corporate office properties trust the preferred provider … 2014.pdf · real estate solutions...

TRANSCRIPT

Patriot Ridge | Virginia

Arundel Preserve | Maryland

Corporate Office Properties Trust

November 2014

Redstone Gateway | Alabama

The National Business Park | Maryland

The Preferred Provider

of Mission Critical

Real Estate Solutions

Columbia Gateway | Maryland

2

I. Company Overview p. 3

II. Value Creation & Growth p. 10

Appendices:

A. Definitions & Glossary

B. Reconciliations

C. Safe Harbor

I. Company Overview

4

Company Overview

COPT is a Class-A Office REIT with two distinctions:

1. Strategic Tenant Niche (“STN”) ― We are a preferred provider of real

estate solutions serving the U.S. Government and defense contractors engaged in information technology and national security related activities

— Our Strategic Tenants’ missions involve fulfilling the high-tech, R&D aspects of defense, including Cyber Security

— The defense installations† where our Strategic Tenants operate are R&D, high-tech knowledge-based centers, not weapons- or troops-oriented

† Defense installations or “government demand drivers” are also referred to as “forts” and “arsenals.”

* Please see Baltimore/Washington region in “Definitions & Glossary” at the back of this presentation.

2. Regional Focus ― We are a

market leader in targeted

submarkets in the B/W Region*

and in Northern Virginia

— B/W Region* and NoVA account for 52% and 19%, respectively, of our 16.9 million SF

5

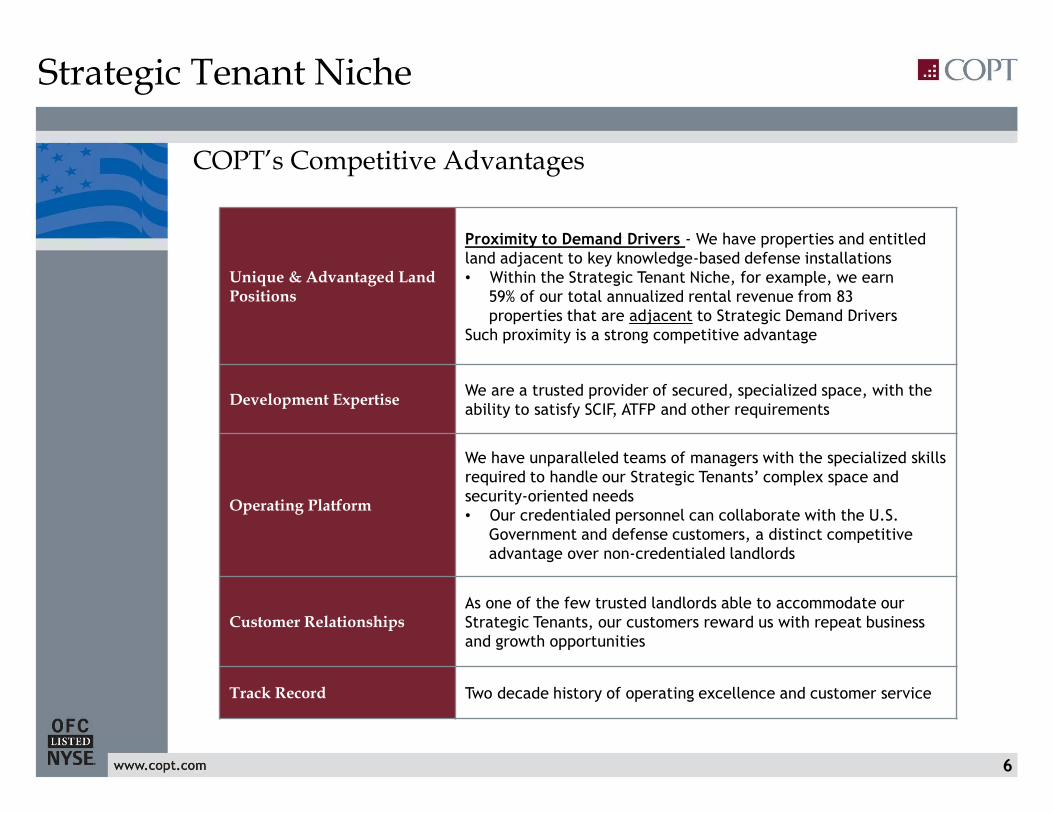

Strategic Tenant Niche

COPT’s Competitive Advantages

Over the course of two decades, we have earned a reputation as one

of the few “go-to” landlords for secured, specialized space, including SCIF and ATFP buildings

