content delivery networks (cdn) industry analysis february 2014

TRANSCRIPT

Content Delivery Networks version 9

Chris Van Noy February 28, 2014

Overview

• CDN Landscape Established Players in CDN Landscape

Emerging / DisrupHve Players in CDN Landscape

• Trends / Forecasts Pricing / Revenue Traffic / Video Growth

• Threats Caching Video CDNs Large Non-‐CDN Players HVEC H.265, MPEG-‐DASH

• CDN OpportuniHes

OpportuniHes List Media OpportuniHes Example Slides

Chris Van Noy 2

Key Takeaways Trends • Market consensus is CDN Delivery Pricing (StaHc & Video Delivery) will decline for the 2-‐3 years. Our

previous view was the pricing would decline for only the next 12-‐18 mos. However, it appears prices have already started level off (Sept ’13) due to market realiHes and customer a^tudes

• Dynamic Site AcceleraHon (DSA) not dropping nearly as quickly • Traffic, and video traffic in parHcular, will increase substanHally between ‘13 – ’17

Threats • Telcos/MVPDs/3rd ParHes creaHng caching CDNs – Has potenHal to take away significant video traffic • Large, non-‐CDN players are real threats to tradiHonal CDNs (Amazon, Google, MSFT, Facebook?, not

Neflix) • New streaming standards/technologies HVEC H.265, MPEG-‐DASH (a couple of years)

Opportuni0es • CDNs must/will diversify into other services or have the CDN business serve another business purpose • We anHcipate that there are large opportuniHes for CDN and other “nexus” players (remove the

complexity) • InnovaHon OpportuniHes (moat around CDN business) – transformaHon, further delivery innovaHon,

security (content, site, commerce), analyHcs, internaHonal • Adjacent Market OpportuniHes – adverHsing, data, B2B secure transport, media warehouse • Expand Further InternaHonally Chris Van Noy 3

CDN Landscape Established Companies

Data from annual reports and company websites Chris Van Noy 4

* Performance Equity Management (PEM), with parHcipaHon from exisHng investors Menlo Ventures and Steamboat Ventures.

Servers / POPs ‘12 Revenue / Net Rev +-‐ / Net +-‐ Notes

130,000/2,000 $1,300M/$230M +16% / +1.5% Good Shape, Media, Finance, Govnt quickly growing. Old Tech. Poor Cust RelaHonships

18,000/67 Debt, CDN loses $ Expansion in Lat Am, EMEA, Asia (Nov ’13), Rev + 37% YoY Q3 ‘13

18,000/80 $180M/($33M) +5% / -‐23% Losing $, ReinvesHng in CDN

???/35 $100M-‐$200M/(???) +100% / ??? July ’13 $54M new funding*. AcquisiHon? IPO?

14,000/26 $205M in debt refinancing (Aug ‘13)

???/25 $100M/(???) Growing Quickly, Scale, Explode DSA, PotenHal DSA concerns

???/24 Cloud services key, CDN not much focus. Xbox One bump not coming

AcquisiHon By Verizon Announced Q4 ’13, finalized Q1 ‘14

CDN Landscape Emerging Players / Disruptors

Chris Van Noy 5

Founded Descrip0on Disrup0on Customers

2011 SSD Based CDN Launched Video Streaming CDN Q3 ‘13

Lowest Latency, Fewer POPs needed, DSA beuer, Less Cost. Going into video and staHc content

Twiuer, Vine, Shazam, Etsy, Github

2011

MulH-‐plaform adapHve video streaming, Video encoding, DRM and EncrypHon, Content Management, AnalyHcs and ReporHng, Dynamic ad inserHon

Does encoding and ad inserHon more efficiently taking services rev from CDNs

Disney/ABC

2008 Dynamic CDN Switching and AnalyHcs

Allows customers to pay less for delivery, avoid exclusivity and have delivery fallback

Many -‐ Neflix, NFL, ABC, Univision etc

2010

Third Party Caching CDN for Video

Allows ISPs to disintermediate CDNs from most popular video

Mediacom, (allegedly negoHaHng w/ 2 Top US cable companies)

Acquired By Verizon Q3 ‘13

CDN Landscape

CDN Market Share, 2013

Chris Van Noy 6

CDN Trends

Pricing / Revenue

Standard Delivery (Objects, Video) Customer spending more than $1M (Sept ’12) Delivered • 3PB/month, $0.03/GB High, $0.01 Low Sustained • 400Mbps/month, $4/Mbps High, $2/Mbps Low

