copyright © 2004 by thomson southwestern all rights reserved. 13-1 asset management for depository...

TRANSCRIPT

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-1

Asset Management for Depository Institutions:

Commercial, Consumer, and Mortgage Lending

Chapter 13

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-2

Trends

Lending has become much more competitive• Large corporations have capital market access• Individuals have multiple sources of loans for

◦ Real estate◦ Consumer credit

Evaluation of credit quality still very important for small &medium-sized firms

Is amount of consumer credit too large?Non-performing loans as a risk measureGrowth in mortgage lending

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-3

Trends in Types of Loans

Total Loans, August 2003: $4,448 trillion

Consumer Loans 13.0%

Real Estate Loans 50.0%

Commercial Loans 20.0%

Other Loans 17.0%

Source: Compiled by the authors from Federal Reserve Bulletin, November 2003, Table 1.26, A15.

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-4

Consumer Credit & Mortgage Debt?

Holders of Consumer Credit

Holders of Mortgage Debt

Individuals and Others 9%

Mortgage Poolsor Trusts 49%

Life Insurance Companies 3%

Commercial Banks 24%

Savings Institutions 10%

Federal and Related Agencies 5%

Nonfinancial Firms 3%

Savings Institutions 4% Finance Companies 13%

Commercial Banks 33% Securitized Pools 35%

Credit Unions 12%

Source: Federal Reserve Bulletin, November 2003, A34

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-5

Lending

Lending• High return – high risk• Default risk can be due to

◦ Mismanagement◦ Economic conditions◦ Uninsurable disasters◦ Fraud

• Longer term is higher risk

Risk of lending is managed, never eliminated

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-6

The Credit Process:Managing & minimizing

Credit RiskLending is highly regulated including

• Types of loans & distribution across industries• Collateral and documentation required• Internal lending process

A bank’s written loan policy details the specificsLoan committee reviewMonitoring & maintenance proceduresWorkout proceduresRole of lending in business development

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-7

Bank’s Written Loan Policy

Major Components Include:• Desired composition and size of loan portfolio• Specification of loan approval process and the

authority of individuals, committees, etc.• Responsibilities of participants• Operating procedures• Documentation required• Loan review & maintenance procedures &

responsibilities• Guidelines for management of loan collateral• Policies and procedures for setting rates and

repayment terms• Statement of quality standards• Description of bank's principal trade area• Procedures for detecting and working out problem

loans

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-8

Regulations on Lending

Purposes• To protect consumers• To minimize possibility of bailout with insurance• To maintain stability of financial system• To standardize procedures, instruments

A business is assumed to be knowledgeable, a consumer is not and full disclosure is mandatory

Discrimination against any member of a protected class is prohibited

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-9

Major Consumer Lending Regulations

The Equal Credit Opportunities Act

The Fair Housing Act

The Fair Credit Reporting Act of 1970

Truth in Lending

Reg Z

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-10

Mortgage Lending Regulations

A Union Residential Loan Application

The Real Estate Settlement Procedures Act

The Home Mortgage Disclosure Act

The Community Reinvestment Act

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-11

Other Major Compliance Policies

Loans to Insiders Act

Limits on Lending to One Party as a Percentage of Total Capital

Credit Execution Policies

Lender Compensation Policies

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-12

Commercial Loan Application Process I

Acquire information• Business description and principal contacts• Amount & purpose of loan• History and operations of firm, industry• Profile of management, experience and

expertise• Full financial statements, credit analysis• Verification of assets, liabilities, income

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-13

Commercial Loan Application Process II

Analyze information received• Spread financial statements and compare to

industry data (Robert Morris Associates, Dun & Bradstreet)

• Collect external information on the firm• Develop recommendation on application

Present application to loan committee• If no, determine what and how to present it• If yes, determine final terms, conditions and

participation, and perfect all documentation

Present decision to applicant

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-14

Five Cs of Credit

Character -the willingness of a customer to pay

Capacity - the ability of a customer to pay in terms of cash flow

Capital - the soundness of a borrower's financial position in terms of equity

Conditions - the industry and economic conditions that may affect a firm’s ability to repay a loan

Collateral - secondary sources of repayment

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-15

Commercial Loan Credit Scoring Model

Purpose• To minimize credit risk (minimize defaults while

making good loans)• To process financial information in a timely and

less expensive way

Models are developed from historical data to discriminate between “good” firms and firms more likely to default

