consolidated financial statements tokai tokyo financial

TRANSCRIPT

Consolidated Financial Statements

Tokai Tokyo Financial Holdings, Inc.

and Subsidiaries

Year ended March 31, 2020

with Independent Auditor’s Report

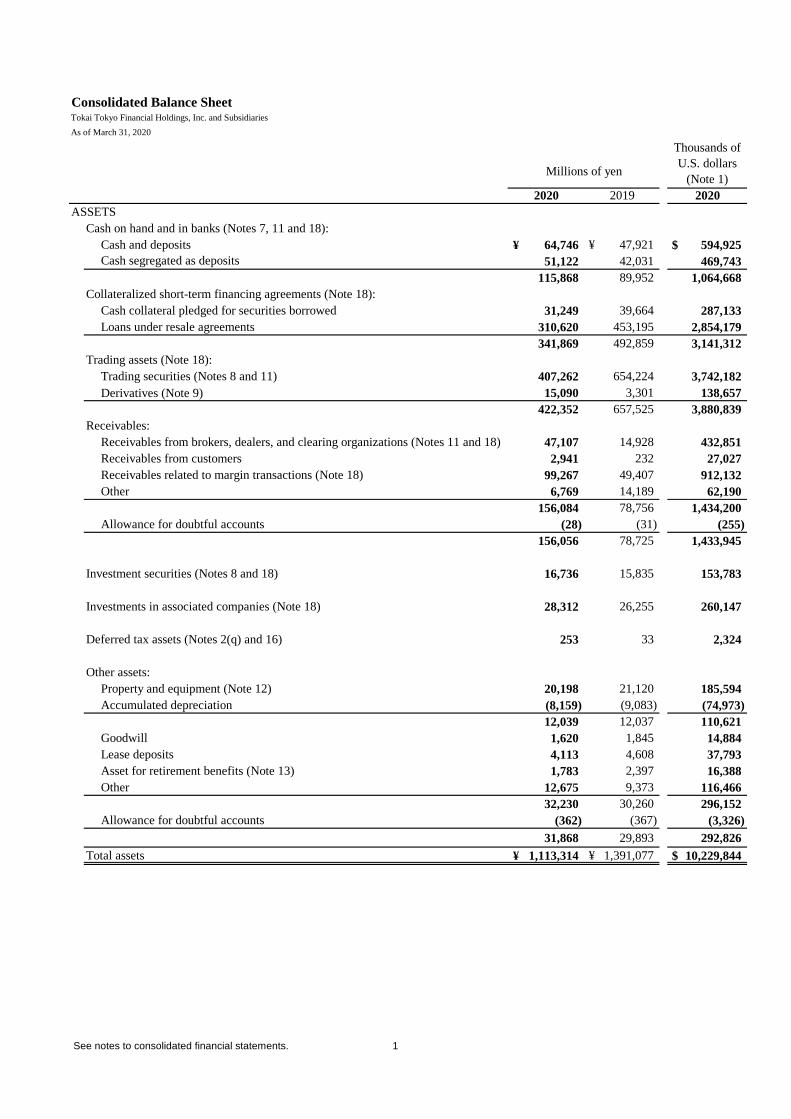

Consolidated Balance SheetTokai Tokyo Financial Holdings, Inc. and Subsidiaries

As of March 31, 2020

ASSETS

Cash on hand and in banks (Notes 7, 11 and 18):

Cash and deposits ¥ 64,746 ¥ 47,921 $ 594,925

51,122 42,031 469,743

115,868 89,952 1,064,668

Collateralized short-term financing agreements (Note 18):

Cash collateral pledged for securities borrowed 31,249 39,664 287,133

Loans under resale agreements 310,620 453,195 2,854,179

341,869 492,859 3,141,312

Trading assets (Note 18):

Trading securities (Notes 8 and 11) 407,262 654,224 3,742,182

Derivatives (Note 9) 15,090 3,301 138,657

422,352 657,525 3,880,839

Receivables:

Receivables from brokers, dealers, and clearing organizations (Notes 11 and 18) 47,107 14,928 432,851

Receivables from customers 2,941 232 27,027

Receivables related to margin transactions (Note 18) 99,267 49,407 912,132

Other 6,769 14,189 62,190

156,084 78,756 1,434,200

Allowance for doubtful accounts (28) (31) (255)

156,056 78,725 1,433,945

Investment securities (Notes 8 and 18) 16,736 15,835 153,783

Investments in associated companies (Note 18) 28,312 26,255 260,147

Deferred tax assets (Notes 2(q) and 16) 253 33 2,324

Other assets:

Property and equipment (Note 12) 20,198 21,120 185,594

Accumulated depreciation (8,159) (9,083) (74,973)

12,039 12,037 110,621

Goodwill 1,620 1,845 14,884

Lease deposits 4,113 4,608 37,793

Asset for retirement benefits (Note 13) 1,783 2,397 16,388

Other 12,675 9,373 116,466

32,230 30,260 296,152

Allowance for doubtful accounts (362) (367) (3,326)

31,868 29,893 292,826

Total assets ¥ 1,113,314 ¥ 1,391,077 $ 10,229,844

Cash segregated as deposits

Thousands of

U.S. dollars

(Note 1)Millions of yen

2020 2019 2020

See notes to consolidated financial statements. 1

Consolidated Balance SheetTokai Tokyo Financial Holdings, Inc. and Subsidiaries

As of March 31, 2020

LIABILITIES AND EQUITY

Borrowings (Notes 10, 11 and 18):

Short-term borrowings ¥ 125,660 ¥ 120,645 $ 1,154,645

Commercial paper 16,000 16,000 147,018

Current portion of long-term debt 31,122 27,765 285,971

Long-term debt 95,406 85,703 876,648

268,188 250,113 2,464,282

Collateralized short-term financing agreements (Notes 11 and 18):

Cash received on securities loaned 12,239 17,789 112,462

Borrowings under repurchase agreements 199,319 327,510 1,831,467

211,558 345,299 1,943,929

Trading liabilities (Note 18):

Trading securities (Note 8) 330,162 540,358 3,033,739

Derivatives (Note 9) 11,255 6,142 103,418

341,417 546,500 3,137,157

Payables (Note 18):

Payables to brokers, dealers, and clearing organizations 50,366 16,170 462,794

Payables to customers 48,173 33,430 442,642

Payables related to margin transactions (Note 11) 8,944 11,656 82,182

Other 15,674 13,698 144,031

123,157 74,954 1,131,649

Deferred tax liabilities (Notes 2(q) and 16) 56 389 514

Accrued and other liabilities:

Income taxes payable 695 349 6,389

Provision for bonuses 1,522 2,016 13,983

Liability for retirement benefits (Note 13) 245 267 2,254

Other 5,452 6,271 50,092

7,914 8,903 72,718

Statutory reserves 619 619 5,690

Total liabilities 952,909 1,226,777 8,755,939

Equity (Notes 14, 15 and 25)

Common stock:

Authorized: 972,730,000 shares

Issued: 36,000 36,000 330,791

Capital surplus 24,588 28,962 225,926

Stock acquisition rights 479 540 4,400

Retained earnings 101,277 100,541 930,596

(5,292) (6,183) (48,628)

Accumulated other comprehensive income:

Unrealized (loss) gain on available-for-sale securities (152) 1,077 (1,392)

Foreign currency translation adjustments (391) (406) (3,588)

Defined retirement benefit plans 500 1,501 4,595

Total 157,009 162,032 1,442,700

Noncontrolling interests 3,396 2,268 31,205

Total equity 160,405 164,300 1,473,905

Total liabilities and equity ¥ 1,113,314 ¥ 1,391,077 $ 10,229,844

Treasury stock, at cost: 12,216,596 shares in 2020

and 12,215,435 shares in 2019

260,582,115 shares in 2020

Thousands of

U.S. dollars

(Note 1)Millions of yen

2020 2019 2020

and 270,582,115 shares in 2019

See notes to consolidated financial statements. 2

Consolidated Statement of IncomeTokai Tokyo Financial Holdings, Inc. and Subsidiaries

For the year ended March 31, 2020

Revenues:

Commissions (Note 19) ¥ 29,172 ¥ 28,954 $ 268,054

Net gain on trading (Note 4) 29,511 32,179 271,162

Interest and dividend income (Note 4) 3,012 3,639 27,674

Total revenues 61,695 64,772 566,890

Interest expense 1,927 2,219 17,705

Net revenues 59,768 62,553 549,185

Selling, general and administrative expenses (Note 20) 60,592 62,945 556,756

Operating loss (824) (392) (7,571)

Other income, net (Note 21) 3,873 1,920 35,589

Income before income taxes 3,049 1,528 28,018

Income taxes (Note 16):

Current 273 605 2,512

Prior years (46) (141) (427)

Deferred 60 (88) 553

Total income taxes 287 376 2,638

Net income 2,762 1,152 25,380

Net (loss) income attributable to noncontrolling interests (1) 72 (9)

