contingent convertibles' the world of cocos -...

TRANSCRIPT

February 2014

'Contingent Convertibles'

The World of CoCos

Jan De Spiegeleer & Wim Schoutens

February 2014

Reacfin's 10th anniversary event

2 Outline

Introduction (Wim)

n Contingent Capital

n The life of a CoCo

n Pro’s and con’s

n Issuers and investors

Regulatory Aspects (Jan)

n Basel III and CRD4

n Bail in vs CoCos

Quantitative Side of CoCos (Wim)

n Anatomy of CoCos

n Modelling CoCos

Risk Management of CoCos (Jan)

n New instruments, new risks.

n The Death-Spiral effect

n Extension Risk

3 Introduction

A Contingent Convertible (CoCo) bond is a debt instrument that converts into equity or writes down as soon as the banks gets into a life threatening situation. Conversion/write down happens via a predefined trigger mechanism: e.g. Common Equity Tier-1 (CET1) falling below 7% and is often accompanied with a regulatory trigger. For CoCos with a conversion feature, this creates dilution for existing shareholders, but protects potentially taxpayers.

4 What is a CoCo ?

In the aftermath of the financial crisis Contingent Capital solutions were proposed to strengthen bank’s Additional Tier 1 (AT1) and Tier 2 (T2) capital levels.

CoCos are such AT1 or T2 instruments and are situated in the hybrids area of the balance sheet in between equity and traditional debt.

Under the new EU Capital Requirements Directive (CRD4), all new AT1 capital needs to have CoCo features.

5 What is a CoCo ?

n CoCos are issued as bonds, but the more the bank is in trouble, the more CoCos start behaving as equity.

n How to model it: as fixed income or as equity ?

n How to threat it : as a child or and adult ?

6 What is a CoCo ?

n CoCos are issued as bonds, but the more the bank is in trouble, the more CoCos start behaving as equity.

n How to model it: as fixed income or as equity ?

n How to threat it : as a child or and adult ?

“Like teenagers, they spend many hours in their bedrooms, suspiciously quiet, you never knowing what they are up to, and then suddenly there’s an outburst of sound and fury, the cause of which you never understand. Hybrid instruments and teenagers are both to be treated with love and understanding.”

