convenience store merchandising study pt1 store... · znacs state of the industry report identified...

TRANSCRIPT

0

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Convenience Store Impulse

Merchandising Study

1

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Key Issues Facing Convenience Retailers

NACS State of the Industry Report identified that pre-tax profits had rebounded in 2003, after 3 years of declines and for the first time in many years actual store counts were down

Pay at the pump and shrinking gasoline margins are a sizeable industry threat

Traditional high volume tobacco sales continue to decline

Labor costs on the rise

Household penetration is flat as is shopping frequency

Drug stores targeting the Convenience tripSource: MVI, Retail Forward;DHC.

2

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Opportunities For Channel Growth

Expansion of Food Service offerings

Understanding the impact of changing consumer demographics

Driving more gas purchasers into the store

Drive up the size of the market basket

Focusing on product mix to maximize your most profitable categories

Sharing merchandising best practices

Source: MVI, Retail Forward; DHC.

3

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

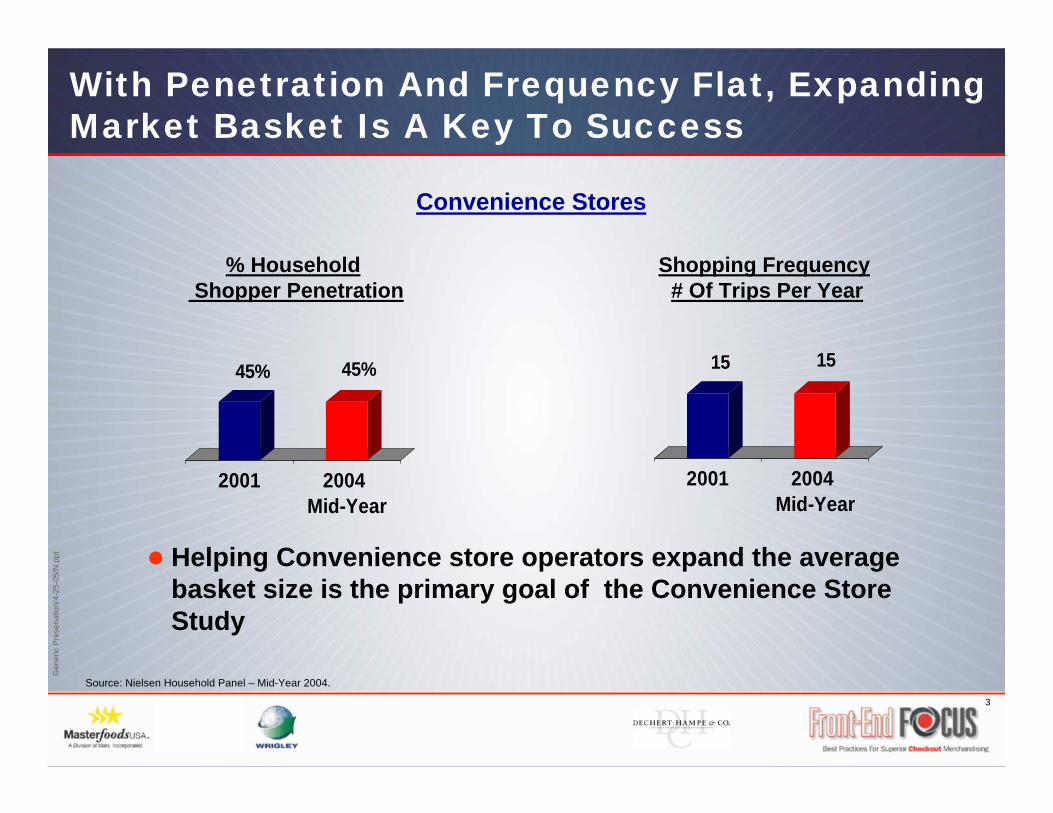

With Penetration And Frequency Flat, Expanding Market Basket Is A Key To Success

% Household Shopper Penetration

Shopping Frequency # Of Trips Per Year

Helping Convenience store operators expand the average basket size is the primary goal of the Convenience Store Study

Source: Nielsen Household Panel – Mid-Year 2004.

45% 45%

2001 2004 Mid-Year

15 15

2001 2004 Mid-Year

Convenience Stores

4

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

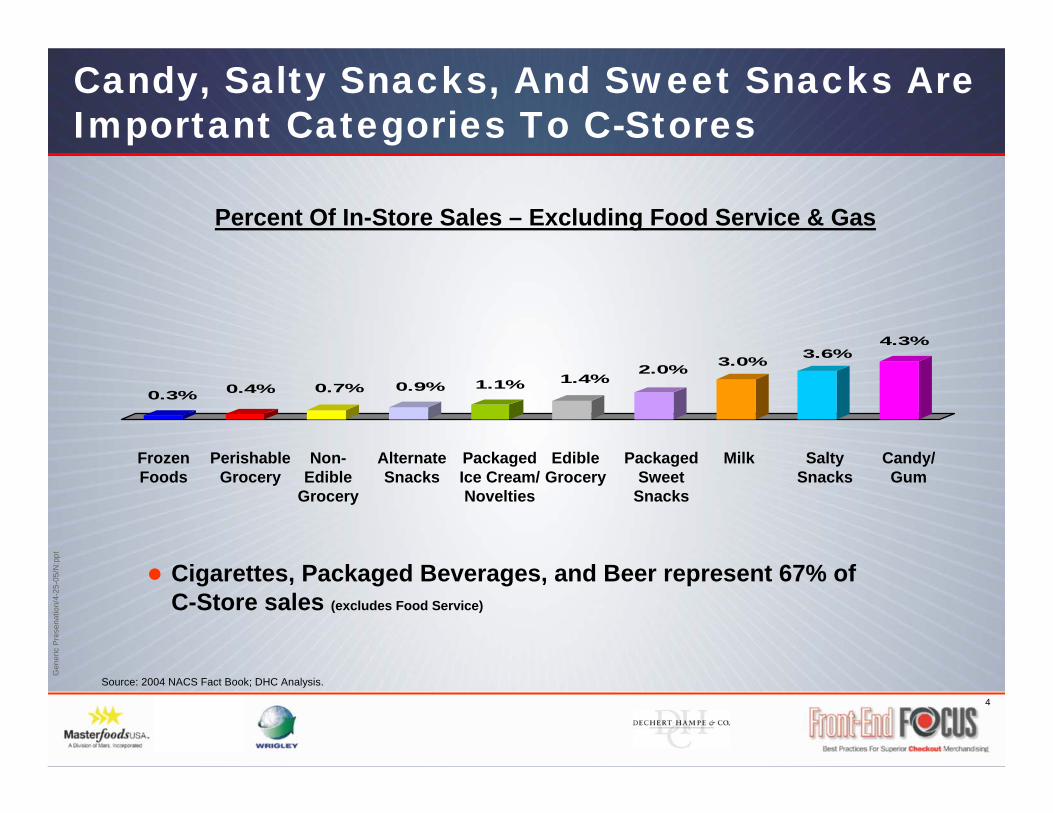

0.3% 0.4% 0.7% 0.9% 1.1% 1.4%2.0% 3.0% 3.6%

4.3%

Candy, Salty Snacks, And Sweet Snacks Are Important Categories To C-Stores

Source: 2004 NACS Fact Book; DHC Analysis.

Percent Of In-Store Sales – Excluding Food Service & Gas

Frozen Foods

Perishable Grocery

Non-Edible

Grocery

Alternate Snacks

Packaged Ice Cream/ Novelties

Edible Grocery

Packaged Sweet

Snacks

Milk Salty Snacks

Candy/ Gum

Cigarettes, Packaged Beverages, and Beer represent 67% of C-Store sales (excludes Food Service)

5

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

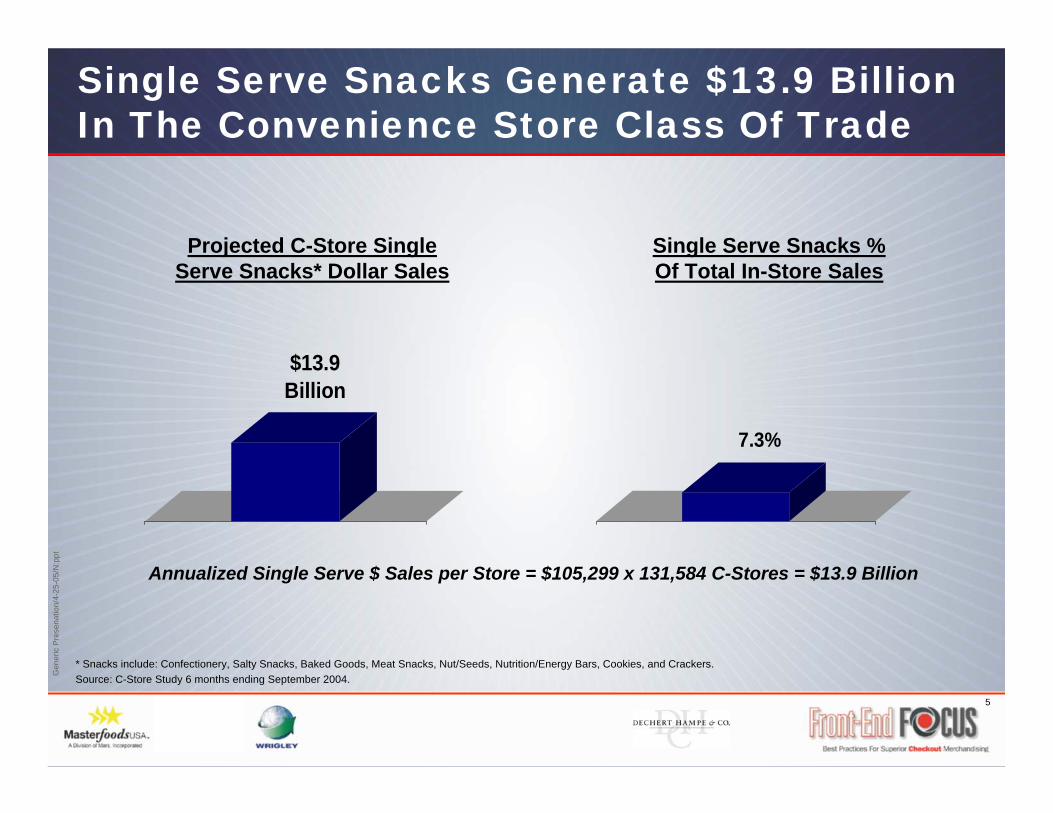

Single Serve Snacks Generate $13.9 Billion In The Convenience Store Class Of Trade

* Snacks include: Confectionery, Salty Snacks, Baked Goods, Meat Snacks, Nut/Seeds, Nutrition/Energy Bars, Cookies, and Crackers.Source: C-Store Study 6 months ending September 2004.

