corporate social responsibility and the market pricing … · corporate social responsibility and...

TRANSCRIPT

Corporate Social Responsibility

and the Market Pricing of Corporate Earnings

Eli Bartov* Leonard N. Stern School of Business

New York University

Yan Li

NUS Business School

National University of Singapore

February 4, 2015

*Corresponding author: New York University, Stern School of Business, 44 W. 4th St., Suite 10-96, New York,

NY 10012. Tel: +1 (212) 998-0016. We appreciate the comments from Siew Hong Teoh, Bernard Yeung, Oliver

Li, Charles Shi, workshop participants at Bocconi University, National University of Singapore, PolyU Hong

Kong, and participants at the 2014 CAAA Annual Conference in Edmonton, Alberta, the 2014 AAAannual

meeting in Atlanta, GA, and the 2014 International Corporate Governance Conference Organized by the Centre

for Corporate Governance and Financial Policy at Hong Kong Baptist University. Yan Li is grateful to the

financial support from Singapore MOE Tier 1 Academic Research Fund.

Corporate Social Responsibility

And the Market Pricing of Corporate Earnings

ABSTRACT:

Does a firm’s corporate social responsibility (CSR) performance relate to the market pricing

of its earnings? While prior CSR research has studied benefits of CSR activities from a

managerial reporting and analyst perspectives, we focus on an investor behavior perspective.

Briefly, motivated by the CSR literature’s assertion that the higher the CSR performance the

higher is the company’s adherence to the spirit of the law and ethical standards and the finding

in the accounting literature that CSR activities are negatively related to earnings management,

we examine whether a firm’s CSR performance is associated with investors’ ability to more

reliably price earnings news. We find in a short window around earnings announcements

higher abnormal stock returns sensitivity to earnings surprises and higher abnormal trading

volumes for firms with higher CSR activities. We also find that the well-known post-earnings

announcement drift decreases in CSR performance. These findings are distinct from the

previously documented corporate governance effect, robust to various measures of earnings

surprises, abnormal returns, and CSR performance, and hold for a battery of validity checks

that considers a possible endogeneity problem, and a variety of alternative explanations.

Keywords: corporate social responsibility; market response to earnings announcements; post-

earnings announcement drift; trading volume

JEL Classification: M14, M41, G14

1

Corporate Social Responsibility

and the Market Pricing of Corporate Earnings

1. Introduction

Corporate social responsibility (CSR) concerns a corporate’s strategy, operations, and

governance structure that create environmental and social values--in addition to maximizing

enterprise value for the benefits of its shareholders--by monitoring and ensuring compliance

with the spirit of the law, ethical standards, and international norms. The goal of CSR is to

encourage a positive impact through its activities on the environment, consumers, employees,

communities, future generations, shareholders and other stakeholders.

The traditional shareholder view on CSR emphasizes the costs and limitations of

compliance with self-imposed social and environmental standards, and asserts that company

managers could not and should not be expected to engage in CSR activities at the expense of

shareholders, i.e., undertaking negative NPV projects or foregoing positive NPV projects (see,

e.g., Friedman 1970). Moreover, if CSR activities take place as a response to pressure from a

broader group of stakeholders, they inevitably result in squandering shareholder value, and are

thus inconsistent with the notion of maximizing enterprise value for the benefits of its

shareholders.

More recently, however, an opposing view on CSR, referred to as “strategic CSR,” has

emerged. This view rests on the assertion that attention to corporate social and environmental

responsibilities is generally in the long-term economic interests of the firm. When companies

implement strategic CSR, they may find there are many benefits, including enhanced trust with

key stakeholders (investors, customers, employees, regulatory agencies, and suppliers), and

strengthened corporate and brand reputations.1

Clearly, CSR activities concern trade-offs. Focusing on its potential downside, prior

1See Porter and Kramer (2006, 2011) for insights and examples of companies that have developed deep linkages

between their business strategies and CSR activities.

2

research has investigated whether managers engage in CSR activities for personal benefit rather

than for the interest of the firm’s stockholders. Jensen and Meckling (1976) and Carroll (1979),

for example, assert that CSR may be associated with managerial opportunistic behavior.

McWilliams, Siegel, and Wright (2006) suggest that CSR is a managerial perquisite; managers

may use CSR to advance their careers or other personal agendas, and Petrovits (2006) and

Prior, Surroca, and Tribo (2008) provide supportive evidence for this view. In contrast to these

findings, Gao, Lisic, and Zhang (2014) predict and find that executives of CSR firms profit

significantly less from insider trades and are less likely to trade prior to future news than

executives of non-CSR firms.

A second strand of the literature has examined benefits from voluntary disclosures of

CSR activities. Dhaliwal, Radhakrishnan, Tsang, and Yang (2012) ask whether CSR voluntary

disclosures help financial analysts. Their results demonstrate that the issuance of a stand-alone

CSR report is associated with higher analyst earnings forecast accuracy. In addition, Dhaliwal,

Li, Tsang, and Yang (2011) document that firms with a high cost of equity capital in year t-1

tend to initiate disclosure of CSR activities in year t, and that initiating firms with superior CSR

performance enjoy a subsequent reduction in the cost of equity capital.

A third strand of the literature has examined whether CSR firms differ from non-CSR

firms with respect to their mandatory financial reporting behavior. While prior work (Trebucq

and Russ 2005; Chih, Shen, and Kang2008) has reported mixed results, Kim, Park, and Wier

(2012)—who investigate whether CSR firms also behave in a responsible manner to constrain

earnings management, thereby delivering more transparent and reliable financial information

to investors—find that socially responsible firms are less likely to engage in earnings

management through discretionary accruals or real operational activities, or to be the subject

of Securities and Exchange Commission (SEC) investigations.2

Trebucq and Russ (000) find mixed results across different specifications Specifically they do not find a

significant association between CSR and earnings management using a net CSR score; they do observe, however,

3

An interesting question arises from the findings of Kim, Park, and Wier (2012), as well

as from the CSR literature’s assertion that the higher the CSR performance the higher is the

company’s adherence to the spirit of the law and ethical standards: Do CSR firms also differ

from non-CSR firms in investors’ pricing of earnings news? In this paper, we contribute to the

recently emerging empirical CSR literature, as well as to the fairly mature but still incomplete

literature on the market pricing of earnings information, by studying three questions related to

potential informational benefits to investors associated with CSR performance.

Our first research question asks: Does the sensitivity of the market reaction to a firm’s

earnings surprise—i.e., the slope coefficient (beta, or ERC, earnings response coefficient) from

regressing earnings announcement stock returns on earnings surprises—relate to its CSR

performance? Clearly, earnings announcements are important corporate events that may

change dramatically investors’ assessment of firms’ future prospects and value. While early

studies (e.g., Ball and Brown 1968) have documented a positive association between earnings

surprises and stock returns, more recent research (e.g., Liu and Thomas 2000) has concluded

that the sensitivity of the stock price response to earnings surprises hinges on the extent to

which earnings are relevant to shareholders and potential shareholders in their investment

decision making.

Recall that according to the CSR literature, the higher the CSR performance the higher

is the company’s adherence to the spirit of the law and ethical standards, which in turn, implies

less earnings management as demonstrated by Kim, Park, and Wier (2012). This, together with

the findings in the ERC literature (Liu and Thomas 2000), opens up the possibility that the

sensitivity of the market response to earnings surprises and CSR performance are positively

a negative relation in other specifications. Using multinational data, Chih, Shen, and Kang (2008) examine the

relation between CSR performance and earnings management, and provide inconsistent results across different

earnings management proxies. They show that CSR firms are more aggressive in accruals management but are

less likely to engage in earnings smoothing and earnings loss avoidance. However, different countries have

different accounting standards and reporting incentives (e.g., Ball, Robin, and Wu 2003), and these cross-country

differences rather than the variation in the CSR performance may explain their findings.

4

related That is the higher a company’s CSR performance the higher is its earnings response

coefficient (ERC) after controlling for determinants other than earnings informativeness (e.g.,

growth and risk) shown by prior research to explain the cross section variation in ERCs.

To be sure, the evidence in Kim, Park, and Wier (2012) is suggestive but not conclusive

with respect to the relation between CSR activities and the sensitivity of the market response

to earnings for three reasons. First, the market may not be able to uncover the earnings

management, in which case the ERC may not vary with CSR activities. Indeed, prior empirical

research has provided evidence indicating the market behaves as if it reacts to reported earnings

numbers mechanically (e.g., Dietrich 1984; Hand 1990; Bartov and Mohanram 2014), and in

particular is unable to decipher earnings management (e.g.,Teoh, Welch, and Wong 1998; Xie

2001;Louis and Sun 2011). 3 This result is further supported by ample and convincing

anecdotal evidence of earnings management that went unnoticed by the market for many years

(e.g., Enron Corporation; WorldCom Inc.; Tyco International Ltd.; HealthSouth

Corporation).4Second, even if the market were able to uncover the earnings management, it is

still not clear whether the earnings management differential across low and high CSR firms is

sufficiently large to affect the returns/earnings relation. Lastly, if the assertion (discussed

above) that managers make suboptimal investment decisions in CSR is valid, then the

sensitivity of the market reaction to earnings surprises may relate negatively, not positively, to

CSR performance, as investors may discount the earnings news.

Our second research question asks: Is the well-known market underreaction to earnings

surprises negatively related to CSR performance? If CSR activities are associated with more

This finding is intuitively appealing for three reasons. First, there is information asymmetry between

management and investors, i.e., investors are privy to only a small subset of a company’s information set, which

precludes them from being able to undo earnings manipulation. Second, findings in prior literature on investor

limited attention implies that even if investors were able to undo the manipulation, it is not clear they would pay

the attention needed to undo it Third if investors undo the manipulation what’s the point of managing earnings?