Paul Wilmott

7 The Life of a CoCo

ISSUE C C C C C C C C C REDEMPTION

C C DISTRESS

Regulatory Trigger

Core Tier 1 Trigger

Bondholder becomes Shareholder or

Bond is (partially) written down

NEW ISSUE Coupon Payments

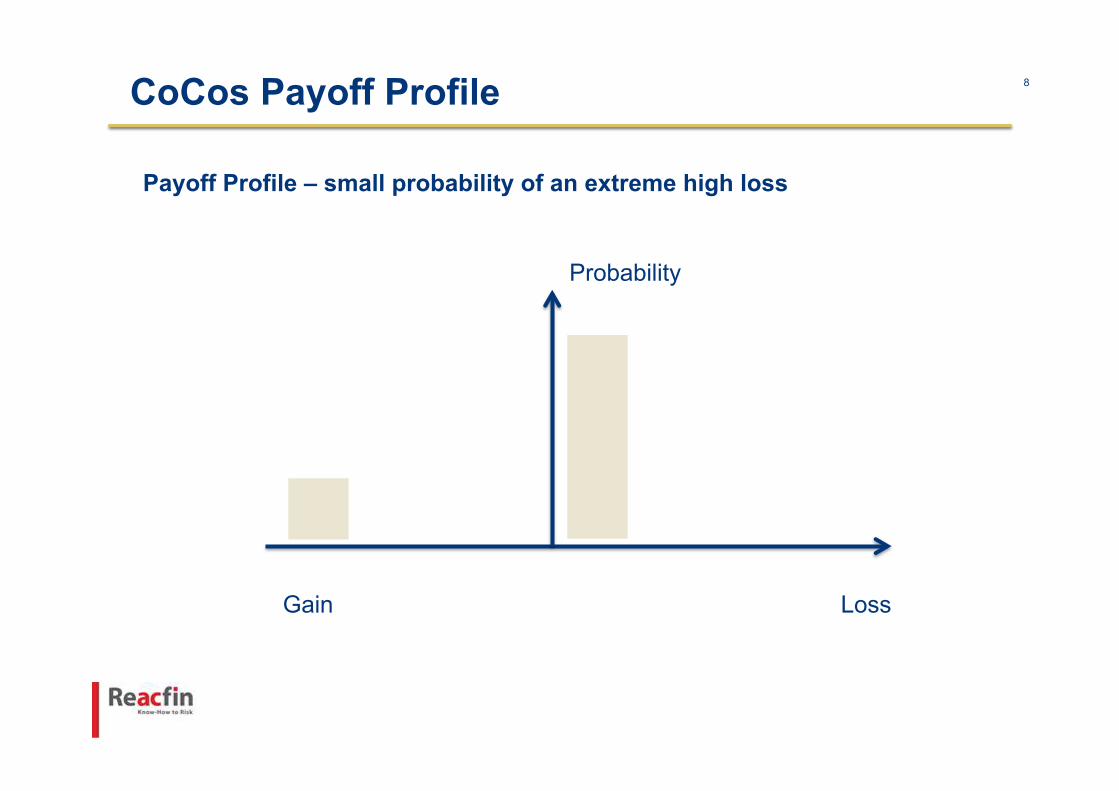

8 CoCos Payoff Profile

Payoff Profile – small probability of an extreme high loss

Gain Loss

Probability

9 Introduction: CoCos Nature

Difference with convertible bonds • High coupons

• Unlimited Downside

(No Bond Floor)

• Limited Upside (Bond Ceiling)

• Negative convexity

10 Major Outstanding European CoCos (Feb/2014)

10

11 CoCo Yield Breakdown • Interest component: in the present low interest rate

environment rather small.

• Liquidity component: CoCos are new asset class with only relative liquidity and a still a lot of regulatory uncertainty and model uncertainty.

• Extension risk component: Most CocCs are callable bonds . However most of the time no step-up is present/allowed.

• Coupon cancellation risk: For some CoCos (T1) coupons are cancellable at the discretion of the issuer/regulator. They are typically non cumulative.

• Conversion component: compensates for the event that the CoCo bond is converted into equities or reduced in value.

• Optional Conversion component: reduces because of the right of the investor to participate in the positive performance of the underlying shares (CoCoCo only).

12 CoCo Yield Breakdown • Interest component: in the present low interest rate

environment rather small.

• Liquidity component: CoCos are new asset class with only relative liquidity and a still a lot of regulatory uncertainty and model uncertainty.

• Extension risk component: Most CocCs are callable bonds . However most of the time no step-up is present/allowed.

• Coupon cancellation risk: For some CoCos (T1) coupons are cancellable at the discretion of the issuer/regulator. They are typically non cumulative.

• Conversion component: compensates for the event that the CoCo bond is converted into equities or reduced in value.

• Optional Conversion component: reduces because of the right of the investor to participate in the positive performance of the underlying shares (CoCoCo only).

150 - 300 bp

400 - 500 bp

50 -100 bp

25 - 50 bp

13 CoCo Yield Breakdown On average, CoCos offer a 4 times spread pickup over senior, or over 400 basis points in absolute terms.

14 Who buys CoCos ?

14

n Asset Managers: Have the expertise and have previously been exposed to hybrid instruments (pre-2008). Have large existing holdings in T1-T2 products. There have been some recent launches of CoCo funds.

n Hedge Funds Have more risk-appetite and have the experience to hedge to some extend the unwanted risks away.

n Insurance Industry Solvency II favors short dated, high rated debt. This is opposite to what CoCos stand for. However the extra yield is often attractive.

n Employees Some investment banks (Barcap, CS) pay CoCo bonuses to their top-management.

15 CoCo Issuance

Dec−09 Dec−10 Jan−12 Jan−13 Feb−140

10

20

30

40

50

60

70

T

USD

(bn)

European Contingent Convertible Issuance

CoCo BondsCoCo Bonds (Write Down)CoCo Bonds (Equity Conversion)

16

Dec−09 Dec−10 Jan−12 Jan−13 Feb−140

10

20

30

40

50

60

70

T

USD

(bn)

European Contingent Convertible Issuance

CoCo BondsCoCo Bonds (Write Down)CoCo Bonds (Equity Conversion)

CoCo Issuance : Lloyds (December 2009)

“…its worth a try…” Mervin King Governor Bank of England

17

Dec−09 Dec−10 Jan−12 Jan−13 Feb−140

10

20

30

40

50

60

70

T

USD

(bn)

European Contingent Convertible Issuance

CoCo BondsCoCo Bonds (Write Down)CoCo Bonds (Equity Conversion)

CoCo Issuance : “Swiss Finish”

“…A finishing school (or charm school) is a private school for girls that emphasizes training in cultural and social activities. The name reflects that it follows on from ordinary school and is intended to complete the educational experience, with and emphasis on etiquette….” CoCos are the finishing touch in the strengthening of the capital of the Swiss banks.

