convergence us gaap & ifrs, what it means in fa...

TRANSCRIPT

1

Convergence US GAAP & IFRS, what it means in FA (EBS)

Seamus Moran

Fusion Financials Development

3

<Insert Picture Here>

IFRS & US GAAP:

Expectations for end of 2011 & 2012

• Converging Standards: Leases & Revenue

• The SEC‟s expected announcement

• After that: “Condorsement?”

• Oracle Solutions: Leases, Revenue, Reporting

– Impact on Fixed Assets

• Oracle Credentials

• Appendix

4

Converging Standards

• SEC Announcement in March 2010:

– If the IASB & FASB are making

progress on Convergence

– If the country is ready for IFRS

– Then, the SEC will make a statement

at the end of 2011

– On the “role of IFRS in US reporting”

5

IASB & FASB focused on Convergence

1. Leasing – all lease assets & liabilities on balance sheet

2. Revenue – liability to customer for future performance

3. Reporting – Exposure draft needs to be re-worked

4. Financial Instruments – Negotiating with Basel, EU, US, etc.

5. Others – normal throughput

-> 2010 2011->

FASB

TWEEDIE

IASB

HOOGERVORST

HERZ SEIDMAN

Converging Standards

6

Leases: All leases are “capital”

• Lease Exposure Draft Last Year, 2010

– Operating Leases are either Capital Leases or Revenue Arrangements

– Changes to Valuation Math

• Input received and considered. Redeliberation not complete by

intended June, 2011 – many revisions

• Revised Exposure Draft October or November 2011

– Anticipated that it will represent the final standard

• Final? March or April 2011? – all US GAAP & IFRS filers worldwide

• Effective not before June 2015 for new transactions

– Probably not before June 2013 for retro-reporting

7

• Operating Leases

• Introduced 1959 when airliner manufacturers introduced jets

• Jets cost much more than “propeller” airplanes, for huge savings, both in fuel,

time spent travelling, and capacity

• But airlines weren‟t capitalized to invest in them

• Bankers created the “operating lease” to enable the manufacturers to

supply the airlines

• Banks: Bought the airplanes, rented them to the airlines, but did not account for

them as FA, as they weren‟t used in the banks business

• Airlines: rented the airplanes, did not account for them as FA as “only” rented

• Airplanes disappeared from the balance sheet: this what the new principle

is fixing

Leases and Fixed Assets

8

Revenue: “Performance Obligations”

• Performance Obligations Exposure Draft Last Year, 2010

– Recognize a liability to customers for obligations to perform

– EITF-8 & VSOE “lite” extended to all industries

• Input received and considered. Redeliberation not complete by

intended June, 2011 – many revisions

• Revised Exposure Draft Winter 2011 (after Leases)

– Anticipated that it will represent the final standard

• Final? March to May 2012? – all US GAAP & IFRS filers world wide

• Effective not before June 2015 for new transactions

– Probably not before June 2013 for retro-reporting

9

SEC’s Expected Announcement

“Role of IFRS in US Reporting Environment”

• Follow Through on March 2010 Announcement

– SEC Act „32 requires “generally accepted accounting principles”

– Converged Standards have been through GAAP review process

– Other IAS/IFRS standards have been through a GAAP Review

process that did include USA institutions (FASB, SEC, others) but

was not the FASB‟s GAAP process

• Not known what the SEC will announce, but sentiment is:

– Will probably neither adopt en masse, nor walk away

– Might say “condorsement”. Defined in a recent SEC paper

– Converge & Endorse

10

SEC’s Expected Announcement

Condorsement?

• Suggestion: FASB publish each existing “older” IAS-IFRS

Statement as an ASU (Accounting Standard Update) to the

US GAAP Codification

– Each would be reviewed as GAAP; endorsed if equivalent,

reworked with IASB if not Generally Accepted

– Similar to process in some other countries

• No big bang “adoption”?

• Would not apply to Stock Options, Leasing, Revenue

• Would not be controversial for many IAS-IFRS statements;

might be for some

11

Timeline

Oracle

OpenWorld

2011

Now

FASB & IASB publish

revised EDs:

Leases & Revenue

This Fall

SEC speech:

role of IFRS

This Winter

FASB & IASB publish

final Principles:

Leases & Revenue

Late Spring 2012

Effective date of:

Leases & Revenue

June 2015

Retro-Reporting on:

Leases & Revenue

June 2013

Oracle

OpenWorld

2012

Next Year

Oracle

OpenWorld

2013

Year After

Oracle

OpenWorld

2014

And Again

Oracle

OpenWorld

2015

Eventually

2011 2012 2013 2014 2015

FASB Begins

Condorsement Process

2012

Some Condorsement

ASUs Published

Possibly by 2014

12

The following is intended to outline our general

product direction. It is intended for information

purposes only,

and may not be incorporated into any contract. It is

not a commitment to deliver any material, code, or

functionality, and should not be relied upon in making

purchasing decisions.

