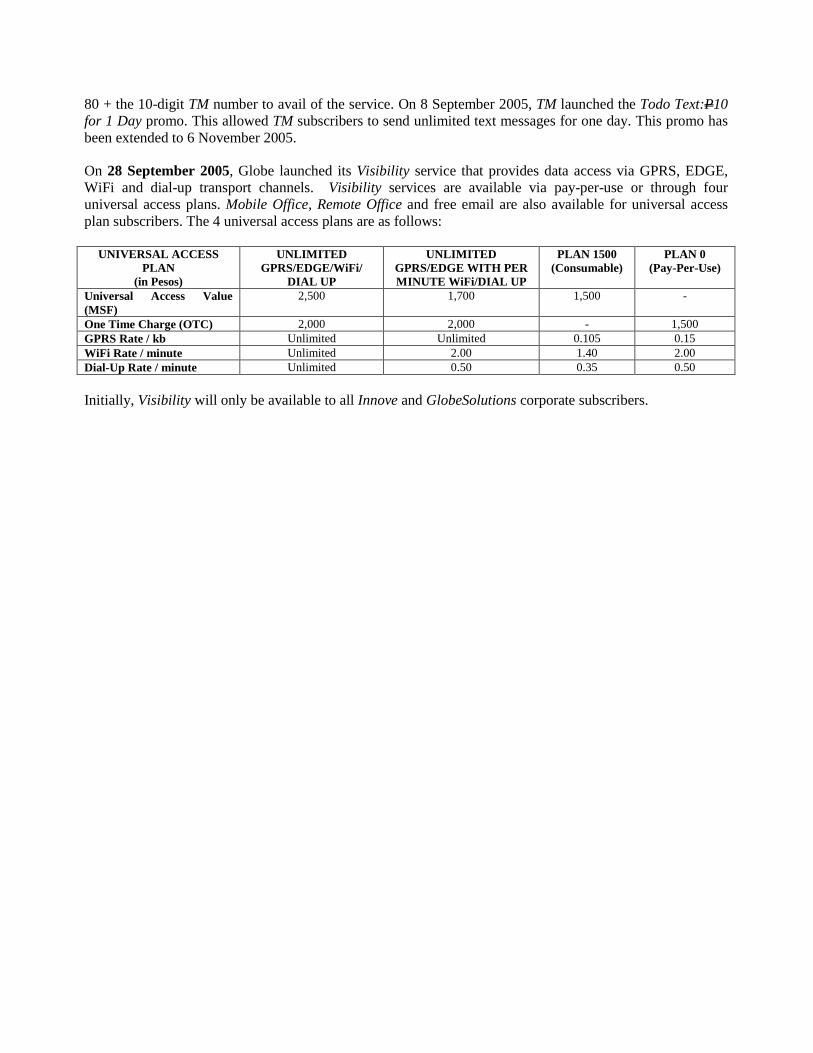

80 + the 10-digit TM number to avail of the service. On 8 September 2005, TM launched the Todo Text:P10 for 1 Day promo. This allowed TM subscribers to send unlimited text messages for one day. This promo has been extended to 6 November 2005. On 28 September 2005, Globe launched its Visibility service that provides data access via GPRS, EDGE, WiFi and dial-up transport channels. Visibility services are available via pay-per-use or through four universal access plans. Mobile Office, Remote Office and free email are also available for universal access plan subscribers. The 4 universal access plans are as follows:

UNIVERSAL ACCESS PLAN

(in Pesos)

UNLIMITED GPRS/EDGE/WiFi/

DIAL UP

UNLIMITED GPRS/EDGE WITH PER MINUTE WiFi/DIAL UP

PLAN 1500 (Consumable)

PLAN 0 (Pay-Per-Use)

Universal Access Value (MSF)

2,500 1,700 1,500 -

One Time Charge (OTC) 2,000 2,000 - 1,500 GPRS Rate / kb Unlimited Unlimited 0.105 0.15 WiFi Rate / minute Unlimited 2.00 1.40 2.00 Dial-Up Rate / minute Unlimited 0.50 0.35 0.50

Initially, Visibility will only be available to all Innove and GlobeSolutions corporate subscribers.

