conflicts of interests among shareholders - efma annual meetings/2011 … · facilities, term...

TRANSCRIPT

Debt Specialization*

Paolo Colla

Università Bocconi†

Filippo Ippolito

Università Bocconi‡

Kai Li

University of British Columbia§

This version: September, 2010 First version: October, 2009

* We thank Miguel Ferreira, Mark Flannery, Emilia Garcia, Mike Lemmon, Dave Mauer, Michael Meloche, Gordon

Phillips, Zacharias Sautner, Philip Valta, seminar participants at the New University of Lisbon (Nova), University

Carlos III de Madrid, Universitat Pompeu Fabra, Stockholm School of Economics and SIFR, and conference

participants at the 6th

Portuguese Finance Network Conference (Azores), the 2010 China International Conference in

Finance (Beijing), the ESSFM Conference (Gerzensee), and the European Finance Association Meetings (Frankfurt)

for helpful comments. We thank Milka Dimitrova and Huasheng Gao for excellent research assistance. Li

acknowledges the financial support from the Social Sciences and Humanities Research Council of Canada. All

remaining errors are our own. † Department of Finance-2-D2-08, Università Bocconi, Via G. Röntgen, 20136 Milano, Italy, (+39) 02.5836.5346,

[email protected]. ‡ Department of Finance-2-D2-02, Università Bocconi, Via G. Röntgen, 20136 Milano, Italy, (+39) 02.5836.5918,

Sauder School of Business, University of British Columbia, 2053 Main Mall, Vancouver, BC V6T 1Z2,

604.822.8353, [email protected].

Debt Specialization

Abstract

This paper provides the first large sample evidence on the patterns and determinants of debt

structure using a new database of publicly listed U.S. firms. Within what is generally referred to

as debt financing, we are able to distinguish between commercial paper, revolving credit

facilities, term loans, senior and subordinated bonds and notes, and capital leases. We first show

that most of the sample firms concentrate their borrowing in only one of these debt instruments,

and only the low growth, low risk large firms with high profitability and the highest level of

leverage borrow through multiple debt instruments. We then show that the extent of debt

specialization is increasing in firm growth opportunities, cash flow risk, and asset maturity, while

decreasing in asset tangibility. Finally, we find that firm characteristics that are known to be

associated with their leverage decisions also affect their usage of different debt instruments. Our

paper suggests that debt structure decisions, like capital structure decisions, are made based on a

cost and benefit analysis to maximize firm value.

Keywords: debt specialization, debt structure, commercial paper, revolving credit facilities, term

loans, senior bonds and notes, subordinate bonds and notes, capital leases

JEL classification: G32

I. Introduction

Much attention has been devoted to the issues of why firms choose between equity and debt, and

how optimal capital structure is designed to minimize the cost of financing (see the survey by

Frank and Goyal (2008) of the voluminous literature on capital structure). In this paper, we focus

on a much less studied topic in capital structure, namely debt structure. Our goals are to explore

the types of debt commonly employed by public U.S. companies, and to relate their usage to the

costs and benefits of different types of debt financing. To our knowledge, our paper is the first to

provide large sample evidence on the subject.

The existing literature suggests a number of important and as of yet unanswered

questions concerning the patterns and determinants of debt structure: How are different types of

debt used in practice to meet corporate funding needs? Do firms tend to specialize in one or two

debt instruments, or do they borrow simultaneously from a variety of sources? How do these

choices vary with firm characteristics, such as their asset maturity structure and their access to

the public bond markets?

To answer these questions, we take advantage of a new database available through

Capital IQ, an affiliate of the Standard and Poor’s, to examine debt structure of publicly listed

U.S. firms.1 Within what is generally referred to as debt financing, we are able to distinguish

between commercial paper, revolving credit facilities, term loans, senior and subordinated bonds

and notes, and capital leases. After merging the Capital IQ database with the Compustat

database, we end up with a large panel data set that comprises 16,115 firm-year observations

involving 3,296 unique firms for the period 2002-2009. In addition to information on debt

structure, the sample also contains leverage and other firm characteristics (e.g., firm size and

profitability).

1 The SEC mandated electronic submission of SEC filings in 1996. Capital IQ has been collecting information about

debt structure since then. The coverage has much improved since 2002 which is the starting point of our sample

period.

2

Our first main finding is that firms specialize in their borrowing: Most sample firms

concentrate their borrowing in only one of the above debt instruments. As primarily an

exploratory exercise, we use cluster analysis to search for patterns of debt structure. We identify

six distinctly different groups of firms: Five of them are predominant users of one single debt

instrument, while only one group relies simultaneously on more than one debt instrument. This

last group is mainly composed of the low growth, low risk large firms with high profitability and

the highest level of leverage. The evidence is suggestive that the average public U.S. firm

specializes in borrowing one type of debt to meet its funding needs.

To further corroborate the above finding, we analyze conditional debt structure. We

require firms to allocate a significant fraction of their debt to a given type of debt, and then

examine the composition of their debt structure under this condition. We find that the majority of

firms rely overwhelmingly on only one type of debt; specifically, the one which we have

conditioned upon. For example, conditioning for firms to have more than 30% of their debt in

term loans, we find that among this subset of firms term loans represent over 70% of their debt.

We show that this result is robust to different specifications of the conditioning threshold.

Second, we find that a key factor for understanding debt structure is credit quality. We

show that debt structure varies substantially between not only rated and unrated firms but also

across firms with different credit ratings: Large and high credit quality firms tend to have access

to different sources of financing, while small and unrated firms rely exclusively on either capital

leases or bank debt for financing. Further, there are some significant non-linear relations between

actual credit ratings and types of debt beyond the usual categorization of firms being rated or not:

For example, the amount of senior bonds and notes is increasing in credit quality, peaks at the

rating of A, and then is decreasing in credit quality as the latter further improves. Faulkender and

Petersen (2006) show that firms that do not have access to the public debt markets, as measured

by not having a debt rating, tend to have lower debt ratios. Our finding highlights that the actual

3

credit rating, a comprehensive measure of firm credit worthiness, affects firm access to different

sources of financing as well.

Third, we analyse the determinants of debt specialization and find that the extent of debt

specialization is decreasing in asset tangibility, while increasing in market-to-book (M/B) ratios,

cash flow volatility, and asset maturity. Interestingly, we also observe that the most recent

financial crisis had a strong impact on firms’ increasing adoption of debt specialization.

Finally, we address the question of how choices of different debt instruments vary with

firm characteristics. We rely on some recent papers in capital structure (see for example, Fama

and French (2002) and Lemmon, Roberts and Zender (2008)) to identify firm characteristics that

are known to be associated with cross-sectional variations in leverage, including profitability,

asset tangibility, M/B ratios, firm size, cash flow volatility, the dividend payer dummy variable,

asset maturity, and firm age. We find that the effects these firm characteristics have on leverage

and on different debt instruments can vary substantially. For example, the previous literature has

established that profitability is negatively and significantly associated with leverage as predicted

by the pecking order theory. Our analysis further shows that this negative association is mainly

driven by three types of debt: senior and subordinated bonds and notes, and capital leases. In

contrast, profitability is positively and significantly associated with commercial paper and

revolving lines of credit. We also show that asset maturity is negatively and significantly

associated with revolving lines of credit and capital leases, while positively and significantly

associated with senior and subordinated bonds and notes. These results indicate that using a

gross measure of leverage such as total debt can be misleading, as it hides heterogeneity across

different debt instruments. The evidence supports our conjecture that debt structure decisions,

like capital structure decisions, are made based on a cost and benefit analysis to maximize firm

value.

Our paper is closely related to and motivated by Rauh and Sufi (2010) who examine

types, sources, and priorities of debt using a sample of 305 randomly selected non-financial rated

4

public firms for the period 1996-2006 (2,453 firm-year observations). They show that almost

three quarters of their firm-year observations employ more than two different debt instruments,

and that a quarter of the sample firms has no significant one-year change in their level of debt but

significant changes in their debt composition. Further, high credit quality firms (BBB and higher)

primarily use two tiers of capital: equity and senior unsecured debt. Low credit quality firms (BB

and lower) tend to use several tiers of debt including secured, senior unsecured, and subordinated

issues.

