composition municipal insurance 101 ny municipal insurance reciprocal robert bambino syllabus 1.town...

TRANSCRIPT

CompositionCompositionMunicipal Insurance 101

NY Municipal

Insurance Reciprocal

Robert Bambino

Syllabus

1. Town Ins. Programs

2. Coverages & Limits

3. Where Premium Dollars are Spent

4. Limits, Exclusions & other Pitfalls to Avoid

I. ‘Typical’ Town Property & Casualty Insurance Program

Property Insurance Loss or damage to buildings, property and equipment

Automobile Insurance Liability claims from third-parties and damage to owned vehicles

General Liability Public liability claims alleging injury, damage to property and other perils

‘Typical’ Town Property & Casualty Insurance Programs

Law Enforcement Liability

Claims arising from law enforcement activities & operations

Public Officials Professional liability claims arising from wrongful acts of the Board, elected and appointed officials

Excess Liability Additional limits above Automobile, General Liability, Law Enforcement and Public Officials Liability

II. Coverages & Limits

Property Dwellings, furniture, supplies, business property, equipment, records, computers; extra expenses

Blanket limit for all insured property within the Town

Automobile

(Liability &

Physical Damage)

Injuries and damages caused by autos, trucks, vans, snow plows; damage to owned/leased autos, trucks and vans

$1,000,000 CSL

$200 – 1,000

deductible for physical damage

Coverages and Limits

General Liability

Streets & roads, sidewalk claims, recreation, assaults

$1,000,000/

2,000,000

Law Enforcement

False arrest, use of force, civil rights

$1,000,000/

2,000,000

Public Officials

Employment practices, civil rights & land use

$1,000,000/

2,000,000

Excess ‘Follow-Form’ Policy

(Excess limits above liability policies)

$5,000,000 to

10,000,000

Other CoveragesInland Marine (“Floaters”) Damage to equipment off

premises with a lower deductible

Boiler & Machinery Damage to boilers & other equipment not covered within the property policy

Crime Coverage Employee theft and embezzlement

Limited Pollution Liability Covers sudden and accidental pollution events emanating on-premises

III. Allocation of Premium Dollars: Mid-Size Town

0% 5% 10% 15% 20% 25%

Gen. Liability

Automobile

Pub. Officials

Excess

Property

Law Enforcement

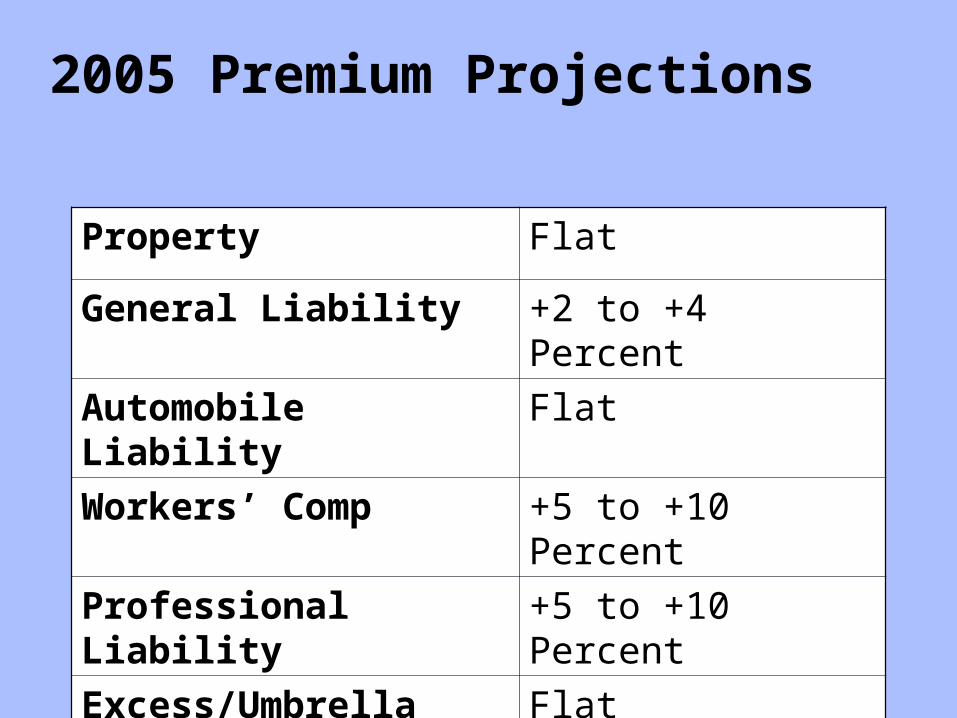

2005 Premium Projections

Property Flat

General Liability +2 to +4 Percent

Automobile Liability Flat

Workers’ Comp +5 to +10 Percent

Professional Liability +5 to +10 Percent

Excess/Umbrella Flat

Breakdown of Incurred Losses: Where are the Loss Dollars Going?