Annualized Single Serve $ Sales per Store = $105,299 x 131,584 C-Stores = $13.9 Billion

$13.9 Billion

Projected C-Store Single Serve Snacks* Dollar Sales

Single Serve Snacks % Of Total In-Store Sales

7.3%

6

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

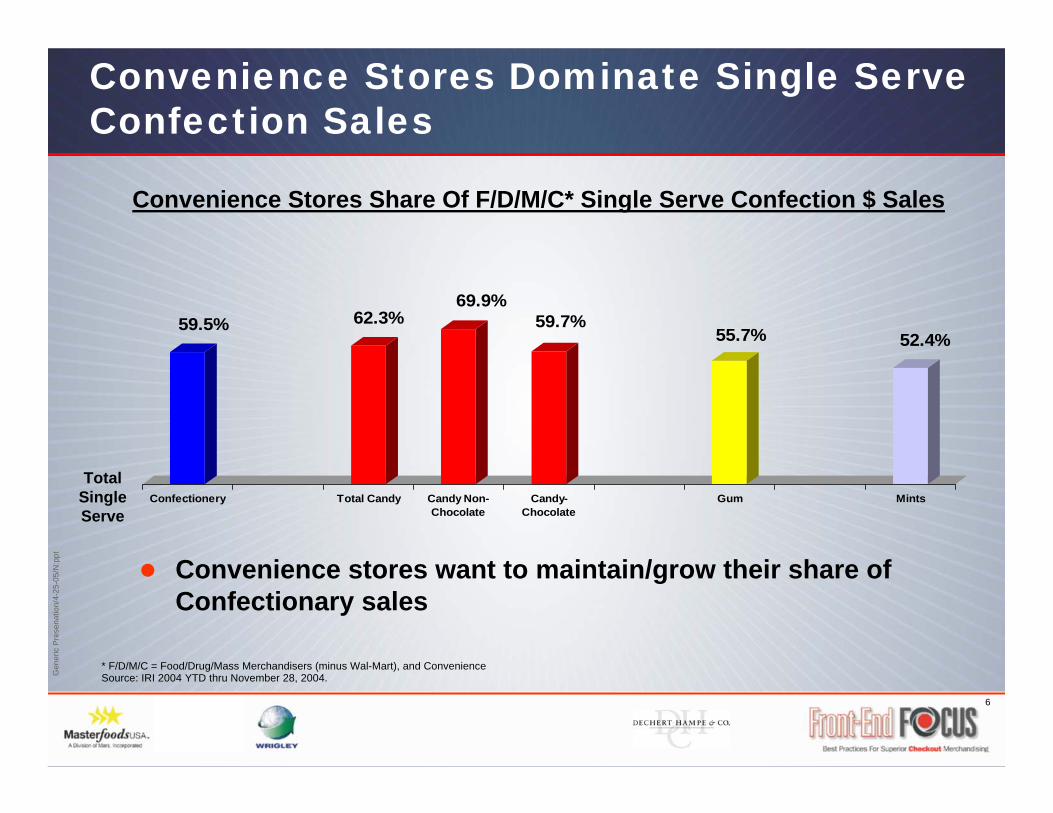

59.5% 62.3%69.9%

59.7%55.7% 52.4%

Confectionery Total Candy Candy Non-Chocolate

Candy-Chocolate

Gum Mints

Convenience Stores Dominate Single Serve Confection Sales

Source: IRI 2004 YTD thru November 28, 2004.

Convenience stores want to maintain/grow their share of Confectionary sales

Convenience Stores Share Of F/D/M/C* Single Serve Confection $ Sales

Total Single Serve

* F/D/M/C = Food/Drug/Mass Merchandisers (minus Wal-Mart), and Convenience

7

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Leadership

8

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Key Elements Of Leadership

Retailer/manufacturer partnerships can improve results for all stakeholders

Leadership is based on an understanding of consumer shopping behavior

Leadership means turning learning and ideas into executable in-store solutions

9

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Leadership Starts With Partnership

Formation of a leadership council including the following manufacturers:

Masterfoods USA, a Division of Mars, Incorporated

The Wm. Wrigley Jr. Company

In partnership with Dechert-Hampe & Company, an independent research and consulting firm

10

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Mission Of The Group

To work in partnership with retail customers and other stakeholders to improve store performance and enhance consumer satisfaction through:

New learning and consumer knowledge

Developing benchmarks and Best Practices

Innovative solutions to optimize in-store merchandising

11

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

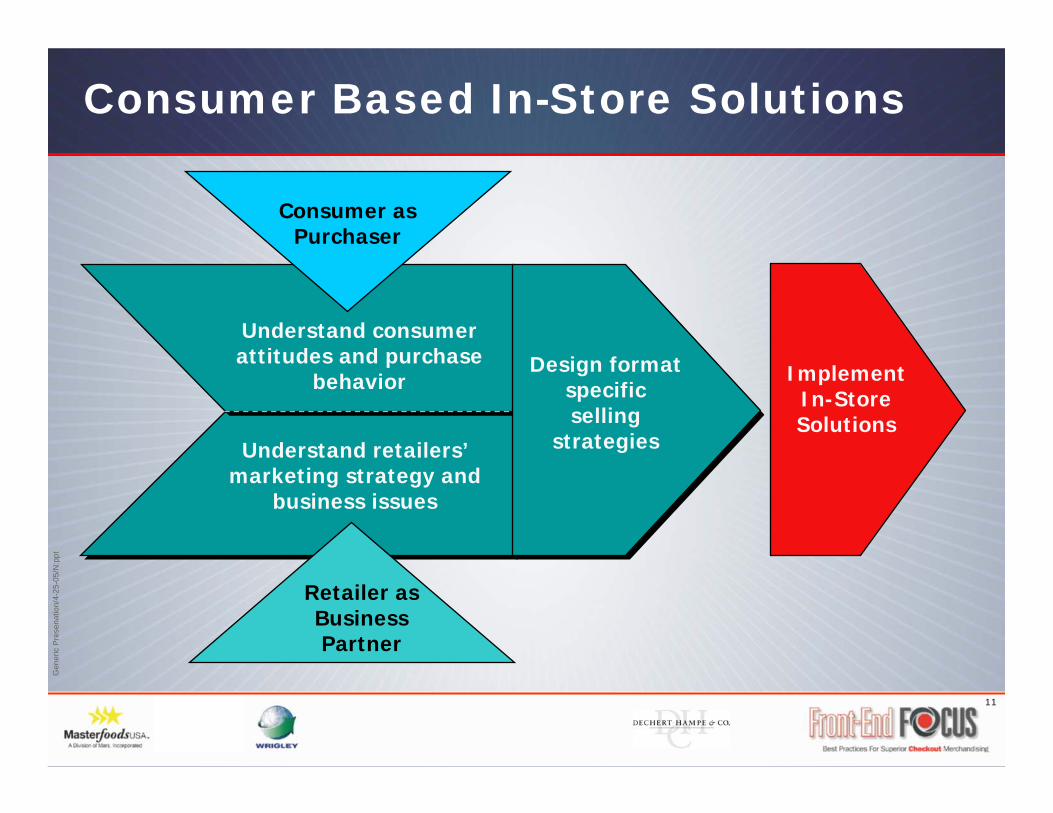

Consumer Based In-Store Solutions

Design format specific selling

strategiesUnderstand retailers’ marketing strategy and

business issues

Understand consumer attitudes and purchase

behavior Implement In-Store Solutions

Consumer as Purchaser

Retailer as Business Partner

12

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Convenience Store Merchandising Study

Objectives

Gain new insights on consumer attitudes and buying behavior in Convenience Stores, especially regarding Single Serve Snacking items, to expand consumer purchase rates

Develop channel performance benchmarks

Identify merchandising “Best Practices” of Single Serve Snacking to expand size of basket to maximize sales and profits

13

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Convenience Store Merchandising Study

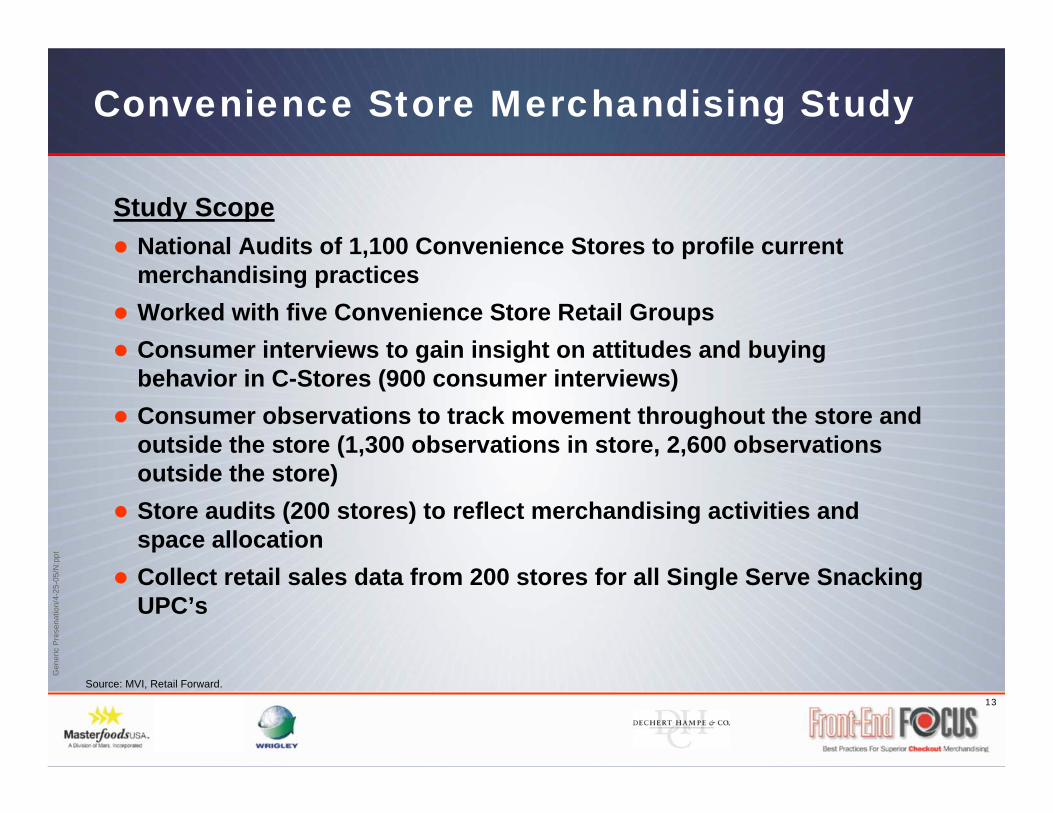

Study ScopeNational Audits of 1,100 Convenience Stores to profile current merchandising practicesWorked with five Convenience Store Retail GroupsConsumer interviews to gain insight on attitudes and buying behavior in C-Stores (900 consumer interviews)Consumer observations to track movement throughout the store andoutside the store (1,300 observations in store, 2,600 observations outside the store)Store audits (200 stores) to reflect merchandising activities and space allocationCollect retail sales data from 200 stores for all Single Serve Snacking UPC’s

Source: MVI, Retail Forward.

14

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

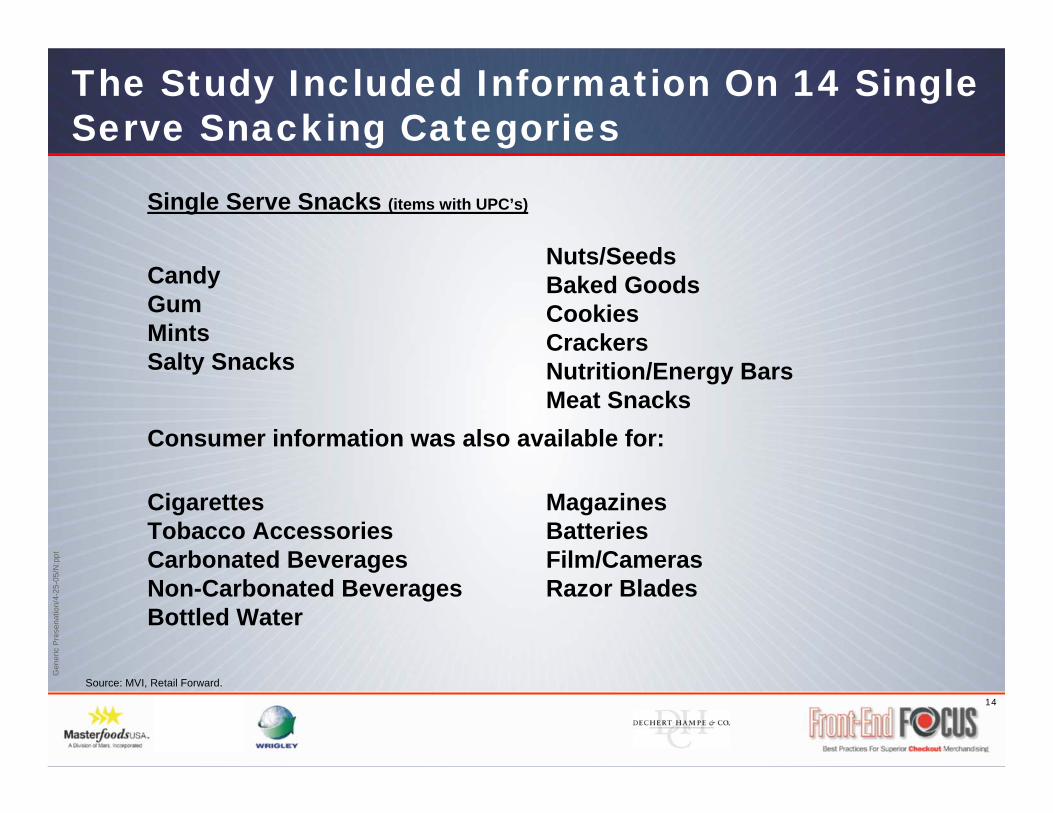

The Study Included Information On 14 Single Serve Snacking Categories

Source: MVI, Retail Forward.

