compliance section - amazon web services€¦ · compliance section this section is ... • the...

TRANSCRIPT

COMPLIANCE SECTION

This section is presented in accordance with:

• Government Auditing Standards, issued by the Comptroller General of the United States• The provisions of Office of Management and Budget (OMB) Circular A-133• Florida Single Audit Act, Chapter 215.97 of the Florida Statutes• The Rules of the Auditor General of the State of Florida, Chapter 10.550

co

mp

lIan

ce S

ec

tIon

Marion County Office of the County Engineer

– Safety Edge Installation

ADDITIONAL ELEMENTS OF REPORT PREPARED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS,

ISSUED BY THE COMPTROLLER GENERAL OF THE UNITED STATES; THE PROVISIONS OF THE U.S. OFFICE OF MANAGEMENT

AND BUDGET (OMB) CIRCULAR A-133; AND THE RULES OF THE AUDITOR GENERAL OF THE STATE OF FLORIDA

217

ADDITIONAL ELEMENTS OF REPORT PREPARED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS,

ISSUED BY THE COMPTROLLER GENERAL OF THE UNITED STATES; THE PROVISIONS OF THE U.S. OFFICE OF MANAGEMENT

AND BUDGET (OMB) CIRCULAR A-133; AND THE RULES OF THE AUDITOR GENERAL OF THE STATE OF FLORIDA

217

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida We have audited, in accordance with the auditing standards generally accepted in the United States of America and standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities, the business-type activities, the discretely presented component unit, each major fund and the aggregate remaining fund information of the Marion County, Florida (the County), as of and for the year ended September 30, 2013, and the related notes to the financial statements, which collectively comprise the County’s basic financial statements, and have issued our report thereon dated March 6, 2014. Internal Control Over Financial Reporting In planning and performing our audit of the financial statements, we considered the County’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the County’s internal control. Accordingly, we do not express an opinion on the effectiveness of the County’s internal control over financial reporting. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe that a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

218

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida We have audited, in accordance with the auditing standards generally accepted in the United States of America and standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities, the business-type activities, the discretely presented component unit, each major fund and the aggregate remaining fund information of the Marion County, Florida (the County), as of and for the year ended September 30, 2013, and the related notes to the financial statements, which collectively comprise the County’s basic financial statements, and have issued our report thereon dated March 6, 2014. Internal Control Over Financial Reporting In planning and performing our audit of the financial statements, we considered the County’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the County’s internal control. Accordingly, we do not express an opinion on the effectiveness of the County’s internal control over financial reporting. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in internal control that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe that a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

218

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

(Concluded) Compliance and Other Matters As part of obtaining reasonable assurance about whether the County’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our test disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose. March 6, 2014 Ocala, Florida

219

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND

OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

(Concluded) Compliance and Other Matters As part of obtaining reasonable assurance about whether the County’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our test disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose. March 6, 2014 Ocala, Florida

219

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida Report on Compliance for Each Major Federal Program We have audited Marion County, Florida (the County)’s compliance with types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133, Compliance Supplement, and the requirements described in the Department of Financial Services’ State Projects Compliance Supplement that could have a direct and material effect on each of the County’s major federal programs and state projects for the year ended September 30, 2013. The County’s major federal programs and state projects are identified in the summary of auditor’s results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs and state projects. Auditors’ Responsibility Our responsibility is to express an opinion on compliance for each of the County’s major federal programs and state projects based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States and OMB Circular A-133, Audits of States, Local Governments and Non-Profit Organizations, and Chapter 10.550, Rules of the Auditor General. Those standards and OMB Circular A-133, and Chapter 10.550, Rules of the Auditor General, require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on major federal program and state project occurred. An audit includes examining, on a test basis, evidence about the County’s compliance with those requirements and performing such other procedures, as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program and state project. However, our audit does not provide a legal determination of the County’s compliance.

220

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida Report on Compliance for Each Major Federal Program We have audited Marion County, Florida (the County)’s compliance with types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133, Compliance Supplement, and the requirements described in the Department of Financial Services’ State Projects Compliance Supplement that could have a direct and material effect on each of the County’s major federal programs and state projects for the year ended September 30, 2013. The County’s major federal programs and state projects are identified in the summary of auditor’s results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility Management is responsible for compliance with the requirements of laws, regulations, contracts, and grants applicable to its federal programs and state projects. Auditors’ Responsibility Our responsibility is to express an opinion on compliance for each of the County’s major federal programs and state projects based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States and OMB Circular A-133, Audits of States, Local Governments and Non-Profit Organizations, and Chapter 10.550, Rules of the Auditor General. Those standards and OMB Circular A-133, and Chapter 10.550, Rules of the Auditor General, require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on major federal program and state project occurred. An audit includes examining, on a test basis, evidence about the County’s compliance with those requirements and performing such other procedures, as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion on compliance for each major federal program and state project. However, our audit does not provide a legal determination of the County’s compliance.

220

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

(Continued)

Opinion on Each Major Federal Program In our opinion, the County complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs and state projects of the year ended September 30, 2013. Report on Internal Control Over Compliance Management of the County is responsible for establishing and maintaining effective internal control over compliance with the types of compliance referred to above. In planning and performing our audit, we considered the County's internal control over compliance with the types of requirements that could have a direct and material effect on a major federal program or state project in order to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and state project and to test and report on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of County’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal or state project on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program or state project will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program or state project that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. Schedule of Expenditures of Federal Awards and State Financial Assistance We have audited the financial statements of the governmental activities, the business-type activities, the discretely presented component units, each major fund and the aggregate remaining fund information of the County, as of and for the year ended September 30, 2013, which collectively comprise the County’s basic financial statements. We issued our report thereon dated March 6, 2014, which contained unmodified opinions on those financial statements. Our audit was performed for the purpose of forming opinions on the financial statements that collectively comprise the basic financial statements. The

221

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

(Continued)