Our work differs from Rauh and Sufi (2010) in the following aspects. First, our much

larger sample allows us to examine the financing patterns of unrated firms as well—these

represent over 60% of our firm-year observations and 9% of the total assets of our sample firms,

and thus account for an important part of the overall economy. By contrast, Rauh and Sufi’s

sample is limited to rated firms. Second, as a result of our broader sample, we are able to

uncover the phenomenon of debt specialization in firm financing behavior, which is otherwise

unobservable. Indeed, Rauh and Sufi conclude that financing through multiple sources of debt is

the norm among large and rated firms in their sample, which we confirm only among a

subsample of our firms. Moreover, we also show that smaller firms with no or poor credit ratings

borrow through only one type of debt. Finally, we examine the determinants of this debt

specialization phenomenon that we uncover.

The outline of the paper is as follows. Section II reviews the related literature and

develops our hypotheses. Section III describes our data and sample, and provides an overview of

debt structure in our sample firms. Section IV presents evidence on the extent of debt

specialization. Section V provides our explanations for the observed financing pattern. Section

VI carries out various robustness checks on our main results. Finally, Section VII summarizes

our findings and concludes.

II. Literature Review and Hypothesis Development

5

How should firms choose their capital structure? In the ideal world of Modigliani-Miller

(1958, 1963), capital structure choices are irrelevant for firm value and so any choice is optimal.

Starting from Miller (1977), finance researchers have reassessed the ―irrelevance‖ result by

reintroducing various market frictions that make firm value dependent on capital structure

choices. Among these frictions, bankruptcy costs, taxes, agency problems, and information

asymmetries are the most well studied (see Myers (2001) for an excellent review). By trading off

the costs and benefits of debt financing, firms with different characteristics employ different

levels of debt at which firm value is maximized.

Extending the optimal capital structure perspective to debt structure choices, we expect

debt structure to vary across firms with different characteristics that capture different costs and

benefits associated with a particular debt type. Indeed, the existing literature on firms’ usage of

different types of debt shows that debt instrument choices depend on, by and large, the same

factors that affect capital structure choices. In this section we review the literature that suggests

that debt specialization happens from a cost and benefit analysis based on firm heterogeneity.

A. Commercial Paper

Although to our knowledge there is no theoretical work specific to commercial paper,

there is ample empirical evidence identifying firm size and default risk as the main firm

characteristics associated with its usage: Only large firms with strong credit ratings have the

opportunity to access the commercial paper market. Kahl, Shivdasani, and Wang (2008) suggest

that commercial paper represents a state-contingent funding source that partially substitutes the

need for precautionary cash holdings. Gao and Yun (2009) examine the interplay between

precautionary cash holdings and commercial paper during the recent financial crisis. They find

that the aggregate commercial paper borrowing declined 15% after the collapse of Lehman

Brothers, but the effect was concentrated among firms with high default risk. These high default

6

risk firms drew heavily from existing lines of credit to substitute lost borrowing from the

commercial paper market. Using large firm size and old firm age to proxy for low default risk,

our first hypothesis with respect to commercial paper is:

H1: The use of commercial paper is increasing in firm size, age, and credit ratings.

B. Revolving Credit Facilities

The literature on revolving credit examines why firms are granted a credit line and why

they draw down on it. Holmström and Tirole (1998), DeMarzo and Sannikov (2006), and

DeMarzo and Fishman (2010) show that credit lines help reduce the trade-off between inefficient

liquidation and moral hazard. A firm cannot wait to borrow funds after a liquidity shock is

realized. The optimal liquidity policy can be implemented either in terms of precautionary cash

holdings, or in terms of an irrevocable line of credit. Empirically, Jiménez, López, and Saurina

(2008) and Sufi (2009) show that drawdowns on credit lines increase as firm financial conditions

worsen. Ivashina and Scharfstein (2009) further show that drawdowns on existing credit lines

increased drastically during the 2008 financial crisis.

This literature suggests that firms with high agency costs and high cash flow uncertainty

are more in need of a credit line. However, these very firms are also more likely to draw down

on the credit line when their financial conditions worsen. Anticipating this, banks offer a credit

line only to firms with low agency costs and low cash flow uncertainty. Using the M/B ratio to

proxy for agency costs, and cash flow volatility to proxy for cash flow uncertainty, our second

hypothesis with respect to revolving credit facilities is thus:

H2: The use of revolving lines of credit is decreasing in M/B ratios and cash flow volatility.

C. Bank versus Bond Financing

7

There is a large theoretical literature that examines the trade-off between bank versus

bond financing. Diamond (1991) first introduces the idea that the choice between borrowing

directly (through issuing corporate bonds, without monitoring) and borrowing through a bank

where monitoring is primarily driven by the lender’s need to reduce moral hazard. Chemmanur

and Fulghieri (1994) further demonstrate that banks’ desire to acquire a reputation for making

the ―right‖ renegotiation versus liquidation decision provides them incentives to devote a larger

amount of resources than bondholders toward such evaluations. In equilibrium, bank loans

dominate bonds from the point of view of minimizing inefficient liquidation; however, firms

with a lower probability of financial distress choose bonds over bank loans. Along similar lines,

Bolton and Freixas (2000) show that firms turn to banks as a source of financing mainly because

banks are good at helping them through times of financial distress. In equilibrium the riskier

firms prefer bank loans, the safer ones tap the bond markets, and the ones in between issue both

equity and bonds.

The empirical evidence mostly provides support for the above key idea that banks

specialize in lending to firms with higher agency and liquidation costs. Houston and James (1996)

show that reliance on bank borrowing is decreasing in firm size, growth opportunities, leverage,

and the firm’s access to public debt markets. Johnson (1997) finds that firms use more public

debt if they have lower information and monitoring costs, lower likelihood and costs of

inefficient liquidation, and weaker incentives to harm the lenders. Hadlock and James (2002)

show that firms are more likely to choose bank loans when asymmetric information problems are

elevated. Cantillo and Wright (2000) find that large companies with abundant cash and collateral

tap credit markets directly; and these markets cater to safe and profitable industries.

In summary, the prior literature suggests that firms with lower monitoring needs and

better fundamentals prefer public debt to bank financing. We expect monitoring needs to be

lower for firms with larger size, higher asset tangibility, higher growth opportunities, and higher

8

credit ratings. Hence our third hypothesis with respect to the choice between bank debt and

public debt is:

H3: The use of bank debt is decreasing in asset tangibility, M/B ratios, firm size, and credit

ratings; while the use of public debt is increasing in asset tangibility, M/B ratios, firm size, and

credit ratings.

D. Capital Leases

The final strand of literature examines leases and shows that the use of leases induces a

trade-off between lower liquidation costs and higher agency costs. Eisfeldt and Rampini (2010)

show that there are two mechanisms at work in a lease: 1) leasing allows the lessor (owner) to

repossess the asset when the lessee files for bankruptcy, which gives the lessor a stronger claim

than that of secured lenders; 2) leasing entails agency costs, as the lessee retains control while

the lessor keeps ownership (separation of ownership and control). They predict that firms that are

financially constrained prefer to lease an asset, while firms that are less constrained prefer to own

the asset. Krishnan and Moyer (1994) document that lessee firms have low retained earnings,

high growth rates, low coverage ratios, and in general a high bankruptcy risk. Yan (2006) further

shows that leases and debt are substitutes and that in those firms with more growth options or

larger marginal tax rates, or in those firms paying no dividends, the substitutability is more

pronounced.

In summary, the existing theory and evidence on capital leases suggest that financially

constrained firms with high growth and high risk are the best candidates for borrowing through

leases, and hence our final hypothesis with respect to capital leases is:

H4: The use of capital leases is decreasing in profitability, dividend payout, and credit ratings,

while increasing in M/B ratios and cash flow volatility.

9

III. Data Overview

A. Sample Description

We start with U.S. firms traded on AMEX, NASDAQ, and NYSE covered by both

Capital IQ (CIQ) and Compustat from 2002 to 2009. CIQ compiles detailed information on

capital structure and debt structure by going through financial footnotes contained in firms’ 10K

SEC filings.2 We remove utilities (SIC codes 4900-4949) and financials firms (SIC codes 6000-

6999) and end up with 27,802 firm-year observations. We further remove 1) firm-years with

missing value of total assets (26,729 observations remaining); 2) firm-years with zero total debt

(19,142 observations remaining); 3) firm-years with market or book leverage outside the unit

interval (as in Lemmon, Roberts and Zender (2008), 17,572 observations remaining); and 4)

firm-years for which the difference between total debt as reported in Compustat and the sum of

debt types as reported in CIQ exceeds 10% of total debt. Our final sample has 16,115 firm-year

observations involving 3,296 unique firms.

