copeland chapter one

DESCRIPTION

Course : Modern Finance theoryChapter 1TRANSCRIPT

Chapter OneIntroduction : Capital Market,

Consumption and Investment

Kawser Ahmed ShibluLecturer

Department of FinanceJagannath University

2

Introduction Consider, a one-person/one-good economy or a single

person economy. The decision maker must choose between consumption now and consumption in the future. The decision not to consume now is the same as investment. Thus his decision is simultaneously one of consumption and investment. In order to decide, he needs two types of information- subjective trade-offs between consumption now and

consumption in the future i.e. the utility and indifference curves

the feasible trade-offs between present and future consumption i.e. the investment and production opportunity sets.

Copeland, Weston & Shastri

Copeland, Weston & Shastri 3

From the analysis of a one-person/one-good economy, a subjective interest rate is determined by the optimal consumption/investment decision which represents the optimal rate of exchange between consumption now and in the future. Again it can be called the price of deferred consumption or the rate of return on investment.

Individual with different subjective interest rate select different consumption/investment decision choices.

Introduction

Opportunities to exchange consumption across time by borrowing or lending in a multiple person or exchange economy results in a single market interest rate that everyone can use as a signal for making optimal consumption/investment decisions.

So when no one is worse off and almost everyone is better off in an exchange economy compared with a single person economy, it can be said an ex change economy is superior to an economy without exchange.

4Copeland, Weston & Shastri

Introduction

Copeland, Weston & Shastri 5

And capital markets help to allocate/exchange resources from one to another. So the ultimate question arise- "Do capital markets benefit society?"

The answer requires to compare a world without capital markets to one with capital markets to show that no one is worse off and that at least one individual is better off in a world with capital markets.

Introduction

Copeland, Weston & Shastri 6

Consumption And InvestmentWithout Capital Markets

Assumptions-all outcomes from investment are known with certainty there are no transactions costs or taxes the marginal utility of consumption is always positive. the marginal utility of consumption is decreasingWealth at present=Y0

