competition policy and the legitimacy of finance: evidence ... · evolution of the uk brewing...

TRANSCRIPT

1

Competition policy and the legitimacy of finance: evidence from the deregulation of the

UK brewing industry

Dr Julie Bower

Birmingham Business School, University of Birmingham

Traditionally the UK brewing model was one that incorporated vertical ownership and control

of public houses (pubs). The political affiliation of the leading firms and their powerful

lobbying interests were sufficient to thwart not just capital market interest but the public

interest objectives of an emerging competition policy regime. Even the 1980s ‘merger wave’

that prompted a return to corporate specialization left the industry largely unchanged.

However, influence over policy came to an abrupt and controversial end in 1989 in the forced

divestment of the major brewers’ pub estates. Financiers seized the opportunity presented by

the change in competition policy. In less than a decade the pub industry was the subject of

‘financialization’ with control migrating to independent firms, the ‘PubCos’, which were

backed, and in some cases operated, by financial services intermediaries. The sustainability of

this business model was questioned by the 2008 Financial Crisis, with several prominent

PubCos struggling to survive and with no obvious exit route for their financial backers. In

presenting this historical case study I draw attention to the interplay between competition

policy and financialization, the latter of which derives legitimacy and is underpinned more

generally by other features of the institutional environment.

INTRODUCTION

For nearly two centuries the UK brewing industry evolved with a vertically-integrated

structure. In eighteenth century London brewers sought to control the retail distribution of

beer as licences became restricted (Gourvish and Wilson, 1994). With subsequent licencing

changes in the late nineteenth century, brewers in other parts of the UK acquired chains of

pub estates which were largely operated by third-party tenants to control the distribution of

their brewery production (Mutch, 2006). The attractions of distributing beer to a narrow

regional area with some form of exclusivity are clear from a comparative historic study of

returns on capital for selected UK brewer-retailers (Higgins and Toms, 2011).

That the industry survived into the 1990s with this structure even though an anti-trust

inquiry in 1969 had identified that it might operate against the public interest, was due largely

to the political voice of what was known as ‘The Beerage’ (‘beer’ plus ‘peerage’) of wealthy

family firms that controlled the industry (Bower and Cox, 2012). Moreover, in the post-World

War II era when the market for corporate control was emerging, a Bank of England that

signalled publicly its disapproval of debt-funded hostile bids offered general support to

traditional firms and industries (Roberts, 1992). Hostile approaches by prominent financiers

and outsiders such as property entrepreneur Charles Clore served to precipitate defensive

industry consolidation in the early 1960s. The creation of what were known as the ‘Big 6’

national brewer-retailers - Allied-Lyons, Bass, Courage, Scottish & Newcastle, Watney Mann

and Whitbread – led to wider concerns about market abuse which prompted competition

policy intervention (Spicer, Thurman, Walters and Ward, 2012). Where the 1969 inquiry

failed to force change, the 1989 inquiry, coinciding with an agenda of deregulation under

Conservative Prime Minister Mrs Thatcher, led to the dismantling of vertical integration of

2

large scale brewing into its constituent production and pub retailing operations. In little over a

decade, financial intermediaries acquired, restructured and came to dominate the operation of

the downstream public house assets of the UK with the approval of regulatory policy.

In reflecting on this subsequent period of the ‘financialization’ of the pub industry

newspaper commentary of international brewer Heineken’s decision to acquire UK pub assets

informs a wider debate on the role of finance in all aspects of corporate and economic

activity: “How on earth did Royal Bank of Scotland become one of Britain's biggest pub

landlords? The answer, of course, can be found in the era when retail banks thought banking

meant whatever they wanted it to mean” (The Guardian, 2 December 2011). The UK state-

owned Royal Bank of Scotland had been the owner of a portfolio of former Scottish &

Newcastle pubs since the early 2000s. In 2011, as several of the other financially-structured

pub models of the late 1990s and 2000s were struggling to survive in the aftermath of the

2008 Financial Crisis, it appeared that the mainstream retail banks might become

unintentional owners of many pub chains on the cusp of bankruptcy. In re-integrating the

former Scottish & Newcastle pub estate with the UK brewing operations it bought in 2007,

the Heineken decision identified a possible exit route for the financialized pub model -

perhaps ironic given the forced separation of industry assets through the 1989 ‘Beer Orders’.

My case study seeks to develop a deeper theoretical understanding of the interaction

between competition policy and financialization as two key elements of the institutional

environment that shape industry structure and operation. My empirical study describes the

evolution of the UK brewing industry through a competition policy-mandated change that

made way for the new business models created and held together, at least initially, by

financialization. Although this industry is somewhat unique in the culture and history of the

UK, the processes it illuminates are of wider relevance in developing a deeper understanding

of the organization and evolution of other industries as some researchers contemplate

financialization of US corporations as a potential threat to economic growth (Lazonick, 2010).

THEORETICAL BACKGROUND

Regulation and the capital markets represent two important points of interaction between

firms and the institutional environment within which they operate. The tensions and

constraining effect of each on firm behaviour and actions is well understood in both

theoretical and practical terms. For example, in implementing a growth strategy relying on

mergers and acquisitions, firms are charged with the dual task of persuading the competition

authorities of the merits of their case - ideally without recourse to a formal investigation – and

encouraging the financial support of bankers and shareholders. It is clear that the process of

discussion and negotiation with these institutional agents requires both powerful words and

actions; the extensive media campaigns, investor road shows and expert advisory support that

accompanies each major acquisition.

The management literature recognises the key role of the institutional environment as

a collective entity in shaping what firms do (Peng, Sun, Pinkham and Chen, 2009) in

particular in influencing structure and behaviour (Child and Rodrigues, 2011; Kostova, Roth

and Dacin, 2008) and researchers have noted the importance of firm interactions with the

competition framework of government (Barney, 2001; Shaffer, 1995; Shaffer and Hillman,

2000) as part of the process of aligning corporate strategies to the wider political context

(Oliver and Holzinger, 2008). Yet despite this evolving institutional literature that also

encompasses co-evolutionary studies of power and politics in the strategic behaviour of firms

(Child, Rodrigues and Tse, 2012) studies of competition policy in action are rare (Peng et al,

3

2009) despite frequent calls for empirical analysis to further the understanding of the

evolution of industrial architecture and firm boundaries (Jacobides and Winter, 2012).

In the following sections I draw attention to theoretical debates in related literature to

expand on the hypothesis that regulation and competition policy is significant in legitimizing

the role of capital market activity in inducing the changes evident in the UK brewing industry.

Further, without change in regulation it is unlikely that financialization would find support. In

considering broader historic debate it is clear that these two aspects of the institutional

environment need to be considered in tandem in discussions of firm and industry structure.

The constraining effect of US competition policy contributed to a thirty year post-World War

II trend which saw the proliferation of diversified industrial conglomerates (Shleifer and

Vishny, 1991). This owed much to the aggressive anti-trust oversight of horizontal mergers

and the centrality of econometric modelling of mergers following the 1957 Du Pont

monopolization case (Massey, 2000; Winerman, 2003). Although the conglomerate form

emerged in the UK in this era, with the absence of a merger regulation in competition policy

until 1965, restrictions on the distribution of capital, tax credits and capital controls led to the

over-accumulation of capital within larger firms, which, absent a fully functioning market for

corporate control underpinned a programme of unrelated diversification in the 1960s and

1970s (Roberts, 1992; Rowlinson, Toms and Wilson, 2007).