Generally used in conjunction with other analysis

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-16

Consumer Credit Scoring Model

Created to • standardize consumer loan decisions

◦ consistent evaluation◦ minimize discrimination claims

• reduce cost of loan application evaluation◦ reduce time required◦ reduce experience level of evaluator

Based on discriminant analysis of past loans and variables affecting them

Used by major corporations as well as banksConsists of a scoring system and a decision

function

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-17

1. Occupation professional (Executive) 12 skilled worker

8 clerical worker 7 student 5 unskilled worker 4 part-time employee 2

2. Housing status owns home 6 rents home or apartment 4 lives with friend or relative

2 3.Credit rating

excellent10

average 5 no record

2 poor

0 4. Length of time on current job

more than one year 5 one year or less 2

5. Length of time at current address more than one year 2 one year or less 1

6. Telephone in residence yes 2 no 0

7. Number of dependents none 3 one 3 two 4 three 4 more than three 2

8. Bank accounts held both checking & savings 4 savings account only 3 checking account only 2 none 0

8. Bank credit card yes 6 no 0

Consumer Credit Scoring SystemAn Example

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-18

Consumer Credit Scoring System Decision Function

Total Score Credit Decision28 or less Reject application29-30 Extend credit up to $50031-33 Extend credit up to $1,50034-36 Extend credit up to $2,50037-38 Extend credit up to $3,50039-40 Extend credit up to $5,00041-45 Extend credit up to $8,000over 45 Extend credit up to $12,000

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-19

Other Credit Risk Management Methods

Credit risk is evaluated• By customer• By type of loan (commercial, consumer, etc)• Overall for the firm

Managing overall firm credit risk• Value at risk (VAR)• CreditMetrics

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-20

Commercial Lending: Financial Statement Analysis

Types of Information Required• Past financial statements• Personal financial information from the owner• Projection of the future financial position• A credit report• Financial performance measures for similar firms as a

basis of comparison• Economic projections

External Sources of InformationEvaluating Risk

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-21

Important Financial Ratios

Overall Profitability: Return on Equity = Net Income/Equity

Return on Assets = Net Income/AssetsCost Efficiency: Net Profit Margin = Net Income/Revenues

Operating Profit Margin = Operating income/RevenuesGross Profit Margin = Gross Income/Revenues

Revenue Generation: Total Asset Turnover = Revenue/SalesFixed Asset Turnover = Fixed Asset/RevenuesInventory Turnover = Cost of Goods Sold/InventoryAccounts Receivables Turnover = Revenues/Accounts Receivables

Days Cash Cycle Inventory Days = 365/Inventory TurnoverAverage Collection Period = 364/AR TurnoverAccounts Payable Days = 365/(CGS/Accounts Payable)

Days Cash to Cash Cycle =Average Collection Period+Days Inventory - Days Accounts PayableDebt and Coverage Ratios Debt to Assets =Total Debt/Total Assets

Interest Coverage = EBIT/Interest ExpenseFixed Charge Coverage = (EBIT + Fixed Charges)/(Int Exp + Fixed

Ch)Cash Flow to Total Debt = Operating Cash Flow/Total Debt

Liquidity Ratios Current Ratio = Current Assets/Current LiabilitiesQuick Ratio = (Current Assets - Inventory)/Current LiabilitiesNet Working Capital Ratio = Net Working Capital/Total Assets

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-22

Commercial LendingSample Loan Presentation

Background and RequestRepayment AnalysisSecondary and Tertiary Sources of RepaymentFinancial Analysis SummaryBalance SheetIncome StatementGuarantor and CollateralRisk Analysis and RecommendationProposed Loan Structure

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-23

Establishing Loan Terms

Loan amount

Lending rate

Maturity and timing of payments

Non-interest terms and fees

Collateral, guarantees, other sources of repayment

Restrictive covenants

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-24

Lending Rate

Lending rate must include• Base lending rate• Default risk premium• Administrative cost premium• Desired profit margin

May be• Fixed (usually for short-term or small loans)• Variable (for longer-term or larger loans)

Copyright © 2004 by Thomson Southwestern All rights reserved.

