complying with the safeguard rule

TRANSCRIPT

Complying With the

Safeguard Rule

Ryan Lane

Director, KPA Sales & Finance Compliance

Jim Radogna

Sales & Finance Compliance Consultant

Moderator

Rebecca Ward

Sr. Marketing Content Specialist

(303) 219-7802

A comprehensive solution for Environmental Health & Safety, HR

Management, and Sales & Finance Compliance.

• 8/10 of the largest dealership groups in the

country count on KPA.

• KPA has been endorsed by 26 national and

state dealer associations

• Founding member of the Clean Auto Alliance.

KPA delivers Environmental Health & Safety, HR Management and Sales & Finance

Compliance programs that help our clients achieve regulatory compliance, control risk, protect

their assets and effectively manage people through a combination of innovative software,

award winning training and on-site consulting. Over 5,200 clients, including 8 out of 10 of the

largest dealership groups in the country, count on KPA for Environmental Health & Safety, HR

Management and Sales & Finance Compliance programs that save them time and save them

money.

KPA minimizes risks and maximizes profit for

5,200 dealers nationwide.

KPA

Environmental

Health &

Safety

KPA Human

Resource

Management

KPA Sales &

Finance

Compliance

Compliance

Presenter

Ryan Lane

Director, KPA Sales & Finance Compliance

(303) 802-3095

Presenter

Jim Radogna

Sales & Finance Compliance Consultant

(303) 228-8770

Questions

If you have questions during

the presentation, please

submit them using the

“Questions” feature

Questions will be answered

at the end of the webinar

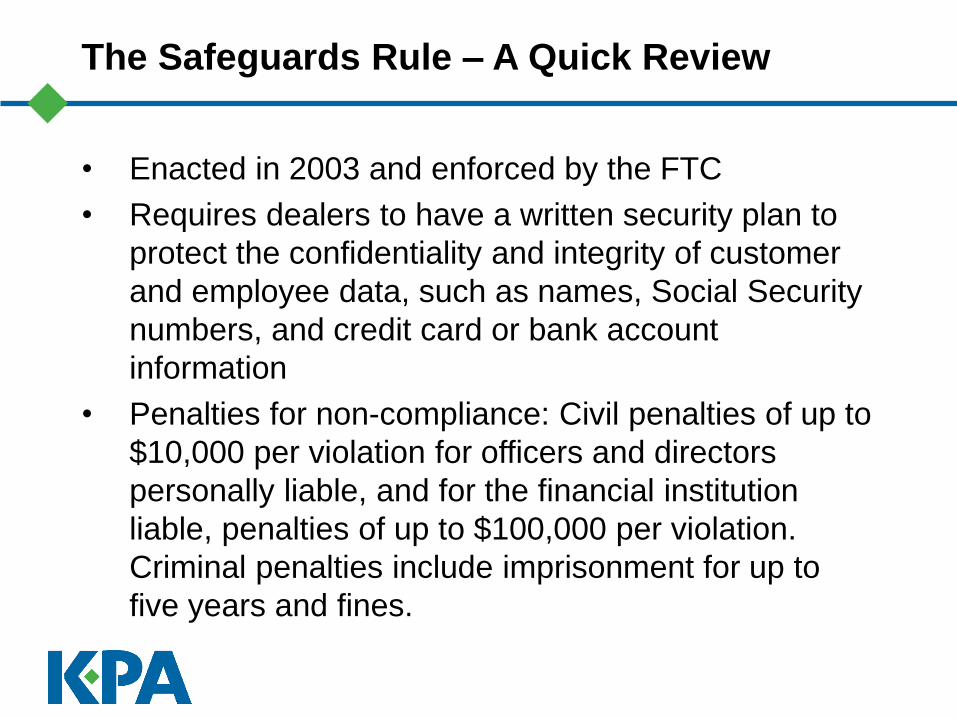

The Safeguards Rule – A Quick Review

• Enacted in 2003 and enforced by the FTC

• Requires dealers to have a written security plan to

protect the confidentiality and integrity of customer

and employee data, such as names, Social Security

numbers, and credit card or bank account

information

• Penalties for non-compliance: Civil penalties of up to

$10,000 per violation for officers and directors

personally liable, and for the financial institution

liable, penalties of up to $100,000 per violation.