Wealth at end=Y1

Consumption at present=C0

Consumption at end=C1

Copeland, Weston & Shastri 7

Consumption And InvestmentWithout Capital Markets

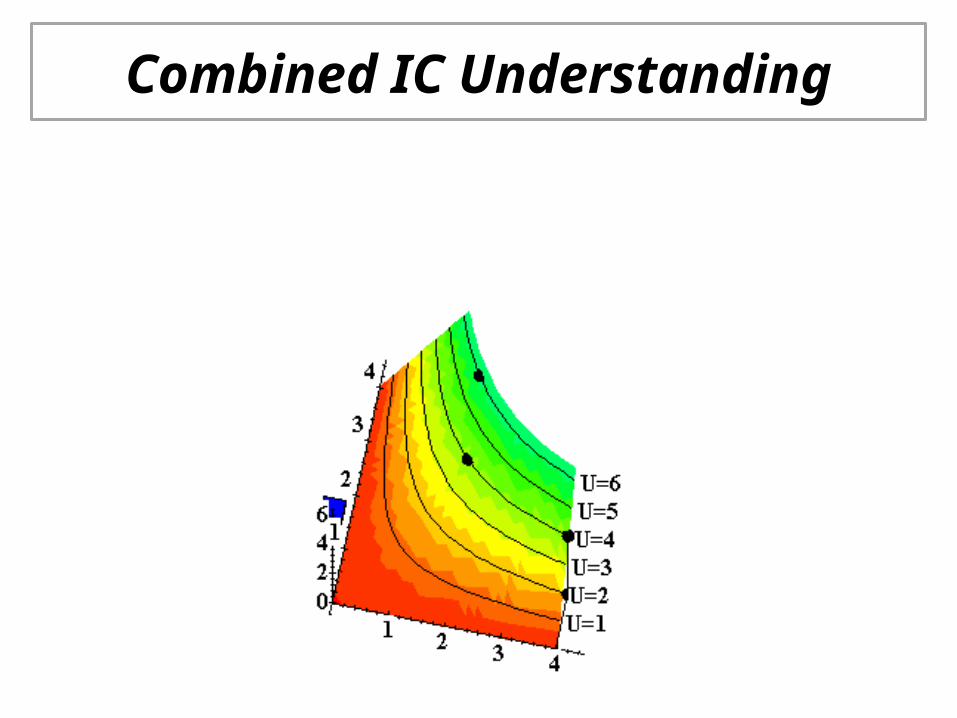

Note that equal increases in consumption cause total utility to increase (marginal utility is positive), but that the increments in utility become smaller and smaller (marginal utility is decreasing).

Provides a description of trade-offs between consumption at the beginning, C0 and consumption at the end, C1

The dashed lines represent various combinations of Co and CI providing the same total utility measured along the vertical axis. Since all points along thedashed line (e.g., points A and B) have equal total utility, the individual will be indifferent with respect to them. Therefore the dashed lines are called indifference curves.

Note that all combinations of consumption today and consumption tomorrow that lie on the same indifference curve have the same total utility.

8Copeland, Weston & Shastri

Consumption And InvestmentWithout Capital Markets

Combined IC Understanding

x1

x2

x1

x2

Combined IC Understanding

x1

x2

Combined IC Understanding

x1

x2

Combined IC Understanding

x1

x2

Combined IC Understanding

x1

x2

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

x1

Combined IC Understanding

Copeland, Weston & Shastri 25

Consumption And InvestmentWithout Capital Markets

Decision maker would be indifferent to point A & B whereas Point A has more consumption at the end but less consumption at the beginning than point B does.

Point D has more consumption in both periods than do eitherpoints A or B, with higher utility.

So curves to the northeast have greater total utility.

MRS: The rate of trade-off between C0 and C1 indicated by the slope of the straight line just tangent to the indifference curve. i.e. how many extra unit received tomorrow in order to give up one unit today to have same utility. MRS can be said as individual’s subjective rate of time preference.

Copeland, Weston & Shastri 26

Consumption And InvestmentWithout Capital Markets

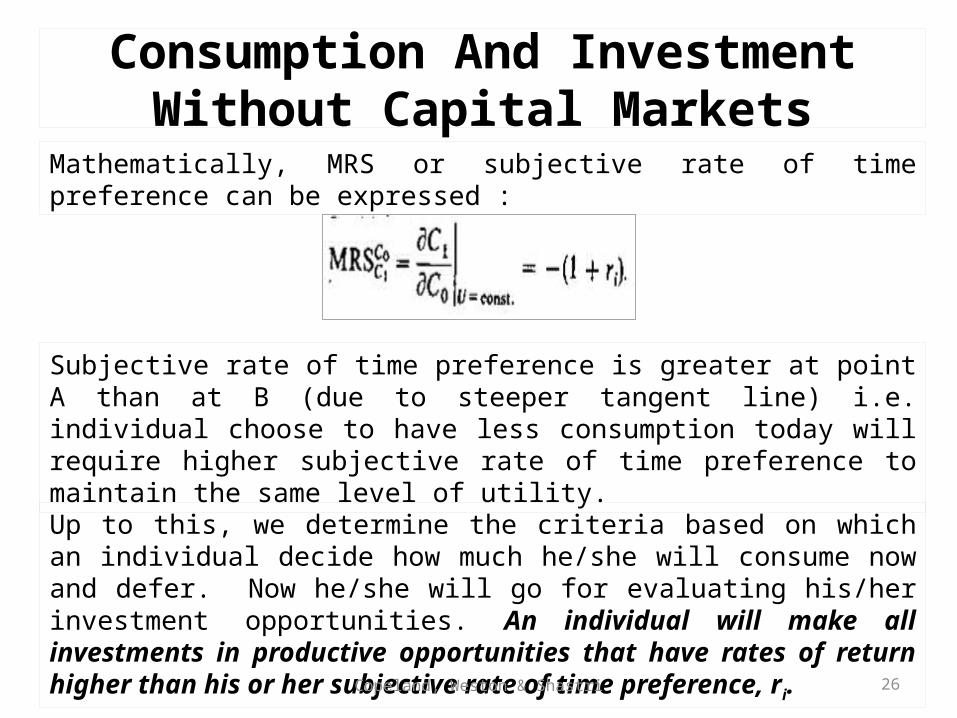

Mathematically, MRS or subjective rate of time preference can be expressed :