The development, release, and timing of any features

or functionality described for Oracle‟s products

remains at the sole discretion of Oracle.

13

Leasing: Product Proposals & Direction

• All Products: New Valuation

Math as specified in new ED

• Landlords & Owners: updates

to existing products

• Tenants & Users: – Lease Portfolio Management

– Industrial Volume Scaling

– Enhanced FA to Lease Liability

– Depreciation & Finance Cost expense

• All Families: EBS, Peoplesoft, JDE

Real

Estate

Equipment

Leasing

Revenue Landlords

Equipment

Owners

Leasing

Expenses Tenants

Equipment

Users

Requirements Outline:

• Reflect new Lease Valuation Rules

• Handle existing Operating Leases as Capital Leases

• Capitalize leased real estate & equipment as Fixed Assets

• Depreciate the Fixed Asset; Expense the finance cost

• Provide friendly lease portfolio management to help handle volume

14

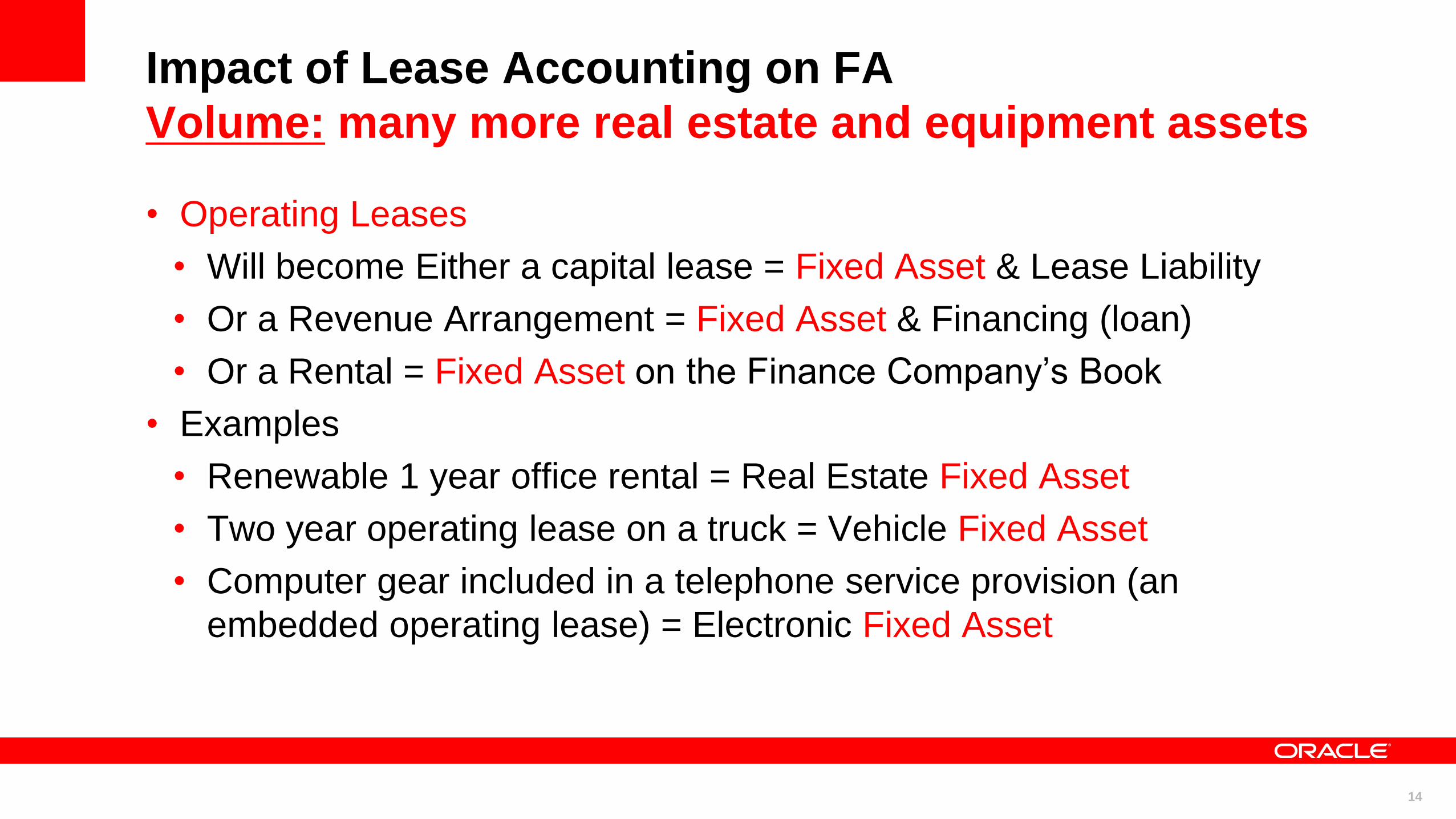

Impact of Lease Accounting on FA

Volume: many more real estate and equipment assets

• Operating Leases

• Will become Either a capital lease = Fixed Asset & Lease Liability

• Or a Revenue Arrangement = Fixed Asset & Financing (loan)

• Or a Rental = Fixed Asset on the Finance Company‟s Book

• Examples

• Renewable 1 year office rental = Real Estate Fixed Asset

• Two year operating lease on a truck = Vehicle Fixed Asset

• Computer gear included in a telephone service provision (an

embedded operating lease) = Electronic Fixed Asset

15

Impact of Lease Accounting on FA

Portfolio management & reporting

• Creation of an asset when you enter into a lease

• Similar to existing AP functionality

• Invoice the asset

• Pay the invoice with the lease

• Cross reference assets & leases (stamp lease number on asset and

asset number on lease)

• Portfolio reporting (which assets to which leases)

• Lease Management (which assets about to expire, etc.)

• Other asset rules unchanged – depreciation, impairment, ARO are all

the same. Useful life must have lease duration factored in

16

Revenue: Product Proposals & Direction

Customer Facing

Existing Product

Examples

Revenue &

Obligation

Engine

Output &

Accounting

Order Management

Provide

Contract

Satisfaction

Billing

Customer

Product

& other

relevant

data

• Identify elements of

arrangements & obligations to

customer, categorize as

performed or not

• Value elements of

arrangements, performance

obligations

• Value revenue, performance

obligation liability

Reporting:

• Transaction &

Document Reporting

• Revenue, Billing &

Obligation

Reconciliation

Account Receivables

Project Management

Contracts

Pricing

Accounting:

• Publish data to

accounting engines

(eg SLA)