Criminal penalties include imprisonment for up to

five years and fines.

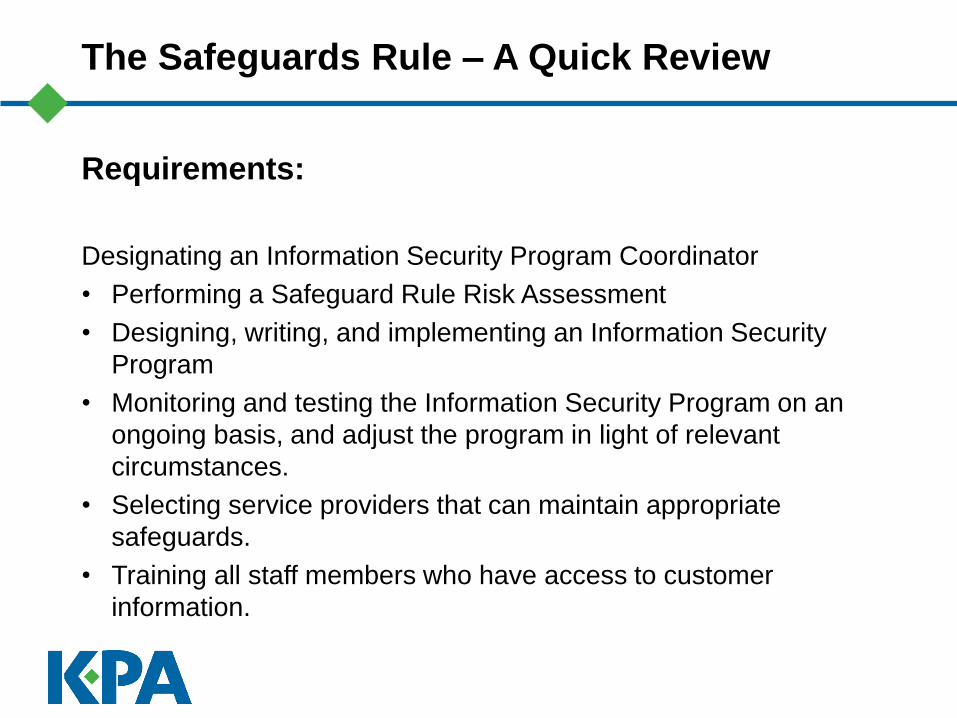

The Safeguards Rule – A Quick Review

Requirements:

Designating an Information Security Program Coordinator

• Performing a Safeguard Rule Risk Assessment

• Designing, writing, and implementing an Information Security

Program

• Monitoring and testing the Information Security Program on an

ongoing basis, and adjust the program in light of relevant

circumstances.

• Selecting service providers that can maintain appropriate

safeguards.

• Training all staff members who have access to customer

information.