Opinion on Each Major Federal Program In our opinion, the County complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs and state projects of the year ended September 30, 2013. Report on Internal Control Over Compliance Management of the County is responsible for establishing and maintaining effective internal control over compliance with the types of compliance referred to above. In planning and performing our audit, we considered the County's internal control over compliance with the types of requirements that could have a direct and material effect on a major federal program or state project in order to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for each major federal program and state project and to test and report on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of County’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal or state project on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program or state project will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program or state project that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. Schedule of Expenditures of Federal Awards and State Financial Assistance We have audited the financial statements of the governmental activities, the business-type activities, the discretely presented component units, each major fund and the aggregate remaining fund information of the County, as of and for the year ended September 30, 2013, which collectively comprise the County’s basic financial statements. We issued our report thereon dated March 6, 2014, which contained unmodified opinions on those financial statements. Our audit was performed for the purpose of forming opinions on the financial statements that collectively comprise the basic financial statements. The

221

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

(Concluded)

Schedule of Expenditures of Federal Awards and State Financial Assistance (Concluded) accompanying schedule of expenditures of federal awards and state financial assistance is presented for the purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and Chapter 10.550, Rules of the Auditor General, and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to underlying accounting and other records used to prepare the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the schedule of expenditures of federal awards and state financial assistance is fairly stated in all material respects in relation to the financial statements as a whole.

The purpose of this report on internal control over compliance is solely to describe our testing of internal control over compliance and the results of that testing based on the requirements of OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General. Accordingly, this report is not suitable for any other purpose. March 6, 2014 Ocala, Florida

222

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR FEDERAL PROGRAM AND STATE PROJECT AND ON INTERNAL CONTROL

OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133; AND CHAPTER 10.550, RULES OF THE AUDITOR GENERAL

(Concluded)

Schedule of Expenditures of Federal Awards and State Financial Assistance (Concluded) accompanying schedule of expenditures of federal awards and state financial assistance is presented for the purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and Chapter 10.550, Rules of the Auditor General, and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to underlying accounting and other records used to prepare the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the schedule of expenditures of federal awards and state financial assistance is fairly stated in all material respects in relation to the financial statements as a whole.

The purpose of this report on internal control over compliance is solely to describe our testing of internal control over compliance and the results of that testing based on the requirements of OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General. Accordingly, this report is not suitable for any other purpose. March 6, 2014 Ocala, Florida

222

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

FEDERAL AWARDS

U.S. Department of Agriculture:

Direct Programs:Cooperative Forestry Assistance:

Forestry Special Details 10.664 13-LE-11080500-004 26,548 -

Passed through Florida Department of Financial Services:Schools and Roads-Grants to States:

Federal Forestry Shared Revenue 10.665 N/A 286,001 -

Total U.S. Department of Agriculture 312,549 -

U.S. Department of Housing and Urban Development:

Direct Programs:Community Development Block Grants/Entitlement Grants 14.218 B-11-UC-12-0019 1,387,515 1,195,532 Community Development Block Grants/Entitlement Grants 14.218 B-12-UC-12-0019 958,955 777,327 CDBG-Neighborhood Stabilization Program (NSP1) 14.218 B-08-UN-12-0011 70,767 - CDBG-Neighborhood Stabilization Program (NSP3) 14.218 B-11-UN-12-0011 1,507,212 -

Total Community Development Block Grants/Entitlement Grants 3,924,449 1,972,859

Home Investment Partnerships Program 14.239 M-08-DC-12-0232 376,963 176,835 Home Investment Partnerships Program 14.239 M-09-DC-12-0232 28,070 16,822

Total Home Investment Partnerships Program 405,033 193,657

Total U.S. Department of Housing and Urban Development 4,329,482 2,166,516

U.S. Department of Justice:

Direct Programs:National Institute of Justice Research, Evaluation, andDevelopment Project Grants:

Solving Cold Cases with DNA 16.560 2010-DN-BX-K011 16,359 -

Direct Programs, continued:Bulletproof Vest Partnership Program 16.607 N/A 7,134 -

Public Safety Partnership and Community Policing Grants:COPS Universal Hiring Program 16.710 2010-UL-WX-0029 473,817 -

Total Public Safety Partnership and Community Policing Grants 473,817 -

JAG Program Cluster:Direct Programs:

Edward Byrne Memorial Justice Assistance Grant Programs:FY 2010 Justice Assistance Grant (JAG) 16.738 2010-DJ-BX-0610 129,386 FY 2011 Justice Assistance Grant (JAG) 16.738 2011-DJ-BX-3452 38,803 FY 2012 Justice Assistance Grant (JAG) 16.738 2012-DJ-BX-0895 76,834 -

Passed through Florida Department of Law Enforcement:Edward Byrne Memorial Justice Assistance Grant Programs:

Marion County DUI Court 16.738 2013-JAGC-MARI-4-D7-237 10,000 - Marion County Juvenile and Dependency Drug Court 16.738 2013-JAGC-MARI-3-D7-235 13,001 - Marion Co. Sheriff Office DARE Program 16.738 2012-JAGC-MARI-3-C4-183 2,440 -

Total Edward Byrne Memorial Justice Assistance Grant Programs 270,464 -

Passed through Office of the State Courts Administrator:Recovery Act-Edward Byrne Memorial Justice Assistance Grant (JAG)Program/Grants to States and Territories:

ARRA-Post-Adjudicatory Drug Court Expansion 16.803 2010-ARRC-STATE-3-W7-133 44,714 - Total Recovery Act-Edward Byrne Memorial JAG/Grants to States and Territories 44,714

Total JAG Program Cluster 315,178 -

Pass-Through Grantor /

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

Federal Grantor /

Program Title / Project Title

223

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

FEDERAL AWARDS

U.S. Department of Agriculture:

Direct Programs:Cooperative Forestry Assistance:

Forestry Special Details 10.664 13-LE-11080500-004 26,548 -

Passed through Florida Department of Financial Services:Schools and Roads-Grants to States:

Federal Forestry Shared Revenue 10.665 N/A 286,001 -

Total U.S. Department of Agriculture 312,549 -

U.S. Department of Housing and Urban Development:

