corporate profile - union bank of colombo...4.9% 2.9% 2.6% 3.2% 5.4% 1h 14 1h 15 1h 16 1h 17 1h 18...

TRANSCRIPT

1

2

Overview

* Adjusted for excess capital and legacy non core investment

Strong foundation built over 24+ years

Robust financial and operational performance

H1 PBT up 52% YoY; Adjusted* ROE of 15%

Improved performance despite challenging operating

environment for the banking sector

Received “Best Cash Management Bank Sri Lanka” at Global

Business Outlook Awards 2019

Superior asset quality & healthy capital adequacy

Ratings upgrade received in May 2019

CAR of 17.23% as at June 2019

Strategic building blocks for delivering best in class ROE:

Above market growth

Best in class Retail & SME franchise

Digitization & Innovation

CASA growth

Stable shareholder base and experienced management team

3

Corporate profile

A strong foundation

• 67 Branches

• 121 ATMs

• Sales Force

• 24Hr Contact Center

• Digital Banking

• Competitive product

range

24 Years

Robust risk

framework

Superior

Asset quality

Strong

Capitalisation

Rating upgrade

in 2019 by Fitch

BBB -lka

Experienced board &

management team

Corporate

Governance

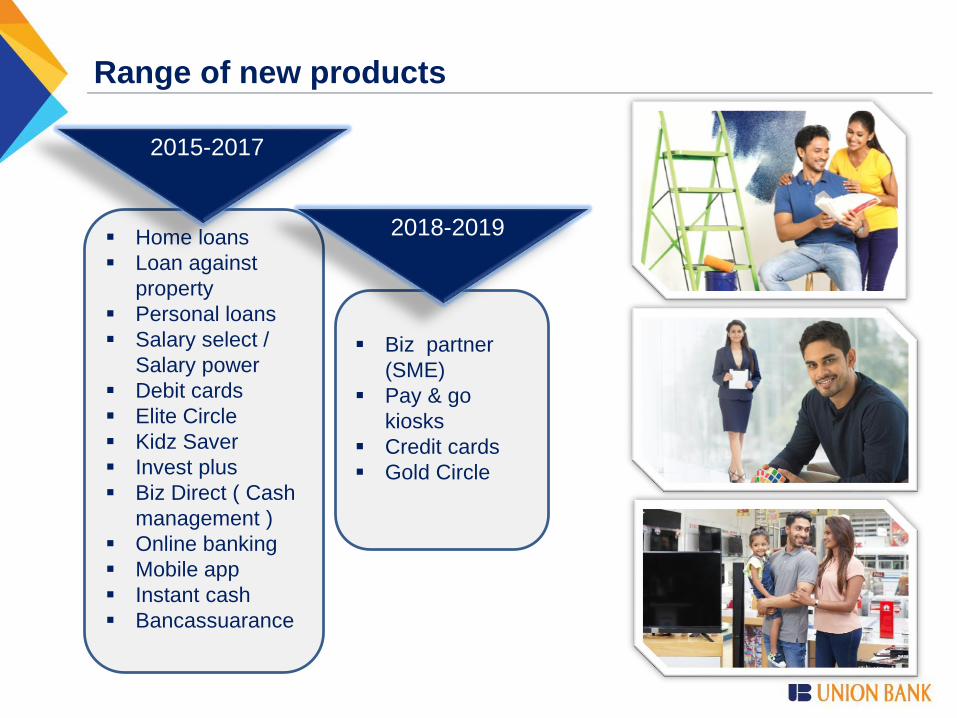

Range of new products

Home loans

Loan against

property

Personal loans

Salary select /

Salary power

Debit cards

Elite Circle

Kidz Saver

Invest plus

Biz Direct ( Cash

management )

Online banking

Mobile app

Instant cash

Bancassuarance

Biz partner

(SME)