Nuts/SeedsBaked GoodsCookies CrackersNutrition/Energy BarsMeat Snacks

CandyGumMints Salty Snacks

Magazines BatteriesFilm/CamerasRazor Blades

CigarettesTobacco AccessoriesCarbonated BeveragesNon-Carbonated BeveragesBottled Water

Consumer information was also available for:

Single Serve Snacks (items with UPC’s)

15

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Consumer Learning

16

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

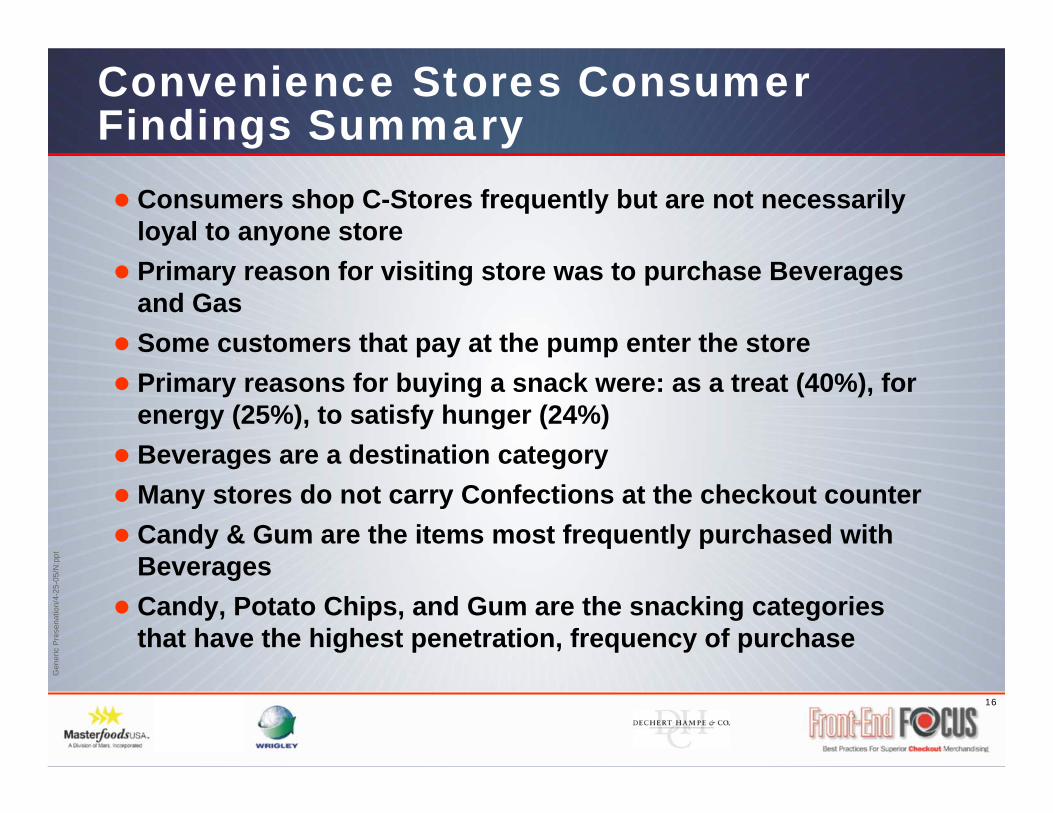

Convenience Stores Consumer Findings Summary

Consumers shop C-Stores frequently but are not necessarily loyal to anyone storePrimary reason for visiting store was to purchase Beverages and GasSome customers that pay at the pump enter the store Primary reasons for buying a snack were: as a treat (40%), for energy (25%), to satisfy hunger (24%)Beverages are a destination categoryMany stores do not carry Confections at the checkout counterCandy & Gum are the items most frequently purchased with BeveragesCandy, Potato Chips, and Gum are the snacking categories that have the highest penetration, frequency of purchase

17

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

84%

13%3%

Once A Week OrMore

Several Times AMonth

Once A Month

C-Store Consumers Will Shop Frequently, But At Multiple Stores

What Percent Of Your C-Store Trips Are At This Store?

29%22%

15%

34%

<25% 26%-50% 51%-75% 76%+

Source: C-Store Study, September 2004.

% Of Respondents

Retailers must focus on getting the most out of each shopping trip

How Often Do You Shop At This Store?

18

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

6%

6%

7%

9%

9%

23%

27%

43%

48%

Restroom

Groceries

Other

Food Service

Lottery

Candy/Gum/Snacks

Cigarettes

Gas

Beverages

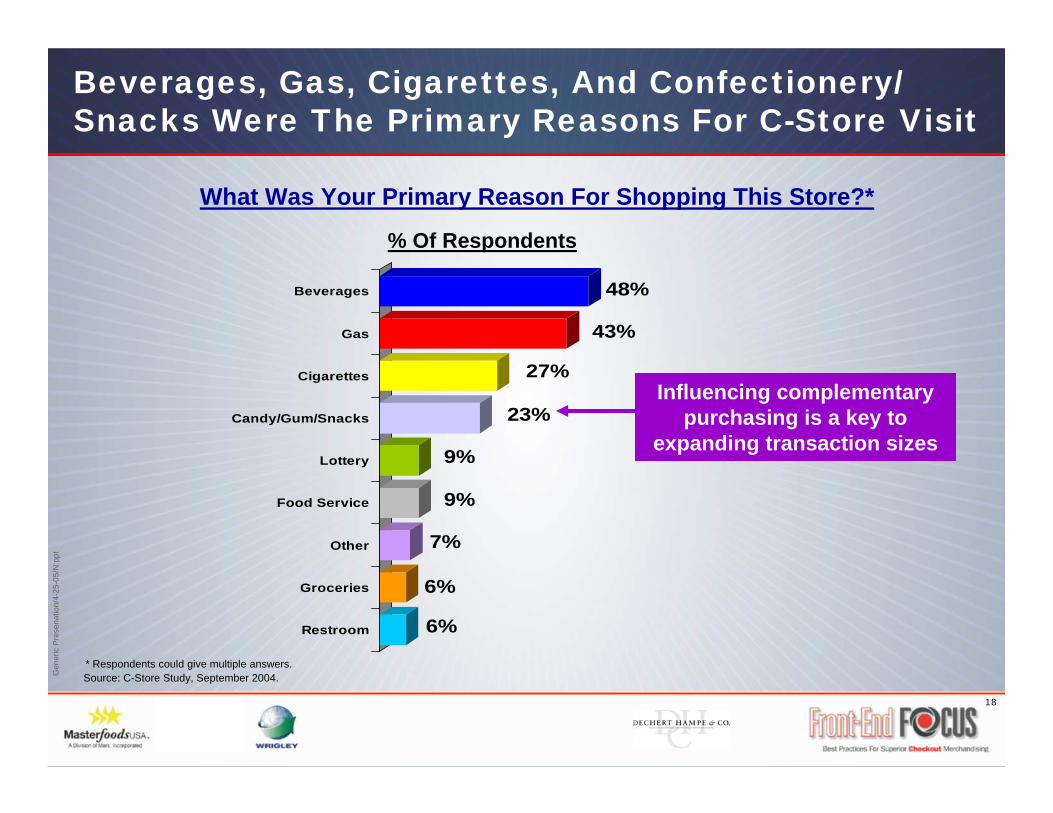

Beverages, Gas, Cigarettes, And Confectionery/ Snacks Were The Primary Reasons For C-Store Visit

What Was Your Primary Reason For Shopping This Store?*

Source: C-Store Study, September 2004.

% Of Respondents

* Respondents could give multiple answers.

Influencing complementary purchasing is a key to

expanding transaction sizes

19

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

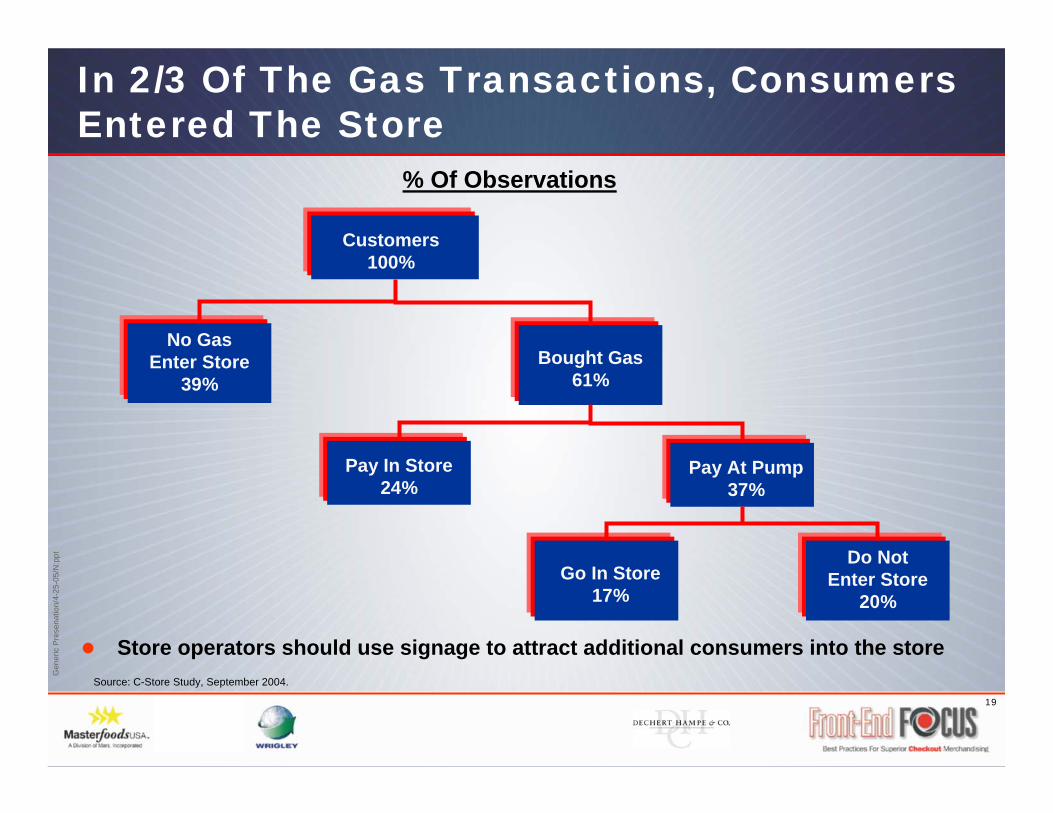

In 2/3 Of The Gas Transactions, Consumers Entered The Store

Source: C-Store Study, September 2004.

