corporate finance 1: corporate financing introduction …1).pdf · introduction the financial...

TRANSCRIPT

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Corporate Finance 1: Corporate FinancingIntroduction and Stylized Facts

Robert Gary-Bobo

Ecole Polytechnique, 2015

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Introduction (1)

The main topics of Corporate Finance are:the issuance of securities by firms: equity (shares ofstock), debt (bonds, bank loans), etc... to finance newinvestment projects, extensions of old projects, etc;payout policies (dividends, share repurchases, retainedearnings);the study of corporate governance and managerialincentives (CEO pay packages, role of stock markets,bankers, venture capitalists, competition and takeovers inthe monitoring of firms).

This part of the course is mainly based on Jean Tirole’s (2006)Theory of Corporate Finance, Princeton Univ. Press, Chapter 2.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Debt and Equity

Debt in its simplest form is a claim to a predetermined levelon the firm’s income.Equity holders (shareholders) receive any profit once thedebt holders have been paid: they are residual claimants.If debt is not repaid, equity holders receive 0 and debtholders are entitled to the existing income.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Debt and Equity (2)

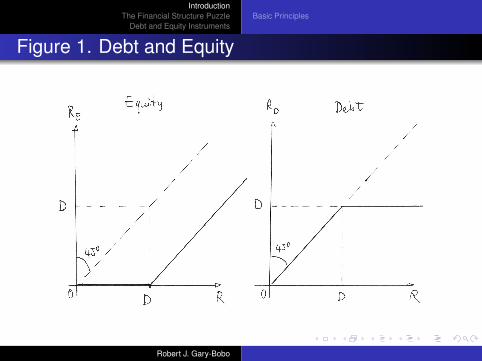

A simple (but useful) description. Let R denote a givenfirm’s income. R is random. Let D be the amount of debt.Debt and equity are claims with random yields RD and RErespectively, depicted on Figure 1.The return on debt is a convex function of R; the return onequity is a convex function of R.This is a simplistic, static description.The firm is an ongoing entity, producing a stream ofuncertain returns in the future and owns some physicalcapital (equipment, etc..)

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Figure 1. Debt and Equity'c

J7

d\tf

~

~

t7~!

cil-'"

"

~

~r

~

l

~

~

'CI

-Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Ownership and Control Rights

Who holds the claims matters. It is for instance importantto know if a firm’s equity is held by insiders (managers,entrepreneurs), or by outsiders (investors).Concentration of ownership matters too. Are theredominant shareholders? Is debt held by a large bank, ordispersed among investors?Financial claims are not simply defined by their attachedreturns. Claim holders also receive control rights: the rightto make certain decisions, specified in advance, or definedby default (residual control rights).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

A Wide Variety of Claims

Debt can be ordinary or secured (secured debt holders canseize the collateral in case of bankruptcy).Debt can be senior of junior (subordinated): there arepriorities among debt holders in case of liquidation, seniordebt holders are reimbursed first. If enough is left, juniordebt holders have a priority over equity holders.Another intermediate type is the preferred stock: holdersare entitled to a fixed repayment; nonrepayment does nottrigger default, but preferred stockholders have priority overcommon stock holders. A dividend cannot be paid tocommon stock holders unless payments due to preferredstock holders have been made.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

A Wide Variety of Claims (2)

Common stock carries voting rights; preferred stockholders usually do not have voting rights.Subordinated (junior) debt and preferred stock areinstances of mezzanine finance: they occupy amiddle-level position in the hierarchy of claims.Convertible debt is one of many claims that take the formof an option. Convertible debt can be exchanged for thefirm’s shares at some predetermined (exercise) price. It islike a bond plus a call option to buy stocks.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Some Basic Decision and Evaluation Principles

To develop a financial theory of the firm, we constantly reston a few basic principles — economic rationality principles.The first one is discounting of future payments.The second is the use of probabilities to assess uncertainsituations, viz., the Expected Utility Principle.Both principles are combined to rank investment projectsaccording to their Net Present Values (hereafter NPV).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

DiscountingSuppose that the decision-makers in a firm want to ranktwo investment projects A and A′.Suppose that project A (resp. A′) has a certain net income(net cash flow) Xt (resp. X ′t ) in period t .Then, A is preferred to project A′ if and only if it has ahigher discounted sum of net incomes, using anappropriate discount rate r∑

t≥0

Xt

(1 + r)t ≥∑t≥0

X ′t(1 + r)t .