18

Dec−09 Dec−10 Jan−12 Jan−13 Feb−140

10

20

30

40

50

60

70

T

USD

(bn)

European Contingent Convertible Issuance

CoCo BondsCoCo Bonds (Write Down)CoCo Bonds (Equity Conversion)

CoCo Issuance : Lloyds (December 2009)

Write Down CoCo bonds outnumber Equity Conversion CoCos

19 CoCos Pros and Cons

Can they save the banking system ? þ extra buffer þ clear upfront conditions þ no taxpayer money at stake þ coco-bonus þ ...

Caveats : n if held by financial institutions,

no reduction of systemic risk n death spiral n can work too slow n ...

20 Regulatory Aspects

21 Avoiding the use of tax payers’ money

Avoiding the use of tax payers’ money

Make bank failure less disruptive

Resolution Authority Living Wills

Make bank failure less

likely

Make banks less volatile

Dodd Frank Ring Fencing

Central Clearing

Make bank debt loss absorbing

Contingent Capital

Bail-In Capital

BASEL III

22 Basel III world : CoCo Friendly

n Regulatory Capital needs to be loss absorbing

n CoCo Bonds are allowed in the capital structure

– 2% Tier 2

– 1.5% Additional Tier 1

► 5.125% Trigger

► Discretionary Coupons

► Perpetual with no incentive to redeem early

► Callable after 5 year

► Subordinated

► Regulatory trigger (Point-of non-viability)

n Leverage Ratio Calculations

n ECB’s comprehensive assessment (2014)

23 CoCos and the ECB’s comprehensive assessment (2014)

Risk Assessment • Liquidity • Funding • Leverage

Asset Quality Review

Stress test • Baseline Scenario • Adverse Scenario

24 CoCos and the ECB’s comprehensive assessment (2014)

CoCos can be used to offset the capital shortfall. The caveat is here the fact that the AT1 CoCo bonds have their trigger set at 5.125%. They therefore cannot be put at work in the stress tests.

Risk Assessment • Liquidity • Funding • Leverage

Asset Quality Review

Stress test • Baseline Scenario (8% CET1)

• Adverse Scenario (5.5% CET1)

Basel III world : CoCo Friendly

25

Jan10 Jan11 Jan12 Jan13 Dec130

5

10

15

20

25

30

35Issuance of Contingent Capital in Europe

T

Issu

e S

ize

($ b

n)

Additonal Tier 1Tier 2

The main focus of the European banks since Q3-2013 was on the issuance of AT1-CoCo Bonds

26 Basel III world : CoCo Un-Friendly

n CoCo Bonds are not-allowed to deal with the extra capital imposed on globally systematic important institutions (G-Sibs)

27 Will CoCo’s Trigger ?

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50 9.00 9.50

Counter Cyclical Buffer

Capital Conservation Buffer Core Equity

28 Will CoCo’s Trigger ?

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50 9.00 9.50

Counter Cyclical Buffer

Capital Conservation Buffer Core Equity

Bank is insolvent in Basel III (CET1<4.5%)

7% CoCo Trigger will recapitalize the bank automatically

29 Will CoCo’s Trigger ?

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 5.50 6.00 6.50 7.00 7.50 8.00 8.50 9.00 9.50

Counter Cyclical Buffer

Capital Conservation Buffer Core Equity

7% CoCo Trigger will recapitalize the bank automatically

As soon as the bank “eats” into its buffers, it will no longer have the initiative : coupon payments, bonus payments are under regulatory scrutiny

Banks could strengthen their capital base before a trigger occurs !

30 Quantitative Aspects of CoCos

31 All CoCos are different CoCos Anatomy • Maturity (> 5y)

• Coupon (7-10 % ?)

• Trigger Event

§ Accounting: e.g. CET1 <7% § Regulatory Trigger § Market Trigger (not implemented)

• Loss Absorbing Mechanism § Conversion

• Conversion Price = Issue Price (Lloyds) CP = S0

• Conversion Price = fraction of Issue Price (BarCap) CP = α S0

• Conversion Price = Trigger Price CP = S*

• Floored Conversion Price (CS, BBVA, …) CP = max (Floor, S*)

• Write-Down • Partially (Rabo (75%)) • Full (Barclays, KBC, CS,… ) • Staggered (ZKB,…)

Conversion/Write-Down Mechanism determines the Recovery Rate of the CoCo

32 CoCo Pricing

32

n Credit Model (Rule of Thumb)

n Equity Derivatives Model (Barrier Option Pricing)

n Others (academic/hard to calibrate):

- firm value valuation

- jump models

- stochastic vol models

- …

CoCos Pricing Methodologies

- EXPECTED YIELD CALCULATION (8-10% Coupons)

- (PROXY) HEDGING and RISK MANAGEMENT (death spiral effect)

- ISSUE SIZE DETERMINATION (free-float vs short sales) - RELATIVE PRICING (investment strategies) …

33

01−Jan−2013 19−May−2013 05−Oct−2013 31−Dec−201350

100

150

200

250

300

350

400

450

T

bps

RABOBANK CREDIT SPREADS

c=65

c=304

SENIOR (40% Recovery)COCO (25% RECOVERY)

Example 1: The Rabobank cds spread (senior) is 65bp. For an expected recovery rate of 40%, this corresponds to an estimate of λdefault of 1.09% = 0.65%/(1-0.4).

