copyright © information resources, inc. 2004. confidential and proprietary. pat handley, tropicana...

Post on 22-Dec-2015

213 views

TRANSCRIPT

Copyright © Information Resources, Inc. 2004. Confidential and proprietary.Beverages & Foods

Pat Handley, Tropicana

Steve Frenda, Mosaic InfoForce

February, 2005

What Trend Data Can’t Tell You About Out-of-StocksTropicana and Mosaic InfoForce

Beverages & Foods

2

Executive Summary - Out-of-Stocks In The Past

• The Traditional View of OOS

Over the last 10 years, Over 50 studies have been conducted

Virtually all studies report OOS in the 5-10% range

Conclude that 70-75% of OOS are the direct result of retail store practices

The consumer components tend to indicate that the retailer will lose nearly 50% of the planned purchases resulting in a loss of 4% of sales.

1

1Retail Out of Stocks: A Worldwide Examination of Extent, Causes and Consumer Responses – GMA, FMI, CIES

The traditional view grossly understates the seriousness of the problem Modernizing the view --- Out-of-stocks + Voids = Not Available For Sale NAS

Beverages & Foods

3

Executive Summary - Out-of-Stocks Today

A Contemporary View of “OOS”

A condition where a shelf tag exists with no product to support sale to the consumer continues to be a problem

More insidious is the product that should be in the store, but isn’t due to either planogram degradation or physical store and shelf limitations

This condition has largely been caused by the explosion of new products’ sizes, flavors, and “healthy for you” entries – Chain & store discipline a problem

Promotional activity has made the problem more serious. More flavors/varieties has put pressure on holding power for top sellers

The traditional view grossly understates the seriousness of the problem Modernizing the view --- Out-of-stocks + Voids = Not Available For Sale NAS

Beverages & Foods

4

The Transformation of OOS / Voids Analysis

Evaluate CurrentConditions

Drill Down ToCritical Times

Daily OOSReport

Use:

Determine RetailOOS, Distribution

& Discipline

Further detail OOS day part risks &

improve execution

Identify OOS events; model & predict drivers

Current Methodology 2005

Census Data& Audit

Census Store Level Daily Data

Day and TimeSpecific Audit

• Timely, Actionable• Store Level Data• Most Efficient

Beverages & Foods

5

OOS – Designing an Appropriate MethodologyOOS – In Reality, The 20% Problem

OOS with hole on shelf will be captured

OOS with pack out hole of substitute product will not likely be captured

without scanning

Inferior audit design solves for 5% of the

20% problem!!

OOS with hole on shelf will be captured

OOS with pack out hole of substitute product will not likely be captured

without scanning

Inferior audit design solves for 5% of the

20% problem!!

Beverages & Foods

6

The Problem is Serious

Across Most Categories, Base OOS is Running in

the 10-15% Range

Beverages & Foods

7

Case Study – Beer CategoryKroger, Michigan Division

Beverages & Foods

8

Case Study – Beer CategoryKroger, Michigan Division

• 112 stores• Average store stocks 185 beer

sku’s• # of items sold in the Division for 4

weeks? A. 200 B. 300C. 400D. 500

Beverages & Foods

9

3

3

4

4

5

6

9

10

11

16

19

8

4

4

6

<110 items

110-119

120-129

130-139

140-149

150-159

160-169

170-179

180-189

190-199

200-209

210-219

220-229

230-239

>240

Kroger – Michigan KMA - # of Beer Items Sold by Store

Distribution in 112 stores - There is a complete lack of consistency in the KMA planograms

• There were 525 different beer SKUs sold in the Michigan KMA last month.

• Average # of items sold by store is 185.

Beverages & Foods

10

A Practical Roadmap to NAS – Total U.S. Supermarket Chains

Beer / Ale – Average Chain/Store - # of Items

Total number of unique UPC’s sold in chain

Average # of unique UPC’s sold in stores

Average # of items observed on shelf audit

510

161

185

Reflects Chain Discipline

Reflects Store POG and Execution Discipline

Results in NASVoids + OOS

Results in NASVoids + OOS

-64%

-13%

Beer Category – From Approved to Customer – a 77% Problem

Beverages & Foods

11

“Healthy” Extensions Adding More Complication

MIF survey: Retailers asked “How high an impact will low carb and healthy product introductions have on your merchandising strategies, 1-10?”; result 7.5

Beverages & Foods

12

Consumers Navigating to Eat “Right” Retailers: “What Do I Stock? …Discontinue?

