corporate fi nance - university of london iii chapter 6: the choice of corporate capital structure...

TRANSCRIPT

Undergraduate study in Economics, Management, Finance and the Social Sciences

Corporate fi nanceP. Frantz, R. Payne, J. Favilukis FN3092, 2790092

2011

This is an extract from a subject guide for an undergraduate course offered as part of the University of London International Programmes in Economics, Management, Finance and the Social Sciences. Materials for these programmes are developed by academics at the London School of Economics and Political Science (LSE).

For more information, see: www.londoninternational.ac.uk

This guide was prepared for the University of London International Programmes by:

Dr. P. Frantz, Lecturer in Accountancy and Finance, The London School of Economics andPolitical Science

R. Payne, Former Lecturer in Finance, The London School of Economics and Political Science

Dr. J. Favilukis, Lecturer, The London School of Economics and Political Science

This is one of a series of subject guides published by the University. We regret that due to pressure of work the authors are unable to enter into any correspondence relating to, or aris-ing from, the guide. If you have any comments on this subject guide, favourable or unfavour-able, please use the form at the back of this guide.

University of London International Programmes

Publication Office

Stewart House

32 Russell Square

London WC1B 5DN

United Kingdom

Website: www.londoninternational.ac.uk

Published by: University of London

© University of London 2011

The University of London asserts copyright over all material in this subject guide except where otherwise indicated. All rights reserved. No part of this work may be reproduced in any form, or by any means, without permission in writing from the publisher.

We make every effort to contact copyright holders. If you think we have inadvertently used your copyright material, please let us know.

Contents

i

Contents

Introduction to the subject guide .......................................................................... 1

Aims of the course ......................................................................................................... 1Learning outcomes ........................................................................................................ 1Syllabus ......................................................................................................................... 2Essential reading ........................................................................................................... 3Further reading .............................................................................................................. 3Online study resources ................................................................................................... 5Subject guide structure and use ..................................................................................... 6Examination advice........................................................................................................ 7Glossary of abbreviations used in this subject guide ....................................................... 8

Chapter 1: Present value calculations and the valuation of physical investment projects ................................................................................................................... 9

Aim .............................................................................................................................. 9Learning outcomes ........................................................................................................ 9Essential reading ........................................................................................................... 9Further reading .............................................................................................................. 9Overview ..................................................................................................................... 10Introduction ................................................................................................................ 10Fisher separation and optimal decision-making ............................................................ 10Fisher separation and project evaluation ...................................................................... 13The time value of money .............................................................................................. 14The net present value rule ............................................................................................ 15Other project appraisal techniques ............................................................................... 17Using present value techniques to value stocks and bonds ........................................... 21A reminder of your learning outcomes .......................................................................... 23Key terms .................................................................................................................... 23Sample examination questions ..................................................................................... 23

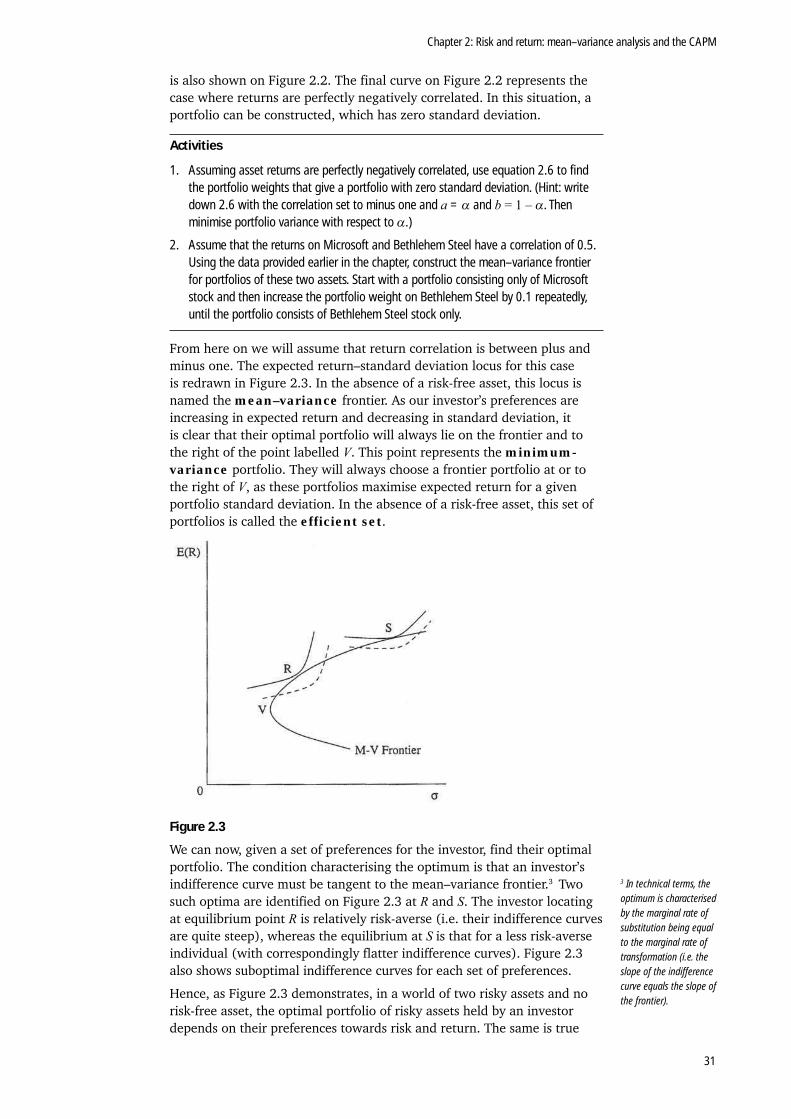

Chapter 2: Risk and return: mean–variance analysis and the CAPM.................... 25

Aim of the chapter ....................................................................................................... 25Learning outcomes ...................................................................................................... 25Essential reading ......................................................................................................... 25Further reading ............................................................................................................ 25Introduction ................................................................................................................ 25Statistical characteristics of portfolios ........................................................................... 26Diversification .............................................................................................................. 28Mean–variance analysis ............................................................................................... 30The capital asset pricing model .................................................................................... 34The Roll critique and empirical tests of the CAPM ......................................................... 37A reminder of your learning outcomes .......................................................................... 40Key terms .................................................................................................................... 40Sample examination questions ..................................................................................... 40Solutions to activities ................................................................................................... 41

Chapter 3: Factor models ..................................................................................... 43

Aim of the chapter ....................................................................................................... 43Learning outcomes ...................................................................................................... 43

