cooperative movement as civil society iniatiative for

TRANSCRIPT

Cooperative Movement as Civil Society Iniatiative for Sustainable Development Goals: Cases of Islamic Cooperatives in Southeast Asia

Zurina ShafiiProfessor of Accounting and Islamic Finance

Faculty of Economics and Muamalat, Universiti Sains Islam MalaysiaEmail: [email protected]

AICIF2020

1

2

ASSOC. PROF. DR. ZURINA SHAFII

• Shariah Committee Member for Standard Chartered Saadiq Malaysia & Khadijah International Waqf Foundation (L).

• Associate Professor, Faculty of Economics and Muamalat, Universiti Sains Islam Malaysia (USIM) and a research fellow in Islamic Finance andWealth Management Institute (IFWMI), USIM. She holds an Accounting Degree from Universiti Teknologi Mara (UiTM) and a Master’sdegree and PhD in Islamic Finance from Durham University, UK. She holds professional accounting qualification, ACCA and a Certified IslamicFinancial Planner.

• Research interests are Shariah audit and assurance, Islamic financial institutions’ accounting and reporting, Islamic financial planning andHalal Compliance Procedures. She authored four books on Islamic financial planning, Shariah audit and Islamic finance.

• In 2014-2015, she was a visiting researcher in Durham University Business School (Durham University, UK), Islamic Research TrainingInstitute (IRTI) of Islamic Development Bank (IDB) and Global Islamic Finance Development Centre, a research centre for World Bank basedin Istanbul.

• She is an expert panel for Finance Accreditation Agency (FAA) as well as serving as an EXCO in International Council of Islamic FinanceEducators (ICIFE).

• In ASAFAS Kyoto University, for 3 months as Visiting Research Scholar, starting 1st June 2018, researching on Strategic Directives for ShariahGovernance Practices Beyond Compliance: Case of Malaysia.

Lecture Outline

1. Social Failure of Islamic Finance

2. Cooperative as Civil Society Movement

3. Theories and Frameworks for Islamic Cooperatives Movement

4. COOP and SDG Goals

5. Practices of Islamic cooperatives within emerging Muslim societies

3

1. Social Failures of Islamic Finance despite the propositions of Islamic Finance for humanity

Sustainable economic

growth

Price stability

Near-full employment

Equilibrium Balance of Payment

Interest-free economy is the solution to economic instability, unemployment, inflation, poverty (Shafiel Karim, 2010)

Cooperative movement: A Mitigation for Social Failures of IBF practice?

Social failures of IBF (MA,2012) Little accommodation of developmental financing No evidence of link of IBFIs and human development index in 25

countries (MA, 2010)

Failures of CSR Shortcomings of corporate governance performance Financialisation of IBF Mimicking of conventional finance that lacks link to real

economy

Popularity of debt financing over asset based financing

2. Cooperative Movement as an Alternative Model for Civil Society (1)• Co-operative as a form of social finance enterprise with potential in

helping people.

• The process of developing and sustaining a co-operative involves promoting the community spirit, identity and social organization (Ahmad Bello, 2005) .

• Cooperative offers mutual structures for islamic financial intermediaries of credit.

6

Cooperative Movement as an Alternative Model for Civil Society (2)• This is to revert from the rent-seeking shariah-artbitrage practices,

where the main focus is on the compliance of forms of contract to literal shariah requirements, without regards to the economics and risk implications to the offering institutions and the customers (El-Gamal, 2005).

• El-Gamal ( 2005) further argued that mutuality in credit intermediation and risk can significantly assist in the realisation of the substance of Shariah as well as its forms.

7

Cooperative Features—Coop as Civil Society Vehicle • With all these qualities, cooperatives make much more natural

vehicles for corporate social responsibility.

• The difference between investor-owned banks and credit unions, which are cooperatively owned financial institutions.

• Large-scale banks have been publicly has been assuming more risks; securitized subprime mortgages, inflated value of assets.

• Heavy pressure from boards and investors to maximize earnings.

8

Cooperative Features

Cooperative Features

Mutuality-based

Structure

Better risk management

People-centric

Local-economy

centric

Social resources

Employment

Social innovation

Social cohesion

9

3. Theories

• The governance of cooperatives is relatively under-theorised in comparison with the governance of business corporations, where there is a large literature on corporate governance (CG) (Pozzobon & Filho, 2007).