Store operators should use signage to attract additional consumers into the store

Do Not Enter Store

20%

No Gas Enter Store

39%

Go In Store17%

Pay At Pump37%

Bought Gas61%

Customers100%

Pay In Store24%

% Of Observations

20

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

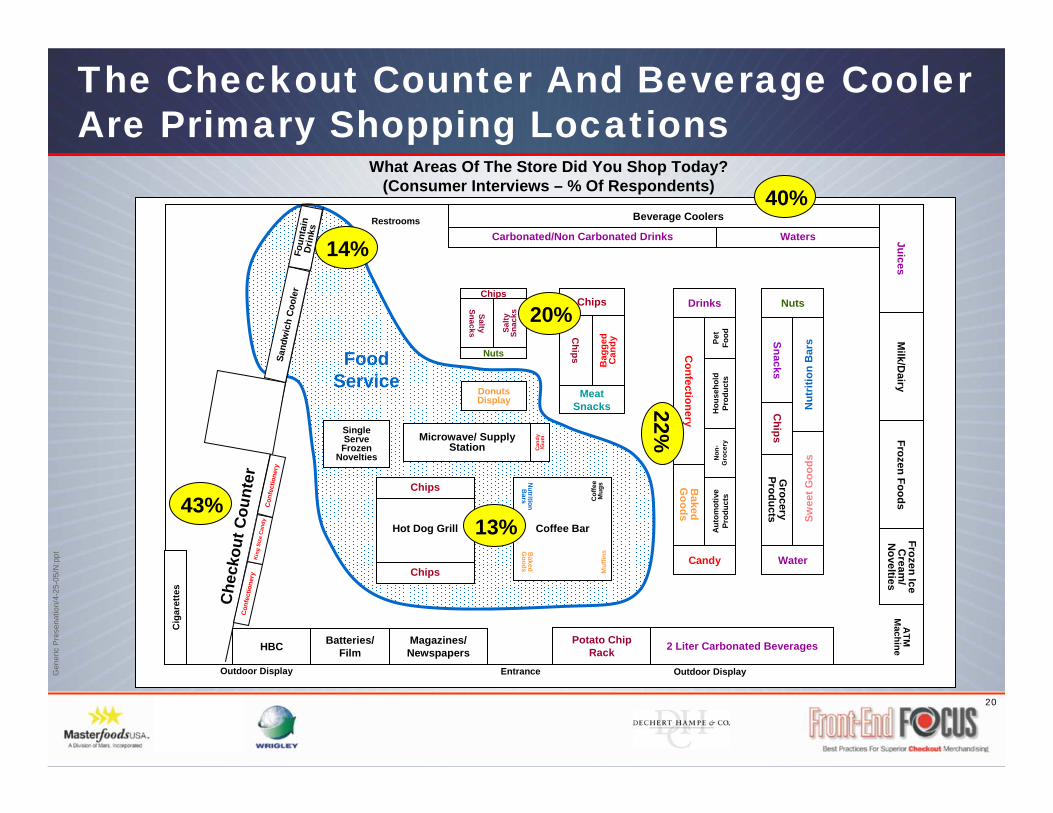

The Checkout Counter And Beverage Cooler Are Primary Shopping Locations

JuicesM

ilk/Dairy

Frozen FoodsFrozen Ice

Cream

/N

oveltiesA

TM

Machine

Potato Chip Rack 2 Liter Carbonated Beverages

Nut

ritio

n B

ars

Swee

t Goo

ds

SnacksG

rocery Products

Nuts

Chips

Water

Bag

ged

Can

dy

Chips

Chips

Meat Snacks

Salty

Sn

acksSalty

Snacks

Chips

Nuts

Donuts Display

Hot Dog Grill

Chips

Chips

HBC Batteries/ Film

Magazines/ Newspapers

Single Serve Frozen

Novelties

Restrooms

Cig

aret

tes

Che

ckou

t Cou

nter

Con

fect

ione

ryK

ing

Size

Can

dyC

onfe

ctio

nery

Sand

wic

h C

oole

rFo

unta

in

Drin

ks

Outdoor Display Outdoor DisplayEntrance

Coffee BarN

utritionB

ars Cof

fee

Mug

sM

uffin

sBaked

Goods

Aut

omot

ive

Prod

ucts

Confectionery

Baked

Goods

Drinks

Candy

Non

-G

roce

ryH

ouse

hold

Pr

oduc

tsPe

t Fo

od

Microwave/ Supply Station C

andy

/Gum

Food Service

Carbonated/Non Carbonated Drinks Waters

Beverage Coolers

What Areas Of The Store Did You Shop Today?(Consumer Interviews – % Of Respondents)

20%

22%

14%

13%

40%

43%

21

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

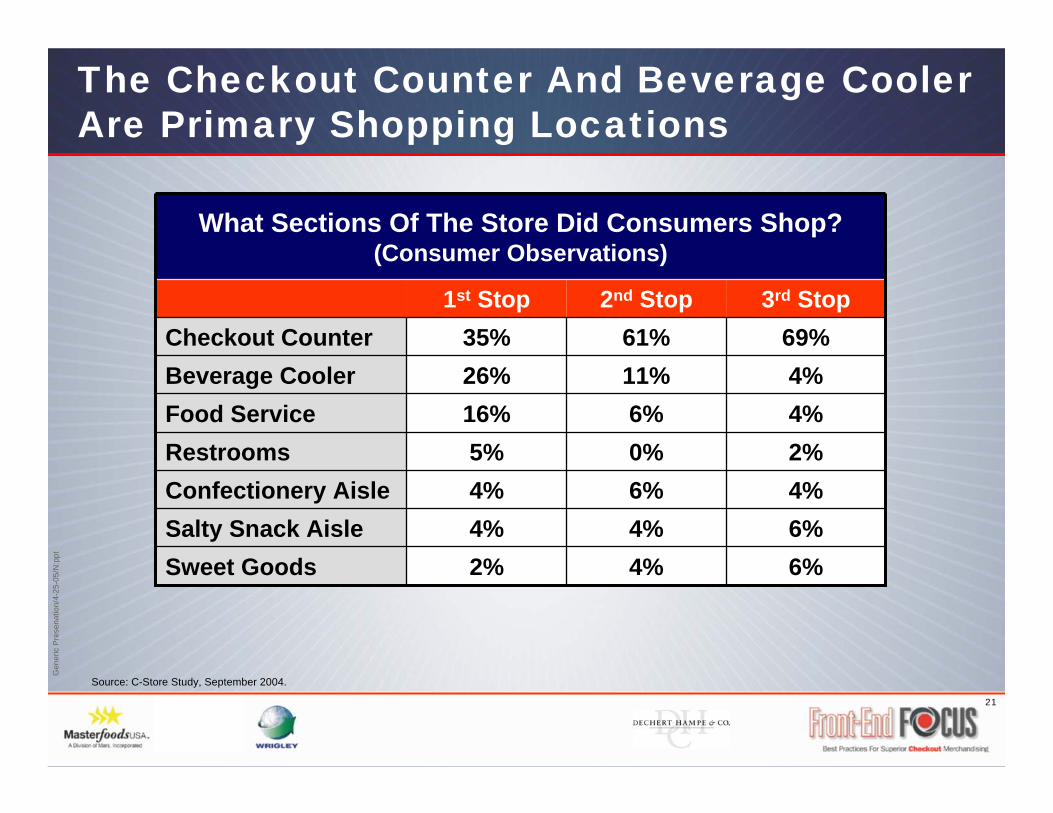

The Checkout Counter And Beverage Cooler Are Primary Shopping Locations

Source: C-Store Study, September 2004.

6%4%2%Sweet Goods6%4%4%Salty Snack Aisle4%6%4%Confectionery Aisle2%0%5%Restrooms4%6%16%Food Service4%11%26%Beverage Cooler

69%61%35%Checkout Counter3rd Stop2nd Stop1st Stop

What Sections Of The Store Did Consumers Shop?(Consumer Observations)

22

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

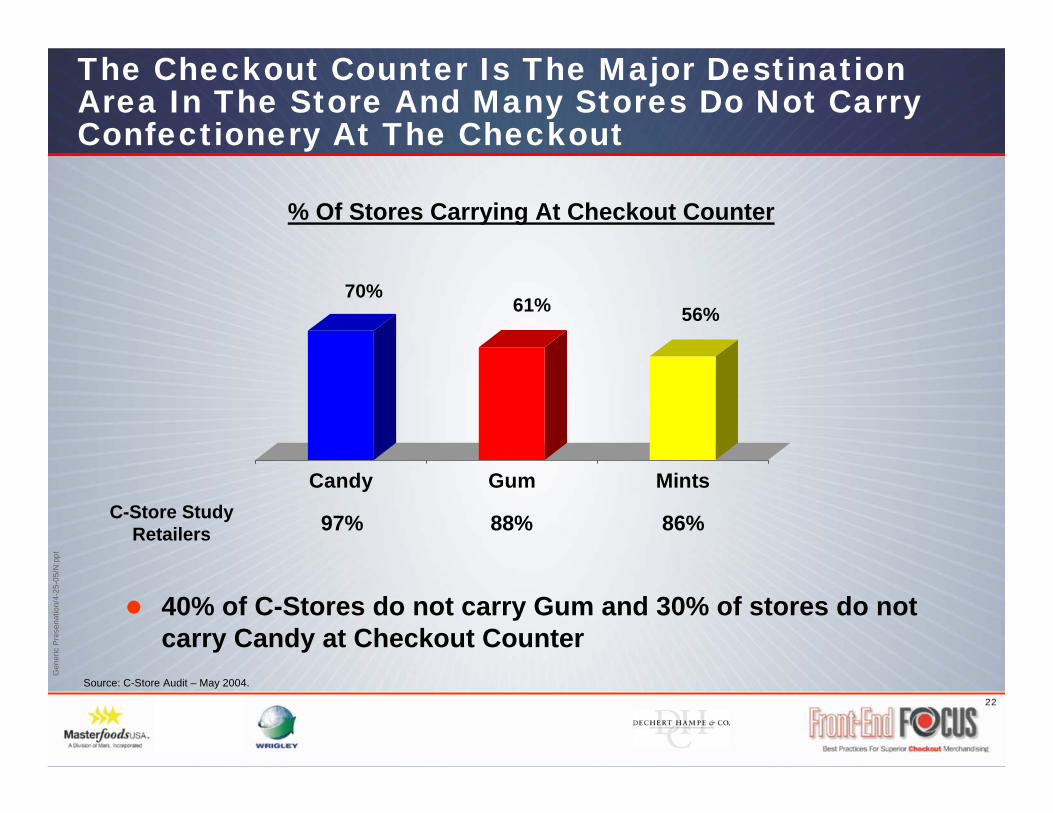

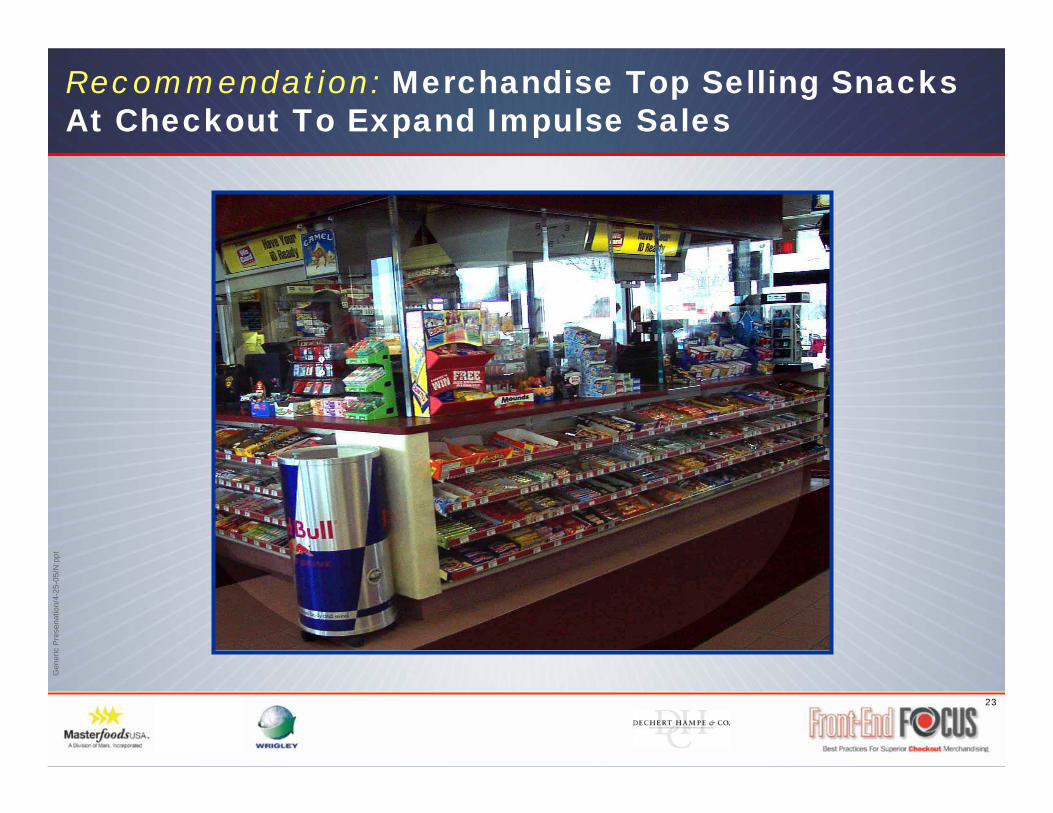

The Checkout Counter Is The Major Destination Area In The Store And Many Stores Do Not Carry Confectionery At The Checkout

% Of Stores Carrying At Checkout Counter

70%61% 56%

Candy Gum Mints

Source: C-Store Audit – May 2004.

