corporate taxation and tax avoidance · personalincometax...

TRANSCRIPT

Corporate Taxation and Tax Avoidance

Jiaming Mao

Xiamen University

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 1 / 26

Copyright © 2014–2018, by Jiaming Mao

This version: Fall 2018

Contact: [email protected]

Course homepage: jiamingmao.github.io/principles-of-economics

All materials are licensed under the Creative CommonsAttribution-NonCommercial 4.0 International License.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 2 / 26

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 3 / 26

Personal Income Tax

U.S. federal personal income tax rates before and after the Tax Cuts and JobsAct (TCJA) of 2017. The table reports marginal rates.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 4 / 26

Personal Income Tax

For a history of U.S. federal personal income tax rates, see here.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 5 / 26

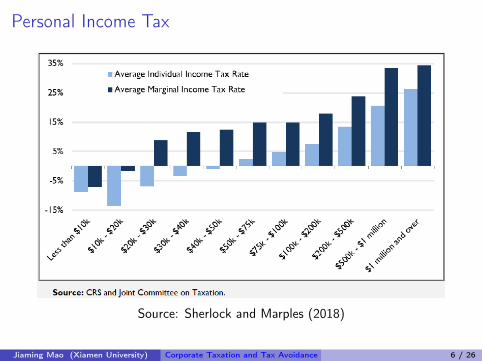

Personal Income Tax

Source: Sherlock and Marples (2018)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 6 / 26

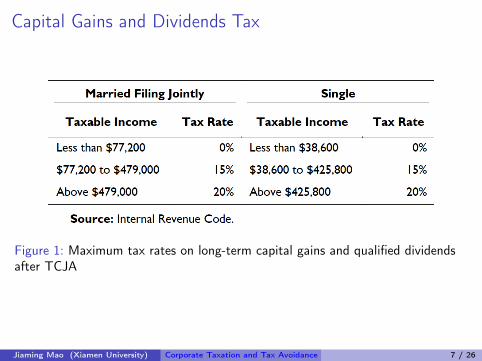

Capital Gains and Dividends Tax

Figure 1: Maximum tax rates on long-term capital gains and qualified dividendsafter TCJA

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 7 / 26

Corporate Income Tax

U.S. federal corporate income tax rates before TCJA. The table reports marginalrates. For a history of U.S. federal corporate income tax rates, see here.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 8 / 26

Corporate Income Tax

Marginal and average tax rates before TCJA. For large U.S. corporations (taxableincome > 18.3mil), both the average and marginal tax rates are 35%.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 9 / 26

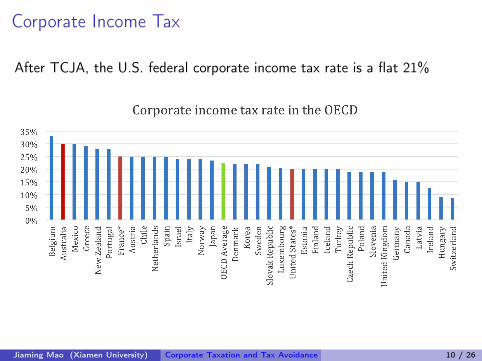

Corporate Income Tax

After TCJA, the U.S. federal corporate income tax rate is a flat 21%

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 10 / 26

Corporate Income Tax

The corporate income tax is one of the primary ways of taxing capital.

Without the corporate income tax, the personal income tax can bedodged or postponed by individuals incorporating themselves andkeeping their income within firms.

When corporate profits are paid out, they are typically taxed at a lowerrate than earned income (Figure 1), as tax authorities recognizedouble taxation.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 11 / 26

Corporate Income Tax

Corporate tax raison d’être:

A prepayment for the personal income tax

A way to tax rents (such as extractive industries) and businessactivities that generate negative externalities

I Tax credits can then be used as subsidies for business activities thatgenerate positive externalities.

A tax on foreign shareholders who benefit from the public goodsprovided by the country

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 12 / 26

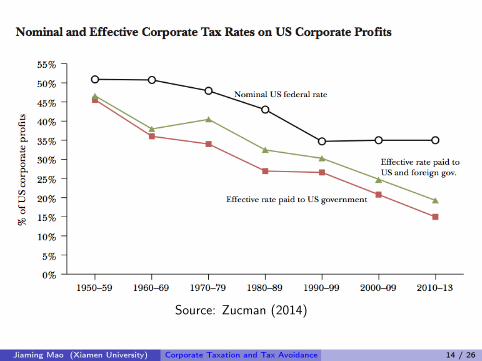

Corporate Income TaxBecause of various tax deductions and loopholes, the effective tax ratespaid by U.S. corporations are significantly lower than the statutory rates.