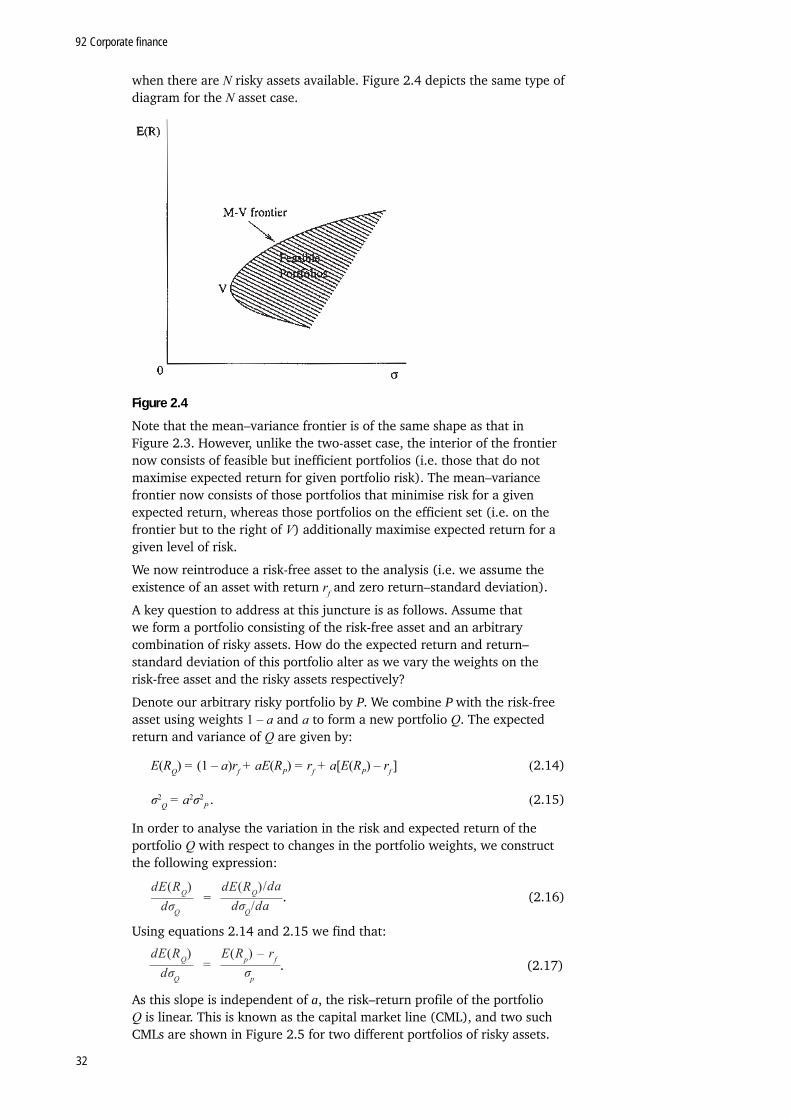

92 Corporate finance

ii

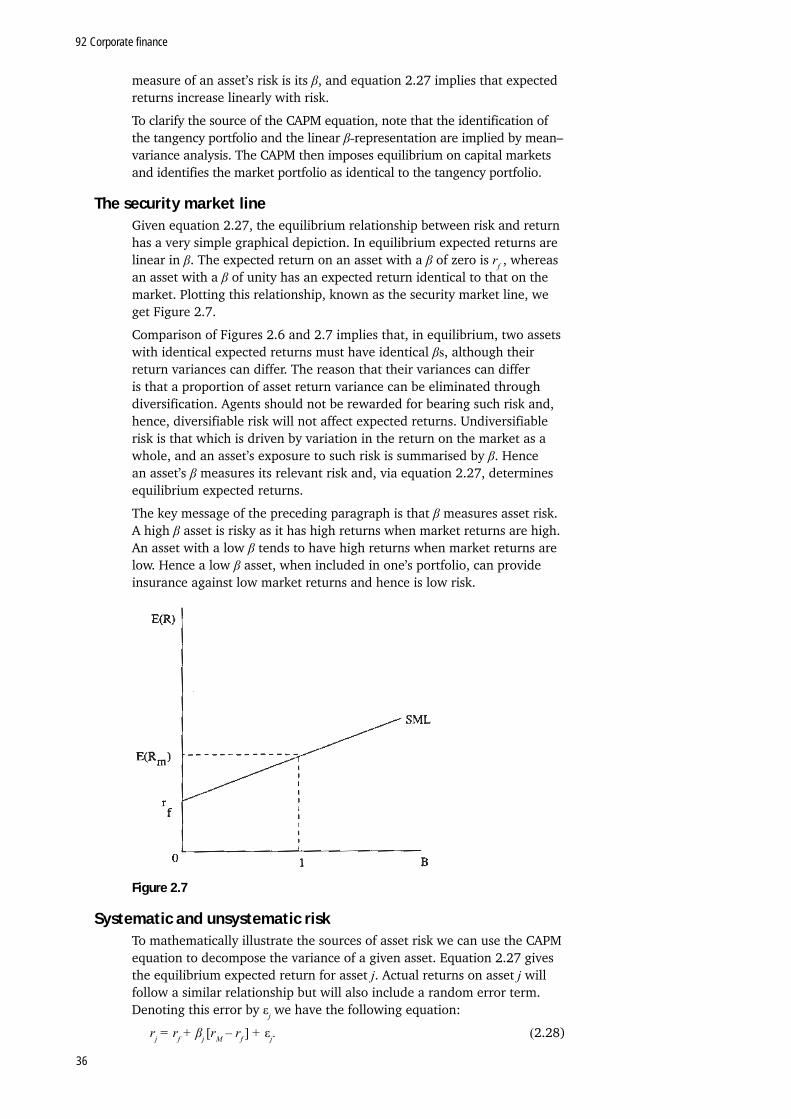

Essential reading ......................................................................................................... 43Further reading ............................................................................................................ 43Overview ..................................................................................................................... 43Introduction ................................................................................................................ 44Single-factor models .................................................................................................... 44Multi-factor models ..................................................................................................... 46Broad-based portfolios and idiosyncratic returns........................................................... 47Factor-replicating portfolios ......................................................................................... 48The arbitrage pricing theory ......................................................................................... 50Multi-factor models in practice ..................................................................................... 51Summary ..................................................................................................................... 52A reminder of your learning outcomes .......................................................................... 52Key terms .................................................................................................................... 53Sample examination question ...................................................................................... 53

Chapter 4: Derivative securities: properties and pricing ..................................... 55

Aim of the chapter ....................................................................................................... 55Learning outcomes ...................................................................................................... 55Essential reading ......................................................................................................... 55Further reading ............................................................................................................ 55Overview ..................................................................................................................... 55Varieties of derivatives ................................................................................................. 56Derivative asset payoff profiles ..................................................................................... 57Pricing forward contracts ............................................................................................. 59Binomial option pricing setting .................................................................................... 60Bounds on option prices and exercise strategies ........................................................... 64Black–Scholes option pricing ....................................................................................... 66Put–call parity ............................................................................................................. 68Pricing interest rate swaps ........................................................................................... 69Summary ..................................................................................................................... 69A reminder of your learning outcomes .......................................................................... 70Key terms .................................................................................................................... 70Sample examination questions ..................................................................................... 71

Chapter 5: Efficient markets: theory and empirical evidence .............................. 73

Aim of the chapter ....................................................................................................... 73Learning outcomes ...................................................................................................... 73Essential reading ......................................................................................................... 73Further reading ............................................................................................................ 73Overview ..................................................................................................................... 74Varieties of efficiency ................................................................................................... 74Risk adjustments and the joint hypothesis problem ...................................................... 75Weak-form efficiency: implications and tests ................................................................ 76Weak-form efficiency: empirical results ......................................................................... 78Semi-strong-form efficiency: event studies .................................................................... 81Semi-strong-form efficiency: empirical evidence ............................................................ 83Strong-form efficiency .................................................................................................. 83Long horizon forecastability ......................................................................................... 83Summary ..................................................................................................................... 85A reminder of your learning outcomes .......................................................................... 85Key terms .................................................................................................................... 85Sample examination questions ..................................................................................... 86

Contents

iii

Chapter 6: The choice of corporate capital structure ........................................... 89

Aim of the chapter ....................................................................................................... 89Learning outcomes ...................................................................................................... 89Essential reading ......................................................................................................... 89Further reading ............................................................................................................ 89Overview ..................................................................................................................... 89Basic features of debt and equity ................................................................................. 90The Modigliani–Miller theorem .................................................................................... 91Modigliani–Miller and Black–Scholes ........................................................................... 93Modigliani–Miller and corporate taxation ..................................................................... 94Modigliani–Miller with corporate and personal taxation ............................................... 97Summary ..................................................................................................................... 98A reminder of your learning outcomes .......................................................................... 99Key terms .................................................................................................................... 99Sample examination questions ..................................................................................... 99

Chapter 7: Leverage, WACC and the Modigliani-Miller 2nd proposition ........... 101

Aim of the chapter ..................................................................................................... 101Learning outcomes .................................................................................................... 101Essential reading ....................................................................................................... 101Further reading .......................................................................................................... 101Overview ................................................................................................................... 101Weighted average cost of capital ............................................................................... 102Modigliani and Miller’s 2nd proposition ..................................................................... 103A CAPM perspective .................................................................................................. 107Summary ................................................................................................................... 108Key terms .................................................................................................................. 108A reminder of your learning outcomes ........................................................................ 108Sample examination questions ................................................................................... 109

Chapter 8: Asymmetric information, agency costs and capital structure .......... 111

Aim of the chapter ..................................................................................................... 111Learning outcomes .................................................................................................... 111Essential reading ....................................................................................................... 111Further reading .......................................................................................................... 111Overview ................................................................................................................... 112Capital structure, governance problems and agency costs ........................................... 112Agency costs of outside equity and debt .................................................................... 112Agency costs of free cash flows .................................................................................. 118Firm value and asymmetric information ...................................................................... 119Summary ................................................................................................................... 123Key terms .................................................................................................................. 123A reminder of your learning outcomes ........................................................................ 124Sample examination questions ................................................................................... 124

Chapter 9: Dividend policy ................................................................................. 127

Aim of the chapter ..................................................................................................... 127Learning outcomes .................................................................................................... 127Essential reading ....................................................................................................... 127Further reading .......................................................................................................... 127Overview ................................................................................................................... 128Modigliani–Miller meets dividends ............................................................................. 128Prices, dividends and share repurchases ..................................................................... 129

92 Corporate finance

iv

Dividend policy: stylised facts ..................................................................................... 129Taxation and clientele theory ..................................................................................... 131Asymmetric information and dividends ....................................................................... 132Agency costs and dividends ....................................................................................... 133Summary ................................................................................................................... 133A reminder of your learning outcomes ........................................................................ 134Key terms .................................................................................................................. 134Sample examination questions ................................................................................... 134

Chapter 10: Mergers and takeovers ................................................................... 135

Aim of the chapter ..................................................................................................... 135Learning outcomes .................................................................................................... 135Essential reading ....................................................................................................... 135Further reading .......................................................................................................... 135Overview ................................................................................................................... 136Merger motivations ................................................................................................... 136A numerical takeover example ................................................................................... 137The market for corporate control ................................................................................ 138The impossibility of efficient takeovers ....................................................................... 139Two ways to get efficient takeovers ............................................................................ 140Empirical evidence ..................................................................................................... 141Summary ................................................................................................................... 143A reminder of your learning outcomes ........................................................................ 143Key terms .................................................................................................................. 143Sample examination questions ................................................................................... 144

Appendix 1: Perpetuities and annuities ............................................................. 145

Perpetuities ............................................................................................................... 145Annuities .................................................................................................................. 146

Appendix 2: Sample examination paper ............................................................ 147

Introduction to the subject guide

1

Introduction to the subject guide

This subject guide for 92 Corporate finance, a ‘300’ course offered on the Economics, Management, Finance and Social Sciences programme, provides you with an introduction to the modern theory of finance. As such, it covers a broad range of topics and aims to give a general background to any student who wishes to do further academic or practical work in finance or accounting after graduation.

The subject matter of the guide can be broken into two main areas.

• The first section covers the valuation and pricing of real and financial assets. This provides you with the methodologies you will need to fairly assess the desirability of investment in physical capital, and price spot and derivative assets. We employ a number of tools in this analysis. The coverage of the risk-return trade-off in financial assets and mean–variance optimisation will require you to apply some basic statistical theory alongside the standard optimisation techniques taught in basic economics courses. Another important part of this section will be the use of absence-of-arbitrage techniques to price financial assets.

• In the second section, we will examine issues that come under the broad heading of corporate finance. Here we will examine the key decisions made by firms, how they affect firm value and empirical evidence on these issues. The areas involved include the capital structure decision, dividend policy, and mergers and acquisitions. By studying these areas, you should gain an appreciation of optimal financial policy on a firm level, conditions under which an optimal policy actually exists and how the actual financial decisions of firms may be explained in theoretical terms.

Aims of the courseThis course is aimed at students interested in understanding asset pricing and corporate finance. It provides a theoretical framework used to address issues in project appraisal and financing, the pricing of risk, securities valuation, market efficiency, capital structure and mergers and acquisitions. It provides students with the tools required for further studies in financial intermediation and investments.

