comparative analysis of company’s

TRANSCRIPT

i

COMPARATIVE ANALYSIS OF COMPANY’S

FINANCIAL PERFORMANCE OF PRE AND POST

MERGER

(Case Study: PT Bank CIMB Niaga Tbk year 2002 – 2007 and 2009

- 2014)

By

Vany Hummaira Ziqra

ID No. 014201100076

A Skripsi presented to the

Faculty of Business President University

in partial fulfillment of the requirements for

Bachelor Degree in Economics in Management

February 2015

ii

SKRIPSI ADVISER

RECOMMENDATION LETTER

This skripsi entitled “COMPARATIVE ANALYSIS OF

COMPANY’S FINANCIAL PERFORMANCE OF PRE AND POST

MERGER (Case Study: PT Bank CIMB Niaga Tbk year 2002 - 2007

and 2009 -2014)” prepared and submitted by Vany Hummaira Ziqra in

partial fulfillment of the requirements for the degree of Bachelor in the

Faculty of Business has been reviewed and found to have satisfied the

requirements for a Skripsi fit to be examined. I therefore recommend this

Skripsi for Oral Defense.

Cikarang, Indonesia, January 21st 2015

Acknowledged by, Recommended by,

Vinsensius Jajat Kristanto SE., MM., MBA. Purwanto, ST, MM

Head of Management Study Program Advisor

iii

DECLARATION OF ORIGINALITY

I declare that the Skripsi, entitled “COMPARATIVE ANALYSIS OF

COMPANY’S FINANCIAL PERFORMANCE OF PRE AND POST

MERGER (Case Study: PT Bank CIMB Niaga Tbk year 2002 - 2007

and 2009 -2014)” is to the best of my knowledge and belief, an original

piece of work that has not been submitted, either in whole or in part, to

another university to obtain a degree.

Cikarang, Indonesia, February 3rd 2015

VANY HUMMAIRA ZIQRA

iv

PANEL OF EXAMINERS

APPROVAL SHEET

The Panel of Examiners declares that the Skripsi entitled

“COMPARATIVE ANALYSIS OF COMPANY’S FINANCIAL

PERFORMANCE OF PRE AND POST MERGER (Case Study: PT

Bank CIMB Niaga Tbk year 2002 - 2007 and 2009 -2014)” that was

submitted by Vany Hummaira Ziqra majoring in Management from the

Faculty of Business was assessed and approved to have passed the Oral

Examinations on February 3rd

, 2015

Ir. Yunita Ismail Masjud, M.Si

Chair – Panel of Examiners

Filda Rahmiati, BBA., MBA

Examiner 1

Purwanto, ST, MM

Examiner 2

v

ABSTRACT

This research aims to identify and find out the comparison of financial performance

of Bank CIMB Niaga of pre and post merger. Through purposive sampling with

secondary data from Bank CIMB Niaga financial statement, this research has got 22

samples from pre merger period which is on 2002 – 2007 as well as 22 samples from

pre merger period which is on 2009 – 2014 with 5 indicators of financial ratios which

are CAR, NPL, OER, LDR and ROE. This research uses quantitative research which

using some analysis methods such as descriptive statistic, normality testing by using

Kolmogorov-Smirnov test method, and hypothesis testing by using paired sample t-

test. The result of this study is that CAR and LDR’s post merger is significant higher

than pre merger then NPL, OER, and ROE’s post merger is lower than pre merger.

Among those 5 variables, LDR is having the most significant difference as it has the

highest of difference of average which is 9.8%. Compared based on the performance

of both periods, CAR, NPL, OER, and LDR of post merger has better performance

rather than in pre merger period. Conversely, ROE is not showing better performance

in post merger period.

Keywords: Pre Merger, Post Merger, CAR, NPL, OER, LDR, ROE

vi

ACKNOWLEDGE

Alhamdulillah all praise and gratitude to Allah SWT, the Blessed One, the Worthy

One, the fully Enlightened One. Shalawat and Salam are poured out to the Great

Prophet Rasulullah Muhammad SAW along with family, friends and followers until

the end of time.

This is the happiest moment after struggling with my undergraduate research and

obtaining my bachelor degree at President University. In this preface, the researcher

would like to express special sincere gratitude to:

a. My beloved Mom and Dad. Hard to describe my gratitude to both of you in

words, I am so glad to have parents like mom and dad who has been very

supportive and care as well as never stop to pray for all the time. I love you so

much.

b. My beloved brothers who cares a lot.

c. My Skripsi adviser, Mr. Purwanto. Thank you so much for your guidance,

attention, patience, and kindness for the betterment of the thesis.

d. To my beloved Banking and Finance 2011, especially to Agunda

Fistariansyah, Irlia Arni, Olga Arthaloka, Jessica Tiur, Novia Utami, Ety,

Raeny TJ, Zikra Azhara, Maria Octaviany, Vanny Christina, Tifani Indah,

Helmy Zulfa, Haniel Imanuel, Yorico Lampus, Nguyen Tuan Anh, Fellucia,

Ikhwan Aditya, and others. Thanks for being best college mates, all sharing

and caring. See you on top guys!

e. To my beloved best mates, Ryanda Rusadi, Erdy Anugrah, Tiara Anisa,

Firdha Aulia who always give huge support, love and care.

f. To Bosses and Colleagues in Citibank who support and make me keep spirit

in finishing this Skripsi. Thanks for caring and supporting during this hard

time.

vii

g. To Triputra Group as well as Triputra scholarship friends who support me in

obtaining the bachelor degree.

h. To all lecturers and staff of President University for supporting the research in

doing this Skripsi.

Without them, the researcher will not able to through the hard time in college life

until finish this research. Last but not least, the researcher would like to apologize for

being unable to mention other contributing person’s name one by one. Thanks for

you all.