Dynamic Site Delivery/Accelera0on Pricing Pricing collected from mid-‐size to large customers, 2 yr contracts (May ’13) • 20 Mbps, $150 high, $110 low • 100 Mbps, $85 high, $50 low • 250 Mbps, $40 high, $25 low • 500 Mbps, $15 high, $6 low

CDN Pricing Decline

Dan Rayburn (May ’13) CVN Predic0on (Aug ’13)

2009 2010 2011 2012 2013 2013 -‐ 45% -‐ 25% -‐ 20% -‐ 15% -‐ 25% -‐ 5%-‐10%

Both Standard and Dynamic delivery pricing has consistently decreased YoY.

Previously anHcipated decline to conHnue for the next 12-‐18 mos. but CDNs already refusing to lower prices (Aug ‘13)

Causes for decline: 1. Increased volume 2. Parity of quality in compeHHon 3. Some players compete on price

(Level3, Edgecast) 4. CDN Switchers (Conviva)

Chris Van Noy 7

Note: While pricing is important, it appears customers aren’t differenHaHng on price anymore.

$-‐

$2.0

$4.0

$6.0

$8.0

2011 2012 2013 2014 2015 2016 2017

Revenu

es (U

S$ Bil)

CDN Revenues Source: (Market and Market)

Global

CDN Trends Forecasts: CDNs are predicted to do well from ‘13 – ‘17 CDN Revenues ‘17: NA: $4.6B, Global $7.4B CAGR: 24.6% Source: MarketandMarkets

Video CDN Rev ‘16: $1.2B CAGR: 15.2% Source: Frost & Sullivan

By ‘17 Over 50% of internet traffic through a CDN Source: Cisco VNI

Chris Van Noy 8

CVN Note: The rev and CAGR here seem very low

CDN Threat Caching Video CDNs -‐ Disintermediates TradiHonal CDN Delivery

Cached CDNs Advantages for ISP/MVPDs/Telcos

1. Frees up upstream capacity 2. Predictable Neflix flow 3. Higher QOS 4. Higher Content Quality 5. Saves Costs 6. Neflix Open Connect

is Free

Results in lower potenHal traffic for CDN’s which is not always bad (Neflix) Verizon, Time Warner Cable, Comcast, Neflix, Google all building. Qwilt is third party service aimed at MVPDs/ISPs

Chris Van Noy 9

• User rouHng is done by control servers, not dependent on client DNS configuraHon

• Request is routed to the nearest available Cached CDN Server

• ISP could control client to cache server config

Video Provider Control Servers

3. Client connects to local video cache 4. Local cache delivers video stream

Cached CDN Server

Broadband ISP

CDNs Disintermediated

CDN Gap

CDN Threat Caching Video CDNs -‐ Disintermediates TradiHonal CDN Delivery

Neflix January, 2012

Neflix June, 2012

Chris Van Noy 10

In the six months since Neflix launch of caching CDN (Open Connect) massive traffic rerouted through the caching CDN

CDN Threat Large, Non-‐CDN Players Coming Into the Space

We believe these are big technology players that already have a large enough internal need that building their own CDN makes sense.

Advantages: 1. Since already

using capacity can price below market

2. Can take Hme to iterate and launch features

3. Unique insight into needs

4. Scale Rolling out Open Connect Caching CDN. Not interested in commercializing service for other content providers

CloudFront is already at $100M at 3yrs. DSA just launched. PotenHally can affect ~75% of market with scale, pricing and educaHon of market

No tradiHonal external CDN service but has the infrastructure and business reason (gathering data) to do so.

Less than 2% of web traffic not likely to move in to the CDN space FB has an edge network to push photos

Azure the Cloud Plaform, is becoming more central in MSFT but the CDN is not a focus. Xbox One will not change that.

Chris Van Noy 11

• In our view, Amazon Cloudfront seems expensive • Cloudfront doesn't do true DSA. Only pull, not post • Does not have many DSA POPs. Co-‐lo'ed on some EC3 servers • DSA not a priority, AMZN has very few resources focused on it (Aug ‘13)

CDN Threat New Streaming Technologies

MPEG-‐DASH (Dynamic AdapHve Streaming over HTTP), a standard for adapHve streaming over HTTP can potenHally replace Microso| Smooth Streaming, Adobe Dynamic Streaming, and Apple HTTP Live Streaming (HLS). A unified standard would be a boon to content publishers, who could produce one set of files that play on all DASH-‐compaHble devices.

