consolidated financial statements …s2.q4cdn.com/231101920/files/doc_financials/q4...

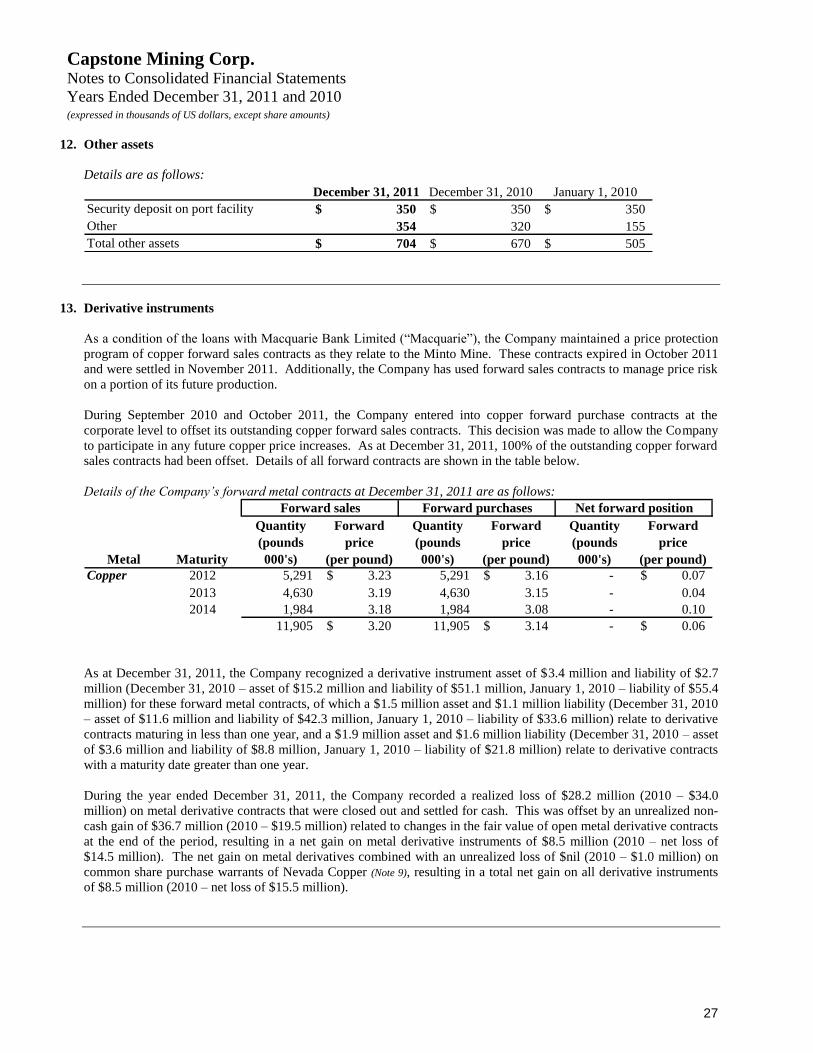

TRANSCRIPT

CONSOLIDATED FINANCIAL STATEMENTS

DECEMBER 31, 2011 and 2010

(Expressed in US Dollars)

2

Independent Auditors’ Report To the Shareholders of

Capstone Mining Corp.

We have audited the accompanying consolidated financial statements of Capstone Mining Corp, which comprise the

consolidated balance sheets as at December 31, 2011, December 31, 2010 and January 1, 2010, and the consolidated

statements of earnings, comprehensive income, changes in equity and cash flows for the years ended December 31,

2011 and December 31, 2010, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in

accordance with International Financial Reporting Standards, and for such internal control as management determines

is necessary to enable the preparation of consolidated financial statements that are free from material misstatement,

whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We

conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that

we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the

consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the

consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or

error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and

fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in

the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal

control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of

accounting estimates made by management, as well as evaluating the overall presentation of the consolidated

financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for

our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of

Capstone Mining Corp. as at December 31, 2011, December 31, 2010 and January 1, 2010 and its financial

performance and its cash flows for the years ended December 31, 2011 and December 31, 2010 in accordance with

International Financial Reporting Standards.

(Signed) Deloitte & Touche LLP

Chartered Accountants

March 13, 2012

Vancouver, Canada

Capstone Mining Corp. Consolidated Balance Sheets

(expressed in thousands of US dollars)

3

ASSETS December 31, 2011 December 31, 2010 January 1, 2010

Current

Cash and cash equivalents (Note 23) 486,287$ 165,945$ 115,931$

Restricted cash - 6,377 2,496

Short-term deposits (Note 6) - 20,039 -

Receivables (Note 7) 29,099 16,392 6,946

Inventories (Note 8) 48,332 67,210 44,438

Prepaids and other 1,360 1,581 1,404

Derivative instrument asset (Note 13) 1,530 11,602 -

566,608 289,146 171,215

Investments (Note 9) 237 2,718 39,105

Mineral properties, plant and equipment (Note 10) 782,924 324,876 316,870

Promissory note receivable (Note 4) 62,520 - -

Notes receivable (Note 11) 8 502 872

Taxes receivable 3,622 - -

Deferred income tax asset (Note 18) 1,022 5,526 15,340

Other assets (Note 12) 704 670 505

Derivative instrument asset (Note 13) 1,890 3,635 -

Total assets 1,419,535$ 627,073$ 543,907$

LIABILITIES

Current

Accounts payable and accrued liabilities 18,699$ 22,277$ 19,782$

Income taxes payable 2,452 8,524 8,041

Advances on concentrate inventories - 33,260 16,702

Current portion of other liabilities (Note 14) 12,324 48,116 47,999

33,475 112,177 92,524

Long-term debt (Note 15) - 11,573 10,821

Finance lease obligations (Note 16) - 10,280 18,425

Derivative instrument liability (Note 13) 1,543 8,812 21,757

Deferred revenue (Note 17) 46,567 60,677 73,465

Deferred income tax liability (Note 18) 41,472 31,285 32,087

Reclamation and closure cost obligations and other (Note 19) 21,593 14,531 10,472

Total liabilities 144,650 249,335 259,551

EQUITY

Share capital (Note 20) 809,892 205,790 196,115

Reserve for equity settled share based transactions 42,441 18,496 16,737

Equity component of convertible debentures 1,146 1,146 1,174

Investment revaluation reserve (315) 821 8,955

Foreign currency translation reserve (7,131) 15,558 -

Retained earnings 196,353 135,927 61,375

Total equity attributable to equity holders of the Company 1,042,386 377,738 284,356

Non-controlling interest 232,499 - -

Total equity 1,274,885 377,738 284,356

Total liabilities and equity 1,419,535$ 627,073$ 543,907$

Commitments (Note 26)

Contingencies (Note 28)

ON BEHALF OF THE BOARD:

(Signed) Darren M. Pylot , Director (Signed) Dale C. Peniuk , Director

See accompanying notes to these consolidated financial statements.

Capstone Mining Corp. Consolidated Statements of Earnings

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share and per share amounts)

4

2011 2010

Gross sales revenue 352,546$ 301,322$

Treatment and selling costs (24,781) (27,369)

Net revenue 327,765 273,953

Operating costs

Cost of sales (119,530) (105,623)

Royalties (8,526) (6,715)

Depletion and amortization (86,537) (43,314)

Earnings from mining operations 113,172 118,301

General and administrative expenses (11,656) (10,069)

Stock-based compensation (Note 20) (8,606) (4,682)

Earnings from operations 92,910 103,550

Other income (expense)

Foreign exchange loss (5,899) (1,496)

Gain (loss) on derivative instruments (Note 13) 8,483 (15,459)

Gain on disposal of investments (Note 9) 1,468 26,117

Loss on disposal of equipment (286) (63)

Earnings before finance costs and income taxes 96,676 112,649

Interest and other income 4,408 867

Interest from discounting reclamation and closure cost obligations (349) (315)

Interest on long term debt (611) (1,683)

Interest on finance lease obligations (146) (1,418)

Earnings before income taxes 99,978 110,100

Current income and mining tax expense (23,864) (25,707)

Deferred income tax expense (15,688) (9,841)

Net earnings 60,426$ 74,552$

Net earnings attributable to:

Shareholders of Capstone Mining Corp. 60,692$ 74,552$

Non-controlling interest (266) -

60,426$ 74,552$

Earnings per share - basic (Note 21) 0.20$ 0.37$

Weighted average number of shares - basic 295,997,095 198,996,825

Earnings per share - diluted (Note 21) 0.20$ 0.37$

Weighted average number of shares - diluted 303,075,854 202,453,289

See accompanying notes to these consolidated financial statements.