Learning outcomesAt the end of this course, and having completed the Essential reading and activities, you should be able to:

• explain how to value projects, and use the key capital budgeting techniques (NPV and IRR)

• understand the mathematics of portfolios and how risk affects the value of the asset in equilibrium under the fundaments asset pricing paradigms (CAPM and APT)

• know how to use recent extensions of the CAPM, such as the Fama and French three-factor model, to calculate expected returns on risky securities

92 Corporate finance

2

• explain the characteristics of derivative assets (forwards, futures and options), and how to use the main pricing techniques (binomial methods in derivatives pricing and the Black–Scholes analysis)

• discuss the theoretical framework of informational efficiency in financial markets and evaluate the related empirical evidence

• understand the trade-off firms face between tax advantages of debt and various costs of debt

• understand and explain the capital structure theory, and how information asymmetries affect it

• understand and explain the relevance, facts and role of the dividend policy

• understand how corporate governance can contribute to firm value

• discuss why merger and acquisition activities exist, and calculate the related gains and losses.

SyllabusNote: A minor revision was made to this syllabus in 2009.

Students may bring into the examination hall their own hand-held electronic calculator. If calculators are used they must satisfy the requirements listed in the Regulations.

If you are taking this course as part of a BSc degree, courses which must be passed before this course may be attempted are 2 Introduction to economics and 5A Mathematics 1 or 5B Mathematics 2 or 174 Calculus.

Project evaluation: Hirschleifer analysis and Fisher separation; the NPV rule and IRR rules of investment appraisal; comparison of NPV and IRR; ‘wrong’ investment appraisal rules: payback and accounting rate of return.

Risk and return – the CAPM and APT: the mathematics of portfolios; mean-variance analysis; two-fund separation and the CAPM; Roll’s critique of the CAPM; factor models; the arbitrage pricing theory; recent extensions of the factor framework.

Derivative assets – characteristics and pricing: definitions: forwards and futures; replication, arbitrage and pricing; a general approach to derivative pricing using binomial methods; options: characteristics and types; bounding and linking option prices; the Black–Scholes analysis.

Efficient markets – theory and empirical evidence: underpinning and definitions of market efficiency; weak-form tests: return predictability; the joint hypothesis problem; semi-strong form tests: the event study methodology and examples; strong form tests: tests for private information; long-horizon return predictability.

Capital structure: the Modigliani–Miller theorem: capital structure irrelevancy; taxation, bankruptcy costs and capital structure; weighted average cost of capital; Modigliani-Miller 2nd proposition; the Miller equilibrium; asymmetric information: 1) the under-investment problem, asymmetric information; 2) the risk-shifting problem, asymmetric information; 3) free cash-flow arguments; 4) the pecking order theory; 5) debt overhang.

Dividend theory: the Modigliani–Miller and dividend irrelevancy; Lintner’s fact about dividend policy; dividends, taxes and clienteles; asymmetric information and signalling through dividend policy.

Corporate governance: separation of ownership and control; management incentives; management shareholdings and firm value; corporate governance.

Mergers and acquisitions: motivations for merger activity; calculating the gains and losses from merger/takeover; the free-rider problem and takeover activity.

Introduction to the subject guide

3

Essential readingThere are a number of excellent textbooks that cover this area. However, the following text has been chosen as the core text for this course due to its extensive treatment of many of the issues covered and up-to-date discussions:

Hillier, D., M. Grinblatt and S. Titman Financial Markets and Corporate Strategy. (Boston, Mass.; London: McGraw-Hill, 2008) European edition [ISBN 978007119027].

At the start of each chapter of this guide, we will indicate the reading that you need to do from Hillier, Grinblatt and Titman (2008).

Detailed reading references in this subject guide refer to the editions of the set textbooks listed above. New editions of one or more of these textbooks may have been published by the time you study this course. You can use a more recent edition of any of the books; use the detailed chapter and section headings and the index to identify relevant readings. Also check the virtual learning environment (VLE) regularly for updated guidance on readings.

Further readingPlease note that as long as you read the Essential reading you are then free to read around the subject area in any text, paper or online resource. You will need to support your learning by reading as widely as possible and by thinking about how these principles apply in the real world. To help you read extensively, you have free access to the VLE and University of London Online Library (see below).

Other useful texts for this course include:

Brealey, R., S. Myers and F. Allen Principles of Corporate Finance. (Boston, Mass., London: McGraw-Hill, 2008) ninth international edition [ISBN 9780071266758].

Copeland, T., J. Weston and K. Shastri Financial Theory and Corporate Policy. (Reading, Mass.; Wokingham: Addison-Wesley, 2005) fourth edition [ISBN 9780321223531].

A full list of all Further reading referred to in the subject guide is presented here for ease of reference.

Journal articlesAsquith, P. and D. Mullins ‘The impact of initiating dividend payments on

shareholders’ wealth’, Journal of Business 56(1) 1983, pp.77–96.Ball, R. and P. Brown ‘An empirical evaluation of accounting income numbers’,

Journal of Accounting Research 6(2) 1968, pp.159–78.Bhattacharya, S. ‘Imperfect information, dividend policy, and “the bird in the

hand” fallacy’, Bell Journal of Economics 10(1) 1979, pp.259–70.Blume, M., J. Crockett and I. Friend ‘Stock ownership in the United States:

characteristics and trends’, Survey of Current Business 54(11) 1974, pp.16–40.

Bradley, M., A. Desai and E. Kim ‘Synergistic gains from corporate acquisitions and their division between the stockholders of target and acquiring firms’, Journal of Financial Economics 21(1) 1988, pp.3–40.

Brock, W., J. Lakonishok and B. LeBaron ‘Simple technical trading rules and stochastic properties of stock returns’, Journal of Finance 47(5) 1992, pp.1731–64.

92 Corporate finance

4

Campbell, J. and R. Shiller ‘The dividend-price ratio and expectations of future dividends and discount ractors’, Review of Financial Studies 1 1988.

Chen, N-F. ‘Some empirical tests of the theory of arbitrage pricing’, The Journal of Finance 38(5) 1983, pp.1393–414.

Chen, N-F., R. Roll and S. Ross ‘Economic Forces and the Stock Market’, Journal of Business 59 1986, pp.383–403.

Cochrane, J.H. ‘Explaining the variance of price-dividend ratios’, Review of Financial Studies 5 1992, pp.243–80.

DeBondt, W. and R. Thaler ‘Does the stock market overreact?’, Journal of Finance 40(3) 1984, pp.793–805.

Fama, E. ‘The behavior of stock market prices’, Journal of Business 38(1) 1965, pp.34–105.

Fama, E. ‘Efficient capital markets: a review of theory and empirical work’, Journal of Finance 25(2) 1970, pp.383–417.

Fama, E. ‘Efficient capital markets: II’, Journal of Finance 46(5) 1991, pp.1575–617.

Fama, E. and K. French ‘Dividend yields and expected stock returns’, Journal of Financial Economics 22(1) 1988, pp.3–25.

French, K. ‘Stock returns and the weekend effect’, Journal of Financial Economics 8(1) 1980, pp.55–70.

Fama, E. and K. French ‘The cross-section of expected stock returns’, Journal of Finance 47(2) 1992, pp.427–65.

Fama, E. and K. French ‘Common risk factors in the returns on stocks and bonds’, Journal of Financial Economics 33 1993, pp.3–56.

Fama, E. and J. MacBeth. ‘Risk, return, and equilibrium: empirical tests’, Journal of Political Economy 91 1973, pp.607–36.

Gibbons, M.R., S.A. Ross, and J. Shanken. ‘A test of the efficiency of a given portfolio’, Econometrica 57 1989, pp.1121–52.

Grossman, S. and O. Hart ‘Takeover bids, the free-rider problem and the theory of the corporation’, Bell Journal of Economics 11(1) 1980, pp.42–64.

Healy, P. and K. Palepu ‘Earnings information conveyed by dividend initiations and omissions’, Journal of Financial Economics 21(2) 1988, pp.149–76.

Healy, P., K. Palepu and R. Ruback ‘Does corporate performance improve after mergers?’, Journal of Financial Economics 31(2) 1992, pp.135–76.

Jegadeesh, N. and S. Titman ‘Returns to buying winners and selling losers’, Journal of Finance 48 1993, pp.65–91.

Jarrell, G. and A. Poulsen ‘Returns to acquiring firms in tender offers: evidence from three decades’, Financial Management 18(3) 1989, pp.12–19.

Jarrell, G., J. Brickley and J. Netter ‘The market for corporate control: the empirical evidence since 1980’, Journal of Economic Perspectives 2(1) 1988, pp.49–68.

Jensen, M. ‘Some anomalous evidence regarding market efficiency’, Journal of Financial Economics 6(2–3) 1978, pp.95–101.

Jensen, M. ‘Agency costs of free cash flow, corporate finance, and takeovers’, American Economic Review 76(2) 1986, pp.323–29.

Jensen, M. and W. Meckling ‘Theory of the firm: managerial behaviour, agency costs and capital structure’, Journal of Financial Economics 3(4) 1976, pp.305–60.

Jensen, M. and R. Ruback ‘The market for corporate control: the scientific evidence’, Journal of Financial Economics 11(1–4) 1983, pp.5–50.

Lakonishok, J., A. Shleifer and R. Vishny ‘Contrarian investment, extrapolation, and risk’, Journal of Finance 49(5) 1994, pp.1541–78.

Lettau, M. and S. Ludvigson ‘Consumption, aggregate wealth, and expected stock returns’, Journal of Finance 56 2001, pp.815–49.

Levich, R. and L. Thomas ‘The significance of technical trading-rule profits in the foreign exchange market: a bootstrap approach’, Journal of International Money and Finance 12(5) 1993, pp.451–74.

Introduction to the subject guide

5

Lintner, J. ‘Distribution of incomes of corporations among dividends, retained earnings and taxes’ American Economic Review 46(2) 1956, pp.97–113.

Lo, A. and C. McKinlay ‘Stock market prices do not follow random walks: evidence from a simple specification test’, Review of Financial Studies 1(1) 1988, pp.41–66.

Masulis, R. ‘The impact of capital structure change on firm value: some estimates’, Journal of Finance 38(1) 1983, pp.107–26.

Miles, J. and J. Ezzell ‘The weighed average cost of capital, perfect capital markets and project life: a clarification’, Journal of Financial and Quantitative Analysis 15 1980, pp.719–30.

