corporate presentation november 2019 · corporate presentation november 2019 ... ibancar started...

TRANSCRIPT

1

Corporate Presentation November 2019

Over the past years Ibancar has designed and refined a business model that:

- Applies a broad consumer credit market positioning strategy- Encompasses the entire spectrum of borrower profiles, from prime to the credit invisible- Integrates modern digital marketing techniques for lead acquisition and processing- Is 100% online and does not require physical presence of the borrower nor the car- Allows a fast and simple application process that can be completed entirely from a smartphone- Generates excellent results with high annual returns- Is profitable with no credit losses

After several years of development Ibancar can capitalise on its existing footprint and is serving the entire consumer credit market, evolving into a new type of lender - offering loans that are:

- Simple, ethical and well understood- As fast and as easy to transact as payday loans but without the inherent marketing challenges- As secure as title lending

Ibancar is bringing secured lending into the mainstream consumer credit market through its proprietary digital lending platform.

Ibancar has redesigned the outdated “car title” loan model and made it scalable for use in the huge online alternative lending space.

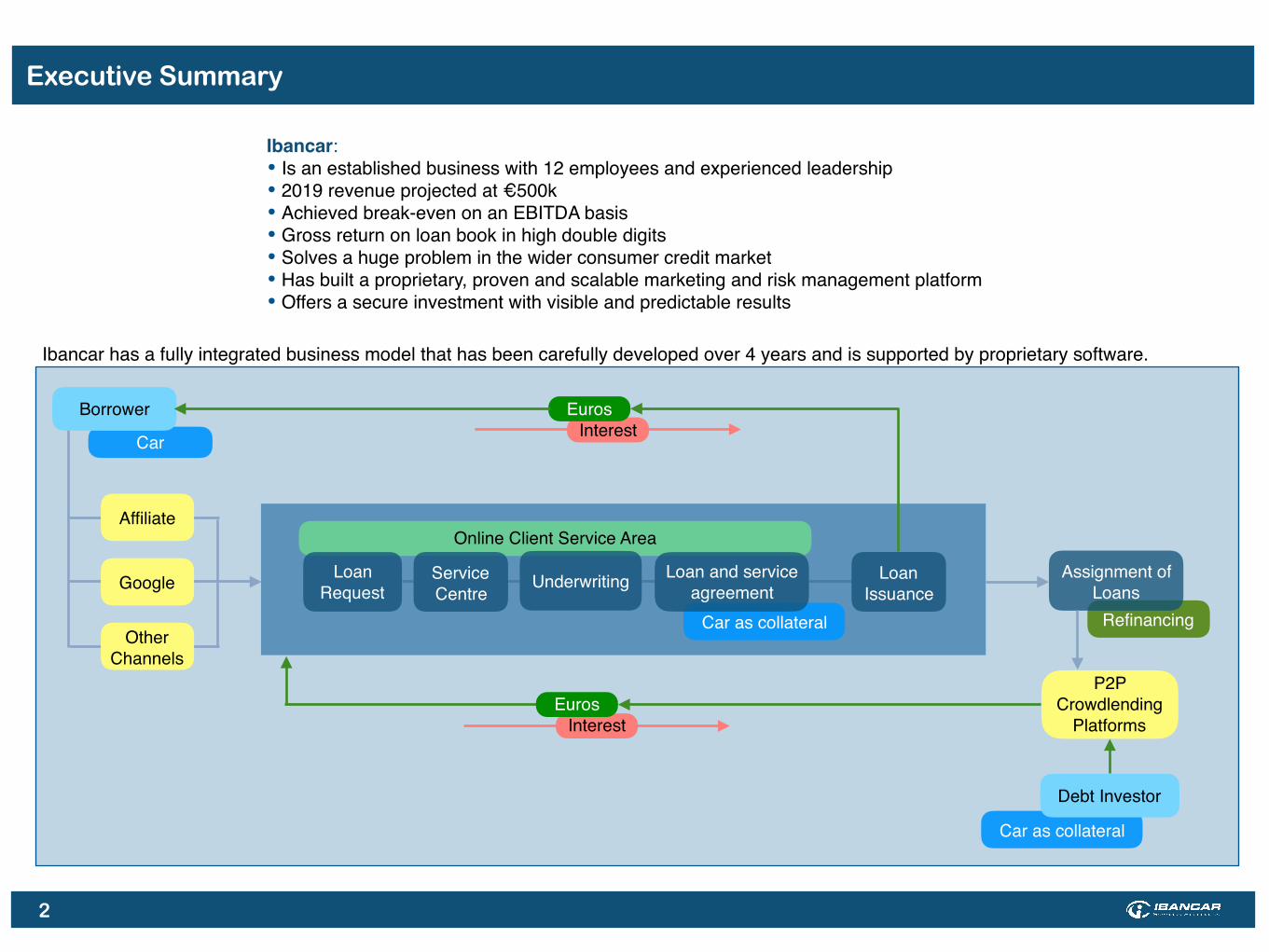

Refinancing

Car

Car as collateral

2

P2P Crowdlending

Platforms

Ibancar has a fully integrated business model that has been carefully developed over 4 years and is supported by proprietary software.

Debt Investor

Interest

Interest

Assignment of Loans

Online Client Service Area

Car as collateral

Loan Issuance

Loan Request

Service Centre

Loan and service agreementUnderwriting

Borrower

Affiliate

Other Channels

Euros

Euros

Executive Summary

Ibancar:• Is an established business with 12 employees and experienced leadership• 2019 revenue projected at €500k• Achieved break-even on an EBITDA basis• Gross return on loan book in high double digits• Solves a huge problem in the wider consumer credit market • Has built a proprietary, proven and scalable marketing and risk management platform • Offers a secure investment with visible and predictable results

Ibancar, a Growth Stage Company Maturing into Full Scalability

