corporations: the financial statements … chapters/nait ch 16 te.pdf · chapter 16 corporations:...

TRANSCRIPT

115

Assessment Questions

AS-1 ( 1 )

How are income taxes recorded for accounting purposes (cash basis vs accrual basis)?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-2 ( 1 )

Define accounting income and taxable income.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-3 ( 1 )

What does “deferred income taxes” refer to?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

CORPORATIONS: THE FINANCIAL STATEMENTS

Chapter 16

Income taxes are recorded in the financial statements using the accrual basis of accounting.

Accounting income represents the amount of profit (per accounting policies) a company

makes during a specific period of time (revenues less expenses). Taxable income is the portion

of income subject to taxation law.

The difference between income taxes payable (calculated using taxable income) and income

tax expense (calculated from accounting income) is known as deferred income tax.

Chapter 16 Corporations: The Financial Statements

116

AS-4 ( 2 )

Describe the steps in preparing closing entries for corporations (assuming the income summary account is used).

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-5 ( 3 )

Define discontinued operations.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-6 ( 3 )

Define other comprehensive income.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-7 ( 4 )

What information must a corporation disclose relative to income and retained earnings?

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

The first step is to close the revenue and expense accounts to the income summary account.

Then, the income summary account is closed to retained earnings.

A discontinued operation is a segment of business that is no longer part of regular operating

activities. Cash flows relating to such operations should be presented separately on the

income statement.

A corporation should show:

• net income for the year

• changes in retained earnings

• basic net income (earnings) per share

• diluted net income per share

Other Comprehensive income includes net income and other changes in equity as a result

of events from non-owner sources. This term is listed below net income on the income

statement.

Chapter 16Corporations: The Financial Statements

117

AS-8 ( 7 )

Define and discuss book value per share.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AS-9 ( 7 )

What ratio is used to assess debt relative to the amount of equity? Discuss.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Book value per share is a ratio used by investors and analysts to assess shares. To calculate the

book value per share, divide the shareholder’s equity minus preferred shares by the number

of common shares outstanding. The larger the book value per share, the more valuable

the share. The amounts (shareholder’s equity, preferred shares, and number of shares) are

all available from the financial statements. Note that the book value of shares does not

necessarily determine the value at which the shares can be sold (i.e. market value). Market

value is dependent on a number of factors such as industry mechanics, analyst predictions

and overall macroeconomic factors. Market value can vary greatly from book value.

The Debt-to-Equity ratio measures the amount of debt to equity for a business. When the

debt-to-equity ratio is 1:1, it means that lenders have the same investment in a business, as do

owners. When the debt to equity ratio is above 1:1, at say 1.5:1, it means that lenders have a

larger investment in the business than the owners. A debt to equity ratio of 1.5:1 means that

for every dollar that owners have invested in a business, lenders have $1.50 invested. A ratio

greater than 1:1 tends to make lenders “nervous” because the lenders have more of an interest

in the success of the business than the owners, because the lenders stand to lose more if the

business becomes bankrupt. The preferred ratio would be less than 1:1, say 0.6:1. That means

that for every dollar that owners have invested, there is only $0.60 for lenders. It is usually

better for the owners to have a greater investment in the company than lenders.

Chapter 16 Corporations: The Financial Statements

118

AS-10 ( 7 )

What ratio is used to determine what amount of a company’s earnings is paid out in dividends?

______________________________________________________________________________

AS-11 ( 7 )

How do you calculate earnings per share?

______________________________________________________________________________

=Net Income - Preferred Dividends

Earnings per shareAverage Number of Common Shares Outstanding

The dividend payout ratio:

Dividends Paid in a YearNet Income after Tax

Chapter 16Corporations: The Financial Statements

119

Application Questions

AP-1 ( 1 )

At year end, Shuster Home Decor Inc. (a small home furnishings retail store run by Terri) has accounting income (before income tax expense calculation) of $102,000. Write the journal entry to record the income tax expense. Assume the tax rate is 30%.