Subjective rate of time preference is greater at point A than at B (due to steeper tangent line) i.e. individual choose to have less consumption today will require higher subjective rate of time preference to maintain the same level of utility.

Up to this, we determine the criteria based on which an individual decide how much he/she will consume now and defer. Now he/she will go for evaluating his/her investment opportunities. An individual will make all investments in productive opportunities that have rates of return higher than his or her subjective rate of time preference, ri.

Copeland, Weston & Shastri 27

Consumption And InvestmentWithout Capital Markets

Each individual has productive investment opportunitiesABX=production/investment opportunity set.Assume, diminishing marginal returns to investment because the more an individual invests, the lower the rate of return on the marginal investment so ABX is concave.Individual endowed with a resource bundle (Y0, Y1)

MRT= Slope of a line tangent to curve ABX is the marginal rate of return from each additional dollar investment.

The line tangent to point A has the highest slope .

Consumption And InvestmentWithout Capital Markets

An investor will continue his/her investment up to the point where investor's subjective marginal rate of substitution is equal to the marginal rate of transformation offered by the production opportunity set i.e.

MRS=MRT Here, the amount of investment is Y0 – C0.

If C0 > Y0, he or she will disinvest. Individuals consumption in each time period is exactly equal to the

output from production i.e. P0=C0 & P1=C1

Without capital markets, individuals with the same endowment and the same investment opportunity set may choose completely different investments because of different indifference curves.

28Copeland, Weston & Shastri

Copeland, Weston & Shastri 29

Consumption And InvestmentWithout Capital Markets

Individual 2, who has a lower rate of time preference will choose to invest more than individual 1.

Copeland, Weston & Shastri 30

Understanding Capacity Test

Suppose your production opportunity set in a world of perfect certainty consists of the following possibilities:

a. Graph the production/investment opportunity set.b. If market rate is 10%, what is the optimum investment?

Project Outlay RR (%)A 1000000 8B 1000000 20C 2000000 4D 3000000 30

Copeland, Weston & Shastri 31

Consumption And InvestmentWith Capital Markets

• What happens if instead of one person, many individuals are said to exist in the economy?

• Intertemporal exchange of consumption bundles will be represented by the opportunity to borrow or lend unlimited amounts at r, a market determined rate of interests.

• Capital market facilitate the transfer of funds between lenders and borrowers. If the interest rates are positive, any amount of funds are lent today will return interest plus principal.

Copeland, Weston & Shastri 32

Consumption And InvestmentWith Capital Markets

We can graph borrowing and lending opportunities along the capital marketline (line W0ABW1). With an initial endowment of (Y0, Y1) that has utility equal to U1, we can reach any point along the market fine by borrowing or lending at the market interest rate plus repaying the principal amount, X0.The present value, W0, of our initial endowment (Y0, Y1) is the sum of cur-rent income, Y0, and the present value of our end-of-period income, Y1(1 + r)-1.

Copeland, Weston & Shastri 33

Consumption And InvestmentWith Capital Markets

Here,Capital Market Line = W0ABW1

Initial endowment = (Y0, Y1)Lending Portion=W1ABorrowing Portion=W0AUtility= U1

Subjective Rate = Slope of U1 at point A.Market Interest rate = Slope of CML at any point.

Notice, here we use the term CML rather than Budget Line. Why???

So we can maximize utility by moving along the market line to the point where our subjective time preference equals the market interest rate i.e.