Miller, M. ‘Debt and taxes’, Journal of Finance 32 1977, pp.261–75.Modigliani, F. and M. Miller ‘The cost of capital, corporation finance and the

theory of investment’, American Economic Review (48)3 1958, pp.261–97.Modigliani, F. and M. Miller ‘Corporate income taxes and the cost of capital: a

correction’, American Economic Review (5)3 1963, pp.433–43.Myers, S. ‘Determinants of corporate borrowing’, Journal of Financial Economics

5(2) 1977, pp.147–75.Myers, S. and N. Majluf ‘Corporate financing and investment decisions when

firms have information that investors do not have’, Journal of Financial Economics 13(2) 1984, pp.187–221.

Poterba, J. and L. Summers ‘Mean reversion in stock prices: evidence and implications’, Journal of Financial Economics 22(1) 1988, pp.27–59.

Roll, R. ‘A critique of the asset pricing theory’s texts. Part 1: on past and potential testability of the theory’, Journal of Financial Economics 4(2) 1977, pp.129–76.

Ross, S. ‘The determination of financial structure: the incentive signalling approach’, Bell Journal of Economics 8(1) 1977, pp.23–40.

Shleifer, A. and R. Vishny ‘Large shareholders and corporate control’, Journal of Political Economy 94(3) 1986, pp.461–88.

Shleifer, A. and R. Vishny ‘Managerial entrenchment: the case of management-specific investment’, Journal of Financial Economics 25, 1989 pp.123–39.

Travlos, N. ‘Corporate takeover bids, methods of payment, and bidding firms’ stock returns’, Journal of Finance 42(4) 1990, pp.943–63.

Warner, J. ‘Bankruptcy costs: some evidence’, Journal of Finance 32(2) 1977, pp.337–47.

BooksAllen, F. and R. Michaely ‘Dividend policy’ in Jarrow, R., W. Maksimovic and

W.T. Ziemba (eds) Handbook of Finance. (Amsterdam: Elsevier Science, 1995) [ISBN 9780444890849].

Haugen, R. and J. Lakonishok The Incredible January Effect. (Homewood, Ill.: Dow Jones-Irwin, 1988) [ISBN 9781556230424].

Ravenscraft, D. and F. Scherer Mergers, Selloffs, and Economic Efficiency. (Washington D.C.: Brookings Institution, 1987) [ISBN 9780815773481].

Online study resourcesIn addition to the subject guide and the Essential reading, it is crucial that you take advantage of the study resources that are available online for this course, including the VLE and the Online Library.

You can access the VLE, the Online Library and your University of London email account via the Student Portal at: http://my.londoninternational.ac.uk

You should receive your login details in your study pack. If you have not, or you have forgotten your login details, please email [email protected] quoting your student number.

92 Corporate finance

6

The VLEThe VLE, which complements this subject guide, has been designed to enhance your learning experience, providing additional support and a sense of community. It forms an important part of your study experience with the University of London and you should access it regularly.

The VLE provides a range of resources for EMFSS courses:

• Self-testing activities: Doing these allows you to test your own understanding of subject material.

• Electronic study materials: The printed materials that you receive from the University of London are available to download, including updated reading lists and references.

• Past examination papers and Examiners’ commentaries: These provide advice on how each examination question might best be answered.

• A student discussion forum: This is an open space for you to discuss interests and experiences, seek support from your peers, work collaboratively to solve problems and discuss subject material.

• Videos: There are recorded academic introductions to the subject, interviews and debates and, for some courses, audio-visual tutorials and conclusions.

• Recorded lectures: For some courses, where appropriate, the sessions from previous years’ Study Weekends have been recorded and made available.

• Study skills: Expert advice on preparing for examinations and developing your digital literacy skills.

• Feedback forms.

Some of these resources are available for certain courses only, but we are expanding our provision all the time and you should check the VLE regularly for updates.

Making use of the Online LibraryThe Online Library contains a huge array of journal articles and other resources to help you read widely and extensively.

To access the majority of resources via the Online Library you will either need to use your University of London Student Portal login details, or you will be required to register and use an Athens login: http://tinyurl.com/ollathens

The easiest way to locate relevant content and journal articles in the Online Library is to use the Summon search engine.

If you are having trouble finding an article listed in a reading list, try removing any punctuation from the title, such as single quotation marks, question marks and colons.

For further advice, please see the online help pages: www.external.shl.lon.ac.uk/summon/about.php

Subject guide structure and useYou should note that, as indicated above, the study of the relevant chapter should be complemented by at least the Essential reading given at the chapter head.

The content of the subject guide is as follows.

• Chapter 1: here we focus on the evaluation of real investment projects using the net present value technique and provide a comparison of NPV with alternative forms of project evaluation.

Introduction to the subject guide

7

• Chapter 2: we look at the basics of risk and return of primitive financial assets and mean–variance optimisation. We go on to derive and discuss the capital asset pricing model (CAPM).

• Chapter 3: we present the arbitrage pricing theory, proposed as an alternative to the CAPM and discuss multifactor models. We study several recent multifactor models, such as the Fama and French three-factor model, and observe that they can explain a large fraction of the variation in risky returns.

• Chapter 4: here we look at derivative assets. We begin with the nature of forward, future, option and swap contracts, then move on to pricing derivative assets via absence-of-arbitrage arguments. We also include a description of binomial option pricing models and end with the Black–Scholes analysis.

• Chapter 5: in this chapter, we examine the efficiency of financial markets. We present the concepts underlying market efficiency and discuss the empirical evidence on efficient markets. We also note that returns may be predictable even in efficient markets if risk is also predictable and discuss evidence in support of predictability of long horizon returns.

• Chapter 6: here we turn to corporate finance issues, treating the decision over a corporation’s capital structure. The essential issue is what levels of debt and equity finance should be chosen in order to maximise firm value.

• Chapter 7: this chapter is complementary to Chapter 6, however, rather than looking at values, as in Chapter 6, this chapter analyses discount rates. We learn that if there are no taxes, while the return on equity gets riskier as the level of debt increases, the average rate the firm pays to raise money is unchanged. In the presence of taxes, as debt increases, the average rate the firm pays to raise money decreases due to tax shields.

• Chapter 8: we look at more advanced issues in capital structure theory and focus on the use of capital structure to mitigate governance problems known as agency costs and how capital structure and financial decisions are affected by asymmetric information.

• Chapter 9: here we examine dividend policy. What is the empirical evidence on the dividend payout behaviour of firms, and theoretically, how can we understand the empirical facts?

• Chapter 10: we look at mergers and acquisitions, and ask what motivates firms to merge or acquire, what are the potential gains from this activity, and how can this be theoretically treated? We also explore how hostile acquisitions may serve as a discipline device to mitigate governance problems.

• There is no specific chapter about corporate governance, but the agency-related topics of Chapters 8 and 10 are inherently motivated by the existence of such problems. See also Hillier, Grinblatt and Titman (2008) Chapter 18 for a broad overview on governance-related issues.

Examination adviceImportant: the information and advice given here are based on the examination structure used at the time this guide was written. Please note that subject guides may be used for several years. Because of this we strongly advise you to always check both the current Regulations for relevant information about the examination, and the VLE where you should be advised of any forthcoming changes. You should also carefully

92 Corporate finance

8

check the rubric/instructions on the paper you actually sit and follow those instructions. Remember, it is important to check the VLE for:

• up-to-date information on examination and assessment arrangements for this course

• where available, past examination papers and Examiners’ commentaries for the course which give advice on how each question might best be answered.

This course will be evaluated solely on the basis of a three-hour examination. You will have to answer four out of a choice of eight questions. Although the Examiners will attempt to provide a fairly balanced coverage of the course, there is no guarantee that all of the topics covered in this guide will appear in the examination. Examination questions may contain both numerical and discursive elements. Finally, each question will carry equal weight in marking and, in allocating your examination time, you should pay attention to the breakdown of marks associated with the different parts of each question.

Glossary of abbreviations used in this subject guideAPT arbitrage pricing theory

CAPM capital asset pricing model

CML capital market line

IRR internal rate of return

MM Modigliani–Miller

NPV net present value

Chapter 1: Present value calculations and the valuation of physical investment projects

9

Chapter 1: Present value calculations and the valuation of physical investment projects

Aim The aim of this chapter is to introduce the Fisher separation theorem, which is the basis for using the net present value (NPV) for project evaluation purposes. With this aim in mind, we discuss the optimality of the NPV criterion and compare this criterion with alternative project evaluation criteria.

Learning outcomesAt the end of this chapter, and having completed the Essential reading and activities, you should be able to:

• analyse optimal physical and financial investment in perfect capital markets setting and derive the Fisher separation result

• justify the use of the NPV rules via Fisher separation

• compute present and future values of cash-flow streams and appraise projects using the NPV rule

• evaluate the NPV rule in relation to other commonly used evaluation criteria

• value stocks and bonds via NPV.

Essential readingHillier, D., M. Grinblatt and S. Titman Financial Markets and Corporate Strategy.

(Boston, Mass.; London: McGraw-Hill, 2008) Chapters 9 (Discounting and Valuation), 10 (Investing in Risk-Free Projects), 11 (Investing in Risky Projects).

Further readingBrealey, R., S. Myers and F. Allen Principles of Corporate Finance. (Boston,

Mass.; London: McGraw-Hill, 2008) Chapters 2 (Present Values), 3 (How to Calculate Present Values), 5 (The Value of Common Stocks), 6 (Why NPV Leads to Better Investment Decisions) and 7 (Making Investment Decisions with the NPV Rule).

Copeland, T. and J. Weston Financial Theory and Corporate Policy. (Reading, Mass.; Wokingham: Addison-Wesley, 2005) Chapters 1 and 2.

Roll, R. ‘A critique of the asset pricing theory’s texts. Part 1: on past and potential testability of the theory’, Journal of Financial Economics 4(2) 1977, pp.129–76.

92 Corporate finance

10

OverviewIn this chapter we present the basics of the present value methodology for the valuation of investment projects. The chapter develops the NPV technique before presenting a comparison with the other project evaluation criteria that are common in practice. We will also discuss the optimality of NPV and give a number of extensive examples.