Capstone Mining Corp. Consolidated Statements of Comprehensive Income

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars)

5

2011 2010

Net earnings 60,426$ 74,552$

Other comprehensive (loss) income

Change in fair value of available-for-sale securities, net of tax

of $64 (2010 - $914) (369) 6,859

Gain on the disposal of available-for-sale securities reclassified

to net earnings on realization, net of tax of $132 (2010 - $2,443) (767) (14,993)

Foreign currency translation adjustment (22,689) 15,558

(23,825) 7,424

Total comprehensive income 36,601$ 81,976$

Total comprehensive income attributable to:

Shareholders of Capstone Mining Corp. 36,867$ 81,976$

Non-controlling interest (266) -

36,601$ 81,976$

See accompanying notes to these consolidated financial statements.

Capstone Mining Corp. Consolidated Statements of Cash Flows

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars)

6

2011 2010

Cash provided by (used in):

Operating activities

Net earnings 60,426$ 74,552$

Adjustments for:

Net finance costs (3,302) 2,549

Current income tax expense 23,864 25,707

Depletion, amortization and accretion 86,940 43,630

Amortization of deferred revenue (13,711) (14,410)

Stock-based compensation 8,606 4,682

Shares issued for compensation 267 309

Deferred income tax expense 15,688 9,841

Gain on disposal of investments (1,468) (26,117)

Loss on disposal of equipment 286 63

Unrealized gain on derivative instruments (36,645) (18,503)

Unrealized loss on foreign exchange 5,318 613

Other - 175

Interest received (paid) 2,719 (25,772) Income taxes paid (28,606) (2,885)

Payments on reclamation and closure cost obligations (114) (125)

Changes in non-cash working capital (Note 24) (33,837) 11,984

86,431 86,293

Investing activities

(Increase) decrease in restricted cash 6,436 (3,544)

Proceeds on sale of investments 2,979 60,912

Purchase of investments (199) (8,228)

Mineral properties, plant and equipment additions (88,244) (55,526)

Purchase of Far West net assets (Note 4) (56,690) -

Sale of non-controlling interest in Far West net assets (Note 4) 277,378 -

Proceeds on maturity of short-term deposits 40,000 -

Purchase of short-term deposits (20,000) (20,000)

Other deposits (64) (856)

161,596 (27,242)

Financing activities

Repayment of long-term debt (7,305) (9,800)

Payment to fund KORES promissory note (Note 4) (83,213) -

Repayment of KORES promissory note (Note 4) 5,454 -

Repayment of finance lease obligations (10,603) (11,026)

Proceeds from issuance of share capital 188,363 6,322

Share issue costs (1,431) -

91,265 (14,504)

Effect of exchange rate changes on cash and cash equivalents (18,950) 5,467

Increase in cash and cash equivalents 320,342 50,014

Cash and cash equivalents - beginning of year 165,945 115,931

Cash and cash equivalents - end of year 486,287$ 165,945$

Supplemental cash flow information (Note 23)

See accompanying notes to these consolidated financial statements.

Capstone Mining Corp. Consolidated Statements of Changes in Equity (expressed in thousands of US dollars, except share amounts)

7

Number of

shares Share capital

Reserve for

equity settled

share based

transactions

Equity

component of

convertible

debentures

Investment

revaluation

reserve

Foreign currency

translation

reserve

Retained

earnings Total

Non-controlling

interest Total equity

December 31, 2010 201,454,802 205,790$ 18,496$ 1,146$ 821$ 15,558$ 135,927$ 377,738$ -$ 377,738$

Private placement (Note 20) 40,198,632 177,958 - - - - - 177,958 - 177,958

Exercise of options 5,647,392 18,125 (7,720) - - - - 10,405 - 10,405

Stock-based compensation - - 8,606 - - - - 8,606 - 8,606

Issued for compensation 80,000 267 - - - - - 267 - 267

Share issue costs - (1,447) - - - - - (1,447) - (1,447)

Deferred income tax on

share issue costs - 365 - - - - - 365 - 365

Purchase of Far West net assets (Note 4) 128,753,385 408,575 23,318 - - - - 431,893 - 431,893

Sale of non-controlling interest in

Far West net assets (Note 4) - - - - - - - - 277,378 277,378

Reduction to carrying value of

mineral property on sale of

Far West net assets (Note 4)- - - - - - - - (44,879) (44,879)

Issued for mineral properties 100,000 259 (259) - - - - - - -

Change in fair value of

available-for-sale securities - - - - (369) - - (369) - (369)

Gains reclassified to earnings - - - - (767) - - (767) - (767)

Net earnings - - - - - - 60,426 60,426 - 60,426

Foreign currency translation - - - - - (22,689) - (22,689) - (22,689)

December 31, 2011 376,234,211 809,892$ 42,441$ 1,146$ (315)$ (7,131)$ 196,353$ 1,042,386$ 232,499$ 1,274,885$

January 1, 2010 197,645,802 196,115$ 16,737$ 1,174$ 8,955$ -$ 61,375$ 284,356$ -$ 284,356$

Exercise of options 3,560,753 8,986 (2,664) - - - - 6,322 - 6,322

Stock-based compensation - - 4,682 - - - - 4,682 - 4,682

Issued for compensation 123,390 309 - - - - - 309 - 309

Issued for mineral properties 100,000 259 (259) - - - - - - -

Issued on conversion of

convertible debentures 24,857 121 - (28) - - - 93 - 93

Change in fair value of available-

for-sale securities - - - - 6,859 - - 6,859 - 6,859

Gains reclassified to earnings - - - - (14,993) - - (14,993) - (14,993)

Net earnings - - - - - - 74,552 74,552 - 74,552

Foreign currency translation - - - - - 15,558 - 15,558 - 15,558

December 31, 2010 201,454,802 205,790$ 18,496$ 1,146$ 821$ 15,558$ 135,927$ 377,738$ -$ 377,738$

Attributable to equity holders of the Company

See accompanying notes to these consolidated financial statements.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

8

1. Nature of operations

Capstone Mining Corp. (the “Company” or “Capstone”), a publicly listed Canadian mining company on the Toronto

Stock Exchange, is engaged in the exploration for and production of base and precious metals in Canada, Mexico,

Chile, and Australia. Minto Explorations Ltd. (“Minto”), a wholly owned Canadian subsidiary, owns and operates the

copper-gold-silver Minto Mine located in Yukon Territory, Canada. Capstone Gold, S.A. de C.V. (“Capstone Gold”),

a wholly owned Mexican subsidiary, owns and operates the copper-silver-zinc-lead Cozamin Mine located in

Zacatecas, Mexico. Minera Santo Domingo SCM (“Santo Domingo”), a 70% owned Chilean subsidiary, is advancing

the Santo Domingo copper-iron-gold project in Chile towards a production decision. Kutcho Copper Corp. (“Kutcho

Copper”), a wholly owned Canadian subsidiary, is advancing the Kutcho copper-zinc-silver-gold project in British

Columbia, Canada towards a production decision. Far West Mining Pty Ltd. (“Far West Australia”), a 70% owned

Australian subsidiary, holds active exploration properties in Australia.

The head office, registered and records office and principal address of the Company are located at 999 West Hastings

Street, Vancouver, British Columbia and the Company is incorporated in British Columbia.

The financial statements were approved by the Board of Directors and authorized for issuance on March 13, 2012.