Direct Programs:Community Development Block Grants/Entitlement Grants 14.218 B-11-UC-12-0019 1,387,515 1,195,532 Community Development Block Grants/Entitlement Grants 14.218 B-12-UC-12-0019 958,955 777,327 CDBG-Neighborhood Stabilization Program (NSP1) 14.218 B-08-UN-12-0011 70,767 - CDBG-Neighborhood Stabilization Program (NSP3) 14.218 B-11-UN-12-0011 1,507,212 -

Total Community Development Block Grants/Entitlement Grants 3,924,449 1,972,859

Home Investment Partnerships Program 14.239 M-08-DC-12-0232 376,963 176,835 Home Investment Partnerships Program 14.239 M-09-DC-12-0232 28,070 16,822

Total Home Investment Partnerships Program 405,033 193,657

Total U.S. Department of Housing and Urban Development 4,329,482 2,166,516

U.S. Department of Justice:

Direct Programs:National Institute of Justice Research, Evaluation, andDevelopment Project Grants:

Solving Cold Cases with DNA 16.560 2010-DN-BX-K011 16,359 -

Direct Programs, continued:Bulletproof Vest Partnership Program 16.607 N/A 7,134 -

Public Safety Partnership and Community Policing Grants:COPS Universal Hiring Program 16.710 2010-UL-WX-0029 473,817 -

Total Public Safety Partnership and Community Policing Grants 473,817 -

JAG Program Cluster:Direct Programs:

Edward Byrne Memorial Justice Assistance Grant Programs:FY 2010 Justice Assistance Grant (JAG) 16.738 2010-DJ-BX-0610 129,386 FY 2011 Justice Assistance Grant (JAG) 16.738 2011-DJ-BX-3452 38,803 FY 2012 Justice Assistance Grant (JAG) 16.738 2012-DJ-BX-0895 76,834 -

Passed through Florida Department of Law Enforcement:Edward Byrne Memorial Justice Assistance Grant Programs:

Marion County DUI Court 16.738 2013-JAGC-MARI-4-D7-237 10,000 - Marion County Juvenile and Dependency Drug Court 16.738 2013-JAGC-MARI-3-D7-235 13,001 - Marion Co. Sheriff Office DARE Program 16.738 2012-JAGC-MARI-3-C4-183 2,440 -

Total Edward Byrne Memorial Justice Assistance Grant Programs 270,464 -

Passed through Office of the State Courts Administrator:Recovery Act-Edward Byrne Memorial Justice Assistance Grant (JAG)Program/Grants to States and Territories:

ARRA-Post-Adjudicatory Drug Court Expansion 16.803 2010-ARRC-STATE-3-W7-133 44,714 - Total Recovery Act-Edward Byrne Memorial JAG/Grants to States and Territories 44,714

Total JAG Program Cluster 315,178 -

Pass-Through Grantor /

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

Federal Grantor /

Program Title / Project Title

223

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

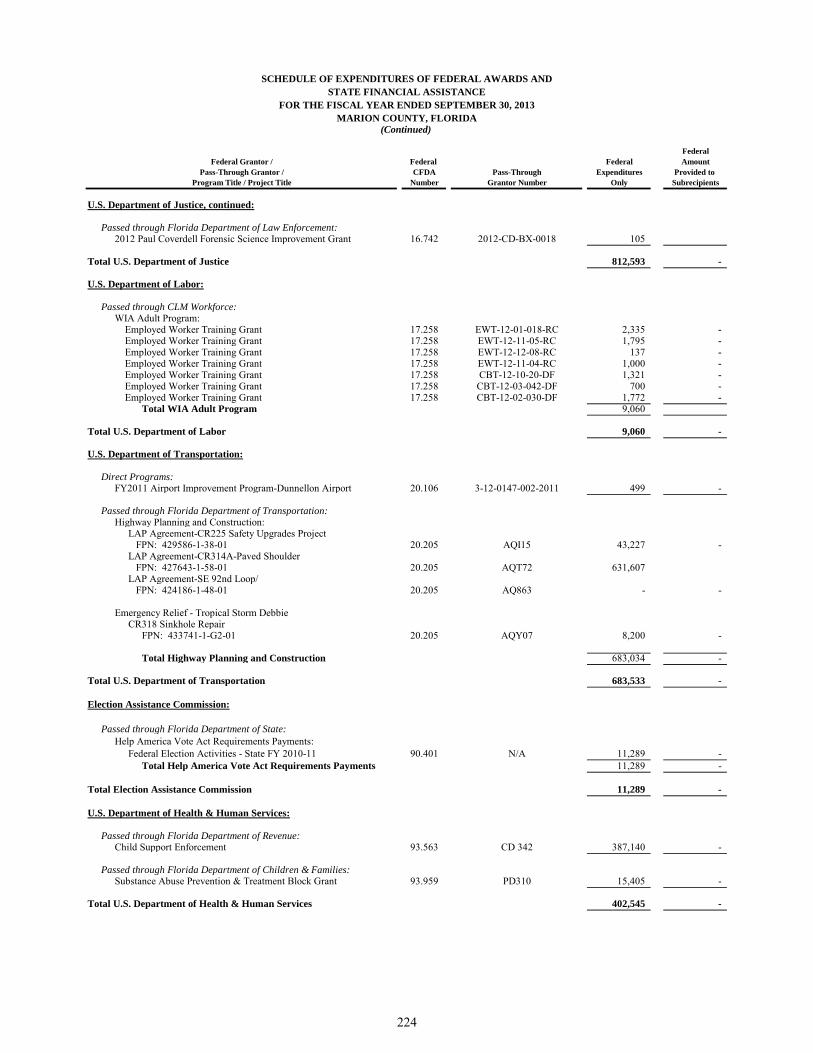

U.S. Department of Justice, continued:

Passed through Florida Department of Law Enforcement:2012 Paul Coverdell Forensic Science Improvement Grant 16.742 2012-CD-BX-0018 105

Total U.S. Department of Justice 812,593 -

U.S. Department of Labor:

Passed through CLM Workforce:WIA Adult Program: Employed Worker Training Grant 17.258 EWT-12-01-018-RC 2,335 - Employed Worker Training Grant 17.258 EWT-12-11-05-RC 1,795 - Employed Worker Training Grant 17.258 EWT-12-12-08-RC 137 - Employed Worker Training Grant 17.258 EWT-12-11-04-RC 1,000 - Employed Worker Training Grant 17.258 CBT-12-10-20-DF 1,321 - Employed Worker Training Grant 17.258 CBT-12-03-042-DF 700 - Employed Worker Training Grant 17.258 CBT-12-02-030-DF 1,772 -

Total WIA Adult Program 9,060

Total U.S. Department of Labor 9,060 -

U.S. Department of Transportation:

Direct Programs:FY2011 Airport Improvement Program-Dunnellon Airport 20.106 3-12-0147-002-2011 499 -

Passed through Florida Department of Transportation:Highway Planning and Construction:

LAP Agreement-CR225 Safety Upgrades Project FPN: 429586-1-38-01 20.205 AQI15 43,227 - LAP Agreement-CR314A-Paved Shoulder FPN: 427643-1-58-01 20.205 AQT72 631,607 LAP Agreement-SE 92nd Loop/ FPN: 424186-1-48-01 20.205 AQ863 - -

Emergency Relief - Tropical Storm DebbieCR318 Sinkhole Repair

FPN: 433741-1-G2-01 20.205 AQY07 8,200 -

Total Highway Planning and Construction 683,034 -

Total U.S. Department of Transportation 683,533 -

Election Assistance Commission:

Passed through Florida Department of State:Help America Vote Act Requirements Payments:

Federal Election Activities - State FY 2010-11 90.401 N/A 11,289 - Total Help America Vote Act Requirements Payments 11,289 -

Total Election Assistance Commission 11,289 -

U.S. Department of Health & Human Services:

Passed through Florida Department of Revenue:Child Support Enforcement 93.563 CD 342 387,140 -

Passed through Florida Department of Children & Families:Substance Abuse Prevention & Treatment Block Grant 93.959 PD310 15,405 -

Total U.S. Department of Health & Human Services 402,545 -

(Continued)

Federal Grantor /Pass-Through Grantor /

Program Title / Project Title

224

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

U.S. Department of Justice, continued:

Passed through Florida Department of Law Enforcement:2012 Paul Coverdell Forensic Science Improvement Grant 16.742 2012-CD-BX-0018 105

Total U.S. Department of Justice 812,593 -

U.S. Department of Labor:

Passed through CLM Workforce:WIA Adult Program: Employed Worker Training Grant 17.258 EWT-12-01-018-RC 2,335 - Employed Worker Training Grant 17.258 EWT-12-11-05-RC 1,795 - Employed Worker Training Grant 17.258 EWT-12-12-08-RC 137 - Employed Worker Training Grant 17.258 EWT-12-11-04-RC 1,000 - Employed Worker Training Grant 17.258 CBT-12-10-20-DF 1,321 - Employed Worker Training Grant 17.258 CBT-12-03-042-DF 700 - Employed Worker Training Grant 17.258 CBT-12-02-030-DF 1,772 -

Total WIA Adult Program 9,060

Total U.S. Department of Labor 9,060 -

U.S. Department of Transportation:

Direct Programs:FY2011 Airport Improvement Program-Dunnellon Airport 20.106 3-12-0147-002-2011 499 -

Passed through Florida Department of Transportation:Highway Planning and Construction:

LAP Agreement-CR225 Safety Upgrades Project FPN: 429586-1-38-01 20.205 AQI15 43,227 - LAP Agreement-CR314A-Paved Shoulder FPN: 427643-1-58-01 20.205 AQT72 631,607 LAP Agreement-SE 92nd Loop/ FPN: 424186-1-48-01 20.205 AQ863 - -

Emergency Relief - Tropical Storm DebbieCR318 Sinkhole Repair

FPN: 433741-1-G2-01 20.205 AQY07 8,200 -

Total Highway Planning and Construction 683,034 -

Total U.S. Department of Transportation 683,533 -

Election Assistance Commission:

Passed through Florida Department of State:Help America Vote Act Requirements Payments:

Federal Election Activities - State FY 2010-11 90.401 N/A 11,289 - Total Help America Vote Act Requirements Payments 11,289 -

Total Election Assistance Commission 11,289 -

U.S. Department of Health & Human Services:

Passed through Florida Department of Revenue:Child Support Enforcement 93.563 CD 342 387,140 -

Passed through Florida Department of Children & Families:Substance Abuse Prevention & Treatment Block Grant 93.959 PD310 15,405 -

Total U.S. Department of Health & Human Services 402,545 -

(Continued)

Federal Grantor /Pass-Through Grantor /

Program Title / Project Title

224

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

U.S. Department of Homeland Security:

Passed through Florida Department of Community Affairs:Emergency Operations Center (EOC) Grant 97.001 11-DS-37-05-52-01-283 15,849 -

Emergency Management Performance Grant 97.042 13-FG-86-05-52-01-109 81,115 - Emergency Management Performance Grant 97.042 14-FG-1M-05-52-01-109 28,210

Total Emergency Management Performance Grants 109,325 -

Homeland Security Grant Program:Citizen Corps Grant 97.067 11-CC-A6-05-52-01-473 6,750 - Citizen Corps Grant 97.067 13-CC-58-05-52-01-422 7,481 - CERT Grant 97.067 11-CI-A6-05-52-01-477 5,292 - CERT Grant 97.067 14-CI-58-05-52-01-137 7,477 - Domestic Security Funding 97.067 12-DS-20-05-52-01-472 96,121 - Domestic Security Funding 97.067 13-DS-97-05-52-01-459 36,662 - Domestic Security Funding 97.067 10-DS-39-05-52-01-330 1,305 - Domestic Security Funding 97.067 11-DS-9Z-05-52-01-385 43,202 -