For justifications of discounting, see basic CorporateFinance or Microeconomics textbooks.The choice of r is of course a delicate problem.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Uncertainty

Future income may be uncertain. We describe uncertaintyby means of probability distributions.Let π(x ; t) = Pr(Xt ≤ x) denote the cdf of Xt at period t .Let π′(x , t) denote the cdf of X ′t .Project A (resp. A′) is characterized by the distributionsπ(x ; t) and π′(x ; t), t ≥ 0.Then, A is preferred to project A′ if and only if, for anappropriate discount rate r ,∑

t≥0

E(Xt)

(1 + r)t ≥∑t≥0

E(X ′t )(1 + r)t .

where E(Xt) is the expected value of Xt with respect todistribution π(., t), etc...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

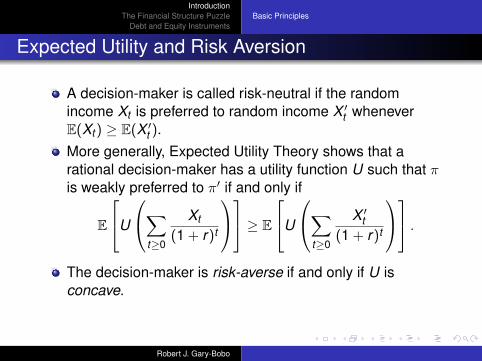

Expected Utility and Risk Aversion

A decision-maker is called risk-neutral if the randomincome Xt is preferred to random income X ′t wheneverE(Xt) ≥ E(X ′t ).More generally, Expected Utility Theory shows that arational decision-maker has a utility function U such that πis weakly preferred to π′ if and only if

E

U

∑t≥0

Xt

(1 + r)t

≥ E

U

∑t≥0

X ′t(1 + r)t

.The decision-maker is risk-averse if and only if U isconcave.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Expected Utility and Risk Aversion

A decision-maker is called risk-neutral if the randomincome Xt is preferred to random income X ′t wheneverE(Xt) ≥ E(X ′t ).More generally, Expected Utility Theory shows that arational decision-maker has a utility function U such that πis weakly preferred to π′ if and only if

E

U

∑t≥0

Xt

(1 + r)t

≥ E

U

∑t≥0

X ′t(1 + r)t

.The decision-maker is risk-averse if and only if U isconcave.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity InstrumentsBasic Principles

Expected Utility and Risk Aversion

A decision-maker is called risk-neutral if the randomincome Xt is preferred to random income X ′t wheneverE(Xt) ≥ E(X ′t ).More generally, Expected Utility Theory shows that arational decision-maker has a utility function U such that πis weakly preferred to π′ if and only if

E

U

∑t≥0

Xt

(1 + r)t

≥ E

U

∑t≥0

X ′t(1 + r)t

.The decision-maker is risk-averse if and only if U isconcave.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Financial Structure of the Firm

Insiders and outsiders of the firm care a lot about thefinancial structure, the equity/debt ratio, the allocation ofcontrol rights, etc.But is it really important? The classic Modigliani and Millerpapers from (1958) and (1961) show that, under someideal conditions, the financial structure should not matter.Finance is a veil.Under some conditions, perfect competition and completeinformation,

(1) the total value of the firm must be independent of itsfinancial structure;

(2) dividend policy doesn’t matter.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Financial Structure of the Firm

Insiders and outsiders of the firm care a lot about thefinancial structure, the equity/debt ratio, the allocation ofcontrol rights, etc.But is it really important? The classic Modigliani and Millerpapers from (1958) and (1961) show that, under someideal conditions, the financial structure should not matter.Finance is a veil.Under some conditions, perfect competition and completeinformation,

(1) the total value of the firm must be independent of itsfinancial structure;

(2) dividend policy doesn’t matter.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Financial Structure of the Firm

Insiders and outsiders of the firm care a lot about thefinancial structure, the equity/debt ratio, the allocation ofcontrol rights, etc.But is it really important? The classic Modigliani and Millerpapers from (1958) and (1961) show that, under someideal conditions, the financial structure should not matter.Finance is a veil.Under some conditions, perfect competition and completeinformation,