2. Significant accounting policies

Basis of preparation and consolidation

These consolidated financial statements represent the first annual financial statements of the Company and its

subsidiaries prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the

International Accounting Standard Board (“IASB”). IFRS 1, First-time Adoption of IFRS, has therefore been applied

in preparing these consolidated financial statements.

These consolidated financial statements have been prepared in accordance with the accounting policies presented

below and are based on the IFRS and International Financial Reporting Interpretations Committee (“IFRIC”)

interpretations issued and effective as of December 31, 2011. The policies set out below were consistently applied to

all the periods presented unless otherwise noted.

The Company's consolidated financial statements were previously prepared in accordance with Canadian generally

accepted accounting principles (“GAAP”), which differs in some areas from IFRS. In preparing these consolidated

financial statements, management has amended certain accounting methods previously applied in the Canadian GAAP

consolidated financial statements to comply with IFRS. The comparative figures for 2010 were restated to reflect

these amendments. Reconciliations and descriptions of the effect of the transition from Canadian GAAP to IFRS on

equity, earnings, and comprehensive income are provided in Note 29.

Use of estimates and judgments

The preparation of consolidated financial statements requires management to select accounting policies and make

estimates and judgments that may have a significant impact on the consolidated financial statements. The Company

regularly reviews its estimates; however, actual amounts could differ from the estimates used and, accordingly,

materially affect the results of operations.

Examples of significant estimates include:

purchase price allocation on business combinations and acquisitions of assets;

mineral resources and mineral reserves;

the carrying values of inventories;

estimated tonnes of waste material mined for calculation of deferred stripping costs;

the carrying values of mineral properties, plant and equipment;

rates of amortization of mineral properties, plant and equipment;

the assumptions used for the determination of reclamation and closure cost obligations;

the valuation of deferred income taxes and allowances;

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

9

estimates used in the assessment of impairment of mineral properties, plant and equipment;

the valuation of financial instruments, including estimates used in provisional pricing calculations;

the carrying values of receivables; and

the valuation of share-based compensation.

Examples of significant judgments, apart from those involving estimation, include:

the accounting policies for mineral properties, plant and equipment;

determination that the transaction with Far West Mining Ltd. constitutes an acquisition of assets;

classification of financial instruments;

classification of leases; and

determination of functional currency.

Translation of foreign currencies

The Company considers the functional currency of its Canadian and Australian operations to be the Canadian dollar

and the functional currency of its Mexican and Chilean operations to be the US dollar. The presentation currency of

the Company is the US dollar. Financial statements of subsidiaries are maintained in their functional currencies and

converted to US dollars for consolidation of the Company’s results. The functional currency of each entity is

determined after consideration of the primary economic environment of the entity.

Transactions denominated in foreign currencies (currencies other than the functional currency of an operation) are

translated at the exchange rates on the date of transaction. Monetary assets and liabilities denominated in foreign

currencies are translated at reporting date exchange rates and any gain or loss on translation is recorded in the

statement of earnings as a foreign exchange gain (loss).

On translation of entities with functional currencies other than the US dollar, statement of earnings items are translated

at average rates of exchange where this is a reasonable approximation of the exchange rate at the dates of the

transactions. Balance sheet items are translated at closing exchange rates as at the reporting date. Exchange

differences on the re-translation of the foreign currency entities at closing rates, together with differences between

statement of earnings translated at average and closing rates, are recorded in the foreign currency translation reserve in

equity.

The following USD/CAD exchange rates have been applied:

2011 2010

January 1 opening rate 0.9946 1.0510

Quarterly average rate

Q1 0.9856 1.0401

Q2 0.9680 1.0283

Q3 0.9808 1.0395

Q4 1.0230 1.0131

December closing rate 1.0170 0.9946

Business combinations

Business combinations are accounted for using the acquisition method whereby identifiable assets acquired and

liabilities assumed, including contingent liabilities, are recorded at 100% of their fair values at the date of acquisition.

The acquisition date is the date at which the Company obtains control over the acquire, which is generally the date that

consideration is transferred and the Company acquired the assets and assumes the liabilities of the acquiree.

Acquisition related costs of business combinations are recorded as expenses.

Non-controlling interests are recorded at their proportionate share of the fair value of identifiable net asets acquired on

initial recognition and are classified as a separate component of equity. The excess of (i) total consideration

transferred by the Company, measured at fair value, including contingent consideration, and (ii) the non-controlling

interests in the acquiree, over the fair value of net assets acquired, is recorded as goodwill.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

10

Cash, cash equivalents and restricted cash

Cash and cash equivalents is comprised of cash on hand, demand deposits and short-term investments with a maturity

less than 90 days on acquisition that are readily convertible into known amounts of cash. Restricted cash is comprised

of cash collateral to secure future debt repayments as well as to fund future reclamation obligations.

Short-term deposits

The Company considers short-term deposits to include amounts held in banks and highly liquid investments with

maturities of more than 90 days and less than one year on acquisition.

Inventories

Inventories for consumable parts and supplies, ore stockpiles and ore concentrates, are valued at the lower of cost and

net realizable value. Costs allocated to consumable parts and supplies are based on average costs and include all costs

of purchase, conversion and other costs in bringing these inventories to their existing location and condition. Costs

allocated to ore stockpiles and ore concentrates are based on average costs, which include an appropriate share of

direct mining costs, direct labour and material costs, mine site overhead, depletion and amortization. If carrying value

exceeds net realizable amount, a write down is recognized. The write down may be reversed in a subsequent period if

the circumstances which caused it no longer exist.

Investments

Investments in shares of companies over which the Company exercises neither control nor significant influence are

designated as available-for-sale and recorded at fair value. Fair values are determined by reference to quoted market

prices at the reporting date. Unrealized gains and losses on available-for-sale investments are recognized in the

investment revaluation reserve. When available-for-sale investments are sold, the cumulative fair value adjustments

previously recorded in the investment revaluation reserve are recognized in the statement of earnings as gain or loss on

investments.

Investments in warrants of companies over which the Company exercises neither control nor significant influence are

designated as derivatives despite the fact they are generally held for long-term investment purposes. Warrants are

recorded at fair value, with fair values determined by a Black-Scholes option pricing model at the balance sheet date.

Unrealized gains and losses on warrants are recognized in the statement of earnings as gain or loss on derivative

instruments.

Mineral properties, plant and equipment

Title to mineral properties involves certain inherent risks due to the difficulties of determining the validity of certain

claims as well as the potential for problems arising from the frequently ambiguous conveyancing history characteristic

of many properties. The Company has investigated title to all of its mineral properties and, to the best of its

knowledge, title to all of its properties is in good standing.

Producing mineral properties

Producing mineral properties are recorded at cost less accumulated depletion and impairment charges. The costs

associated with producing mineral properties include acquired interests in production stage properties representing the

fair value at the time they were acquired. Producing mineral properties also include additional capitalized costs after

initial acquisition. Upon sale or abandonment of producing mineral properties, the cost and related accumulated

depletion and impairment charges, are written off and any gains or losses thereon are included in the statement of

earnings.

Commercial production is deemed to have commenced when management determines that the operational

commissioning of major mine and plant components is complete, operating results are being achieved consistently for

a period of time and that there are indicators that these operating results will continue. The Company determines

commencement of commercial production based on the following factors, which indicate that planned principal

operations have commenced. These include one or more of the following: a significant portion of plant capacity is achieved;

a significant portion of available funding is directed towards operating activities;

a pre-determined, reasonable period of time has passed; and

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

11

a development project significant to the primary business objectives of the enterprise has been completed as

to significant milestones being achieved.

Deferred stripping

Stripping costs are accounted for as variable production costs and included in the costs of inventory produced during

the period that the stripping costs are incurred. However, stripping costs will be capitalized and recorded on the

balance sheet as a component of mineral properties, plant and equipment when the stripping activity provides access to

sources of reserves that will be produced in future periods that would not have otherwise been accessible in the

absence of this activity. The deferred stripping will be amortized on a unit of production basis over the reserves that

directly benefited from the stripping activity as those reserves are actually mined.