In constructing our variables we use the same definitions as in Lemmon, Roberts and

Zender (2008). Table A1 in the Appendix provides a detailed description of the variables used in

our analysis. Total assets are expressed in millions of 2002 U.S. dollars.

Table 1 presents descriptive statistics. Columns (1) and (2) report means and medians of

the key firm characteristics aggregated across all years for our sample firms. Columns (3) and (4)

present means and medians of the same key firm characteristics for the Compustat leveraged

firms, i.e., firms with positive debt. This Compustat sample is formed by imposing similar filters

as to our sample except filter 4) above. Our sample covers approximately 90% of the Compustat

leveraged firms. Columns (5) and (6) test whether our sample is different from the Compustat

leveraged firms.

2 Regulation S-X requires firms to detail their long-term debt instruments. Regulation S-K requires firms to discuss

their liquidity, capital resources, and operating results. As a result of these regulations, firms detail their long-term

debt issues and bank revolving credit facilities. Firms often also provide information on notes payable within a year

(Rauh and Sufi (2010)).

10

We show that over the sample period 2002-2009, the mean (median) market leverage as

measured by the ratio of total debt to the sum of total debt and market value of equity is 0.252

(0.195). Using a sample of non-financial, non-utility firms from Compustat over the period 1986-

2000, Faulkender and Petersen (2006) report that the mean (median) market leverage is 0.222

(0.183) for leveraged firms. In comparison to the Compustat leveraged firm sample, our sample

firms are not significantly different in most dimensions compared except dividend payout

(although the economic significance of this difference is small). We conclude that our sample is

representative of the Compustat leveraged firms.

B. Debt Structure Overview

CIQ decomposes total debt into seven mutually exclusive debt types: commercial paper

(CP), drawn revolving credit facilities (RC), term loans (TL), senior bonds and notes (SBN),

subordinated bonds and notes (SUB), capital leases (CL),3 and other debt (Other).

4 Table A2 in

the Appendix provides an example illustrating how CIQ collects and constructs the various debt

types. Table 2 provides detailed summary statistics for debt types (normalized by total debt).

Panel A of Table 2 shows that first, the majority of sample firms rely on senior bonds and

notes for financing. The sample mean (median) ratio of senior bonds and notes to total debt (TD)

is 0.382 (0.208). Second, the median ratios of both revolving credit and term loans to total debt

are close to zero or zero, while the 75th

percentiles are much greater than zero; suggesting that

between a quarter and half of the sample firms rely on revolving credit facilities or term loans,

both provided by banks. When adding up both debt instruments to obtain total bank debt, we find

3 Capital leases are different from operating leases. While in an operating lease, lease expenses are treated as an

operating cost, a capital lease is recognized both as an asset and as a liability on the balance sheet, and is thus

subject to depreciation. Typically, firms prefer to keep leases off the books and defer expenses, which gives them

the incentive to report all leases as operating leases. As a result, the Financial Accounting Standards Board has ruled

the conditions under which a lease should be reported as a capital lease. Though often disregarded in the existing

literature, the distinction between capital and operating leases is important for our purposes. In our analysis of debt

we will only consider capital leases, as operating leases are not reported as debt on the balance sheet. 4 Other debt mostly consists of short-term borrowings. Occasionally, it takes other forms such as deferred credits,

fair value adjustments related to hedging contracts, or trust-preferred securities.

11

that more than half of the sample firms employ bank debt, with the sample mean (median) at

0.431 (0.322) (untabulated). Third, more than a quarter of the sample firms employ capital

leases, even though they are much less important on average than bank debt. The sample mean

ratio of capital leases to total debt is 0.054, while that of revolving credit (term loans) is 0.220

(0.212). Fourth, less than a quarter of the sample firms use subordinated bonds and notes. Lastly,

the 90th

percentile of commercial paper is zero (untabulated), suggesting that less than 10% of

the sample firms use commercial paper for financing.

Total adjustment is the difference between the total debt variable obtained from

Compustat and the sum of seven debt instruments from CIQ. When forming our sample, we have

imposed the filter that the total adjustment for firms in the sample be less than 10% of total debt.

After applying this filter, there is little discrepancy between the sum of debt instruments from

CIQ and total debt from Compustat: Both the mean and median ratios of total adjustment to total

debt are zero, and the 1st and 99

th percentiles are -0.029 and 0.038, respectively. These statistics,

together with our sample’s broad coverage of the Compustat leveraged firms, are reassuring

about the CIQ’s data quality.

To capture the extent of firms’ concentrated use of different debt instruments, for firm i

in year t we first compute the sum of the squared ratios of seven debt instruments to total debt

outstanding:

2

t,i

t,i

2

t,i

t,i

2

t,i

t,i

2

t,i

t,i

2

t,i

t,i

2

t,i

t,i

2

t,i

t,i

t,i

TD

Other

TD

CL

TD

SUB

TD

SBN

TD

TL

TD

RC

TD

CPSS

(1)

We then normalize SS to get the normalized Herfindahl-Hirschman Index (henceforth simply

referred to as HHI):

711

71SS

HHIt,i

t,i

(2)

12

Thus, a firm that employs exclusively one single debt instrument has HHI equals one, while HHI

equals zero for a firm that simultaneously employs all seven debt instruments in equal

proportions. Higher HHI values indicate firms’ tendency to specialize in fewer debt instruments.

Complementary to HHI, we also compute another specialization measure, the Shannon

Entropy (henceforth referred to as Entropy):

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

t,i

TD

Otherln

TD

Other

TD

CLln

TD

CL

TD

SUBln

TD

SUB

TD

SBNln

TD

SBN

TD

TLln

TD

TL

TD

RCln

TD

RC

TD

CPln

TD

CPEnt

(3)

This ranges from zero (for firms specialized in borrowing through one debt instrument for all

their financing needs) to ln(7) 1.946 (for firms diversified in borrowing across all seven debt

instruments in equal proportions).

Table 2 Panel A shows that the mean (median) HHI is 0.702 (0.729) while for Entropy

the mean (median) is 0.434 (0.426). Moreover, about one fourth of our sample firms have HHI

values close to unity (or equivalently Entropy values close to zero), suggesting that firms have a

great tendency to specialize in one debt instrument.

Table 2 Panel B presents the time series evidence on debt types as well as our two

specialization measures. We find that firms appear to rely more on bank financing (both

revolving credit and term loans) and less on commercial paper, subordinated bonds and notes,

and capital leases over the sample period. Their use of senior bonds and notes and other debt has

been stable over time. Furthermore, there is a moderate increase in the degree of debt

specialization over time: the mean HHI (Entropy) is 0.676 (0.476) in 2002 and increases

(decreases) to 0.719 (0.407) in 2009. The observed temporal variation motivates our introduction

of year fixed effects in our multivariate analysis later.

In summary, although there are many different debt instruments, for our sample of firms,

senior bonds and notes are the most commonly employed debt instrument, followed by revolving

13

credit and term loans. Moreover, many sample firms tend to rely heavily on only one debt

instrument for meeting their financing needs. In the rest of the paper, we provide a more detailed

investigation of the patterns and determinants of debt structure.

C. Credit Ratings and Debt Structure

The literature has previously examined the relation between credit ratings and leverage.

Diamond (1991), Chemmanur and Fulghieri (1994), and Bolton and Freixas (2000) have shown

that credit quality is the primary source of variation driving a firm’s optimal choices of different

types of debt. Faulkender and Petersen (2006) examine the role of the source of capital in firms’

financing decisions, and show that firms with access to public bond markets (as measured by

being rated) have substantially more debt. Kisgen (2006) finds that firm credit ratings affect

capital structure decisions: Firms near a credit rating upgrade or downgrade issue less debt.

Lemmon and Zender (2009) use the likelihood of being rated as a proxy for debt capacity and

show that after accounting for debt capacity, the pecking order appears to be a good description

of a firm’s financing behavior. Rauh and Sufi (2010) document that high credit quality firms

(BBB and higher) rely almost exclusively on two tiers of capital—equity and senior unsecured

debt—while lower credit quality firms (BB and lower) use multiple tiers of debt including

secured, senior unsecured, and subordinated issues.