The central objective of competition policy is to ensure that consumers do not suffer

as a result of an array of anti-competitive practices by dominant firms with policy makers

retaining the ultimate sanction of forcing the separation of assets and defining the boundaries

of the firm (Joskow, 2002). The fact that regulation might not be an efficient or effective

mechanism to control management practices has been the subject of significant academic

enquiry in regulatory economics and the political economy literature.

The concept of ‘regulatory capture’ explains the behavior of interest groups in

influencing public decision makers through corruption and manipulation at the extreme, to the

mere eagerness to please private interests through the course of their repeated interactions

(Dal Bó, 2006; Laffont and Tirole, 1991; Martimort, 1999). The more benign concept of

intellectual capture is a manifestation of the power of words in the persuasive argument of

firms incentivized as rational profit maximizers to ‘game’ the regulator. Although largely the

domain of regulated utility-type industries, empirical studies have, however, identified

political interference and forms of regulatory capture in the less frequent competition and

merger policy process in both the US (Coate, Higgins, and McChesney, 1990), and Europe

(Aktas, de Bodt, and Roll, 2007).

Although broadly defined in the finance and economics literature, financialization

explains the trends of the past thirty years whereby finance and financial institutions have

come to directly and indirectly influence the behaviour of firms in areas such as capital

structure, dividend policy and fixed asset investment strategies (Orhangazi, 2008; Skott and

Ryoo, 2008; Stockhammer, 2004) or the evaluation of the performance of a firm by a

financial measure such as earnings per share (Lazonick, 2010). It is more specifically

associated with the liberalization of the capital markets in the US and the UK where financial

intermediaries, including activist investors, hedge funds and private equity firms have

emerged and been active in precipitating structural change in particular firms and industries,

aided by a process known as ‘securitization’ (Girόn and Chapoy, 2012)1. Securitization took

1 This is a financial innovation whereby contractual debt obligations, such as mortgages and car loans are pooled

and packaged into capital market stocks and shares. Those backed by mortgage payments are called Mortgage-

Backed Securities (MBS) and those backed by other types of payments are called Asset-Backed Securities

(ABS). Particular types of ABS, known as a Collateralized Debt Obligations (CDO) that originated in the

4

financialization one step further in that it established different ways that participants, many of

whom had no prior expertise as either managers of the underlying assets or who were

otherwise new entrants to the capital markets could monetise the benefits from the debt

markets (Jacobides and Winter, 2012).

The political economy literature broadens the concept of financialization to explain

the structural transformation of capitalist economies at the expense of broader social

implications (Becker, Jäger and Leubolt, 2012; Lapavitsas, 2011). The management literature

has investigated in some detail the human resource cost of financialization in the practices of

private equity group ownership, where, for example, the elimination of staff training and

investment has underpinned the value-based control systems that tie manager interests to

those of shareholders (Clark, 2009; Fiss and Zajac, 2004).

With regard to timeline, financialization is normally anchored in the 1980s ‘merger

wave’ of hostile bids which were fuelled by financial innovation in the deregulated US and

UK capital markets (Bhagat, Shleifer and Vishny, 1990). It was from this base that the so-

called shareholder revolution of the 1990s emerged (Orhangazi, 2008, P 864). In this context

financialization is usually considered to have a sole purpose of securing windfalls to financial

intermediaries, of which private equity funds have become the most prominent protagonists

(Wood and Wright, 2010). Contemporary media debate centres on the over-riding control of

the financial system in these liberal economies manifest in a permanent restructuring of

economic activity. An historic analogy is with the role adopted by the new manager

entrepreneur elites that emerged in the 1920s and 1930s (Folkman, Froud, Johal and

Williams, 2007).

The historic analogy is relevant as a theoretical extension of financialization is

anchored more firmly in the organization structures and the relationship with competition

policy that emerged as the market for corporate control was in its infancy (Hannah, 2007).

The 1948 Companies Acts mandated more stringent financial disclosure requirements for

listed firms so that external (institutional) shareholders could gain detailed financial

information about the firms in which they invested (Roberts, 1992; Toms and Wright, 2002).

It was these legislative changes that highlighted to financial entrepreneurs valuation

mismatches of listed property portfolios (Bower and Cox, 2012). Although the capital

restrictions that still remained, in addition to domestic-oriented banking activity tended to

provide a limited restraining influence on managements as agents of independent shareholders

(Jensen and Meckling, 1976), mergers and acquisitions activity, including hostile bids did

occur as a process of intra-industry rationalization of production costs (Bhagat, Shleifer and

Vishny, 1990; Franks and Mayer, 1996).

It was not until the 1980s that many of these conglomerate structures were dismantled

in a return to corporate specialization, supported by deregulation of capital market activities

(Porter, 1996). Political influence and lobbying to direct regulatory policy did not dissipate

entirely, in particular, when mergers involved hostile foreigners; US lawyers Herzel and

Shepro (1990) recounted the $21bn hostile bid from UK financiers, Sir James Goldsmith and

Lord Rothschild for British American Tobacco which saw 200 members of the US Congress

sign a letter urging the US State Department to block the deal. But in general, with policy

moving in the direction of structural independence from the political system, the ‘public

interest’ defence in competition policy which had tended to keep financialization at bay (in

particular in the UK) and in so doing, was laying the foundation for finance-backed business

models in their own right.

corporate debt markets in the 1980s in conjunction with the leveraged buyout phenomenon, are relevant to this

case. These financial instruments are integral in the evolution of the 2008 Financial Crisis.

5

In the 1990s there was an active debate in the role of the capital markets in policing

firm behaviour, as some notable protagonists of principle-agent theory such as Michael

Jensen (Jensen and Meckling, 1976) considered that higher leverage was the best discipline in

the Anglo-American divorced ownership model (Shleifer and Vishny, 1997). This was in

stark contrast to the attraction – at least in national outcome terms – of the German model of

ownership and control. In Germany major banks were more deeply embedded in the industrial

base with supervisory roles on the boards of major German firms, supported by large equity

investments that protected firms from wider capital market scrutiny (Fiss and Zajac, 2004).

The downside of the Anglo-American model was seen in the experiences of the irrationally

exuberant2 Dotcom era, of 1995-2000. Some firms, such as Enron, were seen as gaining more

from the capital markets than from operating productively in their industry (Froud, Johal,

Papazian and Williams, 2004). The exposition of the Enron business model informs a debate

on the financialization of the energy industry, as well as the now infamous illegal corporate

activity. Yet its very existence and survival owed much to the hyped investment environment

that emerged and thrived in that era.

DATA AND METHODOLOGY

I seek by means of a detailed longitudinal case study to develop the theory of financialization

as a process that emerges in conjunction with an interaction with competition policy. It

follows the academic tradition of using case studies to enhance existing theories (Bansal and

Corley, 2011; Doz, 2011; Eisenhardt and Graebner, 2007) notwithstanding the usual pitfalls

of the methodology, namely subjectivity and lack of generalisability. However, given the

complexity and time-dependency of the process involved this approach is considered optimal

in seeking to develop complex phenomena such as path-dependency (Siggelkow, 2007;

Sydow, Schreyögg and Koch, 2009) and interactions between firms and their institutional

environment (Lewin and Volberda, 1999; Peng et al, 2009). This is in contrast to the more

familiar cross-section statistical analysis that underpins much of the academic debate in both

regulation of markets and in studies seeking to understand the role of financial services in

industrial architecture.