viii

TABLE OF CONTENTS

SKRIPSI ADVISER RECOMMENDATION LETTER……………..……………… i

DECLARATION OF ORIGINALITY……………………………………………… ii

PANEL OF EXAMINERS APPROVAL SHEET………………………………...... iii

ABSTRACT……...………………………………………………………….……… iv

ACKNOWLEDGE .…………………………………………………………….….... v

TABLE OF CONTENTS……………………………………………………..…….. vi

LIST OF TABLES...................................................................................................... ix

LIST OF FIGURES ....….……………………………………………………..….…. x

LIST OF ACRONYMS ..........…………………………………………………..….. xi

CHAPTER I: INTRODUCTION……………………………………………………..1

1.1 Background of Study.…………………………………………………………1

1.2 Problem Identification...……………………………………………………... 8

1.3 Statement of Problem.……………...………………………………………... 8

1.4 Research Objective..……………...………………………………………….. 9

1.5 Research Limitation.…..……………………………………………………. 10

1.6 Definition of Terms.…...……………………………………………..…….. 10

1.7 Benefit of the Study.………………………………………….………...…... 11

CHAPTER II: LITERATURE REVIEW……………………………………………13

2.1 Theoretical Review.………...…………………………………...………….. 13

2.1.1 Bank.…..……………………………………...………………….…. 13

ix

2.1.2 Single Presence Policy……………………...……………………… 15

2.1.3 Merger.…...………………………………………………………… 16

2.1.4 Financial Performance.…………………………………………….. 28

2.1.5 The influence of merger towards the improvement of company’s

financial statement.………………………………………………..... 29

2.1.6 Financial ratios analysis.……….…………………………………... 30

2.2 Previous Research.………….…………………………………………….... 35

2.3 Theoretical Framework..…………………………………………………… 38

2.4 Hypothesis……………………………………………………….…………. 40

CHAPTER III: RESEARCH METHODOLOGY…………………………………...41

3.1 Research Method………………………………………….………………... 41

3.2 Research Framework.………………………………………………………. 42

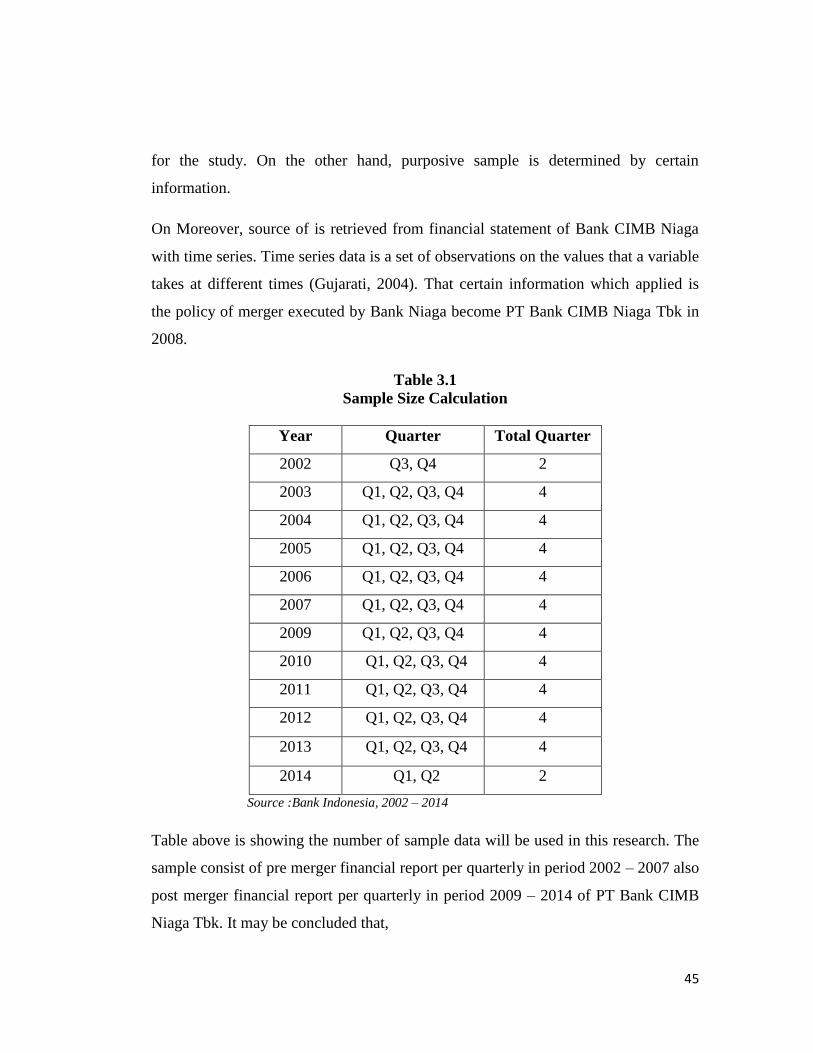

3.3 Research of Data.……………………………………………….………....... 43

3.4 Sampling Design………………………………………………….………... 44

3.5 Operational Definition………………………………………….………….... 46

3.6 Research Instruments.………………………………………………………. 47

3.7 Method of Data Analysis.………………………………………………..…. 48

3.7.1 Descriptive statistic.……..………………………………………….. 48

3.7.2 Normality testing.…………..………………………………………. 48

3.7.3 Hypothesis Testing………………………………………………….. 49

3.7.4 Paired Sample t test.…….………………………………………….. 49

CHAPTER IV: ANALYSIS OF DATA AND INTERPRETATION OF RESULT...52

4.1 Company Profile……………………………………………………..……... 52

4.2 Data Result Analysis…………………………………………………..…… 55

x

4.2.1 Object statistical description……………………………………..… 55

4.2.2 Descriptive statistics of research variable.……….…….……………. 67

4.2.3 Normality testing.………………………………..…….…………… 70

4.2.4 Hypothesis testing.………………………………………………….. 72

4.2.5 Paired sample t test.………………………………………………… 72

4.3 Interpretation of Result.…………………......…………………………….... 77

4.3.1 CAR’s performance of post merger is significant higher than pre

merger...…………………………………………………………...... 77

4.3.2 NPL’s performance of post merger is significant lower than pre

merger..........................................................................................…... 78

4.3.3 OER’s performance of post merger is significant lower than pre

merger..........................................................................................…... 78

4.3.4 LDR’s performance of post merger is significant higher than pre

merger..........................................................................................…... 79

