construction design professional insurance and indemnity

TRANSCRIPT

Construction Design Professional Insurance

and Indemnity: Reconciling Coverage

With Contractual Risks Assessing Indemnification, Additional Insured and

Other Service Provider Agreement Terms to Ensure Adequate Coverage

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, FEBRUARY 4, 2014

Presenting a live 90-minute webinar with interactive Q&A

John D. Broghammer, Partner, Greve Clifford Wengel & Paras, Sacramento, Calif.

William E. Kelley, Attorney, Drewry Simmons Vornehm, Carmel, Ind.

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-871-8924 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your

participation by completing and submitting an Official Record of Attendance (CLE

Form).

You may obtain your CLE form by going to the program page and selecting the

appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For

additional information about CLE credit processing, go to our website or call us at

1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Construction Design Professional Insurance and Indemnity:

Reconciling Coverage With Contractual Risks

WILLIAM E. KELLEY, JR. DREWRY SIMMONS VORNEHM, LLP

C A R M E L / I N D I A N A P O L I S / M E R R I L L V I L L E , I N D I A N A

W W W . D S V L A W . C O M

E - M A I L : W K E L L E Y @ D S V L A W . C O M

T W I T T E R : @ W I L L K E L L E Y J R

F E B R U A R Y 4 , 2 0 1 4

Overview

Overview of Professional Liability Insurance Intended Coverage

Common Exclusions

Overview of CGL Insurance Intended Coverage

Common Exclusions

Overlap in Coverage The Professional Liability Exclusion

Professional Liability Insurance

Professional Liability

1. Commonly referred to as “errors and

omissions”, “E&O” or “E/O” insurance policies

2. Provide coverage for claims arising from negligent acts, errors or omissions during the performance of a design professional’s services

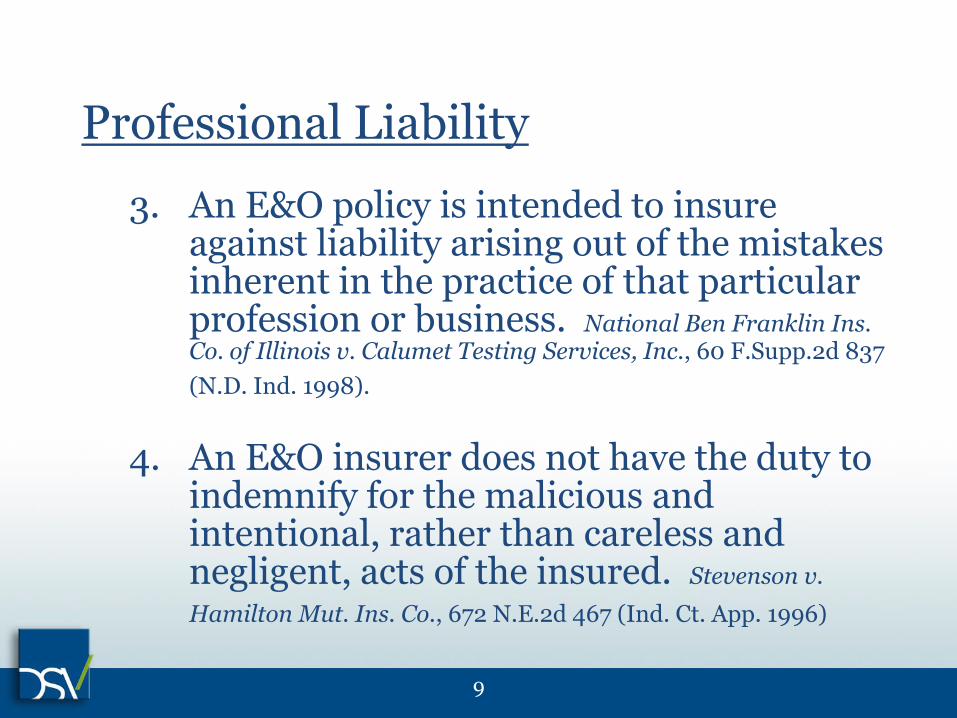

Professional Liability

3. An E&O policy is intended to insure against liability arising out of the mistakes inherent in the practice of that particular profession or business. National Ben Franklin Ins. Co. of Illinois v. Calumet Testing Services, Inc., 60 F.Supp.2d 837

(N.D. Ind. 1998).

4. An E&O insurer does not have the duty to indemnify for the malicious and intentional, rather than careless and negligent, acts of the insured. Stevenson v.

Hamilton Mut. Ins. Co., 672 N.E.2d 467 (Ind. Ct. App. 1996)

9

Professional Liability

5. Typically “claims-made” policies 6. Under “claims-made” policy, coverage is

provided for alleged acts, errors or omissions, so long as the claim is made within the applicable policy period

10

Professional Liability

7. Typically include “defense within limits” or “expenses within limits” provision

8. A “defense within limits” provision

provides that every dollar spent on defense costs and litigation expenses “erodes” or diminishes the amount available under the insurance policy to satisfy settlements or judgments

11

Professional Liability

9. When the policy limits are exhausted, the insurer’s obligation to provide coverage and a defense terminates, and the insured is exposed to any additional liability for both defense costs and any resulting settlement or judgment

12

Professional Liability

10. E&O policies are commonly referred to as “cannibalizing,” “self-consuming,” or “self-liquidating” policies, or as policies with “wasting,” “eroding,” or “exhausting” limits

