copyright oxford university press 2009 chapter 12 income taxes

Post on 19-Dec-2015

219 views

TRANSCRIPT

Copyright Oxford University Press 2009

Chapter 12Income Taxes

Copyright Oxford University Press 2009

• Individual income taxes• Corporate income taxes• Income tax rates at federal and state levels• Capital gains and losses for non-depreciated

assets• After-tax cash flows and after-tax rate of return• Spreadsheets and after-tax cash flows

Chapter Outline

Copyright Oxford University Press 2009

• Calculate taxes for both individuals and corporations

• Determine the combined income tax rates and marginal income tax rates

• Develop after-tax cash flows for a project• Evaluate investment alternatives on an after-tax

basis including asset disposal• Use spreadsheet in solving after-tax economic

analysis problems

Learning Objectives

Copyright Oxford University Press 2009

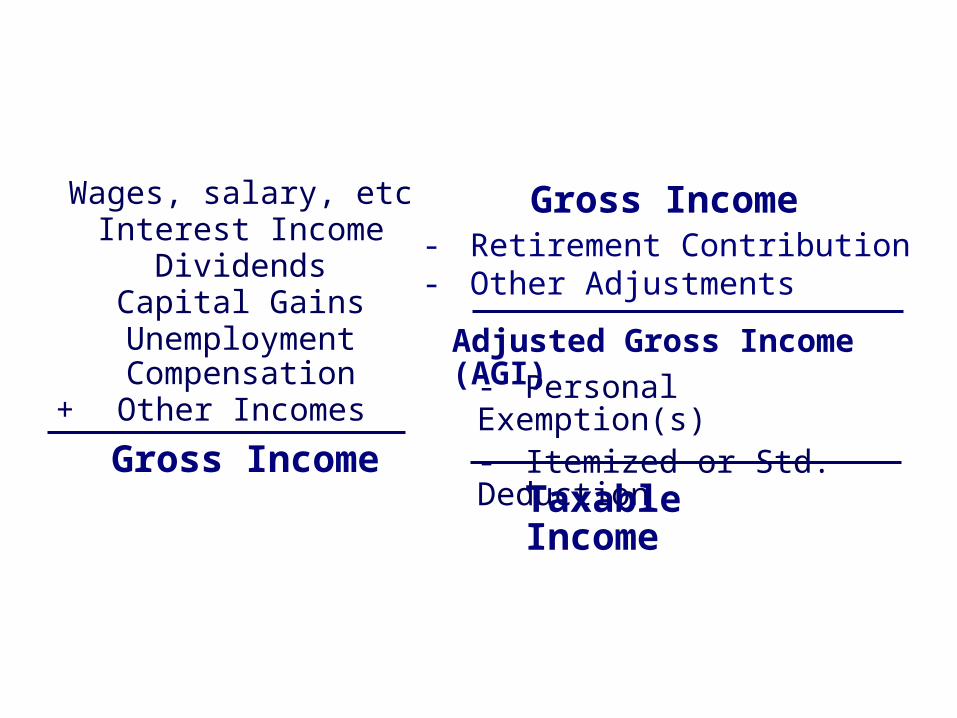

Taxable Income of Individuals

- Personal Exemption(s)- Itemized or Std. Deduction

Wages, salary, etcInterest Income

DividendsCapital Gains

Unemployment Compensation

+ Other Incomes

Gross Income

Gross Income- Retirement Contribution- Other Adjustments

Adjusted Gross Income (AGI)

Taxable Income

Copyright Oxford University Press 2009

Taxable Income of Individuals

Itemized Deduction:• Medical and dental expenses (exceeding 7.5% of AGI)• State and local income, real estate, and personal property tax• Home mortgage interest• Charitable contributions• Casualty and theft losses (exceeding $100 + 10% of AGI)• Job expenses and certain miscellaneous deductions (some

categories must exceed 2% of AGI)

Personal Exemption:• One exemption per dependent ($3400 for 2007 returns)

Standard Deduction:• Single taxpayers, $5350 for 2007 returns• Married taxpayers filing jointly, $10,700 for 2007 returns

Copyright Oxford University Press 2009

Classification ofBusiness Expenditures

Capital Expenses• Expenditures for depreciable assets:

– For facilities or productive equipment with useful life in excess of one year

– Investment recovered through depreciation• Expenditures for nondepreciable assets

– Land – Other assets not used in a trade, in a business, or for

production of income– Assets subject to depletion

Operating expensesAll ordinary and necessary expenditures, including labor,

materials, all direct and indirect costs, facilities and equipment having a life of one year or less

Copyright Oxford University Press 2009

Taxable Income of Business Firms

Gross Income- All expenditures except capital expenditures- Depreciation and depletion charges