The foundation of our unparalleled franchise has five strategic constructs:

1. Unique & Advantaged Land Positions

2. Development Expertise for Secured and/or Specialized Buildings

3. Operating Platform

4. Customer Relationships

5. Track Record

6

Strategic Tenant Niche

COPT’s Competitive Advantages

Unique & Advantaged Land Positions

Proximity to Demand Drivers - We have properties and entitled

land adjacent to key knowledge-based defense installations

• Within the Strategic Tenant Niche, for example, we earn

59% of our total annualized rental revenue from 83

properties that are adjacent to Strategic Demand Drivers

Such proximity is a strong competitive advantage

Development Expertise We are a trusted provider of secured, specialized space, with the

ability to satisfy SCIF, ATFP and other requirements

Operating Platform

We have unparalleled teams of managers with the specialized skills

required to handle our Strategic Tenants’ complex space and

security-oriented needs

• Our credentialed personnel can collaborate with the U.S.

Government and defense customers, a distinct competitive

advantage over non-credentialed landlords

Customer Relationships As one of the few trusted landlords able to accommodate our

Strategic Tenants, our customers reward us with repeat business

and growth opportunities

Track Record Two decade history of operating excellence and customer service

Strategic Tenant Niche

COPT’s portfolio is aligned with defense installations whose missions

involve (i) intelligence gathering, (ii) gaining military efficiencies and (iii)