40% of C-Stores do not carry Gum and 30% of stores do not carry Candy at Checkout Counter

86%88%97%C-Store Study Retailers

23

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Recommendation: Merchandise Top Selling Snacks At Checkout To Expand Impulse Sales

24

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

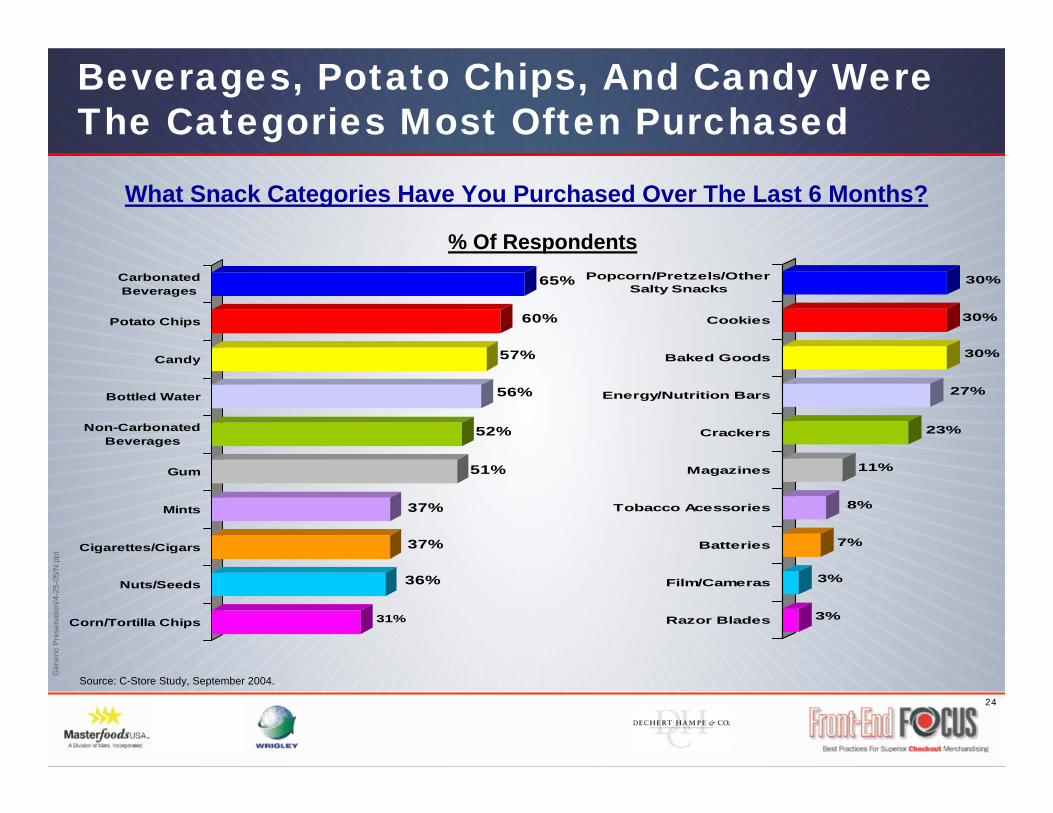

3%

3%

7%

8%

11%

23%

27%

30%

30%

30%Popcorn/Pretzels/OtherSalty Snacks

Cookies

Baked Goods

Energy/Nutrition Bars

Crackers

Magazines

Tobacco Acessories

Batteries

Film/Cameras

Razor Blades31%

36%

37%

37%

51%

52%

56%

57%

60%

65%CarbonatedBeverages

Potato Chips

Candy

Bottled Water

Non-CarbonatedBeverages

Gum

Mints

Cigarettes/Cigars

Nuts/Seeds

Corn/Tortilla Chips

Beverages, Potato Chips, And Candy Were The Categories Most Often Purchased

Source: C-Store Study, September 2004.

What Snack Categories Have You Purchased Over The Last 6 Months?

% Of Respondents

25

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

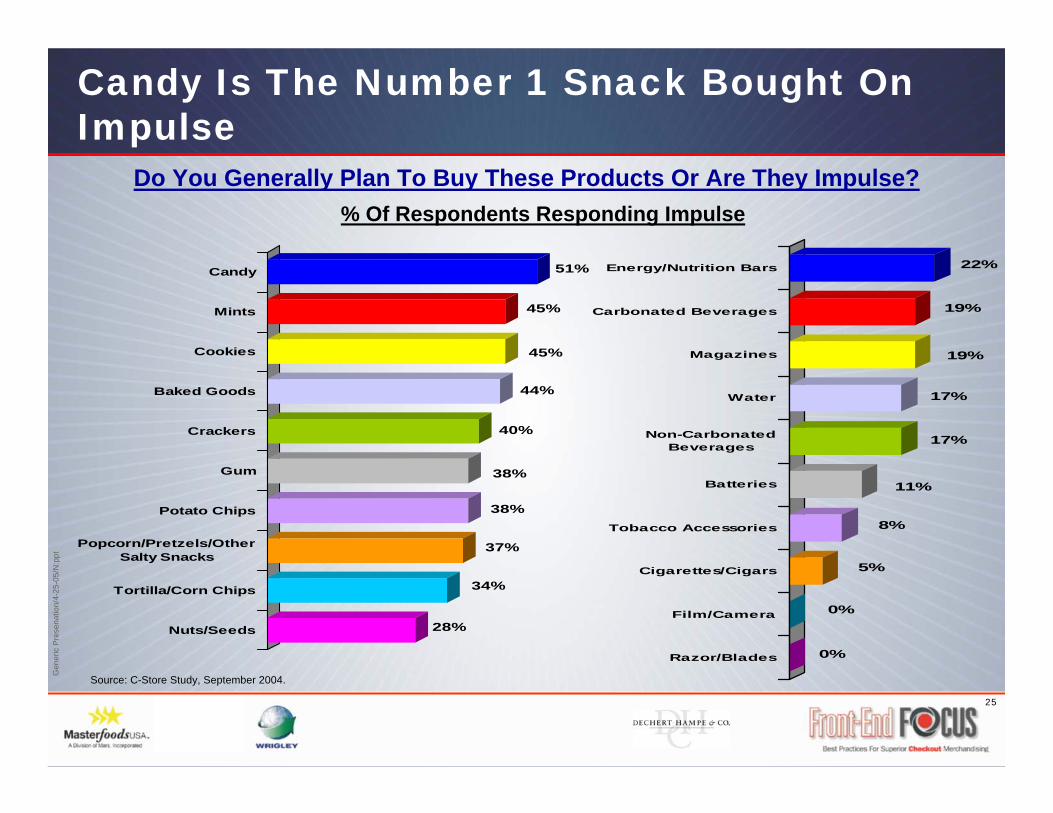

28%

34%

37%

38%

38%

40%

44%

45%

45%

51%Candy

Mints

Cookies

Baked Goods

Crackers

Gum

Potato Chips

Popcorn/Pretzels/OtherSalty Snacks

Tortilla/Corn Chips

Nuts/Seeds

Candy Is The Number 1 Snack Bought On Impulse

Source: C-Store Study, September 2004.

Do You Generally Plan To Buy These Products Or Are They Impulse?% Of Respondents Responding Impulse

0%

0%

5%

8%

11%

17%

17%

19%

19%

22%Energy/Nutrition Bars

Carbonated Beverages

Magazines

Water

Non-CarbonatedBeverages

Batteries

Tobacco Accessories

Cigarettes/Cigars

Film/Camera

Razor/Blades

26

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

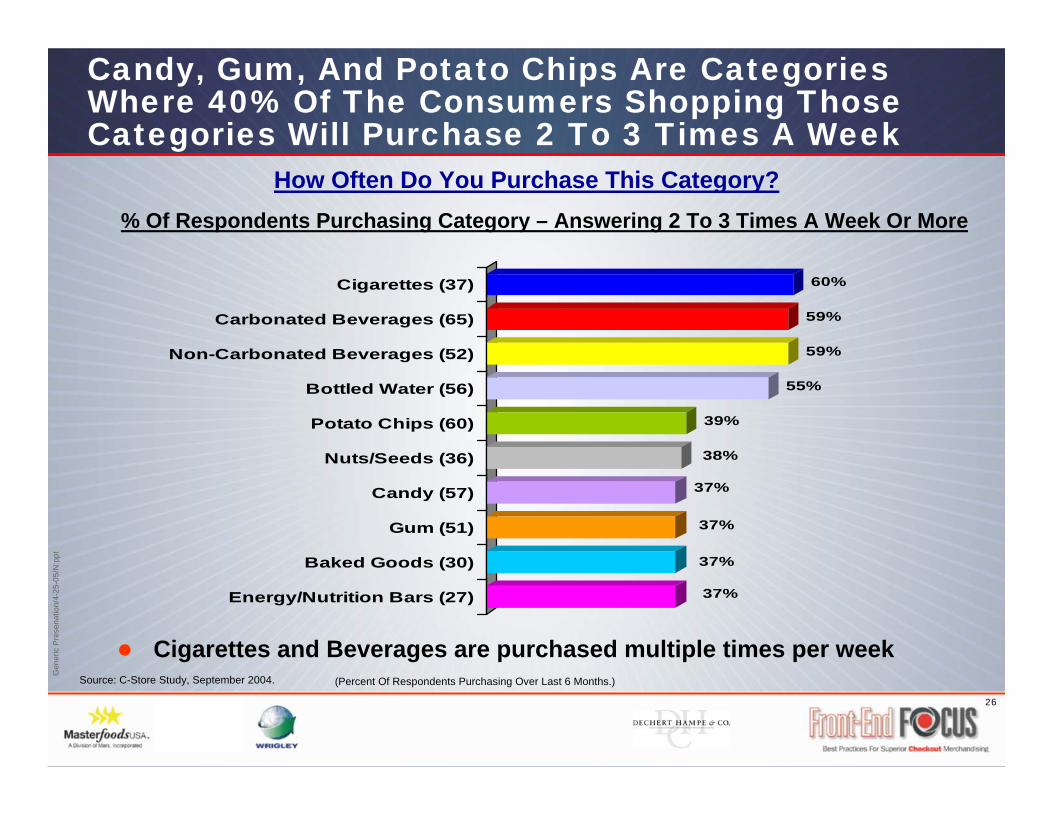

Candy, Gum, And Potato Chips Are Categories Where 40% Of The Consumers Shopping Those Categories Will Purchase 2 To 3 Times A Week

Source: C-Store Study, September 2004.

How Often Do You Purchase This Category?% Of Respondents Purchasing Category – Answering 2 To 3 Times A Week Or More

Cigarettes and Beverages are purchased multiple times per week(Percent Of Respondents Purchasing Over Last 6 Months.)