4.3.5 ROE’s performance of post merger is significant higher than pre

merger………………………………………………………......…... 79

4.3.6 The most difference of ratio in pre and post merger.……………..... 81

4.3.7 The performance of Bank CIMB Niaga of post merger.……………82

CHAPTER V: CONCLUSION AND RECOMMENDATION……………………. 83

5.1 Conclusion………………………………………………………………….. 83

5.2 Recommendation…………………………………………………………… 86

REFERENCES…………………………………………………………………....... 87

APPENDICES………………………………………………………………………. 92

xi

LIST OF TABLES

Table 3.1 Sample Size Calculation….………………………………….………45

Table 3.2 Operational Definitions and Variable………………...……………..46

Table 4.1 CAR Data in Percentage.………………………………..………......56

Table 4.2 NPL Data in Percentage.………………………………..……….......58

Table 4.3 OER Data in Percentage.………………………………..……….......61

Table 4.4 LDR Data in Percentage.………………………………..……….......63

Table 4.5 ROE Data in Percentage.………………………………..……….......65

Table 4.6 Pre merger descriptive analysis.………………………..………........67

Table 4.7 Post merger descriptive analysis.………………………..…………..69

Table 4.8 Pre merger One-sample Kolmogorov-Smirnov test.………………..70

Table 4.9 Post merger One-sample Kolmogorov-Smirnov test.…..…………..70

Table 4.10 CAR Paired sample test……………………………………………. 73

Table 4.11 NPL Paired sample test…………………………………………….. 74

Table 4.12 OER Paired sample test…………………………………………….. 75

Table 4.13 LDR Paired sample test…………………………………………….. 76

Table 4.14 ROE Paired sample test…………………………………………….. 77

Table 4.15 Summary of hypothesis result……………………………..………...78

xii

LIST OF FIGURES

Figure 1.1 Transition logo of Bank Niaga and Lippo Bank become Bank CIMB

Niaga………………………………………………………………… 5

Figure 1.2 Bank CIMB Niaga Position in Banking Industry of Pre Merger..........5

Figure 1.3 Bank CIMB Niaga Position in Banking Industry of Post Merger…....6

Figure 2.1 Merger illustration...………………………………………………….18

Figure 2.2 Acquisition Illustration………………………………..……...….…...19

Figure 2.3 Consolidation Illustration………………..…………………...………..20

Figure 2.4 Theoretical Framework...………………………………………………..38

Figure 3.1 Research Framework……………………………………….…..….42

Figure 4.1 Merger Implementation of Bank Niaga and Lippo Bank …...…….....54

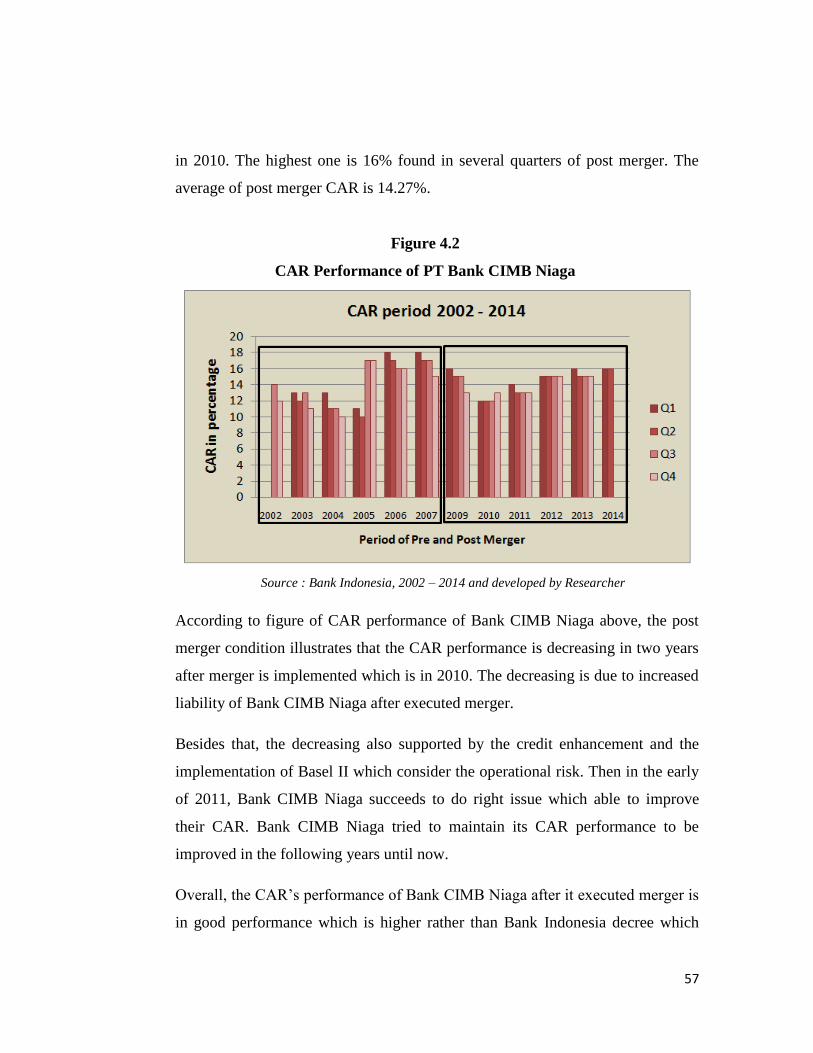

Figure 4.2 CAR Performance of PT Bank CIMB Niaga…………………….….58

Figure 4.3 NPL Performance of PT Bank CIMB Niaga…………………….…..60

Figure 4.4 OER Performance of PT Bank CIMB Niaga…………………….….62

Figure 4.5 LDR Performance of PT Bank CIMB Niaga…………………….….64

Figure 4.6 ROE Performance of PT Bank CIMB Niaga………………………..66

xiii

LIST OF ACRONYMS

API = Arsitektur Perbankan Indonesia

BCHB = Bumiputera-Commerce Holdings Berhard

BPPN = Badan Penyehatan Perbankan Nasional

CAHB = Commerce Asset Holding Berhard

CAR = Capital Adequacy Ratio

DPNP = Direktur Direktorat Penelitian dan Pengaturan Perbankan

IMF = International Monetary Funds

LDR = Loan to Deposit Ratio

LOI = Letter of Intent

NPL = Non Performing Loan

OER = Operating Efficiency Ratio

PBI = Peraturan Bank Indonesia

PSAK = Pernyataan Standar Akuntansi Keuangan

ROE = Return on Equity

SE = Surat Edaran

SME = Small Medium Enterprise

SPP = Single presence Policy

TDF = Third Party Funds

1

CHAPTER I

INTRODUCTION

1.1 Background of Study

The existence of bank is very important in supporting and improving the economy of

society since almost every economy transaction in the community must be related to

the bank. According to Indonesian Law No. 10 of 1988 in article 1 point 2 about

banking, bank is the business entity which gathers funds from society in the form of

saving and channels it to society in the form of credit and other forms in order to

increase the people’s livelihood.

The history also shows the economic development was in line with the development

of banking institutions. According to article 4 year 1992, banking industry has an

active role in advancing the economy of a country. Bank which serves to transmit the

fund in the form of credits to the community help the provision of venture capital so

it can move the real sector. The better the real sector, it will affect to on the rising

national income.

The development of economic growth requires the existence of competing banks to

develop strategies in order to continue to grow and maintain its presence in the

current era of globalization. This effort is done so that the existing banks are not

returning crash as happened in 1997during the financial crisis in Asia which also

affect to Indonesian economy. Indonesia became the most devastated country since

this crisis does not only affect to the economic but also significantly affect to

political system and social situation in Indonesia (Indonesia-investments,2011).

The financial crisis in 1997 also resulted in the decline of the banking sector then

resulting in the government was forced to do tightening liquidity. These conditions

led to a crisis of confidence community against national banks, especially after the

2

revocation of licenses 16 banks on November 1st, 1997. This impact is very bad,

especially triggered the depreciation of confidence in the banking system. As a

manifestation of the crisis of confidence, withdrawals occurred on a large scale.

As a result, many banks are experiencing big liquidity problems (mismatch),

followed by the scarcity of liquidity in the economy as a whole (liquidity crunch).

The situation is exacerbated by the soaring interest rates Interbank Money Market

(Interbank) up to 300% per year. However, actually the liquidation action was

conducted to avoid the spread of banking crisis (systematic risk) and the magnitude

of risk borne by the community (economic cost). Besides that, the liquidation

decision is also the evaluation result and IMF recommendation which written on

Letter of Intent (LoI) between government and IMF on October 31st, 1997 (Bank

Indonesia).

Reflecting to bad experience in financial crisis occurred at 1997 and 1998 which also

resulted in decline of banking, so the strong national banking fundamental is

extremely needed. These things are supported also by Bank Indonesia as the central

bank which issues the Indonesian Banking Architecture (API) which a basic

framework of the Indonesian banking that is comprehensive and gives direction,

shape, and the structure of banking industry for a span of five to ten years into the

future. This policy based on the vision of a healthy banking system in order to create

strong and efficient financial system stability to help drive the growth of national

economy. That thing is done in order to strengthen the internal condition of the

national banking, realize the complete infrastructure and support the creation of a

healthy banking industry. API has six strong pillars which have to be owned by

healthy, strong and efficient banking system which are healthy banking structure,

effective regulatory system, effective and independent oversight system, strong

banking industry, adequate supporting infrastructure, and consumer protection

(Benny, 2007).

3

In order to implement the concept of API, according to Burhanudin Abdullah (2006)

on his book state that in strengthening of Pillar I of the national banking structure and

pillar III, the increasing effectiveness of the system of banking supervision in an

independent and effective, Bank Indonesia as the central bank as well as the

supervisor issued a policy called the policy package in October 2006. One of the

policy package in October 2006, known as Pakto 2006 was the single presence policy

(SPP). SPP is regulated in Bank Indonesia Regulation No. 8/16 / PBI / 2006 dated

October 5, 2006, then set in regulation of Bank Indonesia policy No. 9/12 / PBI /

2006 on article 1, paragraph 2, which states that SPP is a condition where a party just

become the controlling shareholder of the bank.

In addition, SPP also caused by the free trade system which has brought significant

effects to economy system in Indonesia, one of the effects is foreign investors easier

to conduct business transactions in Indonesia one of them is through banking

industry. Based on these conditions, here is the role of SPP in helping Bank

Indonesia to oversee the commercial bank and reduce the number of banks in

Indonesia. Decreasing the number of banks in Indonesia can improve the

effectiveness of supervision of Bank Indonesia. By SPP also, it implies the

controlling shareholders who have a controlling stake of more than one bank have to

choose whether to do the divestiture, merger, or form a bank of holding company.

The policy affected to Bank CIMB Niagawhich the result of Bank Niaga and Lippo

Bank’s merger. The Government of Republic of Indonesia for some time has ever

been a majority shareholder of Bank CIMB Niaga current financial crisis in the late

1990s. In November 2002, Commerce Asset-Holding Berhard (CAHB), now known

as CIMB Group Holdings Berhard (CIMB Group Holdings), acquired a majority

share of the Commercial Bank Restructuring Agency (BPPN). In August 2007, the

entire ownership is migrated to CIMB Group as part of an internal reorganization to

consolidate the activities of all subsidiaries of CIMB Group with universal banking

platform.

4

In a separate transaction, Khazanah which is the majority shareholder of CIMB

Group Holdings acquired majority ownership of Lippo Bank on September 30, 2005.

All share ownership is migrated then belong to CIMB Group on 28th October 2008

as part of the same internal reorganization. As the controlling shareholder of Bank

Niaga (via CIMB Group) and Lippo Bank, since 2007 Khazanah looked merger as an

effort that must be taken in order to comply with the SPP which has been set by Bank

Indonesia so that this merger is being the first merger in Indonesia regarding to SPP

Policy (Bank CIMB Niaga, 2009).

Principle permits for Niaga and Lippo bank in conducting the merger already issued

by Halim Alamsyah, as Bank of Indonesia Director of the Banking Research and

Regulation Directorate (DPNP). SPP which released by Bank of Indonesia is in line

with Niaga and Lippo Bank in conducting the merger so that the controlling

shareholders of more than one banks has to hand the business plan by the end of

2007. That business plan options is divided into merger, selling the shares or forming

the holding company. At that moment, more than 93% of Lippo Bank which owned

by Khazanah through BV Santubong Investments and Greatville Pte Ltd while the

indirect ownership on Bank Niaga is 64% through Bumiputera-Commerce Holdings

Berhard (BCHB) (Antara, 2008).

Bank Niaga and Lippo Bank represent two unique franchises and when combined,

represent one of the more exciting banking sector enterprises in Indonesia. The

merger takes advantage of Bank Niaga’s strong corporate presence and mortgage

niche together with Lippo Bank’s leadership in SME loans and payment processing

system. By combining the strengths of both banks, the merger will result in a bank

well positioned to compete and grow in the increasingly competitive Indonesian

banking environment (Bank CIMB Niaga, 2008).