4In the case of HeathSouth Corporation, for example, William T. Owens, its president and CEO, testified that he

created an accounting method that would hide $2.7 to $4.6 billion in fraudulent earnings to bolster company stock

performance during the 17-year period, 1987-2003.

5

transparent and easier to interpret earnings due to less earnings management, we expect the

well-documented mispricing related to the post-earnings announcement drift (PEAD), to be

negatively related to CSR activities. That is, the higher the CSR activities the lower is PEAD.

Clearly, our first two research questions are not unrelated. If the stronger response to earnings

surprises reflects higher quality earnings information associated with CSR (our first

hypothesis), CSR activities should be associated with smaller drift (our second hypothesis), as

the drift represents market underreaction to earnings news due to investors’ failure to fully

incorporate earnings information into stock prices in a timely fashion (see, e.g., Bernard and

Thomas 1990).

To provide further evidence on how a firm’s CSR activities relate to investors’

perception of its earnings quality, our third and final research question examines whether the

earnings announcements from socially responsible firms generate high trading volume.

Empirical studies interpret earnings announcements that are accompanied by high trading

volume as conveying more information to investors than announcements that generate low

trading volume (see, e.g., Morse 1981; Bamber 1986; Bamber and Cheon 1995). Theoretical

support for this interpretation can be found in analytical models of stock trade by

Pfleiderer(1984), Grundy and McNichols(1989), Holthausen and Verrecchia(1990), and Kim

and Verrecchia(1991). These models imply that the trading volume induced by a public

announcement is positively related to the announcement's precision. In our setting, if CSR

activities relate negatively to earnings management, our third research question predicts a

positive correlation between abnormal trading volume and CSR activities around earnings

announcements, ceteris paribus.

One research-design challenge underlying our study is to quantify a firm’s CSR

performance. However, the recent emergence of rating organizations—reliable third party

institutions with resources to gather the needed information to compute CRS activities—makes

6

quantitative CSR data widely available in a machine readable form. Following prior studies in

the area (e.g., Chatterji, Levine, and Toffel2009; Kim, Park, and Wier2012), we retrieve our

proxy for CSR activities, the Kinder, Lydenburg, and Domini (KLD) ratings, from the KLD

database. However, the KLD’s corporate governance category is excluded when computing

our proxy for CSR activities and is instead used as a control variable so as to disentangle the

effects of CSR and corporate governance, because corporate governance tends to benefit the

firm’s shareholders rather than society at large.

In testing our three research questions, we analyze a broad sample that spans the 21-

year period, 1992 – 2012. Briefly, our analyses demonstrate that the sensitivity of the market

responses to earnings surprises is increasing in CSR activities, and that the extent of the

mispricing of earnings news, the post-earnings announcement drift, is decreasing in CSR

activities. We also find that CSR activities are positively related to abnormal trading volumes

around earnings announcements. These findings hold even after considering a host of control

variables, and are robust to various measures of earnings surprises, abnormal returns, and CSR

performance, and to a battery of validity checks that considers, among other things, a potential

endogeneity problem, a time period effect, and the alternative explanation that a corporate

governance effect confounds our findings.

Our contribution to the literature is threefold. First, we contribute to the strand of the

CSR literature that focuses on the managerial reporting perspective. This literature has

documented a negative association between CSR activities and earnings management (Kim,

Park, and Wier2012). However, the effect of this relation on the pricing of earnings is not clear

because investors, for example, may be unable to decipher the earnings management before

reacting to the earnings news. Our findings thus complement this strand of the literature by

highlighting the investor perspective That is investors’ reaction to earnings announcements

is increasing in CSR activities in terms of both stock prices and trading volumes.

7

Second, our findings complement the strand of the CSR literature that focuses on

financial analyst perspective. This strand of the literature has documented a positive

association between voluntary disclosures of CSR activities and analysts’ earnings forecast

accuracy. Our findings of a negative relation between CSR activities and PEAD add to this

strand of the literature by showing that investors are able to more accurately price stocks of

firms with higher CSR activities.

Lastly, the CSR effect in the market response to earnings we document is distinct from

the corporate governance effect found by prior research. Specifically, while the effect we find

is, as expected, robust to time periods, the corporate governance effect disappears after 2001

(Bebchuk, Cohen, and Wang 2013).

The remainder of the paper is structured as follows. The next section outlines our

sample selection procedures, variable definitions, and descriptive statistics. The third section

describes our tests and reports the results for the analyses on ERC and PEAD. The fourth

section provides validity checks for the findings documented in Section 3. The fifth section

reports the tests and results for abnormal trading volume around earnings announcements.

Section 6 considers the possibility that an endogeneity problem confounds our findings, and

finally, Section 7 summarizes our findings and concludes.

2. Data

2.1. Sample

The computation of a company’s CSR score (described below in detail) is based on

corporate social responsibility ratings provided by the KLD database. The KLD database

coverage starts from 1991 with annual ratings on approximately 650 firms, including all firms

in the S&P 500 and Domini 400 Social SM Index.5 The coverage was substantially expanded

5 Domini 400 Social Index is a market cap weighted stock index of 400 publicly traded companies that have met

certain standards of social and environmental excellence. Potential candidates for this index will have positive

records on issues such as employee and human relations, product safety, environmental safety, and corporate

8

to 1,100 firms in 2001 and to 3,100 firms in 2003, to include firms from Russell 1000 and 2000

indexes as well as from certain social indexes (see, 2006 KLD Research & Analytics, Inc.

manual). We retrieve our financial statement measures from Compustat quarterly database,

and stock returns from the CRSP daily returns database. Other databases used to construct the

control variables include I/B/E/S database for analyst forecast data and Thomson Reuters for

institutional ownership data.

Our sample spans 21 years, from 1992 to 2012; our sample period commences in 1992

because the KLD ratings are available since 1991 and because, to avoid a potential look-ahead

bias, we use the KLD ratings in year t-1 to classify observations into CSR deciles in year t.

Table 1 reports the effect of our sample selection procedures on the size of our final sample.

We begin with the initial sample of KLD annual ratings consisting of 141,200 firm-quarter

observations from 5,576 distinct firms over the 21-year period, 1991 - 2011.6 We then merge

these ratings with the Compustat quarterly database, which results in a loss of 13,357 firm-

quarters (642 distinct firms). Next, we drop 953 firm-quarters (9 distinct firms) with

insufficient data from Compustat to compute time-series based earnings surprises, and 1,081

firm-quarters (10 distinct firms) with a quarter-end stock price of less than $1 to alleviate the

noise caused by small SUE deflators. Then, after removing an additional13,947 observations

(182 distinct firms) not covered by the CRSP daily return file, and 320 observations (4 distinct

firms) without sufficient data from CRSP to compute abnormal returns, our final sample for

the long-window tests (i.e., tests on post earnings announcement drift) consists of 111,541 firm-

quarter observations (4,729 distinct firms). For the short-window tests (i.e., tests on ERC and

abnormal volume in the 3-day window around earnings announcements) we also require that

governance. Companies engaged in the business of alcohol, tobacco, firearms, gambling, nuclear power and

military weapons are automatically excluded. The index is independently maintained by research firm KLD

Research & Analytics, and includes mainly large cap stocks in the S&P 500.

6 The database actually provides 35,300 annual ratings. Since each annual rating is used in the ensuing four

quarters, the number of firm-quarters is 141,200 (=35,300 x 4).

9

I/B/E/S analyst earnings forecasts be available. This additional requirement results in a loss of

13,798 firm-quarters (192 distinct firms). The final sample for the short-window tests thus

contains 97,743 firm-quarter observations (4,537 distinct firms).

[Insert Table 1 about here]

2.2. Variable definitions

2.2.1.CSR scores

In each year, KLD assigns strengths and concerns in six dimensions: environmental

protection, community development, employee relations, diversity practices, product quality,

and corporate governance practices.7Since it is plausible that investors assess a company’s

CSR performance based on the totality of the evidence, and along the lines of prior research

(e.g., Kim, Park, and Wier2012;El Ghoul, Guedhami, and Kwok 2011) we construct our CSR

score, CSR_S, by aggregating total strengths minus total concerns in KLD’s first five

categories.

The KLD’s corporate governance category is excluded when computing CSR_S and is

instead used (by its net value, strengths minus concerns) as a control variable so as to

disentangle the effects of CSR and corporate governance because corporate governance tends

to benefit the firm’s shareholders rather than society at large. We use the KLD score in the

corporate governance dimension as a control variable rather than the Governance Index

(Gompers, Ishii, and Metrick 2003) because the latter measure is not available for our entire

sample period. Still, we replicated our tests below with available Governance-Index data and

found that our results are robust (results not tabulated for parsimony).

To reduce noise and to alleviate concerns that the relation between CSR_S and our

7 Starting from 2002, KLD has also assessed firms in the dimensions of human rights and firearms. Since data for

these two dimensions are not available before 2002, we do not include these two dimensions in constructing the

CSR scores, same as Kim, Park, and Wier (2012).

10

dependent variables is nonlinear, we use the decile ranks of CSR_S rather than their actual

values in our regression analysis. To that end, we first sort all firms in each year by their CSR_S

into ten deciles from lowest KLD score, decile 1, to highest KLD score, decile 10.8 Next, we

assign a decile rank to each firm within the decile, and then scale each decile rank by

subtracting 1 from it and then dividing it by 9, so the CSR decile rank, CSRDEC, ranges from

0 to 1. As an alternative, we define a dummy variable, CSRDUM, which is set to 0 (1) if the

firm-year is in the first (tenth) CSR decile.