IntroductionFor the purposes of this chapter, we will consider a firm to be a package of investment projects. The key question, therefore, is how do the firm’s shareholders or managers decide on which investment projects to undertake and which to discard? Developing the tools that should be used for project evaluation is the emphasis of this chapter.

It may seem, at this point, that our definition of the firm is rather limited. It is clear that, in only examining the investment operations of the firm, we are ignoring a number of potentially important firm characteristics. In particular, we have made no reference to the financial structure or decisions of the firm (i.e. its capital structure, borrowing or lending activities, or dividend policy). The first part of this chapter presents what is known as the Fisher separation theorem. What follows is a statement of the theorem. This theorem allows us to say the following: under certain conditions (which will be presented in the following section), the shareholders can delegate to the management the task of choosing which projects to undertake (i.e. determining the optimal package of investment projects), whereas they themselves determine the optimal financial decisions. Hence, the theory implies that the investment and financing choices can be completely disconnected from each other and justifies our limited definition of the firm for the time being.

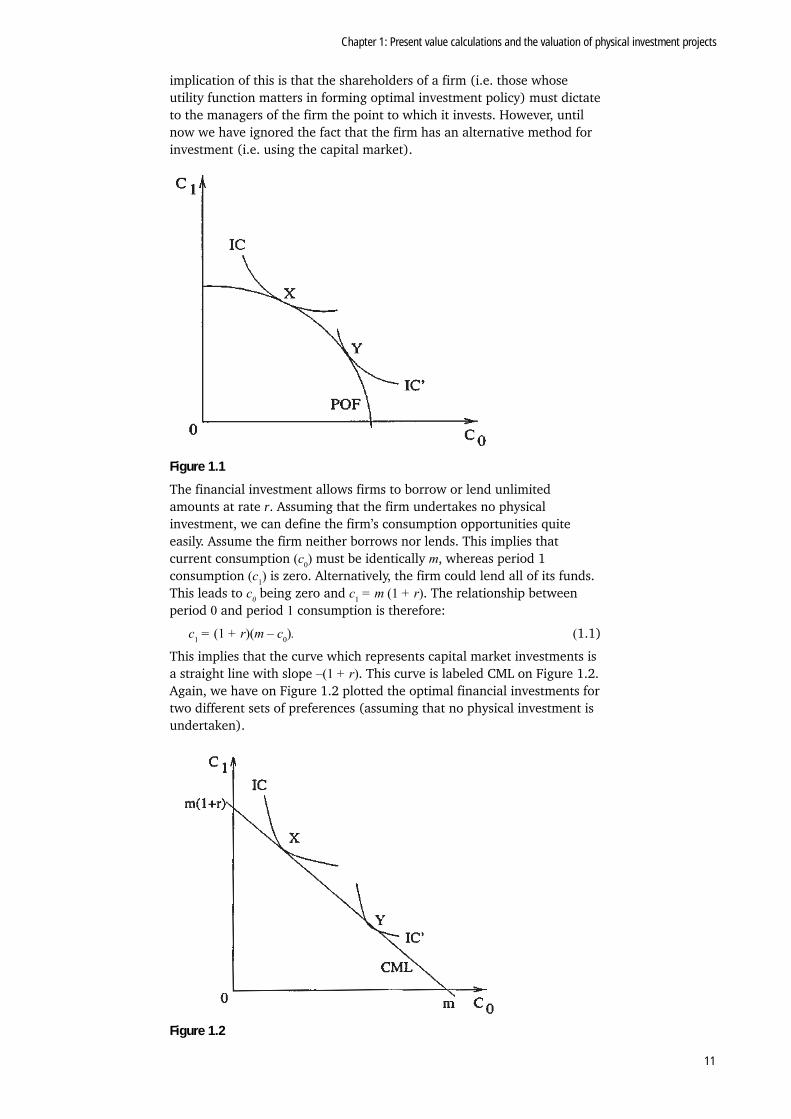

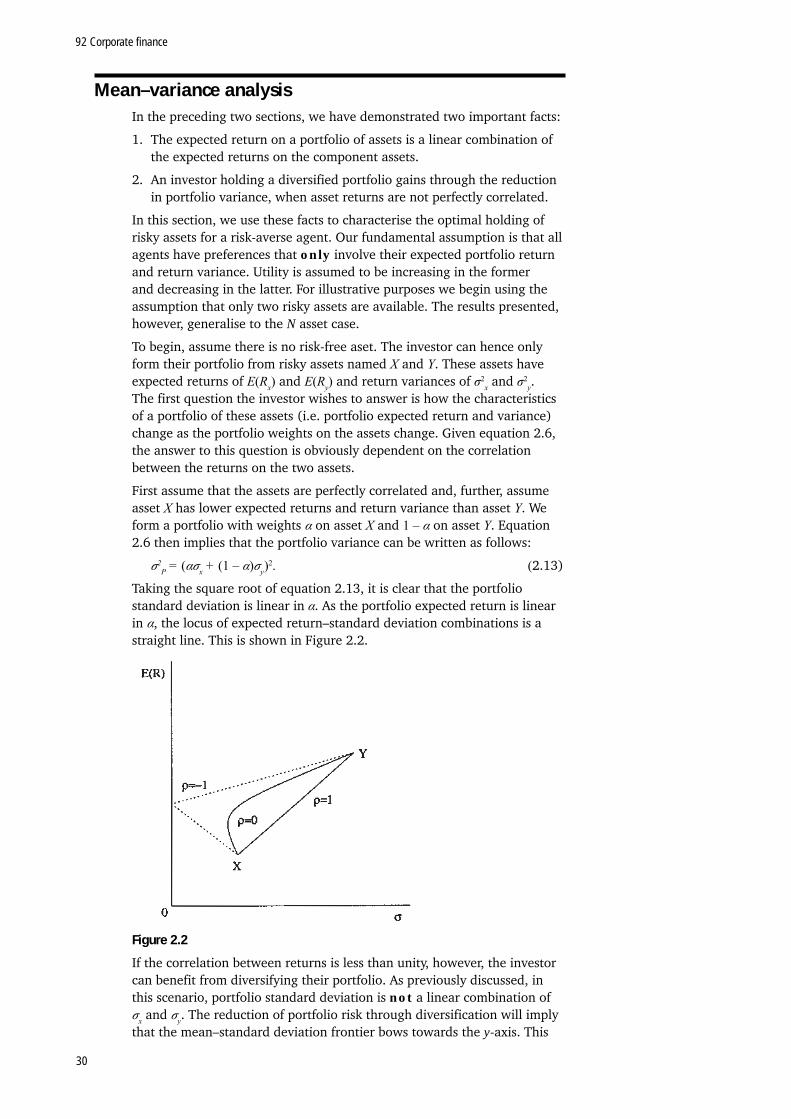

Fisher separation and optimal decision-makingConsider the following scenario. A firm exists for two periods (imaginatively named period 0 and period 1). The firm has current funds of m and, without any investment, will receive no money in period 1. Investments can be of two forms. The firm can invest in a number of physical investment projects, each of which costs a certain amount of cash in period 0 and delivers a known return in period 1. The second type of investment is financial in nature and permits the firm to borrow or lend unlimited amounts at rate of interest r. Finally the firm is assumed to have a standard utility function in its period 0 and period 1 consumption. (By consumption we mean the use of any funds available to the firm net of any costs of investment.)

Let us first examine the set of physical investments available. The firm will logically rank these investments in terms of their return, and this will yield a production opportunity frontier (POF) that looks as given in Figure 1.1. This curve represents one manner in which the firm can transform its current funds into future income, where c0 is period 0 consumption, and c1 is period 1 consumption. Using the assumed utility function for the firm, we can also plot an indifference map on the same diagram to find the optimal physical investment plan of a given firm. The optimal investment policies of two different firms are shown in Figure 1.1.

It is clear from Figure 1.1 that the specifics of the utility function of the firm will impact upon the firm’s physical investment policy. The

Chapter 1: Present value calculations and the valuation of physical investment projects

11

implication of this is that the shareholders of a firm (i.e. those whose utility function matters in forming optimal investment policy) must dictate to the managers of the firm the point to which it invests. However, until now we have ignored the fact that the firm has an alternative method for investment (i.e. using the capital market).

Figure 1.1

The financial investment allows firms to borrow or lend unlimited amounts at rate r. Assuming that the firm undertakes no physical investment, we can define the firm’s consumption opportunities quite easily. Assume the firm neither borrows nor lends. This implies that current consumption (c0) must be identically m, whereas period 1 consumption (c1) is zero. Alternatively, the firm could lend all of its funds. This leads to c0 being zero and c1 = m (1 + r). The relationship between period 0 and period 1 consumption is therefore:

c1 = (1 + r)(m – c0). (1.1)

This implies that the curve which represents capital market investments is a straight line with slope –(1 + r). This curve is labeled CML on Figure 1.2. Again, we have on Figure 1.2 plotted the optimal financial investments for two different sets of preferences (assuming that no physical investment is undertaken).