Pay & go

kiosks

Credit cards

Gold Circle

2015-2017

2018-2019

Technology & convenience

Online

Banking

Mobile

App

24hrCall Center

4000+

ATMS

POS

Web &

Social Media

Pay &

Go

KiosksVISA

Pay Wave

Best Cash Management Bank

Sri Lanka

Global Business Outlook Awards 2019

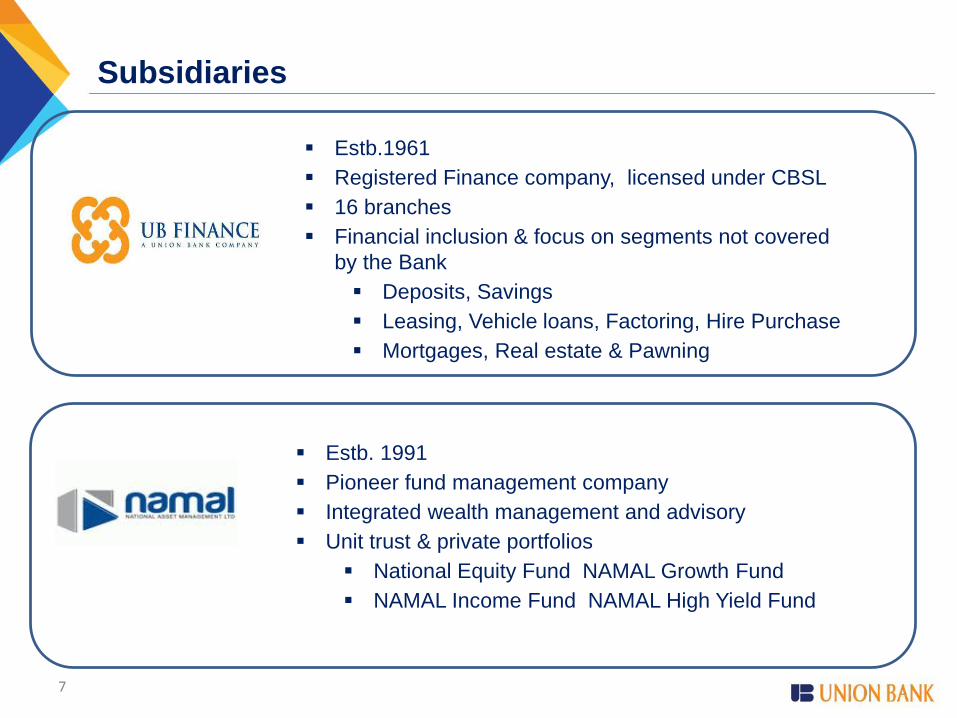

Subsidiaries

7

Estb.1961

Registered Finance company, licensed under CBSL

16 branches

Financial inclusion & focus on segments not covered

by the Bank

Deposits, Savings

Leasing, Vehicle loans, Factoring, Hire Purchase

Mortgages, Real estate & Pawning

Estb. 1991

Pioneer fund management company

Integrated wealth management and advisory

Unit trust & private portfolios

National Equity Fund NAMAL Growth Fund

NAMAL Income Fund NAMAL High Yield Fund

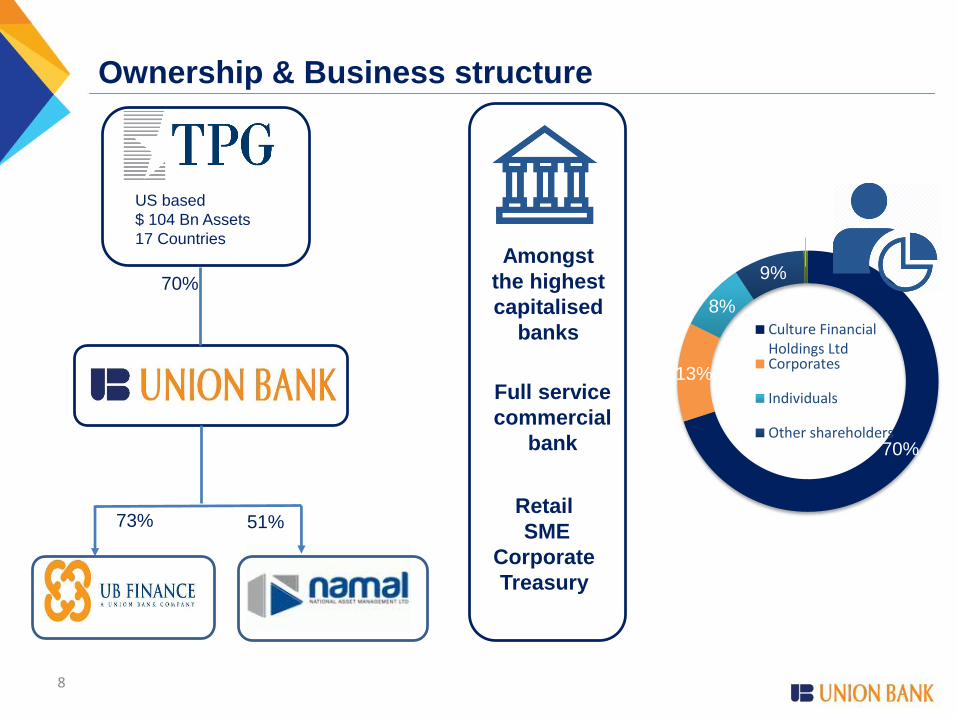

Ownership & Business structure

8

70%

70%

13%

8%

9%

1%

Culture FinancialHoldings LtdCorporates

Individuals

Other shareholders

Full service

commercial

bank

Retail

SME

Corporate

Treasury

Amongst

the highest

capitalised

banks

US based

$ 104 Bn Assets

17 Countries

73% 51%

9

Business Environment

Banking sector

Source: CBSL

13.8%

21.2%17.7%

16.2%19.4%

-0.5%-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

3,000

4,000

5,000

6,000

7,000

8,000

2014 2015 2016 2017 2018 1Q 2019

Net Loans