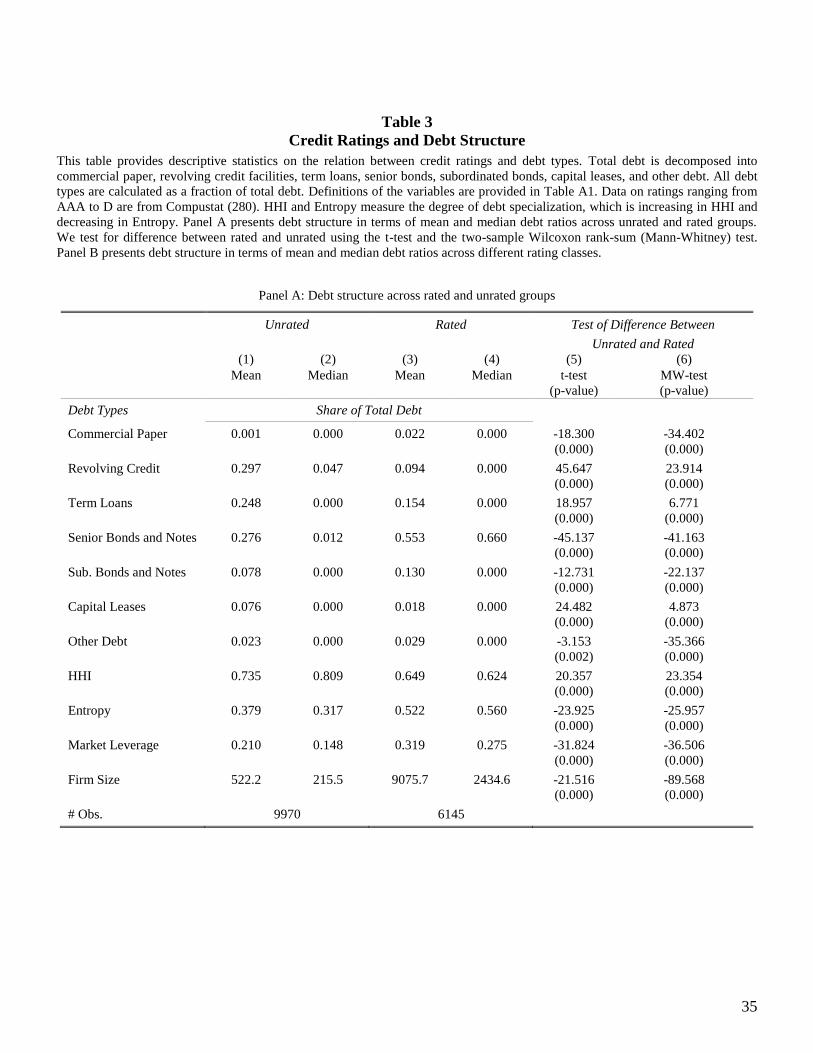

Motivated by this prior body of work, Table 3 presents an overview of the relation

between credit ratings and debt structure. We consider a firm-year to be rated if the firm has at

least one monthly Standard & Poor’s long-term issuer rating, as recorded in Compustat (data

item 280). About 40% of our firm-year observations are unrated. In untabulated analysis, we find

that there is little temporal variation in the fraction of firms being rated over time.5

5 Using Compustat firms over the period 1986-2000, Faulkender and Petersen (2006) show that only 19% (21%) of

firms (with positive debt) have debt ratings. They conclude that public debt is uncommon. In unreported analysis,

we find that rated firms in our sample are larger (both in terms of sales and book value of assets), and have a higher

book leverage ratio than those in Faulkender and Petersen (2006). This is consistent with Lemmon and Zender’s

14

Panel A of Table 3 presents differences in the use of various debt types between unrated

and rated firms in our sample. We show that revolving credit facilities and term loans together,

on average, account for more than half of unrated firms’ total debt, while senior bonds and notes

account for slightly less than 25% of their total debt. Rated firms are much heavier users of

senior and subordinated bonds and notes. Unrated firms are much heavier users of capital leases.

Further, we show that unrated firms are more specialized in borrowing than rated firms, as

captured by both the HHI and Entropy measures. At the bottom of Panel A, we also present

sample mean (median) market leverage of unrated and rated firms. Consistent with Faulkender

and Petersen (2006), we show that unrated firms—with a mean (median) market leverage ratio of

0.210 (0.148)—tend to employ less debt than rated firms—who have a mean (median) market

leverage ratio of 0.319 (0.275). Overall, unrated firms use significantly less commercial paper as

well as senior and subordinated bonds and notes; and significantly more revolving credit, term

loans, and capital leases than their rated counterparts—suggesting that both banks and lessors

have a comparative advantage in dealing with information asymmetry and moral hazard

associated with unrated firms (Diamond (1991), Chemmanur and Fulghieri (1994), and Eisfeldt

and Rampini (2010)).

To further examine the relation between actual credit ratings and debt structure, we first

assign to each monthly S&P letter rating class an integer number ranging from 1 (AAA) to 22

(D). Then, for each rated firm-year we round the average monthly numeric rating class to the

nearest integer, and refer to it as the firm rating in a given year. We find that about 6% of our

firm-years have a credit rating of A and higher, while close to 16% of our sample firms have

investment grade ratings (equal to or higher than BBB-, untabulated).6

(2009) finding that large firms with high leverage are more likely to be rated. Focusing on 305 randomly chosen

Compustat firms with a long-term issuer rating in at least one year from 1996-2006, Rauh and Sufi (2010) show that

three-quarters of their firm-year observations are rated. 6 Using Compustat firms from 1986-2001, Kisgen (2006) shows that 44.2% of his sample firms have a credit rating

of A and higher, and 69.1% of his sample have investment grade ratings. Rauh and Sufi (2010) report 21.7% of their

firms have a credit rating of A and higher, and close to half have investment grade ratings. The difference in rating

15

Panel B of Table 3 provides an overview of differences in the usage of various debt types

(as a share of total debt) across a broad rating spectrum. We first show that commercial paper is

used almost exclusively by investment grade firms, especially AAA- and AA-rated firms.

Second, term loans and subordinated bonds and notes are most heavily used by speculative grade

(equal to or lower than BB-) firms. Third, we document a non-linear relation between credit

quality and the amount of senior bonds and notes used by our sample firms: The amount of

senior bonds is increasing in credit quality, peaks at the rating of A, and then is decreasing in

credit quality. Finally, we find that firms belonging to lower rating classes are characterized by

higher values of HHI (and lower values of Entropy), suggesting that the extent of debt

specialization is decreasing in credit quality.

We conclude that credit quality affects both the composition of debt structure and the

extent of debt specialization. Later in our multivariate analyses, we will include dummy

variables for each different rating class and for firms being unrated to control for the complex

relation between credit ratings and debt structure.7

D. Industries and Debt Structure

Table 4 presents an overview of the relation between two-digit SIC codes and debt

structure and debt specialization measures. The top three most represented industries are

Chemicals and Allied Products (10.45%), Business Services (9.80%), and Electronic Equipment

(8.17%). These three industrial sectors exhibit similar levels of specialization, as captured by

both the HHI and Entropy measures. The three industries with the highest level of debt

specialization are: Legal Services, Furniture and Home Furnishings, and Apparel and Accessory

Stores. The three industries with the lowest level of debt specialization are: Local Passenger

distributions between the Kisgen’s sample and our sample is probably due to the fact that his sample includes

financials and utilities which tend to have better ratings than industrial firms. 7 We assign an integer equal to 23 to the variable ―Rating‖ for an unrated firm-year observation.

16

Transit, Auto Repair and Services, and Electric, Gas, and Sanitary Services. Overall, Table 4

shows significant variation in debt structure and debt specialization across different industries,

which motivates the inclusion of industry dummies in our multivariate analyses later.

IV. Debt Specialization

In this section, we present comprehensive evidence on the extent of debt specialization in

our sample firms.

A. Cluster Analysis

Our first piece of evidence on debt specialization comes from cluster analysis, which is

commonly used to discover unknown structures in data by maximizing variance (in terms of the

Euclidean distance) between clusters and minimizing it within clusters. Once we separate data in

clusters, we effectively remove much of the variance in any of the debt types. Table 5 presents

the mean and median values for different debt types and key firm characteristics across the

identified clusters using firm-year observations, sorted according to ascending group mean firm

size.8 Figure 1 presents the distribution of different debt types within each cluster (mean ratios

are used).

There are a total of six clusters for our sample firms. Across these six clusters, the extent

of debt specialization as captured by the HHI and Entropy measures are fairly similar across the

first five clusters, while it decreases drastically for cluster 6 which includes the largest firms in

the sample. More specifically, cluster 1 includes the smallest firms in our sample with market

leverage close to the sample average. These firms tend to use predominantly revolving lines of

credit for financing. The group mean (median) revolving lines of credit to total debt ratio is 0.84

8 Firm characteristics are measured contemporaneously. Using lagged measures gives qualitatively the same results

except that sample size is slightly smaller.