• The discussion on the theories and frameworks for Islamic cooperative is established to argue for the foundation of a workable alternative economic system.

• There are four theories that can support the cooperative to function as civil society, namely agency theory, stewardship theory, stakeholder theory and institutional theory

10

The Islamic Good Governance of Cooperative

Coop and SDG

• Goal 1: No poverty• (ILO), in 2018, acknowledged that cooperatives have unique business

propositions that could offer solution to poverty within the society. Since cooperatives are run subscribing to the seven (7) international convention principles; open and voluntary membership, democratic control, autonomy and independence and concern for their community

• Goal 8: Decent Work and Economic Growth• The collective pooling of financial resources and skills provided cooperative

members means to create their own economic opportunities.• Through the power of the collective, cooperators can share risk, make

decisions together about the cooperative’s future, strengthen and hone their own skills and reinvest in their communities (ILO,2018)

12

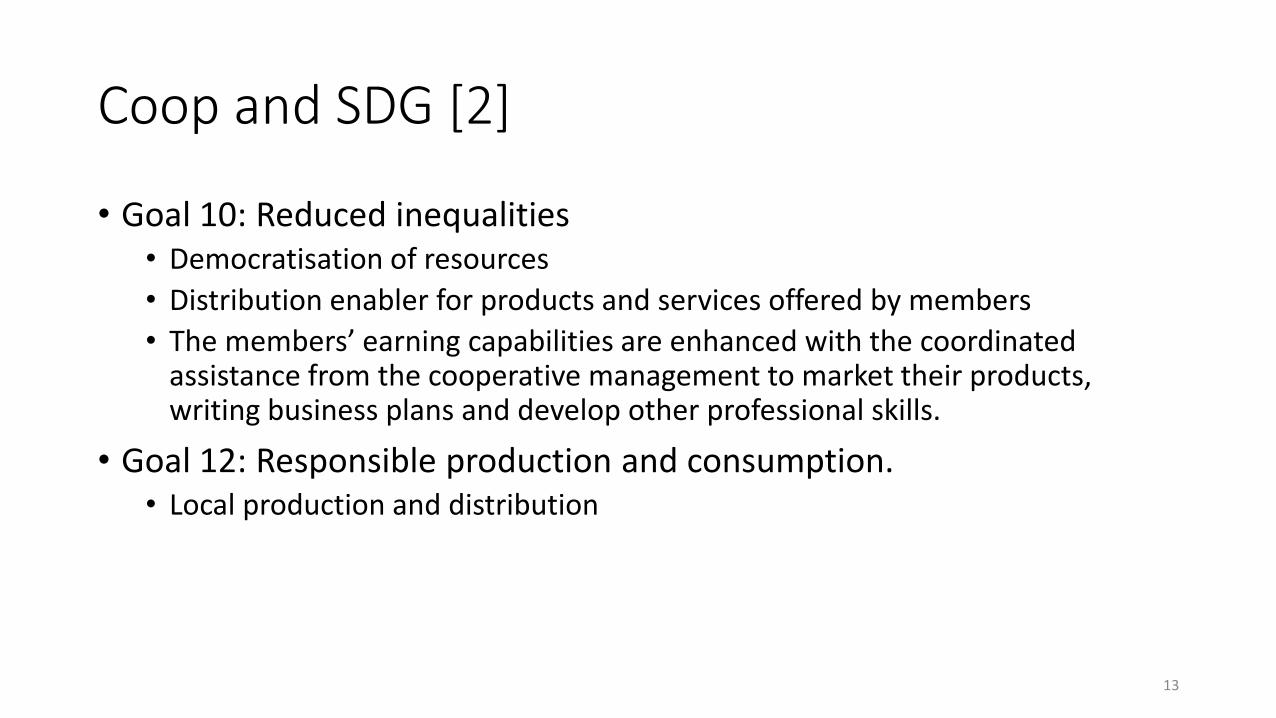

Coop and SDG [2]

• Goal 10: Reduced inequalities• Democratisation of resources

• Distribution enabler for products and services offered by members

• The members’ earning capabilities are enhanced with the coordinated assistance from the cooperative management to market their products, writing business plans and develop other professional skills.