2.2.2.SUE

Along the lines of prior PEAD research (e.g., Bernard and Thomas 1990; Ball and

Bartov 1996), for the post-earnings announcement drift tests we define the quarterly

standardized earnings surprise (SUE) as the seasonal difference in quarterly earnings, scaled

by the stock price, given in the following equation:

𝑆𝑈𝐸𝑖,𝑞 = (𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑞 − 𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑖,𝑞−4)/𝑃𝑖,𝑞 (1)

Where, Earningsi,q is the primary earnings per share before extraordinary items of firm ifor

quarter q, and Pi,q, is the stock price per share of firm i at the end of quarter q. This measure of

SUE is widely available, bias free, and has been widely used in the PEAD literature. However,

following the ERC literature, for our ERC tests we calculate SUE based on analyst forecasts

rather than the seasonal differences in quarterly earnings, and denote this variable as SUE_AF.9

Similar to the fashion in which CSRDEC is computed, we compute DSUE (DSUE_AF)

by first forming in each quarter ten SUE (SUE_AF) deciles from lowest SUE (SUE_AF), decile

1, to highest SUE (SUE_AF), decile 10. We next assign a decile rank to each firm within the

decile, and then adjust each decile rank by subtracting 1 from it and then dividing the difference

8As an alternative, we formed the deciles within industry-year, rather than year, and obtained similar results.

9As expected, this reduces our sample size by approximately 10 percent; employing instead reported earnings

from the same quarter last year has no impact on our findings (results are not tabulated for parsimony).

11

by 9, so DSUE (DSUE_AF) ranges from 0 to 1.

2.2.3. Abnormal returns

We measure the abnormal returns over two windows: the earnings announcement

window that spans three trading days, -1, 0 and +1, where day 0 is the earnings announcement

day, and the post-earnings announcement window that spans 60 trading days commencing two

days after day 0. We define these returns either as cumulative abnormal returns (CAR,

Equations 2 and 3), or as buy-and-hold abnormal returns (BHAR, Equations 4 and 5):

𝐶𝐴𝑅(−1, 1)𝑖𝑞 = ∑ (𝑅𝑖𝑘 − 𝐸𝑅𝑖𝑘)𝑡+1𝑘=𝑡−1 (2)

𝐶𝐴𝑅(2, 60)𝑖𝑞 = ∑ (𝑅𝑖𝑘 − 𝐸𝑅𝑖𝑘)𝑡+60𝑘=𝑡+2 (3)

𝐵𝐻𝐴𝑅(−1, 1)𝑖𝑞 = ∏ (1 + 𝑅𝑖𝑘) −𝑡+1𝑘=𝑡−1 ∏ (1 + 𝐸𝑅𝑘)𝑡+1

𝑘=𝑡−1 (4)

𝐵𝐻𝐴𝑅(2, 60)𝑖𝑞 = ∏ (1 + 𝑅𝑖𝑘) −𝑡+60𝑘=𝑡+2 ∏ (1 + 𝐸𝑅𝑘)𝑡+60

𝑘=𝑡+2 (5)

Where, Rik is the stock-return of firm i and ERik is the stock-return of the matching size-B/M

portfolio on day k, and t is quarter q's earnings announcement date. Each stock is matched with

one of six size-B/M portfolios (i.e., two size and three B/M portfolios) at the end of June, where

size is the market capitalization at the end of June, and B/M is the ratio of book value of equity

at the last fiscal year end to the market capitalization at the end of last calendar year. The daily

returns of the six size-B/M portfolios are from the Kenneth French’s website 10 If a firm delists

during the return accumulation window, we compute the remaining return by using the CRSP

daily delisting return, reinvesting any remaining proceeds in the appropriate benchmark

portfolio, and adjusting the corresponding market return to reflect the effect of the delisting

return on our measures of expected returns (see Shumway 1997; Beaver, McNichols, and Price

2007).11

10 http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data library.html

11 Poor performance-related delistings (delisting codes 500 and 520–584) often have missing delisting returns in

the CRSP database (Shumway 1997). To correct for this bias, we set missing performance-related delisting returns

12

2.2.4. Abnormal trading volume

We denote the three-day average abnormal trading volume as 𝐴𝐵𝑉𝑂𝐿(−1, 1), where

day 0 is the earnings announcement day.12 Following Hirshleifer, Lim, and Teoh (2009), we

define abnormal volume on day j relative to the announcement date t as a normalized difference

between the log dollar volume on day j and the average log dollar volume over the 30-day

period, (−41 −11 ,relative to the earnings announcement date:

𝐴𝐵𝑉𝑂𝐿(𝑗) = 𝐿𝑜𝑔(𝐷𝑜𝑙𝑙𝑎𝑟𝑉𝑜𝑙𝑡+𝑗 + 1) −1

30∑ 𝐿𝑜𝑔(𝐷𝑜𝑙𝑙𝑎𝑟𝑉𝑜𝑙𝑘 + 1)𝑡−11

𝑘=𝑡−41

2.3. Descriptive statistics

Panel A of Table 2 compares descriptive statistics of our sample firms (long-window

tests) with those in the quarterly Compustat universe.13 Since the KLD database only covers

the largest firms, it is not surprising that our sample firms differ from those in the Compustat

universe. Both mean and median comparisons indicate that our sample firms are substantially

larger than firms in the Compustat universe, as measured by sales, total assets, and market

capitalization. Still, this difference should not be overemphasized because the market response

to earnings announcements and post-earnings announcement drift are both decreasing in firm

size presumably because more predisclosure information is available for large firms (Shores

1990; Bernard and Thomas 1990), which implies that our results below may be stronger than

they appear.

Our sample firms are also more profitable than those in the Compustat universe: they

to –100 percent as recommended by Shumway (1997). Overall, the percentage of delisting sample firms is small

(approximately 0.8 percent and 2 percent for the 60-day and 120-day return windows, respectively), which is not

surprising given our relatively short return windows. Still, we replicate our tests excluding delisting returns. The

results, not tabulated for parsimony, are indistinguishable from the tabulated results. 12 Using the average trading volume over the past two weeks as the normal volume as in DellaVigna and Pollet

(2009), yield qualitatively identical results.

13 The results for the sample employed for the short-window tests are very similar (not tabulated for parsimony).

(6)

13

earn higher earnings, are less likely to report a loss, and generate higher return on assets (ROA).

In addition, on average the market response to earnings is positive for both samples, albeit more

so for our sample. This finding is consistent with prior research finding of earnings

announcement premium, i.e., on average stock prices rise around scheduled earnings

announcement dates. Differences in the leverage ratio (debt to assets) suggest that our sample

firms are generally less leveraged than those in the Compustat universe. In addition, the

earnings of our sample firms represent less growth (mean and median SUE are both lower than

the Compustat universe), yet are more likely to beat analyst forecasts (mean and median

SUE_AF are higher than the Compustat universe), their beta is higher, and a larger percentage

of their stock is held by institutions. Overall, the statistics in Table 2 show, as expected, that

our sample firms are larger, more profitable, less leveraged, with more predictable earnings

and higher institutional ownership vis-à-vis Compustat firms not in our sample. To consider

the possibility that these differences confound our findings, the validity checks section below

considers their effects on our results.

Panel B of Table 2 presents the sample distribution by industry as defined by Fama-

French 12 industry classification (see, Fama and French 1995). Notwithstanding the

differences in descriptive statistics between our sample and the Compustat universe, we find

that all industries are well represented in our sample, and our sample displays a similar

distribution as the Compustat sample over the same period. For example, each of the two most

represented industries--finance, and computers, software and electronic equipment--consists of

over 15% of firms in both our sample and the Compustat universe. In addition, the sample

distribution across other industries is also quite similar to that of the Compustat universe. This

relieves the concern of sample selection bias. To further mitigate the potential industry effect,

we control for the industry fixed effect in the regression analyses.

Finally, Panel C of Table 2 reports the year-over-year variation in a firm’s CSR ranking

14

Clearly, the variation is nontrivial as the results indicate that approximately 50 (25) percent of

firms in CSR deciles 2-9 (1, 10) change decile ranking annually.

[Insert Table 2 about here]

3. Tests and Results: Stock Returns

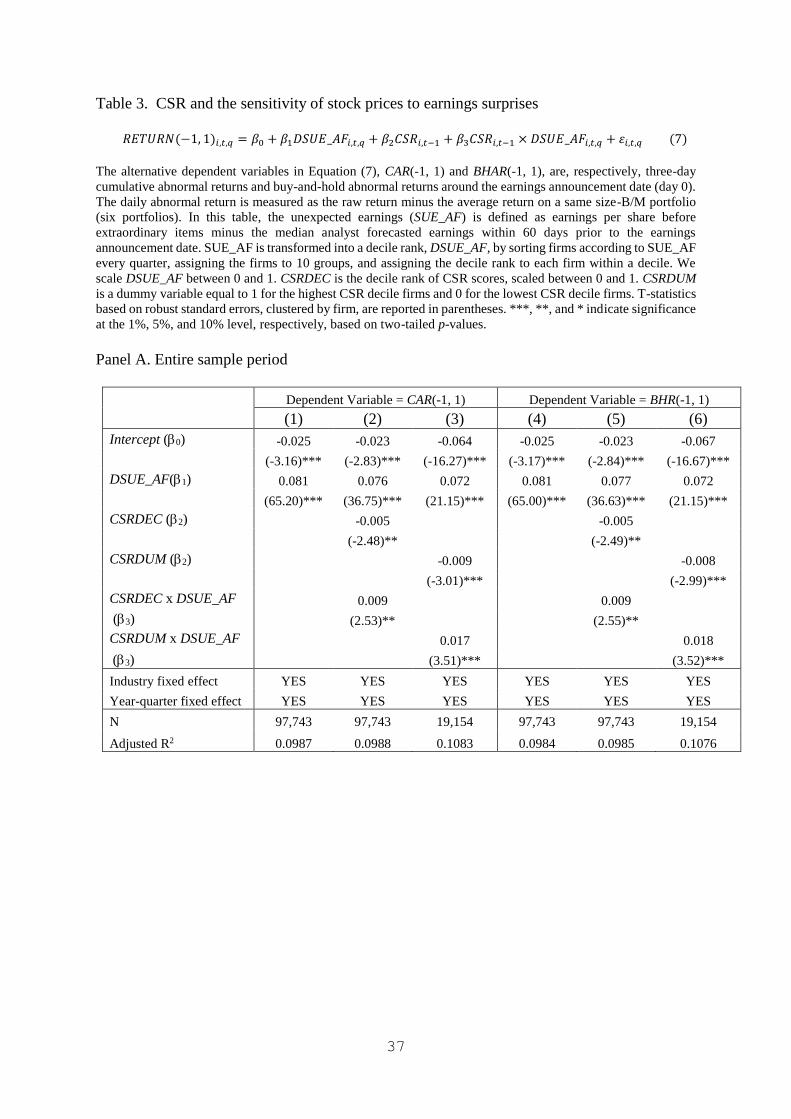

3.1. Tests on the sensitivity of the market response to earnings surprises

3.1.1 Methodology

We test our first research question, the one related to the relation between CSR activities

and the sensitivity of the market response to earnings surprises, by estimating the following

equation:

𝑅𝐸𝑇𝑈𝑅𝑁(−1, 1)𝑖,𝑡,𝑞 = 𝛽0 + 𝛽1𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽2𝐶𝑆𝑅𝑖,𝑡−1 + 𝛽3𝐶𝑆𝑅𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝜀𝑖,𝑡,𝑞(7)

Where, i is the firm index, and t(= 1990 1993 … 0010 and q(=1, 2, 3, 4) designate year and

quarter, respectively. The dependent variable, 𝑅𝐸𝑇𝑈𝑅𝑁(−1, 1)𝑖,𝑡,𝑞 , is either cumulated

abnormal return, CAR(-1, 1), or buy-and-hold abnormal return, BHAR(-1, 1), over the three-

day period centered on the earnings announcement day. DSUE_AF is the scaled decile rank of

SUE_AF.CSR is measured either as the scaled decile ranks of CSR scores, CSRDEC, or as a

dummy variable, CSRDUM.

Our variable of interest, the interaction term between CSR and DSUE_AF, captures the

extent to which investors’ short-term response to a firm’s quarterly earnings surprise varies

with the firm’s CSR activities. In terms of Equation (7), our prediction that the sensitivity of

the market response to earnings surprise is positively associated with CSR activities implies

that𝛽3> 0.

3.1.2. Results

Panel A of Table 3 reports the results from estimating Equation (7) for the entire sample,

15

and Panel B reports the results for two subperiods, 1991 – 1999 and 2000 - 2011. Consider the

results in Panel A first, where the three right-most columns display the results using the three-

day buy-and-hold abnormal returns, BHAR(-1, 1), as the dependent variable, and the three left-

most columns using cumulated abnormal return, CAR(-1, 1). From reading across the table we

first note that for all specifications𝛽1, the coefficient on DSUE_AF, the variable that captures

the earnings surprise, is as expected positive and significant at the 1 percent level, with the

magnitude ranging from 0.072 to 0.081. In addition, measuring the abnormal returns as either

buy-and-hold or cumulative makes little difference, as evidenced by the (nearly) identical

coefficients on corresponding variables and the similarity in the R-squared values across the

two alternative measures for the dependent variable.

[Insert Table 3 about here]

Second, the coefficient on our variable of interest, 𝛽3, capturing the interaction between

CSR activities and earnings surprises (i.e., 𝐶𝑆𝑅𝐷𝐸𝐶 × 𝐷𝑆𝑈𝐸_𝐴𝐹or𝐶𝑆𝑅𝐷𝑈𝑀 × 𝐷𝑆𝑈𝐸_𝐴𝐹),

is significantly positive. This finding indicates a positive association between the sensitivity

of the market reaction to earnings surprises and CSR activities: the higher the CSR activities

the higher the ERC. To illustrate the economic significance of the association between CSR

activities and ERC, consider the results displayed in column (3). Comparing with firms in the

lowest CSR score decile, firms in the highest CSR score decile have an average ERC of 0.089

(=0.072+0.017), representing an increase of approximately 24 percent in the ERC. In other

words, when reporting earnings in the highest earnings surprise decile (DSUE_AF = 1), the

earnings announcement return of firms in the highest CSR decile is 170 bps higher than that of

firms in the lowest CSR decile. Therefore, the positive association between CSR activities and

ERC is not only statistically significant, it is also economically important.

Next, we consider the relation between the CSR effect in the market response to

earnings news and that of corporate governance documented by prior research, and the

16

sensitivity of our findings to a possible time period effect. The motivation for this analysis

follows from Bebchuk, Cohen, and Wang (2013) that show that the correlation between

corporate governance indices and earnings announcement abnormal stock

returnsdocumentedfor1990–1999, subsequently disappeared. According to Bebchuk, Cohen,

and Wang (2013), the correlation and its disappearance are both due to market participants’

gradually learning to appreciate the difference between good-governance and poor-governance

firms.

Note, however, that the story underlying our hypotheses differs from that of Bebchuk,

Cohen, and Wang (2013) in an important way. Specifically, we assert that the stock price

response to earnings is stronger for CSR firms due to higher earnings quality (less earnings

management), whereas Bebchuk et al. hypothesize that the stronger response follows from

investors’ failure to recognize that better-governance firms are managed more efficiently, and

thus will report higher earnings. In other words, the stock price response to earnings may be

expressed as the product of the earnings surprise and the stock price response to a unit of

surprise (i.e., the beta on the earnings surprise, or ERC). While we hypothesize that the

stronger CSR firms’ earnings announcement stock returns follows because CSR firms have a

higher ERC due to higher quality earnings that investors recognize, Bebchuk et al. argue that

the stronger stock price response to better-governance firms’ earnings releases represents

higher earnings surprises due to investors’ failure to recognize that better governance leads to

higher earnings. One important empirical implication of this difference is that the time period

effect observed in Bebchuk et al. setting, should not be expected in ours.

Panel B reports the results by subperiods. We pick 2001 as the cutoff year because

Bebchuk, Cohen, and Wang (2013) show that the corporate governance effect disappeared after

that year. To save space, we tabulate results only for CAR(-1, 1); using instead BHAR(-1, 1)

as the dependent variable does not change the findings. Similar to the results in Panel A, for all

17

specifications and time periods,𝛽1, the coefficient on DSUE, is as expected positive and highly

significant. The magnitude of the coefficient, however, seems to increase nearly three folds

over time, from 0.033 to 0.086 for the first model (columns 1 and 3), and from 0.029 to 0.084

for the second model (columns 2 and 4). One interpretation of this finding is that market learns

over time about its underreaction to earnings surprises and consequently (partially) corrects for

it by responding more strongly in the second period.

As to our coefficient of interest, 𝛽3, capturing the interaction between CSR activities

and earnings surprises (i.e., 𝐶𝑆𝑅𝐷𝐸𝐶 × 𝐷𝑆𝑈𝐸 or 𝐶𝑆𝑅𝐷𝑈𝑀 × 𝐷𝑆𝑈𝐸 ), it is significantly

positive in all specifications and time periods (the only exception is column 3, where it has the

predicted sign but is insignificance). This finding indicates that the positive association

between the sensitivity of the market reaction to earnings surprises and CSR activities is as

expected stable over time, and highlights an important difference between the CSR effect in

the stock price response to earnings announcements we document and the corporate

governance effect found by prior research.

One way to interpret this finding is that investors consider reported earnings of socially

responsible firms more transparent and reliable than those of other firms. Indeed, this

interpretation is consistent with findings in Kim, Park, and Wier (2012) demonstrating that

socially responsible firms are less likely to manipulate earnings and to be the subject of SEC

investigation.

One interesting implication of our findings so far is that CSR activities should alleviate

the well-documented underreaction to earnings announcements. In the next section, we test

this implication by examining the incremental association between CSR performance and post-

earnings announcement drift after controlling for the earnings surprises.

18

3.2. Tests on the Post-Earnings Announcement Drift

3.2.1 Methodology

Recall that our second research question predicts that the mispricing associated with

earnings announcements is decreasing in CSR activities. More specifically, the higher the CSR

activities, the stronger is the sensitivity of the market reaction to earnings surprises, which in

turn alleviates the market underreaction to earnings announcements and thus the post-earnings

announcement drift. To test this prediction, we replicate the estimation of Equation (7) above,

except that the dependent variable is either cumulative abnormal returns, CAR(2, 60) or buy-

and-hold abnormal returns, BHAR(2, 60), from two days after quarterly earnings announcement

day to 60 trading dates afterwards, as follows:

𝑅𝐸𝑇𝑈𝑅𝑁(2, 60)𝑖,𝑡,𝑞 = 𝛽0 + 𝛽1𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽2𝐶𝑆𝑅𝑖,𝑡−1 + 𝛽3𝐶𝑆𝑅𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝜀𝑖,𝑞(8)

In other words, we test the incremental effect of CSR activities on the 60-day post-

announcement abnormal returns after controlling for the SUE effect. If the stronger immediate

response to earnings surprises associated with CSR documented above alleviates the well-

documented underreaction to earnings announcements, we expect a smaller post-earnings

announcement drift for firms with higher CSR scores. In terms of Equation (8), the prediction

that post-earnings announcement drift is decreasing in CSR activities suggests that 𝛽3< 0.

3.2.2. Results

Table 4 reports the results from estimating Equation (8). The three right-most columns

display the results using the 60-day buy-and-hold abnormal returns, BHAR(2, 60),as the

dependent variable, and the three left-most columns using cumulated abnormal return, CAR(2,

60). Two results are noteworthy. First, consistent with findings in prior literature on post-

earnings announcement drift (e.g., Bernard and Thomas 1990;Ball and Bartov 1996), the

coefficient on DSUE, 𝛽1, is significantly positive in specifications that consider current SUE

and future returns without introducing CSR activities (columns 1 and 4 of Table 5). This

19

positive correlation between current earnings surprises and future stock returns, which suggests

that the market underreacts to earnings news, confirms prior literature findings in our sample.