Net income attributable to owners of the parent ¥ 2,763 ¥ 1,080 $ 25,389

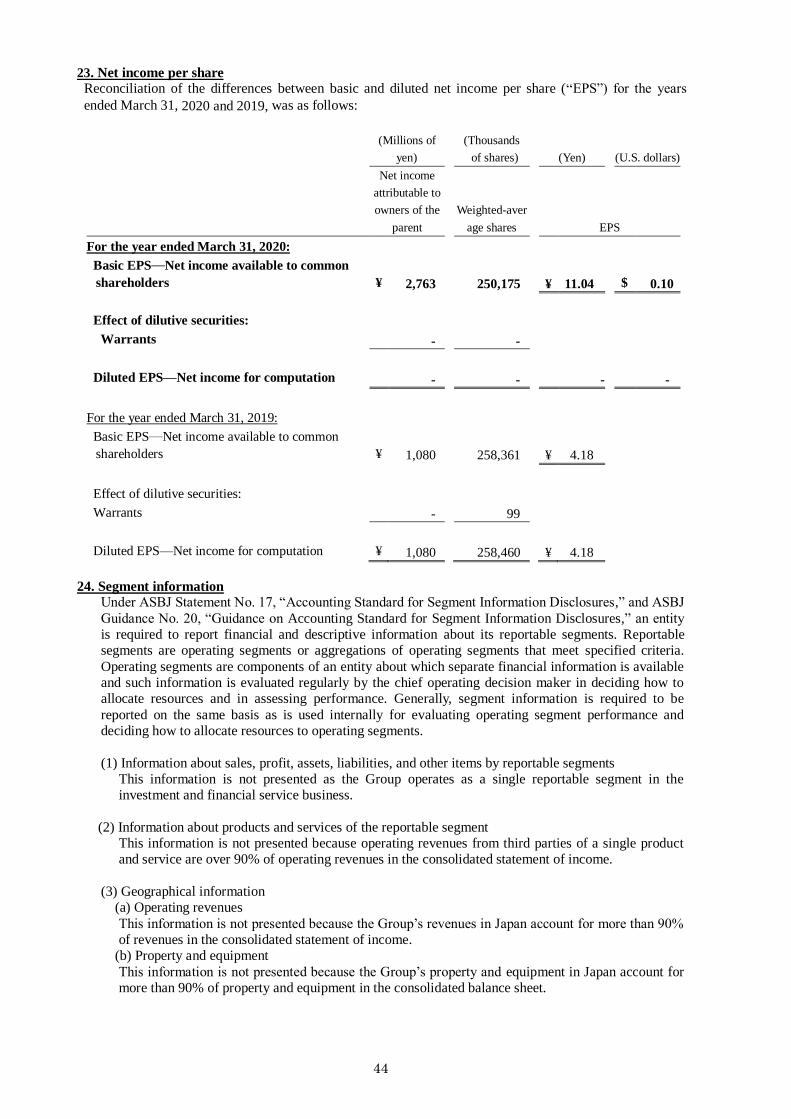

Per share of common stock (Notes 2(t) and 23): U.S. dollars

Basic net income ¥ 11.04 ¥ 4.18 $ 0.10

Diluted net income - 4.18 -

Cash dividends applicable to the year 8.00 16.00 0.07

Thousands of

U.S. dollars

(Note 1)Millions of yen

2020 2019 2020

Yen

See notes to consolidated financial statements. 3

Consolidated Statement of Comprehensive Income

Tokai Tokyo Financial Holdings, Inc. and Subsidiaries

For the year ended March 31, 2020

Net income ¥ 2,762 ¥ 1,152 $ 25,380

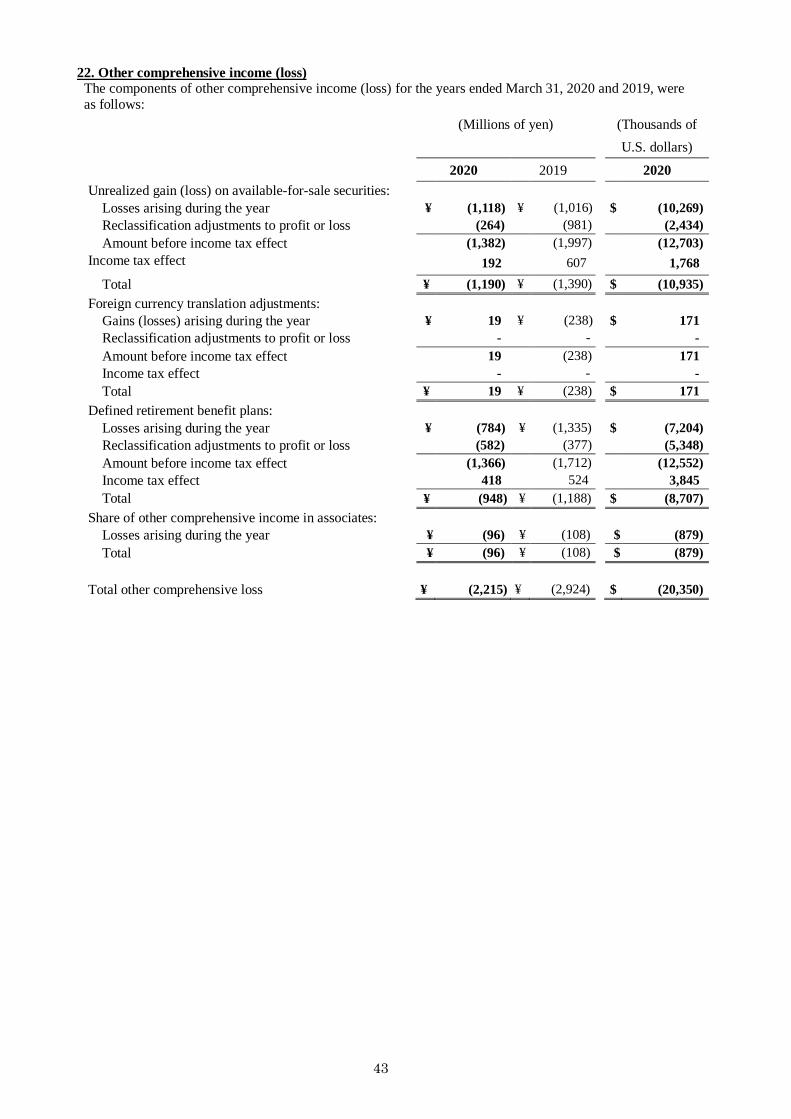

Other comprehensive income (Note 22):

Unrealized loss on available-for-sale securities (1,190) (1,390) (10,935)

Foreign currency translation adjustments 19 (238) 171

Defined retirement benefit plans (948) (1,188) (8,707)

Share of other comprehensive income in associates (96) (108) (879)

Comprehensive income (loss) ¥ 547 ¥ (1,772) $ 5,030

Total comprehensive income (loss) attributable to (Note 22):

Owners of the parent ¥ 548 ¥ (1,844) $ 5,039

Noncontrolling interests (1) 72 (9)

Millions of yen

Thousands of

U.S. dollars

(Note 1)

2020 2019 2020

See notes to consolidated financial statements. 4

Consolidated Statement of Changes in Equity

Tokai Tokyo Financial Holdings, Inc. and Subsidiaries

For the year ended March 31, 2020

Common Treasury

stock stock

Balance as of April 1, 2018 270,582 12,225 ¥ 36,000 ¥ 28,959 ¥ 556 ¥ 108,761 ¥ (6,188) ¥ 2,520 ¥ (168) ¥ 2,745 ¥ 173,185 ¥ 1,664 ¥ 174,849

Net income attributable to owners of the parent - - - - - 1,080 - - - - 1,080 - 1,080

Cash dividends, ¥36.00 per share - - - - - (9,300) - - - - (9,300) - (9,300)

Purchase of treasury stock - 2 - - - - (1) - - - (1) - (1)

Disposal of treasury stock - (12) - 3 - - 6 - - - 9 - 9

Cancellation of treasury stock - - - - - - - - - - - - -

Change in the parent's ownership interest due to transactions

with noncontrolling interests- - - - - - - - - - - - -

Net change in the year - - - - (16) - - (1,443) (238) (1,244) (2,941) 604 (2,337)

Balance as of March 31, 2019 270,582 12,215 ¥ 36,000 ¥ 28,962 ¥ 540 ¥ 100,541 ¥ (6,183) ¥ 1,077 ¥ (406) ¥ 1,501 ¥ 162,032 ¥ 2,268 ¥ 164,300

Net income attributable to owners of the parent - - - - - 2,763 - - - - 2,763 - 2,763

Cash dividends, ¥8.00 per share - - - - - (2,027) - - - - (2,027) - (2,027)

Purchase of treasury stock - 10,001 - - - - (3,441) - - - (3,441) - (3,441)

Disposal of treasury stock - 0 - (0) - - 0 - - - 0 - 0

Cancellation of treasury stock (10,000) (10,000) - (4,332) - - 4,332 - - - - - -

Change in the parent's ownership interest due to transactions

with noncontrolling interests- - - (42) - - - - - - (42) - (42)

Net change in the year - - - - (61) - - (1,229) 15 (1,001) (2,276) 1,128 (1,148)

Balance as of March 31, 2020 260,582 12,216 ¥ 36,000 ¥ 24,588 ¥ 479 ¥ 101,277 ¥ (5,292) ¥ (152) ¥ (391) ¥ 500 ¥ 157,009 ¥ 3,396 ¥ 160,405

Balance as of March 31, 2019 $ 330,791 $ 266,118 $ 4,962 $ 923,832 $ (56,817) $ 9,900 $ (3,726) $ 13,791 $ 1,488,851 $ 20,846 $ 1,509,697

Net income attributable to owners of the parent - - - 25,389 - - - - 25,389 - 25,389

Cash dividends, $0.07 per share - - - (18,625) - - - - (18,625) - (18,625)

Purchase of treasury stock - - - - (31,616) - - - (31,616) - (31,616)

Disposal of treasury stock - (0) - - 0 - - - 0 - 0

Cancellation of treasury stock - (39,805) - - 39,805 - - - - - -

Change in the parent's ownership interest due to transactions

with noncontrolling interests- (387) - - - - - - (387) - (387)