17

(0.90). Cluster 2 includes the second smallest firms in our sample with the lowest level of market

leverage. These firms tend to use predominantly capital leases for financing. The group mean

(median) capital leases to total debt ratio is 0.88 (1.00). Cluster 3 firms tend to use

predominantly term loans for financing. The group mean (median) term loans to total debt ratio

is 0.82 (0.88). Cluster 4 firms tend to use predominantly subordinated bonds and notes for

financing. The group mean (median) subordinated bonds and notes to total debt ratio is 0.79

(0.83). Firms in cluster 5 are considerably bigger and these firms tend to use predominantly

senior bonds and notes for financing. The group mean (median) senior bonds and notes to total

debt ratio is 0.91 (0.95). Finally, cluster 6 includes some of the largest firms in the sample. These

firms tend to use a mix of senior bonds and notes, revolving credit, and term loans. The group

mean (median) senior notes and bonds, revolving credit, and term loans to total debt ratio is 0.48

(0.52), 0.17 (0.10), and 0.14 (0.02), respectively. It is worth noting that this group of firms has

the lowest M/B ratios and cash flow volatility, and the highest level of market leverage among

the sample firms.

In summary, the evidence from cluster analysis suggests that the vast number of sample

firms specialize in borrowing from one type of debt, and only the largest and least risky firms

simultaneously employ multiple types of debt. Moreover, we do not observe asset maturity to

vary considerably across clusters, which suggests that debt specialization cannot be the mere by-

product of firms matching the maturity of their liabilities to that of their assets. Our evidence

thus far is consistent with the prior theoretical literature suggesting that the use of different types

of debt is determined by firm characteristics including their credit quality and ability to access

the public debt market, and within a large sample of firms like ours, there would be some level of

debt specialization based on firms’ costs and benefits analysis. What is striking in our findings is

that debt specialization seems to be a dominant phenomenon.

Our findings on debt specialization are in stark contrast to Rauh and Sufi (2010), who

show that their average sample firm simultaneously employs multiple types of debt. We attribute

18

the difference in findings to the different samples examined in their paper and ours. They focus

primarily on large and rated firms, while in our sample only about 40% of the firms are rated.

B. Conditional Debt Structure

Our second piece of evidence on debt specialization comes from examining conditional

debt structures. Table 6 Panel A presents the shares of firm-year observations conditional on a

particular debt type exceeding 30% of total debt (i.e., the significant user). Looking across the

rows in Panel A, we find that significant users of one debt type are rarely significant users of any

other debt types. This is true with the exception of the significant users of commercial paper

which simultaneously employ a significant amount of senior bonds and notes. In all other cases,

Panel A indicates that if a firm’s use of a particular type of debt exceeds 30% of its total debt,

that type is likely to be its only source of debt financing. These results provide further support for

the phenomenon that firms specialize in borrowing from one type of debt. If firms were

simultaneously employing multiple types of debt, we would have observed few firms exceeding

30% of their debt from a single source of financing.

Panel B presents both the mean and median ratios of each debt type to total debt

conditional on a particular debt type exceeding 30% of total debt. Specifically, we first impose

the condition that a firm’s use of a particular debt type exceeds 30% of its debt, thus identifying

a subset of firms. Then, for this subset we compute mean and median ratios of all debt types to

total debt and test the null hypothesis that the mean (median) ratio is no greater than 30%. We

also report the number of firm-year observations whose particular debt type is strictly greater

than 30% of total debt. For example, in the first row we require that the amount of commercial

paper exceeds 30% of debt. This leaves us with 142 observations. For these observations the

mean (median) ratio of commercial paper to total debt is 0.528 (0.468), the mean (median) ratio

of revolving credit to total debt is 0.038 (0.000), and so on for all other types.

19

Examining the numbers in bold face along the diagonal line of Panel B, we show that the

ratio of a given debt type to total debt is between 65% and 80%, conditional on the ratio of that

particular type of debt to total debt exceeding the threshold of 30% (again with the notable

exception of the significant users of commercial paper). Further, the t- and median tests strongly

reject the null that the mean and median ratios of various debt types are no greater than 30%. The

off-diagonal numbers reveal that any significant reliance on more than one debt type is rarely

observed: The exception is that the significant users of commercial paper are also significant

users of senior bonds. The results in Panel B highlight the general phenomenon that very few

firms use other sources of debt over and beyond the one which we condition upon. This is strong

evidence of firms relying primarily on a single debt instrument.

Figure 2 presents the distribution of different debt types conditional on a particular debt

type exceeding 30% of total debt. With the exception of the significant users of commercial

paper, we observe the conditional mean ratio of various debt types easily exceeding 70% (as

shown along the vertical axis).

We conclude that specialization—not diversity—in types of debt is the dominant

phenomenon for debt structure. The natural question to ask next is what drives debt

specialization.

V. Explaining Debt Specialization and Debt Structure

The vast literature on capital structure has shown that the optimal capital structure

decision is made based on the trade-off between costs and benefits of debt financing. Extending

this line of thinking, we expect that the extent of debt specialization is also driven by firm

characteristics that proxy for costs and benefits of debt specialization.

A. Determinants of Debt Specialization

20

Since we are the first to examine the determinants of debt specialization, we rely on prior

work in capital structure to decide on possible explanatory variables (see for example, Fama and

French (2002), Lemmon, Roberts and Zender (2008), and Frank and Goyal (2008)). We estimate

the following regression:

t,i

t,iAt,iM

t,iDt,iVt,iS

t,iMBt,iTt,iPt,i

FERatingFEIndustryFEYear

AgeFirmMaturityAsset

PayerDividendVolatilityCFSizeFirm

B/MyTangibilitityProfitabiltionSpecializaDebt

1

111

111

(4)

where the dependent variables are the two measures of the extent of debt specialization: HHI and

Entropy. Table 7 Columns (1) and (3) present the OLS regression results.

For both specialization measures, we show that asset tangibility is negatively and

significantly, while M/B ratios, cash flow volatility, and asset maturity are positively and

significantly, associated with the extent of debt specialization. Our findings suggest that when

there are low monitoring costs as captured by high asset tangibility, firms are able to borrow

from a variety of different sources of financing; leading to reduced reliance on a few debt

instruments. On the other hand, when there are severe information asymmetry and high default

risk as captured by high growth and high cash flow risk, firms are forced to concentrate their

borrowing to fewer different sources of financing such as public debt or capital leases (see our

hypotheses H3 and H4). The positive and significant association between asset maturity and debt

specialization is mostly driven by senior bonds and notes, which is shown to be the predominant

source of financing (Table 2 Panel A) and positively associated with asset maturity (Table 5, see

cluster 5). Interestingly, we also show that in the midst of the 2008 financial crisis, firms

scrambled to borrow from as many sources of financing as possible; leading to a significant

decline in the degree of debt specialization, consistent with the evidence reported in Ivashina and

Scharfstein (2009) and Gao and Yun (2009). Afterwards, the degree of debt specialization

reverts back.

21

To get a sense of the extent to which firm characteristics affect the degree of debt

specialization, we consider four alternative specifications of Equation (4) by separately including

firm characteristics, year, industry, or rating fixed effects. Table 7 Columns (2) and (4) present

the OLS regression results when including firm characteristics only, while the lower part in

Table 7 reports the adjusted R2 for the different fixed effects specifications. The effects of firm

characteristics on debt specialization are fairly similar whether the different fixed effects are

included or not. When considering firm characteristics only, large firms appear to be less

specialized, but this effect is not robust to the inclusion of various fixed effects.

The full model specification in Equation (4) achieves an adjusted R2 of 0.084 and 0.099

for HHI and Entropy, respectively, while the goodness-of-fit of a model with firm characteristics

only is about 50% lower. Industry and rating fixed effects contribute similar levels of

explanatory power achieving an adjusted R2 in the range of 0.32 to 0.45, while year fixed effects

alone are not overall effective in explaining debt specialization. All fixed effects together

account for about three-quarters of the total explanatory power achieved by the full model

specification in Equation (4).

In summary, consistent with the theoretical predictions on the relation between the use of

different debt types and firm characteristics reviewed in Section II, we show that the extent of

debt specialization is also driven by concerns of information asymmetry and agency problems.