Niaga and Lippo Bank agree to do merger on June 2nd

, 2008 then those merger banks

also approved by Bank of Indonesia on October 16th

, 2008. The approval was

5

accepted in the form of letter by date of October 15th

, 2008. The merger of both

banks causes PT. Lippo Bank name is missing from Indonesian banking industry

because the asset value owned by Bank Niaga is higher compared with Lippo Bank

so the total asset and liabilities of Lippo Bank is diverted to Bank Niaga and change

the name become Bank CIMB Niaga. This merger is formally announced at Graha

Niaga on November 3rd

, 2008. Thus, then Lippo Bank shares was not listed and

traded anymore at Indonesia Stock Exchange (Harun, 2008).

Figure 1.1 Transition logo of Niaga and Lippo Bank become Bank CIMB Niaga

Source: Bank CIMB Niaga, Merger Process and Achievement Report, January 2009

Figure 1.1 indicates that the new logo of Bank CIMB Niaga is a symbol the merger

result. Bank CIMB Niaga’s management realize that the name of Lippo Bank

resounds with the many activities of Lippo Group, the management deliberated that

the name of the new merged bank should build a new identity to the start of a new

chapter as part of the CIMB Group.

Figure 1.2 Bank CIMB Niaga Position in Banking Industry of Pre

Merger

Source: Bank CIMB Niaga, Merger Process and Achievement Report, January 2009

6

Figure 1.2illustrates the parable of CIMB bank existence that depicted with

combination between Bank Niaga and Lippo bank. Figure above shows that the value

of total asset Bank Niaga of pre merger is on grade 8th

around Rp60.51trillion below

Danamon Bank that has higher assets which has Rp103.46trillion while Lippo Bank

is on 12th

with total asset is Rp39.06trillion. Total asset of Bank CIMB Niaga based

on the figure shows the combination of Niaga and Lippo Bank which has Rp 99.57

trillion pre mergers. The power of Bank Niaga and Lippo Bank places the Bank

CIMB Niaga is on 6th

gradepre merger.

Figure 1.3 Bank CIMB Niaga Position in Banking Industry of Post Merger

Source: Bank CIMB Niaga Merger Process Closing Report, November 2009

Based on picture above, it shows that total asset of Bank CIMB Niaga post merger in

2009 reaches Rp101.8trillion and placed position in 5th

grade after Mandiri Bank,

BCA Bank, BRI Bank and BNI Bank. It shows the increasing of total assets before

merger when Bank CIMB Niaga is on 6th

grade. Total asset experiences a fairly

significant difference before and after merger which shows Bank CIMB Niaga did

great performance and achieved its goals to become the fifth largest bank in

Indonesia in terms of assets as stated by Nazir Razak, Group Chief Executive of

CIMB Group (Buletin Bisnis, 2008).

318,67

228,09 219,64 179,64

103,46 99,57 63,49 57,97 47,22 42,8

Total Asset (Rp Trillion)

7

Merger activities in Indonesia already existed in 1970 which implemented by banks

with aims to strengthen the structure of capital as well as to acquire tax

compensation. In the crisis condition, many companies do merger due to face of

funding problem. However, those activities are not always followed with success.

The percentage of failure also high which is around 50% up to 70% (Cartwight and

Cooper, 1993).

The impact of that merger implementation of course has considerable influence for

internal and external condition of company. One of the impacts which often come up

from the implementation of that merger is on the performance of company. The

impact on the performance of company which should be considered is from its

financial performance.

To assess the success of the company’s financial performance after conducting the

merger can be determined by comparing the financial statement by using financial

ratio as the tools to evaluate the financial performance of the company. Financial

ratios are the analysis tools used to analyze the business and financial performance at

a predetermined time. The financial ratio is used to determine the trends in Industry

which in the end will help the business in improving their activities (Asma Arshad,

2012).

Based on above phenomenon, the researcher interest to do research by analyzing the

merger’s impact of financial performance of bank by using financial ratios which are

Capital Adequacy Ratio (CAR), Non Performing Loan (NPL), Operating Efficiency

Ratio (OER), Loan to Deposit Ratio (LDR) and Return on Equity (ROE)in time

period of 2002 – 2014 quarterly. The title of research which will be analyzed and

discussed is “Comparative Analysis of Company’s Financial Performance of Pre

and Post Merger” (Case Study: PT Bank CIMB Niaga, Tbk year 2002- 2007 and

2009 - 2014).

8

This research will highlight the merger impacts on the financial performance of

organizations and their shareholders. It will be significant importance for the industry

and other firms in the industry to recognize the importance of mergers and impacts

on company’s performance and the synergies achieved through them.

1.2 Problem Identification

Currently, banking industries are experiencing the significant growth, it is evidenced

by many national and international banks contribute to the growth of the banking

industry. To realize the health banking structure as well as restructure the ownership

structure of banks in order to support the effectiveness of bank supervision, Bank

Indonesia issued the regulation No.8/16/PBI/2006 about single ownership of banks in

Indonesia where one party only can be a controlling shareholder in one bank. Merger

is one of ways to meet these conditions. In this research, the researcher focused on

analyzing the comparison on Bank CIMB Niaga financial performance of pre and

post merger. Based on the comparison, the differences of finacial performance after

merger implemented will be carefully identified.

1.3 Statement of Problem

This research is conducted to analyze the merger’s impact of financial performance

of bank. The researcher is using non probability sample to select the object which be

analyze which is Bank CIMB Niaga by comparing the financial ratios such as CAR,

NPL, OER, LDR and ROE in order to find out the comparison of financial

performance especially in post merger activity. Refers to that, the researcher has

constructed problem statements which in this research will be analyzed, which are:

1. Is CAR’s performance of post merger is significant higher than pre merger?

2. Is NPL’s performance of post merger is significant lower than pre merger?

3. Is OER’s performance of post merger is significant lower than pre merger?

4. Is LDR’s performance of post merger is significant higher than pre merger?

9

5. Is ROE’s performance of post merger is significant higher than pre merger?

6. What is the most difference on the financial ratio of Bank CIMB Niaga in pre

and post merger?

7. How is the performance of Bank CIMB Niaga of post merger?

Other performance aspects related to the merger after the implementation of merger

activity is not considered in this research including consolidation (merger that led to

the formation of a new company). Those aspects including the economic and non-

economic aspects such as the impact on technology, taxation, labor, market

expansion, distribution networks, managerial capability, customer satisfaction, and so

on that may be very affected by the implementation of merger.

1.4 Research Objective

Based on the preceding research questions, the research objectives of the study can

be translated as follows:

1. To know if CAR’s performance post merger is significant higher than pre

merger

2. To know if NPL’s performance post merger is significant lower than pre

merger

3. To know if OER’s performance post merger is significant lower than pre

merger

4. To know if LDR’s performance post merger is significant higher than pre

merger

5. To know if ROE’s performance post merger is significant higher than pre

merger

6. To know the most difference on the financial ratio of Bank CIMB Niaga of

pre and post merger

7. To know Bank CIMB Niaga’s performance of post merger

10

1.5 Research Limitation

This research is executed with certain limitation. The limitation put to make the

researcher easier but depth in understanding and analysis, so the beneficial

information can be provided to the readers and researcher-self. A limitation in this

research is regarding to the number of banks that will be chosen as the sample and

also the period of time in analyzing the research, which are:

1. The period will be used for this research is from Q3 2002 – Q2 2014. The

data is separated based on the time of period which is pre and post merger

time. Since merger was occurred in 2008, so the pre merger data will be

obtained from Q3 2002 – Q4 2007 then post merger data will be obtained

from Q1 2009 – Q2 2014.

2. The objects taken by the researcher for this research are commercial banks

which affected by single presence policy and of course listed in IDX, which is

Bank CIMB Niaga. Therefore, the research will focus on merger activity

conducted by Bank CIMB Niaga based on the impact of single presence

policy to get deeply insight of its effect especially in its financial

performance.

3. The indicators will be used are CAR, NPL, OER, LDR and ROE with aims of

this research to find the impact regarding to merger activity conducted by

Bank CIMB Niaga.

1.6 Definition of Term

In this research, some terms are used to strengthen the understanding according to

Investopedia dictionary.

1. CAR is a ratio that shows how much the entire assets banks that contain risks

(credit, equity, precious fibers, the bill other banks) participated financed

from the bank's own capital funds in addition to obtaining funds from sources

outside the bank, such as public funds, loan (debt), and others.

11

2. Financial performance is a subjective measure of how well a firm can use

assets from its primary mode of business and generate revenues. This term is

also used as a general measure of a firm's overall financial health over a given

period of time, and can be used to compare similar firms across the same

industry or to compare industries or sectors in aggregation.