Ibancar started working on its business model in 2015 and the team has been working continuously to develop a hugely scalable platform that offers better and more suitable loans to its clients at the same time as it offers higher and safer returns to investors.

To date the business has been self funded and grown organically at a pace that has enabled us to develop, test and fine tune the model and all its variables.

3

€2.0m cumulative

lending

returns in high double

digits

Zero credit losses

4 years of product

developmentNPLs below 9%

Recovery Rate above

100%

Revenue hits €280k

Dec 2018Cumulative lending

hits €1m

May 2018Successful refinancing on

P2P platforms

Mar 2019

Trial of P2P funding

Oct 2018Projected 2019 revenue €500k

Nov 2019

First affiliate trials

Jan 2018

7th affiliate API connection

Jul 2018

Potential monthly backlog reaches 13,000 leads

Apr 2019

Trials of lead processing via WhatsApp Messenger

Jul 2019

First 7 loans issued

Jul 2014100th loan

issued

Mar 2016

450th loan issued

Feb 2019

Record lending month €95k

Oct 2019

Lending

Marketing

Financial

over 600 issued loans

Problems in the Consumer Credit Market Affect all Borrowers Whether Prime, Subprime, Underbanked or Credit Invisible

In our post financial crisis world getting a loan has become impossible for many - there are millions of consumers who do not have access to any form of credit because regulation, compliance and risk have changed forever. Of the worlds population 35% are credit invisible and outside the formal financial system and some 2 billion working age adults are unbanked or underbanked. This has created a need for alternative lenders and the use of collateral brings these potential borrowers into the market.For many others, whether prime or subprime, the only way to obtain a fast loan is to turn to a payday lender but these do not always offer what the borrower needs as they lend only small amounts for short periods at rates that exceed 800% and need to be redeemed or renewed monthly. A borrower who wants several thousand euros has very few online options as alternative lenders are reticent to offer larger amounts in the online market where non performing loan rates can exceed 35% and capital recovery is slow and uncertain. With its fast, simple, collateralised online loans Ibancar can serve the entire market.

4

Online consumer lending in Europe is largely unsegmented, there is little distinction made between prime and suprime, and the key selling points are speed, size and ease.