The case study utilizes data and information collected and analysed from multiple

sources, including firm archive and official regulatory documentation, some of which has

only recent been made generally available through the National Archive and the London

Metropolitan Archive. The availability of extensive official and archive information in the

UK brewing and pub retailing industry is a reflection of its historic and continuing importance

to aspects of UK society and its juxtaposition in the political infrastructure of the UK. This

relates directly to the formulation and implementation of important anti-trust and merger

policy decisions. Consequently as an industry study it presents a unique dataset from which to

interpret important constructs such as political behaviour and institutional interactions (Child,

Rodrigues and Tse, 2012).

Table I below lists the main official documentary evidence that I have interrogated to

inform the study. It incorporates the data and information from anti-trust and merger inquiry

reports and specific listing particulars from the firms, firm annual reports, data and

information from the British Beer & Pub Association as well as various UK Parliamentary

discussions as shown.

2 A reference to comments made by Federal Reserve Board Chairman, Alan Greenspan, in a speech to the

American Enterprise Institute in 1996

6

TABLE 1: Secondary Data Source Material

Year Document Type Document Title

1969 MMC Inquiry Beer: A Report on the Supply of Beer (HC 216)

1985 MMC Inquiry

Scottish & Newcastle Breweries PLC and Matthew Brown PLC: A Report on the Proposed

Merger (Cmnd 9645)

1986 MMC Inquiry Elders IXL Ltd and Allied-Lyons PLC: A Report on the Proposed Merger (Cmnd 9892)

1988 Defence Document Scottish & Newcastle Breweries – Reject the Inadequate Elders Offers *

1989 MMC Inquiry The Supply of Beer: A Report on the Supply of Beer for Retail Sale in the United Kingdom

(Cm 651)

1989 MMC Inquiry Elders IXL and Scottish & Newcastle Breweries PLC: A Report on the Merger Situations

(Cm 654)

1989 Press Notice Decision on Beer Orders, DTI (89/745) **

1989 EC Official Journal Merger Regulation (4064/89)

1990 MMC Inquiry Elders IXL Ltd and Grand Metropolitan PLC: A Report on the Merger Situations (Cm 1227)

1992 MMC Inquiry Allied-Lyons PLC and Carlsberg A/S: A Report on the Proposed Joint Venture (Cm 2029)

1995 Listing Particulars Scottish & Newcastle PLC Proposed Acquisition of the Courage Business and Rights Issue *

1997 MMC Inquiry Bass PLC, Carlsberg A/S and Carlsberg-Tetley PLC: A Report on the Merger Situation (Cm

3662)

1997 Press Notice Margaret Beckett Blocks Bass/Carlsberg-Tetley Merger, DTI (97/424) **

1997 EC Official Journal Notice on the Definition of Relevant Market for the Purposes of Community Competition

Law (97/C 372/03)

1999 Press Notice Stephen Byers Refers Whitbread PLC’s Proposed Acquisition of Allied Domecq Retailing to

the Competition Commission, DTI

2000 OFT Report The Supply of Beer: A Report on the Review of the Beer Orders by the Former DGFT (OFT

317)

2001 CC Inquiry Interbrew SA and Bass PLC: A Report on the Acquisition by Interbrew SA of the Brewing

Interests of Bass PLC (Cm 5014)

2001 OFT Report Advice on the Report by the Competition Commission into the Acquisition by Interbrew SA

of the Brewing Interests of Bass PLC

2003 Listing Particulars Proposed sale by Scottish & Newcastle PLC of S&N Retail *

2004 EC Report Merger Regulation (139/04)

2009 House of Commons

Report

Pub Companies; Seventh Report of Session 2008-09 (Oral and Written Evidence to Business

and Enterprise Committee)

2009 House of Commons

Report

Pub Companies; Seventh Report of Session 2008-09 (Report and Formal Minutes of Business

and Enterprise Committee)

2009 IFBB Report European Commission: Review of the Competition Rules Applicable to Vertical Agreements

(Submission from The Independent Family Brewers of Britain)

2009 CAMRA Report European Commission: Review of the Competition Rules Applicable to Vertical Agreements

(A Response from the Campaign for Real Ale)

2009 OFT Report Response to CAMRA’s Super-complaint (OFT 1137)

2010 OFT Report CAMRA Super-complaint – OFT Final Decision (OFT 1279)

* Documents provided by Scottish & Newcastle from firm archive

**Documents available from UK Department for Business, Innovation & Skills (formerly Department of Trade and Industry)

archive.

All other documents available to download from official websites

The timeframe for the study is a period of considerable upheaval as the centuries-old UK

vertical brewing structure was dismantled. New entrants, largely finance-backed special

purpose independent public house companies, known as the PubCos, gradually came to

dominate the ownership of the industry’s property assets. Consequently, the industry has

informed academic debates in various business and management-related literatures in

particular in regulatory economics (Nalebuff, 2003; Pinkse and Slade, 2004; Slade, 2011) and

in UK economic and business history (Gourvish and Wilson, 1994; Higgins and Toms, 2011;

Mutch, 2006, 2010; Spicer, Thurman, Walters and Ward, 2012). As a closed-system industry,

its interest to strategic management lies in both the transformation of the ‘Big 6’ brewer-

7

retailer firms from vertically-integrated regional operators to international brewers and spirits

marketers (da Silva Lopes, 2002; Geppert, Dӧrrenbächer, Gammelgaard and Taplin, 2013).

Two anti-trust inquiries (in 1969 and 1989) and several controversial mergers of the 1980s

(Australian conglomerate Elders IXL’s hostile bids for Allied-Lyons and Scottish &

Newcastle and the Guinness/Distillers affair) widened the industry’s appeal to a series of

business and political discussions (Bower and Cox, 2012). Yet the system that had found

political support through many different Governments, aided by political donations and high-

level lobbying was broken apart by a competition policy-mandated change, paving the way

for a change of ownership and control from brewing firms to finance-backed entities, as

discussed is the following sections and summarised in Table 2 below.

DISMANTLING THE UK BREWING INDUSTRY

Traditionally, the UK brewing industry was vertically-integrated, with brewers owning

outright or controlling through a tenant-supply relationship known as a ‘property tie’ the

greater proportion of the UK’s public houses3. In the latter part of the eighteenth century

London brewers sought increasingly to control the retail distribution of beer as licences

became restricted with around half of London’s pubs owned or controlled by brewers by the

1830s (Gourvish and Wilson, 1994: p128). With subsequent licencing changes in the late

nineteenth century, brewers in other parts of the UK acquired pub estates, operated largely by

tenants, as dedicated distribution for their production (Mutch, 2006). That the industry

survived into the 1990s with this structural arrangement was due in large part to the political

influence of ‘The Beerage’ (‘beer’ plus ‘peerage’) of wealthy family firms that controlled the

industry (Bower and Cox, 2012), supported by a trade organisation, The Brewers’ Society,

that acted as a private market-governance institution active in organising collective lobbying

(Yue, Luo and Ingram, 2013).