13

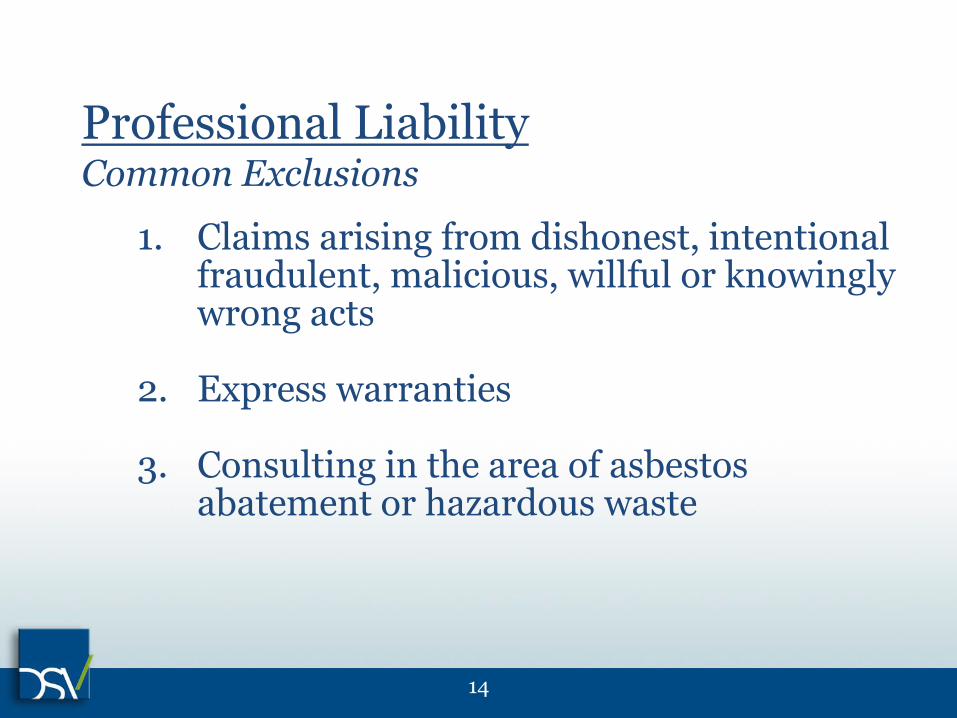

Professional Liability Common Exclusions

1. Claims arising from dishonest, intentional fraudulent, malicious, willful or knowingly wrong acts

2. Express warranties

3. Consulting in the area of asbestos abatement or hazardous waste

14

Professional Liability Common Exclusions

4. Claims made against the design professional by an entity partly owned by the design professional

5. Claims that arise from actual construction services (i.e., construction, assembly, fabrication, installation, demolition, excavation) performed by the design professional

15

Professional Liability Common Exclusions

6. Wrongful acts that occurred prior to the effective date of the policy—unless there is a prior acts endorsement

16

Commercial General Liability (CGL) Insurance

17

CGL Insurance

1. Provides coverage for damages relating to tort liability, as opposed to contractual liability or professional liability for defective work or services

2. Intended for tort liability for physical damages to others, and not for contractual liability of the insured for economic loss suffered because the completed work is not what the damaged person bargained for

18

CGL Insurance

3. Covers “accidents” or “an unexpected

happening without an intention or design.”

4. CGL insurance does not cover an accident of faulty workmanship but rather faulty workmanship which causes an accident

R.N. Thompson & Associates, Inc. v. Monroe Guar. Ins. Co.,

686 N.E.2d 160 (Ind. Ct. App. 1997)

19

CGL Insurance

5. Typically an “occurrence-based” policy

6. Under “occurrence-based” policies, there

may be coverage for alleged acts, errors or omissions that occurred during the applicable policy period, so long as the act, error, or omission giving rise to the claim actually took place during the applicable policy period

20

CGL Insurance

7. Typical CGL policy has two separate and

distinct protections: a. Agreement to indemnify the insured in

amount not to exceed policy limits; and

b. Agreement to provide unrestricted defense against claims

21

CGL Insurance

8. This means that the policy limits are

independent and separate from the defense costs incurred—no eroding policy limits relative to defense costs

22

CGL Insurance Common Exclusions

1. Expected or intended damages

2. Contract liability

3. Worker’s Compensation

4. Pollution

23

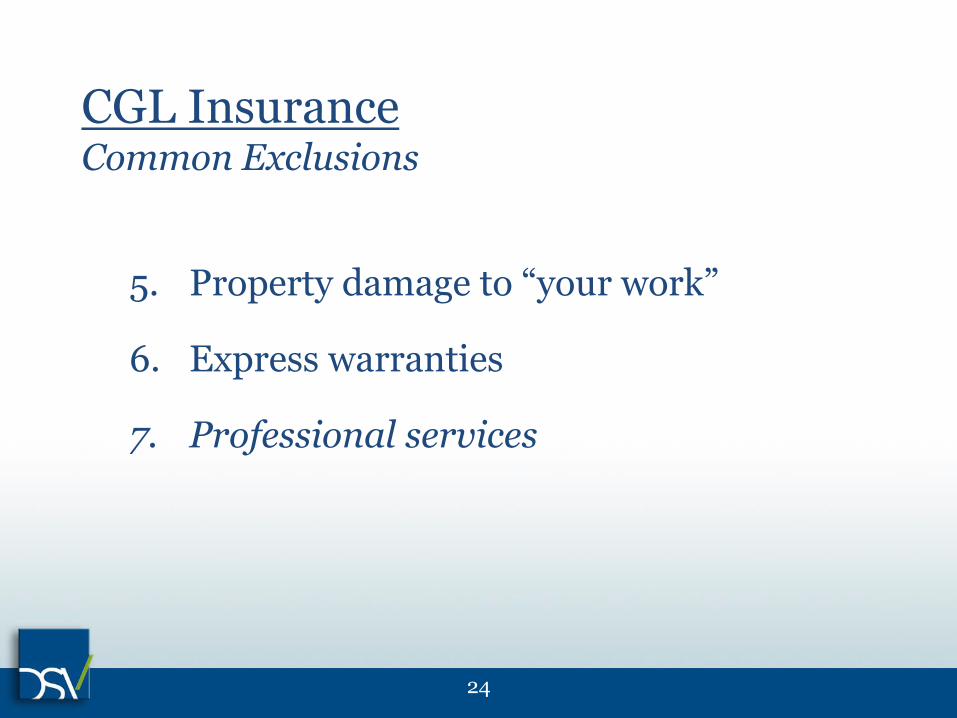

CGL Insurance Common Exclusions

5. Property damage to “your work”

6. Express warranties

7. Professional services

24

Overlap in Coverage: The Professional Services Exclusion

25

CGL Insurance Professional Services Exclusion

1. CGL policy will not cover damages arising from the performance of professional services, which include (a) preparation of drawings; (b) preparation of specifications; (c) supervisory activities; (d) inspection services; (e) architectural services; and (f) engineering services

26

CGL Insurance Professional Services Exclusion

2. The Policy: A general liability policy is not

a substitute for a professional “errors and omission” or malpractice policy. Erie Ins. Group v. Alliance Environmental, Inc., 921 F.Supp. 537 (S.D. Ind.