Net change in the year - - (562) - - (11,292) 138 (9,196) (20,912) 10,359 (10,553)

Balance as of March 31, 2020 $ 330,791 $ 225,926 $ 4,400 $ 930,596 $ (48,628) $ (1,392) $ (3,588) $ 4,595 $ 1,442,700 $ 31,205 $ 1,473,905

Thousands of shares Millions of yen

Accumulated other comprehensive income

Unrealized Foreign Defined

retirement

Common Capital acquisition Retained Treasury available-for-sale translation

Stock (loss) gain on currency

benefit Noncontrolling Total

stock surplus rights earnings stock securities adjustments plans Total interests equity

Thousands of U.S. dollars (Note 1)

Accumulated other comprehensive income

Unrealized Foreign Defined

retirement

Common Capital acquisition Retained Treasury available-for-sale translation

Stock (loss) gain on currency

benefit Noncontrolling Total

stock Surplus rights earnings stock securities adjustments plans Total interests equity

See notes to consolidated financial statements. 5

Consolidated Statement of Cash FlowsTokai Tokyo Financial Holdings, Inc. and Subsidiaries

For the year ended March 31, 2020

Cash flows from operating activities:

Income before income taxes ¥ 3,049 ¥ 1,528 $ 28,018

Income taxes - refund (paid) 232 (5,041) 2,128

Depreciation and amortization 3,227 2,322 29,650

Amortization of goodwill 252 245 2,318

Decrease in allowance for doubtful accounts (7) (39) (69)

Decrease in liability for retirement benefits (827) (630) (7,600)

Increase in provision for statutory reserves 1 7 5

Equity in losses of associated companies 94 62 864

Gain on sales of investment securities (107) (1,466) (983)

Gain on change in equity (2,055) - (18,879)

Gains on sales of fixed assets (144) - (1,320)

Impairment loss on fixed assets 1 152 11

Impairment loss on investment securities 121 258 1,113

Gain on reversal of stock acquisition rights (167) (139) (1,530)

Special retirements benefits - 598 -

Changes in assets and liabilities, net of effects from:

(Increase) Decrease in receivables (75,102) 3,981 (690,087)

Increase (Decrease) in payables 48,034 (19,668) 441,368

Changes in Trading assets and liabilities 30,104 (5,235) 276,617

Changes in Collateralized short-term financing agreements 17,460 (55,980) 160,435

Other, net (13,221) 6,294 (121,488)

Total adjustments 7,896 (74,279) 72,553

Net cash provided by (used in) operating activities 10,945 (72,751) 100,571

Cash flows from investing activities:

Purchases of property and equipment (2,589) (4,915) (23,792)

Proceeds from sales of property and equipment 452 - 4,161

Purchases of investment securities (14,392) (2,928) (132,241)

Proceeds from sales of investment securities 12,394 5,327 113,880

Purchases of a share of associates (45) (5,040) (415)

Proceed from sales of associates - 53 -

Other, net (2,507) (2,113) (23,034)

Net cash used in investing activities (6,687) (9,616) (61,441)

Cash flows from financing activities:

Increase in short-term borrowings - net 5,016 42,144 46,092

Proceeds from long-term debt 61,182 48,925 562,184

Repayment of long-term debt (48,169) (46,418) (442,610)

Proceeds from commercial paper 72,500 74,000 666,177

Redemption of commercial paper (72,500) (70,000) (666,177)

Proceeds from exercise of stock options - 8 -

Purchases of treasury stock (3,440) - (31,612)

Net increase in treasury stock (0) (1) (4)

Cash dividends paid (2,017) (9,300) (18,531)

Subscription money received from the noncontrolling interests 6,324 540 58,111

Payments of cash dividends to noncontrolling interests (7) (8) (69)

Payments from changes in ownership interests in subsidiaries (77) - (708)

that do not result in change in scope of consolidation

Other, net (584) (194) (5,366)

Net cash provided by financing activities 18,228 39,696 167,487

Effect of exchange rate change on cash and cash equivalents (12) (259) (107)

Net increase (decrease) in cash and cash equivalents 22,474 (42,930) 206,510

(5,547) - (50,973)

Cash and cash equivalents at the beginning of year 46,274 89,204 425,199

Cash and cash equivalents at the end of year (Note 7) ¥ 63,201 ¥ 46,274 $ 580,736

Decrease in cash and cash equivalents

resulting from change of scope of consolidation

Adjustments for:

Thousands of

U.S. dollars

(Note 1)Millions of yen

2020 2019 2020

See notes to consolidated financial statements. 6

7

Notes to Consolidated Financial Statements Tokai Tokyo Financial Holdings, Inc. and Subsidiaries

Year ended March 31, 2020

1. Basis of presentation of consolidated financial statements

The accompanying consolidated financial statements have been prepared by Tokai Tokyo Financial

Holdings, Inc. (the “Company”) and its subsidiaries (collectively, the “Group”) in accordance with the

provisions set forth in the Japanese Financial Instruments and Exchange Act and its related accounting

regulations, and in accordance with accounting principles generally accepted in Japan (“Japanese

GAAP”), which are different in certain respects as to the application and disclosure requirements of

International Financial Reporting Standards (IFRS).

In preparing these consolidated financial statements, certain reclassifications and rearrangements have

been made to the consolidated financial statements issued in Japan in order to present them in a form

which is more familiar to readers outside Japan. In addition, certain reclassifications have been made in

the 2019 consolidated financial statements to conform to the classifications used in 2020.

The consolidated financial statements are stated in Japanese yen, the currency of the country in which

the Company is incorporated and operates. The translation of Japanese yen amounts into U.S. dollars is

included solely for the convenience of readers outside Japan, using the prevailing exchange rate at

March 31, 2020, which was ¥108.83 to USD1. The amounts in Japanese yen are directly converted into

U.S. dollar amounts even for the amounts presented only in millions of Japanese yen in the consolidated

financial statements. As such, there are cases in which the conversion of the amounts in millions of

Japanese yen using the prevailing exchange rate are different from those in U.S. dollars shown in the

consolidated financial statements. The translation should not be construed as a representation that the

Japanese yen amounts have been, could have been or could be converted into U.S. dollars at that or any

other rate.

2. Summary of significant accounting policies

a. Principles of consolidation The consolidated financial statements as of March 31, 2020, include the accounts of the Company and its

27 (26 in 2019) subsidiaries. Three consolidated subsidiaries, which were newly established for the year

ended March 31, 2020, were included in the scope of consolidation. One consolidated subsidiary was

excluded from the scope of consolidation and included in associated companies accounted for using the

equity method. Another consolidated subsidiary was also merged and therefore excluded from the scope

of consolidation in the year ended March 31, 2020.

Under the control and influence concepts, those companies in which the Company, directly or indirectly,

is able to exercise control over operations are fully consolidated, and those companies over which the

Group has the ability to exercise significant influence are accounted for by the equity method.

Investments in 12 (10 in 2019) associated companies are accounted for by the equity method. One

consolidated subsidiary, which was excluded from the scope of consolidation, was included in

associated companies accounted for using the equity method.Another associated company was included

in the scope of application of the equity method from the year ended March 31, 2020, as it was become

material.

Cost in excess of the net assets of subsidiaries acquired is amortized on a straight-line basis within a

period of 20 years by judging each respective case.

All significant intercompany balances and transactions have been eliminated in consolidation. All

material unrealized profit included in assets resulting from transactions within the Group is eliminated.

b. Unification of accounting policies applied to foreign subsidiaries for the consolidated financial

statements

Under Accounting Standards Board of Japan (“ASBJ”) Practical Issues Task Force (PITF) No. 18,

“Practical Solution on Unification of Accounting Policies Applied to Foreign Subsidiaries for the

8

Consolidated Financial Statements” the accounting policies and procedures applied to a parent company

and its subsidiaries for similar transactions and events under similar circumstances should in principle be

unified for the preparation of the consolidated financial statements. However, financial statements

prepared by foreign subsidiaries in accordance with either IFRS or generally accepted accounting

principles in the United States of America (FASB Accounting Standards Codification) tentatively may be

used for the consolidation process, except for the following items that should be adjusted in the

consolidation process so that net income is accounted for in accordance with Japanese GAAP, unless

they are not material: (a) amortization of goodwill; (b) scheduled amortization of actuarial gains or

losses of pensions that have been directly recorded in equity through other comprehensive income; (c)

expensing capitalized development costs of R&D; (d) cancellation of the fair value model of accounting

for property, plant and equipment and investment properties and incorporation of the cost model of

accounting; and (e) recording a gain or loss through profit or loss on the sale of an investment in an

equity instrument for the difference between the acquisition cost and selling price, and recording

impairment loss through profit or loss for other-than-temporary declines in the fair value of an

investment in an equity instrument, where a foreign subsidiary elects to present in other comprehensive

income subsequent changes in the fair value of an investment in an equity instrument.

c. Unification of accounting policies applied to foreign associated companies for the equity method ASBJ Statement No. 16, “Accounting Standard for Equity Method of Accounting for Investments”

requires adjustments to be made to conform the associate’s accounting policies for similar transactions

and events under similar circumstances to those of the parent company when the associate’s financial

statements are used in applying the equity method, unless it is impracticable to determine the necessary

adjustments. In addition, financial statements prepared by foreign associated companies in accordance

with either IFRS or generally accepted accounting principles in the United States of America tentatively

may be used in applying the equity method if the following items are adjusted so that net income is

accounted for in accordance with Japanese GAAP, unless they are not material: (a) amortization of

goodwill; (b) scheduled amortization of actuarial gain or loss of pensions that has been directly

recorded in equity through other comprehensive income; (c) expensing capitalized development costs of

research and development (R&D); (d) cancellation of the fair value model of accounting for property,

plant and equipment and investment properties and incorporation of the cost model of accounting; and