Mineral exploration and development properties

Mineral exploration and development properties comprise costs that are directly attributable to:

researching and analysing existing exploration data;

conducting geological studies, exploratory drilling and sampling;

examining and testing extraction and treatment methods; and

activities in relation to evaluating the technical feasibility and commercial viability of extracting a mineral

resource.

The costs associated with mineral exploration and development properties includes acquired interests in development

and exploration stage properties representing the fair value at the time they were acquired. Mineral exploration and

development properties also includes additional capitalized costs after initial acquisition.

Mineral exploration and development properties expenditures for each area of interest are carried forward as an asset

provided that one of the following conditions is met:

such costs are expected to be recouped in full through successful development and exploration of the area

of interest or alternatively, by its sale; or

exploration and evaluation activities in the area of interest have not yet reached a stage which permits a

reasonable assessment of the existence of economically recoverable reserves, however active and

significant operations in relation to the area are continuing, or planned for the future.

The carrying values of capitalized amounts of mineral exploration and development properties are reviewed annually,

or when there are indicators of impairment at each reporting date. In the case of undeveloped projects, there may be

only inferred resources to allow management to form a basis for the impairment review. The review is based on the

Company’s intentions for development of such a project. If a project does not prove viable, all unrecoverable costs

associated with the project are charged to the statement of earnings at the time the determination is made.

Once management has determined that the development potential of the property is economically viable and the

necessary permits are in place for its development, the costs of the exploration asset are reclassified to Producing

mineral properties.

Mill development costs

Mill development costs are recorded at cost less accumulated amortization and impairment losses. Mill development

costs includes in its purchase price, any costs directly attributable to the development of the mill. Upon abandonment

of any mill development costs, the cost and related accumulated amortization and impairment losses, are written off

and any gains or losses thereon are included in the statement of earnings.

Plant and equipment

Plant and equipment are recorded at cost less accumulated amortization and impairment losses. Plant and equipment

includes in its purchase price, any costs directly attributable to bringing plant and equipment to the location and

condition necessary for it to be capable of operating in the manner intended by management and the estimated close

down and restoration costs associated with dismantling and removing the asset. Upon sale or abandonment of any

plant and/or equipment, the cost and related accumulated amortization and impairment losses, are written off and any

gains or losses thereon are included in the statement of earnings.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

12

Construction in progress

Mineral property development and plant and equipment construction commences when approved by management

and/or the Board and the Company has obtained all regulatory permissions to proceed. Development and construction

expenditures are capitalized and classified as Construction in progress. Once completed, the costs associated with all

applicable assets related to the development and construction are reclassified to the appropriate category within

mineral properties or plant and equipment.

Depletion and amortization of mineral properties, plant and equipment

The carrying amounts of mineral properties, plant and equipment are depleted or amortized to their estimated residual

value over the estimated economic life of the specific assets to which they relate, using the depletion or amortization

methods and rates as indicated below. Estimates of residual values and useful lives are reassessed annually and any

change in estimate is taken into account in the determination of the remaining amortization rate. Amortization

commences on the date the asset is available for its use as intended by management.

Depletion and amortization is computed using the following rates:

Item Methods Rates

Producing mineral

properties

Units of production Estimated proven and probable reserves

Deferred stripping costs Units of production Estimated proven and probable reserves

accessible due to stripping activity

Mill development costs Units of production Estimated proven and probable reserves

Plant & equipment Straight line,

Units of production

4 – 10 years,

Estimated proven and probable reserves

Equipment and facilities

under finance leases

Straight line Lesser of lease term and estimated useful

life (7 years)

Mineral exploration and

development properties

Not amortized

Construction in progress Not amortized

Borrowing costs

Interest and other financing costs directly related to the acquisition, development and construction, and production of

qualifying assets are capitalized as construction in progress or in mineral properties until they are complete and

available for use, at which time they are transferred to the appropriate category within mineral properties, plant and

equipment. Borrowing costs incurred after the asset has been placed into service as well as all other borrowing costs

are charged to earnings when incurred.

Impairment of long-lived assets

At each reporting date, the Company reviews the carrying amounts of its assets to determine whether there are any

indicators of impairment. If any such indicator exists, the recoverable amount of the asset is estimated in order to

determine the extent of the impairment, if any.

Where the asset does not generate cash inflows that are independent from other assets, the Company estimates the

recoverable amount of the cash generating unit (CGU) to which the asset belongs. The recoverable amount is

determined as the higher of fair value less direct costs to sell and the asset or CGU’s value in use. In assessing value

in use, the estimated future cash flows are discounted to their present value. Estimated future cash flows are calculated

using estimated recoverable reserves, estimated future commodity prices and the expected future operating and capital

costs. The pre-tax discount rate applied to the estimated future cash flows reflects current market assessments of the

time value of money and the risks specific to the asset for which the future cash flow estimates have not been adjusted.

Determining the discount rate includes appropriate adjustments for the risk profile of the country in which the

individual asset or CGU operates.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

13

If the carrying amount of an asset or CGU exceeds its recoverable amount, the carrying amount of the asset or CGU is

reduced to its recoverable amount. An impairment loss is recognized in the statement of earnings.

Assets that have been impaired are tested for possible reversal of the impairment whenever events or changes in

circumstance indicate that the impairment may have reversed. Where an impairment subsequently reverses, the

carrying amount of the asset or CGU is increased to the revised estimate of its recoverable amount, but only so that the

increased carrying amount does not exceed the carrying amount that would have been determined (net of amortization

or depletion) had no impairment loss been recognized for the asset or CGU in prior periods. A reversal of impairment

is recognized as a gain in the statement of earnings.

Income taxes

Current tax

Current tax for each taxable entity in the Company is based on the local taxable income at the local statutory tax rate

enacted or substantively enacted at the reporting date, and includes adjustments to tax payable or recoverable in

respect of previous periods.

Deferred tax

Deferred tax is accounted for using the balance sheet liability method, providing for the tax effect of temporary

differences between the carrying amount of assets and liabilities for financial reporting purposes and their respective

tax bases.

Deferred income tax liabilities are recognized for all taxable temporary differences except where the deferred income

tax liability arises from the initial recognition of goodwill, or the initial recognition of an asset or liability in a

transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit or

loss nor taxable profit or loss.

Deferred income tax assets are recognized for all deductible temporary differences, carry-forward of unused tax losses

and unused tax credits, to the extent that it is probable that taxable profit will be available against which the deductible

temporary differences, and the carry-forward of unused tax losses can be utilized, and except where the deferred

income tax asset related to the deductible temporary difference arises from the initial recognition of an asset or liability

in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting

profit or loss nor taxable profit or loss.

The carrying amount of deferred income tax assets is reviewed at each reporting date and is adjusted to the extent that

it is no longer probable that sufficient taxable profit will be available to allow all or part of the asset to be utilized. To

the extent that an asset not previously recognized fulfils the criteria for recognition, a deferred income tax asset is

recorded.

Deferred tax is measured on an undiscounted basis using the tax rates that are expected to apply in the period when the

liability is settled or the asset is realized, based on tax rates and tax laws enacted or substantively enacted at the

reporting date. Deferred tax assets and liabilities are offset when they relate to income taxes levied by the same

taxation authority and the Company intends to settle its current tax assets and liabilities on a net basis. Current and

deferred tax relating to items recognized directly in equity are recognized in equity and not in the statement of

earnings.

Mining taxes and royalties are treated and disclosed as current and deferred taxes if they have the characteristics of an

income tax. This is considered to be the case when they are imposed under government authority and the amount

payable is calculated by reference to revenue derived (net of any allowable deductions) after adjustment for items

comprising temporary differences.

Taxes receivable

Taxes receivable are comprised of recoverable value added taxes in Mexico and Chile and recoverable harmonized

sales tax in Canada that the Company has paid.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

14

Derivative instruments

The Company uses derivative instruments to reduce the potential impact of changing metal prices and foreign

exchange rates on its earnings. Derivative instruments are marked-to-market at the end of each reporting period and

the mark-to-market adjustment is recorded as a gain or loss on derivative instruments in the statement of earnings.