Rule of Thumb Pricing for a CDS: Credit Spread = Expected Loss x Default Intensity

cs = (1 – RCDS) x λdefault

Example : When will the Rabobank CoCo trigger: λtrigger = ? On the trigger event, there is a haircut of 75%. The recovery is hence 25% (RCoCo = 25%). Suppose, the CoCo spread of the Rabobank CoCo is 304 bp. λtrigger = 3.04% / (1-0.25)= 4.05%. Note that conversion happens before default : λtrigger > λdefault

Rule of Thumb Pricing for a CoCo Spread: CoCo spread = (1 – RCoCo) x λtrigger

CoCo Pricing

01−Jan−2013 19−May−2013 05−Oct−2013 31−Dec−201321−Feb−20140.5

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

T

Defa

ult P

rob

(%)

ONE YEAR DEFAULT/TRIGGER PROBABILITY RABOBANK

λDefault =1.09%

λTrigger =4.05%Default ProbTrigger Probability

34 CoCo Pricing : Equity Deriva?ves Approach

34

01−Jan−2013 01−Apr−2013 01−Jul−2013 30−Dec−20138

10

12

14

16

18

20

T

S∗/S(%)

Barclays CoCo Bond − US06740L8C27

Non−Callable CoCo [S1]Callable 10Yr NC5 (priced till call date)

35 Risk Management of CoCos

36 Past Performance doesn’t tell us anything…

Dec−10 Jun−11 Dec−11 Jun−12 Dec−12 Jun−13 Feb−1480

90

100

110

120

130

140

150

160

CoCo (Total Return)MSCIJPM Gvt Bond IndexJP Morgan High Yield Index

37 Past Performance doesn’t tell us anything…

0 2 4 6 8 10 12 142

4

6

8

10

12

14

Realized Volatility (%)

Annu

aliz

ed R

etur

n (%

)

Period:12−31−2010 :14−Feb−2014

CoCo (Total Return)MSCIJPM Gvt Bond IndexJP Morgan High Yield Index

Tail Risk

Volatility

38 Death Spiral Risk

The existence of the death-spiral puts a cap on the maximum amount of CoCos a bank can issue.

Death Spiral Risk

Death Spiral Risk increases over time

40 Combing with convertible bonds ? No !

n Convertible bonds have a positive convexity in normal market circumstances

n In distressed market circumstances, the opposite is true

∂2P∂S2

> 0

41 Extension Risk

n The increased issuance of AT1 CoCo bonds emphasizes the extension risk

Jan10 Jan11 Jan12 Jan13 Dec130

5

10

15

20

25

30

35Issuance of Contingent Capital in Europe

T

Issu

e S

ize

($ b

n)

Additonal Tier 1Tier 2

42 Extension Risk

n The increased issuance of AT1 CoCo bonds emphasizes the extension risk

n Companies do not necessarily call back their bonds on the first call date

n Example : Deutsche Bank did not call back a bond in Dec 2008. The market price of the bond dropped 10%

43 Extension Risk

Source : barclays capital

Extending a bond creates no longer a reputational issue

44 Extension Risk

n CoCo bonds cannot be considered to expire on the first call date

n The extension risk has been embedded into our two approaches :

– Credit Derivatives Method

– Equity Derivatives Method

n New Concepts

– Expected Maturity Date

– Expected Extension Period

– Call Probability

– …

n Explanation is available for downloading : http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2390344

45 Extension Risk : Example

Implied Trigger level for Barclays

01−Jan−2013 01−Apr−2013 01−Jul−2013 30−Dec−20138

10

12

14

16

18

20

T

S∗/S(%)

Barclays CoCo Bond − US06740L8C27

Non−Callable CoCo [S1]Callable 10Yr NC5 (priced till call date)

Implied Trigger Levels should not be different ? S*Callable > S*Non-Callable The higher trigger level materializes the extension risk. The bond does not expire on the first call date