• Goal 12: Responsible production and consumption. • Local production and distribution

13

4. Practices of Islamic cooperatives in Southeast Asia: Cases

14

• Malaysia

• Indonesia

• Thailand

Coop by States

15

Coop by Functions

16

Koperasi Muslimin

• Cooperative Muslimin Malaysia Berhad is one of the financial organizations that invites Muslims to practice shariah.

• Its intention is to become a superior financial institution through the cooperative movements by providing the best service to its members.

• On the consciousness of the need for an Islamic financial institution as an alternative to the existing financial system, on November 22, 1980, at the initiative of the Malaysian Ulama Association (PUM), the Koperasi MusliminMalaysia Berhad or its abbreviation, Muslim Cooperative (KMMB) was formed.

• Islam always encourages its people to practice the principles of cooperation in all activities and the Muslim Cooperative will always strive to uphold the Islamic-based economic system in their activities.

17

Koperasi Belia (KBI)

• The Youth Islamic Cooperative Berhad (KBI) was established on 31 May 1977 and registered under the Co-operative Societies Act (1993) Registration: 16 / 31.5.77. The establishment of the KBI was triggered by the Malaysian Islamic Youth Movement (ABIM), an Islamic movement; with the intention of producing an Islamic financial institution.

• At that time (70s) there was a collision of secular Islamic understanding, and even the acceptance of Islam by the people at that time was still low.

• Because of the strengths, perseverance and effort of the key people, KBI has been the first institution in Malaysia to introduce Shariah-compliant financial products and instruments. KBI is governed by the Co-operative Societies Act 1993 and the By-Laws of the Republic of Indonesia.

• Throughout the operation of KBI, it was awarded as the "Cooperative Model" category in 1985 and "Quality Award" in 1993 by the Ministry of Land and Cooperative Development.

18

KOPENAS

• Koperasi Perkhidmatan Pelajaran Nasional Berhad or its abbreviation KOPENAS was established on 11 February 1984 at a meeting held at Victoria High School, Kuala Lumpur.

• Its mission is to be the best cooperative to spur the socio-economic development of the educational community in Malaysia.

19

Products and Services on Offer

20

Coop in Indonesia

• Indonesia is the home to the largest muslim population in the world. Shariah-based cooperatives, thus contribute greatly to the growth agenda of the sector.

• Cooperative sector is the largest public society organizations as well as social enterprises with great potential in rural development and employment creation. It is estimated that 50 per cent of global agricultural output is marketed through cooperatives.

• According to the Indonesian Ministry of cooperatives and SMEs, the number of active cooperatives is 147,249 out of 209,488 in 2014. Most of these cooperatives (around 70 per cent) are located in rural areas. The cooperative movement in Indonesia is considered as one of the largest domestic society organizations as well as social enterprises with great potential in rural development and employment creation (ILO, 2012).