Passed through Florida Department of Financial Services:2007-2010 State Homeland Security Grant Program 97.067 FM257 5,722 5,019 2008-2009 State Homeland Security Grant Program 97.067 FM274 - - 2009-2010 State Homeland Security Grant Program 97.067 FM278 529 - 2010 State Homeland Security Grant Program 97.067 FM285 65,768 7,015

Total Homeland Security Grant Program 276,309 12,034

Total U.S. Department of Homeland Security 401,483 12,034

TOTAL EXPENDITURES OF FEDERAL AWARDS 6,962,534$ 2,178,550$

Notes:

Disaster Relief Funding - Tropical Storm Fay 97.036 09-PA-B9-05-52-00-543 44,808 -

(Continued)

(1) Marion County received the following Disaster Relief Funds from DCA in FY13 for expenditures that occurred in

Federal Grantor /Pass-Through Grantor /

Program Title / Project Title

225

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

FederalFederal Federal AmountCFDA Pass-Through Expenditures Provided to

Number Grantor Number Only Subrecipients

U.S. Department of Homeland Security:

Passed through Florida Department of Community Affairs:Emergency Operations Center (EOC) Grant 97.001 11-DS-37-05-52-01-283 15,849 -

Emergency Management Performance Grant 97.042 13-FG-86-05-52-01-109 81,115 - Emergency Management Performance Grant 97.042 14-FG-1M-05-52-01-109 28,210

Total Emergency Management Performance Grants 109,325 -

Homeland Security Grant Program:Citizen Corps Grant 97.067 11-CC-A6-05-52-01-473 6,750 - Citizen Corps Grant 97.067 13-CC-58-05-52-01-422 7,481 - CERT Grant 97.067 11-CI-A6-05-52-01-477 5,292 - CERT Grant 97.067 14-CI-58-05-52-01-137 7,477 - Domestic Security Funding 97.067 12-DS-20-05-52-01-472 96,121 - Domestic Security Funding 97.067 13-DS-97-05-52-01-459 36,662 - Domestic Security Funding 97.067 10-DS-39-05-52-01-330 1,305 - Domestic Security Funding 97.067 11-DS-9Z-05-52-01-385 43,202 -

Passed through Florida Department of Financial Services:2007-2010 State Homeland Security Grant Program 97.067 FM257 5,722 5,019 2008-2009 State Homeland Security Grant Program 97.067 FM274 - - 2009-2010 State Homeland Security Grant Program 97.067 FM278 529 - 2010 State Homeland Security Grant Program 97.067 FM285 65,768 7,015

Total Homeland Security Grant Program 276,309 12,034

Total U.S. Department of Homeland Security 401,483 12,034

TOTAL EXPENDITURES OF FEDERAL AWARDS 6,962,534$ 2,178,550$

Notes:

Disaster Relief Funding - Tropical Storm Fay 97.036 09-PA-B9-05-52-00-543 44,808 -

(Continued)

(1) Marion County received the following Disaster Relief Funds from DCA in FY13 for expenditures that occurred in

Federal Grantor /Pass-Through Grantor /

Program Title / Project Title

225

StateState State Amount

CSFA State Expenditures Provided to Number Identification Number Only Subrecipients

STATE FINANCIAL ASSISTANCE

Florida Department of Environmental Protection:

Direct Programs:Cooperative Collection Center Grant:

Hazardous Waste Cooperative Collection Center 37.007 S0623 24,906 -

Direct Programs:Divert Wastewater Flows Projects:

SS Regional Wastewater Treatment Fac to SSS Wastewtr. Treatmt. 37.039 S0628 295,204 -

Passed through Southwest Florida Water Management District:Water Protection and Sustainability Program:

Oak Run Reclaimed Water Main (L650) 37.066 09CS0000003 222,004 -

Total Florida Department of Environmental Protection 542,114 -

Florida Department of State:

Direct Programs:State Aid to Libraries 45.030 13-ST-29 159,475 -

Total Florida Department of State 159,475 -

Florida Department of Community Affairs:

Direct Programs:Emergency Management Programs:

Emergency Management Preparedness & Assistance 31.063 13-BG-05-05-52-01-042 83,066 - Emergency Management Preparedness & Assistance 31.063 14-BG-83-05-52-01-042 59,540

Total Emergency Management Programs 142,606 -

Total Florida Department of Community Affairs 142,606 -

Florida Housing Finance Corporation:

Direct Programs:State Housing Initiatives Partnership (SHIP) Program 52.901 N/A 887,486 388,010

Total Florida Housing Finance Corporation 887,486 388,010

Florida Fish and Wildlife Conservation Commission

Direct Programs:Florida Boating Improvement Program (FBIP) 77.006 12259 54,179 -

Total Florida Fish and Wildlife Conservation Commission 54,179 -

Florida Department of Transportation:

Direct Programs:Aviation Development Grants:

JPA-Aircraft Parking Apron @ Dunnellon Airport/FM#: 429799-1-94-01 55.004 AQO81 271,463 -

Total Aviation Development Grants 271,463 -

State Grantor /Pass-Through Grantor /

Program Title / Project Title

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

(Continued)

226

StateState State Amount

CSFA State Expenditures Provided to Number Identification Number Only Subrecipients

STATE FINANCIAL ASSISTANCE

Florida Department of Environmental Protection:

Direct Programs:Cooperative Collection Center Grant:

Hazardous Waste Cooperative Collection Center 37.007 S0623 24,906 -

Direct Programs:Divert Wastewater Flows Projects:

SS Regional Wastewater Treatment Fac to SSS Wastewtr. Treatmt. 37.039 S0628 295,204 -

Passed through Southwest Florida Water Management District:Water Protection and Sustainability Program:

Oak Run Reclaimed Water Main (L650) 37.066 09CS0000003 222,004 -

Total Florida Department of Environmental Protection 542,114 -

Florida Department of State:

Direct Programs:State Aid to Libraries 45.030 13-ST-29 159,475 -

Total Florida Department of State 159,475 -

Florida Department of Community Affairs:

Direct Programs:Emergency Management Programs:

Emergency Management Preparedness & Assistance 31.063 13-BG-05-05-52-01-042 83,066 - Emergency Management Preparedness & Assistance 31.063 14-BG-83-05-52-01-042 59,540

Total Emergency Management Programs 142,606 -

Total Florida Department of Community Affairs 142,606 -

Florida Housing Finance Corporation:

Direct Programs:State Housing Initiatives Partnership (SHIP) Program 52.901 N/A 887,486 388,010

Total Florida Housing Finance Corporation 887,486 388,010

Florida Fish and Wildlife Conservation Commission

Direct Programs:Florida Boating Improvement Program (FBIP) 77.006 12259 54,179 -

Total Florida Fish and Wildlife Conservation Commission 54,179 -

Florida Department of Transportation:

Direct Programs:Aviation Development Grants:

JPA-Aircraft Parking Apron @ Dunnellon Airport/FM#: 429799-1-94-01 55.004 AQO81 271,463 -

Total Aviation Development Grants 271,463 -

State Grantor /Pass-Through Grantor /

Program Title / Project Title

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

(Continued)

226

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

StateState State Amount

CSFA State Expenditures Provided to Number Identification Number Only Subrecipients

Florida Department of Transportation, continued:

Direct Programs, continued:County Incentive Grant Program:

CIGP Agreement-SW 42 Street Flyover/FM#: 424185-1-58-01 55.008 AQ366 1,924,198 -

Transportation Regional Incentive Program:LAP Agreement-SE 92nd Loop/FPN: 424186-1-48-01 55.026 AQ863 1,229,683 -

Total Florida Department of Transportation 3,425,344 -

Florida Department of Children and Families:

Direct Programs:Public Safety, Mental Health, and Substance AbuseLocal Matching Grant 60.115 LHZ32 139,271 -

Total Florida Department of Children and Families 139,271 -

Florida Department of Health:

Direct Programs:Emergency Medical Services County Grant 64.005 C1042 43,633 -

Total Florida Department of Health 43,633 -

TOTAL EXPENDITURES OF STATE FINANCIAL ASSISTANCE 5,394,108$ 388,010$

TOTAL EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE 12,356,642$ 2,566,560$

Notes:

12-13 Local Government Water Supply Funding N/A N/A 8,745

Basis of Presentation

(Concluded)

(1) Marion County received the following Local Government Water Supply Funding Assistance from WRWSA in FY13:

The accompanying schedule of expenditures of federal awards and state financial assistance includes the federal and state grant activity of Marion County, Florida and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Chapter 10.550, Rules of the Auditor General . Therefore, some amounts presented in this schedule may differ from amounts presented in, or used in, the preparation of the financial statements.

Pass-Through Grantor /Program Title / Project Title

State Grantor /

227

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS ANDSTATE FINANCIAL ASSISTANCE

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2013MARION COUNTY, FLORIDA

StateState State Amount

CSFA State Expenditures Provided to Number Identification Number Only Subrecipients

Florida Department of Transportation, continued:

Direct Programs, continued:County Incentive Grant Program:

CIGP Agreement-SW 42 Street Flyover/FM#: 424185-1-58-01 55.008 AQ366 1,924,198 -

Transportation Regional Incentive Program:LAP Agreement-SE 92nd Loop/FPN: 424186-1-48-01 55.026 AQ863 1,229,683 -

Total Florida Department of Transportation 3,425,344 -

Florida Department of Children and Families:

Direct Programs:Public Safety, Mental Health, and Substance AbuseLocal Matching Grant 60.115 LHZ32 139,271 -

Total Florida Department of Children and Families 139,271 -

Florida Department of Health:

Direct Programs:Emergency Medical Services County Grant 64.005 C1042 43,633 -

Total Florida Department of Health 43,633 -

TOTAL EXPENDITURES OF STATE FINANCIAL ASSISTANCE 5,394,108$ 388,010$

TOTAL EXPENDITURES OF FEDERAL AWARDS AND STATE FINANCIAL ASSISTANCE 12,356,642$ 2,566,560$

Notes:

12-13 Local Government Water Supply Funding N/A N/A 8,745

Basis of Presentation

(Concluded)

(1) Marion County received the following Local Government Water Supply Funding Assistance from WRWSA in FY13:

The accompanying schedule of expenditures of federal awards and state financial assistance includes the federal and state grant activity of Marion County, Florida and is presented on the accrual basis of accounting. The information in this schedule is presented in accordance with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations and Chapter 10.550, Rules of the Auditor General . Therefore, some amounts presented in this schedule may differ from amounts presented in, or used in, the preparation of the financial statements.

Pass-Through Grantor /Program Title / Project Title

State Grantor /

227

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FEDERAL AWARD PROGRAMS AND STATE PROJECTS

FOR THE YEAR ENDED SEPTEMBER 30, 2013 MARION COUNTY, FLORIDA

PART A - SUMMARY OF AUDIT RESULTS 1. The auditors' report expresses an unmodified opinion on the basic financial statements

of Marion County, Florida, as of and for the year ended September 30, 2013. 2. No significant deficiencies relating to the audit of the financial statements are reported

in the report on internal control over financial reporting and on compliance and other matters based on an audit of the basic financial statements of Marion County, Florida.

3. No instances of noncompliance material to the basic financial statements of Marion

County, Florida were disclosed during the audit (same report as No. 2 above). 4. No significant deficiencies relating to the audit of the major federal programs and state

projects are reported in the report on compliance with requirements applicable to each major program and on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General.

5. The auditors' report on compliance for the major federal programs and state projects

for Marion County, Florida expresses an unmodified opinion (same report as No. 4 above).

6. The audit disclosed no findings required to be reported in accordance with Section

510(a) of OMB Circular A-133 or Chapter 10.550, Rules of the Auditor General, relative to the major federal programs and state projects for Marion County, Florida.