(1) the total value of the firm must be independent of itsfinancial structure;

(2) dividend policy doesn’t matter.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Modigliani-Miller Theorems (1)

Intuition: The value of all claims over the firm’s income(total value) is independent of the financial structure (andtherefore independent of the level of debt). Decisionsconcerning the financial structure affect only how the “pie”is shared among claim holders, not the total size of the“pie”.An increase in debt dilutes the debt holders claim andbenefits the shareholders, but the latter’s gains exactlyoffset the former’s loss.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Modigliani-Miller Theorems (2)

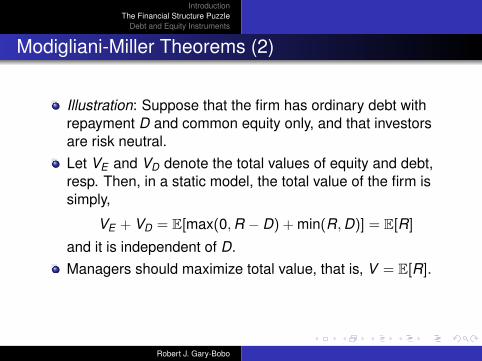

Illustration: Suppose that the firm has ordinary debt withrepayment D and common equity only, and that investorsare risk neutral.Let VE and VD denote the total values of equity and debt,resp. Then, in a static model, the total value of the firm issimply,

VE + VD = E[max(0,R − D) + min(R,D)] = E[R]

and it is independent of D.Managers should maximize total value, that is, V = E[R].

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

MM Theorems: Dividend Policy (1)

Under the Modigliani-Miller assumptions, the payout policyhas no impact on firm value.Consider a firm with no debt (all-equity firm), with discretetime t = 1,2, ... and risk-neutral investors holding shares.In each time period, the net revenue is Xt .A dividend per share dt is paid at time t . The number ofshares at time t is nt .Number of shares can be adjusted nt − nt−1 may bepositive or negative.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

MM Theorems: Dividend Policy (2)

Investment It is sunk.An investment policy is a sequence (It)t≥0; the dividendpolicy is (dt)t≥0; the repurchase/issuance policy is (nt)t≥0.The investment policy is fully observed by investors. Thedistribution of random income Xt is known (and related tothe investment policy).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

MM Theorems: Dividend Policy (2)

Investment It is sunk.An investment policy is a sequence (It)t≥0; the dividendpolicy is (dt)t≥0; the repurchase/issuance policy is (nt)t≥0.The investment policy is fully observed by investors. Thedistribution of random income Xt is known (and related tothe investment policy).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

MM Theorems: Pricing of Shares

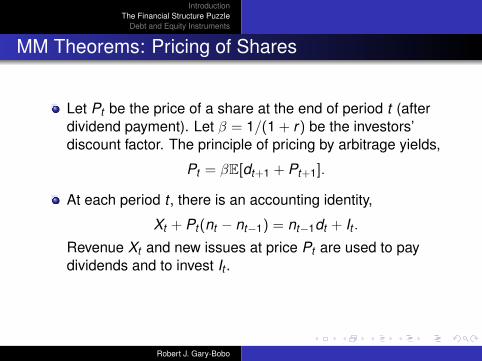

Let Pt be the price of a share at the end of period t (afterdividend payment). Let β = 1/(1 + r) be the investors’discount factor. The principle of pricing by arbitrage yields,

Pt = βE[dt+1 + Pt+1].

At each period t , there is an accounting identity,

Xt + Pt(nt − nt−1) = nt−1dt + It .

Revenue Xt and new issues at price Pt are used to paydividends and to invest It .

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

MM Theorems: Pricing of Shares

Let Pt be the price of a share at the end of period t (afterdividend payment). Let β = 1/(1 + r) be the investors’discount factor. The principle of pricing by arbitrage yields,

Pt = βE[dt+1 + Pt+1].

At each period t , there is an accounting identity,

Xt + Pt(nt − nt−1) = nt−1dt + It .

Revenue Xt and new issues at price Pt are used to paydividends and to invest It .