Regular Fat FreeLight

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

How Can Retailers Properly Stock, Advertise and Display These PrHow Can Retailers Properly Stock, Advertise and Display These Products?oducts?

Regular Fat FreeLight

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

How Can Retailers Properly Stock, Advertise and Display These PrHow Can Retailers Properly Stock, Advertise and Display These Products?oducts?

Beverages & Foods

13

Consumers Navigating to Eat “Right” Retailers: “What Do I Stock? …Discontinue?

Regular Fat FreeLight

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

How Can Retailers Properly Stock, Advertise and Display These PrHow Can Retailers Properly Stock, Advertise and Display These Products?oducts?

Regular Fat FreeLight

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

Low CarbsHigh Fat

High Cholesterol

Low CarbsModerate Fat

High Cholesterol

High CarbsNo Fat

No Cholesterol

How Can Retailers Properly Stock, Advertise and Display These PrHow Can Retailers Properly Stock, Advertise and Display These Products?oducts?

Low CarbsModerate Fat

No CholesterolNo Taste

Beverages & Foods

14

The Collision Between Assortment and Availability

Beverages & Foods

15

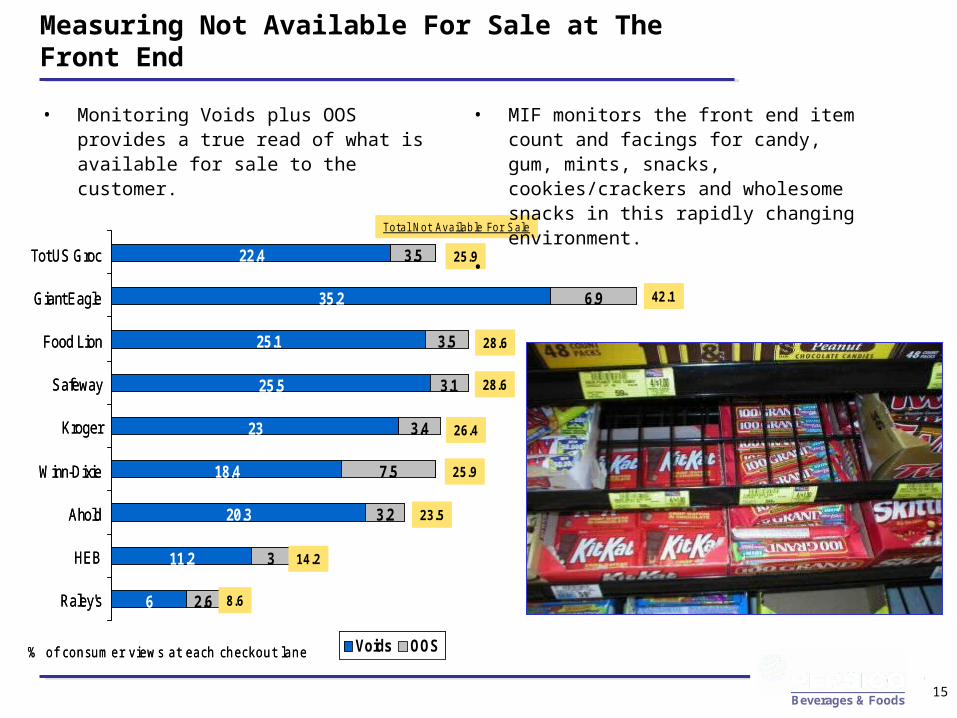

Measuring Not Available For Sale at The Front End

• Monitoring Voids plus OOS provides a true read of what is available for sale to the customer.

6

11.2

20.3

18.4

23

25.5

25.1

35.2

22.4

2.6

3

3.2

7.5

3.4

3.1

3.5

6.9

3.5

Raley's

HEB

Ahold

Winn-Dixie

Kroger

Safeway

Food Lion

Giant Eagle

Tot US Groc

Voids OOS

25.9

23.5

14.2

8.6

25.9

28.6

42.1

28.6

26.4

% of consumer views at each checkout lane

Total Not Available For S ale

6

11.2

20.3

18.4

23

25.5

25.1

35.2

22.4

2.6

3

3.2

7.5

3.4

3.1

3.5

6.9

3.5

Raley's

HEB

Ahold

Winn-Dixie

Kroger

Safeway

Food Lion

Giant Eagle

Tot US Groc

Voids OOS

25.9

23.5

14.2

8.6

25.9

28.6

42.1

28.6

26.4

% of consumer views at each checkout lane

Total Not Available For S ale

• MIF monitors the front end item count and facings for candy, gum, mints, snacks, cookies/crackers and wholesome snacks in this rapidly changing environment.