The Company does not apply hedge accounting to its derivative transactions.

Embedded derivatives

Derivatives may be embedded in other financial instruments (the “host instrument”). Embedded derivatives are

treated as separate derivatives when their economic characteristics and risks are not clearly and closely related to those

of the host instrument, the terms of the embedded derivative are the same as those of a stand-alone derivative, and the

combined contract is not held for trading or designated at fair value. These embedded derivatives are measured at fair

value with subsequent changes recognized in gains or losses on derivative instruments in the statement of earnings.

Compound instruments

The component parts of compound instruments are classified separately as financial liabilities and equity in

accordance with the substance of the contractual agreement. At the date of issue, the fair value of the liability

component is estimated using the prevailing market interest rate for similar non-convertible instruments. This amount

is recorded as a liability on an amortized cost basis until extinguished upon conversion or at the instrument’s maturity

date. The equity component is determined by deducting the amount of the liability component from the face value of

the compound instrument as a whole. This is recognized and included in equity, net of income tax effects, and is not

subsequently remeasured.

Financial instruments

On initial recognition, all financial instruments are recorded at fair value. Financial assets are designated upon

inception as either: (i) “held-to-maturity”; (ii) “fair value through profit or loss”; (iii) “available-for-sale”; or (iv)

“loans and receivables”. The designation determines the method by which the financial assets are carried on the

balance sheet subsequent to inception and how changes in value are recorded. Derivative instruments are classified as

“fair value through profit or loss” with subsequent changes in fair value recognized in the statement of earnings. Cash

and cash equivalents, restricted cash and short-term deposits are also classified as “fair value through profit or loss”.

Receivables, the promissory note, and notes receivable are designated as “loans and receivables” and are carried on the

balance sheet at amortized cost. Investments are designated as “available-for-sale” with changes in fair value

recognized in other comprehensive income.

Financial liabilities are designated as either: (i) “fair value through profit or loss”; or (ii) “other liabilities”. The

designation determines the method by which the financial liabilities are carried on the balance sheet subsequent to

inception and how changes in value are recorded. Derivative instruments are classified as “fair value through profit or

loss” with changes in fair value recognized in the statement of earnings. Accounts payable and accrued liabilities,

advances on concentrate inventories and long-term debt are classified as “other financial liabilities” and carried on the

balance sheet at amortized cost.

Transaction costs associated with “fair value through profit or loss” financial instruments are expensed as incurred,

whereas transaction costs associated with all other financial instruments are added to the initial carrying value of the

asset or liability.

Impairment and uncollectibility of financial assets

An assessment is made at each reporting date to determine whether there is objective evidence that a financial asset or

group of financial assets, other than those classified as “fair value through profit and loss” may be impaired. If such

evidence exists, the estimated recoverable amount of the asset is determined and an impairment loss is recognized for

the difference between the recoverable amount and the carrying amount as follows: the carrying amount of the asset is

reduced to its recoverable amount discounted at the financial asset’s original effective interest rate, either directly or

through the use of an allowance account and the resulting loss is recognized in the statement of earnings for the period.

When an “available-for-sale” financial asset is considered to be impaired, cumulative losses previously recognized in

the investment revaluation reserve in equity are reclassified to the statement of earnings.

With the exception of “available-for-sale” equity instruments, if, in a subsequent period, the amount of the impairment

loss decreases, the previously recognized impairment loss is reversed through the statement of earnings to the extent

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

15

that the carrying amount of the investment at the date the impairment is reversed does not exceed what the amortised

cost would have been had the impairment not been recognized. In respect of “available-for-sale” equity securities,

impairment losses previously recognized in the statement of earnings are not reversed through the statement of

earnings. Any increase in fair value subsequent to an impairment loss is recognized in other comprehensive income.

Deferred revenue

Deferred revenue consists of payments received by the Company in consideration for future commitments to deliver

payable gold and silver contained in concentrate at contracted prices. In addition, it includes the fair value of such

commitments acquired by way of business combination. As deliveries are made, the Company records a portion of the

deferred revenue as sales, based on a proportionate share of deliveries made compared with the total estimated

contractual commitment.

Leases

Assets held under leases which result in the Company receiving substantially all the risks and rewards of ownership of

the asset (finance leases) are capitalized at the lower of the fair value of the plant and equipment or the estimated

present value of the minimum lease payments. The corresponding liability is recognized as a finance lease obligation.

The interest element is allocated to accounting periods during the lease term to reflect the rate of interest on the

remaining balance of the obligation. Operating lease assets are not capitalized and rental payments are included in the

statement of earnings on a straight-line basis over the lease term.

Reclamation and closure cost obligations

A reclamation and closure cost obligation is recognized for close down, restoration and for environmental

rehabilitation costs (which include the dismantling and demolition of infrastructure, removal of residual materials and

remediation of disturbed areas) in the financial period when the related environmental disturbance occurs, based on the

estimated future costs using information available at the balance sheet date. At the time of establishing the provision, a

corresponding asset is capitalized, where it gives rise to a future benefit, and amortized over future production from

the operations to which it relates. The provision is discounted using a current market-based pre-tax discount rate and

the unwinding of the discount is included in the statement of earnings as interest expense from discounting reclamation

and closure cost obligations.

The obligation is reviewed each reporting period for changes to obligations, legislation or discount rates that impact

estimated costs or lives of operations. The cost of the related asset is adjusted for changes in the provision resulting

from changes in the estimated cash flows or discount rate and the adjusted cost of the asset is amortized prospectively.

Provisions

Provisions are recognized when the Company has a present obligation (legal or constructive), as a result of past events,

and it is probable that an outflow of resources that can be reliably estimated will be required to settle the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation

at the reporting date, taking into account the risks and uncertainties surrounding the obligation. Where the effect is

material, the provision is discounted to net present value using an appropriate current market-based pre-tax discount

rate and the unwinding of the discount is included in the statement of earnings as interest expense from discounting

obligations.

Share capital

The proceeds from the exercise of stock options or warrants together with amounts previously recorded over the

vesting periods are recorded as share capital. Share capital issued for non-monetary consideration is recorded at an amount based on fair market value on the date of

issue.

The proceeds from the issue of units is allocated between common shares and common share purchase warrants on a

pro-rata basis based on relative fair values as follows: the fair value of the common shares is based on the market close

on the date the units are issued and the fair value of the common share purchase warrants is determined using the

Black-Scholes option pricing model.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

16

Flow-through shares

Under the terms of Canadian flow-through share legislation, the tax attributes of qualifying expenditures are

renounced to subscribers. To recognize the foregone tax benefits, a deferred income tax expense and offsetting

deferred income tax liability are recognized as the related expenditures are renounced. In addition, any premiums paid

for flow-through shares in excess of the market value of shares without the flow-through features at the time of issue is

credited to other liabilities and recognized in the statement of earnings at the time the qualifying expenditures are

made.

Share-based payments

The Company makes periodic grants of share-based awards to selected directors, officers, employees and others

providing similar service. Contributions to the Company’s employee share purchase plan (“ESPP”) are recorded on a

payroll cycle basis as the Company’s obligation to contribute is incurred.

The fair value of the equity-settled awards is determined at the date of the grant by using the Black-Scholes option

pricing model. At each reporting date prior to vesting, the cumulative expense representing the extent to which the

vesting period has expired and management’s best estimate of the awards that are ultimately expected to vest is

computed. The movement in cumulative expense is recognized in the statement of earnings with a corresponding

entry within equity, against the reserve for equity settled share based transactions. No expense is recognized for

awards that do not ultimately vest.

Revenue recognition

Sales are recognized and revenue is recorded at market prices following the transfer of title and risk of ownership,

provided that collection is reasonably assured, the price is reasonably determinable, the Company has no significant

continuing involvement, and the costs incurred or to be incurred in respect of the transaction can be measured readily.