During the late 1940s prominent financiers emerged in the UK whose paths would

cross with the structure and ownership of the UK brewing and pub retailing industry as well

as the fledgling international spirits industry. Most notable were Charles Clore who launched

an unsuccessful hostile bid for London brewer Watney Mann, in 1959, and Sir Maxwell

Joseph, whose firm Grand Metropolitan was successful in a hostile approach for Watney

Mann in 1972, an acquisition that brought an associated stake in International Distillers &

Vintners, the foundation of today’s global spirits leader, Diageo (Williamson and Rix, 1988).

These hostile approaches triggered a “defensive anxiety” within the UK industry (Gourvish &

Wilson, 1994, P 460), This precipitated a series of mergers among largely family-controlled

firms in the early 1960s, creating what became known as the ‘Big 6’ national brewer-retailers

of Allied-Lyons, Bass, Courage, Scottish & Newcastle, Watney Mann and Whitbread.

With the support of a generally benign competition policy regime, and the political

lobbying efforts of the firms and their industry collective, the large firms were generally

3 Table 2 shows that the bulk of the brewers’ pub portfolios were tenanted outlets; the brewer owned the pub and

a tenant rented the property on (theoretically) below open market rental terms in lieu of an obligation to buy all

beer, wines, spirits and soft drinks from the brewer owner (usually referred to as a ‘property tie’). In addition to

this additional arrangements at that time included some that were similar to those in other Continental European

markets with many independent pubs also being partially controlled by the leading brewers through the

provision of subsidised financing in lieu of an exclusive supply contract (usually referred to a ‘loan-tie’). The

degree to which this also acted against the public interest was discussed extensively in the MMC inquiry into

Scottish & Newcastle’s hostile bid for regional brewer Matthew Brown in 1985 (MMC, Cmnd 9645).

8

supported and protected from the market for corporate control under the oversight of the Bank

of England (Roberts, 1992). Yet the firms were well aware of a threat to their existence from

the arrival of large scale sophisticated finance. Forming an investment structure, known as the

Whitbread Umbrella, to protect not just its own family interests but also those of small family

brewers with whom it had trading relationships, Whitbread’s influential former chief

executive, Sir Sydney Nevile, noted the “present fever of finance in the brewing

industry........I suggested that the interest of his company was merely to speculate in shares

and then sell them to the highest bidder” (File note of conversation with a non-executive

director of the Independent Commercial Finance Corporation on 27 March 1961, London

Metropolitan Archives).

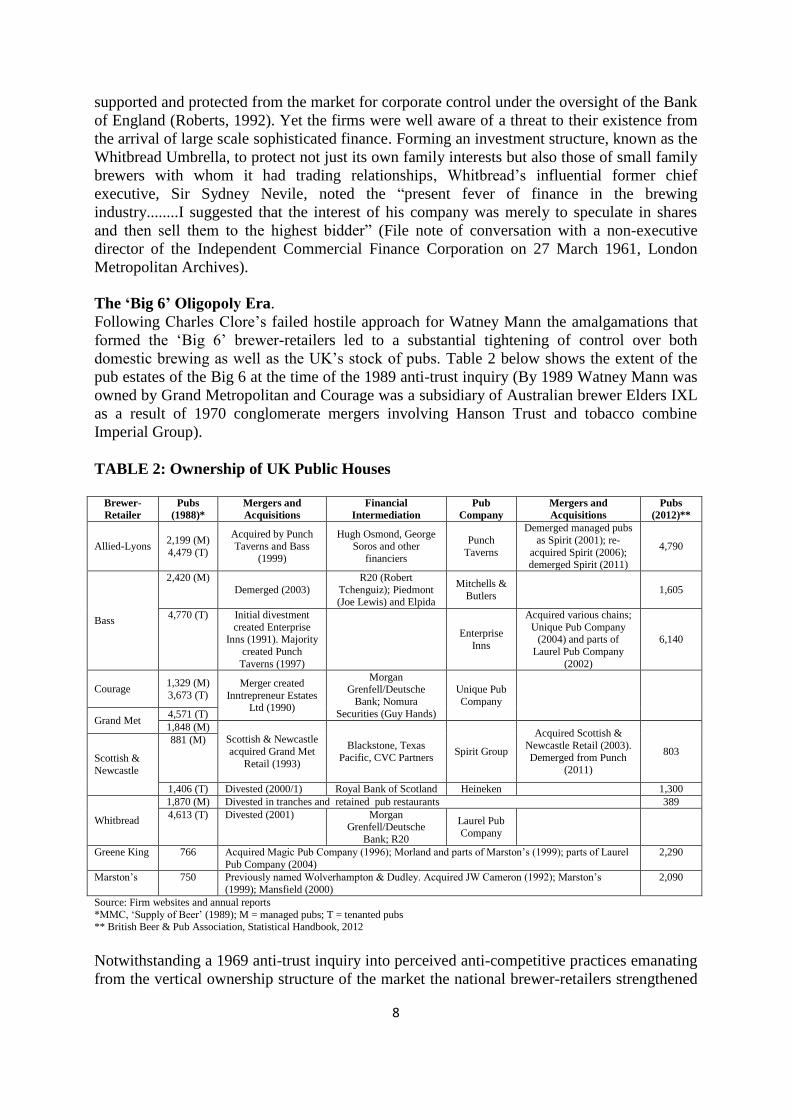

The ‘Big 6’ Oligopoly Era.

Following Charles Clore’s failed hostile approach for Watney Mann the amalgamations that

formed the ‘Big 6’ brewer-retailers led to a substantial tightening of control over both

domestic brewing as well as the UK’s stock of pubs. Table 2 below shows the extent of the

pub estates of the Big 6 at the time of the 1989 anti-trust inquiry (By 1989 Watney Mann was

owned by Grand Metropolitan and Courage was a subsidiary of Australian brewer Elders IXL

as a result of 1970 conglomerate mergers involving Hanson Trust and tobacco combine

Imperial Group).

TABLE 2: Ownership of UK Public Houses

Brewer-

Retailer

Pubs

(1988)*

Mergers and

Acquisitions

Financial

Intermediation

Pub

Company

Mergers and

Acquisitions

Pubs

(2012)**

Allied-Lyons 2,199 (M)

4,479 (T)

Acquired by Punch

Taverns and Bass

(1999)

Hugh Osmond, George

Soros and other

financiers

Punch

Taverns

Demerged managed pubs

as Spirit (2001); re-

acquired Spirit (2006); demerged Spirit (2011)

4,790

Bass

2,420 (M)

Demerged (2003)

R20 (Robert

Tchenguiz); Piedmont (Joe Lewis) and Elpida

Mitchells &

Butlers 1,605

4,770 (T) Initial divestment

created Enterprise Inns (1991). Majority

created Punch

Taverns (1997)

Enterprise

Inns

Acquired various chains;

Unique Pub Company (2004) and parts of

Laurel Pub Company

(2002)

6,140

Courage 1,329 (M)

3,673 (T) Merger created

Inntrepreneur Estates Ltd (1990)

Morgan Grenfell/Deutsche

Bank; Nomura

Securities (Guy Hands)

Unique Pub

Company

Grand Met 4,571 (T)

1,848 (M) Scottish & Newcastle

acquired Grand Met

Retail (1993)

Blackstone, Texas

Pacific, CVC Partners Spirit Group

Acquired Scottish &

Newcastle Retail (2003).