Net Loans (Rs.Bn) Net loans Growth (%)

12.4%

15.3%16.5%

17.5%

14.8%

1.0%0.00%

5.00%

10.00%

15.00%

20.00%

0

2,000

4,000

6,000

8,000

2014 2015 2016 2017 2018 1Q 2019

Deposits

Deposits (Rs.Bn) Deposit Growth (%)

30.3%

18.1%

7.4% 8.2% 7.4%

0.1%0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

0

500

1,000

1,500

2,000

2,500

3,000

2014 2015 2016 2017 2018 1Q 2019

CASA

CASA (Rs.Bn) CASA Growth (%)

Sri Lanka banking sector witnessing challenges on growth and asset quality

4.2%

3.2%

2.6% 2.5%

3.4%

4.2%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

50

100

150

200

250

300

350

2014 2015 2016 2017 2018 1Q 2019

Gross NPA & NPL ratio

Gross NPA (Rs.Bn) Gross NPL Ratio (%)

Source: CBSL

-4%

39%

11%

12%

18%

13%

-

20

40

60

80

100

120

1Q 2014 1Q 2015 1Q 2016 1Q 2017 1Q 2018 1Q 2019

NII

NII (Rs.Bn) NII Growth (%)

-5% -6%

8%15%

31%

-20% -

10

20

30

40

1Q 2014 1Q 2015 1Q 2016 1Q 2017 1Q 2018 1Q 2019

Non Interest Income

Non Interest Income Non Interest Income G (%)

35%

163%

-18%-5%

92%

63%

-

2

4

6

8

10

12

1Q 2014 1Q 2015 1Q 2016 1Q 2017 1Q 2018 1Q 2019

Impairment

Impairment Impairment G (%)

-16%

21%

-2%

39%

23%

-11% -

20

40

60

80

1Q 2014 1Q 2015 1Q 2016 1Q 2017 1Q 2018 1Q 2019

Profit Before all Taxes

PBT PBT G (%)

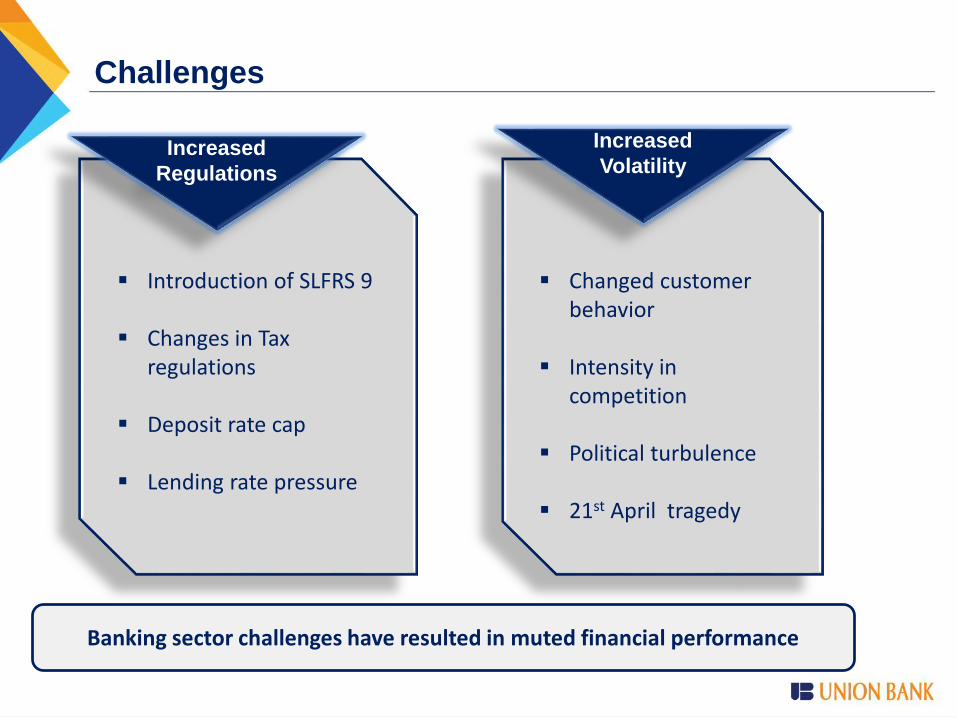

Banking sector Contd….

