construction material management · fsn analysis –based on movement from store ved analysis...

TRANSCRIPT

Construction Material Management

Prepared By :-

Chintan S. Raichura

DIET, Rajkot

❖Introduction :

➢ The importance of material management can be gauged from the

fact that in any typical building project the approximate share of:

➢ Material Cost = 60%

➢ Labour Cost = 25%

➢ POL, overheads, taxes, and profit = 5%

➢ Material management deals with materials along with costs.

➢ It is estimated that about 10-20% of all materials delivered to site

either end up as waste or illegally removed during construction

phase.

➢ In addition to this large quantity of materials are buried or burnt

due to lack of control.

➢ This is why construction material management is essential.

➢ The main construction materials are :

Cement Aggregates Sanitary items

Steel Sand Electrical items

Bricks Soil timber

Stones Bitumen paints

Tiles

❖Objectives of Material Management :

AIM

Reduce Cost

Required Quantity

Required Quality

Appropriate Price

Right Time

Appropriate Supplier

➢ In addition to above main objectives there are several other

objectives of material management are :

➢To purchase, receive, transport and store materials efficiently and

to reduce the related cost.

➢ To reduce the inventory cost of materials.

➢ To modify paper work procedure in order to minimize delays in

procuring materials.

➢ To train personnel in the field of materials management in order to

increase operational efficiency.

➢ Speedy disposal of materials which are no more required.

❖Materials Management Functions :

Material Planning

Procurement

Custody

Materials accounting

Transportation

Inventory monitoring and control

Materials codification

Computerization

Source Development

Disposal

❖ Materials planning :

➢Materials planning involves,

▪ Identifying quantities

▪ Estimating quantities

▪ Defining specifications

▪ Forecasting requirements

▪ Locating right sources for procurement

❖Procurement :

➢ There are two ways of material procurement

(i) Local procurement

(ii) Centralized procurement

❖ Custody (Receiving, Warehousing, and Issuing) :

➢ The documents used during custody of materials are :

▪ Inward register

▪ Material receipt note (MRN)

▪ Delivery challan (DC)

▪ Indent

▪ Dispatch covering note

▪ Outward register

▪ Loan register

▪ Plant and machinery movement register

The functions of warehousing are : receipt, inspection, storage,

issue/dispatch, materials accounting, valuation and insurance.

❖ Materials accounting :

➢ The main purpose of material accounting is monitoring inflow and consumption

of raw materials. Material accounting involves:

▪ Materials stock accounting

▪ Materials issue and returns accounting

▪ Monthly stock taking

▪ Materials wastage analysis, etc.

➢ Materials wastage analysis aims at finding the cause of wastage and rectifying

them.

❖ Transportation :

➢ Construction materials undergo considerable movement starting form its origin

to the actual point of consumption.

➢ Movement form centralized store to site store should also be considered in case

of large companies.

❖ Inventory monitoring and control :

➢ Inventory may be defined as ‘usable but ideal resource’.

➢ If resource is some physical and tangible object such as materials,

then it is generally termed as stock.

➢All this stocks, finished goods, equipment are called inventories.

➢ Following are the main purpose of inventory control :

✓ To avoid excess blockage of funds of the organization

✓ To see that the project is not starved of materials when

needed.

➢Following reasons justify need of inventory :

✓ It protects against lead time and demand uncertainties.

✓Hedges against price changes

✓Hedges against contingencies

✓ Improves customer service

✓Procurement and transportation costs will be reduced if lot

sizes are large.

➢ Methods of inventory control are :

✓ ABC analysis – based on value of consumption

✓ FSN analysis – based on movement from store

✓ VED analysis – based on necessity

❖ Materials codification :

➢ In construction company where thousands of different items are

used during the project period, materials codification is required.

➢ Mainly construction companies follow this methods for materials

coding

✓ Numeric

✓ Alphanumeric

✓ Color codification

➢ A proper codification of materials serves the following purpose :

✓ Avoiding use of long description

✓ Proper identification of items

✓ Avoiding duplicate stocks under different description

✓ Materials accounting and control

❖ Computerization :

➢Various applications of computers in material management are :

▪ Forecasting the price of materials based on past data

▪ Using the construction schedule, materials schedule can be

easily prepared by computers.

▪ By making the suitable changes in the past specification stored

in the computer new specifications can be easily developed.

▪ It is now possible to float enquiries for different materials

online as well as invite bids from different suppliers online.

