copyright 2002, pearson education canada1 the price system and supply and demand chapter 5

Post on 18-Dec-2015

213 views

TRANSCRIPT

Copyright 2002, Pearson Education Canada1

The Price System and Supply and Demand

Chapter 5

Copyright 2002, Pearson Education Canada2

The Price System: Rationing and Allocating Resources

The price system performs two important and closely related functions in a society with unregulated markets: Price Rationing Resource Allocation

Copyright 2002, Pearson Education Canada3

Price Rationing

Price rationing is the process by which the market system allocates goods and services to consumers when quantity demanded exceeds quantity supplied.

Copyright 2002, Pearson Education Canada4

Price Rationing in the Market for Lobsters (Figure 5.1)

In 2001 the market for lobsters is in equilibrium. At $10 per kg the quantity demanded and quantity supplied are both 20 million kg.

The initial equilibrium is at point C.

Copyright 2002, Pearson Education Canada5

Price Rationing in the Market for Lobsters cont. (Figure 5.1)

In 2002 a large part of the lobstering waters are closed.

The supply curve shifts to the left.

Now, at point A, we have an excess demand of 10 million kg.

Copyright 2002, Pearson Education Canada6

Price Rationing in the Market for Lobsters cont. (Figure 5.1)

The reduced supply causes the price to rise.

The market’s price rationing function becomes apparent as the quantity supplied increases and the quantity demanded decreases as we move from A to B.

Finally a new equilbrium is established at $13.75 and 16 million kg.

Copyright 2002, Pearson Education Canada7

Governments or firms may use alternative allocation methods:

Price ceilings Queuing Favoured customers Ration coupons

Copyright 2002, Pearson Education Canada8

Alternative Allocation Methods:

A price ceiling is a maximum price that sellers may charge for a good, usually established by government.

Queuing is a nonprice rationing system that uses waiting in line as a means of distributing goods and services.

Copyright 2002, Pearson Education Canada9

Excess demand created by a ceiling price for Tickle Me Elmo dolls in 1996 (Figure 5.3)

If the price had been set from supply and demand it would have been about $100.

At $35 demand exceeded supply and an alternative rationing system had to be used.

Copyright 2002, Pearson Education Canada10

Alternative Allocation Methods (cont.):

Favoured customers are those who receive special treatment from dealers during situations when there is excess demand.

Ration coupons are tickets or coupons that entitle individuals to purchase a certain amount of a given product per month.

Copyright 2002, Pearson Education Canada11

Black Markets

The problem with these alternatives is that they do not eliminate the excess demand for the products.

Despite best efforts of governments and firms black market can emerge.

A black market is a market in which illegal trading takes place at market-determined prices.

Copyright 2002, Pearson Education Canada12

The Canadian Farm Crisis

The use of subsidies in the form of price floors (minimum guaranteed prices) by U.S. and European governments has distorted world markets.

Canadian producers who do not enjoy the same level of subsidy are at a disadvantage despite being as efficient as their counterparts.

Copyright 2002, Pearson Education Canada13

Agricultural Policy and the Prairie Farm Crisis (Figure 5.4a)

A price support or price floor at Ps will create a surplus of wheat q1q2 and increase income (P*Q) from P0q0 to P2q2.

Copyright 2002, Pearson Education Canada14

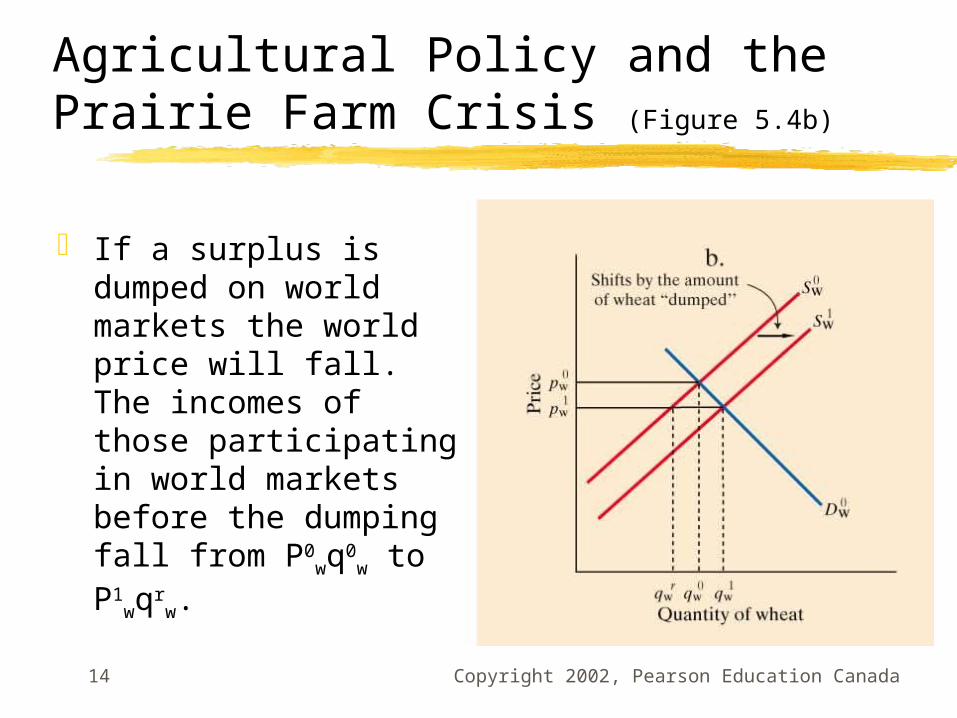

Agricultural Policy and the Prairie Farm Crisis (Figure 5.4b)