Cyber Security ― three activities that remain DOD spending priorities

Demand Driver COPT Asset Missions

Ft. Meade

NBP

Arundel Preserve

Columbia Gateway

Airport Square

Cyber, SIGINT, Info Assurance,

DOD IT Function

Redstone Arsenal Redstone Gateway

Missile Defense, Aviation &

Rocket Testing, Army Materiel

Command & Others

San Antonio Sentry Gateway Air Force Cyber & Others

Ft. Belvoir Patriot Ridge Geospatial Intelligence

NoVA Westfields Intelligence Satellites

7

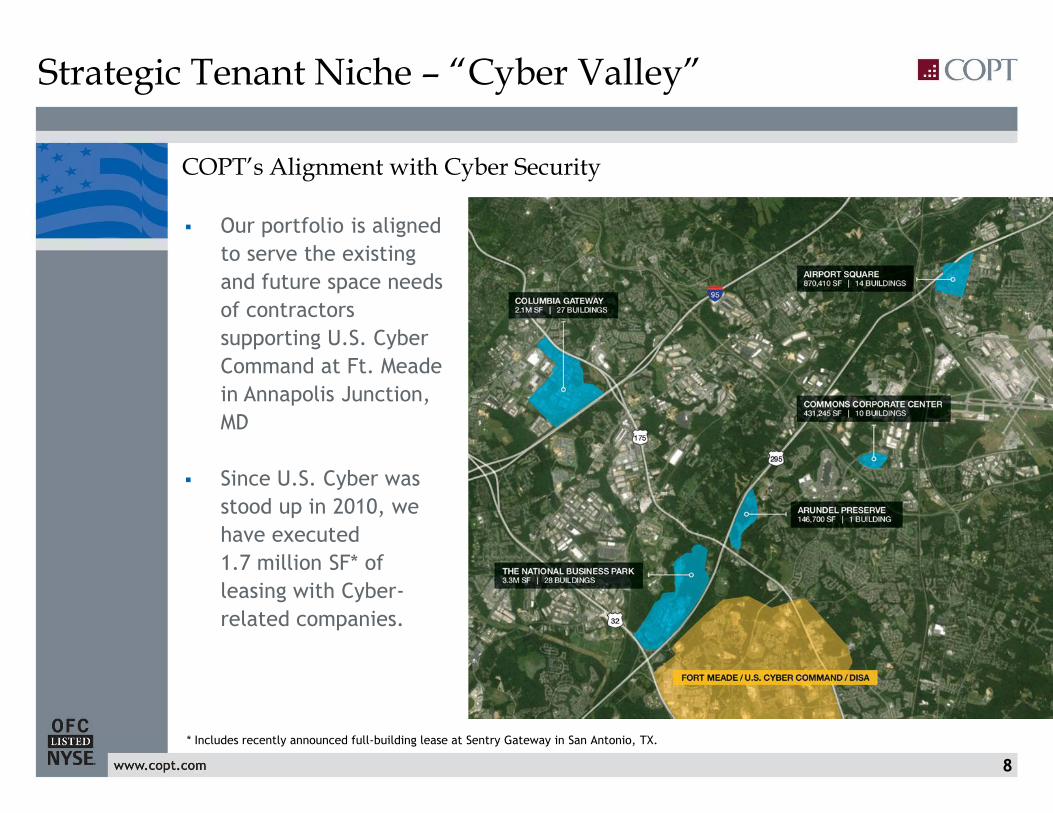

Strategic Tenant Niche – “Cyber Valley”

COPT’s Alignment with Cyber Security

8

Our portfolio is aligned

to serve the existing

and future space needs

of contractors

supporting U.S. Cyber

Command at Ft. Meade

in Annapolis Junction,

MD

Since U.S. Cyber was

stood up in 2010, we

have executed

1.7 million SF* of

leasing with Cyber-

related companies.

* Includes recently announced full-building lease at Sentry Gateway in San Antonio, TX.

In addition to serving our Strategic Tenant Niche, we also are a dominant office landlord in strategic submarkets within the B/W Region and NoVA markets

Our primary markets house the nation’s

largest employer (the U.S. Government),

have highly educated work forces, and

feature strong overall demographics,

including:

— High per capita income

— Above average employment,

even during the 2008-2009

Great Recession

• 71% of COPT’s total SF are located in

the B/W Region and NoVA

• Our “local sharp-shooter” advantage

enables us to add value at the submarket,

customer and property levels

9

Regional Office Portfolio

Data in charts was compiled by Bureau of Economic Analysis, Bureau of Labor Statistics, MD and VA state websites, and COPT.

II. Value Creation & Growth

In 2013, COPT completed a series of strategic initiatives*:

Value Creation & Growth

11

Portfolio Repositioning

• By YE2013, we had disposed of 5.9 million SF, or 29% of the

total 20.6 million SF owned at 3/31/11

• Our dispositions eliminated older, smaller assets, and/or assets

in submarkets with below-average growth prospects

• During this time, we also developed 2.2 million SF and acquired

300,000 SF of Class-A office in our most strategic locations

Balance Sheet

• Between 3/31/11 & 12/31/13, we improved our adjusted debt

to in-place adjusted EBITDA to 6.8x from 9.0x and lowered our

debt to adjusted book ratio to 43.6% from 52.5%

• We achieved Investment Grade Ratings during 2013: o Fitch: BBB- o Moody’s: Baa3 o S&P: BBB-

• Extended average debt maturity by issuing senior debt

De-Risked & Grew Development Pipeline

• By limiting speculative development starts and pursuing more

build-to-suit opportunities, we increased the development

pipeline’s leasing levels to 50% or more, which compares

favorably to the 15% at 3/31/11

* COPT commenced its portfolio & balance sheet initiatives after the first quarter of 2011, and completed them late in 2013.