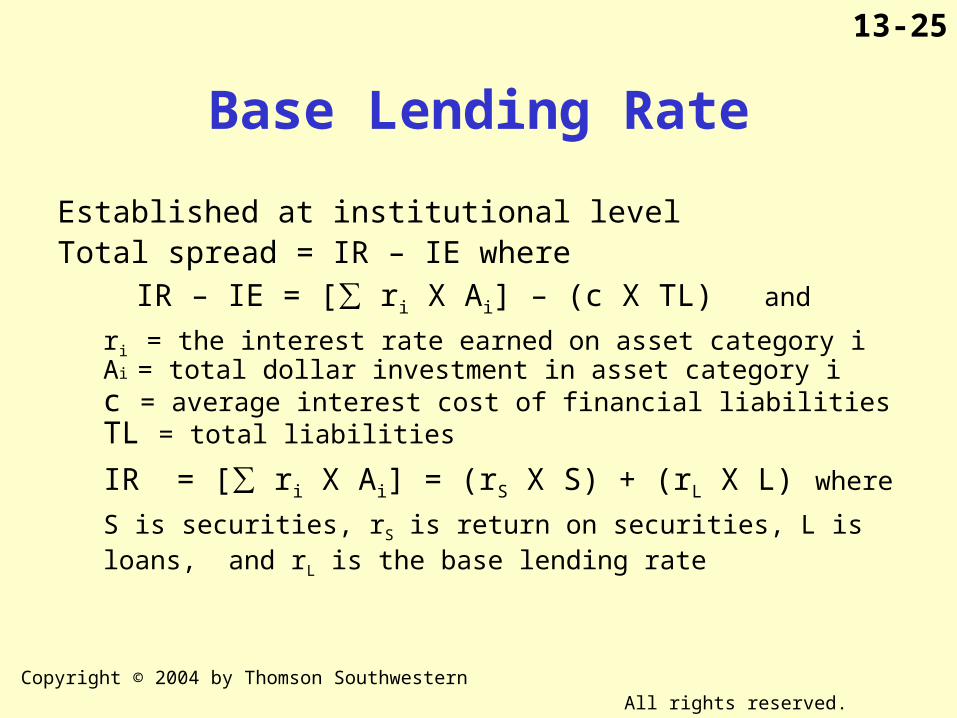

13-25

Base Lending Rate

Established at institutional levelTotal spread = IR – IE where

IR – IE = [∑ ri X Ai] – (c X TL) and

ri = the interest rate earned on asset category iAi = total dollar investment in asset category ic = average interest cost of financial liabilities TL = total liabilities

IR = [∑ ri X Ai] = (rS X S) + (rL X L) where

S is securities, rS is return on securities, L is loans, and rL is the base lending rate

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-26

The cost to the borrower and the yield to the lender can be significantly affected by noninterest loan terms. The table illustrates how a commitment fee on a line of credit can increase an institution’s rate of return.

Stated interest rate 11.5% (base rate plus risk premium)Commitment fee 0.25% on unused portion of the

commitmentTerm 1 yearCompensating balances 8% of commitment plus 4% on

borrowed fundsEstimated average loan balance 60% of commitmentMaximum line of credit $2,000,000

Loan Interest and Noninterest RevenueInterest [$2,000,000(0.6)(0.115)] $138,000Fees [$2,000,000(0.4)(0.0025) 2,000

Total Revenues $140,000

EFFECT OF NONINTEREST LOAN TERMS ON

THE LENDER’S EXPECTED RETURN

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-27

Net Funds InvestedAverage loan balance $1,200,000Portion offset by compensating bal.

$2,000,000(0.08) $ (160,000)$1,200,000(0.04) ( 48,000)

Deduct reserve requirements[10% ×($160,000 + $40,000) ( 20,800)Total offsetting funds (187,200)

Net Invested funds $1,012,800

Total Expected Return(Interest and Noninterest Revenues ) ÷ Net invested

funds

$140,000 ÷ $1,012,800 = 13.82%

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-28

Noninterest Terms and Conditions

These increase bank’s expected return• Compensating Balance Requirements• Lines of credit fees• Commitment fees• Discounted loans• Fees for other banking services

Customer Pricing Using Profitability Analysis

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-29

Noninterest Terms & Conditions (continued)

