concession length and investment timing flexibility chiara d’alpaos, cesare dosi and michele...

Post on 22-Dec-2015

217 views

TRANSCRIPT

Concession Length and Investment Timing Flexibility

Chiara DrsquoAlpaos Cesare Dosi and Michele Moretto

Concession contracts In recent years there has been a significant

increase of private sector participation in the provision of public utilities mainly because of the need for increased capital investments and the lack of public financial resources

Therefore concessions play a key role in those sectors where natural monopoly persists and competition for the market is the only viable option to achieve efficiency gains (eg water services)

Under concession contracts the government retains ownership of the infrastructure but transfers all risk for running the utility and financing the investments to the concessionaire

Concession contracts (2)

The goverment objective function is to maximize the concession value ie the value of the contract

When assigning a concession contract the regulator faces inter alia the issue of setting the concession length

Moreover whether or not allowing the concessionaire to set the timing of new investments is another key issue

Questions addressed in the paper

Does investment timing flexibility always increase the concession value

How should the regulator set the concession length in order to maximize the concession value (ie the value of the contract) when the concessionaire has no obligation about the investment timing

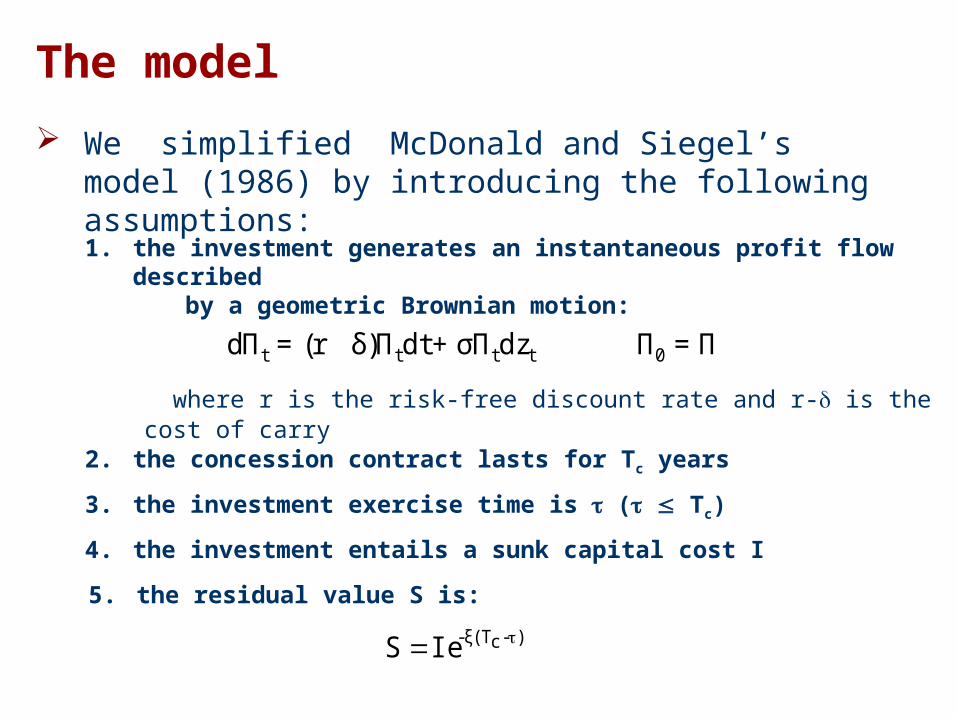

The model

We simplified McDonald and Siegelrsquos model (1986) by introducing the following assumptions

1 the investment generates an instantaneous profit flow described

by a geometric Brownian motion

where r is the risk-free discount rate and r- is the cost of carry

2 the concession contract lasts for Tc years

3 the investment exercise time is ( Tc)