• Activity and Balances

CRM

Shipping

Support

Other Products

Custom

17

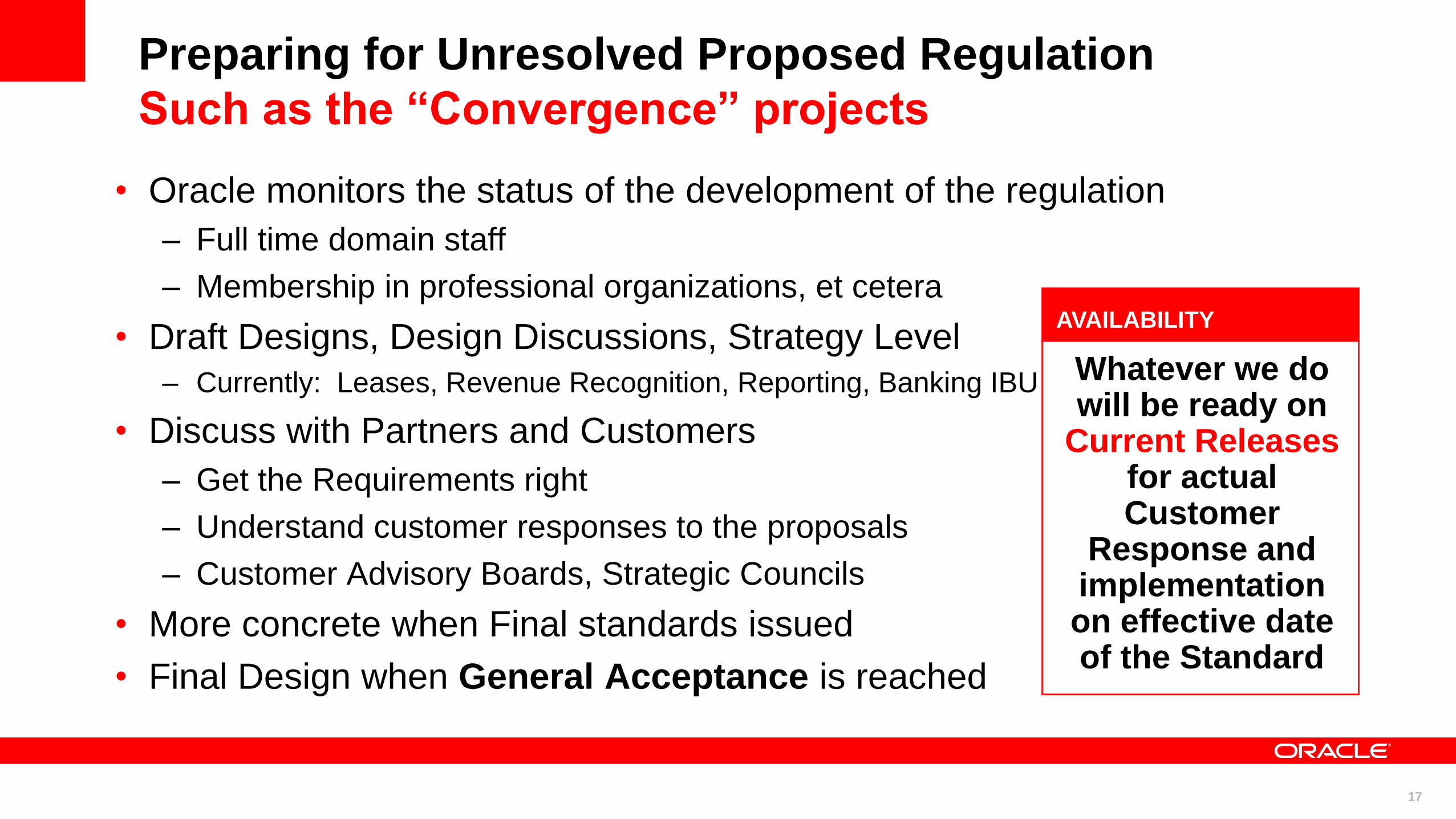

Preparing for Unresolved Proposed Regulation

Such as the “Convergence” projects

• Oracle monitors the status of the development of the regulation

– Full time domain staff

– Membership in professional organizations, et cetera

• Draft Designs, Design Discussions, Strategy Level

– Currently: Leases, Revenue Recognition, Reporting, Banking IBU

• Discuss with Partners and Customers

– Get the Requirements right

– Understand customer responses to the proposals

– Customer Advisory Boards, Strategic Councils

• More concrete when Final standards issued

• Final Design when General Acceptance is reached

Whatever we do will be ready on

Current Releases for actual Customer

Response and implementation on effective date of the Standard

AVAILABILITY

18

Timeline

Oracle

OpenWorld

2011

Now

FASB & IASB publish

revised EDs:

Leases & Revenue

This Fall

FASB & IASB publish

final Principles:

Leases & Revenue

Late Spring 2012

Effective date of:

Leases & Revenue

June 2015

Retro-Reporting on:

Leases & Revenue

June 2013

Oracle

OpenWorld

2012

Next Year

Oracle

OpenWorld

2013

Year After

Oracle

OpenWorld

2014

And Again

Oracle

OpenWorld

2015

Eventually

2011 2012 2013 2014 2015

SEC speech:

role of IFRS

This Winter

FASB Begins

Condorsement Process

2012

Some Condorsement

ASUs Published

Possibly by 2014

Retro-Reporting capabilities in

time to implement before 2013

deadline

New Transaction capabilities in

time to implement before 2015

deadline

, Leases and Revenue: the requirement

19

Allways: Apply Policy and Control Management

Other ERP

Custom, Legacy,

Competitor

Oracle ERP

Oracle Governance, Risk, & Compliance Suite

Oracle Enterprise Performance Management

Industry

Specific Applications

Condorsement?