Banking sector challenges have resulted in muted financial

performance for banks

Challenges

Introduction of SLFRS 9

Changes in Tax regulations

Deposit rate cap

Lending rate pressure

Changed customer behavior

Intensity in competition

Political turbulence

21st April tragedy

Banking sector challenges have resulted in muted financial performance

Increased

VolatilityIncreased

Regulations

13

Financial Performance

Profit After

Tax

Growth YoY

17.5%

Key highlights

Total Capital

Adequacy

Ratio

17.2%

Profit Before

all Taxes

Growth YoY

52.0%

14

CASA

Growth YoY

(Avg)

23.3%

Loans

Growth YoY

(Avg)

7.5%

Deposits

Growth YoY

(Avg)

11.3%

Fitch upgrade

to BBB-

First ever

share buy

back in the

banking

sector

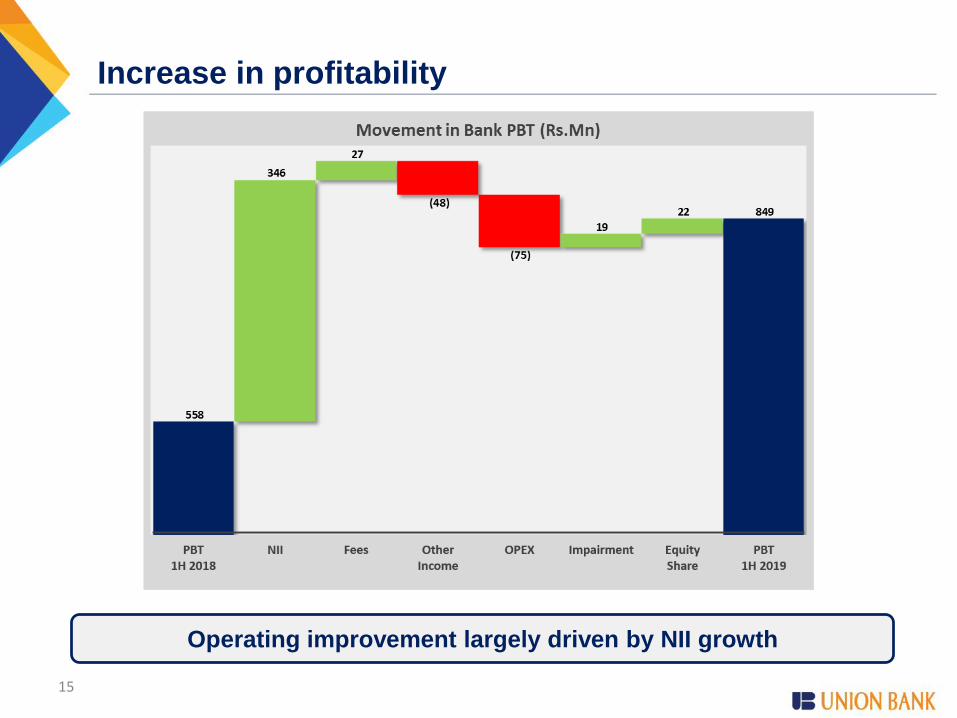

Increase in profitability

C

15

Operating improvement largely driven by NII growth

Growth in assets

16

Bank realigned its loan portfolio amidst volatility in the market

17

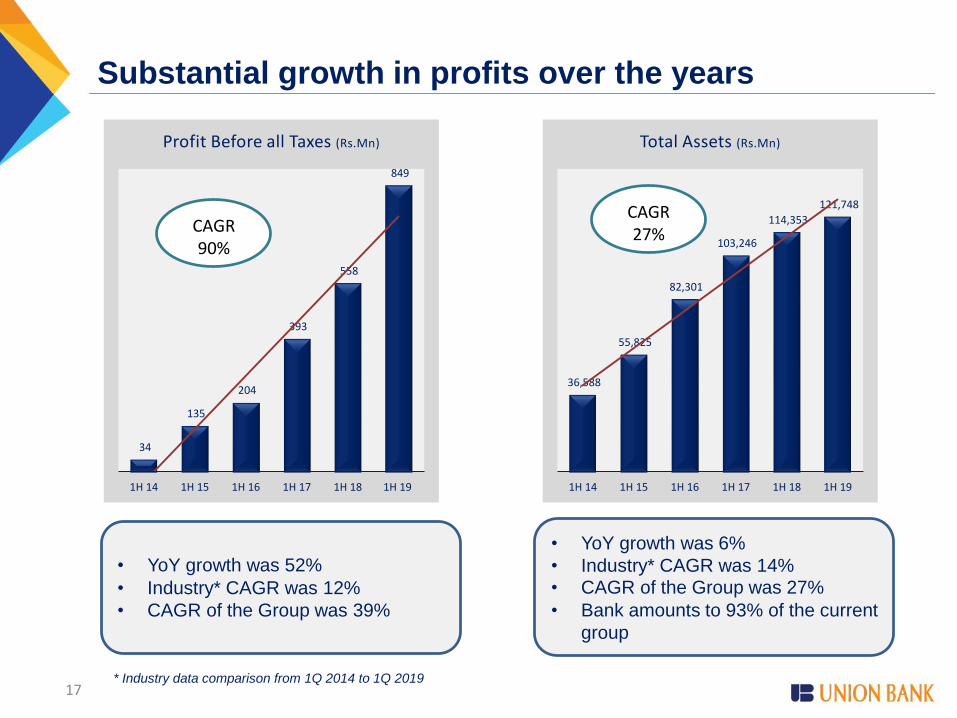

Substantial growth in profits over the years

* Industry data comparison from 1Q 2014 to 1Q 2019

• YoY growth was 52%

• Industry* CAGR was 12%

• CAGR of the Group was 39%

• YoY growth was 6%

• Industry* CAGR was 14%• CAGR of the Group was 27%

• Bank amounts to 93% of the current

group

34

135

204

393

558

849

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Profit Before all Taxes (Rs.Mn)

CAGR90%

36,588

55,825

82,301

103,246

114,353

121,748

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Total Assets (Rs.Mn)

CAGR27%

Increasing Operating Margin

C

18

Effective revenue and cost

management has resulted in

widening jaws

Exponential growth in revenue

Infrastructure investments were done

in the initial stages

-

100

200

300

400

500

600

700

800

900

1,000

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Operating Margin (Rs.Mn)

985 1,350

1,655 2,115

2,575 2,900

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Total Revenue (Rs.Mn)

763

1,108 1,432

1,618 1,899 1,974

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Total Cost (Rs.Mn)