B. Determinants of Debt Structure

To examine the determinants of debt structure, we estimate the following regression

model:

t,i

t,iAt,iM

t,iDt,iVt,iS

t,iMBt,iTt,iPt,i

FERatingFEIndustryFEYear

AgeFirmMaturityAsset

PayerDividendVolatilityCFSizeFirm

B/MyTangibilitityProfitabilTypeDebt

1

111

111

(5)

22

where the dependent variables—debt types—are calculated as a fraction of total debt. As we

have shown in Table 2 Panel A, the distribution of debt types has a ―mass point‖ of observations

at zero for over half of the firm-year observations when a particular debt type is not employed,

which may raise some concerns about the conditional normality of the dependent variable in

Equation (5). As a result, we estimate Equation (5) with a Tobit specification that accounts for

two-sided censoring of the dependent variables at zero and one, and present results in Table 8.9

We show that firm size and age is positively and significantly associated with the use of

commercial paper, consistent with our first hypothesis (H1). Moreover, we show that

profitability, tangibility, M/B ratios, and the dividend payer dummy are positively and

significantly associated with the usage of commercial paper (Column (1)). Given that

profitability and tangibility are important determinants of credit ratings and that dividend

payments may signal profitability, the evidence further corroborates our first hypothesis.

We show that M/B ratios and cash flow volatility are negatively and significantly

associated with revolving credit facilities, consistent with our second hypothesis (H2). Outside

the predictions of our second hypothesis, we also show that profitability, asset tangibility, and

the dividend payer dummy are positively and significantly, while firm size and asset maturity are

negatively and significantly, associated with revolving credit facilities (Column (2)). The former

is consistent with banks’ close monitoring of line of credit drawdowns (Jiménez, López, and

Saurina (2008) and Sufi (2009))—they only provide credit lines to firms that are sufficiently

profitable, i.e., paying dividends. The latter is also intuitive as small firms tend to have more

volatile cash flows leading to lower usage of revolving credit; and as revolving credit facilities

9 In untabulated analysis, we first establish a benchmark by regressing market leverage on the same set of firm

characteristics. We find that consistent with prior research such as Frank and Goyal (2008) and Lemmon, Roberts,

and Zender (2008), profitability, M/B, cash flow volatility, and the dividend payer dummy are negatively and

significantly associated with market leverage; while asset tangibility and firm size are positively and significantly

associated with market leverage.

23

tend to have short maturity, they are expected to be matched with firms with shorter asset

maturity (Stohs and Mauer (1996)).

Columns (3)–(5) present evidence on the choice between bank loans and publicly traded

debt. We show that M/B ratios, firm size, cash flow volatility, and firm age are negatively and

significantly associated with term loans; mostly in support of the first half of our third hypothesis

(H3). Our evidence is consistent with the prior literature suggesting that firms with higher

monitoring costs prefer bank debt to public debt (Diamond (1991) for example). The exception is

that asset tangibility, which reduces the monitoring needs of a lender, is shown to be positively

and significantly associated with term loans. On the other hand, this finding is consistent with

banks’ risk aversion and their common practice of secured lending (Column (3)).

We further show that M/B ratios as well as firm size and age are positively and

significantly associated with senior bonds and notes, mostly consistent with the second half of

our third hypothesis (H3). Our evidence supports the predictions from prior literature that firms

with lower monitoring costs borrow from the public debt market (Chemmanur and Fulghieri

(1994) for example). Outside the predictions of our third hypothesis, we show that cash flow

volatility, the dividend payer dummy, and asset maturity are positively and significantly, while

profitability is negatively and significantly, associated with senior bonds and notes (Column (4)).

In contrast to senior bonds and notes, we show that asset tangibility, M/B ratios, and the dividend

payer dummy are negatively and significantly, while firm size is not significantly, associated

with subordinated bonds and notes. These findings support the idea that subordinated bonds and

notes are likely to be unsecured and made to firms of inferior quality, while term loans and

senior bonds and notes are generally secured. Our results suggest that it is important to separately

examine the determinants of senior versus subordinated bonds and notes as they appear to be

driven by different firm fundamentals.

Column (6) shows that profitability, the dividend payer dummy, and asset maturity are

negatively and significantly associated with capital leases; mostly consistent with our fourth and

24

final hypothesis (H4). M/B ratios or cash flow volatility are not shown to be significantly

associated with capital leases. The positive association between asset tangibility and capital

leases is by construction: capital leases are secured lending. Our evidence confirms the important

trade-off between lower liquidation costs and higher agency costs in capital leases which leads to

only financially constrained firms preferring to lease an asset (Eisfeldt and Rampini (2010)).

Overall, our regression results using different debt instruments as the dependent variables

are in support of our hypotheses. We conclude that low growth, low risk, small and young firms

with tangible assets tend to borrow primarily from banks. Less profitable, high risk, large firms

with long maturity assets use mainly bond financing. More profitable, low risk, large and old

firms with tangible assets use commercial paper. Our results highlight that similar to capital

structure decisions, firms make a tradeoff between the benefits and costs of using different debt

instruments and end up with an optimal debt structure at which firm value is maximized.

VI. Robustness Checks

In this section, we implement various robustness checks on our main results. First, to

mitigate the fact that in our unbalanced panel some firms with complete time series observations

from 2002 to 2009 receive more weight than other firms with fewer observations, we implement

the cluster analysis by using the time series average of each debt type and hence the firm-level

observations. Table 9 Panel A presents the result. We still observe six distinct clusters of firms

with five of them engaged in debt specialization, even though the degree of specialization is

somehow weakened based on the firm-level observations as compared to that based on the firm-

year observations in Table 5. This drop in the degree of specialization is expected if debt

specialization tends to persist over time in the same way that capital structure does (documented

by Lemmon, Roberts, and Zender (2008)), while the time series averaging (as reported in Panel

A) ignores the temporal persistence in debt specialization.

25

Second, we also re-examine conditional debt structures and show that our results are

robust to a different threshold. In Panels B and C we use 10% as the threshold. For example, in

the first row of the table, we require firm-year observations with the ratio of commercial paper to

total debt exceeding 10%. We find that the patterns of specialization in borrowing are

qualitatively similar to what we observe in Table 6 Panels A and B where we use 30% as the

threshold.

Finally, in order to assess the importance of firm characteristics relative to various fixed

effects in explaining debt type choices, we consider four alternative specifications of Equation

(5) by separately including firm characteristics, year, industry, or rating fixed effects. Results

from a Tobit specification are presented in Panel D. The economic and statistical significance of

firm characteristics is overall robust to the inclusion of different fixed effects. The goodness-of-

fit of a specification including firm characteristics only is about 50% of the full specification.

Industry fixed effects are important determinants of the capital leases choice, while rating fixed

effects are mostly relevant in explaining the use of commercial paper and subordinated bonds

and notes.

VII. Conclusions

This paper provides a comprehensive analysis of the patterns and determinants of debt

structure. We first show that debt structure varies substantially between unrated and rated firms

and across a wide spectrum of credit ratings and industry classifications. We then present fresh

evidence on firms’ specialization in borrowing. Cluster analysis identifies six distinct groups of

firms, five of which concentrate their borrowing through one type of debt. Conditional on

borrowing a significant fraction of their debt through a particular type of debt instrument, firms

are found to specialize in borrowing by limiting themselves to a few debt instruments. We find

that debt specialization is decreasing in asset tangibility, increasing in M/B ratios, cash flow

26

volatility, and asset maturity. We further show that debt structure is driven by the same common

factors that are known to explain capital structure, such as profitability, growth opportunities,

and credit ratings; though these factors tend to have very different influences on different types

of debt, consistent with different lenders’ expertise in dealing with information asymmetry and

agency problems. We conclude that debt structure plays an important role in capital structure

decisions.

27

References:

Bolton, Patrick, and Xavier Freixas, 2000, Equity, bonds and bank debt: Capital structure and

financial market equilibrium under asymmetric information, Journal of Political Economy

108, 324-351.

Cantillo, Miguel, and Julian Wright, 2000, How do firms choose their lenders? An empirical

investigation, Review of Financial Studies 13, 155-189.

Chemmanur, Thomas, and Paolo Fulghieri, 1994, Reputation, renegotiation, and the choice

between bank loans and publicly traded debt, Review of Financial Studies 7, 475-506.

DeMarzo, Peter M., and Michael J. Fishman, 2007, Optimal long-term financial contracting,

Review of Financial Studies 20, 2079-2128.