3. LDR is commonly used statistic for assessing a bank's liquidity by dividing

the banks total loans by its total deposits. This number, also known as the

LDR, is expressed as a percentage. If the ratio is too high, it means that banks

might not have enough liquidity to cover any unforeseen fund requirements;

if the ratio is too low, banks may not be earning as much as they could be.

4. Merger is combination of two or more companies, generally by offering the

stockholders of one company securities in the acquiring company in exchange

for the surrender of their stock.

5. NPL is a sum of borrowed money upon which the debtor has not made his or

her scheduled payments for at least 90 days. A nonperforming loan is either

in default or close to being in default.

6. OER is a measurement of bank efficiency ratio of operating expenses to

operating income.

7. ROE is a performance metric that examines how successful a firm's

investment decisions are compared to its debt situations. A negative value

denotes that the firm did not make an optimal decision, because interest

expenses were greater than the amount of returns generated by investments.

1.7 Benefit of the Study

Through this research hopefully could provide benefit, knowledge, information, and

suggestion which can be used for:

12

1. Researcher

To find out deeply about the comparison of the financial performance of a

company pre and post merger which focused on Bank of CIMB Niaga. Then,

to be able to understand in detail how is the function of financial ratios to

measure the financial performance so the research will enrich the knowledge

of researcher about financial matters as the researcher study concentration

which is Banking and Finance.

2. Company and customers

(i) Through this research, the company can find out the comparison of

financial performance of pre and post merger. Then become

references and consideration to the company in choosing the merger

as its strategy to keep its existence and compete with others in this

globalization era.

(ii) As the consideration of the investors to invest their funds in Bank

CIMB Niaga as well as the Investors could determine the prospect of

the investment and reference of company’s image.

3. University students and academics

There are few benefits of the research for university students as well as

academics

This research can be used as the guidance and reference for students as well

as to academics who want to analyze the comparison of financial performance

of Bank CIMB Niaga of pre and post merger.

13

CHAPTER II

LITERATURE REVIEW

2.1 Theoretical Review

2.1.1 Bank

Bank has an important role in economics. The primary role of Bank is to take in

funds (deposits) from those with money, pool them, and lend them to those who need

funds. Banks are intermediaries between depositors (who lend the money to the

bank) and borrowers (to whom the bank lends money). The amount banks pay for

deposits and the income they receive on their loans are both called interest.

1. Definition of bank

Decision letter of Indonesia Finance Ministry No. 792 year 1990 confirms that

bank is an entity with the activities in finance field by collecting and distributing

the funds to the community especially to finance the company’s investment.

Bank is defined as financial institutions with the main activity is to collect funds

from the public and distribute the funds back to the people as well as providing

other banking services (Kasmir, 2008:2).

According to Law No. 10 article 1 year 1988 regarding to the changes in the Law

No. 7 year 1992 about banking is “business entity which collect funds from

community in the form of saving and distribute them to the community in the

form of credit and or others form in order to improve the standard of people

living”.

14

Financial Accounting Standard (PSAK) No. 31 defines that bank is an institution

which acts as a financial intermediary between parties who have surplus of funds

and parties who need the funds, as well as an institution that serves expedite the

payment traffic.

2. Bank Types

According to Banking regulation No. 10 year 1998, Bank can be divided as

follows:

a. Based on the functions

i) Common Bank

Common bank is type of bank that provides the services in kinds of

transaction.

ii) Rural Bank

Rural bank executes the business activities conventionally or based on the

sharia principal which is not provided any services in transaction traffic in

its business activities.

b. Based on the ownership

i) State Bank

State bank is the type of bank which the ownership is belongs to

government in the form of shares.

The state banks in Indonesia such as Bank Mandiri, BRI, BNI and others.

ii) Cooperative Bank

Ownership of the bank's shares is owned by a company incorporated

cooperative. For example: Commercial Cooperative Bank Indonesia

15

iii) National Private Bank

National private bank is type of a bank which the ownership is belongs to

private institution and organization. The national private bank in

Indonesia such as Bank Central Asia (BCA), Danamon, Mega and others.

iv) Foreign Bank

Foreign bank is a type of bank which owned by the multinational

company/groups. In Indonesia, the foreign bank is just like Citibank,

Commonwealth, Bank of America, etc.

2.1.2 Single Presence Policy

Single Presence Policy is condition which only one party as controlling shareholder

at one bank (Benny Soewita, 2008). This policy has objective to achieve a healthy

and strong banking structure, realignment of bank ownership structure as well as to

support the effectiveness of bank supervision. This thing is confirmed by Bank

Indonesia regulation No: 8/16/PBI/2006 article 1, no. 3 which explains the

controlling shareholder is legal entity and or individual or group of business which:

1. Having the bank shares by 25% or more of the issued shares of bank and have

voting rights

2. Having the bank shares less than 25% of the issued shares of bank and have

voting rights but it can be proven that already controlled the bank either

directly or indirectly

The provision regarding to single presence policy is excluded for (Bank Indonesia

regulation No: 8/16/PBI/2006, article 2, paragraph 2):

1. Controlling shareholder in two banks and each of them is conducting the

business activities with different principles, namely conventional and sharia

principles.

2. Controlling shareholder in two banks which one of them is joint venture bank

16

3. Holding company bank, legal entity which is formed and or owned by

controlling shareholder to consolidate and control directly all of bank

activities which is its subsidiaries.

Parties who already became the controlling shareholder on more than one bank are

obligated to do adjustment the ownership structure as follow (Bank Indonesia

regulation No: 8/16/PBI/2006, article 3, paragraph 1):

1. Transferring the part or all of its share to one or more banks under its control

to other parties so that only a part is being part of controlling shareholder in

one bank

2. Do the merger or consolidation of banks which is on its control

3. Forming the holding company by:

a. Establishing new legal entity as holding company bank

b. Designating one of banks under its control as holding company bank

The ownership structure adjustment is done within a period the latest is December

2010. According to the demand of controlling shareholder and banks under his

control, Bank Indonesia is able to give the extension period of ownership structure

adjustment if based on Bank Indonesia the high complexity problem faced by

controlling shareholder or banks under his control because the adjustment of

shareholders cannot be completed with that time period. (Bank Indonesia regulation

No: 8/16/PBI/2006, article 7, paragraph 1 and 2)

2.1.3 Merger

In this globalization era, companies are competing to be the market leader. Strategies

are created to keep maintaining the existence in their industry. One of those strategies

which often found is merger. Merger is the process of two or more companies in

which companies take control will remain standing while the merged entity will

disappear.

17

The parties that still alive or who receives merger called surviving firm or party

whose to issue shares (issuing firm) while companies who stop and scatter after

merger is called merger firm. Surviving firm has larger size due to all of assets and

liabilities of merger firm are transferred to the surviving firm. Merged companies

will leave its legal status as a separate entity and after merger the status changed into

parts (business unit) under surviving firm. Thus, merged firm is unable to act of law

on his own name (Abdul Moin, 2003:6).

According to Scott C. Whitaker (2012), merger is often used as an effort in the

process of merging companies. Merger could be done internally and externally. The

internal merger occurs when the target companies is on the same possession group

while external merger occurs when the target companies is on different possession

group.

1. Difference between merger, acquisition and consolidation

In business is very often found the misunderstanding of defining merger.

Understanding about mergers often in equate with the terms of acquisition which

actually those terms is containing different sense. The other combination of merger is

consolidation.

a. Merger

Regulation of Indonesia government No. 27 year 1998 about merger,

consolidation, and acquisition limited liability companies is defining merger as

follow:

“Merger is legal activity which done by a company or more to merge with

another existing company and then the merging company be liquidated”.

Financial Accounting Standard (PSAK) No. 22 defines that merger is a process of

merger attempt by taking over one or more other companies. After the takeover

occurred so a company that taken over being dissolved or liquidated, so that its

18

existence as a legal entity disappeared, thus its business activities continued by a

company who took over.

The merger will provide synergies to other banks that still keep their existence.

Merger is also one way for the development and growth of the bank. Through the

merger, the banks merge and divide the resources at their disposal to achieve a

common goal. Typically in a merger of the shareholders of the bank who joined

the often remain in the position as co-owners combined entity (Munir Fuady,

2002).

Figure 2.1 Merger illustration

Source: Munir Fuady, 2002

According to several of merger definition above, it can be conclude that merger is

a process of combining two or more companies in which companies take control

will remain standing while the merged entity will disappear.

b. Acquisition

Acquisition is another way of business amalgamation. Company is able to raise

the target company as its subsidiaries, in other words, either the acquiring

company or target company will remain standing (Agus Sartono, 2001).