Collateral assigned by a security agreement• Provides secondary source of repayment• Value must be secure and documentation

proper◦ At outset◦ During the term of the loan

Arrangements include• Floating liens• Warehouse receipts• Floor planning• factoring

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-30

Restrictive Covenants

Protect bank’s interest during term of loanPositive covenant examples

• Borrower will provide current financial statements every quarter

• Borrower will have key person insurance payable to bank

Negative covenant examples• Borrower will maintain certain minimum ratios

for liquidity and debt coverage• No significant assets will be sold or debt

acquired without prior permission of the bank

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-31

Special Consideration for Different Types of Loans

Seasonal Working Capital Loans

Term Loans

Commercial Real Estate Loans

Agricultural Loans

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-32

Consumer Loans

Credit card loans• Unsecured cards• Secured cards

Installment loans• Different ways to calculate interest rates &

returns• The rule of 78s as a prepayment penalty

Home equity loans (hels)Second mortgage loans

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-33

Special Consideration of Mortgage Loans

ARMSDue on Sale ClausesInnovative Mortgages

• Graduated payment mortgages• Reverse annuity mortgages• Growing equity mortgagees• Price-level adjusted mortgages

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-34

Small Business Loans

Are more risky than large business loansSmall Business Administration loansSBA

• Guarantees loans which do not qualify for a conventional loan

• Does not make loan, but guarantees repayment of most of the loan

SBA guarantee reduces default cost to bank but not default probability

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-35

Types of Higher Risk Lending

Sub prime Lending

Leveraged Buyouts

Mezzanine Lending

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-36

Loan Monitoring & Maintenance

Goals• To keep good loans from going bad• Uncover problems while they are small• Accurately estimate quality of loan portfolio

Noncurrent loans can be described as• Past due• Nonperforming• Nonaccruing

Copyright © 2004 by Thomson Southwestern All rights reserved.

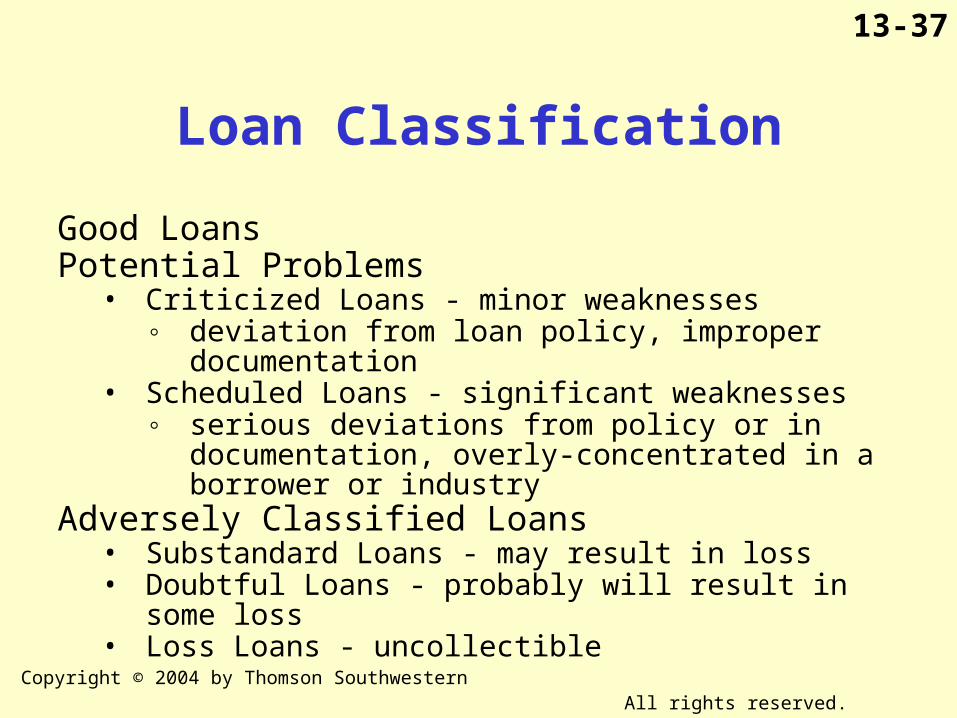

13-37

Loan Classification

Good LoansPotential Problems

• Criticized Loans - minor weaknesses◦ deviation from loan policy, improper

documentation• Scheduled Loans - significant weaknesses

◦ serious deviations from policy or in documentation, overly-concentrated in a borrower or industry