Date Account Title and Explanation Debit Credit

Income Tax Expense 30,600

Income Tax Payable 30,600

To record the income tax expense for the year

30% x $102,000 = $30,600

AP-2 ( 1 )

At year end, F’Brae Cheerleading Inc. (a medium sized distributor of cheerleading outfits) has accounting income of $210,000. Write the journal entry to record the income tax expense. Assume the tax rate is 30%.

Date Account Title and Explanation Debit Credit

Income Tax Expense 63,000

Income Tax Payable 63,000

To record the income tax expense for the year

30% x $210,000 = $63,000

AP-3 ( 1 )

CoreeMonTeeth Dental Inc. is a manufacturer of high quality dental equipment. In the current year it had accounting income of $300,000 which included $40,000 of warranty expenses. Per income taxation law, however, the warranty expenses are not deductible until they are actually paid. Write the journal entry to record income tax payable. Assume the tax rate is 30%.

Date Account Title and Explanation Debit Credit

Income Tax Expense 90,000

Deferred Tax Asset 12,000

Income Tax Payable 102,000

To record the income tax expense for the year

30% x $300,000 = $90,000

30% x $40,000 = $12,000

30% x $340,000 = $102,000

Chapter 16 Corporations: The Financial Statements

120

AP-4 ( 3 )

Green Light Emissions Everyday (otherwise known as GLEE Inc.) has sales of $400,000 and expenses of $120,000 (before calculation of income tax expense). Prepare a basic income statement for GLEE taking into account income tax expense. Assume a tax rate of 30%.

GLEE Inc.Income Statement

For the Year Ended December 31, 20x2

Sales $400,000

Expenses 120,000

Income Tax Expense 84,000 204,000

Income from Continuing Operations $196,000

AP-5 ( 1 )

Born off the coast of Mykonos, Gregory displayed an aptitude for singing at a very early age. In high school, he joined a musical club that participated in numerous singing competitions. His stage name was “Gleek the Greek.” Gregory decided that one day he would like to start his own singing school and is now taking an accounting course to help him become financially literate. He is posed with the following question on his test. Help him solve this question.

“Nacho Libray Inc. has income from continuing operations of $200,000. Their total expenses amounted to $100,000 and, of that, $50,000 pertained to income tax expense. Calculate the income tax rate used.”

______________________________________________________________________________

AP-6 ( 5 )

The bookkeeper for GIFT Inc. noticed that she made an error when recording a $44,000 expenditure in the prior fiscal year. She booked the amount to the Repairs and Maintenance expense account instead of posting to the Equipment account. Write the journal entry that should be recorded to correct the Equipment account. Ignore the impact of depreciation. Assume the tax rate is 30%.

Date Account Title and Explanation Debit Credit

Equipment 44,000

Retained Earnings 30,800

Income Tax Payable ($44,000 x 30%) 13,200

To correct amounts for error recorded in

prior fiscal year

30% x $44,000 = $13,200

Income tax rate is: = 50,000 ÷ [200,000 + 50,000] = 20%

Chapter 16Corporations: The Financial Statements

121

AP-7 ( 5 )

An auditor noticed that TFK Inc. accidently recorded an insurance expenditure of $50,000 as an expense instead of properly recording it as a prepaid. The purchase was made on the last day of the fiscal period. Write the journal entry that should be recorded in the next fiscal period to correct the Prepaid Insurance account. Assume the tax rate is 30%.

Date Account Title and Explanation Debit Credit

Prepaid Insurance 50,000

Retained Earnings 35,000

Income Tax Payable ($50,000 x 30%) 15,000

To correct amounts for error recorded in

prior fiscal year

30% x $50,000 = $15,000

AP-8 ( 7 )

Shown below are sections of the financial statements of Research in Motion. Calculate the book value per share for 2014.