Demerged from Punch

(2011)

803 Scottish &

Newcastle

881 (M)

1,406 (T) Divested (2000/1) Royal Bank of Scotland Heineken 1,300

Whitbread

1,870 (M) Divested in tranches and retained pub restaurants 389

4,613 (T) Divested (2001) Morgan Grenfell/Deutsche

Bank; R20

Laurel Pub

Company

Greene King 766 Acquired Magic Pub Company (1996); Morland and parts of Marston’s (1999); parts of Laurel

Pub Company (2004)

2,290

Marston’s 750 Previously named Wolverhampton & Dudley. Acquired JW Cameron (1992); Marston’s

(1999); Mansfield (2000)

2,090

Source: Firm websites and annual reports

*MMC, ‘Supply of Beer’ (1989); M = managed pubs; T = tenanted pubs ** British Beer & Pub Association, Statistical Handbook, 2012

Notwithstanding a 1969 anti-trust inquiry into perceived anti-competitive practices emanating

from the vertical ownership structure of the market the national brewer-retailers strengthened

9

their control of the industry in the 1970s and 1980s. Their attraction to property-backed

financiers did not diminish; there was a second successful hostile approach for Watney Mann

in 1972 from Sir Maxwell Joseph’s Grand Metropolitan (Williamson and Rix, 1988).

However, neither this acquisition nor the 1972 acquisition of Courage by Imperial Group

served to change the overall structure and operation of the industry. That the policy

environment was benign and helpful to the incumbents was evident in the sanctioning of a

voluntary agreement to reduce overall ownership of pubs, co-ordinated under the auspices of

the industry trade association, the Brewers’ Society (Spicer, Thurman, Walters and Ward,

2012). However, although the control of pubs was reduced from around 70% in the late 1970s

to closer to 50% by the 1980s, most of the reduction was due to sales of smaller tenanted

pubs. In fact ownership of the larger and more profitable managed pubs actually increased

during the 1970s.

The control of beer supply by the Big 6 was often cited as the reason why the price of

beer in pubs rose consistently above the level of general retail prices. Yet, the market for

corporate control did not work efficiently with respect to this industry. The era of corporate

specialization prompted by the emergence of corporate raiders and the 1980s ‘merger wave’

(Shleifer and Vishny, 1991) left the UK brewers largely unscathed. This was not for the want

of trying; Australian brewing/finance conglomerate, Elders IXL made two high profile and

politically-charged attempts to acquire UK brewers in the mid-1980s. Finance entered the

debate directly at the level of competition policy. Elders IXL’s 1985 hostile bid for Allied-

Lyons was referred to the MMC by the Secretary of State (for Trade and Industry) on the

basis that the bidder’s use of financial leverage might work against the public interest.

Although the Bank of England failed to endorse this, the delay, and a high-profile media

campaign through the conduit of The City, provided Allied-Lyons the time to enact the

‘poison pill’ defence of acquiring Canadian spirits firm, Hiram Walker before the bid was

cleared (MMC, Cmnd 9892, 1986). Elders withdrew its bid but returned two years later with

the more audacious and controversial bid for Scottish & Newcastle. The combination of

intense lobbying and wide political backing for the influential Scottish & Newcastle ensured

the bid was referred and somewhat uniquely, blocked (Bower and Cox, 2012; MMC, Cm 654,

1989).

Running concurrently with the Elders/Scottish & Newcastle inquiry, a general anti-

trust investigation concluded that a complex monopoly existed in the UK beer market which

could only be resolved by restricting the degree of industry vertical integration. A mandated

upper limit of 2,000 pubs for any brewer was made, meaning that an estimated 22,000 pubs

(30% of all pubs in England & Wales) would have to be divested by November 1992. The

referral for a second anti-trust inquiry, if not this decision, came as surprise to a previously

successful lobbying campaign spearheaded by the Brewers’ Society. Further high-level

discussions between the industry and Government ensured some moderation to these terms,

requiring the brewers to divest half of the excess of pubs in their stable over the 2,000

threshold (DTI Press Release, 89/745).

The 1989 inquiry anticipated that a less vertically-integrated beer market would both

widen consumer choice and lead to more competitive retail pricing. While choice materialised

quickly, aided by the ‘guest beer’ provision of the legislation (Day and Kelton, 2007) keener

beer prices proved elusive and indeed as Figure 1 below shows the gap between pub beer

prices (‘on-trade’) continued to widen relative to both general prices and wholesale beer

prices (‘PPI’). Moreover, it is clear that the gap with supermarket prices (‘off trade’) also

widened significantly. This has been viewed more recently in a less desirable light given the

perceived link between under-priced alcohol and ‘binge drinking’. It is ironic that the vertical

brewing tie emerged in London in response to legislation designed to promote beer and

10

reduce problematic gin consumption in Georgian London (the Sale of Spirits Act, 1750,

commonly known as the Gin Act).

FIGURE 1: Retail and Producer Prices of UK Beer

Source: Adapted from data supplied by British Beer & Pub Association, Statistical Handbook, 2012

The regulatory intervention through the structural remedy of the ‘Beer Orders’ was an

extreme measure by policy standards. Indeed, some ten years later the Director General of

Fair Trading described the remedy as a draconian requirement that was disproportionate to

the mischiefs the Beer Orders were designed to address (OFT, The Supply of Beer, 2000,

paragraph 2.3). That competition policy might have misunderstood the transmission

mechanism between wholesale and retail prices was highlighted in the dissenting letter of

Professor M E Beesley in the 1992 Allied-Lyons/Carlsberg UK brewing merger, (MMC, Cm

2029, 1992, p 89). As the 1990s progressed it was clear that the adverse effects of the brewing

complex monopoly transferred to an equally potent mechanism for controlling retail pub

prices under the PubCos. The PubCos, whose very existence is traced to a change in policy

and the legitimization of finance as a business model in its own right, were widely criticised

for not passing on the benefits of the keener wholesale beer price terms they extracted from

the brewers during the 1990s (Day and Kelton, 2007).

The ‘Financialization’ Era.

PubCos emerged to acquire blocks of tenanted pubs which the brewers were obliged to divest

to comply with the provisions of the Beer Orders. Over the following decade full-scale

financialization of the pub industry occurred as private equity-backed entities displaced

established brewer operators attracted to the very same attributes that had first attracted the

property financiers of the post-World War II generation. By the late 1990s the PubCos owned

11

and operated more than 50% of all pub outlets, as shown in Figure 2 below. Supporting the

change in ownership was the ability of the PubCos to negotiate substantial beer discounts

from a brewing industry struggling to reduce overcapacity at a time when UK beer

consumption was also declining (Cm1227, pages 11-12; Cm2029, page 44). The combination

of the well-publicised scale of wholesale beer discounts available and the evolution of the

securitization market underpinned an active mergers and acquisitions strategy within the

PubCo sector, as shown in Table 1 above.