Effective Rates Paid by U.S. Corporations by IndustrySource: Ross, Westerfield, and Jaffe (2011)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 13 / 26

Source: Zucman (2014)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 14 / 26

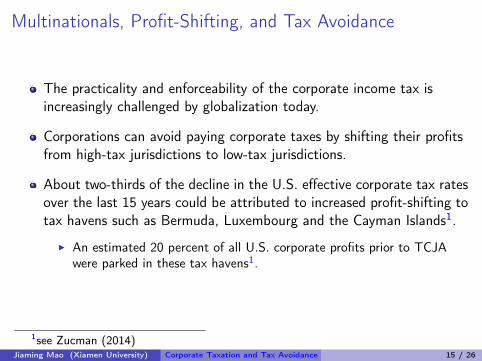

Multinationals, Profit-Shifting, and Tax Avoidance

The practicality and enforceability of the corporate income tax isincreasingly challenged by globalization today.

Corporations can avoid paying corporate taxes by shifting their profitsfrom high-tax jurisdictions to low-tax jurisdictions.

About two-thirds of the decline in the U.S. effective corporate tax ratesover the last 15 years could be attributed to increased profit-shifting totax havens such as Bermuda, Luxembourg and the Cayman Islands1.

I An estimated 20 percent of all U.S. corporate profits prior to TCJAwere parked in these tax havens1.

1see Zucman (2014)Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 15 / 26

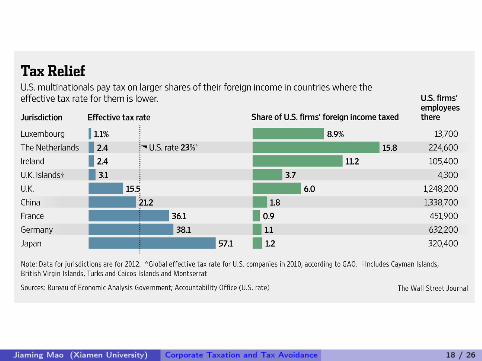

Source: Zucman (2014)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 16 / 26

Source: Zucman (2014)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 17 / 26

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 18 / 26

Countries Listed on Various Tax Haven Lists. Source: Gravelle (2015)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 19 / 26

Multinationals, Profit-Shifting, and Tax Avoidance

A popular method of profit-shifting is through the manipulation oftransfer pricing, the setting of prices at which companies exchangegoods and services internally.

I Consider a corporation, USCo, that grows coffee beans in Brazil at acost of $1/lb and sells them for $12/lb in the U.S. The company has asubsidiary, BrazilCo, in Brazil.

I To avoid paying taxes in either the U.S. or Brazil, USCo could set upanother subsidiary, BermudaCo, in Bermuda and have BrazilCo sellbeans to BermudaCo for $1/lb, who would in turn sell them to USCofor $12/lb.

I Both USCo and BrazilCo would record zero profits, while BermudaCoearns $11/lb in profits but is subject to zero corporate income tax.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 20 / 26

Multinationals, Profit-Shifting, and Tax Avoidance

In practice, to prevent profit-shifting, transfer pricing is required toobey the arm’s length principle: prices of goods and services tradedby related companies must be based on market prices.

Intangibles, such as patents and licenses, however, are hard to valueas relevant market prices may not exist.

I USCo could transfer its patent on coffee growing technology toBermudaCo and have BrazilCo pay royalties to BermudaCo for itsusage.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 21 / 26

Multinationals, Profit-Shifting, and Tax Avoidance

Profit-shifting could also be achieved via debt reallocation, throughwhich a corporation would hold the majority of its debt in high-taxjurisdictions to lower its taxable income in those jurisdictions throughdeductible interest expenses.

Another popular method of profit-shifting is through intragroup loans,whereby subsidiaries in low-tax jurisdictions grant loans to subsidiariesin high-tax jurisdictions, a practice known as earnings stripping.