Defense Spending Environment Supports Higher Demand

The DOD’s Base Budget is no longer in question:

— The Bipartisan Budget Act of 2013 (the “Budget Act”) eliminated some sequester cuts and established a new DOD baseline budget of $500 billion for FY’14 & FY’15 (essentially flat relative to FY’13)

• After FY’15, defense spending levels are expected to grow with inflation

Impact on COPT:

— The Budget Act created certainty regarding Defense spending levels through FY’15, enough time for the DOD to reallocate funding to priority programs such as U.S. Cyber Command

• The DOD has re-started a normal contract awarding process, which has increased demand for space to support growing, priority missions

— Our portfolio aligns with the DOD’s current and future strategic interests, namely: Intelligence, Surveillance, Reconnaissance and Cyber

• The President requested a 10% increase in the DOD’s Cyber Security budget for FY’15

Value Creation & Growth

12

Internal Growth - Leasing existing vacancy will increase FFO & NAV

At 92.1% occupancy, our same-office portfolio is well leased

— Office buildings occupied by Strategic Tenants are 93.7% occupied

— After absorbing known move-outs in 4Q14, our same office occupancy will still exceed 90%

Growth opportunity: Improve same-office occupancy to 92%-93% by year

end 2016

— The more certain Defense spending environment afforded by the Bipartisan Budget Act of 2013, as well as the improving economy, is supportive of higher occupancy levels

Value Creation & Growth

13

Value Creation & Growth

14

External Growth - Development Pipeline

Demand for new construction in our markets remained strong, even in years when the DOD had no budget:

In 2012, COPT executed 1.2 million SF of development leasing, which was the largest annual volume in our history

— 675,000 SF of the total was leased to our Strategic Tenant Niche

In 2013, COPT signed 897,000 SF of development leasing, the third highest development leasing volume in our history

— This included 656,000 SF of leasing to Strategic Tenants

In the three quarters of 2014, we signed another 487,600 SF of development leasing, 88% of which was to Strategic Tenants

Now that the DOD has clarity on spending levels through FY ’15, we anticipate an increase in demand for new and existing office space, especially as we go into the fourth quarter (which is the beginning of the USG’s fiscal year)

Value Creation & Growth

15

Development Pipeline – Fueling Growth

We will continue our disciplined approach to developing space to serve Strategic Tenants and, where demand exists, develop in our regional markets

Our 1.1 million SF pipeline of properties under construction and redevelopment is 51% leased

22 recently completed and active development projects are forecasted to generate $48 million of incremental cash NOI

— Of this $48 million, $33 million of NOI is associated with executed leases, and therefore has no risk

• These leases will contribute total cash NOI of between $8―$9 million in 2014 (including the $5 million they contributed in the first three quarters of 2014)

— Of the $15 million of NOI to be created from new leasing, over half will come from two buildings that have a high level of leasing visibility with Strategic Niche customers

Value Creation & Growth

16

Balance Sheet – Recent Improvements

We are committed to incrementally improving our balance sheet by terming-out debt and locking-in low interest rates for longer durations

In May, we issued $300 million of 7-year senior notes that carry a 3.70% interest rate, which represented a spread over Treasuries of 165 basis points

In June, we redeemed all $50 million of our 7.5% Series H Preferred stock

— The redemption was funded with proceeds from the sale of 8 properties from our White Marsh portfolio and non-strategic land sales (see press releases dated August 14 and September 25, 2014)

In October, we issued $129.3 million* of common stock to further delever and fund future development opportunities

— Proforma the offering, our adjusted debt to in-place adjusted EBITDA is forecasted at 6.5x for year end 20014

* Net proceeds, before exercising the underwriters overallotment; this offering will be completed on November 5, 2014.