1996)

27

CGL Insurance Professional Services Exclusion

3. Professional Services Defined: “A

professional act or service is one arising out of a vocation, calling, occupation, or employment involving specialized knowledge, labor or skill, and the skill involved is predominantly mental or intellectual, rather than physical or manual.

Terre Haute First Nat’l Bank v. Pacific Employers Ins. Co., 634

N.E.2d 1336 (Ind. Ct. App. 1993)

28

4. Professional Services Further Defined:

“any business activity conducted by the insured, which involves specialized knowledge, labor or skill, and is predominantly mental or intellectual as opposed to physical or manual in nature.”

Hurst-Rosche Engineers, Inc. v. Commercial Union Ins. Co., 51

F.3d 1336 (7th Cir. 1994)

CGL Insurance Professional Services Exclusion

29

5. Another Definition: “Acts which could be

done by an unskilled or untrained employee are not subject to a professional services exclusion. Professional services involve discretion acquired by special training and the exercise of special judgment.”

Thermo Terratech v. GDC Enviro-Solutions, Inc., 265 F.3d 329

(5th Cir. 2001)

CGL Insurance Professional Services Exclusion

30

6. The Erie Definition: When the

professional draws upon (or at least should draw upon) his or her professional knowledge, experience and training in taking some action, that is a professional service for insurance purposes.

Erie Ins. Group v. Alliance Environmental, Inc., 921 F.Supp. 537

(S.D. Ind. 1996)

CGL Insurance Professional Services Exclusion

31

Exclusion Applies: Engineering firm sued

for defamation and tortious interference with contract for writing highly critical letter about contractor to company issuing performance bond. Exclusion applied because the letter was written in the course of its professional services.

Hurst-Rosche Engineers, Inc. v. Hartford Accident & Indemnity

Co., 51 F.3d 1336 (7th Cir. 1994)

CGL Insurance Professional Services Exclusion

32

CGL Insurance Professional Services Exclusion

Exclusion Applies: Contract required

architect to “endeavor to guard” the owner against defects and deficiencies in the contractor’s work. Owner sues architect for deficient work by contractor, alleging architect failed to properly supervise the work. Court finds that the exclusion applied. Prisco Serena Sturm Architects, LTD v. Liberty

Mut. Ins. Co., 126 F.3d 886 (7th Cir. 1997)

33

CGL Insurance Professional Services Exclusion

Exclusion Applies: Architect sued after

parking garage collapse; Court applies test: “whether a substantial nexus exists between the context in which the acts complained of occurred and the professional services performed”. Finds supervision of A/E work is a professional service. Wimberly Allison Tong & Goo, Inc. v. Travelers Property Casualty Company of America, 559 F.Supp.2d 504 (D.

New Jersey 2008).

34

CGL Insurance Professional Services Exclusion

Exclusion Applies: Engineer sued after

trench collapse. Court finds that exclusion applies because Complaint did not “allege that it was improper performance of engineer’s non-technical activities that caused the injuries”, but explicitly alleged liability stemmed from breach of professional duties as engineer. QBE Insurance Corporation v. Brown & Mitchell, Inc., 591 F.3d 439 (5th Cir.

2009).

35

CGL Insurance Professional Services Exclusion

Exclusion Applies: Court finds claims

against design professional excluded under professional liability exclusion, even for actions that did not require “specialized knowledge” because actions in question occurred in the course of performance of the professional service. Admiral Insurance Company v. Ford, 604 F.3d 420 (5th Cir.

2010).

36

7th Circuit Observation: “If someone entering [the

architectural firm’s] trailer at the construction site were to slip and fall and then file an injury against [the architectural firm], [the insurer’s] CGL policy would provide coverage. Or, where an [architectural firm] employee were to leave a coffee pot on after departing for the day, resulting in a fire that caused damage to the construction project, claims based on that occurrence

would be covered by the CGL policy.” Prisco Serena Sturm Architects, LTD v. Liberty Mut. Ins. Co., 126 F.3d 886 (7th Cir.

1997)

CGL Insurance Professional Services Exclusion

37

CGL Insurance Professional Services Exclusion

Exclusion Does NOT Apply: Engineering

firm sued for failure to locate underground pipelines; when digging trench, worker struck underground pipeline and caused damage. Court finds that determining location of underground pipelines was not a contractual obligation undertaken by the engineer, and thus exclusion did not apply

Aetna Fire Underwriters, Ins. Co. v. Southwestern Engineering

Co., 626 s.E.2d 99 (Tex. App. 1981)

38

Exclusion Does NOT Apply: Engineer

contracted to perform inspection services. Court finds that alleged failure to make sure that contractor remained in compliance with both its contract and relevant safety laws did not require “engineering acumen”, but rather “normal powers of supervision and observation.”

Reliance Ins. Co. v. National Union Fire Ins. Co. of Pittsburgh,

PA, 262 A.D.2d 64 (N.Y.A.D. 1999)

CGL Insurance Professional Services Exclusion

39

CGL Insurance Professional Services Exclusion

Exclusion Does NOT Apply: Engineer

disconnects power to incinerator’s cooling system and causes fire. Court finds actions at issue could have been performed by individuals with no engineering training or no ability to exercise special judgment unique to the field of engineering, so exclusion did not apply. Thermo Terratech v. GDC

Enviro-Solutions, Inc., 265 F.3d 329 (5th Cir. 2001).

40

CGL Insurance Professional Services Exclusion

Exclusion Does NOT Apply: Engineer

hired to supervise project site and report on work of contractors. Injured worker sues for negligent supervision. Court finds act in question (supervision of cement head removal) did not require professional engineering expertise, so exclusion did not apply. Cochran v. B.J. Services Co., USA, 302 F.3d 499 (5th

Cir. 2002).