▪ Preparing a comparative statement and finalizing the supplier.

▪ Economic order quantity can be decided by using computers.

❖ Source development (Vendor development) :

➢ The vendor’s performance should be evaluated regularly and only

satisfactory vendors should be encouraged.

➢ Initiative such as vendor managed inventory (VMI) can play an

important role in containing and managing the costs.

➢ Good relationship with supplier(vendor) helps in reliable quality

material supply at reasonable rates.

❖Disposal :

➢ Before disposal of old or unused items which are uneconomical to

use should be assessed for its quantity and quality.

➢ The reusable items from the scrape can be retained for future use.

➢ The scrape should be sold to dealer either directly or by tendering.

❖Inventory Management :

➢ Inventory may be defined as ‘usable but idle resource’.

➢ Inventory is one of the indicators of management effectiveness on

the materials management front.

➢ Inventory management deals with the determination of optimal

policies and procedures for procurement of materials.

Inventory turnover ratio =𝑎𝑛𝑛𝑢𝑎𝑙 𝑑𝑒𝑚𝑎𝑛𝑑

𝑎𝑣𝑒𝑟𝑎𝑔𝑒 𝑡𝑢𝑟𝑛𝑜𝑣𝑒𝑟

➢ The inventory turnover ratio is an index of business performance.

➢ A well managed organization will have higher inventory turnover

ratio.

❖ Functions of Inventory :

➢ Inventory is necessary for following reasons :

✓ It aims at absorbing the uncertainties of demand and supply

✓Time leg in deliveries also necessitates building of inventories

✓Quantity discounts, offered by suppliers

✓Anticipated increase in material prices and possibility of future

non-availability

✓Helps in avoiding strain of peak demand.

❖ Inventory policies :

i) Lot size recorder point policy

ii) Fixed order interval scheduling policy

iii) Optimal replacement policy

iv) Two bin system

❖ Selective Inventory Control :

➢Applying scientific inventory control for all the items is neither

feasible nor desirable, as it may increase the cost. Hence, inventory

control has to be exercised selectively.

➢Depending upon the value criticality and usage frequency of an

item, the items are grouped in a few discrete categories.

➢ Important selective inventory control methods are :

1. ABC analysis

2. VED analysis

3. FSN analysis

❖ABC analysis :

➢This method is based on Pareto’s law, which say in any large group

there are ‘significant few’ and ‘insignificant many’.

➢ In construction project only 20% items can be accounting for 80%

of material cost.

➢So this 20% items require more attention and is termed as

‘significant few’.

➢Procedure for preparing ABC curve :

✓ Identify and Estimate quantities of materials required

✓ Identify unit rate of materials

✓ Determine usage value of each materials.

Usage value = estimated quantity X unit rate

✓ Convert usage value into percentage of total project cost

✓ Arrange this percentage value in descending order.

✓Plot a graph of % of average inventory value and % of number

of inventory items.

✓The points on the curve at which there are sudden changes of slopes

are identified.

✓This points are corresponding to top 10% and next 20% are marked

and considered as general indicator of A, B and C type of materials.