Π=ΠdzΠσ+dtΠ)δr(=Πd 0tttt

4 the investment entails a sunk capital cost I

5 the residual value S is

)cT(ξIeS --

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

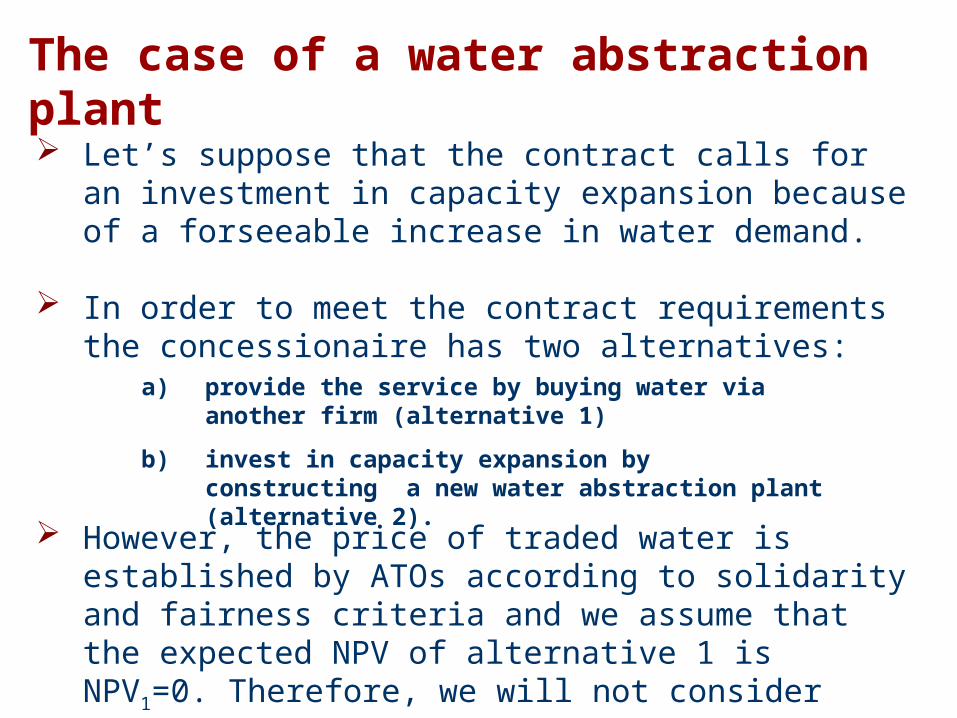

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Concession contracts In recent years there has been a significant

increase of private sector participation in the provision of public utilities mainly because of the need for increased capital investments and the lack of public financial resources

Therefore concessions play a key role in those sectors where natural monopoly persists and competition for the market is the only viable option to achieve efficiency gains (eg water services)

Under concession contracts the government retains ownership of the infrastructure but transfers all risk for running the utility and financing the investments to the concessionaire

Concession contracts (2)

The goverment objective function is to maximize the concession value ie the value of the contract

When assigning a concession contract the regulator faces inter alia the issue of setting the concession length

Moreover whether or not allowing the concessionaire to set the timing of new investments is another key issue

Questions addressed in the paper

Does investment timing flexibility always increase the concession value

How should the regulator set the concession length in order to maximize the concession value (ie the value of the contract) when the concessionaire has no obligation about the investment timing

The model

We simplified McDonald and Siegelrsquos model (1986) by introducing the following assumptions

1 the investment generates an instantaneous profit flow described

by a geometric Brownian motion

where r is the risk-free discount rate and r- is the cost of carry

2 the concession contract lasts for Tc years

3 the investment exercise time is ( Tc)

Π=ΠdzΠσ+dtΠ)δr(=Πd 0tttt

4 the investment entails a sunk capital cost I

5 the residual value S is

)cT(ξIeS --

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Concession contracts (2)

The goverment objective function is to maximize the concession value ie the value of the contract

When assigning a concession contract the regulator faces inter alia the issue of setting the concession length

Moreover whether or not allowing the concessionaire to set the timing of new investments is another key issue

Questions addressed in the paper

Does investment timing flexibility always increase the concession value

How should the regulator set the concession length in order to maximize the concession value (ie the value of the contract) when the concessionaire has no obligation about the investment timing

The model

We simplified McDonald and Siegelrsquos model (1986) by introducing the following assumptions

1 the investment generates an instantaneous profit flow described

by a geometric Brownian motion

where r is the risk-free discount rate and r- is the cost of carry

2 the concession contract lasts for Tc years

3 the investment exercise time is ( Tc)

Π=ΠdzΠσ+dtΠ)δr(=Πd 0tttt

4 the investment entails a sunk capital cost I

5 the residual value S is

)cT(ξIeS --

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Questions addressed in the paper

Does investment timing flexibility always increase the concession value

How should the regulator set the concession length in order to maximize the concession value (ie the value of the contract) when the concessionaire has no obligation about the investment timing

The model

We simplified McDonald and Siegelrsquos model (1986) by introducing the following assumptions

1 the investment generates an instantaneous profit flow described

by a geometric Brownian motion

where r is the risk-free discount rate and r- is the cost of carry

2 the concession contract lasts for Tc years

3 the investment exercise time is ( Tc)

Π=ΠdzΠσ+dtΠ)δr(=Πd 0tttt

4 the investment entails a sunk capital cost I

5 the residual value S is

)cT(ξIeS --

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The model

We simplified McDonald and Siegelrsquos model (1986) by introducing the following assumptions