HEVC H.265 is a video compression standard, a successor to H.264/MPEG-‐4 AVC . It was designed to substanHally improve coding efficiency i.e. to reduce bitrate requirements by half with comparable image quality, at the expense of increased computaHonal complexity

Reduce Complexity Compress Bandwidth/Increase Quality

These technologies are likely to take effect 2-‐3 years out and not really threats but could undermine the revenue potenHal of CDNs. Conversely, the technologies will likely encourage more video delivery and need for services

Chris Van Noy 12

CDN OpportuniHes

Chris Van Noy 13

1. Interna0onal • LaHn America – Brazil, ArgenHna, Colombia, Mexico • Asia – China (difficult), India (difficult)

3. Quickly Growing Ver0cals For CDN Services • Financial Industry • Government • Enterprise (Pharma etc.) • Retail

5. Expanding Past CDN Delivery (Telco/Mobile, MVPDs, Private)

4. Expanding More Deeply into Media/ Entertainment Industry

• Back into content creaHon -‐ B2B i.e. Media Warehouse, Secure Media Delivery

• Forward with services -‐ B2C

(see following slides)

2. Con0nue to Develop Value Added Services on CDN Plaaorm • Security (Content, Site and Infrastructure) • Data • Commerce • Media TransformaHon • Private Cloud CompuHng

• Cable MPEG2 Delivery • Mobile AcceleraHon • Massive Content Storage/TransformaHon

Contact InformaHon

Chris Van Noy 14

Chris Van Noy [email protected] @chrisvannoy www.cvnnyc.com

For More InformaHon:

APPENDIX

CDN OpportuniHes Media/Entertainment Industry

• HTTP Object Delivery

• Large File Delivery

• AnalyHcs • Streaming

• MulHcast support

• Stream prioriHzaHon

Site, App Accelera0on

Cloud Storage

Mobile Delivery

Professional Services

Security

Content Management

Core + Premium

• Cellular Net OpHmizaHon

• OpHcal Network OpHmizaHon

• MVPD Capacity

• Streaming

Network Extension

B2C B2B

Mone0za0on

• IdenHty Layer

• AdverHsing • Payment

ProtecHon/facilitaHon

Licensed CDN

Content Transforma0on

Content Crea0on/Commerce

• Secure Transport

• Secure Display

• CollaboraHon • AccounHng

Data

Security – Site, Content, Commerce Tracking – Commerce, AccounHng etc.