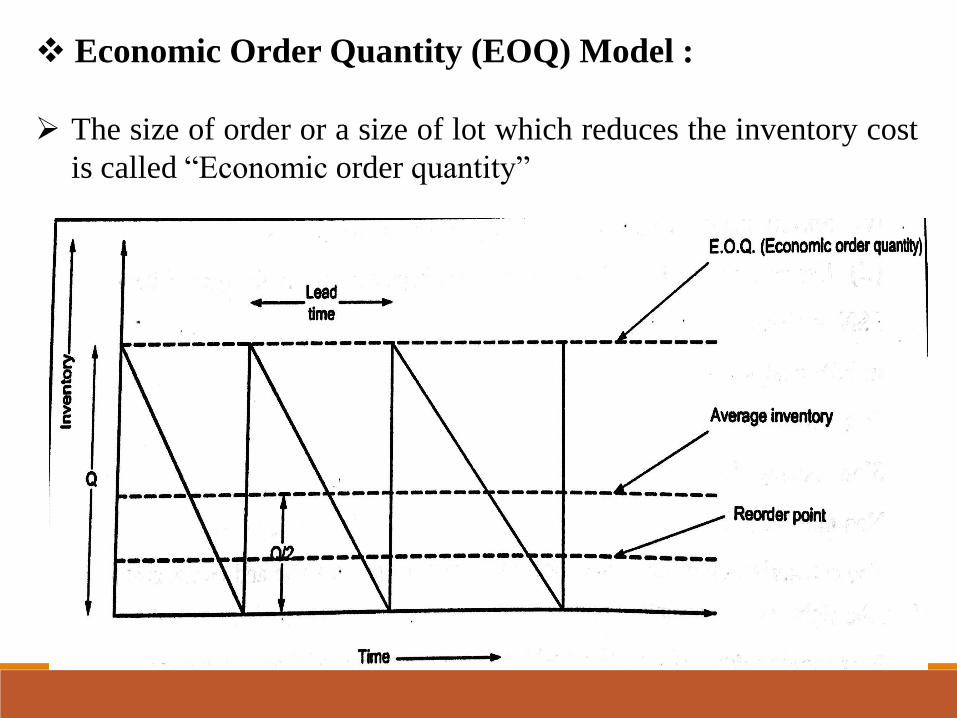

❖ Economic Order Quantity (EOQ) Model :

➢ The size of order or a size of lot which reduces the inventory cost

is called “Economic order quantity”

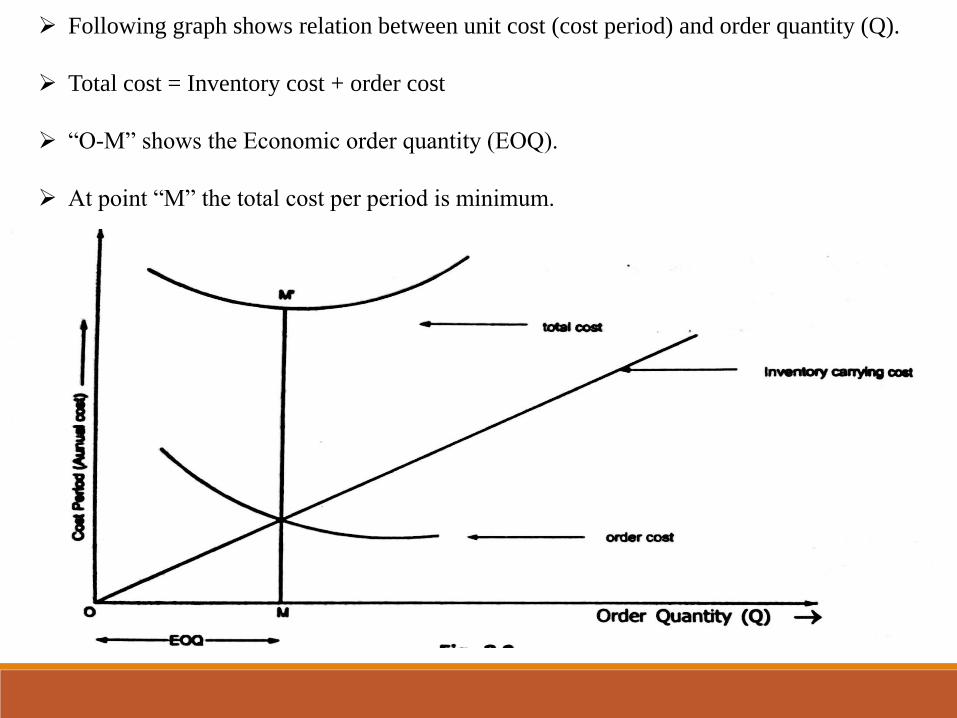

➢ Following graph shows relation between unit cost (cost period) and order quantity (Q).

➢ Total cost = Inventory cost + order cost

➢ “O-M” shows the Economic order quantity (EOQ).

➢ At point “M” the total cost per period is minimum.

EOQ =

{2 𝑥 𝐴𝑛𝑛𝑢𝑎𝑙 𝑐𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛 (𝑢𝑛𝑖𝑡𝑠 𝑝𝑒𝑟 𝑦𝑒𝑎𝑟 𝑥 𝑐𝑜𝑠𝑡 𝑜𝑓 𝑝𝑙𝑎𝑐𝑖𝑛𝑔 𝑎𝑛 𝑜𝑟𝑑𝑒𝑟 𝑝𝑒𝑟 𝑞𝑢𝑎𝑛𝑡𝑖𝑡𝑦)

𝑢𝑛𝑖𝑡 𝑐𝑜𝑠𝑡 𝑥 𝐼𝑛𝑣𝑒𝑛𝑡𝑜𝑟𝑦 𝑐𝑎𝑟𝑟𝑦𝑖𝑛𝑔 𝑟𝑎𝑡𝑒} Τ1 2

Q = √

2 𝑋 𝑁 𝑋 𝐴

𝐶 𝑋 𝐼

Where, Q = Economic order quantity (size)