The Company’s metal concentrates are sold under a pricing arrangement where final prices are determined by quoted

market prices in a period subsequent to the date of sale. Until prices are final, revenues are recorded upon delivery

based on forward market prices for the expected period of final settlement. Subsequent variations in the final

determination of the metal concentrate weight, assay and price are recognized as revenue adjustments as they occur

until finalized. Under the terms of the Company’s off-take agreements, it may request advances from its customers

which are recorded as advances on concentrate inventories until the related revenue is recognized.

Earnings per share

Basic earnings per share is computed by dividing net earnings available (attributable) to common shareholders by the

weighted average number of common shares outstanding during the period. The computation of diluted earnings per

share assumes the conversion, exercise or contingent issuance of securities only when such conversion, exercise or

issuance would have a dilutive effect on earnings per share. The dilutive effect of convertible securities is reflected in

diluted earnings per share by application of the "if converted" method. The dilutive effect of outstanding options and

warrants and their equivalents is reflected in diluted earnings per share by application of the treasury stock method.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

17

3. Adoption of new and revised IFRS and IFRS not yet effective

The accounting policies adopted in the preparation of the consolidated financial statements have been prepared on the

basis of all IFRS and interpretations effective as at December 31, 2011. Comparative figures in the financial

statements and notes as at January 1, 2010 and for the year ended December 31, 2010 have been restated to

consistently apply the same IFRS used for the year ended December 31, 2011.

The Company has not applied the following revised or new IFRS that have been issued but are not yet effective at

December 31, 2011:

Amendments to IAS 1, Presentation of Financial Statements (effective for annual periods beginning on or

after July 1, 2012) require that elements of other comprehensive income that may subsequently be recycled

through profit and loss be differentiated from those items that will not be recycled.

IFRS 9, Financial Instruments (effective January 1, 2015) introduces new requirements for the

classification and measurement of financial assets and liabilities.

IFRS 10, Consolidated Financial Statements, IFRS 11, Joint Arrangements, IFRS 12, Disclosure of

Interests in Associates and Joint Ventures (all effective January 1, 2013) provide guidance on the

accounting treatment and associated disclosure requirements for joint arrangements and associates, and a

revised definition of “control” for identifying entities which are to be consolidated. IAS 27, Separate

Financial Statements and IAS 28, Investments in Associates and Joint Ventures were revised and reissued

to align with the new consolidation guidance.

IFRS 13, Fair Value Measurement (effective January 1, 2013) provides new guidance on fair value

measurement and disclosure requirements.

IAS 19, Employee Benefits (effective January 1, 2013) introduces changes to the accounting for defined

benefit plans and other employee benefits that include modification of the accounting for termination

benefits and classification of other employee benefits.

IFRIC 20, Stripping Costs in the Production Phase of a Mine (effective January 1, 2013 with earlier

application permitted) clarifies the requirements of accounting for the costs of stripping activity in the

production phase when stripping improves the access to further quantities of material that will be mined in

future periods.

Amendments to IAS 32, Financial Instruments (effective for annual periods beginning on or after January

1, 2013) clarifies the application of the offsetting rules and requires additional disclosure on financial

instruments subject to netting arrangements.

The Company is currently assessing the impact that these new accounting standards will have on the consolidated

financial statements.

Detailed disclosures of the effects of transition to IFRS from Canadian GAAP can be found in Note 29.

4. Purchase of mineral properties

Far West Mining Ltd.

On April 15, 2011, Capstone and Far West Mining Ltd. (“Far West”) entered into an agreement to combine by way of

a plan of arrangement, whereby Capstone agreed to purchase all of the outstanding common shares, warrants and

options of Far West (the “Transaction”). The Far West shareholders were entitled to elect to receive, in exchange for

each Far West share held either (i) 1.825 shares of Capstone and C$1.00 in cash, (ii) 2.047 shares of Capstone and

C$0.001 in cash, or (iii) C$9.19 cash, subject to proration on the basis of an aggregate maximum cash amount of

approximately C$79.0 million and provided that no Far West shareholder that elected option (iii) above, would receive

less than C$1.00 in cash per Far West share. On June 17, 2011, Capstone completed its purchase of Far West. Far

West holds the Santo Domingo copper-iron-gold project in Chile as well as active exploration properties in Australia.

The Company is continuing advancement of the Santo Domingo project in Chile towards a production decision.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

18

The transaction has been recorded as an asset purchase of mineral properties with the costs of the acquisition allocated

as follows (expressed in thousands, except share amounts):

Purchase price:

Common shares of Capstone issued (128,753,385 shares) 408,575$

Cash consideration 71,770

Options exchanged 19,270

Warrants exchanged 4,048

Transaction costs 5,451

509,114$

Net assets acquired:

Cash 15,512$

Plant and equipment 331

Mineral properties 491,984

Non-current taxes receivable 3,436

Non-cash operating working capital (net) (2,149)

509,114$

As part of the purchase, Capstone issued 12,091,629 options in exchange for 5,907,000 options of Far West, which

equates to an exchange ratio of 2.047 Capstone options for every Far West option exchanged. Those issued by

Capstone were on the same terms and conditions as those exchanged by the Far West holders. As a result of these

exchanges, Capstone recorded the fair value of the vested options of $19.3 million as a cost of the purchase (Note 20).

As part of the purchase, Capstone issued 4,451,221 warrants in exchange for 2,439,025 warrants of Far West which

equates to an exchange ratio of 1.825 Capstone warrants for every Far West warrant exchanged. Those issued by

Capstone were on the same terms and conditions as those exchanged by the Far West holders, except for the exercise

price, which was reduced by C$1.00. As a result of these exchanges, Capstone recorded the fair value of the vested

warrants of $4.0 million as a cost of the purchase (Note 20).

Concurrent with the Company’s purchase of Far West, the Company announced that it had entered into a strategic

partnership with Korea Resources Corporation (“KORES”). Under the terms of the partnership, Capstone sold to

KORES a 30% indirect interest in the Far West net assets for net cash consideration of $194.2 million. As a result of

this partial disposition of its ownership interest in the Far West net assets, Capstone recorded a $44.9 million reduction

to the carrying value of the Far West mineral properties on the date of purchase. This reduction in mineral properties

represented the amount paid by KORES for its 30% interest in excess of a 30% share of the fair value of the Far West

net assets acquired on closing.

KORES (or its affiliate) agreed to arrange for a debt financier to offer to provide financing for 65% of the financing

required to fund capital costs for the purposes of advancing Santo Domingo to commencement of commercial

production as well as fund 30% of the balance of capital requirements based on its equity ownership share. Further,

KORES (or its affiliate) is obligated to purchase, on then prevailing market terms (at the appropriate time), 50% of all

copper concentrate and iron concentrate produced from Santo Domingo over the life of the mine. Lastly, the

Company issued 40,198,632 shares by way of a private placement at C$4.35 per share to a KORES subsidiary for

gross cash proceeds of $178.0 million. As per the agreement, the subscription price of the shares was equal to a 1%

discount to the 5-day volume weighted average price of Capstone for the period ended April 15, 2011.

The partial disposition of Capstone’s ownership interest in the Far West assets to KORES for net cash consideration of

$194.2 million was effected by way of KORES purchasing a 30% equity interest in 0908113 BC Ltd., a subsidiary of

the Company used in connection with the purchase of the Far West net assets. For its 30% interest, KORES paid cash

consideration of $277.4 million, and then Capstone and KORES received loans of cash back (representing their

respective pro rata equity share of the cash balance in 0908113 BC Ltd.) in the form of Canadian denominated non-

interest bearing promissory notes in the amounts of $194.2 million (C$190.9 million) and $82.3 million (C$81.8

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

19

million) respectively, that are due upon demand. The Capstone note is eliminated on consolidation in these

consolidated financial statements given that it is payable to a subsidiary of the Company.

Under the terms of the shareholders’ agreement between Capstone and KORES, it is acknowledged that cash calls will

be funded to the extent possible, first by way of repayment of the promissory note. In September 2011, KORES

funded a cash call for C$5.3 million, reducing its outstanding balance on the promissory note to C$76.5 million.