17

COPT is positioned to capitalize on its reputation as one of the top office landlords in its markets and to add value for shareholders

The leasing outlook for our portfolio is improving

— Demand for our regionally focused office properties is increasing along with the local economy

— Strategic Tenant demand for new, precisely located office buildings and specialized facilities on land we own is strong and growing

• The establishment of U.S. Cyber Command at Fort Meade will require a significant number of new and/or re-developed buildings to house supporting Defense/IT contractors

• The Bipartisan Budget Act of 2013 created certainty regarding future Defense Spending levels (see slide 12 for more detail)

In addition to increasing portfolio occupancy, low–risk development will continue to be a major driver of growth in our earnings and NAV

— Our Shadow Development Pipeline includes eight potential new projects totaling over 1 million SF

Conclusion

18

Appendices

18

A. Definitions & Glossary

B. Reconciliations

C. Safe Harbor

19

A. Definitions & Glossary

19

Acquisition costs – transaction costs expensed in connection with executed or anticipated acquisitions of operating properties.

Adjusted Book – total assets presented on consolidated balance sheet, excluding effect of accumulated depreciation on real estate properties, accumulated amortization of intangible assets on real estate acquisitions and accumulated amortization of deferred leasing costs, and excluding the effect of properties serving as collateral for debt which is in default that we expect to extinguish via conveyance of properties.

Adjusted debt to in-place adjusted EBITDA ratio - Defined as (1) debt, as adjusted to subtract cash and cash equivalents as of the end of the period and debt in default to be extinguished via conveyance of properties, divided by (2) in-place adjusted EBITDA (defined below) for the three month period that is annualized by multiplying by four.

Adjusted EBITDA – net income (loss) adjusted for the effects of interest expense, depreciation and amortization, impairment losses, gain on sales of properties, gain or loss on early extinguishment of debt, net gain on unconsolidated entities, operating properties acquisition costs, loss on interest rate derivatives and income taxes, and excluding the effect of properties serving as collateral for debt which is in default that we expect to extinguish via conveyance of such properties.

ATFP – Anti-terrorism force protection.

Baltimore/Washington Region (or B/W Region) – includes counties that comprise the Baltimore/Washington Corridor and the Washington, DC-Capitol Riverfront. As of September 30, 2014, 94 of COPT’s properties were located within this defined region. Please refer to page 11 of COPT’s Supplemental Information package dated September 30, 2014 for additional detail.

BRAC – Base Realignment and Closure Commission of the United States Congress. The Congress established the 2005 BRAC Commission to ensure the integrity of the base closure and realignment process. The Commission provided an objective, non-partisan, and independent review and analysis of the list of military installation recommendations issued by the Department of Defense (DOD) on May 13, 2005. The Commission's mission was to assess whether the DoD recommendations substantially deviated from the Congressional criteria used to evaluate each military base. While giving priority to the criteria of military value, the Commission took into account the human impact of the base closures and considered the possible economic, environmental, and other effects on the surrounding communities.

C4ISR – Command, Control, Communications, Computers, Intelligence, Surveillance, Reconnaissance

20

A. Definitions & Glossary

20

Cloud computing infrastructure – per Wikipedia, Cloud computing is computation, software, data access, and storage services that do not require end-user knowledge of the physical location and configuration of the system that delivers the services. Parallels to this concept can be drawn with the electricity grid where end-users consume power resources without any necessary understanding of the component devices in the grid required to provide the service.

Contractor Tail – the estimated number of contractor employees that likely will be required to support a government agency.

Core Portfolio – operating properties held for long-term investment.

Core tenant – office and data center tenants in the United States Government and defense information technology (“Defense IT”) industries.

Customer – how COPT generally refers to its tenants. See also Core tenant, above.

Debt/Adjusted EBITDA – debt, as adjusted to subtract debt in default to be extinguished via conveyance of properties, divided by Adjusted EBITDA for the three month period, multiplied by four.

Debt/Total Market Capitalization – carrying value of our debt, divided by our total market capitalization.

Debt to Adjusted Book – carrying value of our debt, as adjusted to subtract debt in default to be extinguished via conveyance of properties, divided by Adjusted Book, as defined on prior page.

Development profit or yield – calculated as cash NOI divided by the estimated total investment, before the impact of cumulative real estate impairment losses.