41

CGL Insurance Professional Services Exclusion

Exclusion Does NOT Apply: Engineer sued

for “negligent supervision” of wastewater treatment plant after worker injury. Court finds “supervisory” services can include purely professional activities, or more broad services that include non-professional activities. Due to ambiguity, insurer had a duty to defend. Camp Dresser &

McKee, Inc. v. Home Ins. Co., 568 N.E.2d 631 (Mass. App. 1991).

42

Exclusion Does NOT Apply: Several

courts have found that the exclusion does not apply to failure to warn of a known danger and misrepresentation of a condition as safe, when it is known to be dangerous.

St. Hudson Engineers, Inc. v. Pennsylvania National Mut. Cas. Co., 909 A.2s 1156 (N.J. Super. 2006); Gregoire v. AFB Const.

Inc., et al., 478 So.2d 538 (La. App. 1985).

CGL Insurance Professional Services Exclusion

43

Practice Pointers

44

PROJECT DOCUMENTATION AND INSURANCE

COVERAGE

Using Documentation For Risk Allocation Presenter:

John D. Broghammer

Greve, Clifford, Wengel & Paras, LLP

2870 Gateway Oaks Drive, Suite 210

Sacramento, CA 95833

Telephone: (916) 443-2011

Website: http://www.greveclifford.com

YOUR ENEMY IS YOU!!

• Per a large A/E insurance carrier, a dispute is ALMOST ALWAYS caused by a documentation error—not a design error.

– 1. No or poorly drafted contracts;

– 2. Failure to manage expectations;

– 3. Failure to document and follow up.

47

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

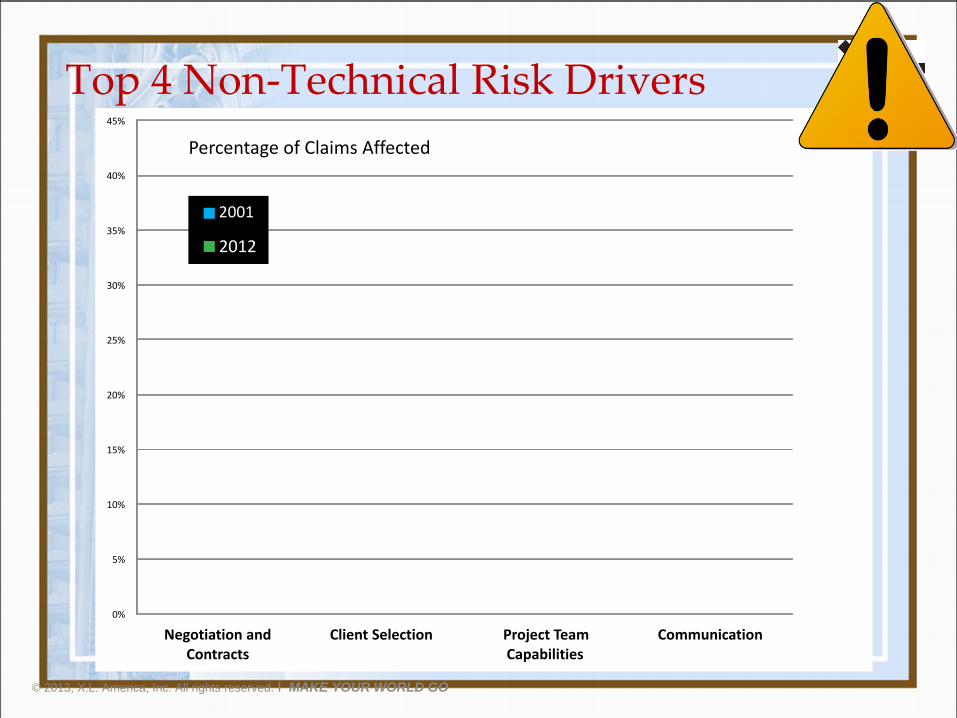

Top 4 Non-Technical Risk Drivers

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

13%

16%

24%

27%

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

13%

16%

24%

27%

6%

23%

25%

39%

GET IT IN WRITING!!!

• Contracts should be in writing and many states require a written contract with specific provisions for inclusion.

• Ancient Chinese proverb: “The faintest of ink is worth more than the strongest memory.”

52

FROM THE “DUH” FILES:

“An oral contract is

not worth the paper

it is written on.”

53

YOU DON’T WIN UNTIL YOU DRAG THE SIGNED CONTRACT HOME.

54

READ YOUR DAMN CONTRACT!!

I’ve never been told by any

client embroiled in a lawsuit

that he or she regretted taking

the time to read and understand their contract.

Or reading or at least reviewing

their insurance policy. 55

Come on, you know this:

• Keep a copy of the contract in separate file.

• Add papers or e-mails that impact the contract and/or your scope of work.

• Scan your contracts and related documents an electronic file.

56

SUN TZU

“The general who wins the battle makes many calculations in his temple before the battle is fought. The general who loses makes but few calculations beforehand.”

• BE PREPARED….

57

Paris Hilton???

What the… what???

58

NEGOTIATIONS • Your contract is your friend…maybe your

only friend on a project.

• It is the single most critical thing on a project.

• Never give contract negotiation short shrift.

• Never ignore your insurance policy as it relates to your contractual scope of work.

59

NEGOTIATIONS

• Be specific. Let others review your drafts for content and errors.

• Better yet, use stock contracts (e.g., AIA).

• Read the RFP (or similar documents) closely and know whether you are insured for the work.

• Memorialize in writing additions/subtractions.