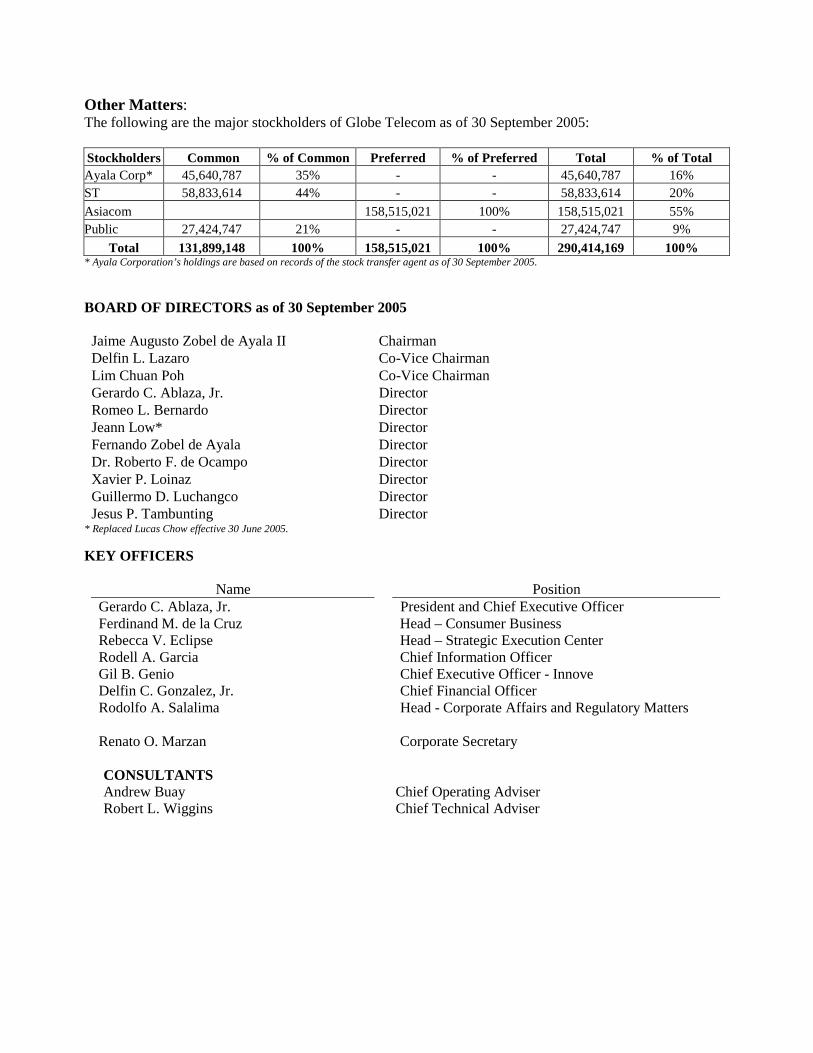

Other Matters: The following are the major stockholders of Globe Telecom as of 30 September 2005: Stockholders Common % of Common Preferred % of Preferred Total % of Total Ayala Corp* 45,640,787 35% - - 45,640,787 16% ST 58,833,614 44% - - 58,833,614 20%

Asiacom 158,515,021 100% 158,515,021 55% Public 27,424,747 21% - - 27,424,747 9%

Total 131,899,148 100% 158,515,021 100% 290,414,169 100% * Ayala Corporation’s holdings are based on records of the stock transfer agent as of 30 September 2005.

BOARD OF DIRECTORS as of 30 September 2005 Jaime Augusto Zobel de Ayala II Chairman Delfin L. Lazaro Co-Vice Chairman Lim Chuan Poh Co-Vice Chairman Gerardo C. Ablaza, Jr. Director Romeo L. Bernardo Director Jeann Low* Director Fernando Zobel de Ayala Director Dr. Roberto F. de Ocampo Director Xavier P. Loinaz Director Guillermo D. Luchangco Director Jesus P. Tambunting Director

* Replaced Lucas Chow effective 30 June 2005.