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Dividend Policy and Total Value of Shares

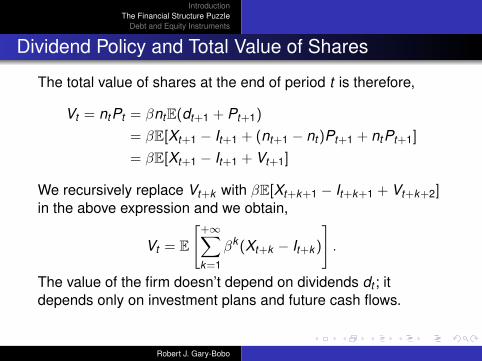

The total value of shares at the end of period t is therefore,

Vt = ntPt = βntE(dt+1 + Pt+1)

= βE[Xt+1 − It+1 + (nt+1 − nt)Pt+1 + ntPt+1]

= βE[Xt+1 − It+1 + Vt+1]

We recursively replace Vt+k with βE[Xt+k+1 − It+k+1 + Vt+k+2]in the above expression and we obtain,

Vt = E

[+∞∑k=1

βk (Xt+k − It+k )

].

The value of the firm doesn’t depend on dividends dt ; itdepends only on investment plans and future cash flows.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

The Role of Financial Structure

To understand why financial structure matters, we need toquestion a number of assumptions.The size of the pie is not fully exogenous when managerialdecisions cannot be fully specified in advance, in acomplete contract.The incentives of managers affect the firm’s income, andtherefore, the split of the pie matters.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Managerial Incentives

There is no reason why managers (insiders) have theappropriate incentives to maximize the total value of thefirm.Managers in particular may not choose the right projects(selection of projects based on private benefits, “empirebuilding”,...).Managers may waste resources (perks, corporate jets,... .Managers may not exert enough supervision of divisions orsubsidiaries; may favor friends (favoritism,..), etc.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Governance Structures

Contractual constraints imposed on managers (covenantsand other clauses in financial contracts...)High-powered managerial incentives to maximize profit(stock options,etc...). Poses many problems...Monitoring by outsiders (claim holders with large stakes inthe firm may act as monitors, and interfere if necessary).Bankruptcy laws may have an impact on financial structure.The threat of takeovers...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Governance Structures, ctd.

We focus on informational problems and on the allocationof control rights.Tax considerations also influence the financial structure (ifdebt enjoys tax advantages as compared to equity; bondsmay be issued to avoid the corporate income tax). We willnot study the role of taxation here, mainly because it iscountry- and time-specific.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Description of typical debt liability

Specify:the amount of borrowing (the principal); the rate of interest;the scheduling; other conditions (indexation, callprovisions: renegotiation rights,...).mechanism to transfer information credibly to the lenders;warranties in which the borrower confirms the accuracy ofinformation about legal status of the firm, its financialstatements, the absence of pending litigation, etc..;affirmative covenants (force the borrower to take actions);negative covenants (place restrictions on the borrower’sability to make decisions that hurt the lenders’ interest).Default and remedy conditions (specify when the lenderscan terminate the lending relationship and their rights).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Maturity, Security, Collateral

“lend against assets” (loan backed by assets) vs. “lendagainst cash flow” (loan unsecured).Collateral (guarantees): lending against assets. Protectionagainst nonpayment of interest or principal. Lenders canrepossess (seize) the assets specified as collateral in caseof default.Can be pledged: inventories, equipment, real estate(mortgage), ...Collateral typically increases the availability of credit but itis costly (transactions costs...)

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Trading and Liquidity

Distinguish public and private placements.Public bonds are issued on a primary market (mainlythrough an underwriter: an investment bank), and tradedon a secondary market (stock exchange).Private placements and bank loans are in principle nottraded after issuance (but there are forms of securitization).The chief determinant of whether a claim can be easilytraded (liquidity) is symmetry of information about thevalue of the claim (lemons problem). Cf. Akerlof (1970).Public bonds are quite liquid. In contrast, privately placeddebt is illiquid.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Maturities