Reporting for Accounting Changes

Top-Side Reporting

Data Capture in Subledgers

Model the Change Take it Home

Process Revision

20

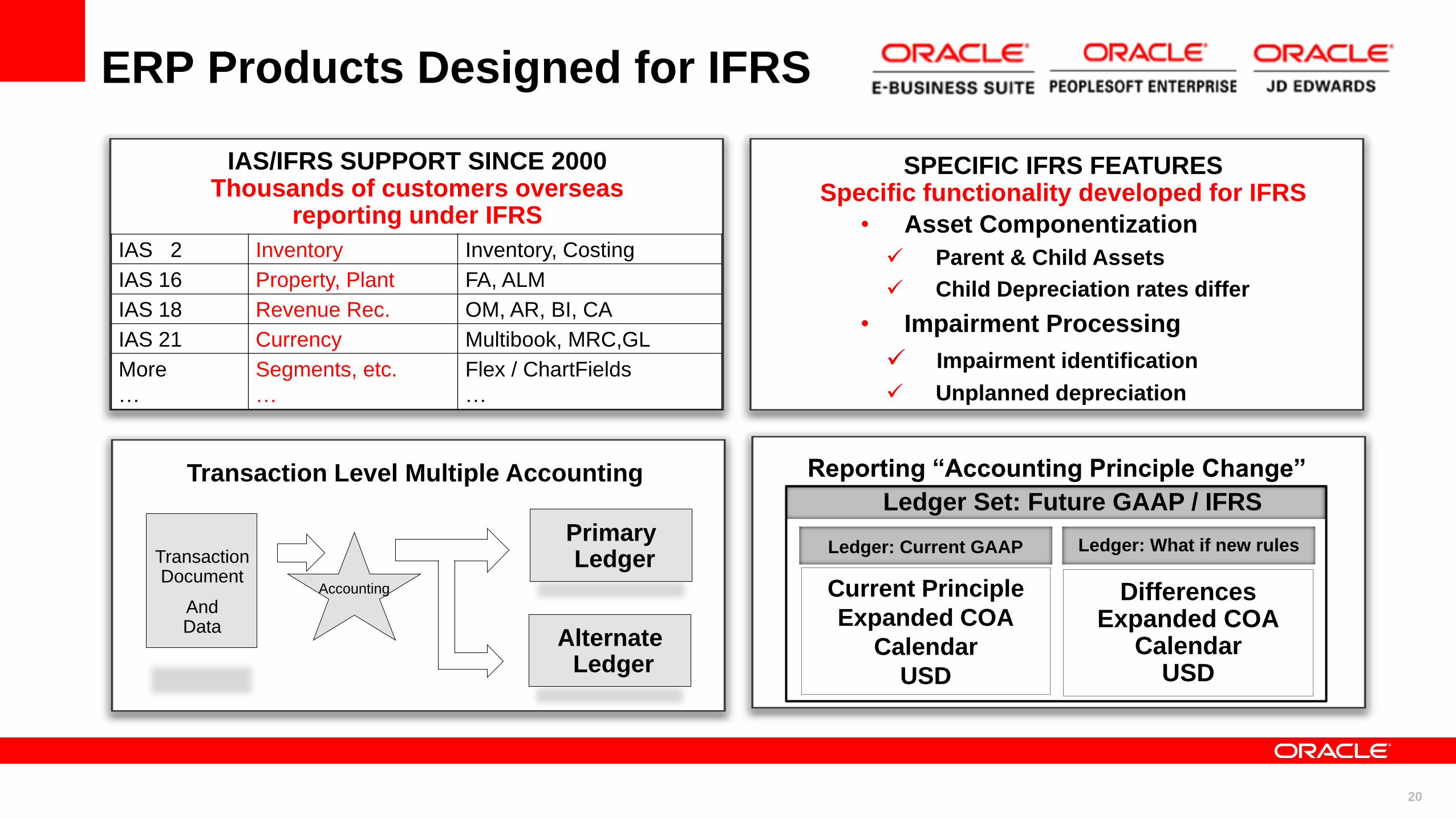

IAS/IFRS SUPPORT SINCE 2000 Thousands of customers overseas

reporting under IFRS

ERP Products Designed for IFRS

SPECIFIC IFRS FEATURES Specific functionality developed for IFRS

IAS 2 Inventory Inventory, Costing

IAS 16 Property, Plant FA, ALM

IAS 18 Revenue Rec. OM, AR, BI, CA

IAS 21 Currency Multibook, MRC,GL

More

…

Segments, etc.