60

CRITICAL CONTRACT CLAUSES

A. Detailed Scope of Work Language.

B. Construction Administration Language.

C. Indemnity Clauses.

D. Standard of Care.

E. Miscellaneous. 61

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

Top 4 Non-Technical Risk Drivers

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

13%

16%

24%

27%

© 2013, X.L. America, Inc. All rights reserved. I MAKE YOUR WORLD GO

Yellow 2

R= 213

G= 206

B= 146

Orange 2

R= 203

G= 125

B= 101

Mag 2

R= 182

G= 114

B= 146

Red 2

R= 239

G= 63

B= 107

LG2

R= 156

G= 162

B=63

Green 2

R= 0

G= 137

B= 143

Cyan 2

R= 0

G= 182

B= 190

DB2

R= 0

G= 65

B= 89

Yellow

R= 255

G= 255

B= 0

Orange

R= 244

G= 121

B= 32

Magenta

R= 236

G= 0

B= 141

Red

R= 237

G= 28

B= 36

Lt Green

R= 141

G= 198

B= 63

Green

R= 57

G= 181

B= 74

Cyan

R= 0

G= 174

B= 239

Dk Blue

R= 45

G= 49

B= 146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Negotiation and Contracts

Client Selection Project Team Capabilities

Communication

2001

2012

Percentage of Claims Affected

Top 4 Non-Technical Risk Drivers

13%

16%

24%

27%

6%

23%

25%

39%

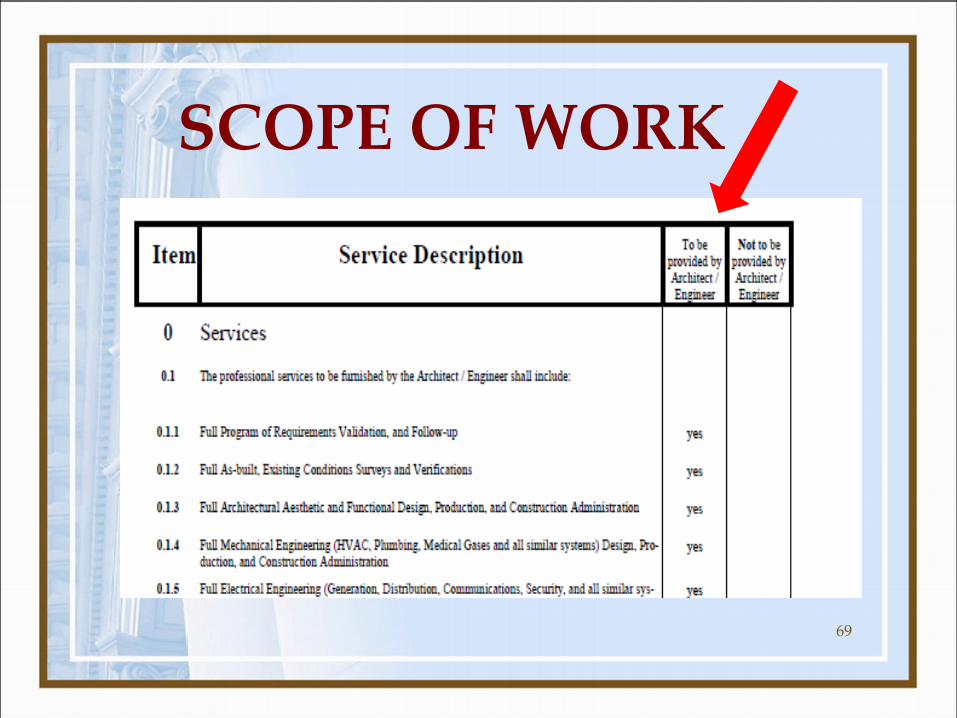

SCOPE OF WORK

• From a prominent A/E insurance carrier re: Scope of Work claims/lawsuits:

“Failure to manage the owner’s

expectations; failure to explain the

scope of work and exclusions thereto.”

• This must be started during negotiations.

66

SCOPE OF WORK Should always be Exhibit A to your contract.

GOOD!!

UH…NOT

GOOD

67

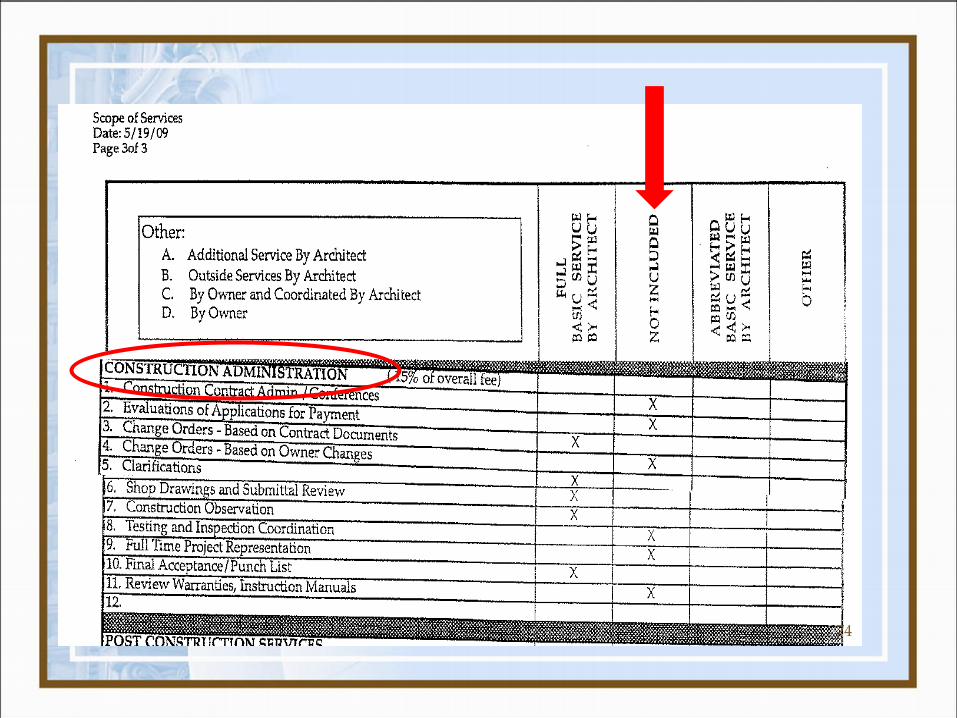

SCOPE OF WORK MATRIX

68

SCOPE OF WORK

69

CRITICAL CONTRACT CLAUSES

A. Detailed Scope of Work Language.

B. Construction Administration Language.

C. Indemnity Clauses.

D. Standard of Care.

E. Miscellaneous. 70

“YOU DO NOT

INSPECT, ONLY

OBSERVE!!!!” 71

CONSTRUCTION ADMININISTRATION

• Construction observation is the periodic observation of completed work to determine general compliance with the plans, specifications and other project documents.

•IT IS NEVER, EVER, AN INSPECTION

72

CUSTOM AND PRACTICE

• Observation is the visual observation of the engineering system for general conformance with the approved plans and specifications.