KEY OFFICERS

Name Position Gerardo C. Ablaza, Jr. President and Chief Executive Officer Ferdinand M. de la Cruz Head – Consumer Business Rebecca V. Eclipse Head – Strategic Execution Center Rodell A. Garcia Chief Information Officer Gil B. Genio Chief Executive Officer - Innove Delfin C. Gonzalez, Jr. Chief Financial Officer Rodolfo A. Salalima Head - Corporate Affairs and Regulatory Matters Renato O. Marzan Corporate Secretary

CONSULTANTS Andrew Buay Chief Operating Adviser Robert L. Wiggins Chief Technical Adviser

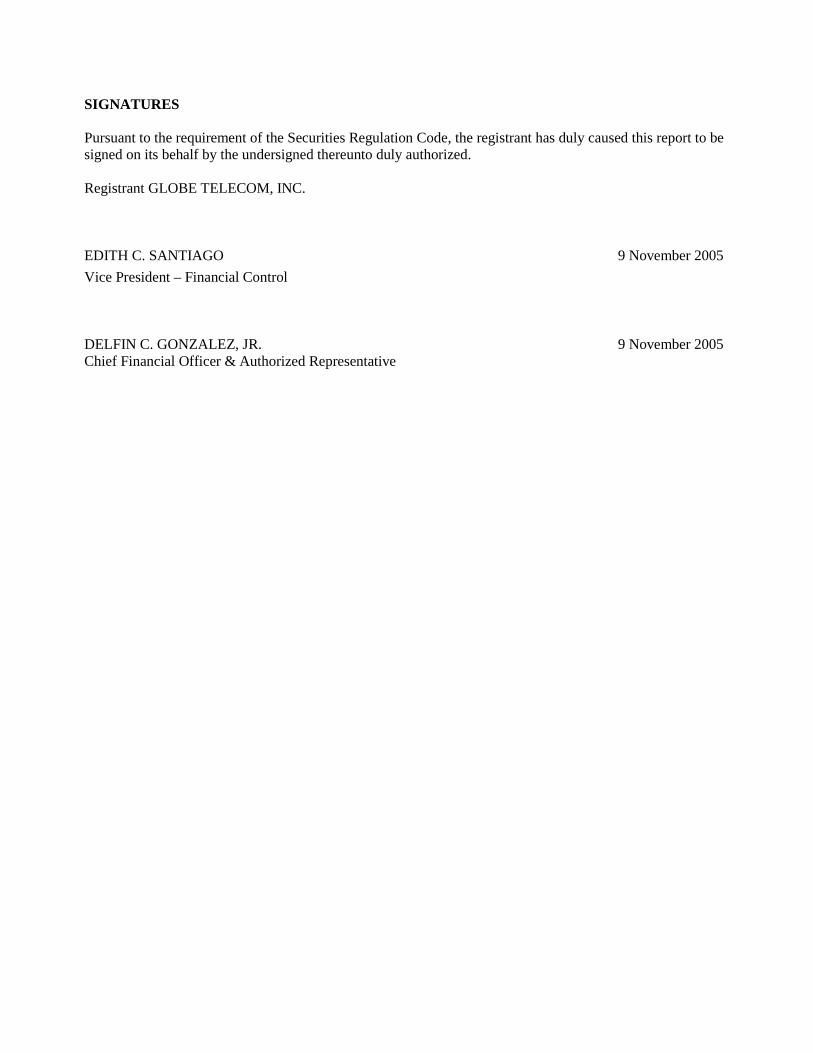

SIGNATURES

Pursuant to the requirement of the Securities Regulation Code, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized. Registrant GLOBE TELECOM, INC.