Borrowing can be short or long term (it is a matter ofconvention what short or long exactly mean).Short-term credit: loan commitments and lines of credit;commercial paper (the only publicly traded short-termdebt. Commercial paper has a low default rate; maturity islower than 9 months, in general lower than one month.Long-term credit corresponds to bank loan agreementsand long-term privately or publicly placed debt.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Short-term CreditCommercial paper is a money-market security issued(sold) by large corporations to obtain funds to meetshort-term debt obligations (for example, payroll), and isbacked only by an issuing bank or corporation’s promise topay the face amount on the maturity date specified on thenote. Since it is not backed by collateral, only firms withexcellent credit ratings from a recognized credit ratingagency will be able to sell their commercial paper at areasonable price.Trade credit (borrowing from suppliers) is an importantsource of short-term financing. It is expensive (typically,the buyer must pay within 30 days, but receives a 2%discount if payment occurs within 10 days (this isequivalent to a rate of 37% per year).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Short-term CreditCommercial paper is a money-market security issued(sold) by large corporations to obtain funds to meetshort-term debt obligations (for example, payroll), and isbacked only by an issuing bank or corporation’s promise topay the face amount on the maturity date specified on thenote. Since it is not backed by collateral, only firms withexcellent credit ratings from a recognized credit ratingagency will be able to sell their commercial paper at areasonable price.Trade credit (borrowing from suppliers) is an importantsource of short-term financing. It is expensive (typically,the buyer must pay within 30 days, but receives a 2%discount if payment occurs within 10 days (this isequivalent to a rate of 37% per year).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Credit Analysis

Lenders analyze the borrower’s financial data; estimate themarket and liquidation value of assets.The “five Cs of credit” (Harvard Business School):

Character (of the managers: questionable characters maycause various problems...Costs of problem loanmanagement);

Capacity(capability of managers, competence, reputation);

Capital (capital structure with enough equity);

Collateral (guarantees alternative source of repayment incase of default);

Coverage (Business Insurance, key-man insurance).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Rating Agencies

Credit analyzes are also performed by third parties: mainlyrating agencies.Centralize credit analysis to save on costs. Issuers ofbonds typically pay fees to rating agencies for beinggraded;Are rating agencies reliable? (Problem of privatecertification). Value of reputation.Dominant rating agencies are Standard and Poor’s, FitchRatings and Moody’s (the “big three").Standard and Poor’s grades: AAA, AA, A, BBB, BB, B,CCC, CC, C and D (default).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Debt Covenants

Covenants can be found in bank loan agreements, in bondissues, in privately placed debt agreements.Positive covenants stipulate actions that the borrower musttake (for instance, the obligation of maintaining assets ingood working order).Negative covenants prohibit some actions.Managers (real authority) and shareholders (formalauthority) are in control of the firm as long as covenantsare not violated.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Debt Covenants (2)

Covenants limit decisions that may increase the risk of nonpayment, or reduce the value of the firm, or actions thatreduce the value of debt and increase the value of equity.Definition of circumstances under which different classesof claim holders (equity- or debt-holders) receive the rightto intervene in management. The transfer of control to debtholders is typically triggered by the non-payment ofinterest.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Covenants (3): Conflict View

Managers and Shareholders may make decisions thatsacrifice the total value of the firm because of personalpreferences (private benefits).Covenant put restrictions on payment to shareholders(cash dividends, share repurchase, loss-makingtransactions through generous transfer prices). Excessivepayments may leave debt-holders with an “empty shell”.Limits on further indebtedness. The issuance of new debtdilutes the value of existing debt. Dilution is strong if thenew debt is secured or senior. Covenants thus putrestrictions on actions that may create senior debts.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Asset Substitution

Actions increasing risk. Shareholders benefit fromincreased risk (because of limited liability, they have aconvex utility and become risk lovers).Debt holders have a concave utility: they are risk averse.Note: Convertibility of debt (into equity) is a protectionagainst excessive risk-taking.Covenants are meant to protect debt-holders againstincreases in risk (examples: prohibit investment in newlines of business, earmarking the loan for specificpurposes, require life insurance for key personnel,...)