Figure 1.2

92 Corporate finance

12

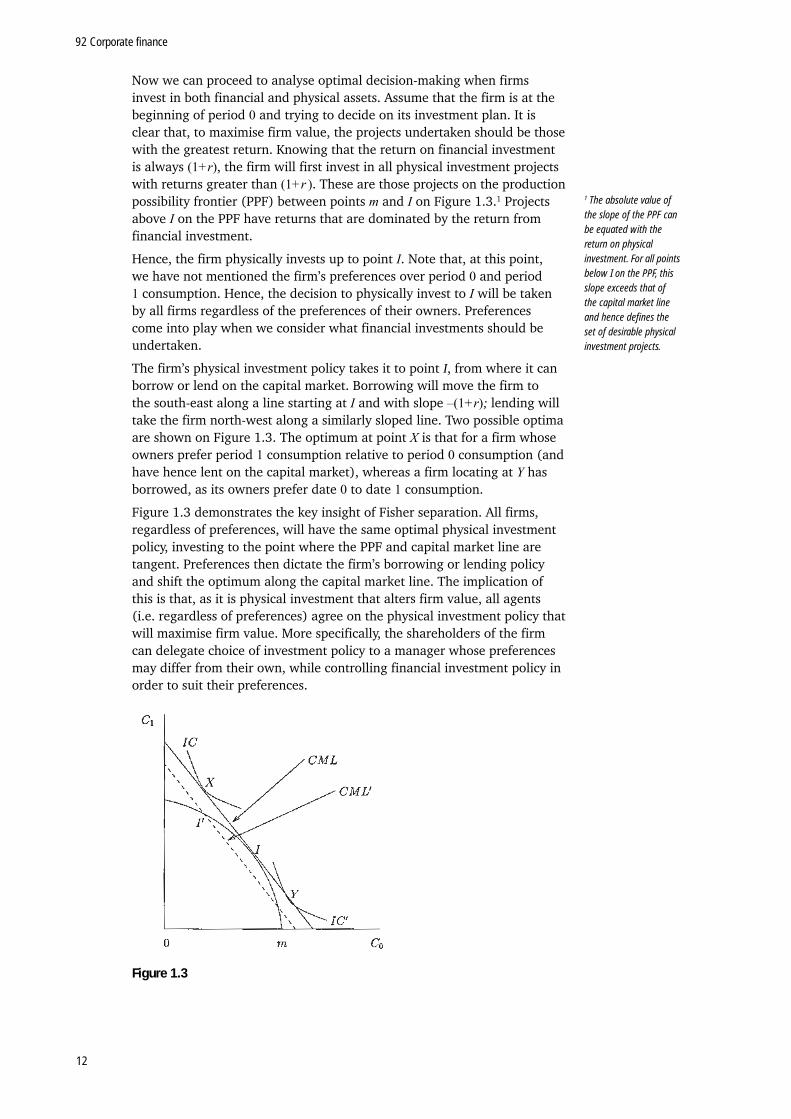

Now we can proceed to analyse optimal decision-making when firms invest in both financial and physical assets. Assume that the firm is at the beginning of period 0 and trying to decide on its investment plan. It is clear that, to maximise firm value, the projects undertaken should be those with the greatest return. Knowing that the return on financial investment is always (1+r), the firm will first invest in all physical investment projects with returns greater than (1+r ). These are those projects on the production possibility frontier (PPF) between points m and I on Figure 1.3.1 Projects above I on the PPF have returns that are dominated by the return from financial investment.

Hence, the firm physically invests up to point I. Note that, at this point, we have not mentioned the firm’s preferences over period 0 and period 1 consumption. Hence, the decision to physically invest to I will be taken by all firms regardless of the preferences of their owners. Preferences come into play when we consider what financial investments should be undertaken.

The firm’s physical investment policy takes it to point I, from where it can borrow or lend on the capital market. Borrowing will move the firm to the south-east along a line starting at I and with slope –(1+r); lending will take the firm north-west along a similarly sloped line. Two possible optima are shown on Figure 1.3. The optimum at point X is that for a firm whose owners prefer period 1 consumption relative to period 0 consumption (and have hence lent on the capital market), whereas a firm locating at Y has borrowed, as its owners prefer date 0 to date 1 consumption.

Figure 1.3 demonstrates the key insight of Fisher separation. All firms, regardless of preferences, will have the same optimal physical investment policy, investing to the point where the PPF and capital market line are tangent. Preferences then dictate the firm’s borrowing or lending policy and shift the optimum along the capital market line. The implication of this is that, as it is physical investment that alters firm value, all agents (i.e. regardless of preferences) agree on the physical investment policy that will maximise firm value. More specifically, the shareholders of the firm can delegate choice of investment policy to a manager whose preferences may differ from their own, while controlling financial investment policy in order to suit their preferences.

Figure 1.3

1 The absolute value of the slope of the PPF can be equated with the return on physical investment. For all points below I on the PPF, this slope exceeds that of the capital market line and hence defi nes the set of desirable physical investment projects.

Chapter 1: Present value calculations and the valuation of physical investment projects

13

Fisher separation and project evaluationFisher separation can also be used to justify a certain method of project appraisal. Figure 1.3 shows a suboptimal physical investment decision (I’) and the capital market line that borrowing and lending from point I’ would trace out. Clearly this capital market line always lies below that achieved through the optimal physical investment policy. Hence, one could say that optimal physical investment should maximise the horizontal intercept of the capital market line on which the firm ends up. Let us, then, assume a firm that decides to invest a dollar amount of I0. Given that the firm has date 0 income of m and no date 1 income, aside from that accruing from physical investment, the horizontal intercept of the capital market line upon which the firm has located is:

where Π(I0) is the date 1 income from the firm’s physical investment. Maximising this is equivalent to the following maximisation problem:

.

The prior objective is the NPV rule for project appraisal. It says that an optimal physical investment policy maximises the difference between investment proceeds divided by one plus the interest rate and the investment cost. Here, the term ‘optimal’ is being defined as that which leads to maximisation of shareholder utility. We will discuss the NPV rule more fully (and for cases involving more than one time period) later in this chapter.

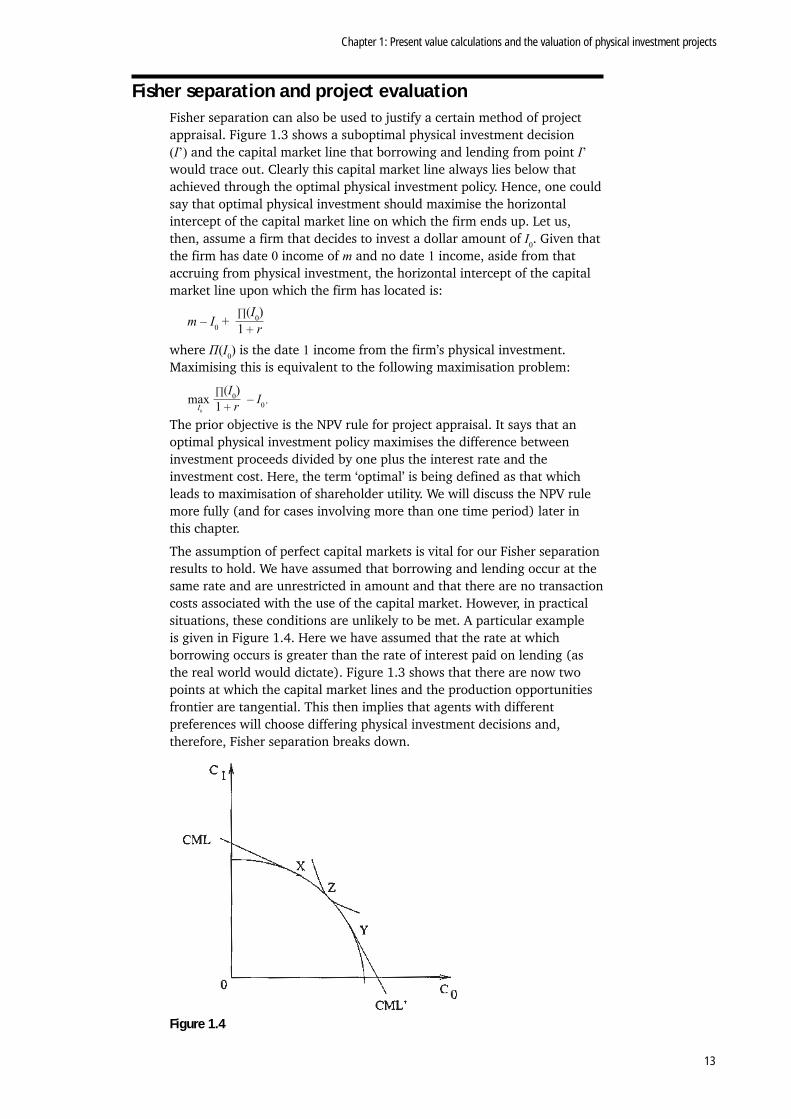

The assumption of perfect capital markets is vital for our Fisher separation results to hold. We have assumed that borrowing and lending occur at the same rate and are unrestricted in amount and that there are no transaction costs associated with the use of the capital market. However, in practical situations, these conditions are unlikely to be met. A particular example is given in Figure 1.4. Here we have assumed that the rate at which borrowing occurs is greater than the rate of interest paid on lending (as the real world would dictate). Figure 1.3 shows that there are now two points at which the capital market lines and the production opportunities frontier are tangential. This then implies that agents with different preferences will choose differing physical investment decisions and, therefore, Fisher separation breaks down.

Figure 1.4

92 Corporate finance

14

Agents with strong preferences for future consumption will physically invest to point X and then financially invest to an optimum on the capital market lending line (CML). Those with strong preferences for current consumption physically invest to point Y and borrow (along CML’). Finally, a set of agents may exist who value current and future consumption similarly, and these will optimise by locating directly on the PPF and not using the capital market at all. An example of an optimum of this type is point Z on Figure 1.4.

The time value of moneyIn the preceding section we demonstrated the Fisher separation theorem and the manner in which physical and financial investment decisions can be disconnected. The major implication of this theorem is that the set of desirable physical investment projects does not depend on the preferences of individuals. In the following sections we shall focus on the way in which individual physical investment projects should be evaluated. Our key methodology for this will be the NPV rule, mentioned in the preceding section. In the following sections we will show you how to apply the rule to situations involving more than one period and with time-varying cash flows.

To begin, let us consider a straightforward question. Is $1 received today worth the same as $1 received in one year’s time? A naïve response to this question would assert that $1 is $1 regardless of when it is received, and hence the answer to the question would be yes. A more careful consideration of the question brings the opposite response however. Let’s assume I receive $1 now. If I also assume that there is a risk-free asset in which I can invest my dollar (e.g. a bank account), then in one year’s time I will receive $(1+r), assuming I invest. Here, r is the rate of return on the safe investment. Hence $1 received today is worth $(1+r) in one year. The answer to the question is therefore no. A dollar received today is worth more than a dollar received in one year or at any time in the future.