Adversely Classified Loans• Substandard Loans - may result in loss• Doubtful Loans - probably will result in some

loss• Loss Loans - uncollectible

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-38

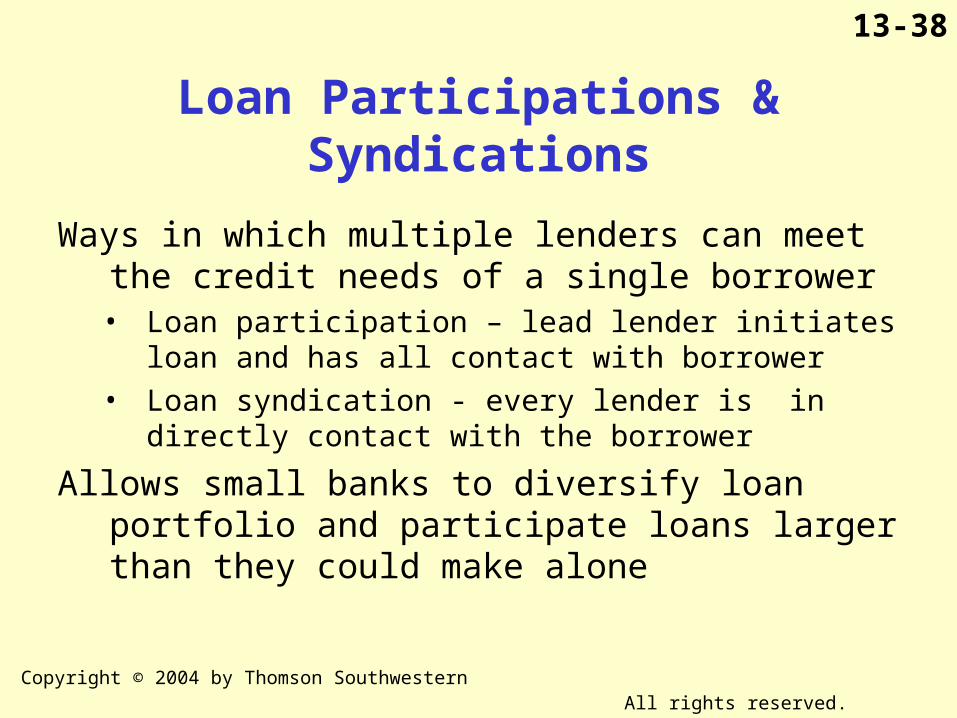

Loan Participations & Syndications

Ways in which multiple lenders can meet the credit needs of a single borrower• Loan participation – lead lender initiates loan

and has all contact with borrower• Loan syndication - every lender is in directly

contact with the borrower

Allows small banks to diversify loan portfolio and participate loans larger than they could make alone

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-39

Lender LiabilityLenders are sometimes sued by borrowers in

financial distress because• They refused to advance funds• Attempted to take position of collateral

Lenders are named in environmental liability suits if collateral used for loans is associated with environmental hazards.• To protect themselves, banks conduct

environmental audits on land and buildings used for collateral.

The best way to prevent lawsuits is to:• follow institutional monitoring procedures

scrupulously;• give ample notice to borrowers if credit is not to

be extended; and• keep excellent records.