DeMarzo, Peter M., and Yuliy Sannikov, 2006, Optimal security design and dynamic capital

structure in a continuous-time agency model, Journal of Finance 61, 2681-2724.

Diamond, Douglas, 1991, Monitoring and reputation: The choice between bank loans and directly

placed debt, Journal of Political Economy 99, 689-721.

Eisfeldt, Andrea L. and Rampini, Adriano A., 2009. Leasing, ability to repossess, and debt

capacity, Review of Financial Studies 22, 1621-1657.

Fama, Eugene F., and Kenneth R. French, 2002, Testing trade-off and pecking order predictions

about dividends and debt, Review of Financial Studies 15, 1-33.

Faulkender, Michael, and Mitchell Petersen, 2006, Does the source of capital affect capital

structure? Review of Financial Studies 19, 45-79.

Frank, Murray Z., and Vidhan Goyal, 2008, ―Tradeoff and pecking order theories of debt,‖ in:

Handbook of Corporate Finance: Empirical Corporate Finance Vol. II (Elsevier/North-

Holland), ed. B. E. Eckbo.

Gao, Pengjie, and Hayong Yun, 2009, Commercial paper, lines of credit, and the real effects of

the Financial Crisis of 2008: Firm-level evidence from the manufacturing industry,

University of Notre Dame Working Paper.

Hadlock, Charles, and Christopher James, 2002, Do banks provide financial slack? Journal of

Finance 57, 1383-1419.

Holmström, Bengt, and Jean Tirole, 1998, Private and public supply of liquidity, Journal of

Political Economy 106, 1-40.

Houston, Joel, and Christopher James, 1996, Bank information monopolies and the mix of private

and public debt claims, Journal of Finance 51, 1863-1889.

28

Ivashina, Victoria, and David S. Scharfstein, 2009, Bank lending during the Financial Crisis of

2008, Harvard Business School Working Paper.

Jiménez, Gabriel, José A. López, and Jesús Saurina, 2009, Empirical analysis of corporate credit

lines, Review of Financial Studies 22, 5069-5098.

Johnson, Shane, 1997, An empirical analysis of the determinants of corporate debt ownership

structure, Journal of Financial and Quantitative Analysis 32, 47-69.

Kahl, Matthias, Anil Shivdasani, and Yihui Wang, 2008, Do firms use commercial paper to

enhance financial flexibility? University of North Carolina Working Paper.

Kisgen, Darren, 2006, Credit ratings and capital structure, Journal of Finance 61, 1035-1072.

Krishnan, V. Sivarama, and R. Charles Moyer, 1994, Bankruptcy costs and the financial leasing

decision, Financial Management 23, 31-42.

Lemmon, Michael, Michael R. Roberts, and Jamie Zender, 2008, Back to the beginning:

Persistence and the cross-section of corporate capital structure, Journal of Finance 63,

1575-1608.

Lemmon, Michael, and Jamie Zender, 2009, Debt capacity and tests of capital structure theories,

Journal of Financial and Quantitative Analysis forthcoming.

Miller, Merton H., 1977, Debt and taxes, Journal of Finance 32, 261-276.

Modigliani, Franco, and Merton H. Miller, 1958, The cost of capital, corporate finance, and the

theory of investment, American Economic Review 48, 261-297.

Modigliani, Franco, and Merton H. Miller, 1963, Corporate income taxes and the cost of capital:

A correction, American Economic Review 53, 443-453.

Myers, Stewart C., 2001, Capital structure, Journal of Economic Perspectives 15, 81-102.

Rauh, Joshua D., and Amir Sufi, 2010, Capital structure and debt structure, Review of Financial

Studies forthcoming.

Stohs, Mark Hoven, and David C. Mauer, 1996, The determinants of corporate debt maturity

structure, Journal of Business 69, 279-312.

Sufi, Amir, 2009, Bank lines of credit in corporate finance: An empirical analysis, Review of

Financial Studies 22, 1057-1088.

Yan, An, 2006, Leasing and debt financing: Substitutes or complements?, Journal of Financial

and Quantitative Analysis 41, 709-731.

29

APPENDIX

Table A1

Description of Compustat Variables

Variable Definition

Profitability Operating Income Before Depreciation (13) / Total Assets (6)

Tangibility Net Property, Plant, and Equipment (PPENT 8) / Total Assets (6)

Preferred Stock Max[Preferred Stock Liquidating Value (10), Preferred Stock Redemption Value (56),

Preferred Stock Carrying Value (130)]

Total Debt Debt in Current Liabilities (34) + Long-Term Debt (9)

MV Equity Stock Price (199) × Common Shares Used to Calculate EPS (54)

M/B (Market Value of Equity + Total Debt + Preferred Stock Liquidating Value (10) –

Deferred Taxes and Investment Tax Credit (35)) / Total Assets (6)

Firm Size Book Value of Total Assets (6)

CF Volatility Standard Deviation of Quarterly Operating Income (13) over Previous 12 Quarters Scaled

by Total Assets (6)

Dividend Payer Dummy =1 if common stock dividends (21) are positive, and zero otherwise

Asset Maturity (Current Assets (4)/(Current Assets (4)+ PPENT)*(Current Assets (4)/Cost of Goods Sold

(41)) + (PPENT/(Current Assets (4)+ PPENT)*( PPENT/Depr. and Amort. (14))

Firm Age Number of years a firm is included with a non-missing stock price in Compustat

Rated Dummy =1 if the firm is rated by the S&P, and zero otherwise

Rating Monthly S&P ratings (280)

Market Leverage Total Debt / (Total Debt + Market Value of Equity)

Book Leverage Total Debt/Total Assets (6)

CP Commercial Paper

RC Revolving Credit Facilities (Drawn)

TL Term Loans

SBN Senior Bonds and Notes

SUB Subordinated Bonds and Notes

CL Capital Leases

Other Other Debt + Total Trust Preferred Stock

Total Principal Due Commercial Paper + Revolving Credit + Term Loans + Senior Bonds + Subordinated

Bonds + Capital Leases + Other

Total Adjustment Total Debt - Total Principal Due

HHI {[[CP/(Total Debt)]2+ [RC/(Total Debt)]

2+ [TL/(Total Debt)]

2+ [SBN/(Total Debt)]

2+

[SUB/(Total Debt)]2+ [CL/(Total Debt)]

2+ [(Other)/(Total Debt)]

2] -(1/7)}/(1-(1/7))

Entropy - [CP/(Total Debt)*ln(CP/(Total Debt))+ RC/(Total Debt)*ln(RC/(Total Debt))+ TL/(Total

Debt)*ln(TL/(Total Debt)) + SBN/(Total Debt)*ln(SUB/(Total Debt)) + CL/(Total

Debt)*ln(CL/(Total Debt)) + Other/(Total Debt)*ln(Other/(Total Debt))]

30

Table A2

An Example of How Capital IQ Classifies Debt Type

The following table illustrates how CIQ calculates each item (in millions of dollars) for AMR Corporation for the fiscal year ended

December 31, 2003. All information is available under Item 8 of Form 10K.

Item CIQ Calculation

Capital Structure Data

Total Debt 13,930 Long-term debt, less current maturities (11,901) + Obligations under capital

leases, less current obligations (1,225) + Current maturities of long-term

debt (603) + Current obligations under capital leases (201) = 13,930

Total Equity 46 Stockholders’ equity (46)

Total Capital 13,976 Total debt + Stockholders’ equity

Debt Structure Data

Total Revolving Credit 834 Credit facility agreement due through 2005 (834)

Total Term Loans 0

Total Senior Bonds and

Notes

11,668 Secured variable and fixed rate indebtedness due through 2021 (6,041) +

Enhanced equipment trust certificates due through 2011 (3,747) + Special

facility revenue bonds due through 2036 (947) + Debentures due through

2021 (330) + Notes due through 2039 (303) + Senior convertible notes due

through 2023 (300)

Total Capital Leases 1,426 Obligations under capital leases, less current obligations (1,225) + Current

obligations under capital leases (201)

Other Borrowings 2 Other (2)

Additional Totals

Total Senior Debt 13,930 = Total debt

Total Convertible Debt 300 Senior convertible notes due through 2023 (300)

Curr. Port. of Long-

Term Debt/Capital

Leases

804 Current maturities of long-term debt (603) + Current obligations under

capital leases (201)

Long-Term Debt (Incl.