CAGR24%

CAGR21%

19 * Industry data comparison from 1Q 2014 to 1Q 2019

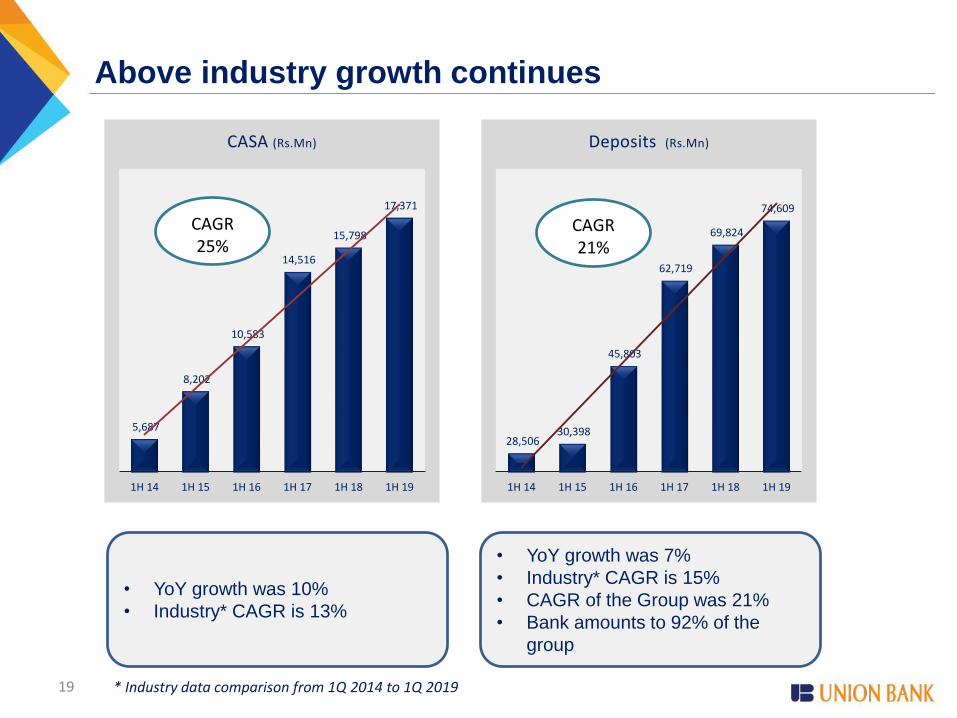

Above industry growth continues

• YoY growth was 10%

• Industry* CAGR is 13%

• YoY growth was 7%

• Industry* CAGR is 15%

• CAGR of the Group was 21%

• Bank amounts to 92% of the

group

5,687

8,202

10,583

14,516

15,798

17,371

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

CASA (Rs.Mn)

CAGR25%

28,506 30,398

45,803

62,719

69,824

74,609

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Deposits (Rs.Mn)

CAGR21%

20

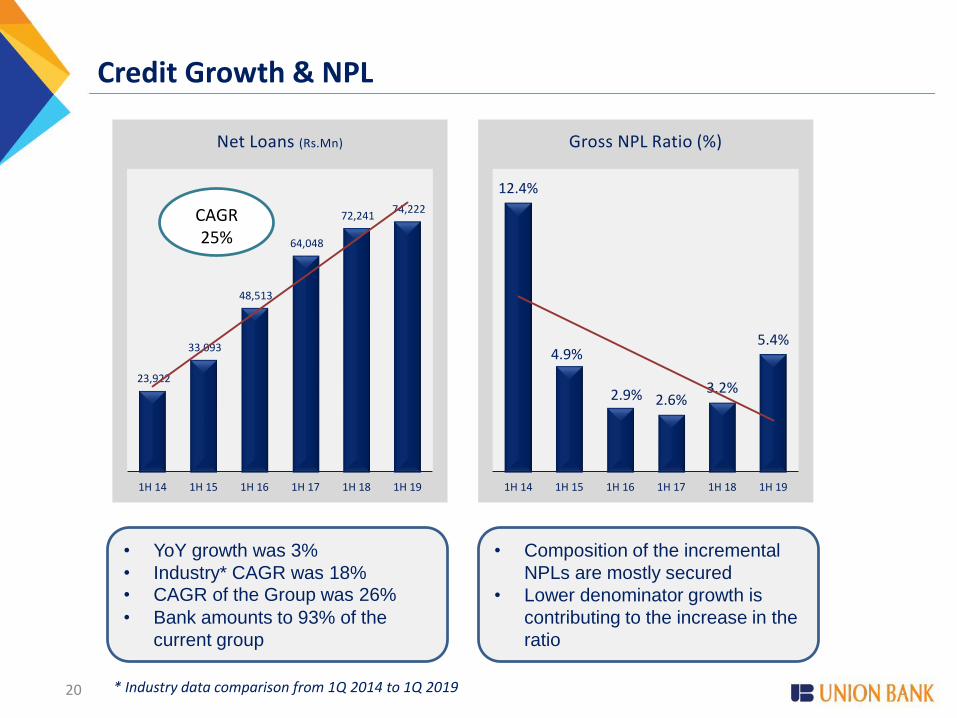

Credit Growth & NPL

12.4%

4.9%

2.9% 2.6%3.2%

5.4%

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Gross NPL Ratio (%)

• YoY growth was 3%

• Industry* CAGR was 18%• CAGR of the Group was 26%

• Bank amounts to 93% of the

current group

• Composition of the incremental

NPLs are mostly secured

• Lower denominator growth is

contributing to the increase in the

ratio

* Industry data comparison from 1Q 2014 to 1Q 2019

23,922

33,093

48,513

64,048

72,241 74,222

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Net Loans (Rs.Mn)