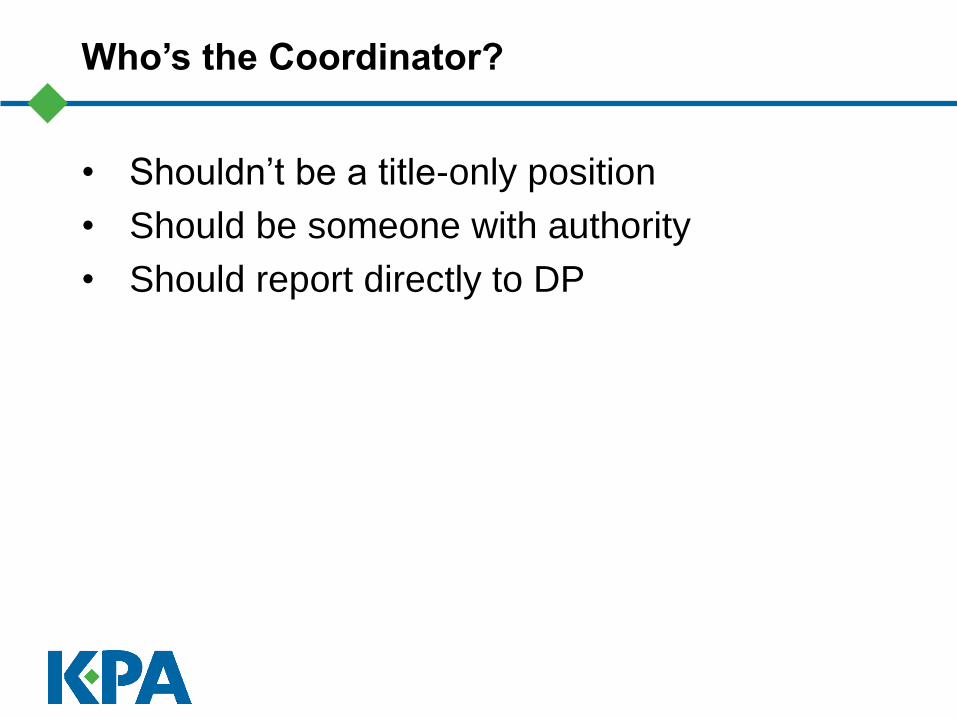

Who’s the Coordinator?

• Shouldn’t be a title-only position

• Should be someone with authority

• Should report directly to DP

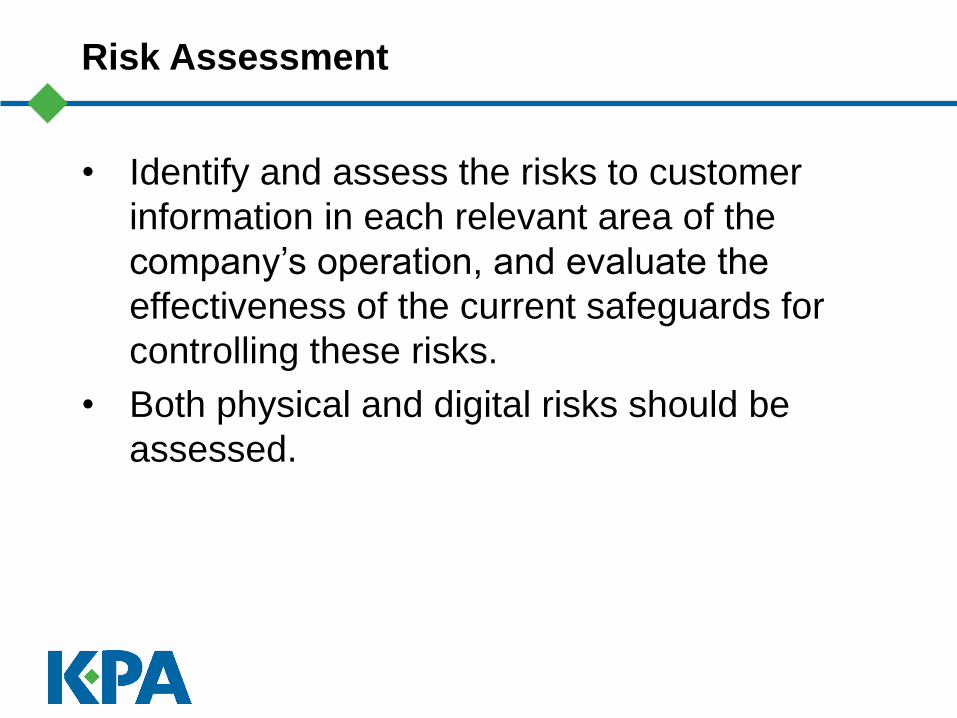

Risk Assessment

• Identify and assess the risks to customer

information in each relevant area of the

company’s operation, and evaluate the

effectiveness of the current safeguards for

controlling these risks.

• Both physical and digital risks should be

assessed.

Written Program

• Must be in writing

• Should be comprehensive

• Shouldn’t be a static document.

• Policy must be implemented

Service Providers

• Should have written agreement with every vendor

that has access to dealer’s customer data.

• Service Provider should represent and warrant that it

will implement and maintain safeguards as are

necessary to protect the customer information provided

by dealer from unauthorized disclosure.

• Agreement should indemnify and hold dealer

harmless from any liability arising out Service

Provider's failure to protect the Customer Information.

Monitoring and Testing

• Most dealers miss this step

• Should be performed on a periodic basis and

documented.

• Should be monitored as frequently as

necessary to ensure that the procedures are

in place and operating effectively.