FIGURE 2: Independent Pub Company Ownership of UK Public Houses

Source: Adapted from data supplied by British Beer & Pub Association, Statistical Handbook, 2012. ‘Other’ includes pubs

held within holding companies, operated on a temporary contract basis and those that are part of chains with less than 30

outlets.

The origins of the PubCo financing model can be traced to the novel ‘breweries-for-pubs

swap’ agreed between Grand Met and Elders IXL’s UK subsidiary, Courage (MMC, Cm

1227, 1990). This was the first merger in the immediate aftermath of the Beer Orders when

the industry was adapting to change in UK competition policy, itself increasingly under the

auspices of harmonization and oversight from European Commission policy directives (Cini

and McGowan, 1998). Specifically under EC Article 81 (3), certain vertical agreements,

including the UK brewers’ vertical tie had been granted a ‘block exemption’ but that expired

in 1997. The uniqueness of the merger agreement between Grand Met and Elders IXL, in

particular the partners’ use of upfront remedies to circumvent more obtrusive regulatory

intervention, was noteworthy in that it established a more conciliatory approach to merger

negotiations at the firm-firm level as well as firm-regulator level (Bower and Cox, 2013). Of

particular interest to this analysis, as it forms the bridge from policy to subsequent

financialization, is the evolution of the merged tenanted estate of 8,500 pubs. This combined

12

entity, known as Inntrepreneur Estates Limited (IEL), represented some 13% of the UK total

pub stock in the early 1990s.

From its inception IEL was structured as an independent joint venture, managed on an

arms-length basis with its own financing terms. The tenants were offered the opportunity to

share in the potential rewards of the new structure through newly established 20 year

assignable leases. Unfortunately as high profile complaints to the European Commission in

the mid-1990s show (Case Number IV/35.628/F3 – a ‘super-complaint’ made by the

Federation of Small Businesses on behalf of a group of former Inntrepreneur lessees) the

terms were not necessarily beneficial to the tenants. The decline of property prices created

significant operational as well as financial pressures and the joint venture parents were

distracted by their other, more substantive operations in other industries and markets. Parts of

the IEL estate were sold, largely to other small PubCos. More significant was a later series of

transactions, firstly with UK investment bank Morgan Grenfell (part of Deutsche Bank) and

then with Nomura Securities, which led to the Japanese bank becoming the UK’s largest

independent PubCo by 1998, under the direction of prominent ex-Goldman Sachs financier

Guy Hands.

The involvement of a well-known financier in the pub market precipitated interest

from other financial institutions. Industry commentary from observers close to many of the

deals drew attention to the weakness of the PubCo financing model. Profitability was flattered

by unsustainably high rents, low levels of capital spending and keen beer supply terms that

were unlikely to last. Moreover, Nomura’s financial backing owed much to the Japanese

bank’s ability to borrow cheaply in Yen, and a deregulated Japanese banking industry that

increasingly incentivised foreign investment (Hoshi and Kashyap, 2000, p164). Financiers

were either not cognisant of, or chose to ignore data that showed IEL tenancy default rates

close to 20% during the 1990/91 recession. In the economic recovery of the mid-late 1990s

default rates naturally fell but these lower default rates were factored into many PubCo

financing models in addition to the beneficial beer supply terms captured and retained in the

PubCo centres. With an active market for securitization of rental cash flows (Girόn and

Chapoy, 2012) an apparent ‘money machine’ encouraged more ambitious merger strategies.

That financialization had come to dominate the structure and operation of the pub

industry, was evident by the latter part of the 1990s, when private equity-backed vehicles

were able to outbid long-standing industry operators for prime retail assets. The 1999 battle

for control of the former Allied-Lyons pub estate is informative in this regard. While the

interjection of the Secretary of State served to thwart the merger proposal of pub industry

leader Whitbread, the ability of the finance-backed Punch Taverns to win the contest put

financiers at the heart of the pub industry (The Lawyer, 1999). Punch Taverns had only been

operating as an independent entity since 1997. Following a listing on the UK stock market,

Punch embarked on an aggressive acquisition strategy funded by large amounts of debt

secured against the firm’s property assets (The Telegraph, 2010), that led eventually to a

proposed all-share merger with Mitchells & Butlers (M&B), the managed pub estate of the

former Bass. Had this deal transacted Punch would have controlled one sixth of the UK pub

market, with some 10,500 outlets. In the ensuing financial crisis of 2008, however, Punch’s

fortunes went into dramatic decline with falling property prices and a weak pub trading

environment forcing the resignation of its chief executive in January 2009, as the group

courted bankruptcy. For its part, M&B, similarly engaged in financial engineering, was forced

to concede that a pre-Financial Crisis interest rate derivative position established with

property entrepreneur, Robert Tchenguiz, to enhance shareholder value had failed. The

subsequent charge to the firm’s accounts of £274m was the basis for the resignation of the

finance director and chief executive officers (M&B annual report, 2008).

13

In concluding this era understanding how the Royal Bank of Scotland, saved by the

UK government and taxpayers in the Financial Crisis, came to own part of the UK pub

industry is also important. As banker to Scottish & Newcastle it had supported that firm’s

mergers and acquisitions growth strategy from its UK base through the subsequent

internationalisation into European brewing. To reduce group debt following these

increasingly large acquisitions (the acquisition of Danone’s French brewing operation,

Kronenbourg in 2000) Scottish & Newcastle was forced to sell its pub estate. Initially it sold

small numbers of tenanted pubs to Royal Bank of Scotland - in April 2000 a small chain of

447 outlets. With further disposals in 2001 Royal Bank of Scotland became a tenanted pub

owner of 1,000 outlets. Scottish & Newcastle retained property management services under a

management contract and a beer supply deal from its brewing division (The Telegraph, 2001).

Ultimately, Scottish & Newcastle, under pressure from shareholders, sold its managed pub

estate to the finance-backed Spirit Group, in October 2003.

Royal Bank of Scotland remained the owner of the former Scottish & Newcastle

tenanted pubs and it is these assets that were acquired in 2011 by international brewer

Heineken. It is with some irony, perhaps, that Heineken acquired these pubs, having acquired

Scottish & Newcastle as part of joint hostile bid with Carlsberg in 2007. Although Heineken

had a presence in the UK brewing industry for many decades through the conduit of a licence

brewing and distribution agreement with Whitbread, it is significant that in developing its

own directly controlled UK operation through Scottish & Newcastle brewing it has also

chosen to re-acquire former Scottish & Newcastle pubs from a finance entity and in so doing

recreate a vertical integration model not unlike the original Big 6 brewers.

CONCLUSIONS

The aim of my article is to highlight how competition policy interacts with finance and the

capital markets in preventing or augmenting change in industry structure and the boundaries

of firms operating within it by recourse to an empirical longitudinal study of the evolution of

the UK brewing and pub industry. The requirement for a deeper understanding of firm and

industry interaction with the institutional environment continues, in particular with regard to

anti-trust and how firms adapt to and seek to influence institutional change and regulatory

shifts in dynamic and complex environments (Child and Rodrigues, 2011; Jacobides and

Winter, 2012; Peng et al, 2009). I presented an empirical study of an industry that was, by

tradition, vertically integrated, and remained so for nearly two centuries supported by history,

political voice and, perhaps, on reflection, a sound base in the theory of transaction costs.