37%

37%

37%

37%

38%

39%

55%

59%

59%

60%Cigarettes (37)

Carbonated Beverages (65)

Non-Carbonated Beverages (52)

Bottled Water (56)

Potato Chips (60)

Nuts/Seeds (36)

Candy (57)

Gum (51)

Baked Goods (30)

Energy/Nutrition Bars (27)

27

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

1%

2%

3%

22%

22%

22%

24%

28%

32%

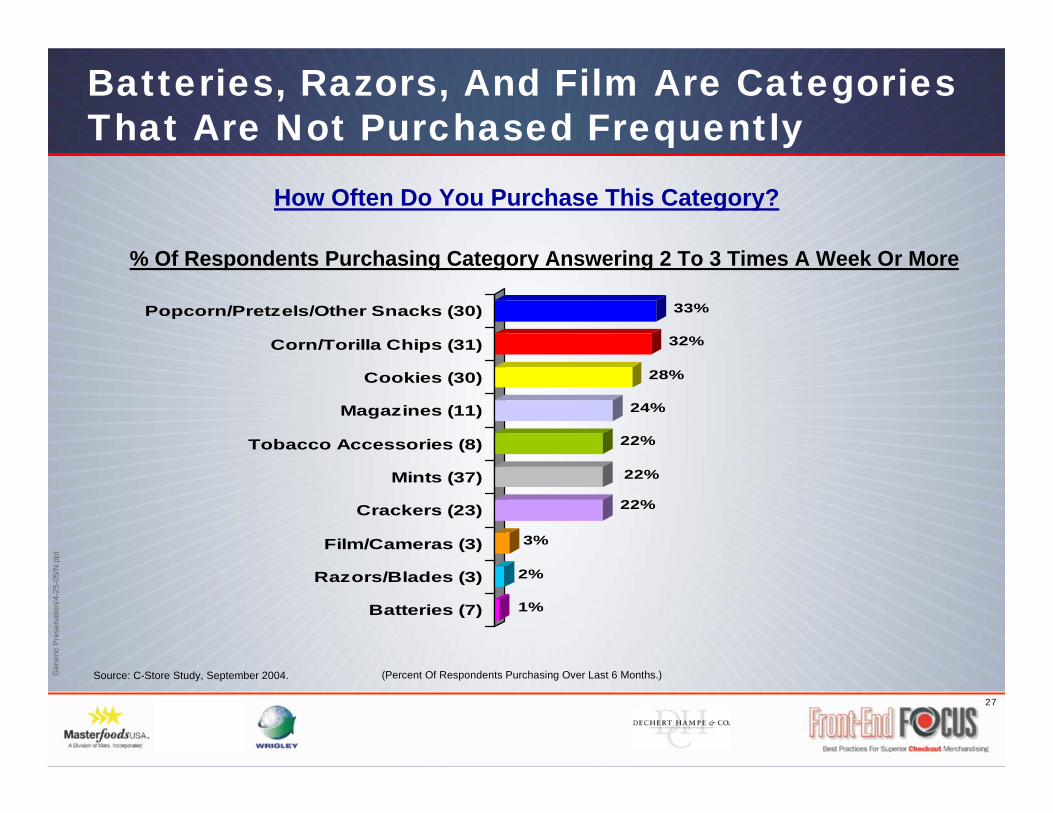

33%Popcorn/Pretzels/Other Snacks (30)

Corn/Torilla Chips (31)

Cookies (30)

Magazines (11)

Tobacco Accessories (8)

Mints (37)

Crackers (23)

Film/Cameras (3)

Razors/Blades (3)

Batteries (7)

Batteries, Razors, And Film Are Categories That Are Not Purchased Frequently

Source: C-Store Study, September 2004.

How Often Do You Purchase This Category?

% Of Respondents Purchasing Category Answering 2 To 3 Times A Week Or More

(Percent Of Respondents Purchasing Over Last 6 Months.)

28

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

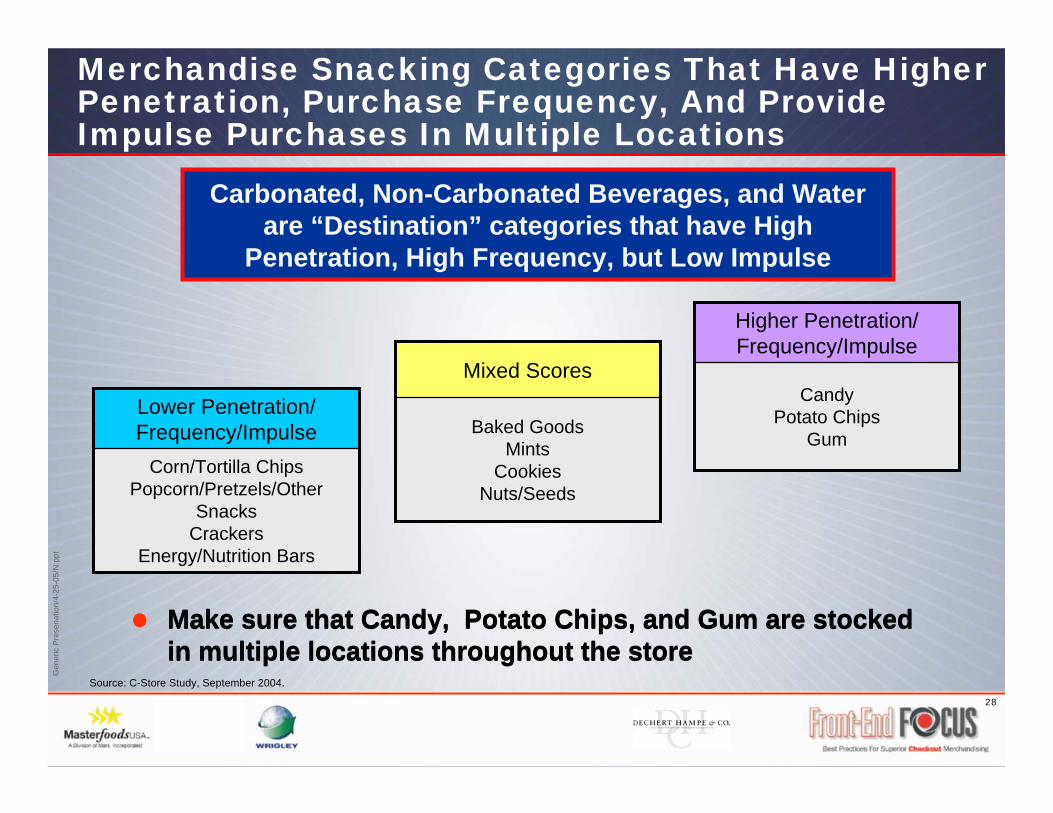

Merchandise Snacking Categories That Have Higher Penetration, Purchase Frequency, And Provide Impulse Purchases In Multiple Locations

Source: C-Store Study, September 2004.

Make sure that Candy, Potato Chips, and Gum are stocked in multiple locations throughout the store

Corn/Tortilla ChipsPopcorn/Pretzels/Other

SnacksCrackers

Energy/Nutrition Bars

Lower Penetration/ Frequency/Impulse

CandyPotato Chips

Gum

Higher Penetration/ Frequency/Impulse

Baked GoodsMints

CookiesNuts/Seeds

Mixed Scores

Make sure that Candy, Potato Chips, and Gum are stocked in multiple locations throughout the store

Carbonated, Non-Carbonated Beverages, and Water are “Destination” categories that have High

Penetration, High Frequency, but Low Impulse

29

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

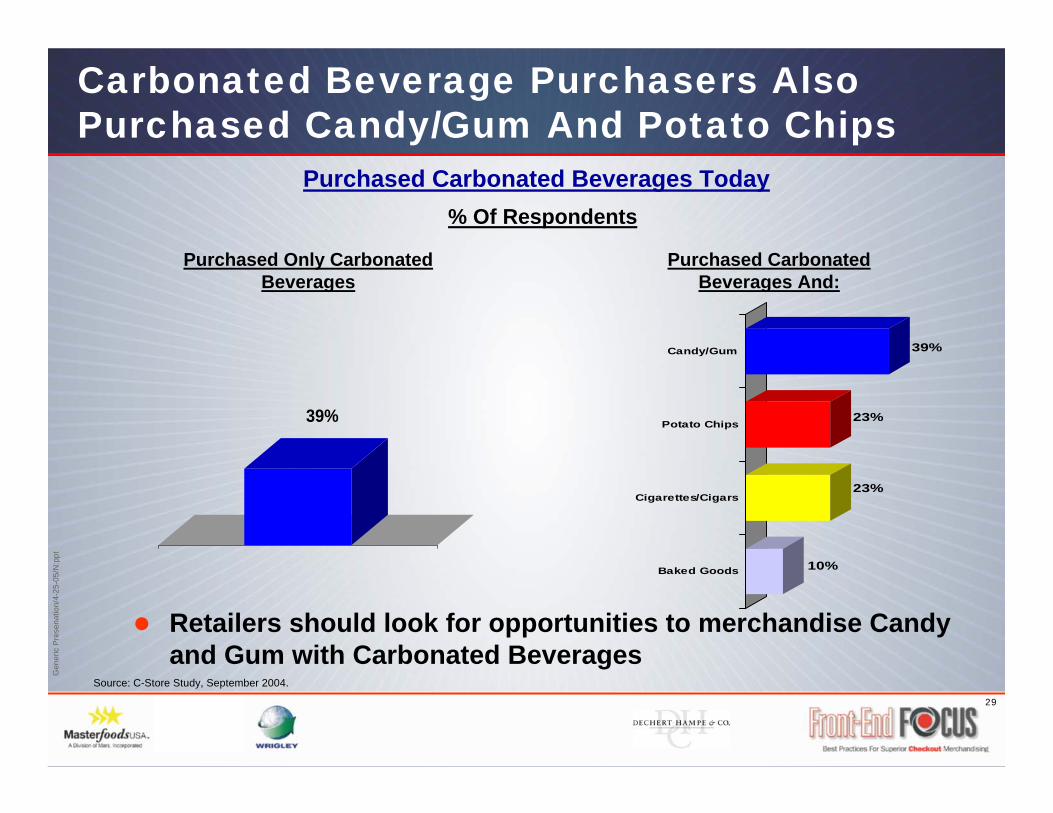

Carbonated Beverage Purchasers Also Purchased Candy/Gum And Potato Chips

Source: C-Store Study, September 2004.

Purchased Carbonated Beverages Today

Retailers should look for opportunities to merchandise Candy and Gum with Carbonated Beverages

% Of Respondents

10%

23%

23%

39%Candy/Gum

Potato Chips

Cigarettes/Cigars

Baked Goods

39%

Purchased Only Carbonated Beverages

Purchased Carbonated Beverages And:

30

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Recommendation: Merchandise Candy In The Refrigerated Coolers To Generate Additional Sales

Source: C-Store Study, September 2004.

31

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

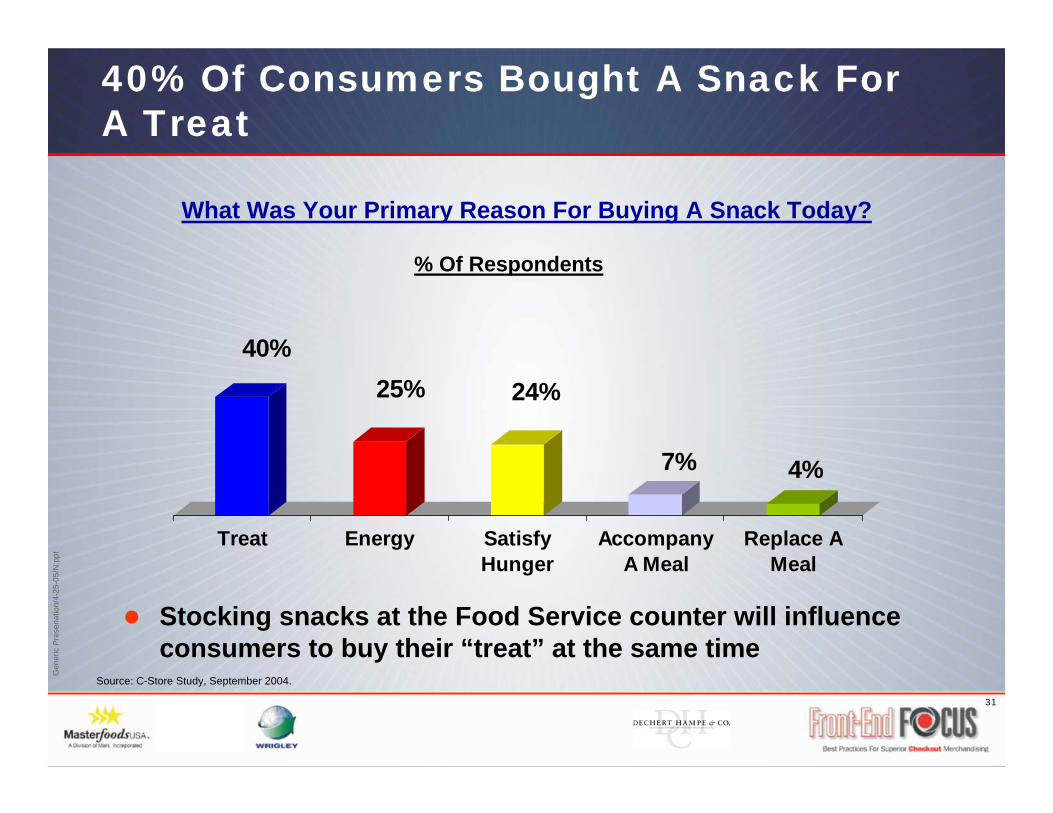

40%25% 24%

7% 4%

Treat Energy SatisfyHunger

AccompanyA Meal

Replace AMeal

40% Of Consumers Bought A Snack For A Treat

What Was Your Primary Reason For Buying A Snack Today?