Details of changes in the balance of the promissory note are as follows (expressed in thousands):

Payment to fund KORES promissory note 83,213$

Repayment of KORES promissory note (5,454)

Currency translation adjustments (2,572)

Balance, December 31, 2011 75,187$

December 31, 2011 December 31, 2010 January 1, 2010

KORES promissory note 75,187$ -$ -$

Less: current portion (12,667) - -

Long-term portion 62,520$ -$ -$

The current portion of the promissory note represents management’s best estimate of the portion of the note that will

be repaid in 2012.

5. Financial instruments

Overview

The Company’s activities expose it to financial risks of varying degrees of significance which could affect its ability to

achieve its strategic objectives for growth and shareholder returns. The principal financial risks to which the Company

is exposed are commodity price risk, credit risk, foreign exchange risk, liquidity risk, and interest rate risk. The Board

of Directors has overall responsibility for the establishment and oversight of the Company’s risk management

framework and reviews the Company’s policies on an ongoing basis.

Commodity price risk

The Company is exposed to commodity price risk given that its revenues are derived from the sale of metals, the prices

for which have been historically volatile. It manages this risk by entering into forward sale agreements with various

counterparties, both as a condition of certain debt facilities as well as to mitigate price risk when management believes

it a prudent decision. Currently the Company has in place derivative contracts for the sale of copper from its Minto

Mine and for the sale of copper, lead and zinc from its Cozamin Mine. Additionally, it has sold forward to Silver

Wheaton Corp. (“Silver Wheaton”) the gold and silver production from the Minto Mine and silver production from the

Cozamin Mine (Note 17).

Credit risk

The Company is exposed to credit risk through its trade receivables on concentrate sales, which are principally with

three counterparties under the terms of off-take agreements described in Note 26. The Company manages this risk by

requiring provisional payments of 90 percent of the value of the concentrate shipped.

The Company enters into derivative instruments with a small number of counterparties, some of which have resulted

in a derivative asset balance at December 31, 2011. These counterparties are large, well diversified multinational

corporations, and credit risk is considered to be minimal.

To mitigate exposure to credit risk on cash and cash equivalents, the Company has established policies to limit the

concentration of credit risk with any given banking institution where the funds are held, to ensure counterparties

demonstrate minimum acceptable credit worthiness and ensure liquity of available funds.

To mitigate exposure to credit risk on the promissory note, the note has been secured against the counterparty’s 30%

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

20

interest in a subsidiary of the Company (Note 4).

As at December 31, 2011, the Company’s maximum exposure to credit risk is the carrying value of its cash and cash

equivalents, restricted cash, receivables, promissory note, notes receivable, and derivative assets.

Foreign exchange risk

The Company is exposed to foreign exchange risk as the Company’s operating costs will be primarily in Canadian

dollars and Mexican Pesos, while revenues will be received in US dollars, hence any fluctuation of the US dollar in

relation to these currencies may impact the profitability of the Company and may also affect the value of the

Company’s assets and liabilities. The Company currently does not enter into financial instruments to manage this risk.

As at December 31, 2011, the Company is exposed to foreign exchange risk through the following assets and liabilities

denominated in currencies other than the functional currency of the applicable subsidiary (expressed in thousands):

US dollar Mexican peso

Cash 79,160$ 12,404$

Receivables and other current assets 4,025 1,797

Deposits and other long-term assets 350 1,201

Derivative instrument asset 3,420 -

Total assets 86,955 15,402

Accounts payable and accrued liabilities 822 3,133

Taxes payable - 572

Deferred income tax liabilities - 14,838

Asset retirement obligations - 7,979

Total liabilities 822 26,522

Net assets (liabilities) 86,133$ (11,120)$

Based on the above net exposures at December 31, 2011, a 10% appreciation of the Canadian dollar vis-à-vis the US

dollar would result in a $8.6 million decrease in the Company’s earnings before income taxes. A 10% appreciation of

the Mexican peso vis-à-vis the US dollar would result in a $1.1 million decrease in the Company’s earnings before

income taxes.

Liquidity risk

The Company has in place a planning and budgeting process to help determine the funds required to ensure the

Company has the appropriate liquidity to meet its operating and growth objectives. The Company maintains adequate

cash balances and credit facilities in order to meet short and long term business requirements, after taking into account

cash flows from operations and believes that these sources will be sufficient to cover the likely short and long term

cash requirements. The Company’s cash is invested in business accounts with Canadian Tier 1 Banks with an AA

Rating or better and which is available on demand for the Company’s programs.

As of December 31, 2011, the Company’s liabilities that have contractual maturities are as follows (expressed in

thousands):

Total 2012 2013-2014 2015-2016 After 2016

Accounts payable and

accrued liabilities 18,699$ 18,699$ -$ -$ -$

Long-term debt 4,487 4,487 - - -

Total* 23,186$ 23,186$ -$ -$ -$

* Amounts above do not include payments related to the Company's reclamation and closure cost obligations and other long term provisions

(Note 19 ).

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

21

Interest rate risk

Currently the Company’s long term liabilities are based on both fixed and variable interest rates. The Company is

exposed to interest rate risk on its variable rate debt facilities, which at December 31, 2011 are undrawn. Variable

interest rates are based on both US dollar and Canadian dollar London Inter-bank Offered Rates (“LIBOR”) plus a

fixed margin. The Company does not enter into derivative contracts to manage this risk.

The Company is also exposed to interest rate risk with respect to the interest it earns on its cash balances.

Financial instruments carrying value and fair value

The Company’s financial instruments consist of cash and cash equivalents, restricted cash, short-term deposits,

receivables, promissory note receivable, investments, notes receivable, accounts payable and accrued liabilities,

advances on concentrate inventories, debt facilities, convertible debentures, and derivative instruments.

The carrying value of receivables, accounts payable and accrued liabilities, and advances on concentrate inventories

approximate their fair values due to their immediate or short-term maturity. Investments that are classified as

available-for-sale are recorded at fair value based on quoted market prices at the reporting date. The fair value of the

Company’s loan facilities are approximated by their carrying values given that the facilities bear interest at variable

rates or, in the case of finance lease obligations, the interest rates have not changed materially.

IFRS 7 establishes a fair value hierarchy that prioritizes the input to valuation techniques used to measure fair value as

follows:

Level 1 – Fair values measured using unadjusted quoted prices in active markets for identical instruments

Level 2 – Fair values measured using directly or indirectly observable inputs, other than those included in Level 1

Level 3 – Fair values measured using inputs that are not based on observable market data

As of December 31, 2011 the Company’s classification of financial instruments within the fair value hierarchy are

summarized below:

Level 1 Level 2 Level 3 Total

Cash and cash equivalents 486,287$ -$ -$ 486,287$

Provisionally priced receivables - 10,978 - 10,978

Investments 237 - - 237

Derivative instrument asset - 3,420 - 3,420

Total Assets 486,524 14,398 - 500,922

Derivative instrument liability - 2,666 - 2,666

Total Liabilities - 2,666 - 2,666

The Company uses valuation models to determine the fair value of its derivative instruments. The inputs to these

models are primarily external observable inputs such as forward prices for metal contracts and the market price of

underlying securities for share purchase warrants.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

22

Set out below are the Company’s financial assets by category:

Fair value through

profit or loss Available-for-sale

Loans and

receivables Total

Cash and cash equivalents 486,287$ -$ -$ 486,287$

Receivables 10,978 - 5,462 16,440

Promissory note - - 75,187 75,187

Derivative instrument asset 3,420 - - 3,420

Investments - 237 - 237

500,685$ 237$ 80,649$ 581,571$

Fair value through

profit or loss Available-for-sale

Loans and

receivables Total

Cash and cash equivalents 165,945$ -$ -$ 165,945$

Restricted cash 6,377 - - 6,377

Short-term deposits 20,039 - - 20,039

Receivables 8,957 - 7,937 16,894

Derivative instrument asset 15,237 - - 15,237

Investments - 2,718 - 2,718

216,555$ 2,718$ 7,937$ 227,210$

Fair value through

profit or loss Available-for-sale

Loans and

receivables Total

Cash and cash equivalents 115,931$ -$ -$ 115,931$

Restricted cash 2,496 - - 2,496

Receivables 3,000 - 4,818 7,818

Investments 1,909 37,196 - 39,105

123,336$ 37,196$ 4,818$ 165,350$

December 31, 2011

December 31, 2010

January 1, 2010

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

23

Set out below are the Company’s financial liabilities by category:

Fair value through

profit or loss

Other financial

liabilities Total

Accounts payable and

accrued liabilities -$ 18,699$ 18,699$

Long-term debt - 4,487 4,487

Derivative instrument liability 2,666 - 2,666

2,666$ 23,186$ 25,852$

Fair value through

profit or loss

Other financial

liabilities Total

Accounts payable and

accrued liabilities -$ 22,277$ 22,277$

Advances on concentrate

inventories - 33,260 33,260

Long-term debt - 11,573 11,573

Derivative instrument liability 51,128 - 51,128

51,128$ 67,110$ 118,238$

Fair value through

profit or loss

Other financial

liabilities Total

Accounts payable and

accrued liabilities -$ 19,782$ 19,782$

Advances on concentrate

inventories - 16,702 16,702

Long-term debt - 20,336 20,336

Derivative instrument liability 55,405 - 55,405

55,405$ 56,820$ 112,225$

December 31, 2011

December 31, 2010

January 1, 2010

6. Short-term deposits

During 2010, the Company invested $20.0 million in a 6-month 5.85% Dual Currency Note (“DCN”) by way of a

private placement with the Bank of Montreal (“BMO”). At maturity on March 1, 2011, the DCN was repaid in US

dollars given that the Bank of Canada USD/CAD foreign exchange rate at the valuation date of February 22, 2011 of

1.0000 USD/CAD had weakened from the strike level of 1.0642 USD/CAD strike level on the date of acquisition.

The principal and interest repaid in US dollars was US$20.6 million.

At December 31, 2010, the DCN was valued in US dollars based on the forward rate of 0.9946 USD/CAD at maturity.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

24

7. Receivables

Details are as follows:

December 31, 2011 December 31, 2010 January 1, 2010

Concentrate 10,978$ 8,957$ 2,999$

Taxes 3,446 2,926 3,060

Other 1,812 3,433 62

Current portion of KORES

promissory note (Note 4) 12,667 - -

Current portion of notes

receivable (Note 11) 196 1,076 825

Total receivables 29,099$ 16,392$ 6,946$

8. Inventories

Details are as follows:

December 31, 2011 December 31, 2010 January 1, 2010

Consumable parts and supplies 10,153$ 8,681$ 7,378$

Ore stockpiles 13,784 24,559 14,259

Concentrates 24,395 33,970 22,801

Total inventories 48,332$ 67,210$ 44,438$

During the year ended December 31, 2011, concentrate inventories recognized as cost of sales amounted to $119.5

million (2010 – $105.6 million).

9. Investments

Details are as follows:

December 31, 2011 December 31, 2010 January 1, 2010

Available-for-sale investments 237$ 2,718$ 37,196$

Derivative investments - - 1,909

Total investments 237$ 2,718$ 39,105$

Available-for-sale investments

During the year ended December 31, 2011, the Company disposed of 6,187,796 shares (2010 – 1,654,500) of Northern

Tiger Resources Inc. for total cash proceeds of $3.0 million (2010 – $1.2 million). The cost base of the shares

disposed was $1.5 million (2010 – $0.4 million), resulting in a gain of $1.5 million (2010 – $0.8 million).

During 2010, the Company disposed of its remaining 1,456,106 shares of Silver Wheaton for total cash proceeds of

$29.2 million. The cost base of the shares disposed was $15.2 million, resulting in a gain of $14.0 million.

Capstone Mining Corp. Notes to Consolidated Financial Statements

Years Ended December 31, 2011 and 2010 (expressed in thousands of US dollars, except share amounts)

25

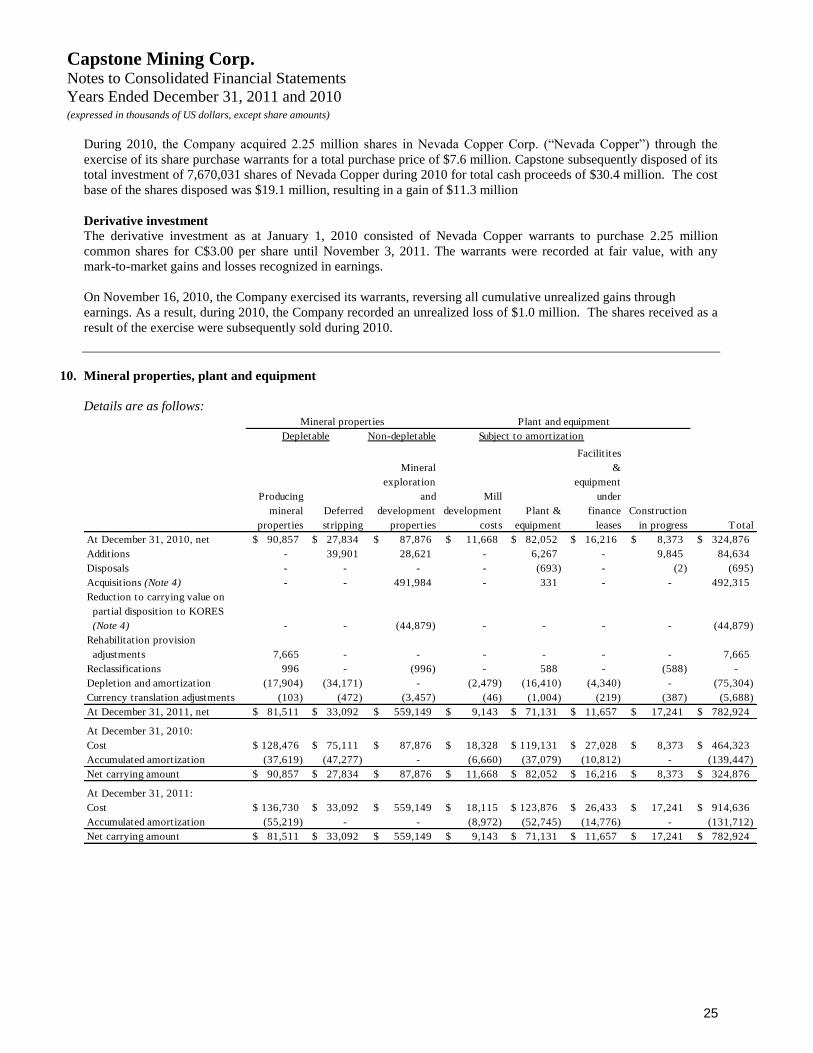

During 2010, the Company acquired 2.25 million shares in Nevada Copper Corp. (“Nevada Copper”) through the

exercise of its share purchase warrants for a total purchase price of $7.6 million. Capstone subsequently disposed of its

total investment of 7,670,031 shares of Nevada Copper during 2010 for total cash proceeds of $30.4 million. The cost

base of the shares disposed was $19.1 million, resulting in a gain of $11.3 million

Derivative investment

The derivative investment as at January 1, 2010 consisted of Nevada Copper warrants to purchase 2.25 million

common shares for C$3.00 per share until November 3, 2011. The warrants were recorded at fair value, with any

mark-to-market gains and losses recognized in earnings.

On November 16, 2010, the Company exercised its warrants, reversing all cumulative unrealized gains through

earnings. As a result, during 2010, the Company recorded an unrealized loss of $1.0 million. The shares received as a

result of the exercise were subsequently sold during 2010.

10. Mineral properties, plant and equipment

Details are as follows:

Non-depletable

Producing

mineral

properties

Deferred

stripping

Mineral

exploration

and

development

properties

Mill

development

costs

Plant &

equipment

Facilitites

&

equipment

under

finance

leases

Construction

in progress Total