7. The programs/projects tested as major programs/projects included the following: ■ Federal Programs ● U.S. Department of Housing and Urban Development ► Community Development Block Grants/Entitlement Grants CFDA No. 14.218 ■ State Projects

● Florida Department of Transportation ► County Incentive Grant Program, CSFA No. 55.008 ► Transportation Regional Incentive Program, CFSA No. 55.026

8. The threshold for distinguishing Type A and Type B programs/projects was $300,000

for major federal award programs and $300,000 major state financial assistance projects.

9. Marion County, Florida did qualify as a low-risk auditee pursuant to OMB Circular A-133.

228

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FEDERAL AWARD PROGRAMS AND STATE PROJECTS

FOR THE YEAR ENDED SEPTEMBER 30, 2013 MARION COUNTY, FLORIDA

PART A - SUMMARY OF AUDIT RESULTS 1. The auditors' report expresses an unmodified opinion on the basic financial statements

of Marion County, Florida, as of and for the year ended September 30, 2013. 2. No significant deficiencies relating to the audit of the financial statements are reported

in the report on internal control over financial reporting and on compliance and other matters based on an audit of the basic financial statements of Marion County, Florida.

3. No instances of noncompliance material to the basic financial statements of Marion

County, Florida were disclosed during the audit (same report as No. 2 above). 4. No significant deficiencies relating to the audit of the major federal programs and state

projects are reported in the report on compliance with requirements applicable to each major program and on internal control over compliance in accordance with OMB Circular A-133 and Chapter 10.550, Rules of the Auditor General.

5. The auditors' report on compliance for the major federal programs and state projects

for Marion County, Florida expresses an unmodified opinion (same report as No. 4 above).

6. The audit disclosed no findings required to be reported in accordance with Section

510(a) of OMB Circular A-133 or Chapter 10.550, Rules of the Auditor General, relative to the major federal programs and state projects for Marion County, Florida.

7. The programs/projects tested as major programs/projects included the following: ■ Federal Programs ● U.S. Department of Housing and Urban Development ► Community Development Block Grants/Entitlement Grants CFDA No. 14.218 ■ State Projects

● Florida Department of Transportation ► County Incentive Grant Program, CSFA No. 55.008 ► Transportation Regional Incentive Program, CFSA No. 55.026

8. The threshold for distinguishing Type A and Type B programs/projects was $300,000

for major federal award programs and $300,000 major state financial assistance projects.

9. Marion County, Florida did qualify as a low-risk auditee pursuant to OMB Circular A-133.

228

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FEDERAL AWARD PROGRAMS AND STATE PROJECTS

FOR THE YEAR ENDED SEPTEMBER 30, 2013 MARION COUNTY, FLORIDA

(Concluded)

PART B - FINDINGS - FINANCIAL STATEMENTS 1. No matters were reported. PART C - FINDINGS AND QUESTIONED COSTS - MAJOR FEDERAL AWARD PROGRAMS 1. No matters were reported. PART D - FINDINGS AND QUESTIONED COST - MAJOR STATE FINANCIAL ASSISTANCE

PROJECTS 1. No matters were reported. PART E - OTHER ISSUES 1. No summary Schedule of Prior Audit Findings is required because there were no prior

audit findings related to federal programs or state projects. 2. No Corrective Action Plan is required because there were no findings required to be

reported under the Federal or Florida Single Audit Acts.

229

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FEDERAL AWARD PROGRAMS AND STATE PROJECTS

FOR THE YEAR ENDED SEPTEMBER 30, 2013 MARION COUNTY, FLORIDA

(Concluded)

PART B - FINDINGS - FINANCIAL STATEMENTS 1. No matters were reported. PART C - FINDINGS AND QUESTIONED COSTS - MAJOR FEDERAL AWARD PROGRAMS 1. No matters were reported. PART D - FINDINGS AND QUESTIONED COST - MAJOR STATE FINANCIAL ASSISTANCE

PROJECTS 1. No matters were reported. PART E - OTHER ISSUES 1. No summary Schedule of Prior Audit Findings is required because there were no prior

audit findings related to federal programs or state projects. 2. No Corrective Action Plan is required because there were no findings required to be

reported under the Federal or Florida Single Audit Acts.

229

MANAGEMENT LETTER The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida We have audited the basic financial statements of Marion County, Florida (the County), as of and for the fiscal year ended September 30, 2013, and have issued our report thereon dated March 6, 2014. We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations; and Chapter 10.550, Rules of the Auditor General. We have issued our Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards, Independent Auditors’ Report on Compliance for Each Major Federal Program and State Project and on Internal Control over Compliance in Accordance with OMB Circular A-133 and Chapter 10.550 Rules of the Auditor General and Schedule of Findings and Questioned Costs. Disclosures in those reports and schedule, which are dated March 6, 2014, should be considered in conjunction with this management letter. Additionally, our audit was conducted in accordance with Chapter 10.550, Rules of the Auditor General, which govern the conduct of local governmental entity audits performed in the State of Florida. This letter includes the following information, which is not included in the aforementioned auditors’ reports or schedule: ■ Section 10.554(1)(i)1., Rules of the Auditor General, requires that we determine whether or not

corrective actions have been taken to address findings and recommendations made in the preceding annual financial audit report. There were no prior year findings or recommendations.

■ Section 10.554(1)(i)2., Rules of the Auditor General, requires our audit to include a review of the

provisions of Section 218.415, Florida Statutes, regarding the investment of public funds. In connection with our audit, we determined that the County complied with Section 218.415, Florida Statutes.

■ Section 10.554(1)(i)3., Rules of the Auditor General, requires that we address in the management

letter any recommendations to improve financial management. In connection with our audit, we did not have any such recommendations.

■ Section 10.554(1)(i)4., Rules of the Auditor General, requires that we address noncompliance with the

provisions of contracts or grant agreements, or abuse, that have occurred, or are likely to have occurred, that would have an effect on the financial statements that is less than material but not which warrants the attention of those charged with governance. In connection with our audit, we did not have any such findings.