Source: C-Store Study, September 2004.

Stocking snacks at the Food Service counter will influence consumers to buy their “treat” at the same time

% Of Respondents

32

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

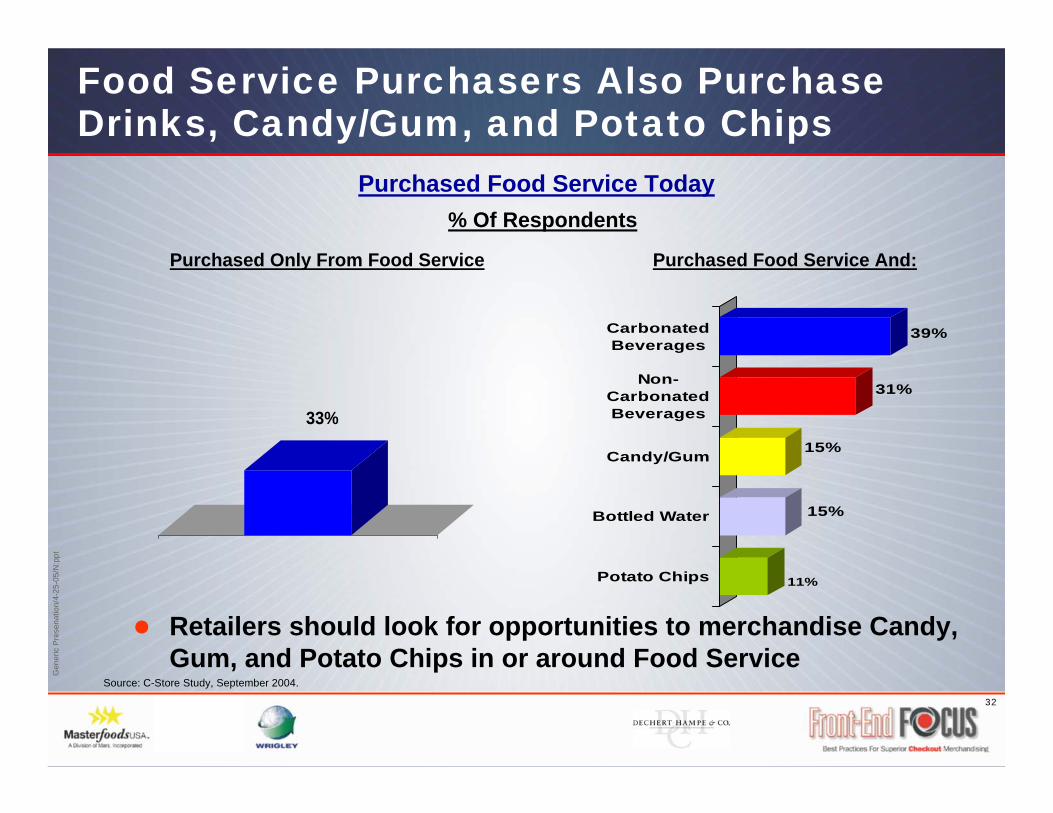

Food Service Purchasers Also Purchase Drinks, Candy/Gum, and Potato Chips

Source: C-Store Study, September 2004.

Purchased Food Service Today

Retailers should look for opportunities to merchandise Candy, Gum, and Potato Chips in or around Food Service

% Of Respondents

11%

15%

15%

31%

39%CarbonatedBeverages

Non-CarbonatedBeverages

Candy/Gum

Bottled Water

Potato Chips

33%

Purchased Only From Food Service Purchased Food Service And:

33

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

Recommendation: Merchandise Single Serve Snacks In The Food Service Area To Generate Additional Snack Purchases

34

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

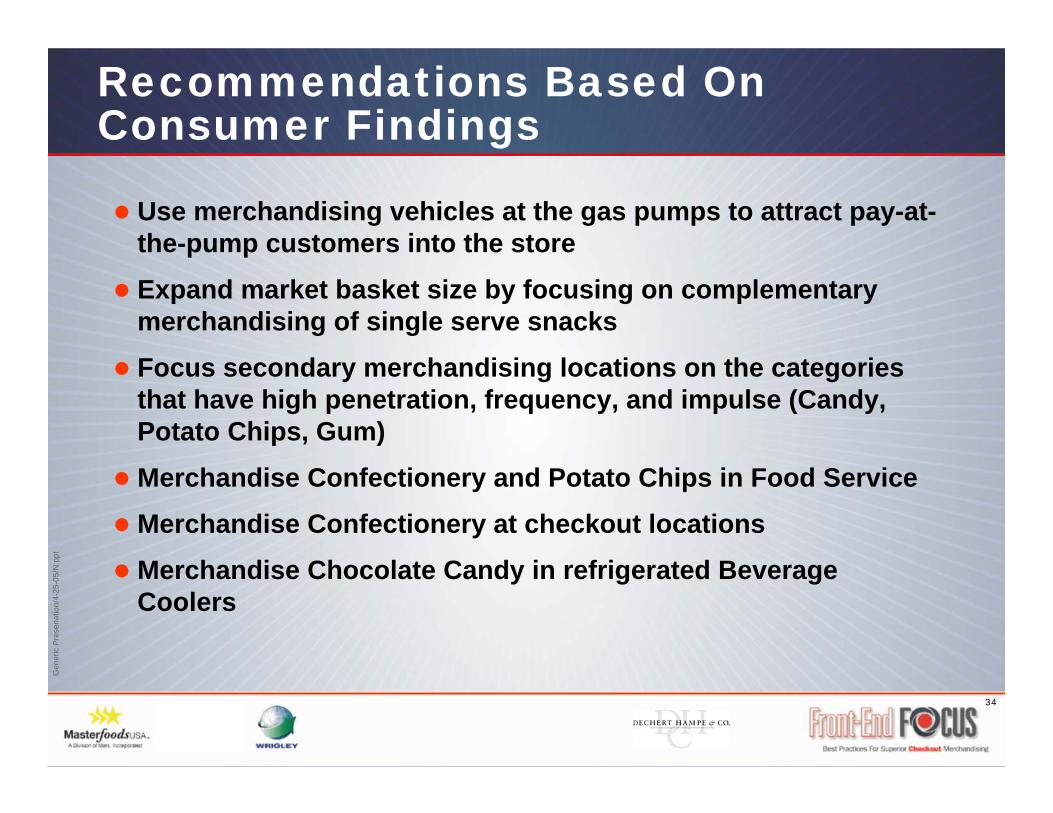

Recommendations Based On Consumer Findings

Use merchandising vehicles at the gas pumps to attract pay-at-the-pump customers into the store

Expand market basket size by focusing on complementary merchandising of single serve snacks

Focus secondary merchandising locations on the categories that have high penetration, frequency, and impulse (Candy, Potato Chips, Gum)

Merchandise Confectionery and Potato Chips in Food Service

Merchandise Confectionery at checkout locations

Merchandise Chocolate Candy in refrigerated Beverage Coolers

35

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

C-Store Single Serve Snacks Sales/Audit Insights

36

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

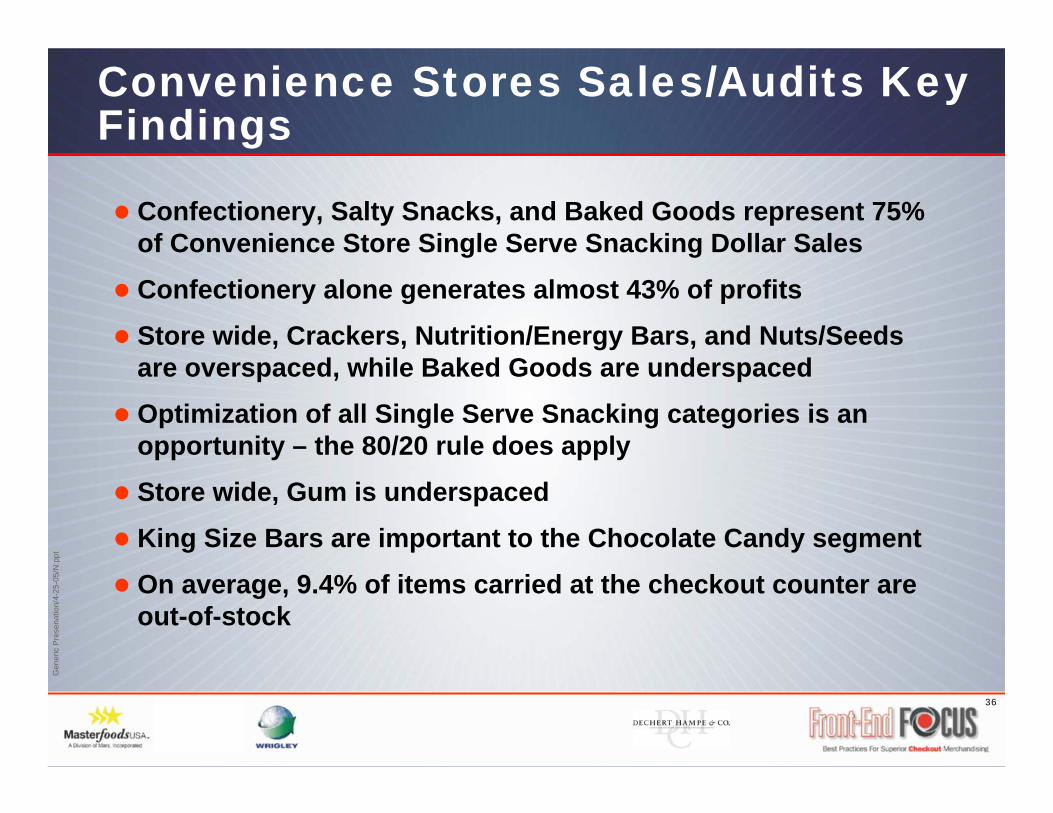

Convenience Stores Sales/Audits Key Findings

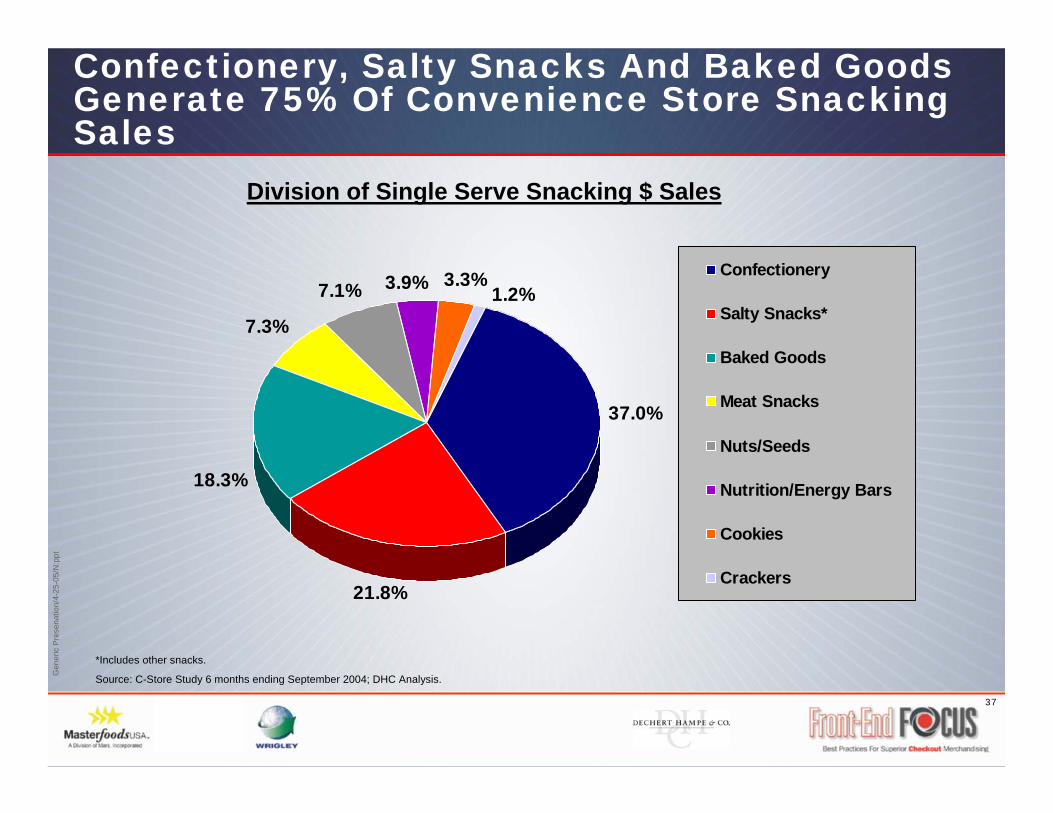

Confectionery, Salty Snacks, and Baked Goods represent 75% of Convenience Store Single Serve Snacking Dollar Sales