21

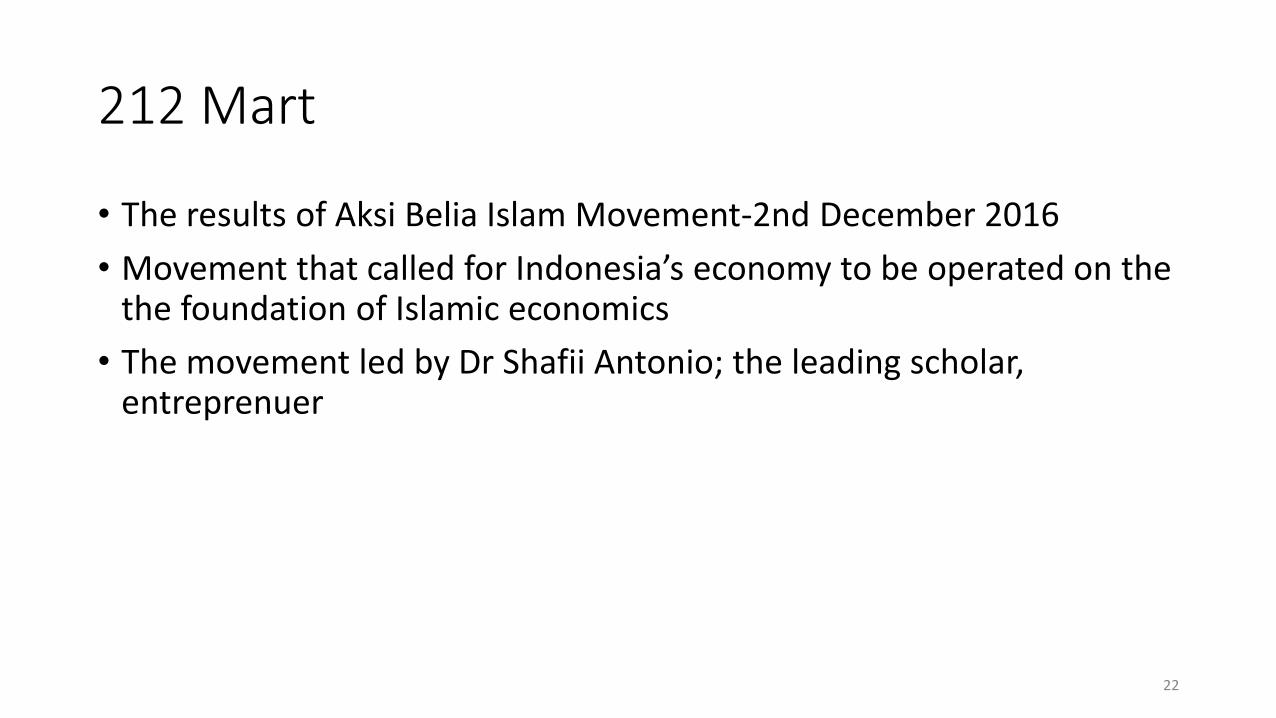

212 Mart

• The results of Aksi Belia Islam Movement-2nd December 2016

• Movement that called for Indonesia’s economy to be operated on the the foundation of Islamic economics

• The movement led by Dr Shafii Antonio; the leading scholar, entreprenuer

22

212 Mart

23

Cooperatives in Thailand

• There are 37 cooperatives operating in Thailand with the total assets amounted 2,000 million THB

• Sakofah Saving is one of the biggest four cooperatives in Thailand, operating in Krabi. Other cooperatives are Siddik in Hat Yai, Ibn Affan in Fattani, and Ibn Auf in Satun.

24

Sakofah Saving Co-op Ltd

• Sakofah Saving cooperative was established in 1995, regulated under the cooperative Ministry.The establishment of the cooperative was the fruit of efforts of Mr. Murod and some of his colleagues during to the time, with the aim to cater the financial need of Muslim community in Krabi.

• The organizational structure consists of supervisory board, director, secretary, managers, and staffs. Regarding the existence of Shariah committee, Sakofah does not have its own Shariah Committee.

• In the case that Sakofah needs Shariah advisory, it has to refer to the Shariah Committee that was established by the Islamic Cooperative Network, which Sakofah is affiliated, along with other cooperatives mentioned in other districts in Thailand.

• Sakofah publishes its annual report in June annually. When it was first established, it had less than 200 members. As in June 2015, the members amounted 8,224.

25

Intermediary and Social Roles of Sakofah

• Sakofah performs its role as an intermediary, collecting fund from the surplus unit and distributing funds to the units which need some financing.

• Sakofah collects the funds through two options; both membership and non-membership. The members can invest their funds in two modes of investments namely musharakahand mudharabah.

• The saving products offered by Sakofah are Musharakah, Mudarabah, Wadiah. From the collected funds, Sakofah makes investment and provides financing for customers. The percentage of investment and financing is currently at the ratio of 50:50 respectively.

• Mostly, Mudharabah and Musyarakah deals with Palm Oil and Real Estate projects. For Palm Oil, Sakofah will share the profit 80:20 for customers and Sakofah respectively. The profit or dividend for Mudarabah will be paid every 3 month.

• For Real estate, 5.5% will be given per year. The dividend will be paid monthly basis and in 24 months period for special project. Other project that the co-op should do is Hotel. For instance, they need 10 million, then Sakofah will collect money from members and do the investment.

26

Conclusion

• Coop is a quick win to be adopted as a vehicle of civil society; concentrates on mutuality

• Coop realises community needs and features relevant SDGs

27