DISA – Defense Information Systems Agency

EBITDA – see Adjusted EBITDA

EUL – Enhanced Use Lease

GSA – United States General Services Administration. In July 1949, President Harry Truman established the GSA to streamline the administrative work of the federal government. The GSA’s acquisition solutions supplies federal purchasers with cost-effective high-quality products and services from commercial vendors. GSA provides workplaces for federal employees, and oversees the preservation of historic federal properties. Its policies covering travel, property and management practices promote efficient government operations.

21

A. Definitions & Glossary

21

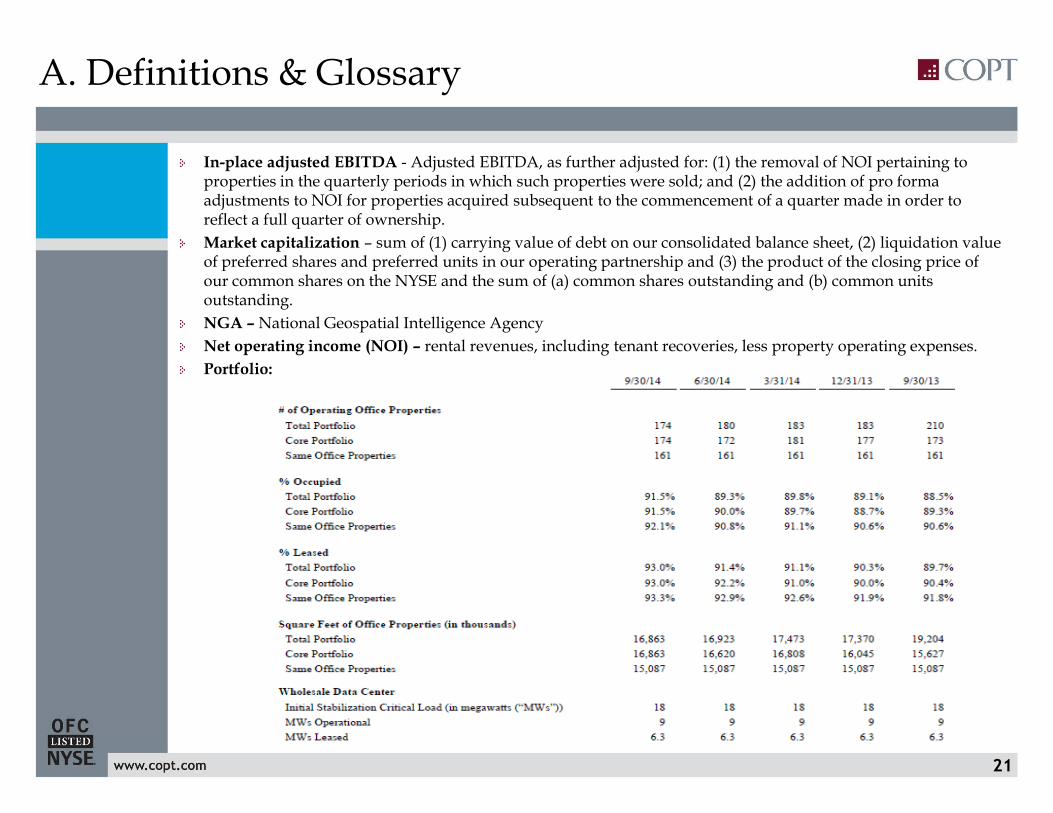

In-place adjusted EBITDA - Adjusted EBITDA, as further adjusted for: (1) the removal of NOI pertaining to properties in the quarterly periods in which such properties were sold; and (2) the addition of pro forma adjustments to NOI for properties acquired subsequent to the commencement of a quarter made in order to reflect a full quarter of ownership.

Market capitalization – sum of (1) carrying value of debt on our consolidated balance sheet, (2) liquidation value of preferred shares and preferred units in our operating partnership and (3) the product of the closing price of our common shares on the NYSE and the sum of (a) common shares outstanding and (b) common units outstanding.