EDITH C. SANTIAGO 9 November 2005

Vice President – Financial Control

DELFIN C. GONZALEZ, JR. 9 November 2005 Chief Financial Officer & Authorized Representative

Annex I

GLOBE TELECOM, INC. AND SUBSIDIARIES Condensed Consolidated Financial Statements September 30, 2005 and 2004 (Unaudited)

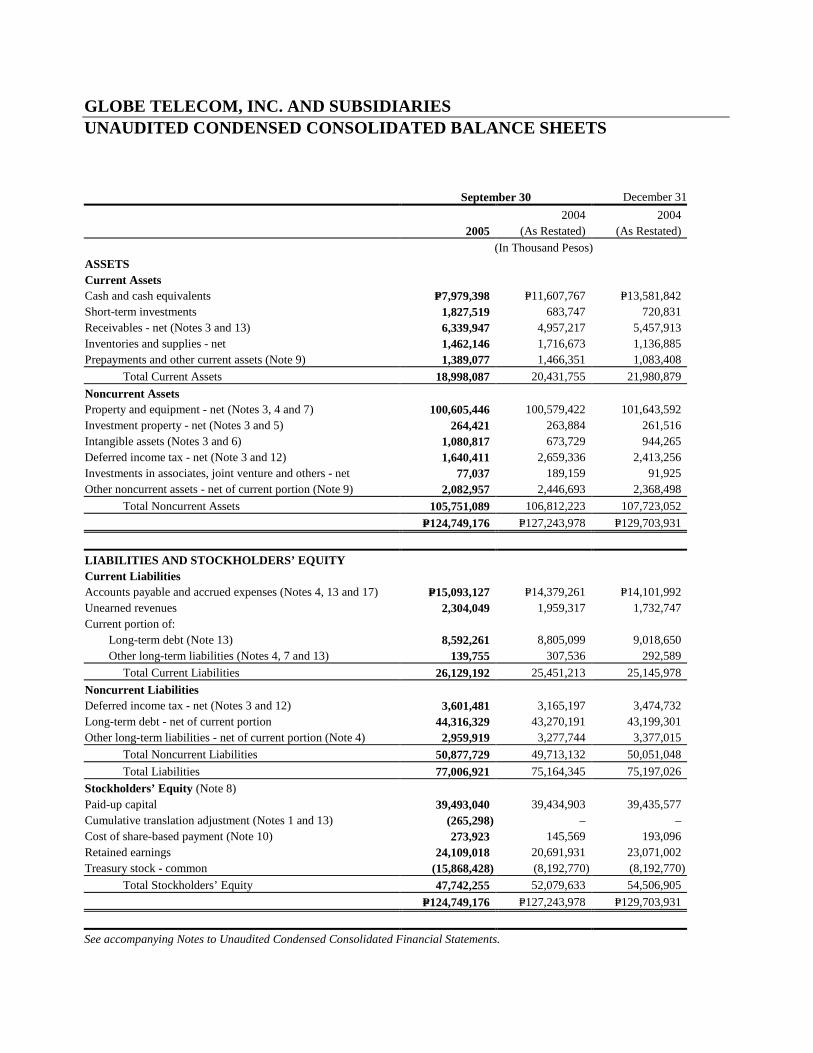

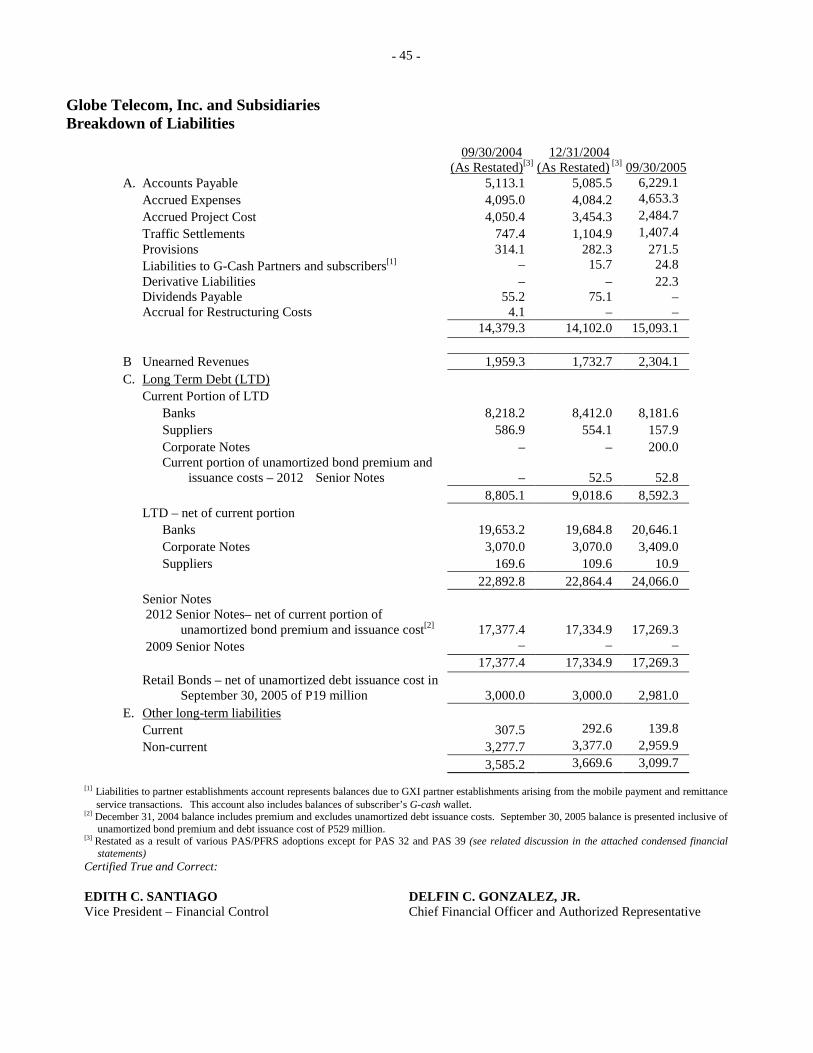

GLOBE TELECOM, INC. AND SUBSIDIARIES UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS September 30 December 31

2005 2004

(As Restated) 2004

(As Restated)

(In Thousand Pesos) ASSETS Current Assets Cash and cash equivalents P=7,979,398 P=11,607,767 P=13,581,842 Short-term investments 1,827,519 683,747 720,831 Receivables - net (Notes 3 and 13) 6,339,947 4,957,217 5,457,913 Inventories and supplies - net 1,462,146 1,716,673 1,136,885 Prepayments and other current assets (Note 9) 1,389,077 1,466,351 1,083,408

Total Current Assets 18,998,087 20,431,755 21,980,879