• Inspection is the monitoring of materials and workmanship that are critical to the integrity of the project to ensure compliance with the approved plans, specifications and applicable laws.

73

74

SAMPLE PROBLEM: Contractor contract language

“best modern practice… highest, best and first class quality.”

75

Same Project…Architect’s Contract…

What does the owner reasonably expect if he expects the contractor to deliver the “highest, best and first class quality?” 76

SAMPLE PROBLEM

• The following language was contained in a construction/design defect problem.

• The claim is alleged to be between a $20-40 million dollar problem.

• Do YOU have insurance for this work or a claim of this size??

77

SAMPLE PROBLEM

• “[Design Professional] shall make…periodic on-site observations, not less than weekly…. Observations shall be conducted deliberately and thoroughly...”

• “Observations shall be for the purpose of ascertaining…that the …quality and detail of construction…complies with…the contract documents.”

78

EXPECTATIONS

• 1. Understand what the law in your state/locale requires.

• 2. Understand the local customs and practices.

• 3. Define your duties and rein in client expectations.

79

Daily Field Reports

• Keep out of other people’s business. Don’t deliberately look outside your area of expertise and scope of work.

• However, IF, and only IF, you see something, say something. Speak up when needed.

80

Daily Field Reports

• Be thorough. Document both what you saw and what you did (and did not see/do if relevant).

• Don’t assume anything and call the office for guidance.

• Know when to say “No” to poor construction and document your objections.

81

Daily Field Reports

• Utilize standard limitation language in your reports and summary letters.

• Avoid expansive words and promises.

• When in doubt, briefly explain.

82

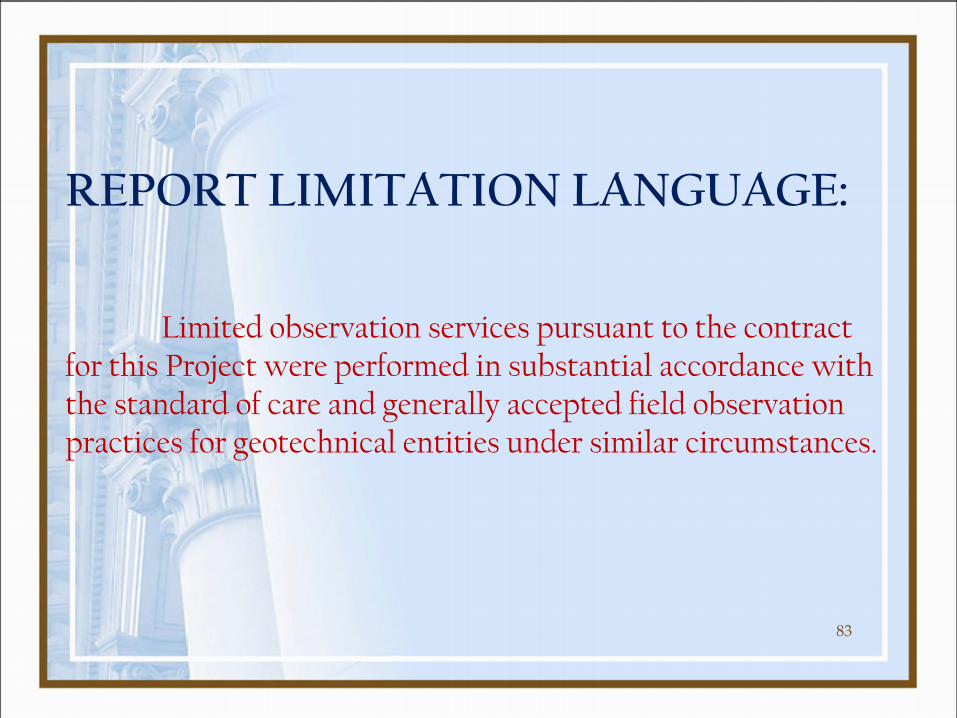

REPORT LIMITATION LANGUAGE: Limited observation services pursuant to the contract for this Project were performed in substantial accordance with the standard of care and generally accepted field observation practices for geotechnical entities under similar circumstances.

83

FOR EXAMPLE: Any testing and information provided herein should not be taken as a guarantee of construction or a representation that the construction work is in conformance with the plans and specifications. No amount of testing or observation services relieves the contractor of his/her primary responsibility to perform construction work in conformance with the Project plans and specifications.

84

FOR EXAMPLE:

Testing services, if any, were done by representative sampling only as specifically directed and requested by the Client and/or Owner. Testing information and results are not intended to be a representation of site-wide conditions. Additional testing will be performed on a time and materials basis as requested by the Client and/or Owner.

85

CONSTRUCTION ADMINISTRATION

BEWARE MISSION CREEP!

Once you start to do something (e.g. inspecting, shop drawing review, warranty coordination, etc.) it will be expected that you continue to do it.

Don’t feed a stray cat.

86

THINGS THAT DRIVE INSURERS

CRAZY

87

SAMPLE PROBLEM

NO!! YOU. DID. NOT.

You arrived for “general observation” not “inspection.”

88

BAD

GOOD!!!

AWFUL!!!! 89

OMG!!!

90

CRITICAL CONTRACT CLAUSES

A. Detailed Scope of Work Language.

B. Construction Administration Language.

C. Indemnity Clauses.

D. Standard of Care.

E. Miscellaneous. 91

INDEMNITY OWNER

DESIGN PROFESSIONAL

INDEMNITY CLAUSE

92

INDEMNITY

≈

INSURANCE

• "An indemnity contract resembles an insurance agreement.” (MacDonald & Kruse v. San Jose Steel

(1972) 29 Cal.App.3d 413, 420.).

93

INDEMNITY

• PURPOSE: Indemnity, like insurance, seeks to shift all or part of the risk of loss from Player A to Player B.

• Usually insurance clauses are strictly construed against insurers….not necessarily indemnity clauses.

94

INDEMNITY

• Insurer’s business model is to collect premiums and spread risk. Insurance works by receiving more premiums than the company pays out in benefits. You do not work this way.

95

INDEMNITY

You do not generally have insurance coverage for

contractual defense and indemnity liability.!!!!