In Spain for example only few consumers have a CIRBE (credit score). Participating financial institutions only report to the database when a single client owes over €9,000 and consulting the database requires the authorisation of the client. This means borrowers can have large debts that the market does not know about because they are spread over several lenders at or are below €9,000.On the other hand missed payments ARE almost always reported into the RAI or ASNEF EQUIFAX system and these are consulted unilaterally by all credit institutions and even the smallest black mark excludes the borrower from the lending market.

This system has several consequences:• It is based on negative scores• A positive credit history is not generally taken into account• Loan approval rates are below 40%

Most borrowers, whether prime or subprime apply to the same lenders end

up paying a similar rate

Prime

Subprime

Underbanked

Credit Invisible

The trend is clear: the entire spectrum of borrowers is relying less on banks because they do not offer the easy 100% online experience and fast response times so they turn to alternative lenders despite the higher interest rates.Borrowers who need a loan for an unplanned expense or an impulsive purchase or to get out of trouble do not differentiate, they just want their problem solved and they go online to do so.

5

In the US, the Federal Deposit Insurance Commission estimates that 20 percent of households are underbanked, while the Center for Financial Services Innovation estimated the alternative financial services market serving underbanked consumers to be $78b.

PwC’s research suggests there may be between 10m and 14m people in the UK, around a quarter of the total adult population, who find it difficult to access credit from mainstream sources, despite having only relatively minor blemishes on their credit history.

According to our recent research, over 130 million people are unbanked or underbanked across Europe.

The €25B Spanish consumer credit market is perfect for creative online lenders to further dis-intermediate traditional credit institutions that are slow to adopt modern marketing techniques and remain very bureaucratic. The credit market in Spain is growing faster than other E.U. countries as confirmed in the Q4 review of Consumer Credit by the European Central Bank. The consumer credit market is now equal in size to the mortgage market at approximately €40 billion per year (€25 billion excluding credit cards). Although the annual increase in consumer credit has been above 10% per year since 2013, the market has not yet fully recovered, in 2007 this number was €56 billion.

Prime borrowers are taking out Ibancar loans because:• They think their bank won't lend to them• Their bank does not offer an online process• They believe a bank loan will be slow and complicated to obtain• They don’t like or trust banks

Subprime and Credit Invisible borrowers take out Ibancar loans because:• They don’t have credit cards• There are very few online lenders open to problem borrowers• Payday lenders do not offer what they need• They use the internet to apply simultaneously to multiple lenders

Ibancar Solves these Problems And Makes Every Borrower a Potential Client

Ibancar is Already Solving these Problems in the Spanish Market

And can Solve the Same Problems in Other Countries

The market is huge: In Europe direct personal loans total €80b per year and payday lending is estimated to be €15b.In the USA direct personal loans total €150b per year and payday lending is estimated at €30b per year.

But with secured Ibancar lending the potential in the consumer credit market is actually much bigger than it appears as less than 40% of loan requests are approved - it may be the case that up to half the real market is not being served at all and there is a huge opportunity to bring the Subprime, Underbanked and Credit Invisible into the loan market through secured lending.

Ibancar is Well PositionedLender All in Cost P.A. Maximum Amount

Bank Loans 6% - 14% Only available to “prime” borrowersCredit Cards 18% - 28% Only available to “prime” borrowersOnline Instalment Loan 40% - 80% Only available to “prime” borrowersIbancar 40% - 60% €6,000Pawn Shops 80% - 120% €3,000Payday Loans 400% - 1200% €500