17%

27%

10%

18%

28%

Automobile

Gen. Liability

Property

Law Enforcement

Public Officials

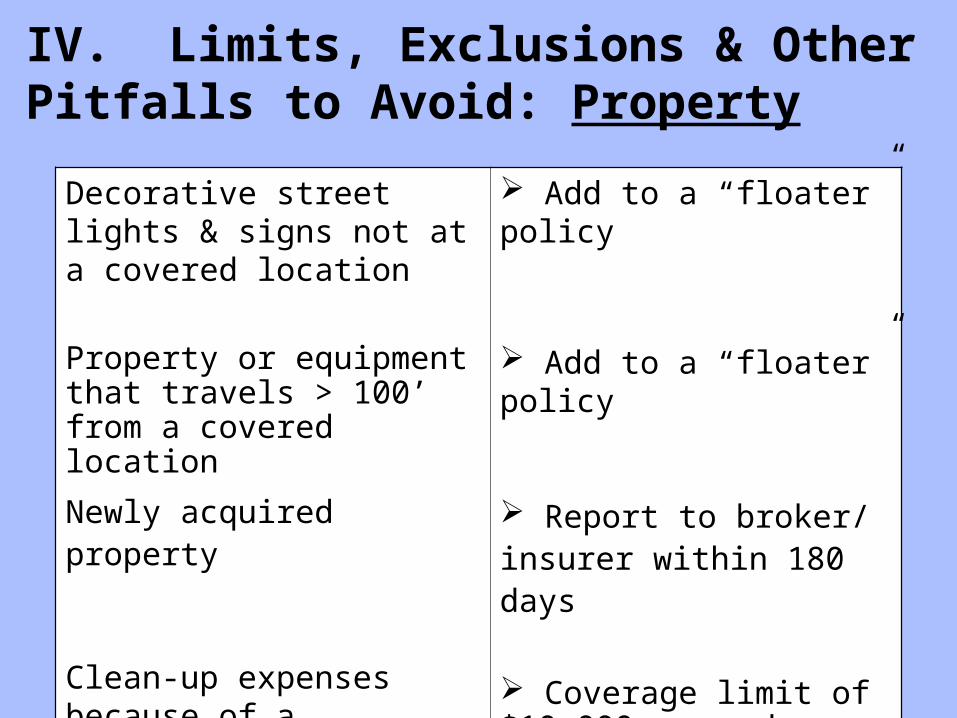

IV. Limits, Exclusions & Other Pitfalls to Avoid: Property

Decorative street lights & signs not at a covered location

Property or equipment that travels > 100’ from a covered location

Newly acquired property

Clean-up expenses because of a pollution loss

Add to a “floater” policy

Add to a “floater” policy

Report to broker/ insurer within 180 days

Coverage limit of $10,000 – purchase higher limits

Limits, Exclusions & Other Pitfalls to Avoid: General Liability

•Owned underground or above ground storage tanks

• Liability deductibles

• Property in Town’s care and custody

• Asbestos/ lead abatement projects

Purchase separate environmental (tank) liability insurance Change for full coverage

Purchase Garage Policy for confiscated vehicles; floater if storing or warehousing nonowned property

Have contractor provide coverage,or purchase separate policy

Limits, Exclusions & Other Pitfalls to AvoidPublic Officials

• Fines & penalties • Wages & benefits – employment practices• Fiduciary liability – financial management of employee benefit plans• Limited land use coverage• EP liability sublimits

Risk control Risk control

Purchase Fiduciary Liability insurance policy

Risk control

Increase, remove or practice risk control

Frequently Asked QuestionsQ: Do I need a Builders Risk Policy?A: Yes, for large renovations and new construction –

unless the Gen. Contractor provides it

Q: What should the limits be for my employee theft coverage?

A: Difficult to determine. You can use: MPL x [ f ] f = efficiency of fraud control methods. Limits may

not be available!

Q: Do I have coverage for skateboard parks, pools and snowmobile trails?

A: Generally – yes, but you should contact your broker or insurer – might be an additional premium

Frequently Asked Questions

Q: Do we need to purchase mold coverage?A: Maybe – its something to check on. There

may be coverage under the GL policy; the Property policy only covers if it is a result of a covered loss.

Q: Which motor vehicles should I cover with Auto Physical Damage insurance?

A: Those vehicles you can’t afford to loose or replace.