(e) recording a gain or loss through profit or loss on the sale of an investment in an equity instrument

for the difference between the acquisition cost and selling price, and recording impairment loss through

profit or loss for other-than-temporary declines in the fair value of an investment in an equity

instrument, where a foreign associate elects to present in other comprehensive income subsequent

changes in the fair value of an investment in an equity instrument.

d. Business combinations Business combinations are accounted for using the purchase method. Acquisition-related costs, such as

advisory fees or professional fees are accounted for as expenses in the periods in which the costs are

incurred. If the initial accounting for a business combination is incomplete by the end of the reporting

period in which the business combination occurs, an acquirer shall report in its financial statements

provisional amounts for the items for which the accounting is incomplete. During the measurement

period, which shall not exceed one year from the acquisition, the acquirer shall retrospectively adjust

the provisional amounts recognized at the acquisition date to reflect new information obtained about

facts and circumstances that existed as of the acquisition date and that would have affected the

measurement of the amounts recognized as of that date. Such adjustments shall be recognized as if the

accounting for the business combination had been completed at the acquisition date. The acquirer

recognizes the bargain purchase gain in profit or loss immediately on the acquisition date after

reassessing and confirming that all of the assets acquired and all of the liabilities assumed have been

identified after a review of the procedures used in the purchase price allocation. A parent's ownership

interest in a subsidiary might change if the parent purchases or sells ownership interests in its subsidiary.

The carrying amount of noncontrolling interests is adjusted to reflect a change in the parent's ownership

interest in its subsidiary while the parent retains its controlling interest in its subsidiary. Any difference

between the fair value of the consideration received or paid and the amount by which the noncontrolling

interest is adjusted is accounted for as capital surplus as long as the parent retains control over its

subsidiary.

e. Cash and cash equivalents

Cash and cash equivalents disclosed in the consolidated statement of cash flows comprise cash on hand,

9

demand deposits and ordinary deposits which can be easily liquidated on demand with original

maturities of three months or less.

f. Financial instruments The purpose of trading activities is to make profits or reduce losses from short-term volatility and

arbitrage between markets in stock prices, interest rates, foreign exchange rates and other market

indices. The scope of trading activities mainly consists of the following:

1) Buying and selling of securities

2) Derivative market transactions

3) Over-the-counter (OTC) derivative transactions

Securities, derivative contracts and other financial instruments classified as trading assets and liabilities

are stated at fair value based on the mark-to-market method.

Other securities, including short-term investment securities and investment securities, are held for

non-trading purposes and are classified as available-for-sale. Available-for-sale securities that have a

market quotation are stated at the market price prevailing at the end of the fiscal year. Differences

between the cost of securities held determined by the moving-average method and the fair value less

associated deferred taxes are recorded in “Unrealized gain (loss) on available-for-sale securities” in

equity in the consolidated balance sheet. Available-for-sale securities without a market quotation are

stated at cost as determined by the moving average. Where available-for-sale securities have declined

significantly and such impairment of value is deemed not temporary, such securities are written down to

their fair value and the resulting losses are charged to income for the period.

g. Property and equipment Property and equipment are stated at cost. Depreciation of tangible fixed assets is calculated by the

declining-balance method based on the estimated useful lives of the assets. However, buildings

(excluding leasehold improvements) acquired by the Company and its domestic consolidated

subsidiaries on or after April 1, 1998, and leasehold improvements and structures acquired on or after

April 1, 2016 are depreciated by the straight-line method. The estimated useful lives of tangible fixed

assets are mainly as follows:

Buildings 2-50 years

Fixtures and furniture 2-20 years

h. Long-lived assets The Group reviews its long-lived assets for impairment whenever events or changes in circumstances

indicate the carrying amount of an asset or asset group may not be recoverable. An impairment loss is

recognized if the carrying amount of an asset or asset group exceeds the sum of the undiscounted future

cash flows expected to result from the continued use and eventual disposition of the asset or asset group.

The impairment loss would be measured as the amount by which the carrying amount of the asset

exceeds its recoverable amount, which is the higher of the discounted cash flows from the continued use

and eventual disposition of the asset or the net selling price at disposition.

i. Intangible fixed assets

Amortization of intangible fixed assets is calculated by the straight-line method. Software for internal

use is amortized by the straight-line method over its economic useful life (five years).

Intangible fixed assets recognized in the acquisition of subsidiaries are amortized over the estimated

useful life reflecting the pattern of the assets’ future economic benefits.

j. Allowance for doubtful accounts For the future loss from doubtful accounts, an allowance for doubtful accounts is recognized using the

historical rate of actual losses for normal receivables and the estimated non-recoverable amount for

specific doubtful receivables after considering the recoverability of each account.

k. Retirement and pension plan The Company and its domestic subsidiaries have defined benefit corporate pension plans and defined

contribution retirement plan. There are some cases in which extra retirement benefits are paid to

employees when they retire. Tokai Tokyo Securities Co., Ltd. (“Tokai Tokyo Securities”), a wholly

owned major subsidiary of the Company, contributed to the retirement benefit trust for its pension plan.

10

Certain domestic consolidated subsidiaries apply the simplified method to state the liability based on the

amount that would be paid if employees retired at the consolidated balance sheet date.

The Company accounts for the liability for retirement benefits based on the projected benefit

obligations and plan assets at the balance sheet date. The projected benefit obligations are attributed to

periods on a straight-line basis. Actuarial gains and losses and past service costs that are yet to be

recognized in profit or loss are recognized within equity (accumulated other comprehensive income),

after adjusting for tax effects and are recognized in profit or loss over 10 years, no longer than the

expected average remaining service period of the employees. The discount rate is determined using a

single weighted average discount rate reflecting the estimated timing and amount of benefit payment.

Certain subsidiaries record retirement benefits for directors and Audit & Supervisory Board members at

the amount that would be required if all directors and Audit & Supervisory Board members retired at

each consolidated balance sheet date.

l. Asset retirement obligations An asset retirement obligation is recorded for a legal obligation imposed either by law or contract that

results from the acquisition, construction, development and the normal operation of a tangible fixed

asset and is associated with the retirement of such tangible fixed asset. The asset retirement obligation is

recognized as the sum of the discounted cash flows required for the future asset retirement and is

recorded in the period in which the obligation is incurred if a reasonable estimate can be made. If a

reasonable estimate of the asset retirement obligation cannot be made in the period the asset retirement

obligation is incurred, the liability should be recognized when a reasonable estimate of the asset

retirement obligation can be made. Upon initial recognition of a liability for an asset retirement

obligation, an asset retirement cost is capitalized by increasing the carrying amount of the related fixed

asset by the amount of the liability. The asset retirement cost is subsequently allocated to expense

through depreciation over the remaining useful life of the asset. Over time, the liability is accreted to its

present value each period. Any subsequent revisions to the timing or the amount of the original estimate

of undiscounted cash flows are reflected as an adjustment to the carrying amount of the liability and the

capitalized amount of the related asset retirement cost.

m. Statutory reserves The Japanese Financial Instruments and Exchange Act and its related regulations require a securities

company to set aside a reserve in proportion to its securities transactions and other related trading to

cover future eventual operational losses caused by the securities company for customer transactions.

n. Stock options

The cost of employee stock options is measured based on the fair value at the date of grant and

recognized as compensation expense over the vesting period as consideration for receiving goods or

services. In the consolidated balance sheet, stock options are presented as stock acquisition rights as a

separate component of equity until exercised.

o. Leases

In March 2007, the ASBJ issued ASBJ Statement No. 13, “Accounting Standard for Lease Transactions,”

which revised the previous accounting standard for lease transactions.

Under the previous accounting standard, finance leases that were deemed to transfer ownership of the

leased property to the lessee were capitalized. However, other finance leases were permitted to be

accounted for as operating lease transactions if certain “as if capitalized” information was disclosed in

the notes to the lessee’s financial statements. The revised accounting standard permits leases that existed

at the transition date and that do not transfer ownership of the leased property to the lessee to continue

to be accounted for as operating lease transactions.

The Group applied the revised accounting standard effective April 1, 2008. In addition, the Group

continues to account for leases that existed at the transition date and do not transfer ownership of the

leased property to the lessee as operating lease transactions. All other leases are accounted for as

operating leases.

p. Bonuses to directors and Audit & Supervisory Board members Bonuses to directors and Audit & Supervisory Board members are accrued at the end of the year to

11

which such bonuses are attributable.

q. Income taxes The provision for income taxes is computed based on the pretax income included in the consolidated

statement of income. The asset and liability approach is used to recognize deferred tax assets and

liabilities for the expected future tax consequences of temporary differences between the carrying

amounts and the tax bases of assets and liabilities. Deferred taxes are measured by applying currently

enacted income tax rates to the temporary differences.

The Group files a tax return under the consolidated corporate-tax system, which allows companies to

base tax payments on the combined profits or losses of the parent company and its wholly-owned

domestic subsidiaries.

A transition was performed to a group tax sharing system established in the “Act for Partial Amendment

of the Income Tax, etc.” (Act. 8 of 2020) and there was a review on the transition to a non-consolidated

taxation system in line with the group tax sharing system. For the items subject to such transition or the

review, the Company and certain consolidated subsidiaries in Japan do not apply the provisions of (44)

of ASBJ Guidance No. 28, “Implementation Guidance on Tax Effect Accounting” in accordance with

the treatment under Paragraph (3) of ASBJ PITF No. 39, “Treatment of Tax Effect Accounting for the

Transition from the Consolidated Taxation System to the Group Tax Sharing System” (March 31, 2020).