Shareholders’ Equity

Contributed Capital

Authorized – unlimited number of non-voting, cumulative, redeemable, retractable preferred shares; unlimited number of non-voting, redeemable, retractable Class A common shares and an unlimited number of voting common shares; Issued – 562,652 voting common shares (March 3, 2013 – 557,613)

2,169,856

Retained Earnings 1,653,094

Paid-in Capital 80,333

Accumulated other comprehensive income (loss) 30,283

Total Shareholders’ Equity 3,933,566

Total Liabilities and Shareholders’ Equity 5,511,187

Information regarding number of shares:

Balance as at March 3, 2013 557,613

Exercise of stock option 5,039

Balance at March 1, 2014 562,652

Chapter 16 Corporations: The Financial Statements

122

Shareholders’ equity $3,933,566

Shares – end of year 562,652

Book value per share $6.99

AP-9 ( 7 )

Refer to AP-8 above. The RIM income statement shows the following:

Net income $1,293,897

Earnings per share

Basic $2.31

Diluted $2.26

Calculate the earnings per share. Your calculation of EPS may not agree with the numbers shown above. See the Critical Thinking Exercise at the end of this chapter for further discussion.

______________________________________________________________________________

AP-10 ( 7 )

Research in Motion’s balance sheet shows total liabilities of $1,577,621. Refer to the equity section of the statements shown in AP-8 above, and calculate the debt-to-equity ratio. Note your comments on the ratio.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Earnings per share = ($1,293,897) ÷ [(557,613 + 562,652) ÷ 2] = $2.31 per share

Total Liabilities = 1,577,621

Total Equity = 3,933,566

Debt to Equity ratio = 1,577,621 ÷ 3,933,566 = 0.40:1

The ratio is “good” since it is below 1:1

For every $1 invested by owners, lenders have invested 40 cents. The ownership is essentially

more responsible for financing the company.

Chapter 16Corporations: The Financial Statements

123

AP-11 ( 7 )

Part of the financial statements of Toromont Industries is shown below:

Consolidated Statements of Retained EarningsFor the Year Ended December 31, 2007 ($ thousands)

Retained Earnings, beginning of year $477,820

Net Earnings 122,280

Dividends (31,061)

Retained Earnings, end of year $539,039

Calculate the dividend payout ratio and discuss.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AP-12 ( 3 , 4 )

The following information was taken from the accounting records of Cutler Inc. at December 31, 2014. Cutler Inc. is a private corporation and follows GAAP.

Line Item AmountPrior-year error – debit to Retained Earnings 15,000Income tax expense on operating income from discontinued operations 19,600Total dividends 67,000Common shares, 75,000 shares issued 201,000Sales revenue 605,000Interest expense 17,000Operating income, discontinued operations 56,000Loss due to lawsuit 16,000Sales discounts 30,000Income tax savings on sale of discontinued operations (sold at a loss) 8,750General expenses 23,000Income tax expense on continuing operations 73,150Preferred shares, $7.00, 1,000 shares issued 60,000Retained earnings, January 1, 2014 (prior to adjustment) 135,000Loss on sale of discontinued operations 25,000Cost of goods sold 310,000

The dividend payout ratio = dividends ÷ net income = 31,061 ÷ 122,280 = 25%

A dividend payout ratio of 25% may be considered to be reasonable. It leaves 75% of net

income in the company for re-investment. Recall that a high net income does not mean that a

corporation has sufficient cash to pay dividends. In any case paying a dividend equal to 100%

of net income would be unwise.

Chapter 16 Corporations: The Financial Statements

124

Required:

a) Prepare an income statement for the year ended December 31, 2014.

b) Prepare a statement of retained earnings for Cutler Inc. for the year ended December 31, 2014.

c) Calculated the EPS ratio.

Assume a tax rate of 35%. During the year, no new shares were issued or redeemed.

a) Cutler Inc.Income Statement

For the Year Ended December 31, 2014

Sales Revenue $605,000

Less: Sales Discounts (30,000)

Net Sales 575,000

Cost of Goods Sold (310,000)

Gross Profit 265,000

Expenses

General Expenses $23,000

Operating Income 242,000

Other Revenue and Expenses

Interest Expense 17,000

Loss Due to Lawsuit 16,000 33,000

Net Income Before Taxes 209,000

Income Tax Expense 73,150

Income from Continuing Operations 135,850

Discontinued Operations

Operating Income 56,000

Less Income Tax (19,600) 36,400

Loss on Sale of Discontinued Operations (25,000)

Less Income Tax Saving 8,750 (16,250)

Net Income $156,000

Chapter 16Corporations: The Financial Statements

125

b)

Cutler Inc.Statement of Retained Earnings

For the Year Ended, December 31, 2014

Retained earnings, January 1, 2014 (as originally reported) $135,000

Correction to prior-year error - debit (15,000)

Retained earnings, January 1, 2014, as adjusted 120,000

Net Income for current year 156,000

276,000

Dividends for 2014 (67,000)

Retained earnings, December 31, 2014 $209,000

c)

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

AP-13 ( 2 )

For the year that just passed, a company experienced a net loss of $140,000. The revenues and expenses have already been closed to the income summary account. Prepare the final entry to complete the closing process.