Taxable Income(12-2)

Copyright Oxford University Press 2009

Example 12-1 Taxable Income

Year 1 Year 2 Year 3Gross income $200 $200 $200Purchase of special tooling -60 0 0All other expenditures -140 -140 -140Cash flows for the year $0 $60 $60

Actual cash flows:

Taxable Income:Year 1 Year 2 Year 3

Gross income $200 $200 $200All other expenditures -140 -140 -140Depreciation charges -20 -20 -20Cash flows for the year $40 $40 $40

Copyright Oxford University Press 2009

Maximum and Minimum Federal Income Tax Rates for Individuals

0

10

20

30

40

50

60

70

80

90

100

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Year

Ma

x.

an

d M

in T

ax

Ra

tes

(%

)

Copyright Oxford University Press 2009

2007 Federal Income Tax Ratesfor Individuals

Single Taxpayers

Taxable Income Tax

Over But Not Over Base Tax PlusOn Income

Over

$0 7,825 $0.00 10% $0

7,825 31,850 782.50 15% 7,825

31,850 77,100 4,386.50 25% 31,850

77,100 160,850 15,698.75 28% 77,100

160,850 349,700 39,148.75 33% 160,850

Over 349,700 101,469.25 35% 349,700

Copyright Oxford University Press 2009

2007 Federal Income Tax Ratesfor Individuals

Married Individuals Filing Jointly

Taxable Income Tax

Over But Not Over Base Tax PlusOn Income

Over

$0 $15,650 $0.00 10% $0

15,650 63,700 1,565.00 15% 15,650

63,700 128,500 8,772.50 25% 63,700

128,500 195,850 24,972.50 28% 128,500

195,850 349,700 43,830.50 33% 195,850

Over 349,700 94,601.00 35% 349,700

Copyright Oxford University Press 2009

Example 12-2Taxable Income of Individuals

Taxable Income = AGI - Exemption - Itemized Deduction = $16,000 – 3,400 – 5,350 = $7,250

Gross Income = Adjusted Gross Income (AGI)= $10,000+6000 = $16,000

An unmarried student earned $10,000 in the summer plus another $6000 during the rest of the year. He is allowed one exemption and he spent $1000 on allowable itemized deductions.

Tax = 10%(7,250) = $725

Copyright Oxford University Press 2009

Maximum and Minimum Federal Corporate Income Tax Rates

0

10

20

30

40

50

60

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Year

Ma

x.

an

d M

in T

ax

Ra

tes

(%

)

Copyright Oxford University Press 2009

2007 Federal Corporate Income Tax Rates

Taxable IncomeTax Rate Corporate Income Tax

Not over $50,000 15% 15% over 0

$50,000-75,000 25% 7,500 + 25% over 50,000

$75,000-100,000 34% 13,750 + 34% over 75,000

$100,000-335,000 39% 22,250 + 39% over 100,000

$335,000-10 million 34% 113,900 + 34% over 335,000

$10 million-15 million

35% 3,400,000 + 35% over 10 mil.

$15 million - 18,333,333

38% 5,150,000 + 38% over 15 mil.

over $18,333,333 35% 6,416,667 + 35% over 18,333,333

Copyright Oxford University Press 2009

Average Federal Corporate Income Tax Rates

0%

5%

10%

15%

20%

25%

30%

35%

40%

0 2 4 6 8 10 12 14 16 18 20 22

Taxable Income (Million)

Av

g.

Co

rp.