The amounts of deferred tax assets and deferred tax liabilities are based on the provisions of the Tax Act

prior to the amendment.

r. Foreign currency transactions

All short-term and long-term monetary receivables and payables denominated in foreign currencies are

translated into Japanese yen at the exchange rates at the consolidated balance sheet date. The foreign

exchange gains and losses from translation are recognized in the consolidated statement of income to

the extent that they are not hedged by forward exchange contracts.

s. Foreign currency financial statements The balance sheet and statement of income accounts of the consolidated foreign subsidiaries are

translated into Japanese yen at the current exchange rate as of the balance sheet date except for equity,

which is translated at the historical rate. Differences arising from such translation are shown as “Foreign

currency translation adjustments” under accumulated other comprehensive income in a separate

component of equity.

t. Per share information

Basic net income per share is computed by dividing net income attributable to common shareholders by

the weighted-average number of common shares outstanding for the period, retroactively adjusted for

stock splits.

Diluted net income per share reflects the potential dilution that could occur if securities were exercised

or converted into common stock. Diluted net income per share of common stock assumes full

conversion of the outstanding convertible notes and bonds at the beginning of the year (or at the time of

issuance) with an applicable adjustment for related interest expense, net of tax, and full exercise of

outstanding warrants.Diluted net income per share is not disclosed because it is anti-dilutive for the year

ended March 31, 2020.

Cash dividends per share presented in the accompanying consolidated statement of income are

dividends applicable to the respective fiscal years, including dividends to be paid after the end of the

year.

u. Accounting changes and error corrections

Under Statement No. 24, “Accounting Standard for Accounting Changes and Error Corrections,” and

ASBJ Guidance No. 24, “Guidance on Accounting Standard for Accounting Changes and Error

Corrections,” accounting treatments are required as follows: (1) Changes in Accounting

Policies―When a new accounting policy is applied following a revision of an accounting standard, the

new policy is applied retrospectively unless the revised accounting standard includes specific

12

transitional provisions, in which case the entity shall comply with the specific transitional provisions.

(2) Changes in Presentation―When the presentation of financial statements is changed, prior-period

financial statements are reclassified in accordance with the new presentation. (3) Changes in

Accounting Estimates―A change in an accounting estimate is accounted for in the period of the change

if the change affects that period only and is accounted for prospectively if the change affects both the

period of the change and future periods. (4) Corrections of Prior-Period Errors―When an error in

prior-period financial statements is discovered, those statements are restated.

v. New accounting pronouncement

(1) Revenue Recognition

On March 30, 2018, the ASBJ issued ASBJ Statement No. 29, “Accounting Standard for Revenue

Recognition,” and ASBJ Guidance No. 30, “Implementation Guidance on Accounting Standard for

Revenue Recognition.” The core principle of the standard and guidance is that an entity should

recognize revenue to depict the transfer of promised goods or services to customers in an amount that

reflects the consideration to which the entity expects to be entitled in exchange for those goods or

services. An entity should recognize revenue in accordance with that core principle by applying the

following steps:

Step 1: Identify the contract(s) with a customer

Step 2: Identify the performance obligations in the contract

Step 3: Determine the transaction price

Step 4: Allocate the transaction price to the performance obligations in the contract

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

The accounting standard and guidance are effective for annual periods beginning on or after April 1,

2021. Earlier application is permitted for annual periods beginning on or after April 1, 2018.

The Company expects to apply the accounting standard and guidance for annual periods beginning on

or after April 1, 2021, and is in the process of measuring the effects of applying the accounting standard

and guidance in future applicable periods.

(2) Fair Value Measurement

On July 4, 2019, the ASBJ issued ASBJ Statement No. 30, "Accounting Standard for Fair Value

Measurement" and ASBJ Guidance No. 31, "Implementation Guidance on Accounting Standard for Fair

Value Measurement," and revised related ASBJ Statements and ASBJ Guidance (the "New Accounting

Standards"). Under the New Accounting Standards, nonmarketable available-for-sale equity securities

are stated at cost, while under the current accounting standards, nonmarketable available-for-sale

securities are stated at cost.

The New Accounting Standards are effective for the annual periods beginning on or after April 1, 2021.

Earlier application is permitted for annual periods beginning on or after April 1, 2020, or annual periods

ending on or after March 31, 2020. The New Accounting Standards shall be applied prospectively,

however, under certain circumstances, it is permitted to be applied retrospectively.

The Company expects to apply the accounting standard and guidance for annual periods beginning on

or after April 1, 2021 and is in the process of measuring the effects of applying the accounting standards

and guidance in future applicable periods.

(3) Accounting Policy Disclosures, Accounting Changes and Error Corrections On March 31, 2020, the ASBJ issued ASBJ Statement No.24 (revised 2020) “Accounting Standard for

Accounting Policy Disclosures, Accounting Changes and Error Corrections.”

The core principle of the standard is that an entity should disclose the principle and the outline of the

adopted accounting treatment for those which are not clearly stated in the related accounting standards.

The Company expects to apply the accounting standard on and after March 31, 2021.

(4) Disclosure of Accounting Estimates

On March 31, 2020, the ASBJ issued ASBJ Statement No. 31 “Accounting Standard for Disclosure of

13

Accounting Estimates.”

The core principle of the standard is that an entity should disclose the useful information for the users of

the financial statements regarding the accounting estimates reflected to the financial statements for the

current fiscal year involving risks which may significantly impact the financial statements for the

following fiscal year.

The Company expects to apply the accounting standard on and after March 31, 2021.

14

3. Accounting Change Starting from the fiscal year ended March 31, 2020, the consolidated subsidiaries of the Company

which adopt IFRS has adopted IFRS 16, “Lease” and recognize the right of use asset and the lease

liability at the date of the initial application for the leases that the Company as lessee. The effect of the

change is immaterial.

4. Change in Presentation

Prior to the fiscal year ended March 31, 2020, the derivative gain and loss related to the bonds issued

by the Group was included in “Interest and dividend income” or “Interest expense” in the Consolidated

Statement of Income. Since during this fiscal year ended March 31, 2020, the amount increased

significantly due to the business diversification, such amount is disclosed in “Net gain on trading” of

the Consolidated Statement of Income for the year ended March 31, 2020. The amount included in

“Interest and dividend income” for the fiscal year ended March 31, 2019, was ¥1,899 million.

5. Business Combination

Merger between consolidated subsidiaries

Based on the resolution at the Board of Directors meeting by the Company held on March 1, 2019, two

consolidated subsidiaries, Takagi Securities Co., Ltd. (“Takagi Securities”) and Tokai Tokyo Securities

Co., Ltd. have merged.

(1) Outline of the business combination

(a) Name of the companies involved and business outline

Surviving company:

Name - Tokai Tokyo Securities

Business outline - Financial instrument business

Dissolving company:

Name - Takagi Securities

Business outline - Financial instrument business

(b) Effective date of the business combination

September 1, 2019

(c) Legal form of the business combination

An absorption-type merger, with Tokai Tokyo Securities as the surviving company and Takagi

Securities as the dissolving company

(d) Name of the company after the business combination

Tokai Tokyo Securities

(e) Major reason for the business combination

The purpose of this merger is to effectively realize further improvement of customer service

and to enhance of corporate value of the Group in response to fierce competition given entries

of multiple industries into the securities industry, and changes in the environment surrounding

the securities industry and market trends.

(2) Outline of the accounting treatment applied for this business combination

This business combination was accounted for as a transaction under common control in accordance

with "Accounting Standard for Business Combinations" (ASBJ Statement No.21, January 16, 2019)

and “Implementation Guidance on Accounting Standard for Business Combinations and Accounting

Standard for Business Divestitures” (ASBJ Statement No. 10, January 16, 2019).

6. Additional Information Corporate restructuring within the Group, capital increase by third-party allotment to a consolidated

subsidiary and change in the scope of consolidation

(1) Summary and purpose of corporate restructuring

Based on the resolution at the Board of Directors meeting on January 30, 2019, the Company made an

absorption-type split agreement with Juroku Bank, Ltd. (“Juroku Bank”) and the corporate split was

completed on June 3, 2019. Juroku Tokai Tokyo Securities (“JTTS”) succeeded to one of the

businesses of Tokai Tokyo Securities, a wholly-owned subsidiary of the Company, on four locations in

Gifu prefecture by the way of corporate split.

Consequently, JTTS was excluded from the scope of the consolidation and accounted for by the equity

method, as JTTS increased its capital by third-party allotment to Juroku Bank on June 3, 2019.

15

(a) Business alliance

The Company has started the management plan, “New Age's, Flag Bearer 5,” under which the

Company is adapting to rapid changes in the business environment represented by diversification and

sophistication of customer needs, and penetration of digital financial services such as FinTech and AI,

and is aiming at evolution into an advanced "comprehensive financial group."

Juroku Bank started the fourteenth medium-term management plan, “All For Your Smile: Providing

Wholehearted Services ~2nd stage~,” under which Juroku Bank is aiming to be “a financial group that

is needed by customers and grows with customers.” At the same time, Juroku Bank is making efforts to

transform the business model on the basis of “engagement first” principle in which Juroku Bank can

contribute to customers and regional economic growth, and a sustainable income structure to support

the region circulates virtuously.

Business alliance among these entities based in Tokai region will enable them to support mutually as

equal partners, reinforce their sales infrastructure, and promote contribution to the region.