Noncurrent Assets Property and equipment - net (Notes 3, 4 and 7) 100,605,446 100,579,422 101,643,592 Investment property - net (Notes 3 and 5) 264,421 263,884 261,516 Intangible assets (Notes 3 and 6) 1,080,817 673,729 944,265 Deferred income tax - net (Note 3 and 12) 1,640,411 2,659,336 2,413,256 Investments in associates, joint venture and others - net 77,037 189,159 91,925 Other noncurrent assets - net of current portion (Note 9) 2,082,957 2,446,693 2,368,498

Total Noncurrent Assets 105,751,089 106,812,223 107,723,052

P=124,749,176 P=127,243,978 P=129,703,931

LIABILITIES AND STOCKHOLDERS’ EQUITY Current Liabilities Accounts payable and accrued expenses (Notes 4, 13 and 17) P=15,093,127 P=14,379,261 P=14,101,992 Unearned revenues 2,304,049 1,959,317 1,732,747 Current portion of: Long-term debt (Note 13) 8,592,261 8,805,099 9,018,650 Other long-term liabilities (Notes 4, 7 and 13) 139,755 307,536 292,589

Total Current Liabilities 26,129,192 25,451,213 25,145,978

Noncurrent Liabilities Deferred income tax - net (Notes 3 and 12) 3,601,481 3,165,197 3,474,732 Long-term debt - net of current portion 44,316,329 43,270,191 43,199,301 Other long-term liabilities - net of current portion (Note 4) 2,959,919 3,277,744 3,377,015