Date Account Title and Explanation Debit Credit

Dec 31 Retained Earnings 140,000

Income Summary 140,000

To close net loss for the year to

retained earnings

Since Preferred Dividends = $7.00 x 1,000 = $7,000 and assuming the same number of shares

have been outstanding throughout the year:

EPS = (156,000 – 7,000) ÷ 75,000 = $1.99

Chapter 16 Corporations: The Financial Statements

126

AP-14 ( 2 )

An extract from MC Consulting’s pre-closing trial balance for the year ended December 31, 2014 is shown below. The company’s net income for the year was $82,000.

MC ConsultingTrial Balance (Extract)

December 31, 2014Account Debit Credit

Sales Revenue 240,000Cost of Goods Sold 85,000Salaries Expense 50,000Rent Expense 10,000Income Tax Expense 13,000

Prepare the closing entries for MC Consulting assuming the company uses the income summary account.

Date Account Title and Explanation Debit CreditDec 31 Sales Revenue 240,000

Income Summary 240,000

To close the revenue account

Dec 31 Income Summary 158,000

Cost of Goods Sold 85,000

Salaries Expense 50,000

Rent Expense 10,000

Income Tax Expense 13,000

To close expense accounts

Dec 31 Income Summary 82,000

Retained Earnings 82,000

To close net income for the year

to retained earnings

Chapter 16Corporations: The Financial Statements

127

AP-15 ( 7 )

Marry Inc. provided you following information from its accounting records for year ending December 31, 2014 and 2013.

2014 2013

Income from continuing operations (net of tax) $840,000 $740,000Income from discontinued operations (net of tax) 150,000 70,000Net income 990,000 810,000Each year, 100,000 shares were outstanding. No new shares were issued in either year

1,000,000 1,000,000

Beginning Retained Earnings 1,990,000 1,580,000Current liabilities 560,000 420,000Non-current debt 980,000 760,000Market price per share 15 13Total dividends paid 500,000 400,000

No shares were issued during the two years.

Required:

Calculate the following ratios for both years:

(a) EPS Ratio

(b) EPS for each type of income reported on the income statement

(c) Dividend Payout Ratio

(d) Price- Earnings Ratio.

(e) Debt-To-Equity Ratio

(f) Book Value per Share

(a) EPS Ratio

2014 2013

Average shares = (100,000 + 100,000) ÷ 2 = 100,000 shares

($990,000 ÷ 100,000) ($810,000 ÷ 100,000)

EPS Ratio $9.90 $8.10

(b) EPS for each area reported on the income statement:

2014 2013

Income from continuing operations $8.40 $7.40

Income from discontinued operations $1.50 $0.70

Net income $9.90 $8.10

Chapter 16 Corporations: The Financial Statements

128

(c) Dividend Payout Ratio

Dividend Payout Ratio =Dividends paid in year

Net income after tax (NAT)

2014 2013

Dividend Payout Ratio = $500,000 ÷ 990,000 =$400,000 ÷ 810,000

=51% =49%

(d) Price - Earnings Ratio

2014 2013

Market price per share $15 $13

EPS 9.90 8.10

P/E ($15 ÷ 9.90) 1.52 1.60

(e) Debt-to-Equity Ratio

Sample Calculation for 2014 2014 2013

Total debt = $560,000+980,000 1,540,000 1,180,000

Shareholder’s Equity =$1,990,000+1,000,000+990,000- 500,000

3,480,000 2,990,000

0.44 0.39

(f) Book Value per Share

2014 2013

Shareholders’ Equity $3,480,000 $2,990,000

# of Common Shares 100,000 100,000

34.80 29.90

Chapter 16Corporations: The Financial Statements

129

AP-16 ( 7 )

The following data is available for two companies, Sam Corporation and Tally Corporation for the year ended December 31, 2014.