SR = MR

34

Consumption And InvestmentWith Capital Markets

Copeland, Weston & Shastri

• Point B represents the consumption bundle on the highest attainable indifference curve i.e. we desire to lend because the capital market offers a rate of return higher than what we subjectively require as our subjective time preference, represented by the slope of a line tangent to the indifference curve at point A, is less than the market rate of return.

• So our optimum consumption= C0*, C1* at Utility U2 which is greater than Utility U1.

• Now, it can be said our initial endowment must be equal to the sum of our two period consumptions. In other words, our wealth must be equal to our consumptions.

Consumption And InvestmentWith Capital Markets

35Copeland, Weston & Shastri

• The present value of wealth, W0 is the sum of current income, Y0, and the present value of our end-of-period income, Y1(1 + r)-1 i.e.

• Again, the present value of our endowment equals the present value of our consumption and both are equal to our wealth,W0. i.e.

36

Consumption And InvestmentWith Capital Markets

Copeland, Weston & Shastri

Thus the capital market line has an intercept at W1 and a slope of -(1+r).

Note that moving along the capital market line does not change one's wealth, but it does offer a pattern of consumption that has higher utility.

Up to these we Ignore production for the time being and graph borrowing and lending opportunities along the capital market line.

What happens if the production/consumption decision takes place in a world where capital markets facilitate the exchange of funds at the market rate of interest?

Next graph combines production possibilities with market exchange possibilities.

Lets see what happens….

Copeland, Weston & Shastri 37

Consumption And InvestmentWith Capital Markets

With the family of indifference curves U1, U2, and U3 and endowment (Y1, Y2) at point A, what actions will we take in order to maximize our utility?

Starting at point A, we can move either along the PPC or along the CML.

Both alternatives offer a higher rate of return than our subjective time preference, but production offers the higher return, (steeper slope). So we choose to invest and move along the production opportunity frontier.

Copeland, Weston & Shastri 38

Consumption And InvestmentWith Capital Markets

• Without the opportunity to borrow or lend along the capital market line, we would stop investing at point D, where MRT=MRS and our level of utility has increased from U1 to U2.

• With the opportunity to borrow, we can actually do better. At point D the borrowing rate, represented by the slope of the CML, is less than the rate of return on the marginal investment, which is the slope of the production opportunity set at point D.

• Since further investment returns more than the cost of borrowed funds, we will continue to invest until the marginal return on investment is equal to the borrowing rate at point B.

Copeland, Weston & Shastri 39

Consumption And InvestmentWith Capital Markets

• We can now reach any point on the market line. Since our time preference at point B is greater than the market rate of return, we will consume more than Po, which is the current payoff from production.

• By borrowing we can reach point C on the capital market line. Our optimal consumption is found where our subjective time preference just equals the market rate of return.

• Our utility has increased from U1 at point A (our initial endowment) to U2 at point D (the Single person solution) to U3 at point C (the exchange economy solution). We are clearly better off when capital markets exist since U3 > U2.

Copeland, Weston & Shastri 40

Consumption And InvestmentWith Capital Markets

The decision process that takes place with production opportunities and capital market exchange opportunities occurs in two separate and distinct steps:

1. First, choose the optimal production decision by taking on projects until marginal rate of return on investment equals objective market rate;

2. then choose the optimal consumption pattern by borrowing or lending along the capital market line to equate your subjective time preference with the market rate of return.

The separation of the investment (step 1) and consumption (step 2) decisions is known as the Fisher separation theorem.

Fisher separation theorem: Given perfect and complete capital markets, the production decision is governed solely by an objective market criterion (represented by maximizing attained wealth) without regard to individuals' subjective preferences that enter into their consumption decisions.

Copeland, Weston & Shastri 41

Consumption And InvestmentWith Capital Markets

What is the implication of this theory in business???An important implication for corporate policy is that the

investment decision can be delegated to managers i.e. given the same opportunity set, every investor will make the same production decision (P0, P1) regardless of the shape of his or her indifference curves.