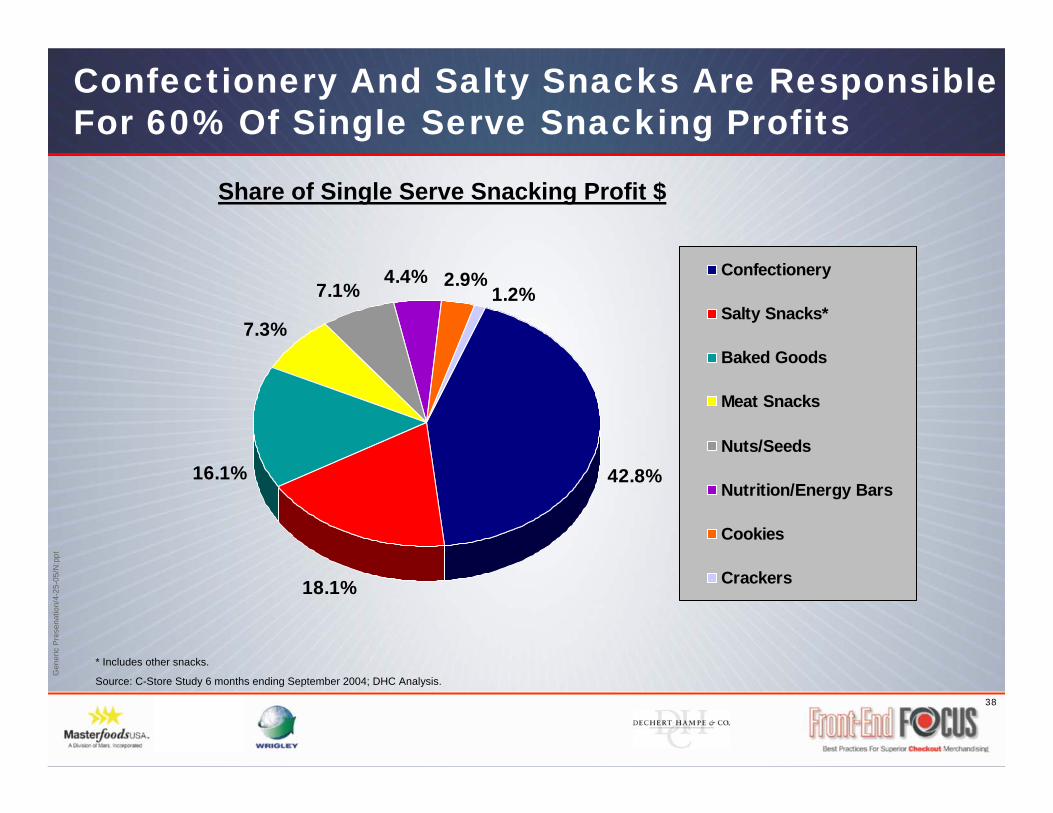

Confectionery alone generates almost 43% of profits

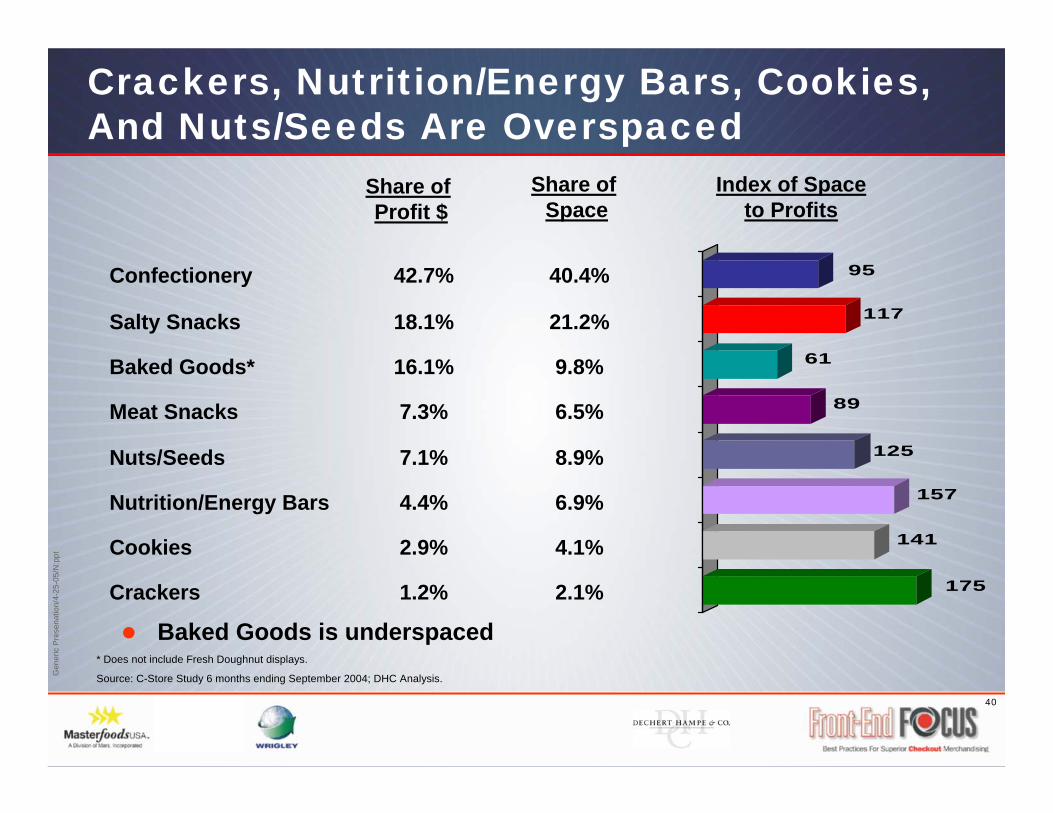

Store wide, Crackers, Nutrition/Energy Bars, and Nuts/Seeds are overspaced, while Baked Goods are underspaced

Optimization of all Single Serve Snacking categories is an opportunity – the 80/20 rule does apply

Store wide, Gum is underspaced

King Size Bars are important to the Chocolate Candy segment

On average, 9.4% of items carried at the checkout counter are out-of-stock

37

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

37.0%

7.3%

21.8%

18.3%

1.2%3.3%3.9%7.1%

Confectionery

Salty Snacks*

Baked Goods

Meat Snacks

Nuts/Seeds

Nutrition/Energy Bars

Cookies

Crackers

Confectionery, Salty Snacks And Baked Goods Generate 75% Of Convenience Store Snacking Sales

Division of Single Serve Snacking $ Sales

*Includes other snacks.

Source: C-Store Study 6 months ending September 2004; DHC Analysis.

38

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

42.8%

7.3%

18.1%

16.1%

1.2%2.9%4.4%

7.1%Confectionery

Salty Snacks*

Baked Goods

Meat Snacks

Nuts/Seeds

Nutrition/Energy Bars

Cookies

Crackers

Confectionery And Salty Snacks Are Responsible For 60% Of Single Serve Snacking Profits

Share of Single Serve Snacking Profit $

* Includes other snacks.

Source: C-Store Study 6 months ending September 2004; DHC Analysis.

39

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

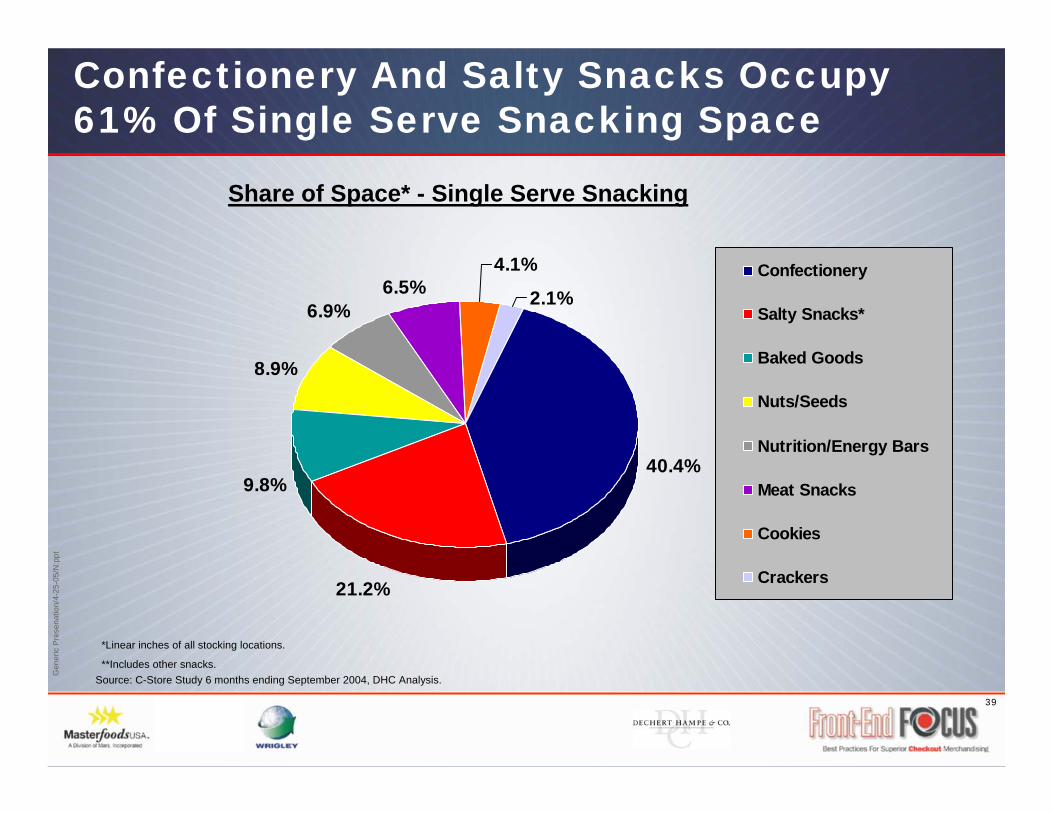

Confectionery And Salty Snacks Occupy 61% Of Single Serve Snacking Space

Share of Space* - Single Serve Snacking

Source: C-Store Study 6 months ending September 2004, DHC Analysis.

40.4%

21.2%

9.8%

8.9%

6.9%6.5%

4.1%

2.1%Confectionery

Salty Snacks*

Baked Goods

Nuts/Seeds

Nutrition/Energy Bars

Meat Snacks

Cookies

Crackers

*Linear inches of all stocking locations.

**Includes other snacks.

40

Gen

eric

Pre

sena

tion/

4-25

-05/

N:p

pt

175

141

157

125

89

61

117

95

Crackers, Nutrition/Energy Bars, Cookies, And Nuts/Seeds Are Overspaced

Share of Profit $

* Does not include Fresh Doughnut displays.

Source: C-Store Study 6 months ending September 2004; DHC Analysis.

Share of Space

Index of Space to Profits

2.1%1.2%Crackers

4.1%2.9%Cookies

6.9%4.4%Nutrition/Energy Bars

8.9%7.1%Nuts/Seeds

6.5%7.3%Meat Snacks

9.8%16.1%Baked Goods*

21.2%18.1%Salty Snacks

40.4%42.7%Confectionery

Baked Goods is underspaced