Sam Corporation

Tally Corporation

Income from continuing operations (net of tax) $710,000 $510,000Income from discontinued operations (net of tax) 120,000 60,000Net income 830,000 570,000Average number of shares outstanding during the year: 100,000 issued by Sam and 50,000 by Tally

800,000 450,000

Beginning Retained Earnings 2,070,000 1,580,000Current liabilities 560,000 420,000Non-current debt 980,000 760,000Market price per share 14 11Total dividends paid 200,000 120,000

Required:

a) Calculate the following ratios for both companies:

1. EPS Ratio2. EPS for each area reported on the income statement3. Dividend Payout Ratio4. Price - Earnings Ratio5. Debt-to-Equity Ratio

1. EPS Ratio

Sam Corporation

Tally Corporation

EPS Ratio $8.30 $11.40

2. EPS for each area reported on the income statement:

Sam Corporation

Tally Corporation

Income from continuing operations $7.10 $10.20

Income from discontinued operations 1.20 1.20

Net income $8.30 $11.40

Chapter 16 Corporations: The Financial Statements

130

3. Dividend Payout Ratio

Sam Corporation

Tally Corporation

Total dividends paid $200,000 $120,000

Net income after tax 830,000 570,000

Dividend payout ratio 24.10 % 21.05%

4. Price - Earnings Ratio

Sam Corporation

Tally Corporation

Market price per share $14 $11

EPS 8.30 11.40

P/E ($14 ÷ $8.30) 1.69 0.96

5. Debt-to-Equity Ratio

Sam Corporation

Tally Corporation

Total debt 1,540,000 1,180,000

Shareholder’s Equity 3,500,000 2,480,000

0.44 0.48

b) Compare the performance and position of the two companies by interpreting the ratios calculated in Part a.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

1. The EPS ratio is an indicator of the profitability of a company. It shows how much of the earnings

belong to each share. The EPS is better for Tally Corporation than Sam Corporation which, on the

surface, may show that Tally is more profitable than Sam (from a common shareholder point of

view). To actually make such a claim, however, other ratios and factors have to be considered.

2. The dividend payout ratio for Sam Corporation is higher than Tally Corporation. So even

though Sam Corporation has a smaller earnings per share, they are paying more of their

earnings to their shareholders in the form of dividends.

3. The price earnings ratio is higher for Sam Corporation. It means that the shares are selling

for 1.69 times the earnings. It should be clear that an increasing P/E ratio may not necessarily

mean the corporation has improved its attractiveness as an investment because shareholders

may suddenly react negatively to the higher share price and sell their shares which will then

cause share prices to fall.

Chapter 16Corporations: The Financial Statements

131

AP-17 ( 3 , 4 )