•

Beverages & Foods

16

The Front End – A Rapidly Changing Environment

An average supermarket sells 120 single serve candy, gum

and mint items

1,520

Beverages & Foods

17

Maximizing Consumer Choice

• 75% of Check Lanes Sell Chocolate Candy in This Chain

Percent Check Lanes Stocking UPC

Source: Mosaic InfoForce Check Lane Audit – Total U.S. Chain

Beverages & Foods

18

Maximizing Consumer Choice

• 75% of Check Lanes Sell Chocolate Candy in This Chain

Percent Check Lanes Stocking UPC

Source: Mosaic InfoForce Check Lane Audit – Total U.S. Chain

Beverages & Foods

19

Store Conditions - Realities

• Intentions of retailers and Field Sales are good, but distractions are many– Retailers see 30,000 new items per year– Broker consolidation = less brand dedication

• Many revenue “top dogs” now “second tier”

– No sense of urgency

• Planogram deterioration begins immediately

• Limited consumer support on line extensions cannot carry new product success alone

Beverages & Foods

20

Conclusions

• Quality retail execution can make or break success

• Must determine which KPI’s will drive performance for your brand, products or stores

• Set standards for retail field organization

• Measure performance – “inspect what you expect”

• Make results transparent throughout organization - ASAP– Offer tools that are accessible and easy to use– Focus limited field resources on categories or stores with biggest opportunity

gap

Copyright © Information Resources, Inc. 2004. Confidential and proprietary.Beverages & Foods

Pat Handley - Pepsico

Beverages & Foods

22

Providing reliable tracking and diagnostics of out of stocks is critical

We needed to provide measurement on OOS levels which was:

1. Actionable at retail

2. Simple to understand

3. Timely

4. Cost effective

Cost effective, accurate, timely, on going tracking methodology needed to monitor out of stocks

Beverages & Foods

23

New methodology utilizes both scanner data and audit data:• Actionable: Data available for 125 Retailers (3000 store audit)• Ongoing: Conducted quarterly • Timely: Results available in 2 weeks • Robust: Historic data available for benchmarking• Simple: Combines scanner (what’s available) with audit (what’s

in-stock)• Accurate: Measures both observed (tagged but unavailable) and

unobserved (item not tagged but selling in store) OOS

Prior methodologies were limited:• Scanner Based

‾ Cost prohibitive‾ Inaccurate‾ Complicated

• Custom Audit Based‾ Cost prohibitive‾ Not timely ‾ Not actionable – few retailers, sporadic timing

Success required a new OOS tracking methodology

Beverages & Foods

24

Limited shelf space despite brand and item proliferation creates tremendous pressure at shelf

Section Size-Feet

17.0 17.4

'99 '03

• Category space increased only 2% since 2001 Average Items in Chilled Case

97

125

'99 '03

Average # of Brands

26

29

'99 '03

• While # items increased 29%!

• And # of brands increased 12%

Beverages & Foods

25

Cluttered shelf results in limited space and days of supply issues for fast selling SKUs driving high OOS.

Top SKUsDays of Supply

3.1

6.3

Top SKUs AO

10.4

5.3

Share of Volume Share of Space

Top SKUsSpace allocation

•Days Of Supply for fastest selling SKUs only half that of other SKUs.

•Fastest selling SKUs only receive half their fair share of shelf.

•Nationally, OOS represent over a $100MM opportunity

Fast moving chilled case turns every 5 1/2 days

ResultingIn

High OOS

Beverages & Foods

26

OOS levels in the category are high both nationally and with individual customers.

National

• OOS rampant with 90% of stores having at least one item out of stock

Account Level Example

• At a customer level, up to ¼ off items may not be available

92%

24%30%

25%

13%

Any Item 1-2 Items 3-5 Items 6-10 Items >10 Items

8% 8% 8%10%

12%15%

22%

27%

AccountA

AccountB

AccountC

AccountD

AccountE

AccountF

AccountG

AccountH

% of Stores OOS % of Items OOS

Beverages & Foods

27

70%

30%

30%

70%

50%

50%

0%

20%

40%

60%

80%

100%

1st Time 2nd Time 3rd Time

Substitute Not BuyNo loss = 40%

Buy Same Brand, Different Flavor/Size

Manufacturer loss = 60%

Buy Different Brand, Same Flavor/Size *Wait Until Next Trip, Same StoreBuy a Different Beverage

Retailer Loss = 20%Go To A Different Store *Wait Until Next Trip, Same Store

When out of stock, both the Manufacturer and the Retailer lose.