If a surplus is dumped on world markets the world price will fall. The incomes of those participating in world markets before the dumping fall from P0

wq0w to P1

wqrw.

Copyright 2002, Pearson Education Canada15

Agricultural Policy and the Prairie Farm Crisis (Figure 5.4c)

A policy that combines restrictions on imports and a price support will result in a dramatic expansion of the agricultural sector in a country implementing these policies. In this example output of wheat grows from q1

0 to q1

3

Copyright 2002, Pearson Education Canada16

Supply and Demand Analysis: The Price of Gasoline (Figure 5.5a)

The market is in equilibrium in February 1999 with the spot price at US$11.53, and 76 million barrels a day purchased and sold.

A shift in supply or demand is required for an increase in price.

Copyright 2002, Pearson Education Canada17

Supply and Demand Analysis: The Price of Gasoline (Figure 5.5b)

At a meeting in March 1999, OPEC members agree to cut production by 4 million barrels to improve revenue.

This shifts the supply curve to S1 and causes consumers to bid the price up to US$34 by November.

The increased price also leads to movement along the supply curve from B to C and movement along the demand curve from A to B to reach the new equilibrium.

Copyright 2002, Pearson Education Canada18

Supply and Demand Analysis: The Price of Gasoline (Figure 5.5c)

By February 2000, OPEC increases supply slightly, but demand also has increased.

The new equilibrium is at a higher quantity but the same price.

Copyright 2002, Pearson Education Canada19

Elasticity

Elasticity is a general concept that can be used to quantify the response in one variable when another variable changes.

If some variable, A, changes in response to a change in another variable, B, then:

Elasticity of A with respect B = % change in A % change in B

Copyright 2002, Pearson Education Canada20

Price Elasticity of Demand

The price elasticity of demand is the ratio of the percentage change in quantity demanded to the percentage change in price.

Price Elasticity of Demand = % change in quantity demanded % change in price

Copyright 2002, Pearson Education Canada21

Perfectly Inelastic Demand

Perfectly inelastic demand is demand in which quantity demanded does not respond at all to a change in price.

An example could be the demand for insulin.

Copyright 2002, Pearson Education Canada22

Inelastic Demand

Inelastic demand is demand that responds somewhat, but not a great deal, to changes in price. Inelastic demand always has a numerical value between zero minus one.

An example would be the demand for housing or telephone service.

Copyright 2002, Pearson Education Canada23

Unitary Elasticity

Unitary elasticity is a demand relationship in which the percentage change in quantity of a product demanded is the same as the percentage change in price.

The elasticity is always equal to minus one.

Copyright 2002, Pearson Education Canada24

Elastic Demand

Elastic demand is a demand relationship in which the percentage change in quantity demanded is larger in absolute value than the percentage change in price.

The demand elasticity has an absolute value greater than one.

An example could be the demand for bananas or any other product for which there are close substitutes.

Copyright 2002, Pearson Education Canada25

Perfectly Elastic Demand

Perfectly elastic demand is demand in which quantity demanded drops to zero at the slightest increase in price.

An example could be the demand for wheat on the world market, or any other good that can only be sold at a predetermined price.