The link between transaction cost economics and the regulatory environment lies in

the oversight of vertical restraint in competition policy. Indeed, the transaction cost

economics framework was established by Williamson in his early analysis of anti-trust and

competition policy (Williamson, 1971; 1991; 2010). In a market with the potential for

foreclosure efficiency benefits from vertical integration are unlikely to outweigh the welfare

cost of the restraint of trade (Lafontaine and Slade, 2010). However, although the mostly

econometric analyses highlights adverse welfare effects of vertical arrangements, legal

scholars have cautioned that competition policy needs to be cognisant of the transaction-based

attributes of incumbent firm organizational structures, the reasons why they emerged, and the

consequences of changing them through divestiture (Joskow, 2002).

Although an extensive discussion of transaction cost economics is outside the scope of

this article, its advantage to the UK brewing industry, the economic support for which was

14

dismissed by the 1989 ‘Beer Orders inquiry4, is relevant to contextualizing Heineken’s recent

decision to acquire pubs from the Royal Bank of Scotland. For an international brewer with

no prior ownership of public houses despite its long association with the UK brewing

industry, this decision may be as significant in policy terms as it is in signalling that

financialization has reached an end-point in this industry. The financialized business model of

the PubCos might therefore constitute further examples of interim hybrid structures and new

organizational forms, some of which are ultimately unstable, that emerge in other frequently

vertically-integrated industries, such as the electricity industry (Delmas and Tokat, 2005;

Russo, 2001) although several earlier empirical studies have shown that firms can co-exist for

extended periods with organizational structures that are anomalous (Chiles and McMackin,

1996).

The change imposed by competition policy corresponded to the era of more readily

available finance and financial innovation. Without the former the PubCo business model

might not have emerged. It is perhaps more certain that without the latter, it would have

remained a minority structural innovation; its wider acceptance owed much to the entry of a

prominent financier, backed by the balance sheet of a leading international investment bank.

Anchored in the era of securitization (Girόn and Chapoy, 2012) and the financialized business

model of firms such as Enron (Froud et al, 2004) the lower default pub rental cashflows and

keener beer supply terms encouraged both new entry and consolidation. The PubCos were

able to out-compete and out-bid traditional firms such as Whitbread in the acquisition of other

attractive chains of pubs and restaurants.

The experience of the last few years in the aftermath of the Financial Crisis has shown

that the PubCo model and some of the more esoteric financial instruments supporting it are

fundamentally unstable. What appears to be unfolding is the destabilizing impact of strategies

that are supported by financialization rather than genuine business logic in a financially

repressed era. The consequences for policy makers in the politically and socially sensitive

area of alcohol distribution are potentially significant. The ownership and structure of firms

and the manner in which industry value chains operate today is the subject of a wider

institutional and political debate, as the recent UK food industry scandals demonstrate.

Certainly the Beer Orders did not anticipate the degree to which beer consumption patterns

would change and in particular the significance of the take-home trade now controlled by the

leading supermarket groups. Moreover, with financial and tax engineering a topical media

line of inquiry in both the US and UK, ownership structures and novel business models that

dominate other socially important sectors have come under greater scrutiny. A recent article

concerning the former state-controlled UK water firms (‘UK water companies avoid paying

tax’, The Telegraph, 15 February 2013) highlighted how this core domestic utility is now

largely owned by non-UK domiciled financial intermediaries with highly leveraged financial

arrangements. Financialization extends into an unavoidable discussion of what might happen

in the event of a debt default by a firm that provides an essential public service. As we have

discovered for the banking industry, tax payers are almost invariably the owner or lender of

last resort, as indeed they became, albeit temporarily, for parts of the UK pub industry.

4 As part of the evidence presented to the inquiry, the Brewers’ Society commissioned an academic analysis by

two leading University of Oxford regulatory economists, Professors Morris and Yarrow, to present a detailed set

of reasons why vertical integration was an efficient organizational structure which did not act against the public

interest (MMC, Cm 651, paragraphs 5.18-5.57 and Appendix 5.2).

15

REFERENCES

Aktas, N., de Bodt, E., & Roll, R. 2007. Is European M&A regulation protectionist? The

Economic Journal, 117:1096-1121.

Bansal, P., & Corley, K. 2011. The coming of age for qualitative research: Embracing the

diversity of qualitative methods. Academy of Management Journal, 54(2): 233-237.

Becker, J., Jäger, J., & Leubolt, B. 2010. Peripheral financialization and vulnerability to

crisis: A regulationist perspective. Competition and Change, 14(3-4): 225-247.

Bhagat, S., Shleifer, A., & Vishny, R. W. 1990. Hostile takeovers in the 1980s: The return to

corporate specialization. Brookings Papers: Microeconomics.

Bower, J., & Cox, H. 2012. How Scottish & Newcastle became the UK’s largest brewer: A

case of regulatory capture? Business History Review, 86: 43-68.

Bower, J., & Cox, H. 2013. Merger regulation, firms and the co-evolutionary process: An

empirical study of internationalisation in the UK alcoholic beverages industry 1985-

2005. Working paper no 48, Centre for Globalisation Research, Queen Mary,

University of London, UK.

Child, J., & Rodrigues, S. B. 2011. How organizations engage with external complexity: A

political action perspective. Organization Studies, 32(6): 803-824.

Child, J., Rodrigues, S. B., & Tse, K. K-T. 2012. The dynamics of influence in corporate co-

evolution. Journal of Management Studies, 49(7): 1246-1273.

Chiles, T. H., & McMackin, J. F. 1996. Integrating variable risk preferences, trust and

transaction cost economics. Academy of Management Review, 21(1): 73-99.

Coate, M. B., Higgins, R. S., & McChesney, F. S. 1990. Bureaucracy and politics in FTC

merger challenges. Journal of Law and Economics, 33(2): 463-482.

Dal Bó, E. 2006. Regulatory capture: A review. Oxford Review of Economic Policy, 22(2):

203-225.

Da Silva Lopes, T. 2002. Brands and the evolution of multinationals in alcoholic beverages.

Business History, 44(3): 1-30.

Day, H., & Kelton, R. 2007. The valuation of licensed premises. Journal of Property

Investment & Finance, 25(3): 306-321.

Delmas, M., & Tokat, Y. 2005. Deregulation, governance structures and efficiency: The US

electric utility sector. Strategic Management Journal, 26: 441-460.

Dobson, P. 2002. Merger assessment in oligopolistic markets: Lessons from Interbrew/Bass.

Paper presented at NIE Conference on Competition Policy and Regulation.

Doz, Y. 2011. Qualitative research for international business. Journal of International

Business Studies, 42(4): 582-590.

Eisenhardt, K. M., & Graebner, M. E. 2007. Theory building from cases: Opportunities and

challenges. Academy of Management Journal, 50(1): 25-32.

Franks, J., & Mayer, C. 1996. Hostile takeovers in the UK and the correction of managerial

failure. Journal of Financial Economics, 40(1): 163-181.

Fiss, P. C., & Zajac, E. J. 2004. The diffusion of ideas over contested domain: The (non)

adoption of a shareholder value orientation among German firms. Administrative

Science Quarterly, 49: 501-534.