Total Noncurrent Liabilities 50,877,729 49,713,132 50,051,048

Total Liabilities 77,006,921 75,164,345 75,197,026

Stockholders’ Equity (Note 8) Paid-up capital 39,493,040 39,434,903 39,435,577 Cumulative translation adjustment (Notes 1 and 13) (265,298) – – Cost of share-based payment (Note 10) 273,923 145,569 193,096 Retained earnings 24,109,018 20,691,931 23,071,002 Treasury stock - common (15,868,428) (8,192,770) (8,192,770)

Total Stockholders’ Equity 47,742,255 52,079,633 54,506,905

P=124,749,176 P=127,243,978 P=129,703,931

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

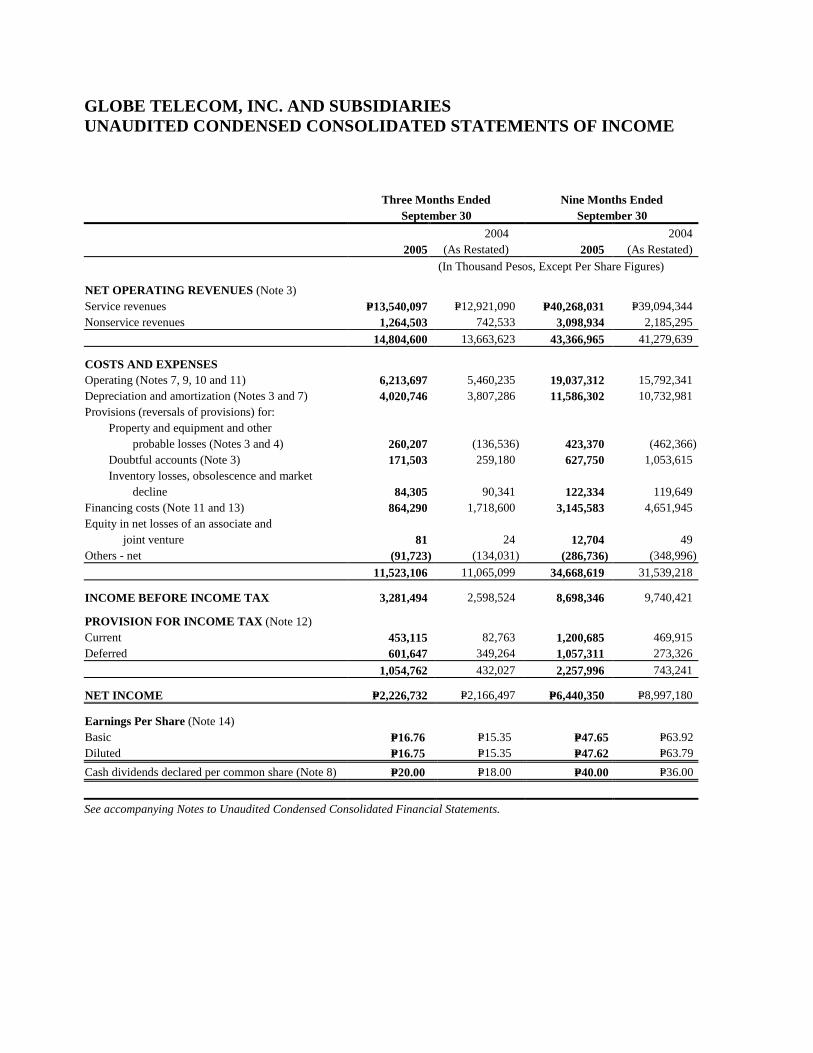

GLOBE TELECOM, INC. AND SUBSIDIARIES UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF INCOME

Three Months Ended

September 30 Nine Months Ended

September 30

2005 2004

(As Restated) 2005 2004

(As Restated)

(In Thousand Pesos, Except Per Share Figures)

NET OPERATING REVENUES (Note 3) Service revenues P=13,540,097 P=12,921,090 P=40,268,031 P=39,094,344 Nonservice revenues 1,264,503 742,533 3,098,934 2,185,295