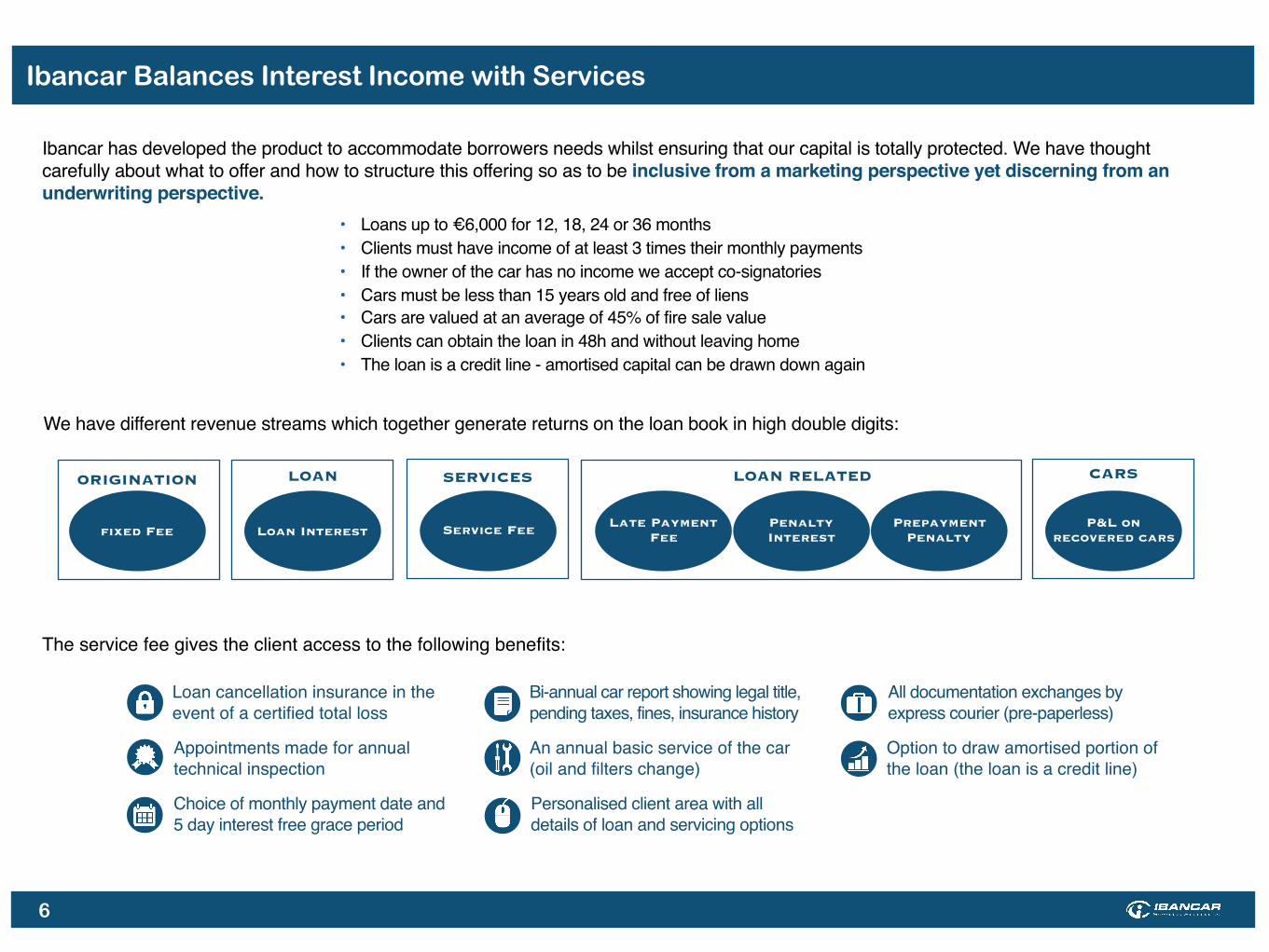

CARSSERVICESLOANORIGINATION LOAN RELATED

Ibancar Balances Interest Income with Services

Loan cancellation insurance in the event of a certified total loss

An annual basic service of the car (oil and filters change)

Appointments made for annual technical inspection

Personalised client area with all details of loan and servicing options

Bi-annual car report showing legal title, pending taxes, fines, insurance history

Option to draw amortised portion of the loan (the loan is a credit line)

All documentation exchanges by express courier (pre-paperless)

Choice of monthly payment date and 5 day interest free grace period

The service fee gives the client access to the following benefits:

We have different revenue streams which together generate returns on the loan book in high double digits:

• Loans up to €6,000 for 12, 18, 24 or 36 months• Clients must have income of at least 3 times their monthly payments• If the owner of the car has no income we accept co-signatories• Cars must be less than 15 years old and free of liens • Cars are valued at an average of 45% of fire sale value• Clients can obtain the loan in 48h and without leaving home• The loan is a credit line - amortised capital can be drawn down again

Ibancar has developed the product to accommodate borrowers needs whilst ensuring that our capital is totally protected. We have thought carefully about what to offer and how to structure this offering so as to be inclusive from a marketing perspective yet discerning from an underwriting perspective.