Therefore, the Company and Juroku Bank made an agreement for this corporate split as the initial

business alliance was agreed on March 23, 2018, and opened JTTS on January 30, 2019.

(b) Corporate split

The corporate split is an absorption-type corporate split, in which Tokai Tokyo Securities and JTTS are

the restructuring company and the succeeding company, respectively.

(c) Capital increase by third-party allotment

Juroku Bank underwrote the capital increase by third-party allotment immediately after the corporate

split and JTTS became a joint venture of Juroku Bank and the Company (held 60% and 40%

respectively).

(2) Outline of corporate split

(a) Effective date: June 3, 2019

(b) Assets and liabilities split and succeeded were as follows:

Assets (Millions of

yen)

(Thousands of U.S. dollars)

Cash and deposits ¥ 4 $ 34

Cash segregated as deposits 607 5,580

Receivables related to margin transactions 246 2,260

Other current assets 3 29

Tangible assets 95 870

Intangible assets 1 12

Investments and other assets 37 343

Total assets ¥ 993 $ 9,128

Liabilities (Millions of

yen) (Thousands of

U.S. dollars)

Payables related to margin transactions ¥ 246 $ 2,260 Payables to customers 566 5,197

Other current liabilities 43 393

Other fixed liabilities 0 0

Total liabilities ¥ 855 $ 7,850

(c) Consideration for the corporate split

The succeeding company, JTTS, issued 3,500 shares of common stock, and delivered them to Tokai

Tokyo Securities on the effective date. On the same day, Tokai Tokyo Securities distributed the above

shares to the Company as a dividend.

(3) Outline of the capital increase by third-party allotment

(a) Subscription and allotment of new shares: The third-party allotment

(b) Number of shares newly issued: 5,400 shares of common stock

(c) Issue price: ¥1 million ($9 thousand) per share

(d) Total issue price: ¥5,466 million ($50,225 thousand)

16

(e) Capital incorporation;

Increased common stock: ¥2,950 million ($27,107 thousand)

Increased capital surplus: ¥2,516 million ($23,119 thousand)

(f) Payment date: June 3, 2019

(4) Change in the scope of consolidation

The capital increase by third-party allotment above resulted in a decrease in the Company’s share in

JTTS. Consequently, JTTS was excluded from the scope of consolidation and became an equity

method affiliate of the Company. As a result, the Company recognized ¥2,055 million ($18,879

thousand) of “Gain on change in equity” in “Other income, net” in the consolidated statements of

income in June 2019.

7. Cash and cash equivalents Reconciliations between cash and cash equivalents in the consolidated statement of cash flows and cash

and deposits in the consolidated balance sheet as of March 31, 2020 and 2019, were presented as follows:

(Thousands of U.S. dollars) (Millions of yen)

2020 2019 2020

Cash and deposits ¥ 64,746 ¥ 47,921 $ 594,925

Time deposits with maturity of over three months (1,545) (1,647) (14,189)

Cash and cash equivalents ¥ 63,201 ¥ 46,274 $ 580,736

17

8. Securities (1) Trading securities as of March 31, 2020 and 2019, consisted of the following:

(2) Investment securities with market value as of March 31, 2020 and 2019, consisted of the following: (Millions of yen)

2020 2019

Balance

Sheet

Acquisition

Cost Difference

Balance Sheet

Acquisition Cost

Difference

Available-for-sale securities

Securities with market values that

exceed acquisition cost:

¥

1,212

¥

732

¥

480

¥

3,959

¥

2,879

¥

1,080

Stocks 1,212 732 480 3,958 2,878 1,080

Other - - - 1 1 0

Securities with market values that

do not exceed acquisition cost:

3,492 4,840 (1,348) 1,993 2,543 (550)

Stocks 3,492 4,840 (1,348) 1,993 2,543 (550)

¥ 4,704 ¥ 5,572 ¥ (868) ¥ 5,952 ¥ 5,422 ¥ 530

(Thousands of U.S. dollars)

2020

Balance

Sheet Acquisition

Cost Difference

Available-for-sale securities:

Securities with market values that

exceed acquisition cost: $ 11,135 $ 6,722 $ 4,413

Stocks 11,135 6,722 4,413

Other - - -

Securities with market values that

do not exceed acquisition cost: 32,090 44,475 (12,385)

Stocks 32,090 44,475 (12,385)

$ 43,225 $ 51,197 $ (7,972)

(Thousands of U.S. dollars) (Millions of yen)

2020 2019 2020

Trading assets:

Equity and warrants

¥ 8,012 ¥ 34,674 $ 73,623

Bonds

360,714 582,327 3,314,468

Beneficiary certificates of investment trusts

38,536 37,223 354,091

Total ¥ 407,262 ¥ 654,224 $ 3,742,182

Trading liabilities:

Equity and warrants

¥ 64,896 ¥ 26,735 $ 596,303

Bonds

264,885 513,623 2,433,936

Beneficiary certificates of investment trusts

381 0 3,500

Total ¥ 330,162 ¥ 540,358 $ 3,033,739

18

(3) The proceeds from sales of investment securities and gross realized gain and loss on investment

securities for the years ended March 31, 2020 and 2019, were summarized as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Proceed from sales ¥ 12,393 ¥ 5,327 $ 113,880

Stocks 324 4,886 2,978

Bonds - - -

Other 12,069 441 110,902

Gross realized gain 156 1,520 1,434

Gross realized loss (49) (53) (451)

(4) The impairment loss on available-for-sale securities for the years ended March 31, 2020 and 2019

were ¥121 million ($1,113 thousand) and ¥258 million, respectively.

9. Derivatives The Group enters into derivative financial instruments, including foreign currency forward contracts,

currency swaps, and currency options to hedge foreign exchange risk associated with certain assets and

liabilities denominated in foreign currencies. The Group also makes use of derivative financial instruments

such as bond futures, interest rate futures, interest rate swaps, caps and floors, and swaptions to manage its

interest rate exposures on certain liabilities. In addition, the Group entered into stock-related derivative

transactions to manage the fluctuation of stock prices.

The methods for calculating fair value are based on the internal rules for calculating fair value. The

principal methods for calculating fair value are as follows:

Category Method

Stock index options Settlement price at the main financial instruments exchange.

Bond future options

Foreign currency forward

contracts

Discounting the receipt and payment amounts using the interest rate of

the applicable currency and converting them into yen at the currency

exchange rate of the day, and then subtracting the present value of

payments from the present value of receipts.

Stock index futures Liquidation index at the main financial instruments exchange.

Interest rate futures Liquidation price or equivalent price at the financial instruments

exchange or foreign financial instruments exchange.

Bond futures Liquidation price at the main financial instruments exchange.

OTC equity options

Stock lending transactions

with equity options

Equity swaps

Present value calculated by price valuation model based on interest

rate, dividend yield, volatility, prices of underlying securities, length of

transaction, etc.

Currency options

Calculating the future value of receipts and payments by reference to

the swap rate, volatility, correlation, etc., and discounting them using

the interest rate of the respective currencies, and then converting them

into yen at the currency rate of the day. The present value of payments

in yen is subtracted from the present value of receipts in yen.

Interest rate swaps

Caps and floors

Currency swaps

Interest rate swaptions

Calculating the future value of receipts and payments by reference to

the swap rate, volatility, etc., and discounting them using the interest

rate of the respective currencies, and then converting them into yen at

the currency rate of the day. The present value of payments in yen is

subtracted from the present value of receipts in yen.

For transactions in which mutual payment of cash is generated or

expired under certain conditions, the present value is the discounted

amount of future value reflecting the probability distribution of the net

amount of receipts and payments.

Derivative transactions to which hedge accounting is not applied

19

(1) Currency-related transactions (Millions of yen)

At March 31, 2020

Contract

amount

Contract

amount

due after

one year

Fair value

Unrealized

gain

(loss)

OTC:

Foreign currency forward contracts:

Selling ¥ 42,813 - ¥ 68 ¥ 68

Buying 40,043 - 109 109

Currency options contracts:

Selling 225,997 ¥ 127,872 9,842 348

Buying 181,804 99,275 5,530 (1,145)

Currency swaps contracts 77,593 66,086 769 769

(Millions of yen)

At March 31, 2019

Contract amount

Contract amount

due after one year

Fair value

Unrealized gain

(loss)

OTC:

Foreign currency forward contracts:

Selling ¥ 45,646 - ¥ 53 ¥ 53

Buying 30,096 - 12 12

Currency options contracts:

Selling 110,848 ¥ 88,521 6,258 1,379

Buying 96,868 69,786 3,753 (1,064)

Currency swaps contracts 42,979 35,035 677 677

(Thousands of U.S. dollars)

At March 31, 2020

Contract

amount

Contract

amount

due after

one year

Fair value

Unrealized

gain

(loss)

OTC:

Foreign currency forward contracts:

Selling $ 393,394 - $ 629 $ 629

Buying 367,943 - 1,002 1,002

Currency options contracts:

Selling 2,076,610 $ 1,174,969 90,437 3,194

Buying 1,670,528 912,206 50,814 (10,522)

Currency swaps contracts 712,971 607,238 7,068 7,068

20

(2) Interest rate-related transactions (Millions of yen)

At March 31, 2020

Contract

amount

Contract

amount

due after

one year

Fair value Unrealized

gain (loss)

Listed:

Interest rate futures:

Selling - - - -

Buying - - - -

Bond futures:

Selling ¥ 23,785 - ¥ 53 ¥ 53

Buying 27,726 - (9) (9)

Bond futures option:

Selling 51 - 16 34

Buying 58 - 15 (44)

OTC:

Interest rate swaps:

Fixed rate receipt, floating rate payment 215,173 ¥ 203,505 3,442 3,442

Fixed rate payment, floating rate receipt 210,292 202,742 (983) (983)

Yen/Yen basis swap 88,950 84,950 63 63

Fixed rate receipt, Fixed rate payment 12,500 12,500 88 88

Caps and Floors:

Selling 5,000 5,000 1 205

Buying 4,000 4,000 0 (57)

Interest rate swaptions:

Selling 78,500 78,500 1,416 78

Buying - - - -

(Millions of yen)

At March 31, 2019

Contract amount

Contract amount

due after one year

Fair value Unrealized gain (loss)

Listed:

Interest rate futures:

Selling ¥ 133,052 - ¥ (187) ¥ (187)

Buying 133,071 - 231 231

Bond futures:

Selling 21,601 - (136) (136)

Buying 147,294 - 205 205

Bond futures option:

Selling - - - -

Buying 29,035 - 16 (1)

OTC:

Interest rate swaps:

Fixed rate receipt, floating rate payment 87,190 ¥ 78,078 1,765 1,765

Fixed rate payment, floating rate receipt 94,786 72,935 (1,559) (1,559)

Yen/Yen basis swap 56,450 56,450 (143) (143)

Fixed rate receipt, Fixed rate payment 12,500 12,500 185 185

Caps and Floors:

Selling 5,000 5,000 4 201

Buying 4,000 4,000 2 (56)

Interest rate swaptions:

Selling 52,000 52,000 727 224

Buying - - - -

21

(Thousands of U.S. dollars)

At March 31, 2020

Contract

amount

Contract

amount

due after

one year

Fair value Unrealized

gain (loss)

Listed:

Interest rate futures:

Selling - - - -

Buying - - - -

Bond futures:

Selling $ 218,548 - $ 488 $ 488

Buying 254,765 - (79) (79)

Bond futures option:

Selling 466 - 151 315

Buying 534 - 133 (401)

OTC:

Interest rate swaps:

Fixed rate receipt, floating rate payment 1,977,147 $ 1,869,934 31,630 31,630

Fixed rate payment, floating rate receipt 1,932,300 1,862,922 (9,033) (9,033)

Yen/Yen basis swap 817,330 780,575 581 581

Fixed rate receipt, Fixed rate payment 114,858 114,858 812 812

Caps and Floors:

Selling 45,943 45,943 9 1,881

Buying 36,755 36,755 4 (528)

Interest rate swaptions:

Selling 721,308 721,308 13,015 715

Buying - - - -

(3) Stock-related transactions (Millions of yen)

At March 31, 2020

Contract

amount

Contract

amount

due after

one year

Fair

value

Unrealized

gain (loss)

Listed:

Stock index futures:

Selling ¥ 8,657 - ¥ 50 ¥ 50

Buying 71,287 - 6,362 6,362

Stock index options:

Selling 74,271 ¥ 6,825 3,193 (967)

Buying 51,538 4,350 2,798 968

Equity options:

Selling - - - -

Buying 6 - 0 0

OTC:

Stock lending transactions with equity options:

Selling - - - -

Buying 2,305 - 248 230

OTC equity options:

Selling 10,786 1,165 1,554 (658)

Buying 37,350 - 1,562 460

Equity swaps 12,287 6,320 3,032 3,032

22

(Millions of yen)

At March 31, 2019

Contract Amount

Contract

amount due after one year

Fair

value

Unrealized gain (loss)

Listed:

Stock index futures:

Selling ¥ 18,881 - ¥ 32 ¥ 32

Buying 10,680 - 53 53

Stock index options:

Selling 60,153 ¥ 8,375 937 88

Buying 69,698 5,550 541 (96)

Equity options:

Selling - - - -

Buying - - - -

OTC:

Stock lending transactions with equity options:

Selling - - - -

Buying 6,020 - 87 59

OTC equity options:

Selling 5,411 1,754 487 (28)

Buying 6,760 - 226 (9)

Equity swaps 12,850 6,540 2,739 2,739

(Thousands of U.S. dollars)

At March 31, 2020

Contract

Amount

Contract

amount

due after

one year

Fair

value

Unrealized

gain (loss)

Listed:

Stock index futures:

Selling $ 79,548 - $ 458 $ 458

Buying 655,032 - 58,463 58,463

Stock index options:

Selling 682,452 $ 62,712 29,339 (8,885)

Buying 473,565 39,971 25,713 8,891

Equity options:

Selling - - - -

Buying 52 - 1 1

OTC:

Stock lending transactions with equity options:

Selling - - - -

Buying 21,180 - 2,278 2,114

OTC equity options:

Selling 99,106 10,708 14,279 (6,045)

Buying 343,196 - 14,348 4,228

Equity swaps 112,901 58,072 27,856 27,856

Derivative transactions to which hedge accounting is applied

There are no derivative transactions to which hedge accounting is applied.

23

10. Borrowings Borrowings as of March 31, 2020 and 2019, were as follows:

(Thousands of U.S. dollars)

(Weighted-aver

age interest rate or interest rate

range) (Millions of yen)

2020 2019 2020

2020

Short-term borrowings:

Borrowings from financial institutions ¥ 125,260 ¥ 120,245 $ 1,150,970

Borrowings from securities finance

companies

400

400

3,675

Total ¥ 125,660 ¥ 120,645 $ 1,154,645 0.14%

Commercial paper:

Short-term bonds ¥ 16,000 ¥ 16,000 $ 147,018 0.05-0.07%

Total ¥ 16,000 ¥ 16,000 $ 147,018

Long-term debt:

Borrowings from financial institutions ¥ 91,930 ¥ 71,452 $ 844,710 0.47-0.56%

Straight bonds 16,743 22,134 153,842 0.05-2.85%

Exchangeable bonds 12,147 9,720 111,614 0.10-19.10%

Step-up callable bonds 700 700 6,432 0.40-0.81%

Callable bonds 2,800 7,200 25,728 0.51-1.70%

Dual currency bonds 1,808 1,072 16,617 0.15-8.60%

Floating rate bonds 400 400 3,676 0.55%

Index-linked bonds - 790 - 0.95-7.40%

Total ¥ 126,528 ¥ 113,468 $ 1,162,619

Less current portion (31,122) (27,765) (285,971)

Long-term debt, less current portion ¥ 95,406 ¥ 85,703 $ 876,648

Total borrowings ¥ 268,188 ¥ 250,113 $ 2,464,282

The aggregate annual maturities of long-term debt as of March 31, 2020, were as follows:

Year ending March 31

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2020

2021 ¥ 31,122 $ 285,971

2022 9,191 84,449

2023 2,005 18,424

2024 18,105 166,360

2025 3,505 32,206

2026 and thereafter 62,600 575,209

Total ¥ 126,528 $ 1,162,619

24

11. Assets pledged as collateral (1) Assets pledged as collateral for borrowings as of March 31, 2020 and 2019, were summarized as

follows:

(Millions of yen)

Obligations

secured by

pledged assets

Pledged assets

Cash and

Deposits

Trading

Securities

Receivables

from brokers,

dealers, and

clearing

organizations

Total

2020 Short-term borrowings ¥ 80,400 ¥ 1,001 ¥ 120,202 - ¥ 121,203

Cash received on

securities loaned

12,239 - - - -

Borrowings under

repurchase

agreements

199,319 - 172,781 - 172,781

Payables related to

margin transactions 6,876 - 570 ¥ 21,100 21,670

Total ¥ 298,834 ¥ 1,001 ¥ 293,553 ¥ 21,100 ¥ 315,654

(Millions of yen)

Obligations secured by

pledged assets

Pledged assets

Cash and

Deposits Trading

Securities Receivables from

brokers, dealers,

and clearing

organizations

Total

2019

Short-term borrowings ¥ 80,400 ¥ 12 ¥ 114,438 - ¥ 114,450

Cash received on

securities loaned 17,789 - - - -

Borrowings under

repurchase

agreements

327,510 - 282,962 - 282,962

Payables related to

margin transactions 9,627 - 570 - 570

Total ¥ 435,326 ¥ 12 ¥ 397,970 - ¥ 397,982

(Thousands of U.S. dollar)

Obligations

secured by

pledged assets

Pledged assets

Cash and

Deposits

Trading

Securities

Receivables

from brokers,

dealers, and

clearing

organizations

Total

2020 Short-term borrowings $ 738,767 $ 9,196 $ 1,104,491 - $ 1,113,687

Cash received on

securities loaned

112,462 - - - -

Borrowings under

repurchase

agreements

1,831,467 - 1,587,624 - 1,587,624

Payables related to

margin transactions 63,186 - 5,239 $ 193,881 199,120

Total $ 2,745,882 $ 9,196 $ 2,697,354 $ 193,881 $ 2,900,431

25

(*1) In addition to the above, the following were pledged as collateral for the above obligations:

(Thousands of U.S. dollars) (Millions of yen)

2020 2019 2020

Stocks received as collateral from customers

under self-financing margin transactions ¥ 1,131 ¥ 6,405 $ 10,394

Securities received as collateral for short-term

guarantees

- 148 -

Securities borrowed for collateralized short-term financing agreements

72,390 81,276 665,169

(*2) The following assets were pledged as initial margin for futures transactions and as collateral for other

transactions:

(Thousands of U.S. dollars) (Millions of yen)

2020 2019 2020

Trading securities - ¥ 15 -

Receivables from brokers, dealers, and clearing

organizations ¥ 15 - $ 138

(2) The fair values of securities pledged and received as collateral at March 31, 2020 and 2019, were

as follows:

(Millions of yen) (Thousands of U.S. dollars)

2020 2019 2020

Pledged securities:

Securities loaned to customers for margin transactions ¥ 2,071 ¥ 2,110 $ 19,026

Securities pledged as collateral to securities finance

companies or securities exchange brokers for borrowings under margin transactions

6,523 9,482 59,938

Securities loaned for collateralized short-term

financing agreements 12,612 18,897 115,888

Securities sold under repurchase agreements 198,938 328,132 1,827,967

Securities pledged as collateral for short-term

guarantees 4,249 11,452 39,041

Received securities:

Securities borrowed from finance companies or

securities exchange brokers for margin transactions ¥ 71,471 ¥ 18,110 $ 656,717

Securities received as collateral from customers for

loans under margin transactions 20,252 28,348 186,087

Securities borrowed for collateralized short-term

financing agreements 44,042 53,100 404,682

Securities purchased under resale agreements 310,253 454,197 2,850,802

Securities received as collateral for short-term

guarantees 37,427 38,385 343,907

Other 1,112 1,050 10,217

26

12. Property and equipment Property and equipment as of March 31, 2020 and 2019, consisted of the following:

(Thousands of U.S. dollars) (Millions of yen)

2020 2019 2020

Land ¥ 3,435 ¥ 3,769 $ 31,558

Buildings 7,640 8,458 70,205

Fixtures and furniture 9,123 8,893 83,831

Total 20,198 21,120 185,594

Accumulated depreciation (8,159) (9,083) (74,973)

Net property and equipment ¥ 12,039 ¥ 12,037 $ 110,621

13. Retirement benefits The Company and its domestic subsidiaries have a defined benefit corporate pension plan as a main

defined benefit plan and have a defined contribution retirement plan. There are some cases in which extra

retirement benefits are paid to employees when they retire. Tokai Tokyo Securities contributed to the

retirement benefit trust for its pension plan. Certain domestic consolidated companies apply the simplified

method to state the liability based on the amount that would be paid if employees retired at the

consolidated balance sheet date.

In addition, retirement benefits to directors and Audit & Supervisory Board members of ¥64 million ($587

thousand) and ¥75 million at March 31, 2020 and 2019, respectively, were included in “Liability for

retirement benefits” in the consolidated balance sheet.

1. Defined benefit plans, excluding the plans to which the simplified method is applied

(1) The changes in defined benefit obligation for the years ended March 31, 2020 and 2019, were as

follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Balance at beginning of year ¥ 11,814 ¥ 11,602 $ 108,558

Current service cost 588 615 5,401

Interest cost 110 108 1,009

Actuarial losses 57 462 525

Benefits paid (1,074) (973) (9,868)

Balance at end of year ¥ 11,495 ¥ 11,814 $ 105,625

(2) The changes in plan assets for the years ended March 31, 2020 and 2019, were as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Balance at beginning of year ¥ 14,211 ¥ 15,144 $ 130,584

Expected return on plan assets 242 225 2,220

Actuarial losses (727) (873) (6,678)

Contributions from the employer 626 688 5,755

Benefits paid (1,074) (973) (9,868)

Balance at end of year ¥ 13,278 ¥ 14,211 $ 122,013

27

(3) Reconciliation between the liability and asset recorded in the consolidated balance sheet and the

balances of defined benefit obligation and plan assets were as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Funded defined benefit obligation ¥ 11,495 ¥ 11,814 $ 105,625

Plan assets (13,278) (14,211) (122,013)

Total ¥ (1,783) ¥ (2,397) $ (16,388)

Unfunded defined benefit obligation - - -

Net asset arising from defined benefit

obligation

¥ (1,783) ¥ (2,397) $ (16,388)

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Liability for retirement benefits - - -

Asset for retirement benefits ¥ 1,783 ¥ 2,397 $ 16,388

Net asset arising from defined benefit

obligation

¥ (1,783) ¥ (2,397) $ (16,388)

(4) The components of net periodic benefit costs for the years ended March 31, 2020 and 2019, were

as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Service cost ¥ 588 ¥ 615 $ 5,401

Interest cost 110 108 1,009

Expected return on plan assets (242) (225) (2,220)

Amortization of prior service benefit (530) (326) (4,880)

Recognized actuarial gains (51) (51) (468)

Net periodic benefit costs ¥ (125) ¥ 121 $ (1,158)

(5) Amounts recognized in other comprehensive income (before income tax effect) in respect of

defined retirement benefit plans for the years ended March 31, 2020 and 2019, were as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Prior service benefit ¥ (51) ¥ (51) $ (468)

Actuarial losses (1,315) (1,661) (12,084)

Total ¥ (1,366) ¥ (1,712) $ (12,552)

(6) Amounts recognized in accumulated other comprehensive income (before income tax effect) in

respect of defined retirement benefit plans as of March 31, 2020 and 2019, were as follows:

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Unrecognized prior service benefit ¥ (38) ¥ (89) $ (351)

Unrecognized actuarial gains (752) (2,067) (6,907)

Total ¥ (790) ¥ (2,156) $ (7,258)

28

(7) Plan assets

(a) Components of plan assets

Plan assets as of March 31, 2020 and 2019, consisted of the following:

2020 2019

Equity investments 51.00% 53.02%

Debt investments 31.02 29.44

General account 12.92 11.42

Others 5.06 6.12

Total 100.00% 100.00%

(*1) The retirement benefit trust contributed to the pension plan is included in the plan assets and constitutes 32.52% and 32.92% of the total plan assets at March 31, 2020 and 2019, respectively.

(b) Method of determining the expected rate of return on plan assets

The expected rate of return on plan assets is determined considering the current and future

asset portfolio and the long-term rates of return which are expected currently and in the

future from the variety of asset portfolios in plan assets.

(8) Assumptions used for the years ended March 31, 2020 and 2019, were set forth as follows:

2020 2019

Discount rate 0.93% 0.93%

Expected rate of return on plan assets 1.69 1.43

Expected rate of future salary increases 4.70 5.40

(*1) These percentages are based on a weighted average.

2. Defined benefit plans to which the simplified method is applied

(1) The changes in liability for retirement benefits for the years ended March 31, 2020 and 2019,

were as follows:

(Millions of yen)

(Thousands of U.S.

dollars)

2020 2019 2020

Balance at beginning of year ¥ 192 ¥ 209 $ 1,760

Net periodic benefit costs 44 54 409

Benefits paid (55) (71) (502)

Decrease by the change in the

scope of consolidation -

- -

Balance at end of year ¥ 181 ¥ 192 $ 1,667

(2) Reconciliation between the liability and asset recorded in the consolidated balance sheet and the

balances of defined benefit obligation and plan assets

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Unfunded defined benefit obligation ¥ 181 ¥ 192 $ 1,667

Net liability arising from defined

benefit obligation

¥ 181 ¥ 192 $ 1,667

29

(Millions of yen)

(Thousands of

U.S. dollars)

2020 2019 2020

Liability for retirement benefits ¥ 181 ¥ 192 $ 1,667

Net liability arising from defined

benefit obligation

¥ 181 ¥ 192 $ 1,667

Net periodic benefit costs based on the simplified method for the years ended March 31, 2020 and

2019, were ¥44 million ($409 thousand) and ¥54 million, respectively.

3. Defined contribution retirement plan

The Group’s contributions to the defined contribution pension plan for the years ended March 31,

2020 and 2019, were ¥575 million ($5,283 thousand) and ¥585 million, respectively.

14. Equity Japanese companies are subject to the Companies Act of Japan (the “Companies Act”). The significant

provisions in the Companies Act that affect financial and accounting matters are summarized below:

(a) Dividends

Under the Companies Act, companies can pay dividends at any time during the fiscal year in addition

to the year-end dividend upon resolution at the shareholders’ meeting. Additionally, for companies that

meet certain criteria including (1) having a Board of Directors, (2) having independent auditors, (3)

having an Audit & Supervisory Board, and (4) the term of service of the directors being prescribed as

one year rather than the normal two year term by its articles of incorporation, the Board of Directors

may declare dividends (except for dividends-in-kind) at any time during the fiscal year if the company

has prescribed so in its articles of incorporation. With respect to the third condition above, the Board of

Directors of companies with an audit and supervisory committee (as implemented under the Company

Act effective May 1, 2015) may also declare dividends at any time during the fiscal year. Because such

companies by nature, meet the criteria under the Companies Act. However, the Company has not

described so in its articles of incorporation.

The Companies Act permits companies to distribute dividends-in-kind (noncash assets) to shareholders

subject to certain limitations and additional requirements. Semiannual interim dividends may also be

paid once a year upon resolution by the Board of Directors if the articles of incorporation of the

company so stipulate. The Companies Act provides certain limitations on the amounts available for

dividends or the purchase of treasury stock. The limitation is defined as the amount available for

distribution to the shareholders, but the amount of net assets after dividends must be maintained at no

less than ¥3million.

(b) Increases/decreases and transfer of common stock, reserve and surplus

The Companies Act requires that an amount equal to 10% of dividends must be appropriated as a legal

reserve (a component of retained earnings) or as additional paid-in capital (a component of capital

surplus), depending on the equity account charged upon the payment of such dividends, until the

aggregate amount of the legal reserve and additional paid-in capital equals 25% of common stock.

Under the Companies Act, the total amount of additional paid-in capital and legal reserve may be

reversed without limitation. The Companies Act also provides that common stock, legal reserve,

additional paid-in capital, other capital surplus and retained earnings can be transferred among the