96

97

WHAT IS INSURANCE?

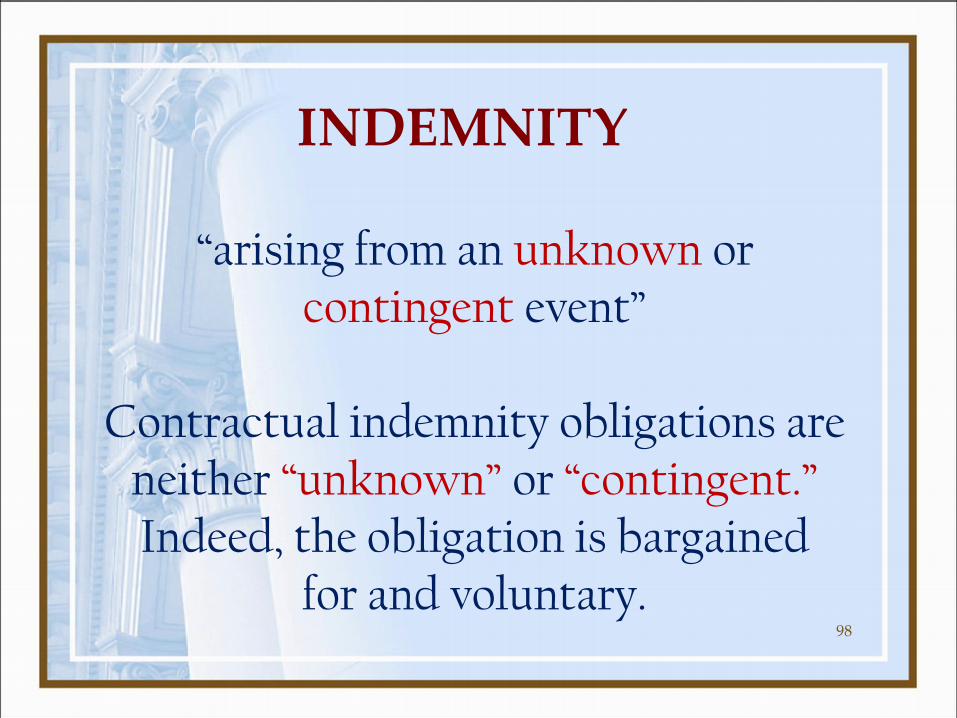

Third Party Insurance: A common definition of “insurance,” is a “contract whereby one undertakes to indemnify another against loss, damage, or liability arising from an unknown or contingent event.” (1 Couch on Insurance (3d rev. ed. 2009) § 1:6, p. 1-16.)

INDEMNITY

“arising from an unknown or contingent event”

Contractual indemnity obligations are

neither “unknown” or “contingent.” Indeed, the obligation is bargained

for and voluntary. 98

INDEMNITY

What to look for….and why to look for it?

99

“Except to the extent of Contractor’s sole negligence or intentional misconduct, and without regard to any negligence or fault on the part of Consultant, Consultant agrees to defend and indemnify …Contractor from and against any and all claims, demands, losses, damages, … and/or liabilities …, arising out of, resulting from, or related to (a) the materials and services provided, (b) the performance or failure in performance of the work, (c) Consultant's contractual obligations, and/or (d) …. 100

“Except to the extent of Contractor’s sole negligence or intentional misconduct....” “Sole” and “solely” are red flag language in any indemnity clause. It is a sure sign of trouble.

101

“and without regard to any negligence or fault on the part of Consultant” This is not normally insurable. You do not have to be negligent to trigger the indemnity obligations—but you usually have to be negligent to trigger insurance. 102

“Consultant agrees to indemnify …, arising out of, resulting from, or related to…” Again, possibly not insurable. Almost ANYTHING is “related to” your work. The plumber’s work is “related to” the mechanical engineer’s work. The framer’s work “arises out of” the architect’s design. 103

“Consultant agrees to defend and indemnify …Contractor from and against any and all claims, demands, losses, damages, … and/or liabilities….” Normally, the duty to defend is very broad and also not insurable. In some states the duty to defend is automatically triggered by an indemnity obligation.

104

INDEMNITY

• The Consultant will indemnify the Client for actual damages for which the Client becomes liable if the damage upon which the liability is based was caused by the proven active negligence of the Consultant.

• If the Client is determined to be liable for damage caused by the proven active negligence of the Consultant, the Consultant will reimburse the Client for the reasonable value of the defense costs insured to defend against the damages caused by the Consultant’s proven negligence.

105

INDEMNITY

Suppose your Client insists that you defend it if it is sued. Then, use:

Consultant has no obligation to pay for Client’s defense costs until there is a final determination of liability. Consultant’s obligation to reimburse Client’s defense cost shall be limited to the Consultant’s percentage of liability based upon Consultant’s comparative fault.

106

HIRE A LAWYER!!

107

CRITICAL CONTRACT CLAUSES

A. Detailed Scope of Work Language.

B. Construction Administration Language.

C. Indemnity Clauses.

D. Standard of Care.

E. Miscellaneous. 108

STANDARD OF CARE

“A [professional] is negligent if he/she fails to use the skill and care that a reasonably careful [professional] would have used in similar circumstances. This level of skill, knowledge, and care is sometimes referred to as “the standard of care.””

Cal. Jury Instruction 600

109

STANDARD OF CARE

• As a general rule, NEVER, ever, agree to contract language that alters the standard of care. A higher standard, like indemnity, can impose liability for non-negligent conduct…and thus lead to no insurance.

110

STANDARD OF CARE

GOOD!

UH…NOT…GOOD!

Best means better than everyone else.

111

STANDARD OF CARE

• Perfection is not required.

• HOWEVER, you are generally held to a higher standard when performing inspections.

• Explain in the contract that perfection is not the standard.