Late Payment FeeLoan Interest Service Feefixed Fee

Penalty Interest

Prepayment Penalty

6

P&L on recovered cars

Ibancar Operates Ethically to Support the Financial Wellbeing of its Clients

Being a responsible and ethical lender in this sector goes beyond numbers and percentages - we have to price our loans so that they:

• Reflect the credit profile of the average borrower• Remain attractive in comparison to alternatives • Allow us to build a sustainable business

We have both an economic and a social purpose because the cheapest forms of credit are simply not available to the majority of borrowers and many more have either been totally excluded from the market or only have access to loans at rates in excess of 100% p.a.

Our goal is to be a responsible lender in a sector where there is great need and we remain very aware that many of our clients are experiencing financial difficulties. Putting our clients in an even worse financial situation will not benefit us so we believe it is imperative to operate ethically and our culture and processes are firmly rooted in this philosophy. This applies to how products are structured and priced but, more importantly, how NPLs are managed.

Our business is not primarily about collateral, it is about psychology. With a traditional loan the “worry” remains with the lender but with a secured loan this “worry” is transferred to the borrower. Our role is to help

our clients obtain credit and then to help them maintain the ownership of their car.

7

TRANSACTABILITY

The only 100% online service Loan available in 48 hours all from home

No change of ownership of the car

FLEXIBILITY

Flexible payment dates payment holidays 2x per year

Drawdown amortised capital again

SUPPORTIVE CREDIT MANAGEMENT

Always attempt restructuring before escalation Do not attempt to profit from collateral Never been to court to resolve dispute

TRANSPARENCY

Only lender offering fast loans longer than 1m Only lender offering amortising loans

ACCEPTANCE

Cars up to an age of 15 years Accept bad credit history

Accept retired / self employed Consider family income

Accept bad credit history

Product and Credit Process Carefully Developed To Ensure the Predictability of Returns and Recovery of Capital

We have developed our own credit scoring process and combine technical and behavioural analysis - this means human factors have an impact on our credit decisions.

We verify the condition and value of the collateral first, ensuring that after we have received dated photographs of the car, that is taxed, insured, free of finance and liens and generally road legal. If the collateral is acceptable we look at the borrower. Our base scenario is acceptance and our scoring works with LTV reduction criteria which ensure that there remains enough free equity in the car to encourage the borrower to pay the instalments.

We value the cars according to tables published quarterly by “GANVAM” (National Association of Car Dealers). The maximum LTV offered to the borrower increases with the value of the car. Currently the maximum LTV is based on the average purchase price paid by dealers for that specific brand, model and year. We then adapt this maximum loan amount to take into account the borrowers monthly income.

Current loan book LTV is 43%

8

• Value of the collateral • Ability to repay• Online / social network profile

In this context it is important to note that Ibancar only started using public registered liens in 2018 and although this did not improve the outcome of our NPLs we intend to keep using them as they have at least as much psychological as technical value - the borrower always signs the official registry forms with the knowledge that a lien will be registered and as part of our loan agreement he also signs a contractual lien agreeing not to sell the vehicle until the loan is repaid.It is our objective to have 85% of loans backed by a successfully registered lien at any time.

Our underwriting process does not result in a binary “yes” or “no” and we do not use interest rates to compensate for perceived risk on a case by case basis. Instead we ask ourselves how much should we lend to this borrower based on the following criteria:

Once a loan is issued we register a lien (“reserva de dominio”) against the car in the public registry which is intended to prevent the borrower from selling the car. If there is already a lien registered against the vehicle we turn down the loan application.