Capital Leases)

13,126 Long-term debt, less current maturities (11,901) + Obligations under capital

leases, less current obligations (1,225)

Total Bank Debt 834 Credit facility agreement due through 2005 (834)

Total Secured Debt 11,214 Secured variable and fixed rate indebtedness due through 2021 (6,041) +

Enhanced equipment trust certificates due through 2011 (3,747) +

Obligations under capital leases, less current obligations (1,225) + Current

obligations under capital leases (201)

Total Unsecured Debt 2,716 Special facility revenue bonds due through 2036 (947) + Credit facility

agreement due through 2005 (834) + Debentures due through 2021 (330) +

Notes due through 2039 (303) + Senior convertible notes due through 2023

(300) + Other (2)

31

Figure 1

The Distribution of Debt Types within A Cluster

CPRCT

L

SB

N

SU

BCL

Oth

er

Clu

ste

r 1

Clu

ste

r 2

Clu

ste

r 3

Clu

ste

r 4

Clu

ste

r 5

Clu

ste

r 6 A

ll

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Cluster 1 Cluster 2 Cluster 3 Cluster 4 Cluster 5 Cluster 6 All

32

Figure 2

The Distribution of Debt Types Conditional on Significant Amount Employed (30% threshold)

CPRCT

L

SB

N

SU

BCL

Oth

er

CP RC T

L

SB

N

SU

B CL

Oth

er

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

CP RC TL SBN SUB CL Other

33

Table 1

Sample Overview

The sample consists of non-utilities (excluding SIC codes 4900-4949) and non-financials (excluding SIC codes 6000-6999) U.S.

firms covered by both Capital IQ and Compustat from 2002 to 2009. Definitions of the variables are provided in Table A1. We

have removed 1) firm-years with missing value of total assets, 2) firm-years with market or book leverage outside the unit interval,

3) firm-years with total principal due missing or smaller than $1 million, 4) firm-years for which total adjustment exceed 10% of

total debt. After the above filtering, there are 16,115 firm-year observations involving 3,296 unique firms in the sample. Applying

the same filters (except the data discrepancy filter 4) to the Compustat population over the same time period as our sample, we

obtain 18,164 (leveraged) firm-year observations. Firm Size is expressed in millions of 2002 dollars. This table presents means and

medians aggregated across all years for our sample and Compustat leveraged firms. We test for difference between our sample and

the Compustat sample using the t-test and the two-sample Wilcoxon rank-sum (Mann-Whitney) test.

Our Sample

Compustat Leveraged

Firms

Test of Difference

Compustat Leveraged Firms vs.

Our Sample

(1) (2) (3) (4) (5) (6)

Mean Median Mean Median t-test

(p-value)

MW-test

(p-value)

Mkt Leverage 0.252 0.195 0.252 0.193 0.301

(0.763)

-0.630

(0.529)

Profitability 0.086 0.114 0.083 0.113 -1.275

(0.202)

-1.618

(0.106)

Tangibility 0.288 0.213 0.286 0.212 -0.909

(0.363)

-0.893

(0.372)

M/B 1.503 1.148 1.497 1.138 -0.328

(0.743)

-1.464

(0.143)

Firm Size 3784.9 565.8 3631.5 532.7 -0.736

(0.462)

-2.039

(0.042)

CF Volatility 0.018 0.010 0.018 0.010 0.679

(0.497)

1.541

(0.123)

Dividend Payer 0.342 0.000 0.330 0.000 -2.227

(0.026)

-2.227

(0.026)

Asset Maturity 4.501 2.767 4.497 2.757 -0.078

(0.938)

-0.427

(0.669)

Firm Age 17.711 13.000 17.593 13.000 -0.798

(0.425)

-0.706

(0.480)

# Obs. 16,115 18,164

34

Table 2

Summary Statistics for Debt Types

This table reports summary statistics for the various debt types, which include commercial paper, revolving credit facilities, term

loans, senior bonds and notes, subordinated bonds and notes, capital leases, and other debt. All debt types are calculated as a

fraction of total debt. Definitions of the variables are provided in Table A1. HHI and Entropy measure the degree of debt

specialization, which is increasing in HHI and decreasing in Entropy. Panel A reports mean and key percentiles across all firm-year

observations for all the above variables. Panel B presents time series evidence on debt types.

Panel A: Percentiles of debt types

Debt Types Share of Total debt

Mean 1st

Percentile

5th

Percentile

25th

Percentile

Median 75th

Percentile

95th

Percentile

99th

Percentile

Comm. Paper 0.009 0.000 0.000 0.000 0.000 0.000 0.010 0.280

Revolving Credit 0.220 0.000 0.000 0.000 0.006 0.345 0.999 1.000

Term Loans 0.212 0.000 0.000 0.000 0.000 0.343 0.999 1.000

Sen. Bonds and Notes 0.382 0.000 0.000 0.000 0.208 0.806 1.000 1.000

Sub. Bonds and Notes 0.098 0.000 0.000 0.000 0.000 0.000 0.831 1.000

Capital Leases 0.054 0.000 0.000 0.000 0.000 0.012 0.308 1.000

Other Debt 0.025 0.000 0.000 0.000 0.000 0.001 0.118 0.695

Total Adjustment 0.000 -0.029 -0.001 0.000 0.000 0.000 0.006 0.038

HHI 0.702 0.202 0.276 0.449 0.729 0.993 1.000 1.000

Entropy 0.434 0.000 0.000 0.022 0.426 0.702 1.077 1.267

Panel B: Debt types over time

Year Debt Types

CP RC TL SBN SUB CL Other HHI Entropy # Obs.

2002 0.011 0.229 0.185 0.359 0.124 0.063 0.030 0.676 0.473 1747

2003 0.009 0.204 0.181 0.389 0.132 0.056 0.028 0.691 0.451 2075

2004 0.010 0.192 0.186 0.406 0.117 0.059 0.029 0.708 0.428 2101

2005 0.010 0.199 0.203 0.403 0.105 0.056 0.025 0.706 0.427 2104

2006 0.011 0.221 0.213 0.390 0.092 0.053 0.020 0.706 0.428 2113

2007 0.011 0.229 0.237 0.374 0.079 0.050 0.021 0.709 0.422 2120

2008 0.008 0.263 0.245 0.347 0.067 0.045 0.023 0.699 0.436 2119

2009 0.005 0.221 0.247 0.384 0.065 0.051 0.027 0.719 0.407 1736

35

Table 3

Credit Ratings and Debt Structure

This table provides descriptive statistics on the relation between credit ratings and debt types. Total debt is decomposed into

commercial paper, revolving credit facilities, term loans, senior bonds, subordinated bonds, capital leases, and other debt. All debt

types are calculated as a fraction of total debt. Definitions of the variables are provided in Table A1. Data on ratings ranging from

AAA to D are from Compustat (280). HHI and Entropy measure the degree of debt specialization, which is increasing in HHI and

decreasing in Entropy. Panel A presents debt structure in terms of mean and median debt ratios across unrated and rated groups.

We test for difference between rated and unrated using the t-test and the two-sample Wilcoxon rank-sum (Mann-Whitney) test.

Panel B presents debt structure in terms of mean and median debt ratios across different rating classes.

Panel A: Debt structure across rated and unrated groups

Unrated Rated Test of Difference Between

Unrated and Rated

(1) (2) (3) (4) (5) (6)

Mean Median Mean Median t-test

(p-value)

MW-test

(p-value)

Debt Types Share of Total Debt

Commercial Paper 0.001 0.000 0.022 0.000 -18.300

(0.000)

-34.402

(0.000)

Revolving Credit 0.297 0.047 0.094 0.000 45.647

(0.000)

23.914

(0.000)

Term Loans 0.248 0.000 0.154 0.000 18.957

(0.000)

6.771

(0.000)

Senior Bonds and Notes 0.276 0.012 0.553 0.660 -45.137

(0.000)

-41.163

(0.000)

Sub. Bonds and Notes 0.078 0.000 0.130 0.000 -12.731

(0.000)

-22.137

(0.000)

Capital Leases 0.076 0.000 0.018 0.000 24.482

(0.000)

4.873

(0.000)

Other Debt 0.023 0.000 0.029 0.000 -3.153

(0.002)

-35.366

(0.000)

HHI 0.735 0.809 0.649 0.624 20.357

(0.000)

23.354

(0.000)

Entropy 0.379 0.317 0.522 0.560 -23.925

(0.000)

-25.957

(0.000)

Market Leverage 0.210 0.148 0.319 0.275 -31.824

(0.000)

-36.506

(0.000)

Firm Size 522.2 215.5 9075.7 2434.6 -21.516

(0.000)

-89.568

(0.000)