The existence of thousands of bilateral tax treaties between countrieshas also created a web of inconsistent rules that corporations canexploit by choosing the location of their affiliates, a practice known astreaty shopping.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 22 / 26

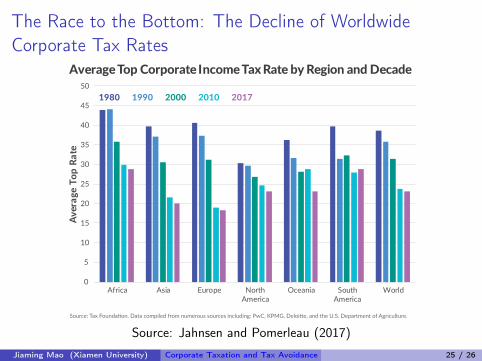

The Race to the Bottom: The Decline of WorldwideCorporate Tax Rates

The ability of multinationals to shift profits from high-tax jurisdictionsto low-tax jurisdictions exerts pressure on national governments tolower their corporate tax rates in order to remain competitive, creatinga “race to the bottom.”

Over the past 37 years, the average worldwide statutory corporate taxrate has declined by over 40%. In 2000, 42% of the countries in theworld imposed a statutory rate below 30%. In 2010, the numberincreased to 77%.

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 23 / 26

The Race to the Bottom: The Decline of WorldwideCorporate Tax Rates TAX FOUNDATION | 9

FIGURE 3.

All regions saw a net decline in average statutory rates between 1980 and 2017. The average declined the most in Europe, with the 1980 average of 40.5 percent dropping to 18.35 percent, representing almost a 55 percent rate reduction. South America has seen the smallest decline, with the average only decreasing by 28 percent from 39.66 percent in 1980 to 28.73 percent in 2017.

Africa, Oceania, and South America all saw periods where the average statutory rate increased, although the average rates decreased in all regions over the full period. In each instance of an average rate increase, the change was relatively small, with the absolute change being less than 1 percentage-point between decades.

Source: Tax Foundation. Data compiled from numerous sources including: PwC, KPMG, Deloi e, and the U.S. Department of Agriculture.

TAX FOUNDATION

1980

1990

2000

2010

2017

The Worldwide Distribution of Statutory Corporate Income Tax Rates, 1980-2017

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70%

Top Marginal Corporate Tax Rate

Source: Jahnsen and Pomerleau (2017)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 24 / 26

The Race to the Bottom: The Decline of WorldwideCorporate Tax Rates

TAX FOUNDATION | 10

FIGURE 4.

ConclusionThe last time the United States reduced its federal corporate income tax rate was in 1986. Since then, countries throughout the world have significantly reduced their statutory tax rates. Today, the United States statutory corporate tax rate is one of the highest in the world and stands well above the worldwide average. Reducing the statutory corporate tax rate to around the worldwide average as part of tax reform could discourage profit shifting and encourage companies to locate investment in the United States.

Source: Tax Foundation. Data compiled from numerous sources including: PwC, KPMG, Deloi e, and the U.S. Department of Agriculture.

TAX FOUNDATION

0

5

10

15

20

25

30

35

40

45

50

Africa Asia Europe NorthAmerica

Oceania SouthAmerica

World

vera

ge T

op R

ate

verage Top Corporate Income Tax Rate by Region and Decade

1980 1990 2000 2010 2017

Source: Jahnsen and Pomerleau (2017)

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 25 / 26

Reference

Gravelle, J. G. 2015. “Tax Havens: International Tax Avoidance andEvasion,” Congressional Research Service report, R40623.

Jahnsen, K. and K. Pomerleau. 2017. “Corporate Income Tax Ratesaround the World, 2017,” Tax Foundation, Fiscal Fact No. 559.

KPMG. 2018. “Tax Reform - KPMG Report on New Tax Law,” KPMGLLP.

Ross, S., R. Westerfield, and J. Jaffe. 2011. Corporate Finance (10th

ed.). McGraw-Hill Education.

Sherlock, M. F. and D. J. Marples. 2018. “Overview of the Federal TaxSystem in 2018,” Congressional Research Service report, R45145.

Zucman, G. 2014. “Taxing across Borders: Tracking Personal Wealthand Corporate Profits,” Journal of Economic Perspectives, 28(4).

Jiaming Mao (Xiamen University) Corporate Taxation and Tax Avoidance 26 / 26