[Insert Table 4 about here]

Second, when the model is augmented to include the interaction between CSR activities

and earnings surprises, which is measured as either 𝐶𝑆𝑅𝐷𝐸𝐶 × 𝐷𝑆𝑈𝐸or 𝐶𝑆𝑅𝐷𝑈𝑀 × 𝐷𝑆𝑈𝐸,

𝛽1 is still significantly positive. In these specifications, the positive 1 means that the

underreaction to earnings news is observed when CSR activities are relatively low (for firms

in the lowest CSR decile). Moreover, 1 is larger in these specifications relative to the

unaugmented model (e.g., 0.013 in column 1 vis-à-vis 0.022 in column 2), implying that the

drift for low CSR companies is larger than the drift for an average CSR company. More

importantly, 𝛽3 —the coefficient on our variable of interest, capturing the effect of CSR

activities on the post-earnings announcement drift—is significantly negative in all

specifications. This finding indicates a negative association between post-earnings

announcement drift and CSR activities; that is, for a given earnings surprise the higher the CSR

activities the lower post-earnings announcement drift. Taken together, the picture that emerges

from the findings so far is that CSR activities are positively associated with perceived earnings

quality (i.e., more decision useful) that results in more efficient market valuation of earnings.

This is evidenced by the positive association between CSR activities and the sensitivity of

market response to earnings news (Table 3) and the negative association with post-earnings

accounting drift (Table 4). In the next section, we perform validity checks to assess the

reliability of our findings.

4. Validity Checks

In this section, we perform sensitivity tests that consider the robustness of our findings

so far to model specification.

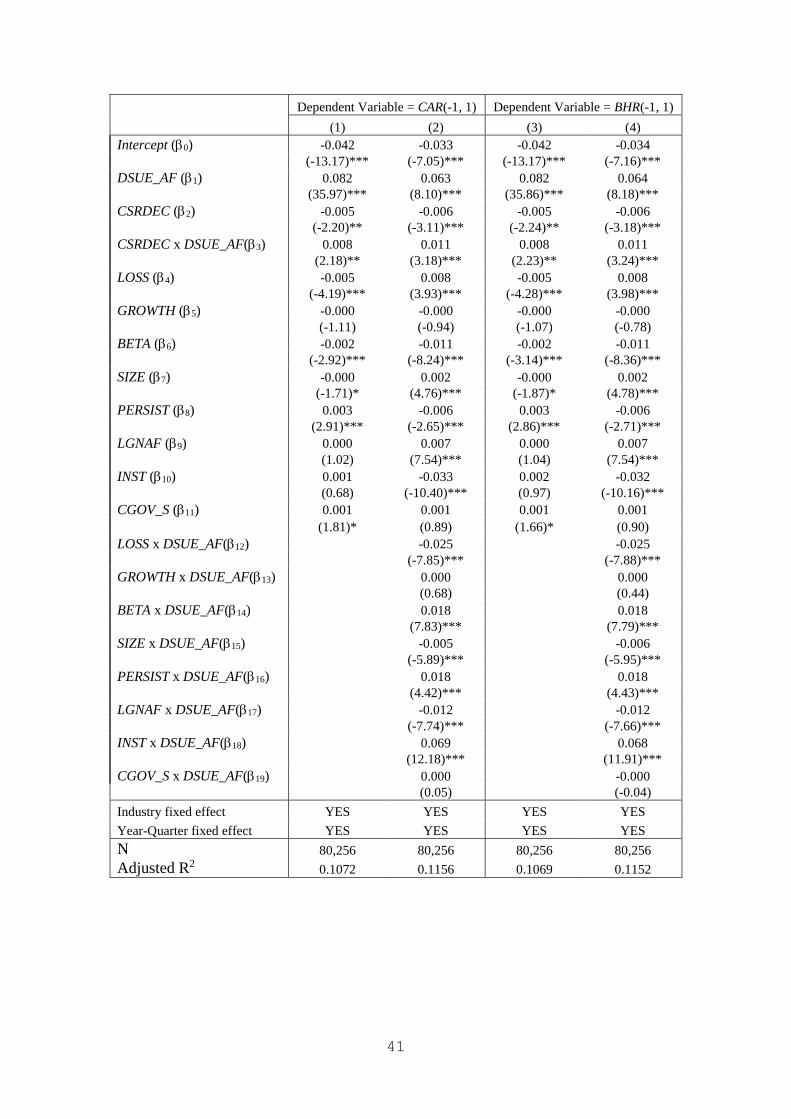

4.1. CSR activities and the sensitivity of market response to earnings news

20

In the last four decades, ample empirical accounting research has documented a number

of determinants underlying the sensitivity of stock price changes to earnings surprises in

regressions of returns on current earnings (see, e.g., Collins and Kothari 1989;Lundholm and

Myers 2002; Balsam, Bartov, and Marquardt 2002).Growth, risk (beta), earnings persistence,

firm size, ownership sophistication, and the presence of an accounting loss have all been shown

to be significantly related to the coefficient on current earnings (i.e., ERC). Thus, an alternative

explanation for our results is that CSR activities serve simply as a proxy for these determinants.

To test this alternative explanation, we augment Equation (7) above by adding eight

variables as stand-alone as well as interaction variables, as follows:

𝑅𝐸𝑇𝑈𝑅𝑁(−1, 1)𝑖,𝑡,𝑞 = 𝛽0 + 𝛽1𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽2𝐶𝑆𝑅𝑖,𝑡−1 + 𝛽3𝐶𝑆𝑅𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 +

𝛽4𝐿𝑂𝑆𝑆𝑖,𝑡−1 + 𝛽5𝐺𝑅𝑂𝑊𝑇𝐻𝑖,𝑡−1 + 𝛽6𝐵𝐸𝑇𝐴𝑖,𝑡−1 + 𝛽7𝑆𝐼𝑍𝐸𝑖,𝑡−1 + 𝛽8𝑃𝐸𝑅𝑆𝐼𝑆𝑇𝑖,𝑡,𝑞 + 𝛽9𝐿𝐺𝑁𝐴𝐹𝑖,𝑡,𝑞 +

𝛽10𝐼𝑁𝑆𝑇𝑖,𝑡,𝑞 + 𝛽11𝐶𝐺𝑂𝑉_𝑆𝑖,𝑡 + 𝛽12𝐿𝑂𝑆𝑆𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽13𝐺𝑅𝑂𝑊𝑇𝐻𝑖,𝑡−1 ×

𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽14𝐵𝐸𝑇𝐴𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽15𝑆𝐼𝑍𝐸𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽16𝑃𝐸𝑅𝑆𝐼𝑆𝑇𝑖,𝑡,𝑞 ×

𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽17𝐿𝐺𝑁𝐴𝐹𝑖,𝑡,𝑞 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽18𝐼𝑁𝑆𝑇𝑖,𝑡,𝑞 × 𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝛽19𝐶𝐺𝑂𝑉_𝑆𝑖,𝑡 ×

𝐷𝑆𝑈𝐸_𝐴𝐹𝑖,𝑡,𝑞 + 𝜀𝑖,𝑡,𝑞

Where, as before i is the firm index, t (= 1990 1993 … 0010 and q (=1, 2, 3, 4) designate

year and quarter, respectively, and the RETURN, DSUE_AF, and CSR variables are as defined

in Equation (7) above. Our first control variable, LOSSt-1is a dummy variable equal to one if

income before extraordinary items in year t-1 is negative, and equal to zero otherwise.

GROWTH t-1 is the difference between total assets at the end of year t-1 and total assets at the

end of year t-2.BETAt-1 is the CAPM beta measured based on daily returns over the yeart-1.

SIZEt-1 is the firm’s market capitalization at the end of year t-1.PERSIST is earnings persistence

measured as follows: using data from the most recent 16 quarters up to quarter q-1 (minimum

4 observations), we regress by firm IBCq on IBCq-4, where IBC is quarterly income before

extraordinary items scaled by total assets. The coefficient on IBCq-4 is assigned as the

persistence measure for each firm in quarter q. To mitigate the effect of outliers and similar to

the way we compute DSUE_AF, we replace the value of the coefficient on IBCq-4 by its

(9)

21

rank.14LGNAF is the logarithm of (1+ the number of analysts who provide earnings forecast

for the company’s current fiscal quarter INSTi,t,q, our proxy for ownership sophistication, is

the percentage of institutional holdings at the end of the most recent calendar quarter

constructed based on Thomson-Reuters 13f database.

Finally, to assess the possibility that our CSR scores simply represent another

manifestation of corporate governance, we add to our model CGOV_S, the KLD score in the

corporate governance dimension, measured, as before, as the KLD net score (i.e., total score of

strengths minus total score of concerns).As discussed before, we use CGOV_S rather than the

Governance Index (Gompers, Isshii, and Metrick 2003) because the latter measure is not

available for our entire sample period. Still, we replicated our tests below in the sample with

available Governance-Index data and found that our results are robust (results not tabulated for

parsimony).

Table 5 displays the results from estimation Equation (9): in the two right-most (left-

most) columns the dependent variable is the three-day buy-and-hold (cumulative) abnormal

returns. The primary takeaway from Table 5 is that our results are robust to the inclusion of

the additional control variables. This is evidenced by the significantly positive coefficient on

both𝛽1 , the coefficient on DSUE_AF, and 𝛽3 , the coefficient on our variable of interest,

𝐶𝑆𝑅𝐷𝐸𝐶 × 𝐷𝑆𝑈𝐸_𝐴𝐹, in all specifications. In addition, the incremental contribution of the

control variables in explaining earnings persistence is limited, once the CSR activities are

considered. This point is perhaps best illustrated by how little the control variables contribute

incrementally to the regression ability to explain the cross sectional variation in the market

response to earnings surprises. For example, the R-Squared in Table 3 above for the

specification that considers CAR(-1, 1) as the dependent variable and CSRDEC as an

Controlling for earnings growth and persistence is particularly important in the current context because in

addition to higher earnings quality, CSR performance also implies higher quality work force and more sustainable

earnings.