230

MANAGEMENT LETTER The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida We have audited the basic financial statements of Marion County, Florida (the County), as of and for the fiscal year ended September 30, 2013, and have issued our report thereon dated March 6, 2014. We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations; and Chapter 10.550, Rules of the Auditor General. We have issued our Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards, Independent Auditors’ Report on Compliance for Each Major Federal Program and State Project and on Internal Control over Compliance in Accordance with OMB Circular A-133 and Chapter 10.550 Rules of the Auditor General and Schedule of Findings and Questioned Costs. Disclosures in those reports and schedule, which are dated March 6, 2014, should be considered in conjunction with this management letter. Additionally, our audit was conducted in accordance with Chapter 10.550, Rules of the Auditor General, which govern the conduct of local governmental entity audits performed in the State of Florida. This letter includes the following information, which is not included in the aforementioned auditors’ reports or schedule: ■ Section 10.554(1)(i)1., Rules of the Auditor General, requires that we determine whether or not

corrective actions have been taken to address findings and recommendations made in the preceding annual financial audit report. There were no prior year findings or recommendations.

■ Section 10.554(1)(i)2., Rules of the Auditor General, requires our audit to include a review of the

provisions of Section 218.415, Florida Statutes, regarding the investment of public funds. In connection with our audit, we determined that the County complied with Section 218.415, Florida Statutes.

■ Section 10.554(1)(i)3., Rules of the Auditor General, requires that we address in the management

letter any recommendations to improve financial management. In connection with our audit, we did not have any such recommendations.

■ Section 10.554(1)(i)4., Rules of the Auditor General, requires that we address noncompliance with the

provisions of contracts or grant agreements, or abuse, that have occurred, or are likely to have occurred, that would have an effect on the financial statements that is less than material but not which warrants the attention of those charged with governance. In connection with our audit, we did not have any such findings.

230

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

MANAGEMENT LETTER (Concluded)

■ Section 10.554(1)(i)5., Rules of the Auditor General, requires that the name or official title and legal

authority for the primary government and each component unit of the reporting entity be disclosed in this management letter, unless disclosed in the notes to the financial statements. The legal authority for the County and its component units is reported in Note 1 to the basic financial statements, provides that the auditor may, based on professional judgment, report the following matters that have an inconsequential effect on the financial statements, considering both quantitative and qualitative factors: (1) violations of provisions of contracts or grant agreements, fraud, illegal acts, or abuse; and (2) deficiencies in internal control that are not significant deficiencies. In connection with our audit, we did not have any such findings.

■ Section 10.554(1)(i)6.a., Rules of the Auditor General, requires a statement be included as to whether

or not the local governmental entity has met one or more of the conditions described in Section 218.503(1), Florida Statutes, and identification of the specific condition(s) met. In connection with our audit, we determined that the County did not meet any of the conditions described in Section 218.503(1), Florida Statutes.

■ Section 10.554(1)(i)6.b., Rules of the Auditor General, requires that we determine whether the annual

financial report for the County for the fiscal year ended September 30, 2013, filed with the Florida Department of Financial Services pursuant to Section 218.32(1)(a), Florida Statutes, is in agreement with the annual financial audit report for the fiscal year ended September 30, 2013. In connection with our audit, we determined that these two reports were in agreement.

■ Pursuant to Sections 10.554(1)(i)6.c. and 10.556(7)., Rules of the Auditor General, we applied

financial condition assessment procedures. It is management’s responsibility to monitor the County’s financial condition, and our financial condition assessment was based in part on representations made by management and the review of financial information provided by same.

Our management letter is intended solely for the information and use of Legislative Auditing Committee, members of the Florida Senate and Florida House of Representatives, the Florida Auditor General, Federal and other granting agencies, and applicable management, and is not intended to be and should not be used by anyone other than these specified parties. We wish to take this opportunity to thank you and your staff for the cooperation and courtesies extended to us during the course of our audit. Please let us know if you have any questions or comments concerning this letter, our accompanying reports, or other matters. March 6, 2014 Ocala, Florida

231

The Honorable Board of the County Commissioners Marion County, Florida Ocala, Florida

MANAGEMENT LETTER (Concluded)

■ Section 10.554(1)(i)5., Rules of the Auditor General, requires that the name or official title and legal

authority for the primary government and each component unit of the reporting entity be disclosed in this management letter, unless disclosed in the notes to the financial statements. The legal authority for the County and its component units is reported in Note 1 to the basic financial statements, provides that the auditor may, based on professional judgment, report the following matters that have an inconsequential effect on the financial statements, considering both quantitative and qualitative factors: (1) violations of provisions of contracts or grant agreements, fraud, illegal acts, or abuse; and (2) deficiencies in internal control that are not significant deficiencies. In connection with our audit, we did not have any such findings.

■ Section 10.554(1)(i)6.a., Rules of the Auditor General, requires a statement be included as to whether

or not the local governmental entity has met one or more of the conditions described in Section 218.503(1), Florida Statutes, and identification of the specific condition(s) met. In connection with our audit, we determined that the County did not meet any of the conditions described in Section 218.503(1), Florida Statutes.

■ Section 10.554(1)(i)6.b., Rules of the Auditor General, requires that we determine whether the annual

financial report for the County for the fiscal year ended September 30, 2013, filed with the Florida Department of Financial Services pursuant to Section 218.32(1)(a), Florida Statutes, is in agreement with the annual financial audit report for the fiscal year ended September 30, 2013. In connection with our audit, we determined that these two reports were in agreement.

■ Pursuant to Sections 10.554(1)(i)6.c. and 10.556(7)., Rules of the Auditor General, we applied

financial condition assessment procedures. It is management’s responsibility to monitor the County’s financial condition, and our financial condition assessment was based in part on representations made by management and the review of financial information provided by same.

Our management letter is intended solely for the information and use of Legislative Auditing Committee, members of the Florida Senate and Florida House of Representatives, the Florida Auditor General, Federal and other granting agencies, and applicable management, and is not intended to be and should not be used by anyone other than these specified parties. We wish to take this opportunity to thank you and your staff for the cooperation and courtesies extended to us during the course of our audit. Please let us know if you have any questions or comments concerning this letter, our accompanying reports, or other matters. March 6, 2014 Ocala, Florida

231

232

232