112

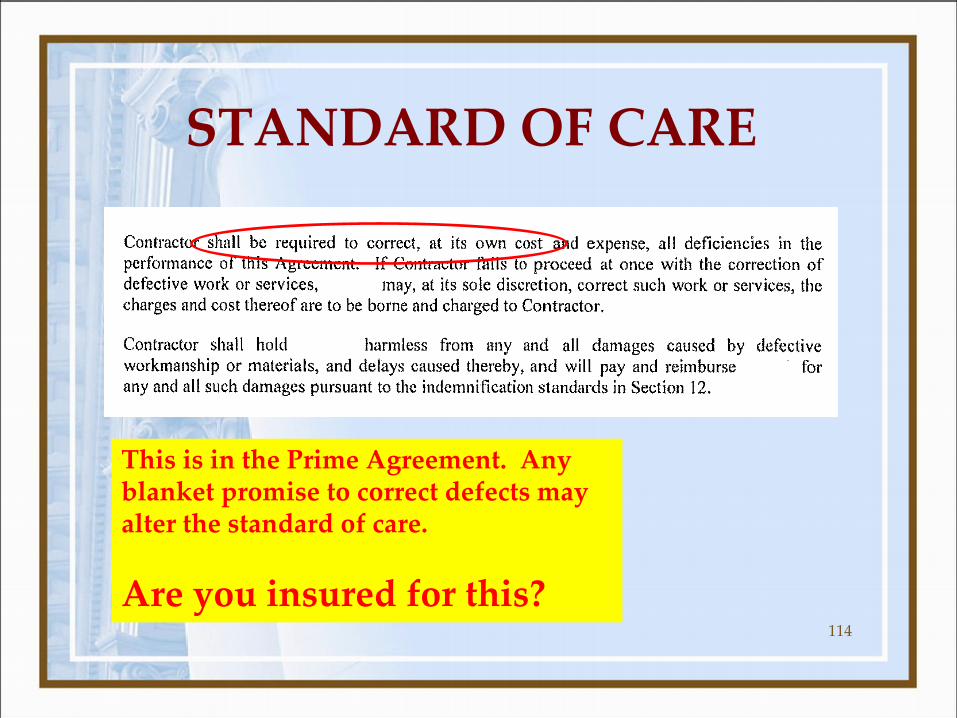

STANDARD OF CARE “C. Performance Standard. Architect’s services provided under this

Agreement shall be performed and completed pursuant to generally accepted standards of professional practice, skill and care in effect at the time of performance, as expeditiously as is consistent with professional skill and care and the orderly progress of the Project. “

Many pages later in the same contract…..

“E. Architect will perform the Services in accordance with the highest standard of care and practice appropriate to the nature of the technical and professional services rendered.”

113

STANDARD OF CARE

This is in the Prime Agreement. Any blanket promise to correct defects may alter the standard of care.

Are you insured for this? 114

STANDARD OF CARE

• Beware of warranties, guarantees, and certifications which effectively turn the Standard of Care into a promise of perfection.

• You normally do not have insurance coverage for such warranties, guarantees, and certifications.

115

CRITICAL CONTRACT CLAUSES

A. Detailed Scope of Work Language.

B. Construction Administration Language.

C. Indemnity Clauses.

D. Standard of Care.

E. Miscellaneous. 116

THIRD PARTY BENEFICIARY

• The Architect’s services under this Agreement are being performed solely for the Client's benefit, and no other party or entity shall have any rights or a claim against the Architect ….

• This provision may be waived only by express written consent of the Architect.

117

NON-ASSIGNMENT

• Neither the Client nor the Architect shall assign this Agreement without the express written consent of the other.

118

119

MISCELLANEOUS

1. Billing and Payment Provisions: Payment terms, interest, attorney fees and collection cost provisions. Terms for suspension or termination for non-payment.

2. Certifications, Guarantees & Warranties: Delete whenever possible. Delete an agreement for code compliance or that construction will be pursuant to “all laws, regulations and codes.” Some state laws define “certify” for architects and engineers to mean only an expression of opinion, not a warranty or guarantee.

3. Arbitration and Dispute Resolution: Generally avoid mandatory arbitration provisions. Other forms of dispute resolution are acceptable.

120

MISCELLANEOUS

4. Job Site Safety: You should not be responsible (directly or indirectly) for job site safety. You should not be responsible for construction means and methods. Ensure language that keeps these responsibilities with contractor or owner.

5. Liquidated Damages: Liquidated damages provisions should not be included in your contract. There are too many variables not in your control as the designer.

6. Limitation of Liability: Where possible insert limitation of liability clause or some type of cap on damages. Be willing to receive a lower fee to obtain this protection. Try to limit damages to “available insurance limits” or similar insurance limitations.

121

MISCELLANEOUS

7. Attorney Fees & Costs: Generally delete all such clauses where possible. Or, limit the clause to very specific disputes, such as fee disputes.

8. Insurance Requirements: Assure yourself that the owner agrees to what insurance is needed for a project (and make sure you AND subs comply). Many policies do not cover certain contractual risk assumptions.

9. Shop Drawing Review: Define shop drawing review responsibilities. Ensure non-responsibility shop drawings and that review is only for general plan conformance. Make sure owner and contractor know the scope of your review.

122

INSURANCE

Errors & Omissions Insurance is always “claims made,” meaning coverage is triggered by the date of a claim or suit—not the project date.

Claims made policies almost always have declining policy limits. Attorney fees and litigation costs reduce the policy limits.

Consider “project insurance” which covers a specific project rather than specific insureds.

123

INSURANCE

• Be aware: High deductibles can be fool’s gold. Deductibles must be paid by you first before the insurer will participate. A high deductible can bankrupt you.

• Some carriers do offer programs that allow you to spread out your deductible over time, such as a 20%/80% split or “first dollar defense” with the payment of the deductible later.

124

INSURANCE

•Buy enough primary E&O insurance!!

•Consider an umbrella or excess policy.

125

INSURANCE

• Make sure your subconsulting contracts comply with insurance provisions of the prime contract.

• Have someone in your office responsible for obtaining Certificates of Insurance from your subs. Get renewal certificates annually.

• Have your insurance company review your contracts for coverage issues or lack of coverage.

126

PROJECT DOCUMENTATION

Presenter:

John D. Broghammer

Greve, Clifford, Wengel & Paras, LLP

2870 Gateway Oaks Drive, Suite 210

Sacramento, CA 95833

Telephone: (916) 669-3905

Website: http://www.greveclifford.com

127