Inc

om

e T

ax

Ra

te

Copyright Oxford University Press 2009

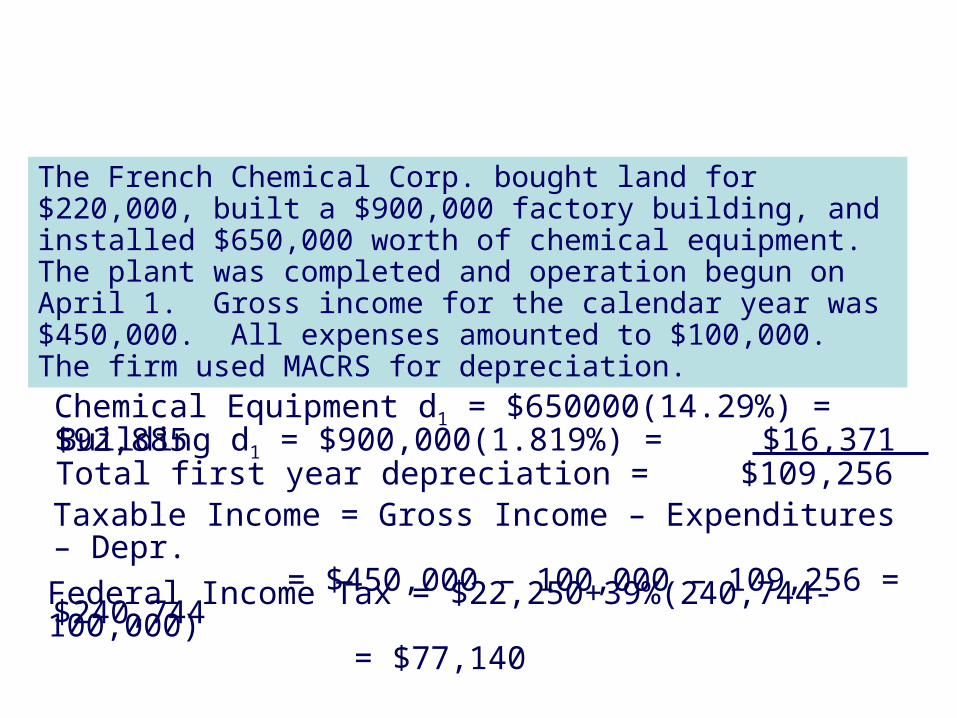

Example 12-3 Federal Corporate Income Tax

Chemical Equipment d1 = $650000(14.29%) = $92,885

Federal Income Tax = $22,250+39%(240,744-100,000) = $77,140

Taxable Income = Gross Income – Expenditures – Depr.= $450,000 – 100,000 – 109,256 = $240,744

The French Chemical Corp. bought land for $220,000, built a $900,000 factory building, and installed $650,000 worth of chemical equipment. The plant was completed and operation begun on April 1. Gross income for the calendar year was $450,000. All expenses amounted to $100,000. The firm used MACRS for depreciation.

Total first year depreciation = $109,256Building d1 = $900,000(1.819%) = $16,371

Copyright Oxford University Press 2009

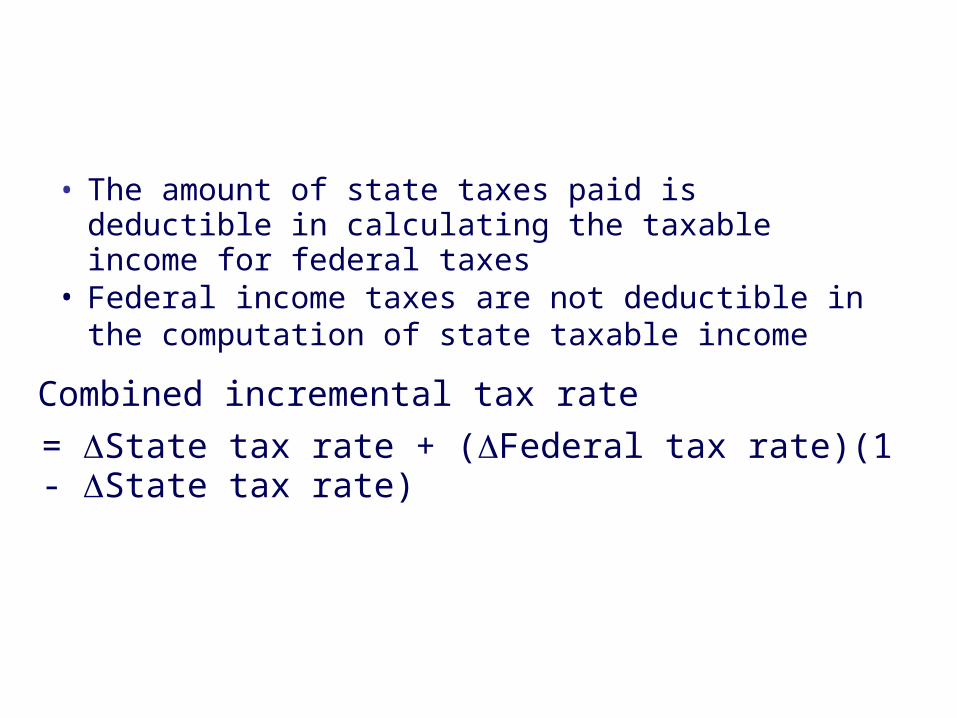

Combined Federal and State Income Taxes

• The amount of state taxes paid is deductible in calculating the taxable income for federal taxes

• Federal income taxes are not deductible in the computation of state taxable income

Combined incremental tax rate

= State tax rate + (Federal tax rate)(1 - State tax rate)

Copyright Oxford University Press 2009

Selecting an Income Tax Rate for Economy Studies

• The tax rate to use is the incremental tax rate that applies to the change in taxable income projected in the economic analysis