• Behaviour• Credit history • Employment status

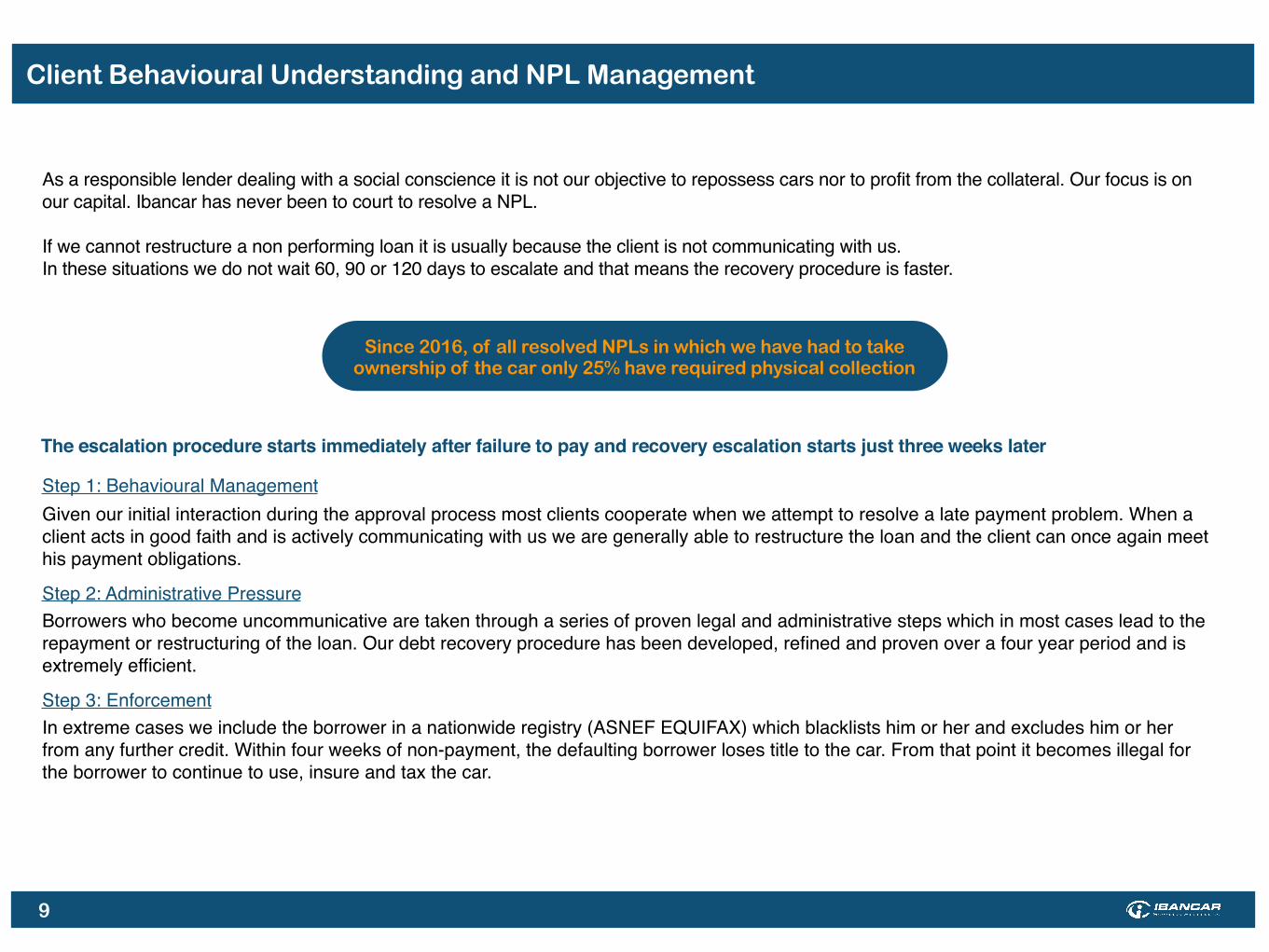

Client Behavioural Understanding and NPL Management

As a responsible lender dealing with a social conscience it is not our objective to repossess cars nor to profit from the collateral. Our focus is on our capital. Ibancar has never been to court to resolve a NPL.

If we cannot restructure a non performing loan it is usually because the client is not communicating with us. In these situations we do not wait 60, 90 or 120 days to escalate and that means the recovery procedure is faster.