What do you do if the item you want is Out of Stock?

Delayed Purchase *

OOS result in lost sales for both the Manufacturer and the Retailer. The more prevalent the problem, the higher the cost.

* Source: GMA “Retail Out-of-Stocks: A Worldwide Examination of Extent, Causes and Consumer Responses”

Reoccurring out of stocks increase lost sales.

Copyright © Information Resources, Inc. 2004. Confidential and proprietary.Beverages & Foods

Customer Example

Beverages & Foods

29

91.2%97.5%

Segment A Segment B

16.6

13.714.9

May '03 Nov '03 May '04

Total Account X

% StoreWith Any Item OOS

Average # Items OOS

% ofItemsOOS

15.9% 16.3% 13.4%

Current OOS Situation

Out of stocks impact more than 90% of stores and average at least 13 items.

Implication: Reducing out of stocks is an opportunity at Account X.

Beverages & Foods

30

Understanding What Drives Out of Stocks

Shelf / MarketAccount/ Dynamics

Store OperationsSupply Chain

Inventory

• Degree of Merchandising

• Pricing Strategy

• High/Low BDI Markets

• Shelving Best Practices

– How to Shelve

– Assortment Mix

– Mix of space

• Length of time for average OOS

– When should re-stocking

occur

• Re-stocking Process

– Any hindrances?

• Re-stocking Time of Day

– Is it timed with OOS?

• Logistics

• Ordering

Hypothesized Out of Stock Drivers

Results to Share Today

Additional Research Needed

Additional Research Needed

Beverages & Foods

31

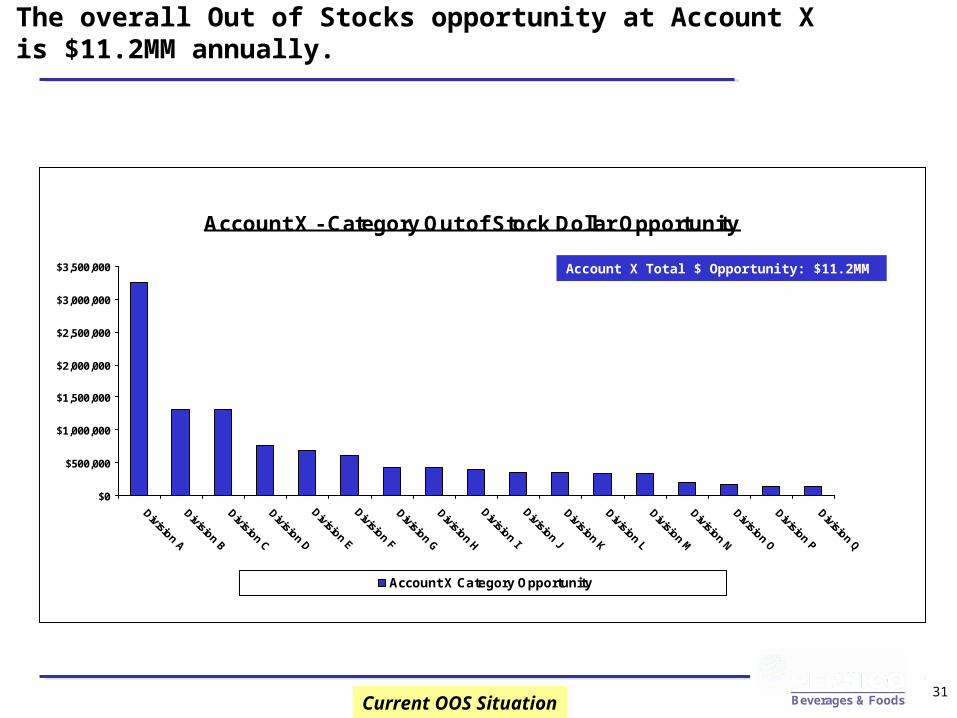

The overall Out of Stocks opportunity at Account X is $11.2MM annually.