Investors will direct the manager of their firm to choose production combination (P0, P1). They can then take the output of the firm and adapt it to their own subjective time preferences by borrowing or lending in the capital market.

Copeland, Weston & Shastri 42

Consumption And InvestmentWith Capital Markets

Both investor 1 & 2 will direct the manager of their firm to choose production combination (P0, P1).Investor 1 will consume more than current production (point A) by borrowing today in the capital market and repaying out of future production.Investor 2 will lend because s/he consumes less than current production.Either way, they are both better off with a capital market. But how???Without capital market opportunities to borrow or lend, investor I & 2 would be worse off at point Y & X which have lower utility.

Copeland, Weston & Shastri 43

Consumption And InvestmentWith Capital Markets

Finally, in equilibrium, the marginal rate of substitution for all investors is equal to the market race of interest, and this in turn is equal to the marginal rate of transformation for productive investment. i.e.

MRS= -(1+r) =MRT

They allow the efficient transfer of funds between borrowers and lenders. Individuals who have insufficient wealth to take advantage of all their investment opportunities that yield rates of return higher than the market rate are able to borrow funds and invest more than they would without capital markets. In this way, funds can be efficiently allocated from individuals with few productive opportunities and great wealth to individuals with many opportunities and insufficient wealth. As a result, all (borrowers and lenders) are better off than they would have been without capital markets.

Copeland, Weston & Shastri 44

Does establishment of capital markets increase the transaction cost???

Assume that we have a primitive economy with N producers, each making a specialized product and consuming a bundle of all N consumption goods. Given no marketplace, bilateral exchange is necessary. During a given time period, each visits the other in order to exchange goods.

For example, there are five individuals and five consumption goods in this economy & the cost of each leg of a trip is T dollars.

I. If there is no market place, then how many trips individual1, individua2 individual3, individual4 & individual5 makes ? How many trips all individuals make? What will be the total cost?

II. If market place exists, then then how many trips individual1, individua2 individual3, individual4 & individual5 makes ??? How many trips all individuals make? What will be the total cost?

III. Is anyone better off or worse off for having market place? If yes, how much?

45

Does establishment of capital markets increase the transaction cost????

Without Capital Market With Capital Market

Copeland, Weston & Shastri

Total Trips= (N (N-1))/2 Total Trips= N

Total savings or better off= [{N (N-1)}/2 - N ] T

Copeland, Weston & Shastri 46

Understanding Capacity Testing

• There are 12 individuals and 12 consumption goods in the economy & the cost of each leg of a trip is BDT. 50.

I. If there is no market place, then how many trips each individual makes? How many trips all individuals altogether make? What will be the total cost?

II. If market place exists, then then how many trips each individual makes? How many trips all individuals altogether make? What will be the total cost?

III. Is anyone better off or worse off for having market place? If yes, how much?

Copeland, Weston & Shastri 47

Does transaction cost create any problem to Fisher

Theory??? The theory of finance is greatly simplified if we assume

that capital markets are perfect. Obviously they are not. If transactions costs are trivial, then borrowing and lending

interest rate will be same. Then there will be no problem to Fisher theory of separation.

But if transactions costs are nontrivial, the borrowing rate will be greater than the lending rate. Different borrowing and lending rates will have the effect of invalidating the Fisher separation principle.

Without a single market rate, investors will not be able to delegate the investment decision to the manager of their firm.

Copeland, Weston & Shastri 48

Consumption And InvestmentWith Capital Markets

Individual 1 would direct the manager to use the lendingrate and invest at point B.Individual 2 would use the borrowing rate and choosepoint A. A third individual might choose investments between points A and B, where his or her indifference curve is directly tangent to the production opportunity set.

The effects of taxes and information asymmetries are certainly nontrivial, so these also create problems in theories. These all will be discussed in later chapters.

Copeland, Weston & Shastri 49

Best of Luck!!!