In the business terms, acquisition can be defined as takeover ownership or control

of the share or assets of an enterprise by another enterprise, and in both

companies who take control or who taken control will be exist as a separate legal

entity (Abdul Moin, 2003).

19

Financial Accounting Standard (PSAK) No. 22 defines that acquisition is the

form of company’s ownership takeover by acquirer so will transfer the control of

acquired entity (acquire). Company’s control which questioned is the power to:

i) Manage the financial and operation policies of the company

ii) Appoint and dismiss the management

iii) Acquire the majority of voting rights in the editorial meeting.

Basically, Acquisition is different with merger since acquisition does not cause

other parties dismissed as legal entity. Companies involved in the acquisition of

juridical still stands and operate independently but has been transferred by the

acquirer. Compared with shareholder of acquirer company, most of target

company’s shareholders will obtain many benefits in the acquisition process.

These things could happen when the tender of takeover, many companies are

participating so the share dealing of company becomes higher.

Figure 2.2 Acquisition Illustration

Source: Munir Fuady, 2002

c. Consolidation

According to regulation of Indonesia government No. 27 year 1998 about merger,

consolidation and acquisition limited liability companies is defining

consolidation as follow:

20

“Consolidation is legal act performed by two or more to consolidate by

forming new company and each of them who are consolidating becomes

dismissed”.

According to Abdul Moin (2007) defines consolidation is legal act which done by

both companies or more to consolidate and each of those company that

consolidate become dismissed”.

Figure 2.3 Consolidation Illustration

Source: Munir Fuady, 2002

2. Types of merger

According to Lawrence J Gitman (2009:766) defines types of merger based on

economic activities that serves to get new technologies, reduces tax payers, expands

the access to distributors, customers, products, purveyors, and creditors. Those types

of mergers are:

a. Horizontal Merger

Horizontal Merger is merger between two or more companies in the same

industry. It occurs between firms who operate in the same space, often as

competitors offering the same good or service.

b. Vertical Merger

Vertical Merger is integration which involving the companies in the

production or operation process. It occurs when two or more firms, operating

at different levels within an industry's supply chain, merge operations. Most

21

often the logic behind the merger is to increase synergies created by merging

firms that would be more efficient operating as one.

c. Conglomerate Merger

Merger between two or more companies which each of them moves in the

unrelated industry. There are two types of conglomerate mergers: pure and

mixed. Pure conglomerate mergers involve firms with nothing in common,

while mixed conglomerate mergers involve firms that are looking for product

extensions or market extensions.

d. Market Extension Merger

Merger which done by two or more companies that have objective to expand

the market. The main purpose of the market extension merger is to make sure

that the merging companies can get access to a bigger market and that ensures

a bigger client base.

e. Product Extension Merger

Merger which done by two or more companies in order to expand the line of

company’s product. It allows the merging companies to group together their

products and get access to a bigger set of consumers. This ensures that they

earn higher profits.

3. Merger motives

According to Lawrence J Gitman (2009:764), merger motives as follow,

a. Growth or Diversification

Company which has objective of market shares growth. Companies can

achieve the same goals in a short time in combining the companies. This

strategy more save on the cost compared with floating production capacity

required.

22

b. Synergy

Merger synergy is economies scale resulted by overhead of the company

combined which lower. The clearer synergy is when the company do merger

with other company in the same field since many of the functions excessive

and employees could be deducted. It could reduce the production cost.

c. Fund Raising

Companies are merging to improve their skills in raising the funds. Company

cannot obtain the funds to have internal expansion, however they can obtain

external funds merger. The objective of this merger allows the funds raised

externally with the lower cost.

d. Increased Managerial Skill or Technology

Company will have good potential that it finds itself cannot fully develop due

to shortage in certain areas of the management or the absence of product

needed or production technology needed. Merger which done to complete the

lack of technology field.

e. Tax Consideration

Tax consideration is one of the key motives to merger. Generally, tax benefits

derived from the fact that one of company has tax loss forward.

f. Increased Ownership Liquidity

The merger of small and big companies can provide smalls business owners

with greater liquidity. This is due to higher selling power associated with a

large company shares.

g. Defense against Takeover

To be more effective, a defensive takeover must create the value for

shareholders and they will realize after the company is merged with other

company.

23

4. Processes of merger

According to Estanol and Jo (2005), there are three stages in doing merger which are,

a. Pre – Merger

This stage is the situation before merger which in this stage, the task of entire

board of directors and management of the two or more companies is

collecting the competent and significant information for the benefit of the

merger of the company so it can happen that the synergy of the merger will be

carried out.

b. Merger

When company decides to do merger, thing to do for the first time in this

stage is adjustment and mutual integrate themselves with their partners, so the

synergy can occurs.

c. Post – Merger

In this stage, there are some steps should be done by company. The first step

is by restructuring which often occurs in merger is the leadership dualism that

will bring bad influence in organization. The second step is by building a new

culture in which this culture can be a combination of both company’s culture

or also can be a completely new culture for the company. The third step is by

smoothing the transition which should be done in this case is to build a

partnership also can be a combined team or mutual cooperation.

5. Factors that determine the success of merger

The success of a merger depends heavily on the accuracy of the analysis and

thorough research on the factors aligning or compatibility between organizations that

will join. Neil M. Kay (1997) in his book, Pattern in Corporate Evolution, stated that

merger and acquisition will be success if among companies will join has a market

and technological links. Robins (2000) in his book, Organizational Behavior,

explained that the compatibility of organizational culture which will join in a merger

24

is often non-economic factors are crucial in supporting the success of merger itself.

While Pringle and Harris (1987) in his book, Essentials of Managerial Finance,

consider that financial performance of merged company is crucial factor should be

considered when two or more companies will join.

a. Factors of markets and marketing

According to Neil Kay (1997), the company can succeed in doing merger if

there is similarity in the market which he described as market linkages. One

of the expected results of merger is synergy generated by increasing the

company access to a new market that has not been touched.

Potential sources in this case are combining the market opportunities by

market share respectively occupied (cross marketing). With a boarder product

line, every company can sell more products to customers of that has been

done. This cross marketing allows each company to increase its revenue very

quickly. Thus, enabling cross selling that will increase the company’s

revenues result of mergers and acquisition. For example, a means of cross

marketing is one of product’s brand powers will give effect to the others

product which generated from the result of merger and acquisition.

The sustainability of company is highly dependent on the positive market

toward what they offer. Even though it has the ability to produce quality

goods or services if market does not have positive response so the company

will not earn profit while profit is fundamental to the survival of a company.

b. Factors of technology

According to Neil Kay (1997), company can execute merger and acquisition

if there is similarity in technology resources and production that he said as

technological linkages. This technological linkage can include the

incorporation of the production process due to the sample process as was the

case in horizontal mergers.

25

The process of product development also can be a means of achieving

synergies of information technology in the organization. When the same

technology used, the potential synergy can be created. By doing merger and

acquisition process in a healthy potential synergies will result the useful

economy of scale and scope. Technology can be defined as the ability of

production and innovation owned by company which is reflected from

qualifications of human resources, skills, and expertise they have, the type of

product they over as well as the capital goods equipment they use.

This is where the policy makers also need to be careful. Do not let the

company resulted from merger and acquisition instead become unproductive

due to technological gap.

c. Factors of culture

Organizational culture is one of non economic factors that really important to

be considered when two or more companies will do merger and acquisition.

In some of merger’s case in companies, the problem of culture is often

become a crucial problem. The difference of cultural backgrounds among

employee can cause the employee are reluctant to cooperate, each are trying

to do something based on the way of method that they have been done for a

long time, to be able to adapt often takes a long time.

Organizational culture is defined by Robins (2000) as shared perceptions

adopted by the members of organization. Schein (1997) stated that the

organizational refers to shared system adopted by the members which

distinguishes the organization from others. While Kotter and Heskett (1992)

explained that in a organization, culture represents the value and how that is

shared by those involved in organization. The value itself viewed as basic

beliefs about what should or should not to be done and what is important and

what is not important to the organization.

26

This difference of culture can cause conflicts. The impact is the cooperation is

hard to created, weak organizational cohesiveness, synergy is not created, the

productivity of company eventually result of mergers and acquisitions as well

be worse than before.