NGA – National Geospatial Intelligence Agency

Net operating income (NOI) – rental revenues, including tenant recoveries, less property operating expenses.

Portfolio:

22

A. Definitions & Glossary

22

Redevelopment – properties previously in operations on which activities to substantially renovate such properties are underway.

SCIF - a Sensitive Compartmented Information Facility, or “SCIF,” in U.S. military, security and intelligence parlance is an enclosed area within a building that is used to process classified information within formal access controlled systems (as established by the Director of National Intelligence).

Stabilization – generally defined as properties that are at least 90% occupied.

Strategic Tenant Properties – office properties held for long-term investment located near defense installations and other knowledge-based government demand drivers, or that were otherwise at least 50% leased as of most recent year end by United States Government agencies or defense contractors.

Under construction – properties under active construction and properties that we are contractually committed to construct.

23

B. Reconciliations

23

For the Three For the Three

(Dollars in thousands) Months Ended Months Ended

December 31, 2013 March 31, 2011

Reconciliation of GAAP net income (loss) to adjusted earnings before interest, income taxes,

depreciation and amortization ("Adjusted EBITDA") and in-place adjusted EBITDA

Net income (loss) 92,672$ (18,566)$

Interest expense on continuing and discontinued operations 23,181 26,928

Total income tax expense (benefit) 1,917 (544)

Depreciation and amortization 31,817 33,645

Impairment losses 921 27,742

Gain on early extinguishment of debt on continuing and discontinued operations (67,808) -

Gain on sales of operating properties (9,004) (2,701)

Net loss on investments in unconsolidated entities included in interest and other income 221 (538)

Operating property acquisition costs - 23

Adjusted EBITDA 73,917$ 65,989$

NOI from properties in quarter of disposition (5,107) -

In-place adjusted EBITDA 68,810$ 65,989$

12/31/13 3/31/11

Total Assets 3,629,952$ 3,865,809$

Accumulated depreciation 597,649 526,825

Accumulated amort. of real estate intangibles and deferred leasing costs 193,142 176,406

Denominator for debt to adjusted book 4,420,743$ 4,569,040$

Total Debt 1,927,703$ 2,396,795$

Less: Cash and cash equivalents (54,373) (12,606)

Numerator for adjusted debt to in-place adjusted EBITDA ratio 1,873,330$ 2,384,189$

Debt to adjusted book 43.6% 52.5%

Adjusted debt to in-place adjusted EBITDA ratio (1) 6.8x 9.0x

(1) Computed based on annualized in-place adjusted EBITDA for three months ended.

24

C. Safe Harbor

Unless otherwise noted, information in this presentation represents the Company’s consolidated portfolio as of or for the quarter ended September 30, 2014.

Defined terms for Non-GAAP measures used throughout may be found in the Disclosure. In addition, Reconciliations of Non-GAAP measures to the most comparable GAAP measures are included in the Disclosure.

This presentation may contain “forward-looking” statements, as defined in Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, that are based on the Company’s current expectations, estimates and projections about future events and financial trends affecting the Company. Forward-looking statements are inherently subject to risks and uncertainties, many of which the Company cannot predict with accuracy and some of which the Company might not even anticipate. Accordingly, the Company can give no assurance that these expectations, estimates and projections will be achieved. Future events and actual results may differ materially from those discussed in the forward-looking statements.

Important factors that may affect these expectations, estimates, and projections include, but are not limited to:

• general economic and business conditions, which will, among other things, affect office property and data center demand and rents, tenant creditworthiness, interest rates, financing availability and property values;

• adverse changes in the real estate markets, including, among other things, increased competition with other companies; and

• governmental actions and initiatives, including risks associated with the impact of a government shutdown or budgetary reductions or impasses, such as a reduction in rental revenues, non-renewal of leases, and/or a curtailment of demand for additional space by strategic customers.

The Company undertakes no obligation to update or supplement any forward-looking statements. For further information, please refer to the Company’s filings with the SEC.