46 Extension Risk : Example

Implied Trigger level for Barclays

01−Jan−2013 01−Apr−2013 01−Jul−2013 30−Dec−20138

10

12

14

16

18

20

T

S∗/S(%)

Barclays CoCo Bond − US06740L8C27

Non−Callable CoCo [S1]Callable 10Yr NC5 [S2]Callable 10Yr NC5 (with Extension Risk) [S3]

Adjusting the model for a possible Extension risk creates a better fit between S*Callable and S*Non-Callable for the CoCo Bond

48

References

[1] De Spiegeleer, J. and Schoutens W. (2011) Contingent Convertible Coco-Notes: Structuring & Pricing. EuromoneyBooks. [2] De Spiegeleer, J. and Schoutens, W. (2012) Pricing Contingent Convertibles: A Derivatives Approach. Journal of Derivatives, Vol. 20, No. 2: pp. 27-36. [3] De Spiegeleer, J., Schoutens, W. (2012). Steering a bank around a death spiral: Multiple Trigger CoCos. Wilmott Magazine, 2012 (59), 62-69. [4] De Spiegeleer, J., Schoutens, W. (2013) Multiple Trigger CoCos: Contingent debt without death-spiral risk. Financial Markets, Institution and Instruments Journal 22 (2). [5] Corcuera, J. M., De Spiegeleer, J., Ferreiro-Castilla, A., Kyprianou, A.E, Madan, D., Schoutens, W. (2013), Pricing of Contingent Convertibles under Smile Conform Models. Journal of Credit Risk, Journal of Credit Risk 9(3), 121–140. [6] Maes, S. and Schoutens, W. (2012) Contingent Capital: An In-Depth Discussion, Economic Notes, vol. 41, no. 1/22, pp. 59–79 [7] De Spiegeleer, J., Forys, M., Schoutens, W. (2012). Contingent Convertibles. In: Encyclopedia of Debt Finance Euromoney Books. [8] De Spiegeleer, J., Van Hulle, C., Schoutens, W. (2011). Cracking the coco pricing conundrum, July issue, 20-21 pp: CreditFlux. [9] Madan, D.B. and Schoutens, W. (2011) Conic coconuts: the pricing of contingent capital notes using conic finance , Mathematics and Financial Economics, Volume 4, Issue 2, pp 87-106. [10] Campolongo, F., De Spiegeleer, J., Di Girolamo, F. and Schoutens W. (2012) Contingent Conversion Convertible Bond: New avenue to raise bank capital. Working paper. [11] De Spiegeleer, J., Dhaene, J. and Schoutens, W. (2013). Swiss Re’s $750m solvency trigger coco is much riskier than it seems. Credit Flux. Technical Analysis, April 2013. [12] Corcuera, J.M., De Spiegeleer, J., Fajardo, J., Jönsson, H., Schoutens W. and Valdivia, A. (2014) Close form pricing formulas for CoCa CoCos, Journal of Banking and Finance, to appear. [13] De Spiegeleer, J., Van Hulle, C., Schoutens, W. (2014). The Handbook of Hybrid Securities: Convertible Bonds, CoCo Bonds and Bail-In, The Wiley Finance Series.

49 APPENDIX

50 CoCos Anatomy (APPENDIX)

Inconsistency in how the conversion to equity takes place

Dec−09 Dec−10 Jan−12 Jan−13 Feb−140

10

20

30

40

50

60

70

T

USD

(bn)

European Contingent Convertible Issuance

CoCo BondsCoCo Bonds (Write Down)CoCo Bonds (Equity Conversion)

51

ASSUME: Triggering happens when the stock prices hits a certain barrier. We replace the “CET1 falling below X%”event by “Stocks hits the a low barrier H”.

• For Equity Conversion CoCos, the expected loss is determined by the value of the shares (S*) when conversion takes place : The CoCo investor pays Cp for each share with value S*: Recovery Rate (%) = RCoCo = S* / Cp

CoCo Pricing (APPENDIX)

Rule of Thumb Pricing : CoCo spread = (1 – S* / Cp) x λtrigger Equity Model: Smile Adjusted Black-Scholes

52

• We break down a CoCo bond into different derivative instruments:

A. Face Value + Coupons: BOND (long)

B. Conversion into stock: DOWN-AND-IN-FORWARD (long) Write-down: BINARY DOWN-AND-IN-BARRIER (short)

C. Cancellation of Coupons BINARY DOWN-AND-IN BARRIERS (short)

CoCo Pricing : Equity Deriva?ves Approach (APPENDIX)

CoCo Price = A (Bond Part) + B (Loss Absorption) + C (Coupon Loss)

Pricing formula needs essentially two inputs: Volatility σ and implied trigger level S*