Differences in organizational culture can certainly be resolved, because

culture itself is something that can be changed. But it takes time and ability to

manage the change properly. Therefore prior to mergers and acquisitions

carried out would need to be prepared models of cultural transition that can be

accepted and followed by all components in each company will mergers and

acquisitions.

d. Factors of financial

One of the reasons why mergers and acquisitions is implemented is the

expectation of the synergy through the resources combination of some

company.

From financial sides, this synergy means the ability to generate the profit of

mergers and acquisitions company which greater than the ability if each

company’s earnings before mergers and acquisitions. These synergies that

become the beginning of merger are occurred. These synergies also allow the

company can finance the mergers and acquisitions process as well as able to

give the premium dividend to the shareholders.

The synergy effect of mergers and acquisition is rooted to two activities

which are synergy in operational and financial matters. Operational synergy

can be revenue enhancement and cost reduction.

In practice, effort to increase the revenue is more difficult rather than effort to

reduce the production cost. This is because production cost is more visible

and measurable so easily identified. While synergy in financial thing is

related to the possibility of lower costs of capital gain for the company

27

resulted from merger and acquisition for company rather than before merger

and acquisition is executed.

The planners of mergers and acquisitions are likely to see the reduction of

costs as the main source of operational synergies. This cost reduction is much

more derived from economies of scale which is reduction in the cost per unit

of product generated by the improvement of production volume or company’s

operational scale.

High of the cost per unit of product come due to operational fixed costs which

only generate few outputs. Process which increases the amount of output that

subsequently resulted in a decrease in the cost per unit is usually called

spreading overhead. Another source that can reduce costs is increasing

specialization of labor and management, as well as the use of more efficient

capital goods, which is not possible at low output levels.

6. Advantages and disadvantages of merger

Merger is one common strategy implemented by the company to maintain its

existence in the industry has a lot of advantages, namely: (Abdul Moin, 2003)

a. Obtain the quick cash flow because the product and the market is already

clear

b. Obtain the ease funding or financing because creditor is more confidence with

the company that has been established

c. Obtain the employees who have experienced

d. Obtain the customers who already well established without having pioneered

from the beginning.

e. Obtain well established operational and administrative system

f. Reduce the risk of business failure because it does not need to find the new

customers

g. Save time to enter the new business

28

h. Obtain the infrastructure to achieve the faster growth

However, beside the advantages, mergers also have some disadvantages which are,

a. The process of integration which is not easy

b. Difficulty in determining accurately the value of the target company

c. The cost of expensive consultant

d. The increasing complexity of bureaucracy

e. The coordination cost which is expensive

f. Often demoralize the organization

g. Does not guarantee an increase in the value of the company

h. Does not guarantee an increase in shareholders’ wealth

2.1.4 Financial Performance

One of methods to assess the success of company is by looking at its financial

performance. Financial performance can be retrieved from company’s financial

statement which can be a consideration for investors to assess the condition of

companies.

Irham Fahmi (2006:64) defines the financial performance as follow,

“Financial performance as reflection of company’s achievement can be

interpreted as the results achieved of various activities which have done.

Financial performance which assessed based on the financial statement

presented by management will give meaning when analyzed towards the

implementation of work. From the analysis result, will be able to know the

level of companies’ health also can be found the weaknesses as well as the

achievement owned by the companies, so the interested parties will be able to

use it as the consideration in making the decision”.

According to definition above, it can be concluded that financial performance of

company is the achievement in finance field achieved by the company in the certain

period of time which can be assess through its financial statement. This financial

performance would get high attention from interested parties through the result of

performance development, so the involved parties are able to take their decision.

29

Anita Febriyani and Rahadian Zulfadin (2003:42) explain that information given by a

company’s financial performance can be used as analysis and evaluation of financial

statement. The information of financial position and performance in the future and

other things which directly attract the attention of its user such as dividend payment,

wages, price securities of movement and company’s skill to meet its commitment

when the due date.

To determine the financial performance of the company so generally need to analyze

the financial statements which according to Brigham and Houston (2001, p78)

contains, (1) comparison of the company’s performance with other companies in the

same industry and (2) evaluation of a company's financial position trend over time.

Theoretically, the size of company is going to be larger on post merger due to asset,

liabilities, and equity of companies combined together and post merger’s

performance is supposed to be better compared with pre merger.

Financial performance also used as factor to measure the effectiveness and efficiency

of an organization. The decreasing of financial performance continuously can lead to

financial distress. Financial distress on bank which not directly solved can cause the

loss of customers’ confidence.

2.1.5 The influence of merger towards the improvement of company’s financial

performance

According to Moin (2007, p.308), immediately after the merger, the size of the

company by itself increases because the assets, liabilities and equity of the company

merged together. Basic logic of measurement based accounting is that if the size of

the company grew coupled with the synergies resulting from the combined activities

simultaneously, the company's profit also increased. Therefore, the post-merger

company's financial performance should have been better than it was before the

merger. With the merger between the two companies supposedly an increase in

30

financial performance. Allegation of improved financial performance can be

described in the following form:

a. CAR’s company of post merger is higher than pre merger

b. NPL’s company of post merger is lower than pre merger

c. ROA’s company of post merger is higher than pre merger

d. ROE’s company of post merger is higher than pre merger

e. OER’s company of post merger is lower than pre merger

f. LDR’s company of post merger is higher than pre merger

g. PER’s company of post merger is higher than pre merger

h. EPS’s company of post merger is higher than pre merger

i. PBV’s company of post merger is higher than pre merger

2.1.6 Financial ratios analysis

For business people especially investors, it becomes the important thing to be able to

determine the condition of funds disposition which done by knowing the exact

condition, stability, and continuity of the effort. Thus, the demand of maximum as

well as accurate information is an absolute must since with the complete of

information can be analyzed how exactly the condition of the business.

Analysis conducted can be used for several analysis methods which already existed,

one of them is by using financial ratio. Financial ratio helps the several of company’s

strength and weaknesses (Keown 1996:94).

The analysis of financial performance in this research aims to assess the

implementation of company’s strategy in terms of merger. According to Brigham and

Houston (2001, p7) can be measured by using financial ratios to determine the power

of company simultaneously as well as correcting the weaknesses of the company.

31

Basically, ratio analysis is a past event, therefore the factors that may exist in the

coming period, may affect the financial position or results of operations in future. For

that an analysis is required in order to give the results of the analysis and

interpretation of good and careful, because the results of this analysis will be useful

in determining the discretion of management for retrieval in the future.

Financial ratios used in the measurement of company performance pre and post

merger in this research are CAR, NPL, OER, LDR and ROE

a. CAR

Lukman Dendiwijaya (2005:121) stated that CAR is ratio of bank’s financial

performance to measure the capital adequacy of banks to support assets that

contain or produce risk. It is the capital ratio which shows the ability of bank in

providing the funds for business development and to accommodate the risk

caused by bank operational. This ratio is measuring how far the decreasing in

total assets which still could be covered by equity capital available.

According to Taswan (2003:57), CAR can be formulated as:

Eq. (3)

The minimum limit of CAR specified in criteria matrix rank determination of

capital in Bank Indonesia Circular Letter dated May 31, 2004 No. 6/23/DPNP

obtained standard for CAR is 8%, the higher value of the CAR of the bank, the

bank’s capital is better.

According to Malayu S.P Hasibuan (2002:58), state that the aims of CAR

determination of 8% is as follow:

1. Maintaining the public confidence of banking

2. Protecting the third parties funds in the relevant bank

32

3. To fulfill the provisions of BIS international banking standards with the

following formula:

a. 4% of primary capital which consist of shareholder equity, preferred

stock, and free reserves.

b. 4% of secondary capital which consist of subordinate debt, loan loss

provision, hybrid securities and revolution reserves.

b. NPL

According to Teguh Hidayat (2010), NPL is the ratio between loans that are not

returned by the borrower (bad debts) or refunded but haltingly, with total loans

distributed by banks to the public.

This ratio indicates that the ability of bank management in managing problem

loans granted by the bank. It is credit given to third parties excluding loans to

other banks. Nonperforming loans are loans classified as substandard, doubtful

and loss (Almilia and Herdiningtyas, 2005).

It is also described in Financial Accounting Standards No. 31 (revised 2000)

which states that:

"Non-performing loans generally are loans for which the principal / or interest

have been past ninety days or more after the due date or credits timely

collection is very doubtful."

According to Bank Indonesia Circular Letter No. 3/30/DPNP Date December 14,

2001, the NPL can be calculated by the formula:

Eq. (2)

33

According to Bank Indonesia Regulation No.6/10/PBI/2004, 12 April 2004

concerning the Rating System for Commercial Banks, the higher the value of

NPLs (above 5%), the bank is not healthy.