Copyright 2002, Pearson Education Canada26

Demand Curves and Elasticity

P

D

Q

P

D

Q

PD

Q

P

D Q

Perfectly elastic

Perfectly inelastic

Relatively elastic

Relatively inelastic

Copyright 2002, Pearson Education Canada27

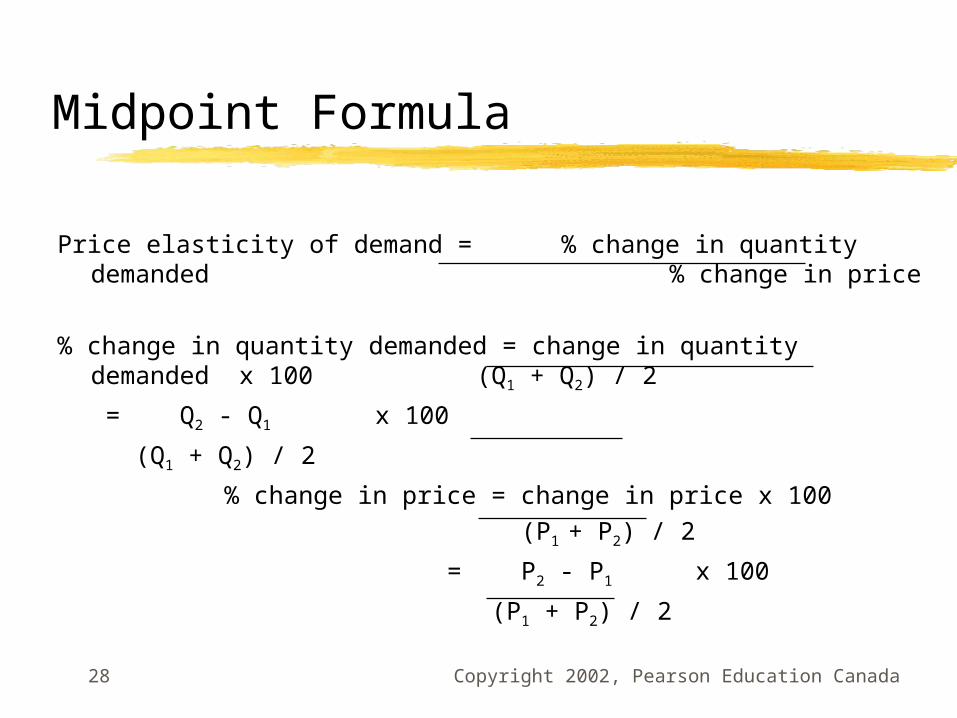

Calculating Elasticity Using the Midpoint Formula

The midpoint formula is a more precise way of calculating percentages using the value halfway between P1 and P2 for the base in calculating the percentage change in price, and the value halfway between Q1 and Q2 as the base for calculating the percentage change in quantity demanded.

Using the initial values of P and Q as the base to calculate percentages is misleading.

Copyright 2002, Pearson Education Canada28

Midpoint Formula

Price elasticity of demand = % change in quantity demanded % change in price

% change in quantity demanded = change in quantity demanded x 100 (Q1 + Q2) / 2

= Q2 - Q1 x 100

(Q1 + Q2) / 2

% change in price = change in price x 100 (P1 + P2) / 2

= P2 - P1 x 100

(P1 + P2) / 2

Copyright 2002, Pearson Education Canada29

Elasticity Changes Along a Straight-Line Demand Curve (Figure 5.8)

Demand is quite elastic from A to B and quite inelastic from C to D.

Copyright 2002, Pearson Education Canada30

Calculating Price Elasticity From A to B

% change in quantity demanded = Q2 - Q1 x 100

(Q1 + Q2) / 2

= 4 - 2 x 100 = 66.7% (4 + 2) / 2

% change in price = P2 - P1 x 100

(P1 + P2) / 2

= 9 - 10 x 100 = - 10.5% (9 +10) / 2

Elasticity of demand = % change in quantity demanded = 66.7% = - 6.4 % change in price -10.5%

Copyright 2002, Pearson Education Canada31

Calculating Price Elasticity From C to D

% change in quantity demanded = Q2 - Q1 x 100

(Q1 + Q2) / 2

= 18 - 16 x 100 = 11.7% (18 + 16) / 2

% change in price = P2 - P1 x 100

(P1 + P2) / 2

= 2 - 3 x 100 = - 40% (3 +2) / 2

Elasticity of demand = % change in quantity demanded = 11.7% = - 0.294 % change in price -40%

Copyright 2002, Pearson Education Canada32

Elasticity and Total Revenue

Effect of a price increase on a product with inelastic demand: P x Qd = TR

Effect of a price increase on a product with elastic demand: P x Qd = TR

Effect of a price cut on a product with elastic demand: P x Qd = TR

Effect of price cut on a product with inelastic demand: P x Qd = TR

Copyright 2002, Pearson Education Canada33

Relationship Between Elasticity and Total Revenue (Figure 5.9)

Copyright 2002, Pearson Education Canada34

Determinants of Demand Elasticity

Availability of substitutes When substitutes are not readily available, demand

is likely to be less elastic.

The importance of being unimportant When an item represents a small proportion of our

total budget, demand is likely to be less elastic.

The time dimension In the longer run, demand is likely to become more

elastic, or responsive, because households make adjustments over time.

Copyright 2002, Pearson Education Canada35

Other Important Elasticities

Income elasticity of demand Measures the responsiveness of demand with

respect to changes in income

Cross-price elasticity of demand A measure of the response of the quantity of

one good demanded to a change in the price of another good

Copyright 2002, Pearson Education Canada36

Other Important Elasticities (cont.)

Elasticity of supply A measure of the response of the quantity of a

good supplied to a change in the price of that good. Likely to be positive in output markets

Elasticity of labour supply A measure of the response of labour supplied

to a change in the price of labour. Can be negative or positive

Copyright 2002, Pearson Education Canada37

Review Concepts and Terms

black market cross-price elasticity of

demand elastic demand elasticity elasticity of labour supply elasticity of supply favoured customers income elasticity of

demand

inelastic demand midpoint formula perfectly elastic demand perfectly inelastic demand price ceiling price elasticity of demand price rationing queuing ration coupons unitary elasticity