22

explanatory variable is 9.88 percent (see column 2 of Table 3), and after augmenting the model

by adding the eight control variables either as stand-alone variables (column 1 of Table 5) or

as stand-alone and interaction variables (column 2 of Table 5) the corresponding R-Squared is

only slightly higher, 10.72 percent and 11.56 percent, respectively.15

[Insert Table 5 about here]

4.2. CSR activities and the market underreaction to earnings news

We document above negative relation between post-earnings announcement drift and

CSR activities. However, in addition to post-earnings announcement drift prior research

demonstrates that accruals are also mispriced around earnings announcements (e.g., Sloan

1996), and that other variables, corporate governance, the number of analysts following a firm,

and ownership sophistication may also be related to the market underreaction to earnings

announcements. To test whether the explanatory power of CSR activities for post-earnings

announcement drift is above and beyond these variables, we estimate the following model:

𝑅𝐸𝑇𝑈𝑅𝑁(2, 60)𝑖,𝑡,𝑞 = 𝛽0 + 𝛽1𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽2𝐶𝑆𝑅𝑖,𝑡−1 + 𝛽3𝐶𝑆𝑅𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽4𝐿𝐺𝑁𝐴𝐹𝑖,𝑡,𝑞 +

𝛽5𝐼𝑁𝑆𝑇𝑖,𝑡,𝑞 + 𝛽6𝐶𝐺𝑂𝑉_𝑆𝑖,𝑡−1 + 𝛽7𝐴𝐵𝐴𝐶𝐶𝑖,𝑡−1 + 𝛽8𝐿𝐺𝑁𝐴𝐹𝑖,𝑡,𝑞 × 𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽9𝐼𝑁𝑆𝑇𝑖,𝑡,𝑞 ×

𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽10𝐶𝐺𝑂𝑉_𝑆𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝛽11𝐴𝐵𝐴𝐶𝐶𝑖,𝑡−1 × 𝐷𝑆𝑈𝐸𝑖,𝑡,𝑞 + 𝜀𝑖,𝑡,𝑞

Where, as before i is the firm index, t (= 1990 1993 … 0010 and q (=1, 2, 3, 4) designate

year and quarter, respectively, the RETURN, DSUE, and CSR variables are as defined in

Equation (8) above, and LGNAF, INST, and CGOV_S are as defined in Equation (9). ABACC,

the abnormal accruals, are measured in two alternative methods: DA_JONES based on the

modified Jones model (Dechow, Sloan, and Sweeney 1995), and DA_DD based on the Dechow

and Dichev (2002) model. We pick an abnormal accruals variable to control for the accruals

anomaly because evidence in prior research (e.g., Xie 2001) demonstrates that the mispricing

of total accruals documented by Sloan (1996) is due largely to abnormal (or discretionary)

15Notice that the sample size reduces somewhat from 97,743 firm-quarter observations in Table 3 to 80,256

observations in Table 5 due to missing data for the control variables.

(10)

(11)

23

accruals.

We derive our first estimate of abnormal accruals, DA_JONES, by running the

following cross sectional regression in each industry-year with a minimum of 20 observations:

𝑇𝐴𝐶𝐶𝑖,𝑡 = 𝛼0 + 𝛼1(∆𝑅𝐸𝑉𝑖,𝑡 − ∆𝐴𝑅𝑖,𝑡) + 𝛼2𝑃𝑃𝐸𝑖,𝑡 + 𝜀𝑖,𝑡 (11)

where TACC is the total accruals calculated as income before extraordinary items minus

operating cash flow; ∆REV and ∆AR are change in sales revenue and change in accounts

receivables, respectively; PPE is the gross book value of property, plant and equipment. All

variables are scaled by the total assets at the beginning of the year. To mitigate the effect of

outlying observations, we winsorize all variables at the top and bottom one percent of their

distributions. The residual from regression (11), DA_JONES, is our first estimate of abnormal

accruals.

We obtain our second estimate of abnormal accruals, DA_DD, by running the following

time-series regression for each firm with minimum of 10 observations:

∆𝑊𝐶𝑖,𝑡 = 𝛼0 + 𝛼1𝑂𝐶𝐹𝑖,𝑡−1 + 𝛼2𝑂𝐶𝐹𝑖,𝑡 + 𝛼3𝑂𝐶𝐹𝑖,𝑡+1 + 𝜀𝑖,𝑡 (12)

Where ∆WC is change in working capital, and OCF is operating cash flows. All variables are

scaled by the total assets at the beginning of the year and are winsorized at the top and bottom

1 percent of their distributions. The residual from regression (12), DA_DD, is our second

estimate of abnormal accruals.

Panel A and Panel B of Table 6 display the results from estimating nested and full

versions of Equation (10). The primary take away from the table is that our results of the

relation between CSR activities and post-earnings announcement drift are robust to

specifications that control for corporate governance, accruals, institutional holdings, and

analyst coverage. Specifically, in both panels DSUE is significantly positive in all

specifications, ranging from 0.19 (t-statistic = 4.20) to 0.22 (t-statistic = 4.52) in Panel A, and

from 0.051 (t-statistic = 4.95) to 0.066 (t-statistic = 6.25) in Panel B. More importantly, our

24

variable of interest, 𝐶𝑆𝑅𝐷𝐸𝐶 × 𝐷𝑆𝑈𝐸, is significantly negative, ranging from -0.20 (t-statistic

= -2.57) to -0.23 (t-statistic = -2.82) in Panel A, and from -0.20 (t-statistic = -2.57) to -0.21

(t-statistic = -2.80) in Panel B. Thus, when CSR activities are relatively low (CSRDEC = 0)

the post-earnings announcement drift is observed, but when CSR activities are high (CSRDEC

= 1) the drift disappears as evidence by insignificant 𝛽1 + 𝛽3 (Panel A), or substantially

declines,𝛽1 + 𝛽3 <𝛽1(Panel B).

[Insert Table 6 about here]

5. Tests and Results: Abnormal Trading Volume

5.1. CSR activities and abnormal trading volume around earnings announcements

5.1.1. Methodology

Along the lines of Hirshleifer, Lim, and Teoh (2009), we test our third hypothesis that

predicts a positive relation between CSR activities and trading volumes around earnings

announcements by estimating the following model:

𝐴𝐵𝑉𝑂𝐿(−1, 1)𝑖,𝑡,𝑞 = 𝛽0 + 𝛽1𝐶𝑆𝑅𝐷𝐸𝐶𝑖,𝑡−1 + 𝛽2𝐷_𝐴𝐵𝑆(𝑆𝑈𝐸_𝐴𝐹)𝑖,𝑡,𝑞 +

𝛽3𝑆𝐼𝑍𝐸𝑖,𝑡−1+𝛽4𝐺𝑅𝑂𝑊𝑇𝐻𝑖,𝑡−1 + 𝛽5𝐿𝐺𝑁𝐴𝐹𝑖,𝑡,𝑞 + 𝛽6𝑅𝐸𝑃𝐿𝐴𝐺𝑖,𝑡,𝑞 + 𝛽7𝑃𝐸𝑅𝑆𝐼𝑆𝑇𝑖,𝑡,𝑞 + 𝛽8𝐼𝑁𝑆𝑇𝑖,𝑡,𝑞 +

𝛽9𝑆𝑇𝑈𝑅𝑁𝑂𝑉𝐸𝑅𝑖,𝑡,𝑞 + 𝜀𝑖,𝑡,𝑞

Where, as before, i is the firm index, t (= 1990 1993 … 0010 and q (=1, 2, 3, 4) designate

year and quarter, respectively,𝐴𝐵𝑉𝑂𝐿(−1, 1) is the average abnormal trading volume over the

three-day period, (-1, 1),relative to the earnings announcement date (day 0). CSRDEC is the

decile rank of CSR scores, scaled between 0 and 1. D_ABS(SUE_AF), our measure of the

earnings surprise, is computed as the deciles based on quarterly independent sort by absolute

forecast errors, then scaled to vary between 0 and 1.We use absolute earnings surprises, not

signed surprises, because both extreme positive and negative surprises are likely to generate

large trading volume. SIZE is the firm’s market capitalization at the end of last fiscal year

GROWTH is the difference between total assets at the end of year t and total assets at the end

of year t-1. LGNAF is the logarithm of (1 + number of analysts who provide earnings forecast

(13)

25

for the company’s current fiscal quarter For firm-quarters that are not covered by the I/B/E/S

database, the number of analysts is set to zero. REPLAG is the logarithm of (1+ number of days

from quarter-end to the earnings announcement date). PERSIST is earnings persistence

measured as follows: using data from the most recent 16 quarters up to quarter q-1 (minimum

4 observations), we regress by firm IBCq on IBCq-4, where IBC is quarterly income before

extraordinary items scaled by total assets. The coefficient on IBCq-4 is assigned as the

persistence measure for each firm in quarter q. To mitigate the effect of outliers, we replace

the value of the coefficient on IBCq-4 by its rank. INST is the percentage of institutional

holdings. STURNOVER is the average monthly share trading volume divided by the average

number of shares outstanding during a one-year period ending at the end of the corresponding

fiscal quarter. In term of Equation (13), our third hypothesis predicts that 𝛽1> 0.