Folkman, P., Froud, J., Johal, S., & Williams K. 2007. Working for themselves? Capital

market intermediaries and present day capitalism. Business History, 49(4): 552-572.

Froud, J., Johal, S., Papazian, V., & Williams, K. 2004. The temptation of Houston: A case

study of financialisation. Critical Perspectives on Accounting, 15: 885-909.

16

Geppert, M., Dӧrrenbächer, C., Gammelgaard, J., & Taplin, I. 2013. Managerial risk-taking in

international acquisitions in the brewery industry: Institutional and ownership

influences compared. British Journal of Management, 24: 316-332.

Girόn, A., & Chapoy, A. 2012. Securitization and financialisation. Journal of Post Keynesian

Economics, 35(2): 171-188.

Gourvish, T. R., & Wilson, R. G. 1994. The British Brewing Industry 1830-1980.

Cambridge, UK: Cambridge University Press.

Hannah, L. 1974. Takeover bids in Britain before 1950: An exercise in business ‘pre-history’.

Business History, 16(1): 65-77.

Hannah, L. 2007. The ‘divorce’ of ownership from control from 1900 onwards: Re-

calibrating imagined global trends. Business History, 49(4): 404-438.

Higgins, D. M., & Toms, S. 2011. Explaining corporate success: The structure and

performance of British firms, 1950-84. Business History, 53(1): 85-118.

Hoshi, T., & Kashyap, A. 2000. The Japanese banking crisis: Where did it come from and

how will it end? In B. S. Bernanke & J. J. Rotemburg (Eds), National Bureau of

Economics Research, Macroeconomics Annual, 14: 129-212. MIT, US.

Jacobides, M. G., & Winter, S. G. 2005. The co-evolution of capabilities and transaction

costs: Explaining the institutional structure of production. Strategic Management

Journal, 26: 395-413.

Jacobides, M. G., & Winter, S. G. 2012. Capabilities: structure, agency and evolution.

Organization Science, 23(5): 1365-1381.

Joskow, P. L. 2002. Transaction cost economics, antitrust rules, and remedies. The Journal of

Law, Economics, & Organization, 18(1): 95-116.

Kostova, T., Roth, K., & Dacin, M. T. 2008. Institutional theory in the study of multinational

corporations: A critique and new directions. Academy of Management Review, 33(4):

994-1006.

Laffont, J-J., & Tirole, J. 1991. The politics of government decision-making: A theory of

regulatory capture. The Quarterly Journal of Economics, 106(4): 1089-1127.

Lafontaine, F., & Slade, M. E. 2010. Transaction cost economics and vertical market

restrictions – evidence. The Antitrust Bulletin, 55(3): 587-611.

Lazonick, W. 2010. Innovative business models and varieties of capitalism: Financialization

of the US corporation. Business History Review, 84(Winter): 675-702.

Martimort, D. 1999. The life cycle of regulatory agencies: dynamic capture and transaction

costs. Review of Economic Studies, 66: 929-947.

Massey, P. 2000. Market definition and market power in competition analysis: Some practical

issues. The Economic and Social Review, 31(4): 309-328.

Mutch, A. 2006. Allied Breweries and the development of the area manager in British

brewing, 1950-1984. Enterprise & Society, 7(2): 353-379. Mutch, A. 2010. Improving the public house in Britain, 1920-40: Sir Sydney Nevile and ‘social work’.

Business History, 52(4): 517-535.

Orhangazi, O. 2008. Financialisation and capital accumulation in the non-financial corporate

sector: A theoretical and empirical investigation on the US economy, 1973-2003.

Cambridge Journal of Economics, 32: 863-886.

Peng, M. W., Sun, S. L., Pinkham, B., & Chen, H. 2009. The institution-based view as a third

leg for a strategy tripod. Academy of Management Perspectives, (August): 63-81.

Porter, M. E. 1996. What is strategy? Harvard Business Review, (Nov-Dec): 61-78.

Roberts, R. 1992. Regulatory responses to the rise of the market for corporate control in

Britain in the 1950s. Business History, 34(1): 183-200.

17

Rowlinson, M., Toms, S., & Wilson, J. F. 2007. Competing perspectives on the ‘Managerial

Revolution’: From ‘Managerialist’ to ‘Anti-Managerialist’. Business History, 49(4):

464-482.

Russo, M. V. 2001. Institutions, exchange relations, and the emergence of new fields:

Regulatory policies and independent power production in America, 1978-1992.

Administrative Science Quarterly, 46: 57-86.

Shaffer, B. 1995. Firm-level responses to government regulation: Theoretical and research

approaches. Journal of Management, 21(3): 495-514.

Shaffer, B., & Hillman, A. J. 2000. The development of business-government strategies by

diversified firms. Strategic Management Journal, 21: 175-190.

Shleifer, A., & Vishny, R. W. 1991. Takeovers in the ‘60s and the ‘80s: Evidence and

implication. Strategic Management Journal, 12: 51-59.

Shleifer, A., & Vishny, R. W. 1997. A survey of corporate governance. The Journal of

Finance, 52(2): 737-783.

Siggelkow, N. 2007. Persuasion with case studies. Academy of Management Journal, 50(1):

20-24.

Skott, P., & Ryoo, S. 2008. Macroeconomic implications of financialisation. Cambridge

Journal of Economics, 32: 827-862.

Slade, M. E. 2011. Competition policy towards brewing: Rational response to market power

or unwarranted interference in efficient markets? In J. F. N. Swinnen (Ed), The

Economics of Beer. Oxford, UK: Oxford University Press.

Spicer, J., Thurman, C., Walters, J. & Ward, S. 2012. Intervention in the Modern UK

Brewing Industry. Basingstoke, UK: Palgrave Macmillan.

Stockhammer, E. 2004. Financialisation and the slowdown of accumulation. Cambridge

Journal of Economics, 28: 719-741.

Thackray, J. 1986. Leveraged buyouts: the LBO craze flourishes amid warnings of disaster

Euromoney Magazine. 2 January.

The Lawyer. 1999. Punch drunk, 13 September.

The Telegraph. 2001. Scottish & Newcastle offloads pubs to bank, 27 October.

The Telegraph. 2010. Giles Thorley: The pub boss who loved the good time’, 31 March.

Toms, S., & Wright, M. 2002. Corporate governance, strategy and structure in British

business history, 1950-2000. Business History, 44(3): 91-124.

Williamson, O. E. 1971. The vertical integration of production: Market failure considerations.

American Economic Review, 61: 112–123.

Williamson, O. E. 1991. Strategizing, economizing, and economic organization. Strategic

Management Journal, 12: 75-94.

Williamson, O. E. 2010. Reflections on antitrust. The Antitrust Bulletin, 55(3): 543-544.

Williamson, P., & Rix, B. 1988. Grand Metropolitan PLC. London Business School, Case

Study, 9-788-01.

Winerman, M. (2003). ‘The origins of the FTC: concentration, cooperation, control and

competition’. Antitrust Law Journal, 71, 1-97.

Wood, G., & Wright, M. 2010. Wayward agents, dominant elite or reflection of internal

diversity? A critique of Folkman, Froud, Johal and Williams on financialisation and

financial intermediaries. Business History, 52(7): 1048-1067.