Account X - Category Out of Stock Dollar Opportunity

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

Division A

Division B

Division C

Division D

Division E

Division F

Division G

Division H

Division I

Division J

Division K

Division L

Division M

Division N

Division O

Division P

Division Q

Account X Category Opportunity

Account X Total $ Opportunity: $11.2MM

Current OOS Situation

Beverages & Foods

32

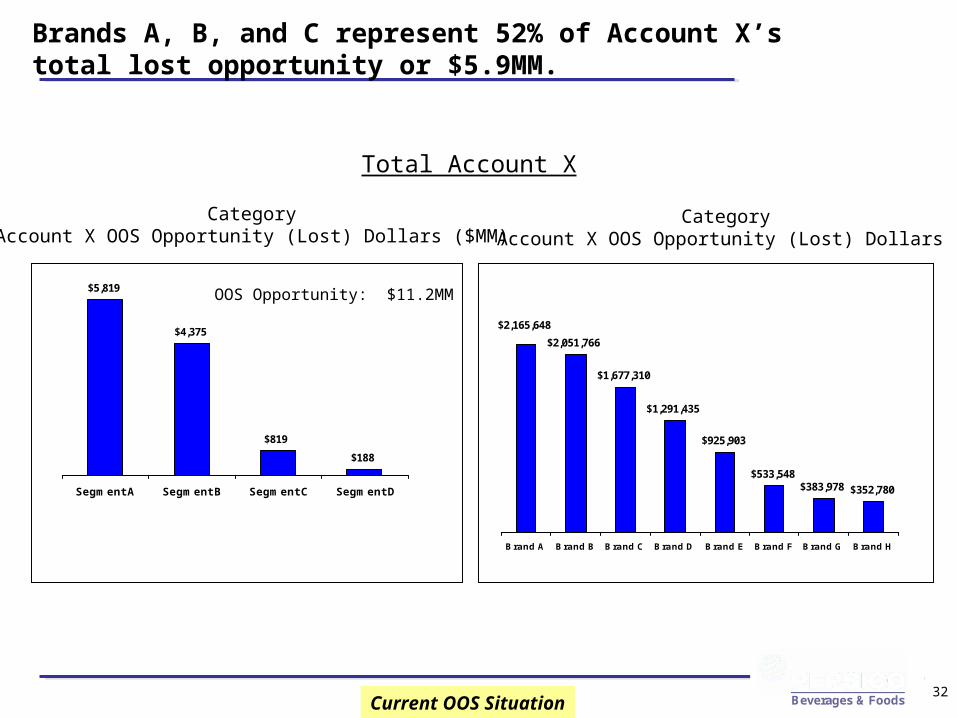

Brands A, B, and C represent 52% of Account X’s total lost opportunity or $5.9MM.

Total Account X

CategoryAccount X OOS Opportunity (Lost) Dollars ($MM)