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Covenants (4): the Control View

Some covenants are made to shift control to debt holdersin case of bad performance.For example total debt cannot exceed a fraction of totalassets, or the firm’s net worth (i.e., book value of assetsminus value of liabilities) must exceed some minimum.Some covenants require a minimal amount of liquidity(firm’s working capital must be large enough) to make surethat the firm will be able to face its short-term obligations.Liquidity problems and solvency problems (a liquidityproblem may be a signal of a solvency problem).The debt holders exert control mainly by threatening not torefinance or to apply the default and remedy conditions(the possibility for a bank to accelerate the collection of itsloan) when a covenant is violated.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Covenants (5): the Control View

The shift-of-control mechanism is limited by the availabilityof information (are lenders sufficiently well informed aboutpossible violations of covenants?).There are informational covenants. For instance,covenants specifying rights of inspection of facilities andbooks by the lender. In case of bank loan, the requirementthat the firm’s principal checking accounts be maintainedwith the bank.Another problem comes from the possibility of accountingmanipulations (use of creative accounting).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Covenants (5): the Control View

The shift-of-control mechanism is limited by the availabilityof information (are lenders sufficiently well informed aboutpossible violations of covenants?).There are informational covenants. For instance,covenants specifying rights of inspection of facilities andbooks by the lender. In case of bank loan, the requirementthat the firm’s principal checking accounts be maintainedwith the bank.Another problem comes from the possibility of accountingmanipulations (use of creative accounting).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Creative Accounting

Borrower and lender agree on an accounting method(example: use standards of Generally AcceptedAccounting Practices or GAAP). For example a covenantmay prohibit the sale of more than a specified fraction ofthe assets or else require that the proceeds be used torepay the debt.Problem of off-balance-sheet liabilities: for instance leasing(long term rental) arrangements, asset sales with arepurchase agreement, various options).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

BankruptcyIn case of default, creditors may force bankruptcy (cf.Bankruptcy laws: in the US, the rules of chapter 11). Theimportant point: priority rules during liquidation. In the UnitedStates, priority order is as follows:

1. Administrative expenses of the bankruptcy process.2. Government; unpaid taxes or debts to social security(pension benefits)3. Workers’ wage claims (up to some ceiling)4. Secured and senior creditors5. Junior creditors6. Preferred shares (priority over common stock)7. Ordinary shareholders.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Equity Instruments: Summary

First we describe Venture Capital.Second, Initial Public Offerings (IPOs), seasoned Publicofferings.Financing Patterns.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Privately Held Equity (the Case of Startups)

Companies may need to sell their equity to some large,sophisticated investor.An important type of investors in privately held companies:venture capitalists.Venture capitalists provide finance for young, high-riskfirms.See also LBOs.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Venture Capital

Venture capital is used to finance start-up companies inhigh-tech industries. Venture capitalists take concentratedequity positions in the company they finance and seats inthe board of directors.For instance: Apple, Intel, Microsoft, Google, etc. startedwith venture capital.Many projects fail but some make spectacular profits.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Venture Capital: Drastic Conditions

Screening of firms is intense (many projects rejected).A very detailed outline of the various stages of financing.At each stage the firm is given just enough cash to reachthe next stage.The venture capitalist has the right to unilaterally stopfunding at any stage.The venture capitalist has the right to fire managers ifsome objective is not met; imposes non-compete clauseson key employees.Venture capitalists have preemptive rights to participate innew financing. They often hold preferred stock (senior tothe manager’s claim in liquidation)

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Venture Capital: Drastic Conditions (2)Some covenants: obligation to purchase life insurance forkey employees.Exit Mechanism: at some stage, the company will go public(shares will be sold on the stock market). The venturecapitalist will sell part or all of his(her) shares.Venture capitalists’ rights are often contingent on verifiablemeasures of financial and nonfinancial performance(financial performance: EBIT, earnings before interest andtaxes). Nonfinancial performance includes: patents, orapproval by administration (for a new drug), or the founderremaining in the firm,...Following good performance, the entrepreneur obtainsmore control rights. Contingent allocation of the rights ofcontrol is key.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Venture Capital: Drastic Conditions (3)

Debt is not a good solution to finance start-ups.Ideas are not good collateral (debt could not easily besecured).Many new high tech firms do not generate enough cashflows for quite a while (a short term debt obligation wouldlead to bankruptcy).So, equity financing is the solution. But venture capitalcombines features of equity and debt.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Initial Public Offerings (IPOs)

Four stages of equity financing:

1. Equity is held by one or several entrepreneurs.

2. The entrepreneurs raise equity capital from a small numberof investors (private placement), or have a privilegedrelationship with a bank.