High NPL caused a decline in profits that will be accepted by the bank. Profit

decline resulted in the dividend also diminishing so that the growth rate of retun

bank stocks will decline.

c. OER

OER is the ratio that can provide an assessment of banking efficiency is

calculated by comparing total operating expenses to total operating income (SE

BI No. 6/23/DPNP/2004, 31 Mei 2004). Based on the criteria matrix rank

determination of capital in Bank Indonesia Circular Letter, standard of OER is

below then 94.72%.

The value of OER can be calculated by the formula (Dendawijaya, 2009:147):

OER =

x 100% Eq. (3)

If the bank OER ratio in a year decreased from the previous year, the operations

of the bank more efficient while if the OER ratio increased from the previous

year, the bank's operations are increasingly inefficient. This means showing the

lower the value of a bank's OER shows more efficient the bank (Financial

Institution Statistics, 2009: 30).

d. LDR

LDR is ratio which used to measure the composition of the total loans amount

compared to the amount of public funds and equity capital used. Based on

Kasmir (2011) LDR is used to measure the composition of the number of loans

compared to the amount of public funds and equity capital used.

34

According to Bank Indonesia Circular Letter No. 6/23/DPNP on May 31st 2004,

Loan to Deposit (LDR) is credit ratio given to third party funds (Current

Account, Savings, Certificates of Deposit, and Time).

Slamet Riyadi (2006:195) stated the understanding of LDR is as follow:

"LDR is a comparison between the total loans to total Third Party Funds

(TPF), which can be collected by the bank."

Taswan (2003:59) explains the formula to calculate LDR, as follow:

Eq. (4)

The greater this ratio indicates that the more aggressive bank liquidity, otherwise

the smaller this ratio is also greater in third party funds are not used for placement

to credit so will a lot of idle funds. LDR maximum allowed by BI is 100%.

e. ROE

ROE is a profitability ratio that measures the ability of a firm to generate profits

from its shareholders investments in the company. ROE illustrates how far the

company’s ability to generate profits can be gained by shareholders (Tandelilin,

2001).

The higher of this ratio means the better equity productivity in earning the profit.

It means that the profitability achieved by bank is greater and the possibility of

getting trouble is smaller (Statistik Lembaga Keuangan, 2009:32).

The growth of ROE shows the prospect of company which better since it means

the potential for increased company profits. This is captured by investors as the

positive signal for company so it will increase the investor’s confidence and will

facilitate the management of company to make the capital in the form of shares.

35

If there is an increasing of share’s demand of company, then it will indirectly

increase its share price on the stock market (Irawan, 1996).

Based on Bank of Indonesia decree No 23/67/KEP/DIR, the minimum value of a

good ROE is 10%.

ROE can be measured by using formula as follow (Agus Sartono, 2001):

Eq. (1)

The level of quality and character of shareholders affect capital adequacy because

their policies determine whether the return is distributed or not.

If the owner of the bank prefers return as retained earnings (so ROE decreases)

then return can be used to meet capital (Faisal, 2003). Retained earnings are

reinvested to company as a source of internal funds. The existence of retained

earnings on balance sheet will add the total earnings paid because retained

earnings is the property of the shareholders in the form of undistributed profits

(Jogiyanto, 2003).

2.2 Previous Research

M. Aji Nugroho (2010) in his research titled “Analisis Perbandingan Kinerja

Keuangan Perusahaan Sebelum dan Sesudah Merger dan Akuisisi” explain that there

is no any significant difference for NPM, ROA, ROE, Debt Ratio, EPS, TATO and

CR in research for 1 year before and after merger & acquisition as well as 1 and 5

year after merger & acquisition. However, there is little difference on comparison

between 1 year before with 2,3 and 4 year after merger & acquisition where the

financial ratio which is DER indicates there is difference significantly.

36

Deri Triawan Anugrah (2013) in his research titled “Analisis Perbandingan Tingkat

Kesehatan Bank Sebelum dan Sesudah Merger (Studi Kasus Bank OCBC NISP)”.

From the result of the research, there is no significant difference of pre and post

merger. There are only CAR, NPL, NIM, and OER which has significant difference

of pre and post merger. It is concluded that merger implemented is not effective due

to performance achieved after merger implemented is not facing significant

improvement.

Research by Dita Awalia Afriani (2012) entitled “Analisis Kinerja Keuangan

Sebelum dan Setelah Merger (Studi Kasus: Bank UOB Indonesia”. The analysis

result showed although based on t-test indicated that cash ratio, LDR, LAR, ROA,

ROE, OER, CAR, DER, and DTAR is not significant different of pre and post

merger however those ratios showed the improvement.

Research by R. ArisDijkgraaf in (2012) entitled “Analisis Perbandingan Kinerja

Keuangan Bank Sebelum dan Sesudah Merger”. From ratios used to analyze the

comparison of financial performance of pre and post merger which are CAR, NPL,

OER, ROA, ROE, NIM and LDR, only CAR nad LDR that has difference of pre and

post merger. Conversely, NPL, OER, ROA, ROE and NIM that has no difference of

pre and post merger.

Journal “Analysis and Impact of Financial Performance of Commercial Banks After

Mergers in India” written by Nedunchezhian & Premalatha (2013) has objective to

find out whether the bank achieved performance during the post-merger period

namely in the areas of Capital Adequacy Ratio, Management Efficiency Ratio,

Earnings and Profitability Ratio, Leverage Ratio. Method used is comparing the local

banks during the pre-merger period (2003-2006) and post-merger period (2008-

2011). The result of this study shows the growth rate of Return on Asset ratio and

other Income to Total Income except Indian Overseas Bank shows less improvement

after mergers. Overall, the performance of selected Banks after merger shows better

improvement in most of the areas.

37

Research by Ika Sisbintari (2011) entitled “Analisis Komparatif CAR, LDR, ROA,

dan ROE Sebelum dan Sesudah Merger Pada PT. Bank CIMB Niaga Tbk” explain

that the result of ratio calculation indicates the increasing of benefits achieved by

Bank CIMB Niaga characterized by the increase in ROA and ROE after merger

while the higher lending is marked with the increasing of LDR as well as the decline

of CAR at 2010 which indicates the minimum bank’s capital ownership is decreasing

due to the increase in liabilities of the bank after the merger.

Yulinda Lestari (2011) in her research article with title, “Perbandingan Kinerja

Keuangan Sebelum dan Setelah Merger” indicates that there are significant

differences between the Financial Performance Pre and Post-merger if measured by

using liquidity is LDR. But if measured by using asset quality are NPL, APB, PPAP

ratios, sensitivity to market risk are IRR and PDN ratios, profitability ratios are

ROA,OERand NIM and capital ratios, there are no significant between Financial

Performance pre and Post-merger

Payamta & Sholikah (2001) in his journal with title, “Pengaruh Merger dan Akuisisi

Terhadap Kinerja Perbankan di Indonesia”, the analysis use CAMEL and shows

that there is no significant difference in the level of financial performance measured

by CAMEL ratios for 1 year pre and post merger. Negative result also found by

Payamta & Setiawan (2004) which examines the financial performance of companies

doing mergers and acquisitions of financial ratios. From his research shows financial

ratios two years before and after the events of mergers and acquisitions do not

undergo significant changes.

38

2.3 Theoretical Framework

Figure 2.4: Theoretical Framework

Comparing (Paired Sample T-Test)

Source: Self-developed by the researcher and supported by previous research

Based on the theoretical review from previous research that explained previously, the

researcher has developed model for theoretical framework of this research that

presented above. As can be seen, in this research, the researcher wants to compare

the financial performance of pre and post merger by using financial ratios which can

be one of measurement of company whether it success or not in implementing

Pre Merger

CAR

NPL

OER

LDR

ROE

Post Merger

CAR

NPL

OER

LDR

ROE

Financial Performance

Financial Ratios

Performance of bank of post merger

39

merger activity. Those variables which are CAR, NPL, OER, LDR, and ROE then

will be explained briefly below.

1. Capital Adequacy Ratio is one of capital ratio which shows the ability of bank

in providing the funds for business development and to accommodate the risk

caused by bank operational. This ratio is importance because it measure how

far the decreasing in total assets which still could be covered by equity capital

available. The researcher interest to analyze the capital adequacy which bank

has of post merger. The minimum limit of CAR is 8% which means the

higher value of the CAR of the bank, the bank’s capital is better.

2. Non Performing Loan defined as ratio to indicate the ability of bank