1 the investment generates an instantaneous profit flow described

by a geometric Brownian motion

where r is the risk-free discount rate and r- is the cost of carry

2 the concession contract lasts for Tc years

3 the investment exercise time is ( Tc)

Π=ΠdzΠσ+dtΠ)δr(=Πd 0tttt

4 the investment entails a sunk capital cost I

5 the residual value S is

)cT(ξIeS --

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The model (2)

The market value of the project is the expected present value of discounted cash flows

where E is the expectation operator under the risk neutral probability measure (Cox and Ross 1976 Harrison and Kreps 1979)

)cT)(ξr()cT(δ

)cT(rt

rtcT0

Ie)e1(δΠ

SedtΠeE)Π(V

The value of the opportunity to invest F (ie the Extended Net Present Value) is analogous to a European call option on a dividend paying asset 0I)Π(VmaxeE τ

)t(rtt )t)tΠ(F

where )e1()Π(V )cT(δδΠ )e1(II )cT)(ξr(

is the expiration date and is the projectrsquos cash flow at time

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The model (3)

Imposing a non-arbitrage condition F (Vtt) can be obtained by solving the following second order differential equation (Black and Scholes 1973 Merton 1973)

0FrFF)V)(δr(F)V(σ21

tVVV22

subject to the terminal condition (DrsquoAlpaos and Moretto 2004)

and the boundary conditions

1V)tV(Flim0)t0(F ttV

0]0)I)Π(V[(maxlim)Π(FlimcT

τcT

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The model (4)

The solution of the second order differential equation is given by (Black and Scholes 1973)

where

and () is the cumulative standard normal distribution function

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

tσ

)t)(2σδr()I)Π(Vln()Π(d

2t

t1

tσ)Π(d)Π(d t1t2

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The Reform of the Italian Water Service Sector

The Law 3694 opened up the water service sector to competition and established a separation between water resource planning and the construction operation and management of water utilities

The resource planning is assigned to the local water authority (ATO) which in turn assigns the operation of water utilities to a concessionaire and fixes the tariff

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The case of a water abstraction plant Letrsquos suppose that the contract calls for an

investment in capacity expansion because of a forseeable increase in water demand

In order to meet the contract requirements the concessionaire has two alternatives

a) provide the service by buying water via another firm (alternative 1)

b) invest in capacity expansion by constructing a new water abstraction plant (alternative 2)

However the price of traded water is established by ATOs according to solidarity and fairness criteria and we assume that the expected NPV of alternative 1 is NPV1=0 Therefore we will not consider alternative 1

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The case of a water abstraction plant (2) Assuming a profit function linear in X we obtain

where Rt are the revenues per cubic meter Ct the operating costs for cubic meter X is the plantrsquos capacity (m3) i volume losses in the network

We make the following assumptions

XCX)i1(RΠ ttt

a) revenues are non stochastic since the tariffs are set by the ATO

b) operating costs follow a geokmetric Brownian motion with growth rate (r-) and volatility

tttt dzCσdtC)δr(dC

c) the risk free discount rate is constant over time

d) the projectrsquos residual value at the end of its lifetime is zero

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The case of a water abstraction plant (3) Therefore

bullX=03 m3s

bullI=3500000 Euros

bullTc=30 years

bullC=013 Eurom3 R=030 Eurom3

bulli=20 =2 r=5 =30

X)e1(

δC

e1r

R)i1(

Xdt]CR)i1[(eEV

)cT(δ)cT(r

ttrtcT

0

I)d(Φe)Π(V)d(Φe)tΠ(F 2)t(r

t1)t(δ

t

and

Summary information for the water abstraction plant

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

The concession value F is concave in

Figure 1 Concession value for different Tc

The case of an abstraction plant results

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Figure 2 Concession value for different and Tc

The case of a water abstraction plant results (2)

In order to maximize the concession value should determine the couple )T( c

that maximizes F

F

F

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Concluding Remarks

We investigated the impact of concession length and investment timing flexibility on concession value

It is generally argued that long-term contracts are privately valuable as they allow the concessionaire to increase the overall discounted returns

The real option theory suggests that investments timing flexibiltiy has a value making it possible to avoid costly errors

Our results suggest that it is not always the case

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-

Concluding Remarks (2) In fact there is not a monotone relationship between F and Tc

Investment timing flexibility not always increases the concession value

Under a short-term contract it might become optimal to invest immediately (NPV F)

Tc affects the optimal investment timing Therefore if the concession contact is ldquotoo longrdquo the concessionaire might be forced to defer investments in order to reduce uncertainty over future returns

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

-