CAGR25%

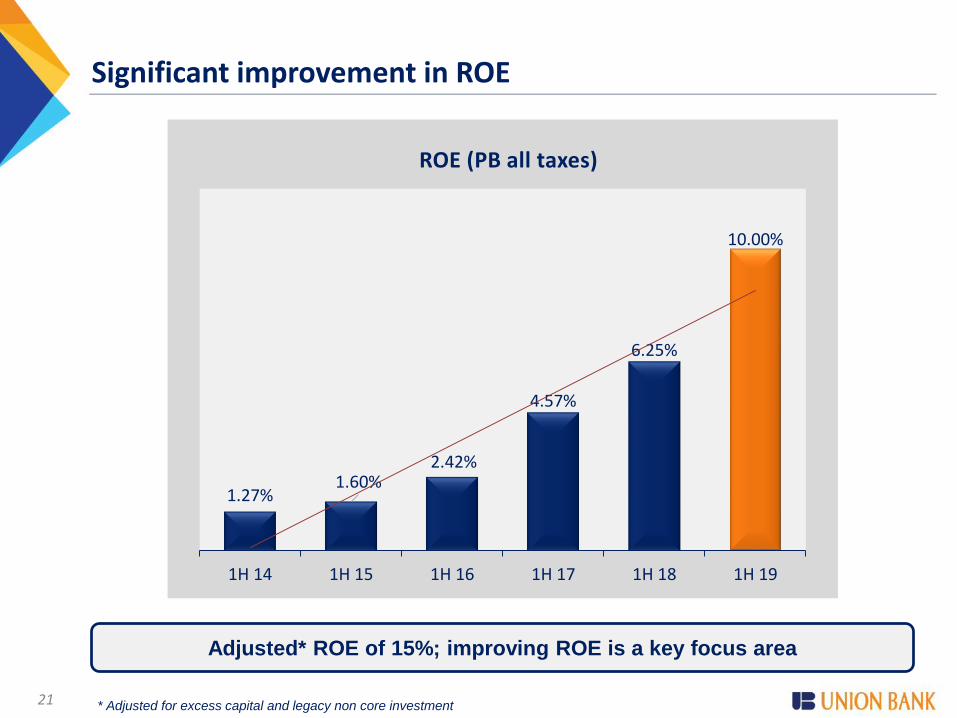

Significant improvement in ROE

21

Adjusted* ROE of 15%; improving ROE is a key focus area

1.27%1.60%

2.42%

4.57%

6.25%

10.00%

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

ROE (PB all taxes)

* Adjusted for excess capital and legacy non core investment

22

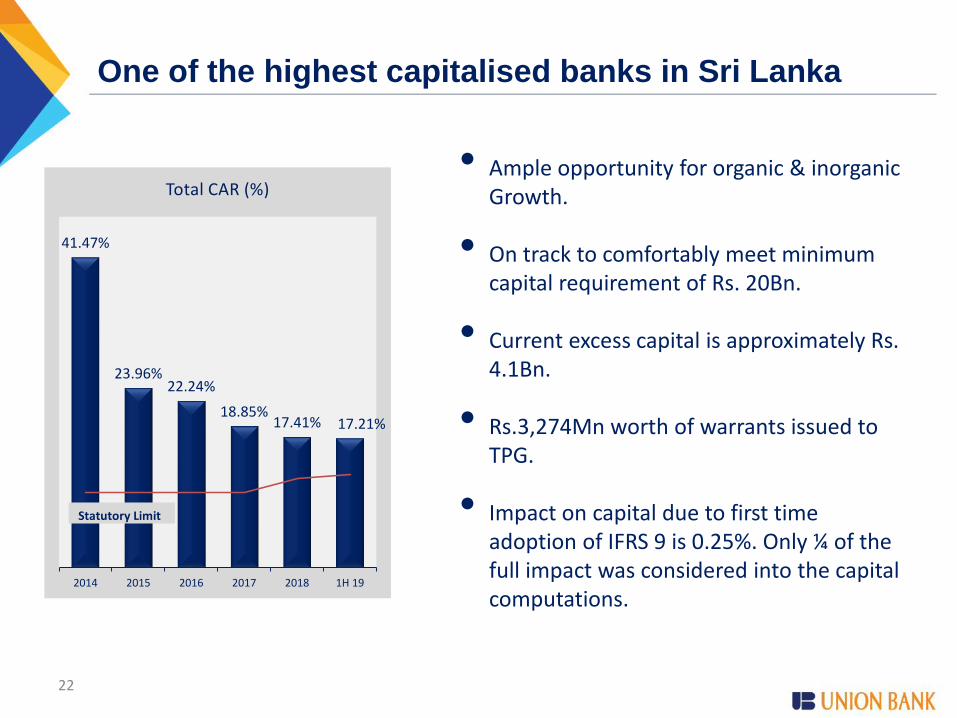

One of the highest capitalised banks in Sri Lanka

• Ample opportunity for organic & inorganic Growth.

• On track to comfortably meet minimum capital requirement of Rs. 20Bn.

• Current excess capital is approximately Rs. 4.1Bn.