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-40

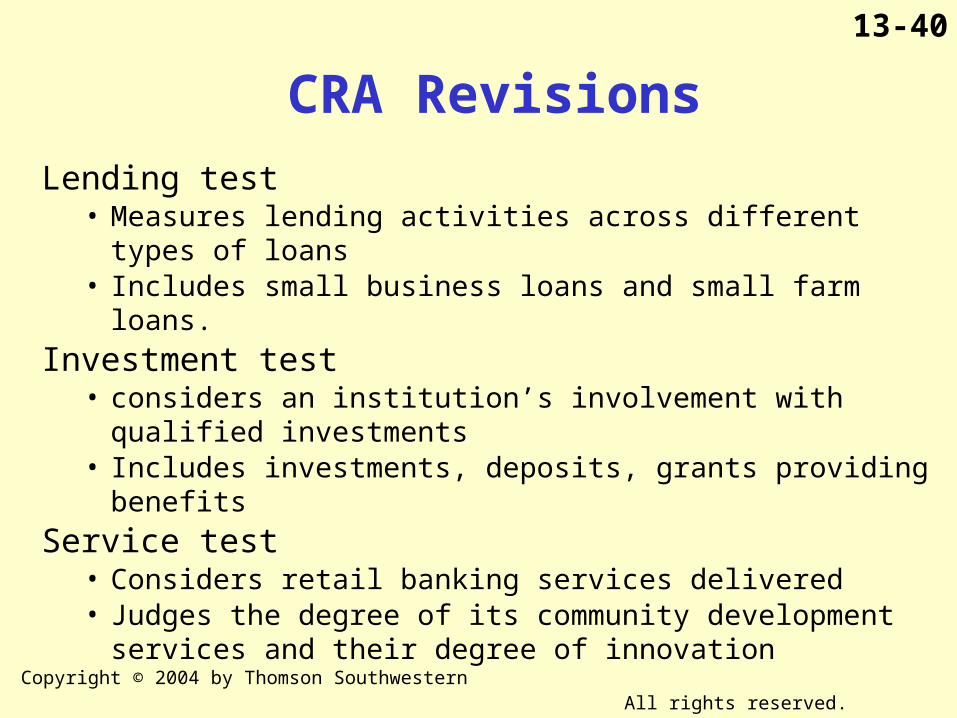

CRA Revisions

Lending test • Measures lending activities across different types of

loans • Includes small business loans and small farm loans.

Investment test • considers an institution’s involvement with qualified

investments• Includes investments, deposits, grants providing

benefitsService test

• Considers retail banking services delivered• Judges the degree of its community development

services and their degree of innovation

Copyright © 2004 by Thomson Southwestern All rights reserved.

13-41

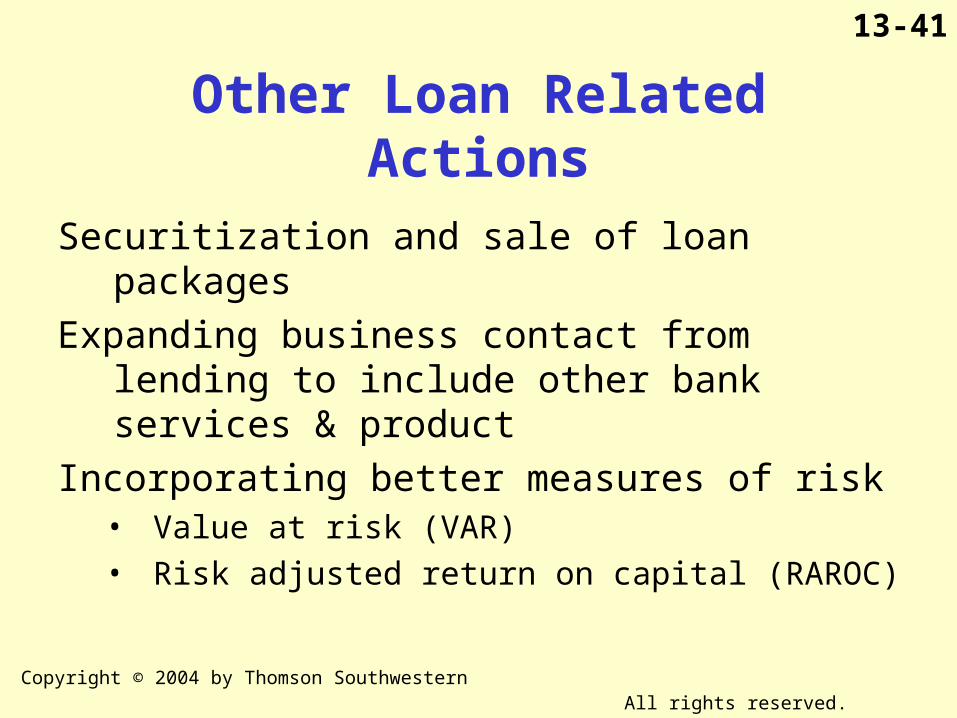

Other Loan Related Actions

Securitization and sale of loan packagesExpanding business contact from lending to

include other bank services & productIncorporating better measures of risk

• Value at risk (VAR)• Risk adjusted return on capital (RAROC)