The above argument characterises the time value of money. Funds are more valuable the earlier they are received. In the previous paragraph we illustrated this by calculating the future value of $1. We can similarly illustrate the time value of money by using present values. Assume I am to receive $1 in one year’s time and further assume that the borrowing and lending rate is r. How much is this dollar worth in today’s terms? To answer this second question, put yourself in the position of a bank. Knowing that someone is certain to receive $1 in one year, what is the maximum amount you would lend him or her now? If I, as a bank, were to lend someone money for one year, at the end of the year I would require repayment of the loan plus interest (at rate r). Hence if I loaned the individual $x, I would require a repayment of $x(1+r). This implies that the maximum amount I should be willing to lend is implicitly defined by the following equation:

$x(1+r) = $1 (1.2)

such that:

(1.3)

The value for x defined in equation 1.3 is the present value of $1 received in one year’s time. This quantity is also termed the discounted value of the $1.

Chapter 1: Present value calculations and the valuation of physical investment projects

15

You can see the present and future value concepts pictured in Figure 1.2. If you recall, Figure 1.2 just plots the CML for a given level of initial funds (m) assuming no funds are to be received in the future. The future value of this amount of money is simply the vertical intercept of the CML (i.e. m(1+r)), and obviously the present value of m(1+r) is just m.

The present and future value concepts are straightforwardly extended to cover more than one period. Assume an annual compound interest rate of r. The present value of $100 to be received in k year’s time is:

(1.4)

whereas the future value of $100 received today and evaluated k years hence is:

FVK (100) = 100(1 + r)K. (1.5)

Activity

Below, there are a few applications of the present and future value concepts. You should attempt to verify that you can replicate the calculations.

Assume a compound borrowing and lending rate of 10 per cent annually.

a. The present value of $2,000 to be received in three years time is $1,502.63.

b. The present value of $500 to be received in five years time is $310.46.

c. The future value of $6,000 evaluated four years hence is $8,784.60.

d. The future value of $250 evaluated 10 years hence is $648.44.

The net present value ruleIn the previous section we demonstrated that the value of funds depends critically on the time those funds are received. If received immediately, cash is more valuable than if it is to be received in the future.

The NPV rule was introduced in simple form in the section on Fisher separation. In its more general form, it uses the discounting techniques provided in the previous section in order to generate a method of evaluating investment projects. Consider a hypothetical physical investment project, which has an immediate cost of I. The project generates cash flows to the firm in each of the next k years, equal to Ck. In words, all that the NPV rule does is to compute the present value of all receipts or payments. This allows direct comparisons of monetary values, as all are evaluated at the same point in time. The NPV of the project is then just the sum of the present values of receipts, less the sum of the present values of the payments.

Using the notation given above and again assuming a rate of return of r, the NPV can be written as:

. (1.6)

Note that the cash flows to the project can be positive and negative, implying that the notation employed is flexible enough to embody both cash inflows and outflows after initiation.

Once we have calculated the NPV, what should we do? Clearly, if the NPV is positive, it implies that the present value of receipts exceeds the present value of payments. Hence, the project generates revenues that outweigh its costs and should therefore be accepted. If the NPV is negative the project should be rejected, and if it is zero the firm will be indifferent between accepting and rejecting the project.

92 Corporate finance

16

This gives a very straightforward method for project evaluation. Compute the NPV of the project (which is a simple calculation), and if it is greater than zero, the project is acceptable.

Example

Consider a manufacturing firm, which is contemplating the purchase of a new piece of plant. The rate of interest relevant to the firm is 10 per cent. The purchase price is £1,000. If purchased, the machine will last for three years and in each year generate extra revenue equivalent to £750. The resale value of the machine at the end of its lifetime is zero. The NPV of this project is:

NPV = 750 + 750 + 750 – 1000 = 865.14. (1.1)3 (1.1)2 (1.1)1

As the NPV of the project exceeds zero, it should be accepted.

In order to familiarise yourself with NPV calculations, attempt the following activities by calculating the NPV of each project and assessing its desirability.

Activity

Assume an interest rate of 5 per cent. Compute the NPV of each of the following projects, and state whether each project should be accepted or not.

• Project A has an immediate cost of $5,000, generates $1,000 for each of the next six years and zero thereafter.

• Project B costs £1,000 immediately, generates cash flows of £600 in year 1, £300 in year 2 and £300 in year 3.

• Project C costs ¥10,000 and generates ¥6,000 in year 1. Over the following years, the cash flows decline by ¥2,000 each year, until the cash flow reaches zero.

• Project D costs £1,500 immediately. In year 1 it generates £1,000. In year 2 there is a further cost of £2,000. In years 3, 4 and 5 the project generates revenues of £1,500 per annum.

Up to this point we have just considered single projects in isolation, assuming that our funds were enough to cover the costs involved. What happens, first of all, if the members of a set of projects are mutually exclusive?2 The answer is simple. Pick the project that has the greatest NPV. Second, what should we do if we have limited funds? It may be the case that we are faced with a pool of projects, all of which have positive NPVs, but we only have access to an amount of money that is less than the total investment cost of the entire project pool. Here we can rely on another nice feature of the NPV technique. NPVs are additive across projects (i.e. the NPV of taking on projects A and B is identical to the NPV of A plus the NPV of B). The reason for this should be obvious from the manner in which NPVs are calculated. Hence, in this scenario, we should calculate all project combinations that are feasible (i.e. the total investment in these projects can be financed with our current funds). Then calculate the NPV of each combination by summing the NPVs of its constituents, and finally choose the combination that yields the greatest total NPV.

Finally, we should devote some time to discussion of the ‘interest rate’ we have used to discount future cash flows. Until now we have just referred to r as the rate at which one can borrow or lend funds. A more precise definition of r is that r is the opportunity cost of capital. If we are considering the use of the NPV rule within the context of a firm, we have to recognise that the firm has several sources of capital, and the cost of each of these should be taken into account when evaluating the firm’s

2 By this we mean that taking on any one of the set of projects precludes us from accepting any of the others.

Chapter 1: Present value calculations and the valuation of physical investment projects

17

overall cost of capital. The firm can raise funds via equity issues and debt issues, and it is likely that the costs of these two types of funds will differ. Later on in this chapter and in those that follow, we will present techniques by which the firm can compute the overall cost of capital for its enterprise.

Other project appraisal techniquesThe NPV methodology for project appraisal is by no means the only technique used by firms to decide on their physical investment policy. It is, however, the optimal technique for corporate management to use if they wish to maximise expected shareholder wealth. This result is obvious from our Fisher separation analysis. In this section we talk about three of NPV’s competitors, the payback rule, the internal rate of return (IRR) rule, and the multiples method, which are sometimes used in practice.

The payback rulePayback is a particularly simple criterion for deciding on the desirability of an investment project. The firm chooses a fixed payback period, for example, three years. If a project generates enough cash in the first three years of its existence to repay the initial investment outlay, then it is desirable, and if it doesn’t generate enough cash to cover the outlay, it should be rejected. Take the cash-flow stream given in the following table as an example.

Year 0 1 2 3 4

Cash flow –1,000 250 250 250 500

Table 1.1

A firm that has chosen a payback period of three years and is faced with the project shown in Table 1.1 will reject it as the cash flow in years 1 to 3 (750) doesn’t cover the initial outlay of 1,000. Note, however, that if the firm used a payback period of four years, the project would be acceptable, as the total cash flow to the project would be 1,250, which exceeds the outlay. Hence, it’s clear that the crucial choice by management is of the payback period.

We can also use the preceding example to illustrate the weaknesses of payback. First, assume that the firm has a payback period of three years. Then, as previously mentioned, the project in Table 1.1 will not be accepted. However, assume also that, instead of being 500, the project cash flow in year 4 is 500,000. Clearly, one would want to revise one’s opinion on the desirability of the project, but the payback rule still says you should reject it. Payback is flawed, as a portion of the cash-flow stream (that realised after the payback period is up) is always ignored in project evaluation.

The second weakness of payback should be obvious, given our earlier discussion of NPV. Payback ignores the time value of money. Sticking with the example in Table 1.1, assume a firm has a payback period of four years. Then the project as given should be accepted (as total cash flow of 1,250 exceeds investment outlay of 1,000). But what’s the NPV of this project? If we assume, for example, a required rate of return of 10 per cent, then the NPV can be shown to be negative. (In fact the NPV is –36.78. As a self-assessment activity, show that this is the case.) Hence application of the payback rule tells us to accept a project that would decrease expected shareholder wealth (as shown by application of the NPV rule). This flaw could be eliminated by discounting project cash flows that accrue within

92 Corporate finance

18

the payback period, giving a discounted payback rule, but such a modification still wouldn’t solve the first problem we highlighted.