• Rs.3,274Mn worth of warrants issued to TPG.

• Impact on capital due to first time adoption of IFRS 9 is 0.25%. Only ¼ of the full impact was considered into the capital computations.

41.47%

23.96%22.24%

18.85%17.41% 17.21%

2014 2015 2016 2017 2018 1H 19

Total CAR (%)

Statutory Limit

23

Strategic Direction

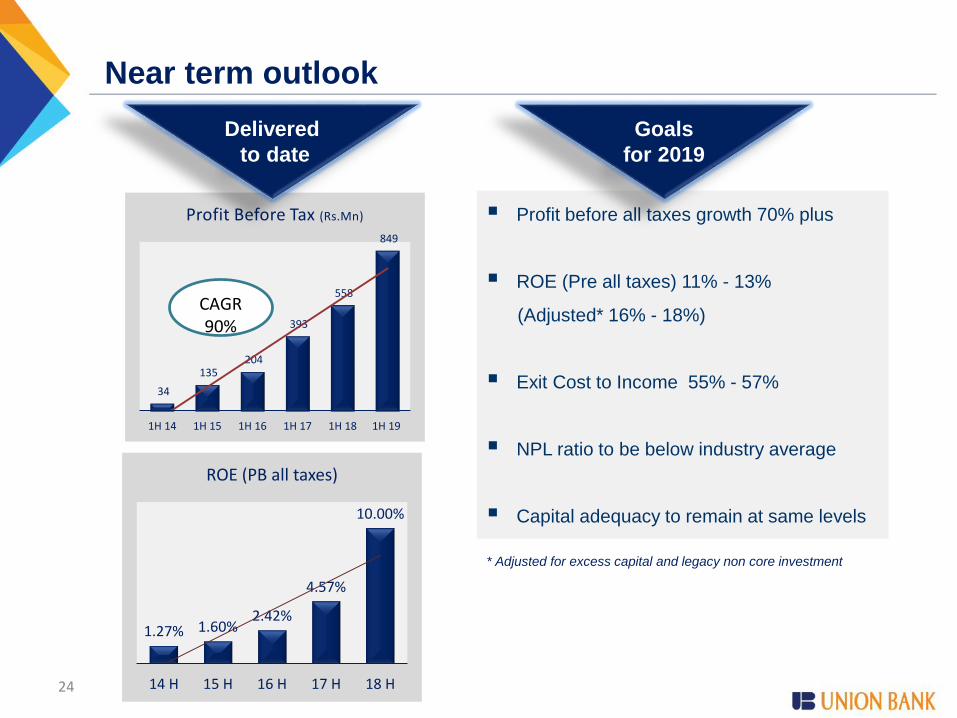

Near term outlook

24

34

135 204

393

558

849

1H 14 1H 15 1H 16 1H 17 1H 18 1H 19

Profit Before Tax (Rs.Mn)

CAGR90%

1.27% 1.60%2.42%

4.57%

10.00%

14 H 15 H 16 H 17 H 18 H

ROE (PB all taxes)

Profit before all taxes growth 70% plus

ROE (Pre all taxes) 11% - 13%

(Adjusted* 16% - 18%)

Exit Cost to Income 55% - 57%

NPL ratio to be below industry average

Capital adequacy to remain at same levels

Delivered

to date

Goals

for 2019

* Adjusted for excess capital and legacy non core investment

Robust Capital Adequacy

Rs 3.5bn worth of warrants

issued to TPG

Capital People

& ExecutionOperating

Leverage

Performance driven culture

Highest standards in ethics

and governance

Key focus on productivity

Energetic and young

workforce

Proficient team with

specialist skills

Alternate Channels

Digital Banking

Robust Analytics

Centralised Model

Flexibility

25

Internal accruals

Less Brick & Motor

Competitive advantage

26

Our strategy

Focus on business segments

that are profitable and scalable.

Credit cards to be a significant

business proposition.

Market leadership in Transaction

Banking services.

Stringent risk frameworks.

Digital Banking as a key enabler

Actively explore inorganic

opportunities

Our aspirations

Profit before all taxes 4.5X in 3

years

ROE (Pre all taxes) 30% - 35%

Exit Cost to Income below 45%

Retail & SME revenue

contribution to be 70%

Best in class NPL ratio

Robust Capital adequacy

Future outlook

27

Increased

returns on

equity to

shareholders

Increased

employee

satisfaction

Governance &

Regulatory

compliance at

the highest

level

Superior

customer

satisfaction

Strategic CSR

with focus on

children and

youth