3. The firm goes public in an initial public offering (but mostfirms do not arrive at this point).

4. The firm may conduct secondary seasoned public offerings(SPOs) to raise capital.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Going Public Decision

Going public is costly: supply detailed information toregulators and investors; pay substantial underwriting andlegal fees (in the US, commissions paid to investmentbankers are around 7% of the transaction).A fixed number of shares is issued at some pre-specifiedprice.Shares are rationed if there is excess demand at the offerprice.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Going Public Decision

Going public is costly: supply detailed information toregulators and investors; pay substantial underwriting andlegal fees (in the US, commissions paid to investmentbankers are around 7% of the transaction).A fixed number of shares is issued at some pre-specifiedprice.Shares are rationed if there is excess demand at the offerprice.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Going Public Decision

Going public is costly: supply detailed information toregulators and investors; pay substantial underwriting andlegal fees (in the US, commissions paid to investmentbankers are around 7% of the transaction).A fixed number of shares is issued at some pre-specifiedprice.Shares are rationed if there is excess demand at the offerprice.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Underpricing

It is well-known that IPOs with a preset price areunderpriced. Shares are traded on the secondary marketshortly after the IPO at a premium of 15-20% on averagerelative to the preset price.Standard explanation: the “winner’s curse” (cf. Auctiontheory). Informational problem. Insiders have superiorinformation.Family firms still dominate the landscape (control has avalue).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Underpricing

It is well-known that IPOs with a preset price areunderpriced. Shares are traded on the secondary marketshortly after the IPO at a premium of 15-20% on averagerelative to the preset price.Standard explanation: the “winner’s curse” (cf. Auctiontheory). Informational problem. Insiders have superiorinformation.Family firms still dominate the landscape (control has avalue).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Underpricing

It is well-known that IPOs with a preset price areunderpriced. Shares are traded on the secondary marketshortly after the IPO at a premium of 15-20% on averagerelative to the preset price.Standard explanation: the “winner’s curse” (cf. Auctiontheory). Informational problem. Insiders have superiorinformation.Family firms still dominate the landscape (control has avalue).

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Benefits of Going Public

Going public enables the firm to use new sources offinance (enables firm growth).The firm relies less on a single bank.Going public facilitates exit; it allows entrepreneur todiversify their portfolios.The market value of shares is a more objective measure ofthe firm’s assets.Going public may help to discipline managers (threat oftakeovers). But a more dispersed ownership can alsoreduce the intensity of monitoring.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Benefits of Going Public

Going public enables the firm to use new sources offinance (enables firm growth).The firm relies less on a single bank.Going public facilitates exit; it allows entrepreneur todiversify their portfolios.The market value of shares is a more objective measure ofthe firm’s assets.Going public may help to discipline managers (threat oftakeovers). But a more dispersed ownership can alsoreduce the intensity of monitoring.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Benefits of Going Public

Going public enables the firm to use new sources offinance (enables firm growth).The firm relies less on a single bank.Going public facilitates exit; it allows entrepreneur todiversify their portfolios.The market value of shares is a more objective measure ofthe firm’s assets.Going public may help to discipline managers (threat oftakeovers). But a more dispersed ownership can alsoreduce the intensity of monitoring.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Benefits of Going Public

Going public enables the firm to use new sources offinance (enables firm growth).The firm relies less on a single bank.Going public facilitates exit; it allows entrepreneur todiversify their portfolios.The market value of shares is a more objective measure ofthe firm’s assets.Going public may help to discipline managers (threat oftakeovers). But a more dispersed ownership can alsoreduce the intensity of monitoring.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Retentions and Returns to the Capital Market

Retentions (retained earnings) are the difference betweenpost-tax income and total payments to investors (includingpayouts to shareholders and payments to creditors,principal and interest).Payouts: Dividends and share repurchases.Returns to the capital market: issuing of new shares andbonds; and new loans.The firm is exposed to the risk of being unable to findfunding for projects that have a positive net present value(NPV), because lenders may be reluctant...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Retentions and Returns to the Capital Market