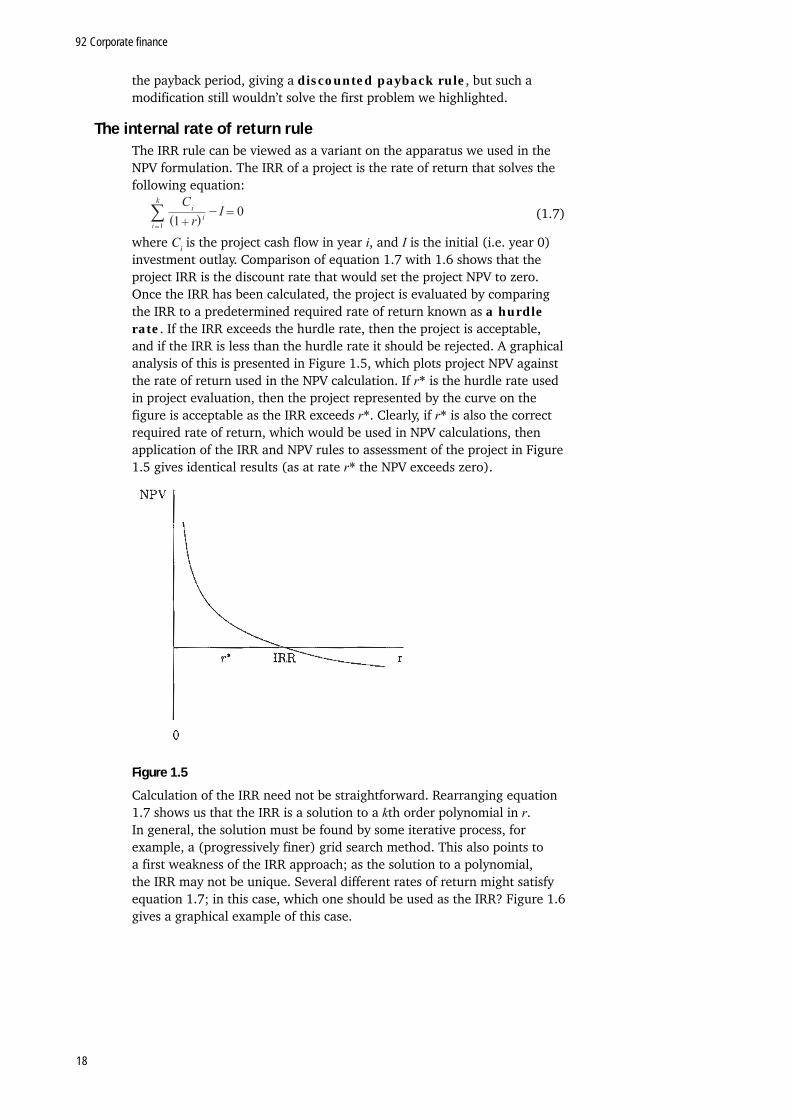

The internal rate of return ruleThe IRR rule can be viewed as a variant on the apparatus we used in the NPV formulation. The IRR of a project is the rate of return that solves the following equation:

(1.7)

where Ci is the project cash flow in year i, and I is the initial (i.e. year 0) investment outlay. Comparison of equation 1.7 with 1.6 shows that the project IRR is the discount rate that would set the project NPV to zero. Once the IRR has been calculated, the project is evaluated by comparing the IRR to a predetermined required rate of return known as a hurdle rate. If the IRR exceeds the hurdle rate, then the project is acceptable, and if the IRR is less than the hurdle rate it should be rejected. A graphical analysis of this is presented in Figure 1.5, which plots project NPV against the rate of return used in the NPV calculation. If r* is the hurdle rate used in project evaluation, then the project represented by the curve on the figure is acceptable as the IRR exceeds r*. Clearly, if r* is also the correct required rate of return, which would be used in NPV calculations, then application of the IRR and NPV rules to assessment of the project in Figure 1.5 gives identical results (as at rate r* the NPV exceeds zero).

Figure 1.5

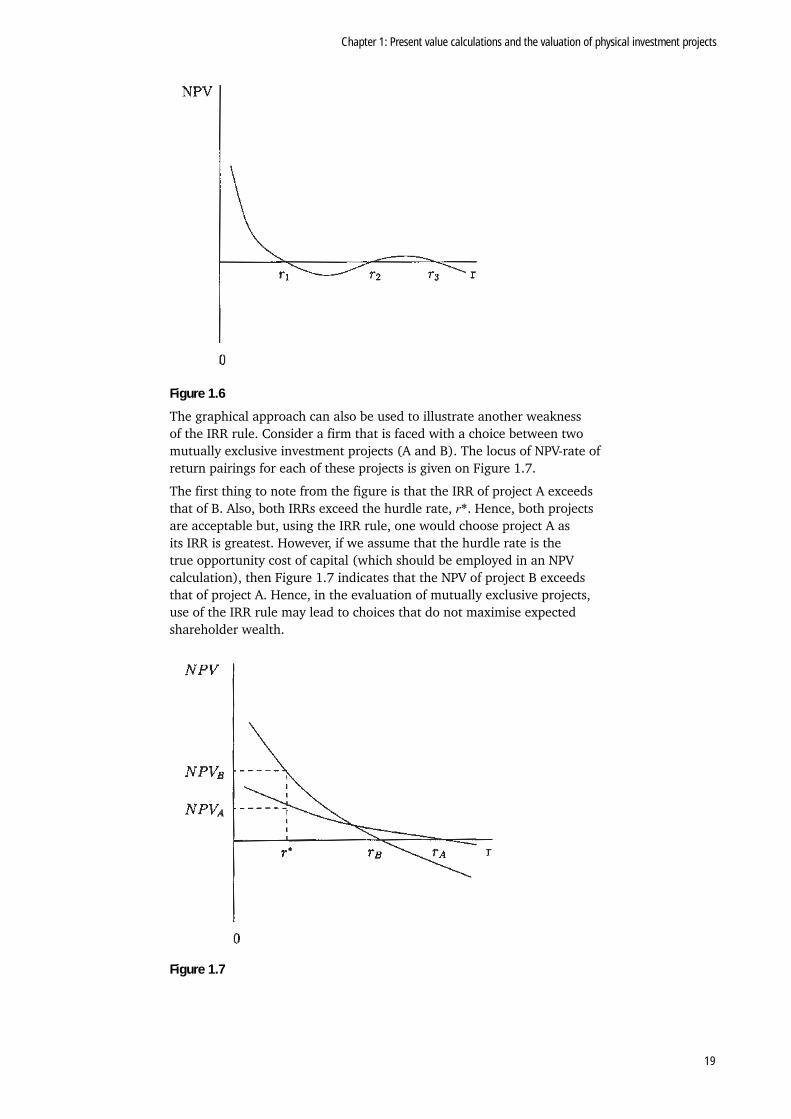

Calculation of the IRR need not be straightforward. Rearranging equation 1.7 shows us that the IRR is a solution to a kth order polynomial in r. In general, the solution must be found by some iterative process, for example, a (progressively finer) grid search method. This also points to a first weakness of the IRR approach; as the solution to a polynomial, the IRR may not be unique. Several different rates of return might satisfy equation 1.7; in this case, which one should be used as the IRR? Figure 1.6 gives a graphical example of this case.

Chapter 1: Present value calculations and the valuation of physical investment projects

19

Figure 1.6

The graphical approach can also be used to illustrate another weakness of the IRR rule. Consider a firm that is faced with a choice between two mutually exclusive investment projects (A and B). The locus of NPV-rate of return pairings for each of these projects is given on Figure 1.7.

The first thing to note from the figure is that the IRR of project A exceeds that of B. Also, both IRRs exceed the hurdle rate, r*. Hence, both projects are acceptable but, using the IRR rule, one would choose project A as its IRR is greatest. However, if we assume that the hurdle rate is the true opportunity cost of capital (which should be employed in an NPV calculation), then Figure 1.7 indicates that the NPV of project B exceeds that of project A. Hence, in the evaluation of mutually exclusive projects, use of the IRR rule may lead to choices that do not maximise expected shareholder wealth.

Figure 1.7

92 Corporate finance

20

The multiples methodAn alternative to using forecasts of a firm’s or project’s cash flows to calculate value, market information can be used to estimate the value. The multiples method assesses the firm’s value based on the value of a comparable publically traded firm. For example, consider the firm’s market value to earnings ratio, this ratio tells us how much a dollar of earnings contributes to the present value according to the market’s consensus view. For publically traded firms, this ratio is available. The firm we wish to value may not have a publically available market value, however we are likely to know its earnings. If we assume that these two firms should have similar market value to earnings ratios, then we can value the firm by taking the publically available ratio and multiplying it by the firm’s earnings.

Common multiples to use are market value to earnings, market value to EBITDA, market value to cash flow, and market value to book value. Some firms, especially younger firms, have no earnings or even negative earnings. In this case it may be better to value the firm as of some future date in which the firm’s cash flows have stabilised, and then to discount to today’s value. An alternative is to use more creative multiples, for example price to patent ratio, price to subscriber ratio, or price to Ph.D. ratio. It is often better to take an average over several comparable firms to calculate the multiple. If you believe the firm being valued is better or worse than the comparable firms, you can shade the multiple down or up, as in the example below. The multiples method is not an exact science but rather a convenient way to incorporate market beliefs. It should always be used in conjunction with another method, such as NPV.

Example

Below are the equity values, debt values, and earnings (in billions) for several large US retailers. Additionally provided is earnings growth for the past 10 years.

Equity Debt E E (10 yr) %

JCP 17.48 3.81 1.10 7.8

COST 24.08 2.22 1.10 15.5

HD 82.08 12.39 6.01 21.2

WMT ? 47.44 11.88 15.7

TGT 50.14 14.14 2.58 19.2

Walmart’s (WMT’s) equity value is excluded as this is the quantity we wish to estimate. We can first calculate the market value of equity to earnings ratio for the average firm in the industry (excluding Walmart), this is: [(17.48/1.1) + (24.08/1.1) + (82.08/6.01) + (50.14/2.58)]/4 = 17.72

We now multiply this number by Walmart’s earnings to get Walmart’s equity value estimate: 17.72*11.88=210.49. Walmart’s actual equity value was $192.48 billion.

In the example above we used multiples to value equity, we sometimes wish to the value of the full business (sometimes called enterprise value), in this case we would need to use the full business value (for example, debt plus equity) in the numerator instead of just equity value.

Notice that the debt to equity ratio of Costco (COST) was 9.2% while that of Target (TGT) was 28.2%. In this example, we have ignored the effects of leverage (debt in the capital structure), however as we will see in a later chapter, leverage affects both firm value and the expected return on equity. Therefore, firms with different leverage ratios that look otherwise similar

Chapter 1: Present value calculations and the valuation of physical investment projects

21

may have very different value to earnings ratios. We will learn how to adjust the multiples method for the effects of leverage later.

The multiples method allows us to check whether the value of a conglomerate is equal to the sum of its parts. To estimate the value of each business division of a conglomerate we can calculate each division’s earnings and multiply it by the average value to earnings multiple of stand alone firms in the same sector. Adding up the value of all divisions gives us an estimated value for the conglomerate, this estimate is on average 12% greater than the traded value of the conglomerate. This is called the conglomerate discount. The reasons for the conglomerate discount are not fully understood. It is possible that conglomerates are a less efficient form of organisation due to inefficient capital markets. It is also possible that the multiples method is inappropriate here because single segment firms are too different from divisions of a conglomerate operating in the same industry.