Chris Van Noy 16

Media Warehouse

Chris Van Noy 17

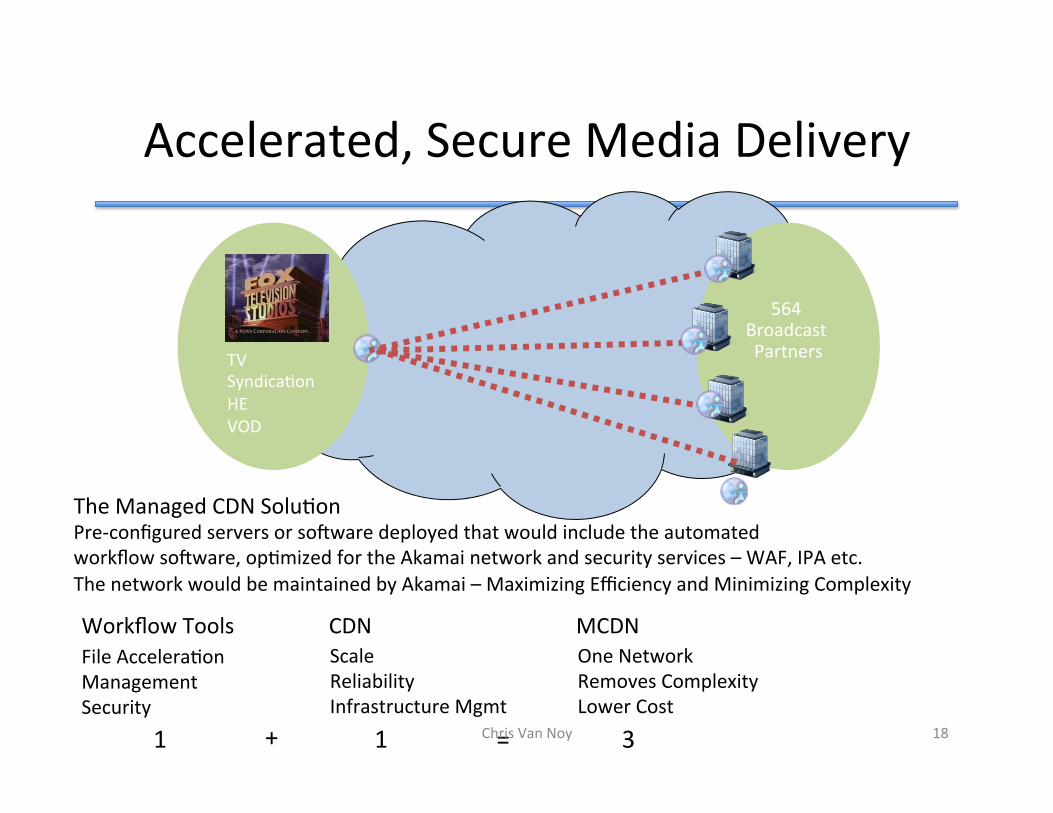

Accelerated, Secure Media Delivery

564 Broadcast Partners TV

SyndicaHon HE VOD

The Managed CDN SoluHon Pre-‐configured servers or so|ware deployed that would include the automated workflow so|ware, opHmized for the Akamai network and security services – WAF, IPA etc. The network would be maintained by Akamai – Maximizing Efficiency and Minimizing Complexity

Workflow Tools CDN File AcceleraHon Management Security

1 + 1 = 3

Scale Reliability Infrastructure Mgmt

One Network Removes Complexity Lower Cost

MCDN

Chris Van Noy 18

Studios (Theatrical, HE Combined)

Metadata File

Mezzanine File

Supplemental

Material

Enhanced Services, Fulfillment & DistribuHon

Theaters InternaHonal DistribuHon

Display

Sy

stem

s Contract Management Business Intelligence Product Metadata Rights & Avails

Fulfillment Metadata Mgmt Transcoding

EncrypHon/DRM Storage

Enhanced Services Packaging SubHtling

Dubbing, etc. QC

DistribuHon Fast Transfer Physical Satellite

Billing & Finance OperaHons/ReporHng Digital Asset Management

Theatrical Workflow -‐ Physical

ProducHon

File

Archive Long Term Archive Disaster Recovery

Retailers Cable /

Broadcasters / Satellite

Digital Cinema

Closed Networks

DVD Distributors

Film Asset

DVD / Blu-‐Ray

MPEG 2

Development Pre-‐ProducHon

Sales Manufacturing

MarkeHng Stream Screeners Ancillary Media AdverHsing

Measurement

Post-‐ProducHon Transport Mezz Enhance Video

OperaHons Archive

Transport Mezz Externally

ProducHon Transport Video Stream Dailies

AccounHng Asset Tracking Royalty/Rights

Tracking

Tape Asset

Chris Van Noy 19

Development Pre-‐ProducHon

Sales Manufacturing

Studios (Theatrical, HE Combined)

Metadata File

Mezzanine File

Supplemental

Material

Enhanced Services, Fulfillment & DistribuHon

Intermediary

Display AdverHsing Payment

Authen/Author Metadata MGMT

DRM RecommendaHons Asset Rights Data

E-‐Retailers E-‐Retailer Servicing

Storefront/ Inventory Storage CMS

Media ID Media

Recommend Secure CE delivery Ad MGMT

Cloud

POS Royalty Statements Intermediaries

Contract Terms Pricing Promos DistribuHon Availability

Sy

stem

s Contract Management Business Intelligence Product Metadata Rights & Avails

Audience Measurement

Royalty/Revenue Tracking & Fulfillment

Asset profitability Measurement

Fulfillment Metadata Mgmt Transcoding

EncrypHon/DRM Watermarking

Storage

Enhanced Services Packaging SubHtling

Dubbing, etc. QC

DistribuHon Fast Transfer Physical Satellite

MarkeHng Stream Screeners Ancillary Media AdverHsing

Measurement

Post-‐ProducHon Transport Mezz Enhance Video

OperaHons Archive

Transport Mezz Externally

ProducHon Transport Video Stream Dailies

AccounHng Asset Tracking Royalty/Rights

Tracking

Billing & Finance OperaHons/ReporHng Digital Asset Management

Theatrical Workflow -‐ Digital

ProducHon

File

Archive Long Term Archive Disaster Recovery

Mezzanine or Display

File

Metadata File

Supplemental

Material

Chris Van Noy 20