Copyright Oxford University Press 2009

Economic Analysis taking Income Tax into Account

• Before-tax cash flow• Depreciation• Taxable income = Before-tax cash flow

- Depreciation• Income taxes = Taxable income

x Incremental tax rate• After-tax cash flow = Before-tax cash flow

- Income taxes

Copyright Oxford University Press 2009

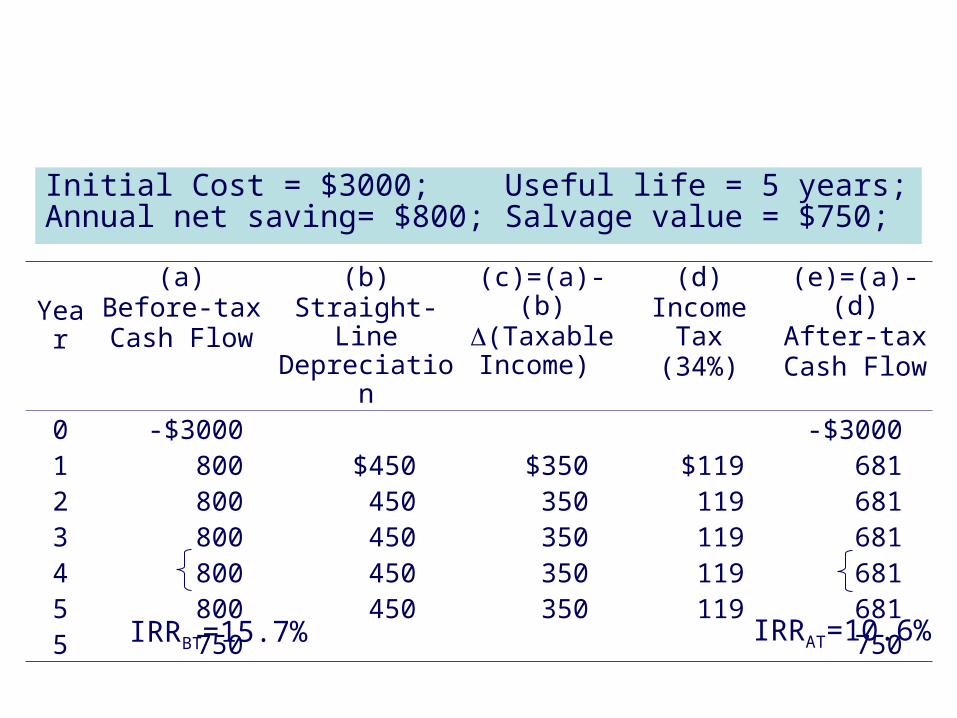

Example 12-5 Calculation of After-tax Cash Flows

Initial Cost = $3000; Useful life = 5 years; Annual net saving= $800; Salvage value = $750;

Year(a)

Before-taxCash Flow

(b)Straight-Line Depreciation

(c)=(a)-(b)(Taxable Income)

(d)Income Tax

(34%)

(e)=(a)-(d)After-tax

Cash Flow0 -$3000 -$30001 800 $450 $350 $119 6812 800 450 350 119 6813 800 450 350 119 6814 800 450 350 119 6815 800 450 350 119 6815 750 750

IRRBT=15.7% IRRAT=10.6%

Copyright Oxford University Press 2009

Example 12-6 Calculation of After-tax Cash Flows

Initial Cost (inventory) = $20000; Useful life = 4 years; Annual net saving= $1000, 1500…; Salvage value = $20000;

Year(a)

Before-taxCash Flow

(b)

Depreciation

(c)=(a)-(b)(Taxable Income)

(d)Income Tax

(39%)

(e)=(a)-(d)After-tax

Cash Flow0 -$20000 -$200001 1000 $1000 $390 6102 1500 1500 585 9153 2000 2000 780 12204 2500 2500 975 15254 20000 20000

IRRBT= 8.5% IRRAT= 5.2%

Copyright Oxford University Press 2009

Capital Gains and Losses for Non-depreciated Assets

• If the selling price of the capital asset exceeds the original cost basis, the excess is called capital gain.

• If the selling price of the capital asset is less than the original cost basis, the difference is a capital loss.

basis cost Original - price SellingLoss

GainCapital

Copyright Oxford University Press 2009

Table 12-5 Tax Treatment of Capital Gains and Losses

For IndividualsCapital Gain

• For most assets held for less than 1 year, taxed as ordinary income

• For most assets held for more than 1 year, taxed at 15% tax rateCapital Loss

• Subtract capital losses from any capital gains; balance may be deducted from ordinary income, but not more than $3000 per year

• Excess capital losses may be carried forward indefinitelyFor CorporationsCapital Gain

• Taxed as ordinary income

Capital Loss

• Deduct capital losses only to the extent of capital gains• Excess capital losses may be carried back 2 years, and, if not

completely absorbed, is then carried forward for up to 20 years