N = Annual consumption (units per year)

A = Cost of placing an order (Per Q quantity)

C = Unit cost (cost of unit materials)

I = Inventory carrying rate

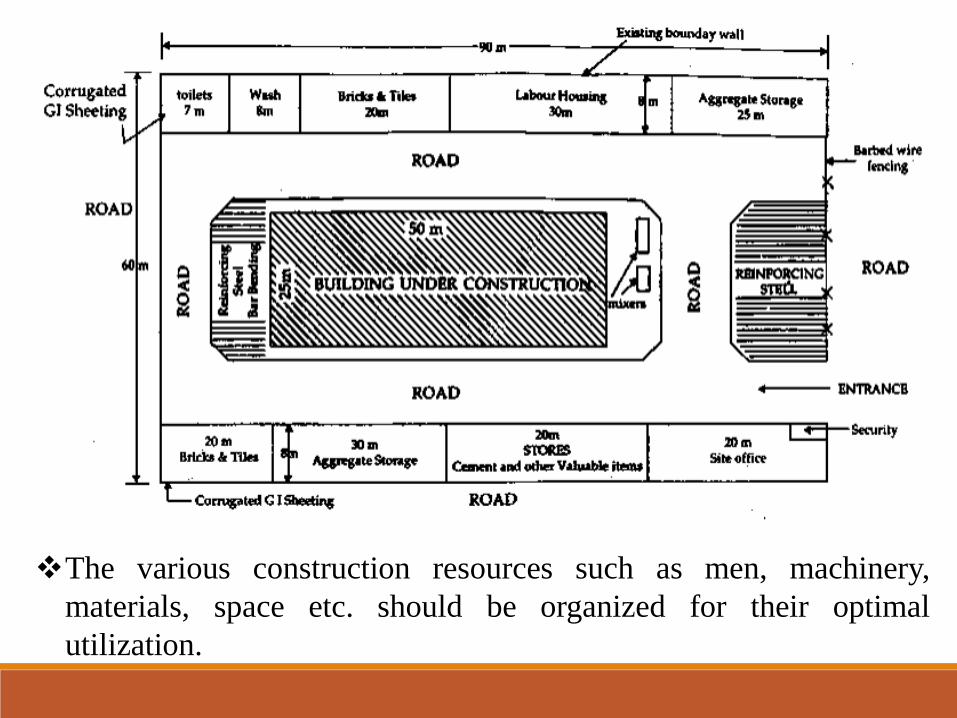

❖Job Layout :

➢ A job layout is a scaled drawing of the proposed construction site

showing all the relevant features such as,

▪ Entry point

▪ Exit point

▪ Storage areas of materials – bricks, cement, sand,

aggregate

▪ Temporary services – washing, toilets

▪ Contractor’s site office

▪ Areas for keeping equipments such as mixers

▪ Bar bending area

▪ Labour housing

➢ A job layout is prepared to ensure that work proceeds smoothly

without interruption.

❖The various construction resources such as men, machinery,

materials, space etc. should be organized for their optimal

utilization.

❖Objectives of preparing job layout :

➢ To same time in handling materials on site

➢ To safeguard materials from damage and deterioration

➢ To provide minimum lead and lift distance and to reduce carting cost.

➢ To adopt best mode of working.

➢ To complete the work with minimum use of equipment and machinery

➢ To take maximum output from labour and machines

➢ To provide safety to workers and passer-by.

➢ To avoid damage to adjacent property due to construction activity.

➢ To store common use materials such as coarse and fine aggregate near

to each other

➢ To store all the materials near to their place of use.

❖ Factors affecting Job Layout :

➢Nature of Project

➢Construction Methods

➢Availability of Resources

➢Medical Facilities

➢Contractor’s, site engineer’s offices

➢Provision for Temporary Roads

➢Other Facilities

❖ Principles of preparing Job Layout :

➢Administrative Block

➢Warehouse/godowns

➢Entry and Exit

➢Locations of workshop

➢Services

➢Temporary roads

➢Staff accommodation

COPYRIGHT : PROF. CHINTAN RAICHURA, DARSHAN INSTITUTE OF TECHNOLOGY, RAJKOT

THANK YOU

“Time is the most valuable thing a man

can spend.”

~ Theophrastus