5.1.2. Results

Table 7 reports the results from estimating Equation (13). Column (1) displays the

results for a nested specification that considers only our test variable, CSRDEC, and column

(2) reports the results for the full model.16Two results are noteworthy. First, as predicted,𝛽1,

the coefficient on CSRDEC, is significantly positive in both columns (1) and (2). This implies

that trading volume around earnings announcements is increasing in CSR activities. This is

expected if, as we assert, earnings of CSR firms are more reliable than those of non-CSR firms

(due to less earnings management). Second, seven out the eight control variables are

significant. Importantly, the coefficients on the earnings surprise variable, D_ABS(SUE_AF),is

significantly positive. Since abnormal trading volume reflects changes in expectations of

individual investors (see, e.g., Beaver 1968, p. 69), the positive coefficient suggests the higher

the earnings surprise the more investors adjust their (heterogeneous) expectations and thus

16In column (2) the number of observations declines to 80,237 due to the additional data requirements for the

control variables.

26

trade more. In addition, this positive correlation between earnings surprises and trading volume

is consistent with findings in prior literature, and thus increases confidence in the reliability of

our findings.

[Insert Table 7 about here]

6. Endogeneity Problem: 2SLSAnalysis

An assumption underlying the OLS analyses we have conducted so far is that the level

of a firm’s CSR performance is exogenous However it is possible that managers’ choice of

CSR investment depends on investors’ pricing of a company’s earnings news This possibility

raises concerns because it implies that our test variables (CSRDEC and CSRDUM) are

correlated with the regressions’ error term. In this situation, an OLS regression generally

produces biased and inconsistent estimates. However, if an instrumental variable (IV) is

available, consistent estimates may still be obtained.

An instrumental variable does not itself belong to the explanatory equation, but is

(partially) correlated with the endogenous explanatory variable, CSRDEC and CSRDUM,

conditional on the other covariates, and is uncorrelated with the dependent variable, RETURN

(-1, 1) and RETURN (2, 60), other than through its correlation with CSRDEC and CSRDUM

(as the instrumental variable cannot suffer from the same problem as the original explanatory

variable). Thus, in addition to performing OLS analyses, we use in this section the 2SLS

procedure to test our hypotheses.17,18In identifying our instruments, we consider prior CSR

17 We report the OLS results, in addition to the 2SLS results, because evidence shows that the OLS procedure is

more robust against specification errors than the 2SLS procedure, and that predictions from models estimated by

OLS often compare favorably with those of 2SLS (See, Maddala 1997, p. 231).

18 We test for the presence of an endogeneity problem in each of the three regressions (ERC, PEAD, and abnormal

volume). The results from the Durbin-Wu-Hausman test (not tabulated for parsimony) indicate the presence of

an endogeneity problem only in the PEAD regression; for the ERC and abnormal volume regressions the test fails

to reject the null of exogeneity. We also perform an underidentification test based on the Kleibergen-Paaprk LM

statistic that rejects the null that our models are underidentified. Finally, the Cragg-Donald Wald F-Statistic shows

our instrumental variables pass the weak instrument test.

27

literature. Giuli and Kostovetsky (2014) document that Democratic-leaning firms spend

significantly more on CSR than Republican-leaning firms. We thus choose the state’s political

preference as an instrument for CSR activities because it is associated with CSR investment

but there is no intuitive reason to believe that it would systematically affect investors’ response

to earnings news. Therefore in the 2SLS analysis, we use the political preference of the state

where the firm’s headquarter is located as an instrumental variable. We retrieve the presidential

election data from www.uselectionatlas.org and based on the final presidential voting data we

construct two state-level measures of the degree of Democratic-leaning. One measure is a

dummy variable, DEMDUMMY, equal to one if in the state the number of votes for the

Democratic candidate is greater than that for the Republican candidate (i.e., Democratic-

leaning) and equal to zero otherwise. The other one is a continuous measure, DEMPCT, which

is the percentage of all votes go to the democratic candidate. The higher DEMPCT, the more

Democratic-leaning is the state in the election. Of course, the measures for the instruments are

available every four years. The CSR data are thus matched with the most recent election data.

For example, CSR ratings in year 2000, 2001, 2002, and 2003 are all matched with the data

from the quadrennial presidential election of 2000 that took place on November 7th, 2000.

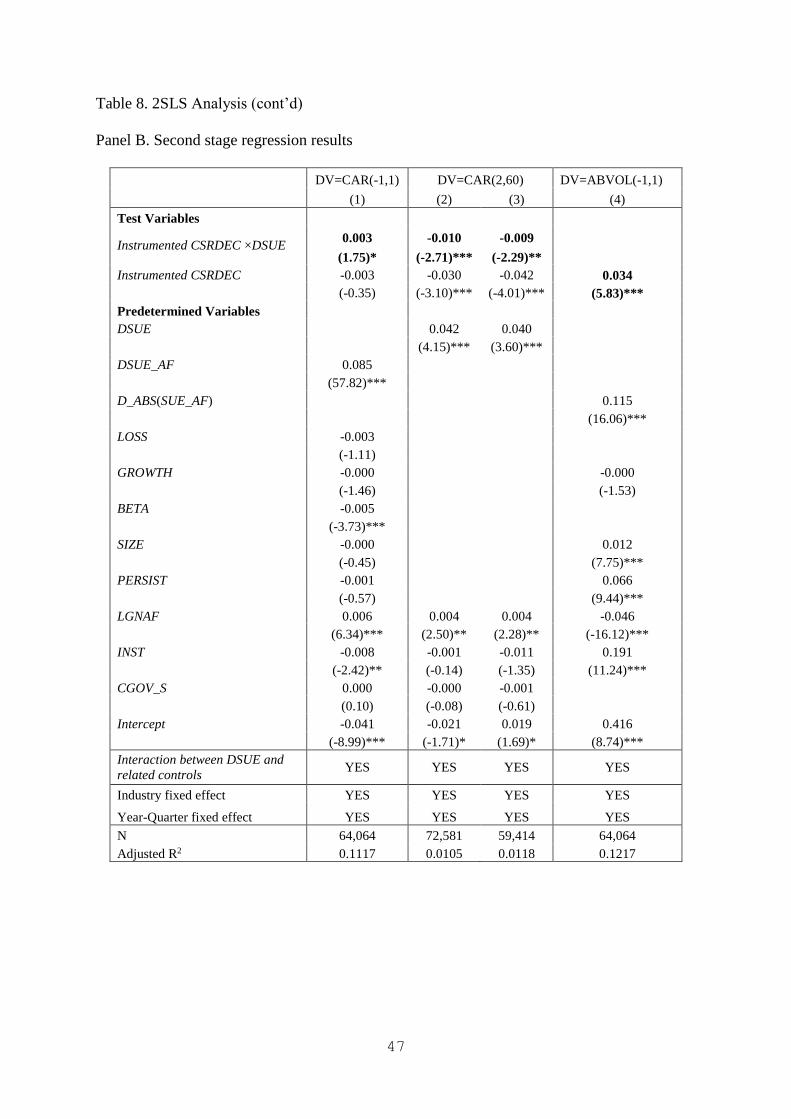

In the first stage, we run a regression of CSRDEC and include the two instruments,

DEMDUMMY, DEMPCT, and all other control variables involved in the regressions of ERC,

PEAD, and abnormal volume.19 In the second stage, we re-run the regressions of ERC, PEAD,

and abnormal volumes after replacing CSRDEC with the predicted values of CSRDEC

estimated from the first stage. Panels A and B of Table 8 report, respectively, the first and

second stage regression results.

In Panel A, both DEMDUMMY and DEMPCT are positive and significant, consistent with

the finding in prior research that democratic-leaning firms engage in higher level of CSR

19 As expected, the two instruments are correlated with a correlation coefficient of approximately 0.73.

Alternatively, we used one at a time and obtained nearly identical results (not tabulated for parsimony).

28

activities. This finding corroborates the results from the weak instrument test reported above,

and thus increases confidence that the instruments are valid. In the second stage, we rerun

Equations (9), (10), and (13), after replacing the CSR measure CSRDEC with its predicted

values from the first stage. The results reported in Panel B of Table 8 reveal that our findings

are robust to the 2SLS analysis. In particular, we find, as before, that when the firm has high

CSR activities the market returns around earnings announcement are more sensitive to the

firm’s unexpected earnings; the abnormal trading volume during the earnings announcement

window is larger; and the post earnings announcement drift for these firms is smaller.

[Insert Table 8 about here]

7. Conclusion

The traditional view on CSR activities emphasizes the trade-off between the short-term

cost borne by the firm and the long-term benefit to the society. Under this view, when

companies undertake CSR activities they may have to forgo profitable projects or invest in

unprofitable projects. In other words, corporate social responsibility involves a compromise on

the business objective of profit maximization. A recent view, strategic CSR, integrates

business objective and social responsibility by arguing that corporate success and social

welfare are synergetic. Under this view, business success and CSR activities are goal

congruent, not trade-offs.

By studying three questions that delve into the association between the market pricing

of earnings and the firm’s CSR activities, we complement prior research that has investigated

benefits associated with CSR performance from management perspective, and shed more light

on the validity of the two opposing views in the CSR literature. Our motivation follows from

the CSR literature’s assertion that the higher the CSR performance the higher is the company’s

adherence to the spirit of the law and ethical standards and the finding in the accounting

literature that CSR activities are negatively related to earnings management. Using three-day

29

abnormal returns surrounding earnings announcements, we find higher stock return sensitivity

to earnings surprises for firms with high CSR activities relative to firms with low CSR activities

(first research question), and that this finding is distinct from the corporate governance effect

in the market response to earnings news documented by prior research.

Our long return window analysis demonstrates that the positive association between the

60-day post-earnings announcement abnormal returns and the earnings surprises documented

by prior research is less pronounced for firms with high CSR activities relative to firms with

low CSR activities (second research question). In other words, the post-earnings

announcement drift decreases in CSR activities.

These findings are robust to various measures of earnings surprises, CSR performance,

and abnormal returns, and also hold for a battery of validity checks that considers, among other

things, a potential endogeneity problem, a time period effect, an alternative explanation that a

corporate governance effect confounds our findings, and a variety of control variables. In

addition, trading volume analysis around earnings announcements reveals a positive

association between CSR activities and abnormal trading volume (third research question).