…

Flex / ChartFields

…

• Asset Componentization

Parent & Child Assets

Child Depreciation rates differ

• Impairment Processing

Impairment identification

Unplanned depreciation

Ledger Set: Future GAAP / IFRS

Differences Expanded COA

Calendar USD

Current Principle

Expanded COA

Calendar

USD

Ledger: What if new rules

Reporting “Accounting Principle Change”

Ledger: Current GAAP

Transaction Level Multiple Accounting

Transaction Document

And Data

Accounting

Primary Ledger

Alternate Ledger

21

Asset Componentization

A feature in today’s offering: in use outside USA

Comp

-onent

Name Useful

Life

1 Airframe 25

2 Engines 5

3 Interior 10

4 Electronics 3

5 Total airplane 25

US GAAP today:

One Airplane, one FA

Pool Depreciation OK

US GAAP with IAS 16 Condorsed into it:

One Airplane, Five FA

Pool Depreciation NOT OK

22

Asset Componentization

A numeric example: a Building

US GAAP IFRS

Asset Elevator Roof Frame Land Parent

Asset

Building # 171 5,000,000

Components 500,000 250,000 2,000,000 2,250,000 5,000,000

Useful Life 25 years 5 years 10 years 25 years 50 years Mixed

Simple Depreciation PY 200,000 100,000 25,000 80,000 45,000 250,000

No. of asset records 1 5

No. of deprn. methods 1 5

No. of reconciliations 0 1

No. of Historic rates 1 5

Feature: Parent-Child Assets; depreciation at different rates for each child

23

Condorsement & IAS 16

(The Fixed Asset IFRS standard)

• Condorsement, if announced

– FASB will publish IAS 16 as an ASU (Accounting Standard Update)

– You and everyone else in the US community will have an

opportunity to comment on IAS 16

– Favorable comments will mean it gets endorsed

– Unfavorable comments will mean the FASB tells the IASB it did not

meet General Acceptance

– The issue will have to be examined, discussed, and GA will have to

be renegotiated

24

Asset Impairment

• Common thinking in US GAAP & IFRS – semantic convergence

only required

• All assets that don‟t have a specified impairment model

– Cash Impairable

– AR Bad debt & similar reserves

– Inventory Lower of cost & market, inventory reserves

– Intangibles Impairable

– PP&E Impairable

– Financial Instruments Specific Impairment principles

– Subsidiaries Impairable

– Businesses Impairable

25

Asset Impairment

• Unforeseen loss of value in an asset

– If foreseen, you should have baked it into the useful life

• Based on future cash flows, so you need to figure the CGU, Cash

Generating Unit

– But it is unforeseen, so you don‟t know the CGU until it happens

– Never applies to easy-to-sell assets – a pick-up truck should never be impaired!

• Examples: say we own a…

Asset Reason for Impairment Relevant CGU

Sugar Mill Nationalized in a country All/only businesses in that country

Sugar Market Collapse All our Sugar Businesses

Milling method outlawed by FDA Sugar business in the USA

Nuclear Power Plant Chernobyl Disaster Power from all Chernobyl style plants

Fukushima Disaster (Germany) Power from all German Nuclear plants

Fukushima Disaster (USA) None

26

Asset Impairment

• FA Feature facilitates flagging, valuation

• I think (personal opinion) initial accounting work will be

done in EPM, Consolidation products

– Similar to “Discontinued Operations”

– Might be actually incorporated separately to isolate and contain

– Pushed back to GL in company codes and cost centers

– And then to Fixed Assets

27 Delivering an Integrated Close 27

28

DOCUMENT ATTACHMENTS

CORE CONSOLIDATION FEATURES

FLEXIBLE REPORTING

CUSTOM DIMENSIONS

GAAP IFRS

Flexible Rules Engine

Journal Entries and Audit

Enables tracking of

GAAP vs. IFRS

adjustments

Multiple reporting standards in a

single solution

Creates “Electronic

Binder” of all

adjustments

Easy to reconcile

and trend GAAP

vs. IFRS results

Hyperion Financial Management Features Enable Top End IFRS Reporting

29

GRC DOCUMENTATION REPOSITORY

IFRS Compliance: Use your GRC Manage changes to policies and controls

COMPLIANCE WORKFLOW

Single subledger transaction creates multiple accounting representations

APPLICATION CONTROLS MONITORING COMPLIANCE DASHBOARDS

Automate steps to audit IFRS compliance

Record changes to business process due to IFRS

Control changes to ERP applications

Monitor status of testing and exceptions

30

We encourage you to use the newly minted corporate tagline

“Hardware and Software, Engineered to Work Together.”

at the end of all your presentations. This message should

replace any reference to our previous corporate tagline

“Software. Hardware. Complete.”

31