CategoryAccount X OOS Opportunity (Lost) Dollars

$4,375

$819

$188

$5,819

Segment A Segment B Segment C Segment D

$925,903

$533,548$383,978 $352,780

$2,165,648

$1,291,435

$1,677,310

$2,051,766

Brand A Brand B Brand C Brand D Brand E Brand F Brand G Brand H

Current OOS Situation

OOS Opportunity: $11.2MM

Beverages & Foods

33

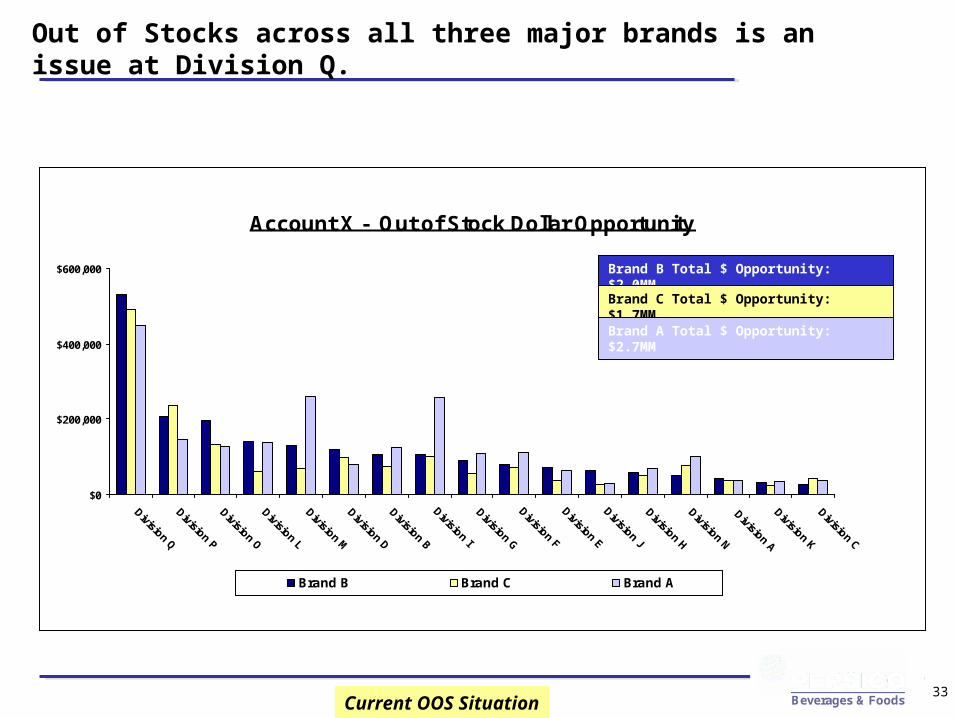

Out of Stocks across all three major brands is an issue at Division Q.

Account X - Out of Stock Dollar Opportunity

$0

$200,000

$400,000

$600,000

Division Q

Division P

Division O

Division L

Division M

Division D

Division B

Division I

Division G

Division F

Division E

Division J

Division H

Division N

Division A

Division K

Division C

Brand B Brand C Brand A

Brand B Total $ Opportunity: $2.0MM

Current OOS Situation

Brand C Total $ Opportunity: $1.7MM

Brand A Total $ Opportunity: $2.7MM

Beverages & Foods

34

The top 20 moving items represent a $2.9MM opportunity.

$0

$100,000

$200,000

$300,000

Ite

m A

Ite

m B

Ite

m C

Ite

m D

Ite

m E

Ite

m F

Ite

m G

Ite

m H

Ite

m I

Ite

m J

Ite

m K

Ite

m L

Ite

m M

Ite

m N

Ite

m O

Ite

m P

Ite

m Q

Ite

m R

Ite

m S

Ite

m T

DOS 1.3 6.6 5.3 4.9 5.4 4.9 4.1 3.3 4.9 0.1 7.5 4.0 3.6 6.2 6.5 4.7 4.6 6.0 3.7 3.5

% of Tot. Opp. 0.2 0.5 0.6 0.6 0.7 0.9 1.0 1.2 1.2 1.3 1.3 1.4 1.5 1.5 1.5 1.6 1.9 2.1 2.1 2.3

Current OOS Situation

Account X OOS Annual $ Opportunity for Top 20 Moving ItemsTop 20 Ranked on Velocity

Item Rank 20 10 1

Beverages & Foods

35

Segment A and Brand B have higher OOS rates when Brand G is in distribution.

Shelf / Market Account Dynamics

No Brand G Dist.

With Brand G Dist.

Total Account X

3.2%

8.8%

6.3%

12.7%

Brand A Item 1 %OOS Brand A Item 2 %OOS

6.6%

9.6%

Segment A % OOS

Beverages & Foods

36

Display Support - % ACV Display Segment A

14.2%

6.3%

Account X Divisions w/ LowDisplay Support (< 10%)

Account X Divisions w/ High Display Support (> 30%)

Shelf / Market Account Dynamics

Out of stock rates are lower when display support is stronger.

Implication: Offering display support can be a lever used to help reduce category out of stocks.

Segment A - % OOS

Annual OOS $ Opportunity $694M $1.1MM

Beverages & Foods

37

Day of Week Ad Breaks

Average Weekly Out of Stock Rates for Top 20 Items by Compared by Day of

Week Ad Breaks

11.5% 12.1%

7.3%9.6%

Sunday Monday Wednesday Thursday

Weekly out of stock rates are lower when feature ads break on Sunday.

Implication: Focus on reducing out of stocks in Divisions that have ad break days on Wednesday/Thursday (high traffic days) and larger OOS opportunities.

Shelf / Market Account Dynamics

Beverages & Foods

38

Out of Stock Rates for top 20 selling Items

9%10%

Higher # of Items Lower # of Items

# of Items stocked

Shelf / Market Account Dynamics

Avg. # Items 117

Out of stock rates were similar irregardless of number of items shelved in the category.

Avg. # Items 90

Implication: Just reducing the number items will not deliver lower out of stock rates. The right mix of items must be shelved.

Beverages & Foods

39

Optimizing space for the top 20 OOS items at fair share will improve volume, dollars and profitability.

Category

3.0%

4.0%

3.3%

Volume Dollars Profit

Increasing top 20 OOS items space to fair share will drive growth

Implication: Focus on getting right space for the right items