This evidence further supports our assertion that earnings announcements of CSR firms convey

more information to investors.

Overall, our findings contribute to the literature by casting light on the relation between

CSR activities and investor behavior around earnings announcements. They complement the

findings in prior research that has focused on managerial reporting perspective, financial

analyst perspective, and corporate governance effect in the market response to earnings news.

30

Reference

Ball R and E Bartov 1996 How naive is the stock market’s use of earnings information?

Journal of Accounting and Economics 21, 319-337.

Ball, R., Brown, P., 1968. An empirical evaluation of accounting income numbers. Journal of

Accounting Research 6, 159-178.

Ball, R., A. Robin, and J.S. Wu.2003. Incentives versus standards: properties of accounting

income in four East Asian countries. Journal of Accounting and Economics 36, 235-270.

Balsam, S., E. Bartov, and C. Marquardt. 2002. Accruals management, investor sophistication,

and equity valuation: Evidence from 10-Q filing. Journal of Accounting Research40, 987

– 1012

Bamber, L. S. 1986. The information contents of annual earnings releases: A trading volume

approach. Journal of Accounting Research 24, 40-56.

Bamber, L. S., and Y. S. Cheon. 1995. Differential price and volume reactions to accounting

earnings announcements. The Accounting Review 70, 417-441.

Bartov, E., and P. Mohanram. 2014. Does income statement placement matter to investors?

The case of gains/losses from early debt extinguishment ” Forthcoming in The Accounting

Review 54.

Beaver, W. 1968. The information content of annual earnings announcements. Journal of

Accounting Research 6, 67-92.

Beaver, W., M. McNichols, and R. Price. 2007. Delisting returns and their effect on

accounting-based market anomalies. Journal of Accounting and Economics 43, 341-368.

Bebchuk, L.A., A. Cohen, and C.C.Y. Wang. 2013. Learning and the disappearing association

between governance and returns. Journal of Financial Economics108, 323–348.

Bernard, V.L., and J. K. Thomas. 1990. Evidence that stock prices do not fully reflect the

implications of current earnings for future earnings. Journal of Accounting and

Economics 13, 305-340.

Carroll, A. 1979.A three-dimensional conceptual model of corporate performance. The

Academy of Management Review 4(4): 497–505.

Chatterji, A. K., D. I. Levine, and M. W. Toffel. 2009. How well do social ratings actually

measure corporate social responsibility? Journal of Economics & Management Strategy

18(1), 125–169.

Chih, H., C. Shen, and F. Kang.2008. Corporate social responsibility, investor protection, and

earnings management: Some international evidence. Journal of Business Ethics79 (1/2),

179–198.

31

Collins, D.W. and S.P. Kothari. 1989. An analysis of intertemporal and cross-sectional

determinants of earnings response coefficients. Journal of Accounting and Economics 11,

143-181.

Dechow, P. M., and I. D. Dichev. 2002. The quality of accruals and earnings: the role of accrual

estimation errors. The Accounting Review 77 (Supplement), 35-59.

Dechow, P. M., R. Sloan, and A. Sweeney. 1995. Detecting earnings management. The

Accounting Review 70, 193-225.

DellaVigna, S., and J.M. Pollet. 2009. Investor inattention and Friday earnings announcements.

The Journal of Finance 64(2), 709-749.

Dhaliwal, D. S., O. Z. Li, A. Tsang, and Y. G. Yang. 2011. Voluntary nonfinancial disclosure

and the cost of equity capital: The initiation of corporate social responsibility reporting.

The Accounting Review 86(1), 59 – 100.

Dhaliwal, D. S., S. Radhakrishnan, A. Tsang, and Y. G. Yang. 2012. Nonfinancial Disclosure

and Analyst Forecast Accuracy: International Evidence on Corporate Social

Responsibility Disclosure. The Accounting Review 87(3), 723 – 759.

Dietrich, J.R. 1984. Effects of early bond refundings: An empirical investigation of security

returns. Journal of Accounting and Economics 6(1), 67–96.

El Ghoul, S., O. Guedhami, C. Y. Kwok, and D. R. Mishra. 2011. Does corporate social

responsibility affect cost of capital? Journal of Banking & Finance 35(9), 2388-2406.

Fama, E. F., K. R. French. 1995. Size and book-to-market factors in earnings and returns. The

Journal of Finance 50(1), 131- 155.

Friedman, M., 1970. The social responsibility of business is to increase its profits. The New

York Times, September 13, 32–33, 122–26.

Gao, F., L.L, Lisic, and I. Zhang. 2014. Commitment to social good and insider trading.

Forthcoming in Journal of Accounting and Economics.

Giuli, A. D., and L. Kostovetsky. 2014. Are red or blue companies more likely to go green?

Politics and corporate social responsibility. Journal of Financial Economics 111(1), 158–

180.

Gompers, P., J. Ishii, and A. Metrick. 2003. Corporate governance and equity prices. The

Quarterly Journal of Economics118, 107-155

Grundy, B. D. and M. McNichols. 1989. Trade and the revelation of information through prices

and direct disclosures. Review of Financial Studies 2(4), 495-526.

Hand, J. 1990.A test of the extended functional fixation hypothesis. The Accounting Review

65(4), 740-763.

32

Hirshleifer, D., S. Lim, and S. H. Teoh. 2009. Driven to distraction: Extraneous events and

underreaction to earnings news. Journal of Finance 63(5), 2287-2323.

Holthausen, R. W. and R. E. Verrecchia. 1990. The effect of informedness and consensus on

price and volume behavior. The Accounting Review 65(1), 191-208.

Jensen, M., and W. Meckling.1976. Theory of the firm: Managerial behavior, agency cost and

capital structure. Journal of Financial Economics 3(4), 305–360.

Kim, Y., M. S. Park, and B. Wier. 2012. Is earnings quality associated with corporate social

responsibility? The Accounting Review 87(3), 761 – 796.

Kim, O. and R. E. Verrecchia. 1991. Trading volume and price reactions to public

announcements. Journal of Accounting Research 29(2), 302-321.

Liu, J., Thomas, J., 2000. Stock returns and accounting earnings. Journal of Accounting

Research 38, 71-101.

Louis, H., Sun, A.X. 2011. Earnings management and the post-earnings announcement drift.

Financial Management 40(3), 591–621.

Lundholm, R., and L. A. Myers. 2002. Bring the future forward: The effect of disclosure on

the returns-earnings relation. Journal of Accounting Research 40(3), 809-839.

Maddala, G.S. 1977. Econometrics. New York: McGraw-Hill.

McWilliams, A., D. Siegel and P Wright 0006 Guest editors’ introduction corporate social

responsibility: Strategic implications. Journal of Management Studies 43(1), 1–18.

Morse, D. 1981. Price and trading volume reaction surrounding earnings announcements: A

closer examination. Journal of Accounting Research 19 (Autumn), 374-383.

Petrovits, C. 2006. Corporate-sponsored foundations and earnings management. Journal of

Accounting and Economics 41(3), 335–361.

Pfleiderer, P. 1984. The volume of trade and the variability of prices: A framework for analysis

in noisy rational expectations equilibria. Working Paper, Stanford University.

Porter, M., and M. Kramer. 2006. Strategy and society: The link between competitive

advantage and corporate social responsibility. Harvard Business Review 84(12), 78-92.

Porter, M., and M. Kramer. 2011. Creating shared value: How to reinvent capitalism and

unleash a wave of innovation and growth. Harvard Business Review 89(1/2), 62-77.

Prior, D., J. Surroca, and J. Tribo. 2008. Are socially responsible managers really ethical?

Exploring the relationship between earnings management and corporate social

responsibility. Corporate Governance 16(3), 160–177.

Shores, D., 1990. The association between interim information and securities return

surrounding earnings announcements. Journal of Accounting Research 28(1), 164-181.

33

Shumway, T. 1997. The delisting bias in CRSP data. The Journal of Finance 52(1), 327-340.

Sloan, R.G. 1996. Do stock prices fully reflect information in accruals and cash flows about

future earnings? The Accounting Review 71(3), 289-315.

Teoh, S.H., Welch, I, and T.J. Wong. 1998. Earnings management and the underperformance

of seasoned equity offerings. Journal of Financial Economics 50, 63-99.

Trebucq S and R Russ 000) The Case of earnings and stakeholder management: Towards

an integrated theory of managerial behavior Working paper Universite Montesquieu

Bordeaux I.

Xie, H. 2001. The mispricing of abnormal accruals. The Accounting Review 76(3), 357-373.

34

Table 1. Sample Selection

Number of

firm-

quarters

Number of

distinct

firms

All firm-quarter observations in KLD database 141,200 5,576

Less:

Observations not covered by Compustat quarterly file (13,357) (642)

Observations without sufficient data to compute SUE (953) (9)

Observations with quarter-end stock price of less than $1 (1,081) (10)

Observations not covered by CRSP daily return file (13,947) (182)

Observations without sufficient data

to compute abnormal returns (321) (4)

Final sample for long-window tests 111,541 4,729

Less:

Observations without I/B/E/S analyst earnings forecasts (13,798) (192)

Final sample for short-window tests 97,743 4,537

35

Table 2. Summary Statistics

Panels A and B compare the descriptive statistics and the industry distribution, respectively, of our final sample

for the long-window tests with the Compustat universe over the sample period. Panel C reports, by CSR decile,

the percentage of firms that move up down or stay in the same CSR decile We compare a firm’s CSR

classification in two consecutive years. If the firm is classified in a higher (lower) CSR decile in the next year, it

is categorized as Up (Down). If the firm stays in the same CSR decile in next year, it is categorized as No Change.

Industries are defined according to Fama-French 12 industry classification. CAR(-1, 1) and BHAR(-1, 1), are,

respectively, three-day cumulative abnormal returns and buy-and-hold abnormal returns around the earnings