Step 3: EnforcementIn extreme cases we include the borrower in a nationwide registry (ASNEF EQUIFAX) which blacklists him or her and excludes him or her from any further credit. Within four weeks of non-payment, the defaulting borrower loses title to the car. From that point it becomes illegal for the borrower to continue to use, insure and tax the car.

Borrowers who become uncommunicative are taken through a series of proven legal and administrative steps which in most cases lead to the repayment or restructuring of the loan. Our debt recovery procedure has been developed, refined and proven over a four year period and is extremely efficient.

Step 2: Administrative Pressure

Given our initial interaction during the approval process most clients cooperate when we attempt to resolve a late payment problem. When a client acts in good faith and is actively communicating with us we are generally able to restructure the loan and the client can once again meet his payment obligations.

Step 1: Behavioural Management

Since 2016, of all resolved NPLs in which we have had to take ownership of the car only 25% have required physical collection

The escalation procedure starts immediately after failure to pay and recovery escalation starts just three weeks later

9

Loan Book Zoom Use of Collateral and Proactive Credit Management Generate Positive Outcomes

As a result of the proactive credit process Ibancar maintains an exceptionally high rate of capital recovery. Our main aim is always to protect capital and we prefer to push for capital to be returned quickly, even with zero yield, instead of going through lengthy recovery processes. We seek quick resolutions and when these are not possible we escalate quickly. Our use of collateral means a non performing loans does not necessarily imply a loss.

47.67%

1.5%

4 Legacy NPLs

10

(All 600 Issued Loans) (All 600 Loans minus 275 Still Active Loans)

22 NPLs on 01/11/19

Loan Book Zoom Historical Resolved Non Performing Loans

Having issued over 600 loans over 4 years Ibancar has accumulated credit profits resulting from an above par recovery rate. Our clients need their cars and even if they are unable to keep up contractual payments a new payment schedule can usually be agreed. Repossession is a last resort and we do not aim to profit from the cars. We approach every NPL with the desire to agree an amicable solution.

26 NPL cars sold

141 Days Average

600 loans issued

123% capital recovery rate

Non performing loans affect our yield and our cash flow but have not affected our overall capital recovery rate