Retentions (retained earnings) are the difference betweenpost-tax income and total payments to investors (includingpayouts to shareholders and payments to creditors,principal and interest).Payouts: Dividends and share repurchases.Returns to the capital market: issuing of new shares andbonds; and new loans.The firm is exposed to the risk of being unable to findfunding for projects that have a positive net present value(NPV), because lenders may be reluctant...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Retentions and Returns to the Capital Market

Retentions (retained earnings) are the difference betweenpost-tax income and total payments to investors (includingpayouts to shareholders and payments to creditors,principal and interest).Payouts: Dividends and share repurchases.Returns to the capital market: issuing of new shares andbonds; and new loans.The firm is exposed to the risk of being unable to findfunding for projects that have a positive net present value(NPV), because lenders may be reluctant...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Retentions and Returns to the Capital Market

Retentions (retained earnings) are the difference betweenpost-tax income and total payments to investors (includingpayouts to shareholders and payments to creditors,principal and interest).Payouts: Dividends and share repurchases.Returns to the capital market: issuing of new shares andbonds; and new loans.The firm is exposed to the risk of being unable to findfunding for projects that have a positive net present value(NPV), because lenders may be reluctant...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Sources of Corporate Finance

In all countries, internal financing (retained earnings)constitutes the main source of finance.Bank loans provide the bulk of external financing.New equity issues are only a small fraction of newfinancing.The role of bond financing differs across countries: bondmarkets are more important in the US than in Europe.In France in the seventies-eighties: Retentions 44%; Loans42%; Bonds 2%; and Shares 10%...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Sources of Corporate Finance

In all countries, internal financing (retained earnings)constitutes the main source of finance.Bank loans provide the bulk of external financing.New equity issues are only a small fraction of newfinancing.The role of bond financing differs across countries: bondmarkets are more important in the US than in Europe.In France in the seventies-eighties: Retentions 44%; Loans42%; Bonds 2%; and Shares 10%...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Sources of Corporate Finance

In all countries, internal financing (retained earnings)constitutes the main source of finance.Bank loans provide the bulk of external financing.New equity issues are only a small fraction of newfinancing.The role of bond financing differs across countries: bondmarkets are more important in the US than in Europe.In France in the seventies-eighties: Retentions 44%; Loans42%; Bonds 2%; and Shares 10%...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Sources of Corporate Finance

In all countries, internal financing (retained earnings)constitutes the main source of finance.Bank loans provide the bulk of external financing.New equity issues are only a small fraction of newfinancing.The role of bond financing differs across countries: bondmarkets are more important in the US than in Europe.In France in the seventies-eighties: Retentions 44%; Loans42%; Bonds 2%; and Shares 10%...

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Payout Policy and Leverage

There is much evidence that growth opportunities arecorrelated with a lower dividend distribution.Key findings about empirical determinants of leverage(debt).1. Firms that are safe, produce steady cash flows andassets that can be pledged as collateral (for instance:airplanes in airline companies);2. Risky firms with little current cash flow and firms withintangible assets (substantial R&D and advertising) tend tohave low leverage.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Payout Policy and Leverage

There is much evidence that growth opportunities arecorrelated with a lower dividend distribution.Key findings about empirical determinants of leverage(debt).1. Firms that are safe, produce steady cash flows andassets that can be pledged as collateral (for instance:airplanes in airline companies);2. Risky firms with little current cash flow and firms withintangible assets (substantial R&D and advertising) tend tohave low leverage.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Seasoned Financing

SPOs have an informational impact (fall in stock price ofabout 3% in the wake of an announcement of a seasonedequity issue).But the stock price rises when a bank loan agreement isannounced.Stock price increases with an announcement of higherdividends.

Robert J. Gary-Bobo

IntroductionThe Financial Structure Puzzle

Debt and Equity Instruments

Debt InstrumentsEquity InstrumentsFinancing Patterns

Link between Financing and the Business Cycle

Bank finance is counter-cyclical. The percentage ofunsecured bank loans varies inversely with businessconditions.Small and medium-sized firms who rely more on banks aremore affected than larger firms by business cycles.Equity issues are more frequent in booms.Equity issues are more frequent after an increase in thefirm’s own stock value. Firms repurchase their shareswhen prices are low.

Robert J. Gary-Bobo