14,804,600 13,663,623 43,366,965 41,279,639

COSTS AND EXPENSES Operating (Notes 7, 9, 10 and 11) 6,213,697 5,460,235 19,037,312 15,792,341 Depreciation and amortization (Notes 3 and 7) 4,020,746 3,807,286 11,586,302 10,732,981 Provisions (reversals of provisions) for: Property and equipment and other

probable losses (Notes 3 and 4)

260,207 (136,536) 423,370 (462,366) Doubtful accounts (Note 3) 171,503 259,180 627,750 1,053,615 Inventory losses, obsolescence and market

decline

84,305 90,341 122,334 119,649 Financing costs (Note 11 and 13) 864,290 1,718,600 3,145,583 4,651,945 Equity in net losses of an associate and joint venture

81 24 12,704 49

Others - net (91,723) (134,031) (286,736) (348,996)

11,523,106 11,065,099 34,668,619 31,539,218

INCOME BEFORE INCOME TAX 3,281,494 2,598,524 8,698,346 9,740,421

PROVISION FOR INCOME TAX (Note 12) Current 453,115 82,763 1,200,685 469,915 Deferred 601,647 349,264 1,057,311 273,326

1,054,762 432,027 2,257,996 743,241

NET INCOME P=2,226,732 P=2,166,497 P=6,440,350 P=8,997,180

Earnings Per Share (Note 14) Basic P=16.76 P=15.35 P=47.65 P=63.92 Diluted P=16.75 P=15.35 P=47.62 P=63.79

Cash dividends declared per common share (Note 8) P=20.00 P=18.00 P=40.00 P=36.00

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

GLOBE TELECOM, INC. AND SUBSIDIARIES UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

Capital

Stock*

Additional

Paid-in Capital - Common

Treasury

Stock - Common

Cost of

Share-Based Payment

Cumulative

Translation Adjustment

Retained

Earnings Total

For The Nine Months Ended September 30, 2005 (In Thousand Pesos) As of January 1, 2005,

as previously reported P=8,323,023 P=31,111,790 (P=8,192,770) P=– P=– P=25,774,446 P=57,016,489

Effect of changes in accounting

policies (Notes 2 and 10) – 764 – 193,096 – (2,703,447) (2,509,587)

Cumulative effect of change in

accounting policy for financial

instruments as of January 1, 2005

(Notes 2 and 13) – – – – (151,008) 33,686 (117,322)

As of January 1, 2005, as restated 8,323,023 31,112,554 (8,192,770) 193,096 (151,008) 23,104,685 54,389,580

Changes in fair value of cash flow

hedges (164,712) – (164,712)

Transferred to income and expense

for the period 27,740 – 27,740

Tax effect of items taken directly to

or transferred from equity 43,830 – 43,830

Changes in fair value of available-for-

sale equity investments (21,148) – (21,148)

Net income recognized directly in

equity (114,290) – (114,290)

Net income for the period 6,440,350 6,440,350

Total recognized income for the period (114,290) 6,440,350 6,326,060

Acquisition of treasury shares for the

period (Note 8) – – (7,675,658) – – – (7,675,658)

Dividends on common stock (Note 8) – – – – – (5,436,017) (5,436,017)

Cost of share-based payment – – – 121,566 – – 121,566

Collections of subscriptions

receivable - net of refunds 9,481 – – – – – 9,481

Exercise of stock options - net of

related expenses 2,967 45,015 – (40,739) – – 7,243

As of September 30, 2005 P=8,335,471 P=31,157,569 (P=15,868,428) P=273,923 (P=265,298) P=24,109,018 P=47,742,255

For The Nine Months Ended September 30, 2004 (In Thousand Pesos) As of January 1, 2004,

as previously reported P=8,307,828 P=31,110,194 (P=8,192,770) P=– P=– P=19,628,747 P=50,853,999

Effect of changes in accounting

policies (Note 2) – – – 59,090 – (2,842,323) (2,783,233)