• It may also be beneficial to hire an outside

party to audit the system on a regular basis,

providing the dealership with an independent

view.

Technology Challenges

• Dealerships are far more technologically

advanced than they were when the Safeguards

Rule first came into play

• Protecting consumer information has

become quite a bit more challenging

• No longer just a matter of making sure that

credit apps aren’t laying on top of desks in the

showroom or that deal jackets are stored in

locking cabinets.

Technology Challenges

• A dealer’s Safeguards system is only as good as its ability to

respond to the latest threat

• The FTC charged a GA dealer with illegally exposing the

sensitive personal information of thousands of consumers by

allowing peer-to-peer, file-sharing software

• An employee downloaded consumer data files onto a flash

drive and took them home to work on them using his home

computer

• The home computer contained the peer-to-peer software that

triggered the breach

• None of the dealership's computers ever were loaded with the

peer-to-peer software

• Any violation of the 20 year consent decree could cost the

dealer $16,000 each

Best Practices

• Access to customer information should be limited to employees

who have a business reason to see it; to the extent they need it to

do their jobs.

• Dealership employees should not be permitted to use or

reproduce customer information for their own use or for any use not

authorized by the Dealership.

• Customer information should not be allowed to leave the

dealership, either in paper form or on employees’ electronic

devices.

• Customer information should always remain in management

control.

• Allowing staff members to retain “working” customer files for

follow-up purposes is risky at best.

Best Practices

• Consider limiting CRM access to dealership computers only for

all but the most trusted top-level personnel.

• If you allow certain employees to use personal computers to

store or access customer data, they should be required to use

protections against viruses, spyware, and other unauthorized

intrusions.

• The dealership should utilize anti-virus software and maintain

computer firewalls.

• The ability to download customer information from dealership

computers to portable media such as USB drives, external hard

drives, or other remote devices should be disabled.

Best Practices

• Paper-based customer information should not be left exposed

and unattended in an unsecured area, and should be stored in a

room or file cabinets that are locked or otherwise not available to

the general public. Be aware that consumer information in plain

sight can be taken or even photographed with a cell phone.

• All customer information should be disposed of in a secure

manner. Paper-based customer information should be shredded

prior to disposal and electronic information should be effectively

deleted prior to hardware disposal. This includes the hard drives of

digital copiers, fax machines and PCs.

• Electronic customer information should be stored on secure

servers and access to the information should be password

controlled.

Best Practices

• Computer monitors in non-secure areas should be locked when

not in use. Password-activated screen savers should be used to

lock employee computers after a period of inactivity.

• “Strong” passwords should be required and changed on a

regular basis. (Tough-to-crack passwords require the use of at least

six characters, upper- and lower-case letters, and a combination of

letters, numbers, and symbols.) Passwords should not be shared or

openly posted in work areas.

• Inbound or outbound credit card information, credit applications,

or other sensitive financial data transmitted to the dealership

directly from consumers should only be sent through an encrypted

or secure connection.

Best Practices

• Consumers should be advised against transmitting sensitive

data by email or fax. If sensitive data must be transmitted to the

dealership by email, such transmissions should be password

controlled or otherwise protected from theft or unauthorized access.

• Customer financial information should not be stored on any

computer system with a direct Internet connection.

• Policies should be in place for appropriate use and protection of

laptops, PDAs, cell phones, and other mobile devices.

• Terminated employees should be prevented from accessing

customer information by immediately deactivating their passwords

and user names and taking other appropriate measures.

Best Practices

• Procedures should be established to preserve the security,

confidentiality and integrity of customer information in the event of a

computer or other technological failure.

• The dealership should notify customers promptly if their

customer information is subject to loss, damage or unauthorized

access. The FTC requires this and time will be critical in the

aftermath of a breach to identify the problem, fix it, and take

appropriate response measures.

• Employee training is a key component of an effective

Safeguards program. Staff members should be trained to take

basic steps to maintain the security, confidentiality, and integrity of

customer information.

• New employees should be trained immediately and all

employees should be retrained regularly.

You Never Know Who’s Lurking…

High-tech data breaches are challenging but

low-tech problems are still common…

Questions and Answers

Contact Information

The recorded webinar and presentation slides will be emailed to

you today including your local representative’s contact information.

www.kpaonline.com

866-228-6587