11

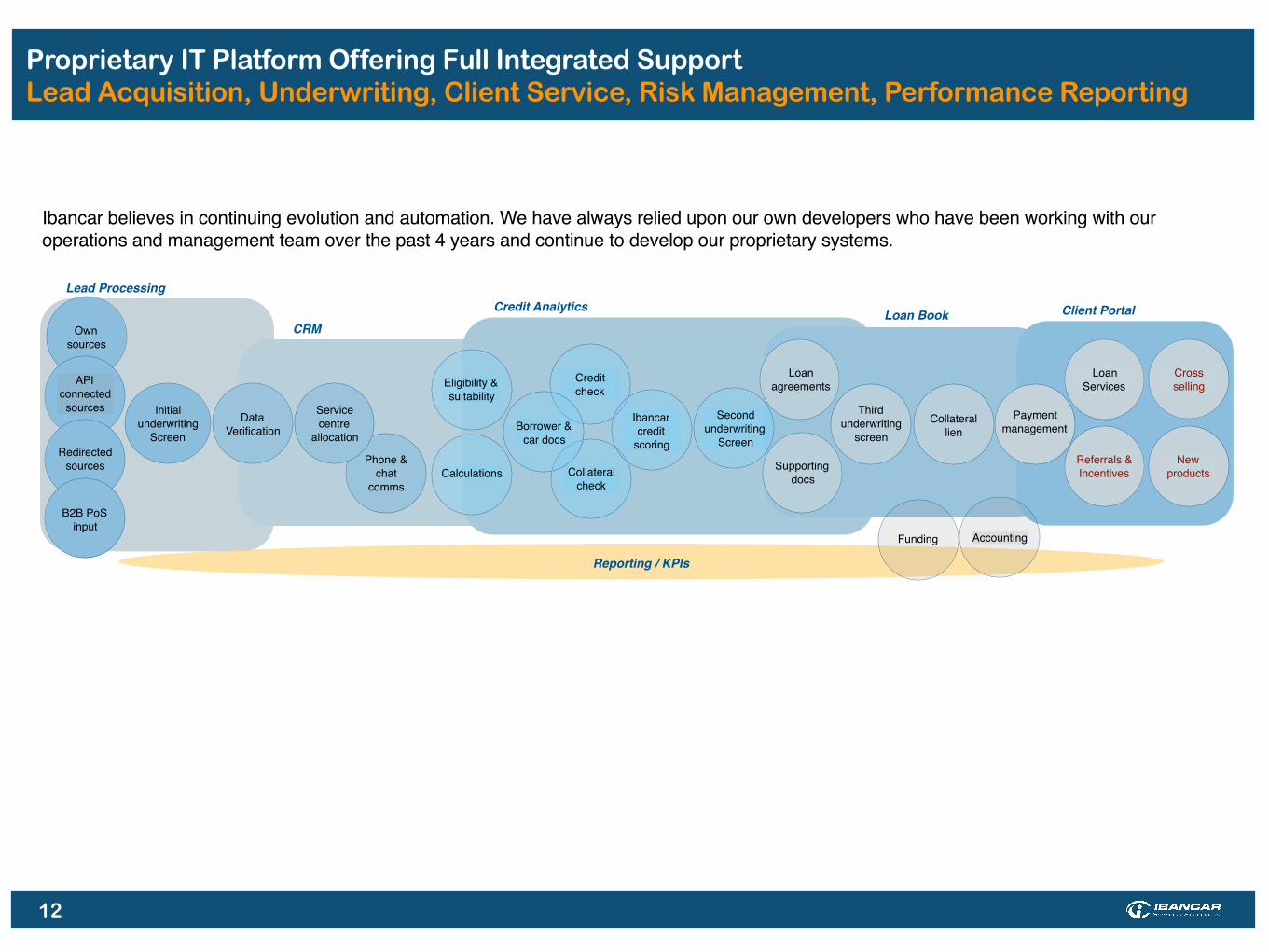

Proprietary IT Platform Offering Full Integrated Support Lead Acquisition, Underwriting, Client Service, Risk Management, Performance Reporting

Ibancar believes in continuing evolution and automation. We have always relied upon our own developers who have been working with our operations and management team over the past 4 years and continue to develop our proprietary systems.

Referrals & Incentives

Own sources

Initial underwriting

Screen

API connected sources

Client PortalLead Processing

Loan Services

CRMCredit Analytics Loan Book

Phone & chat

comms

Eligibility & suitability

Second underwriting

Screen

Data Verification

Credit check

Collateral check

Third underwriting

screen

Loan agreements

Supporting docs

Ibancar credit

scoring

Collateral lien

Payment management

Calculations

Borrower & car docs

Cross selling

New products

Reporting / KPIs

AccountingFunding

Redirected sources

B2B PoS input

Service centre

allocation

12

The Team

Senior management brings both in depth finance and corporate expertise.

Founder & CEOAlexander Melis (Dutch) is an ex investment banker who was MD in Fixed Income at Credit Suisse and BNP Paribas. Prior to his banking career Alex spent 10 years working as a management consultant and besides his financial knowledge brings management and organisational skills to the table.Contact: [email protected]

Full profiles are available on LinkedIn

The IBANCAR team leadership consists mainly of women and this is considered by some to be a key part of our success. All key team members are equity incentivised and have spent an average of 3 years at the company

General ManagerEster Ruiz Nuñez

Financial ControllerZenobia Ruiz

Senior DeveloperJose C

DeveloperJavi N

Underwriting

AccountantPedro C

Operations ManagerAna G

Customer ServiceDani M

Customer ServiceMercedes M

Javi R

13

Board Member, Non Executive DirectorRoger Welsch (Dutch) is a Director at ING Investment Bank. Previously he was involved in Treasury management at Dutch public sector bank BNG. He is fixed income specialist with 25 years experience of debt capital markets, derivatives and debt structuring. Alex and Roger have known each other for 20 years.Contact: [email protected]

To be appointed

Contact: @ibancar.com

Board Member, Non Executive Director