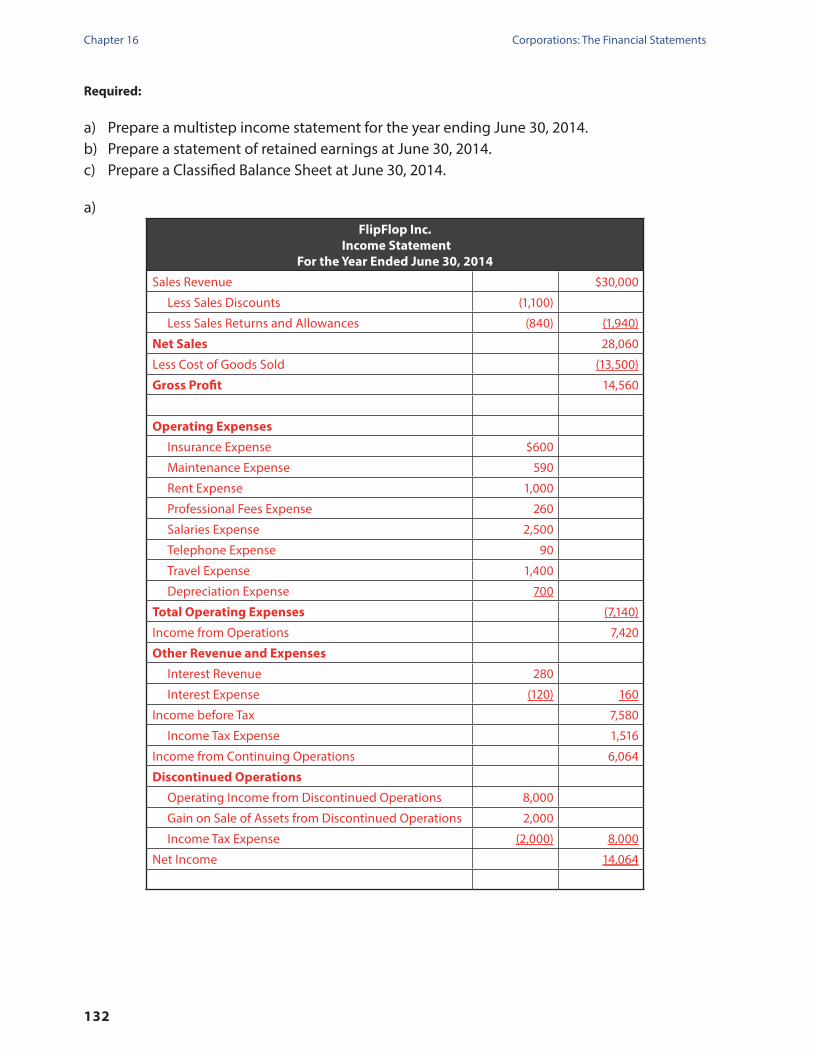

Below is a list of accounts and balances for FlipFlop Inc. for the year ending June 30, 2014. Based on the information provided, answer the required questions.

Account Title BalanceAccounts Payable $8,900Accounts Receivable 6,100Accumulated Depreciation 1,200Bank Loan 21,000Cash 19,000Common Shares 10,000Cost of Goods Sold 13,500Depreciation Expense 700Dividends 3,500Gain on Sale of Assets from Discontinued Operations 2,000Insurance Expense 600Interest Expense 120Interest Revenue 280Income Tax Expense (Continuing Operations) 1,516Income Tax Expense (Discontinued Operations) 2,000Inventory 18,000Maintenance Expense 590Operating Income from Discontinued Operations 8,000Prepaid Insurance 3,250Professional Fees Expense 260Property, Plant & Equipment 25,000Rent Expense 1,000Retained Earnings (beginning balance) 17,986Salaries Expense 2,500Sales Discounts 1,100Sales Returns and Allowances 840Sales Revenue 30,000Telephone Expense 90Travel Expense 1,400Unearned Revenue 1,700

Notes:

Unlimited common shares are authorized and 2,000 have been issued.The bank loan is payable over 5 years and $4,200 will be paid by June 30, 2015.

Chapter 16 Corporations: The Financial Statements

132

Required:

a) Prepare a multistep income statement for the year ending June 30, 2014.b) Prepare a statement of retained earnings at June 30, 2014.c) Prepare a Classified Balance Sheet at June 30, 2014.

a)FlipFlop Inc.

Income StatementFor the Year Ended June 30, 2014

Sales Revenue $30,000

Less Sales Discounts (1,100)

Less Sales Returns and Allowances (840) (1,940)

Net Sales 28,060

Less Cost of Goods Sold (13,500)

Gross Profit 14,560

Operating Expenses

Insurance Expense $600

Maintenance Expense 590

Rent Expense 1,000

Professional Fees Expense 260

Salaries Expense 2,500

Telephone Expense 90

Travel Expense 1,400

Depreciation Expense 700

Total Operating Expenses (7,140)

Income from Operations 7,420

Other Revenue and Expenses

Interest Revenue 280

Interest Expense (120) 160

Income before Tax 7,580

Income Tax Expense 1,516

Income from Continuing Operations 6,064

Discontinued Operations

Operating Income from Discontinued Operations 8,000

Gain on Sale of Assets from Discontinued Operations 2,000

Income Tax Expense (2,000) 8,000

Net Income 14,064

Chapter 16Corporations: The Financial Statements

133

b)

FlipFlop Inc.Statement of Retained Earnings

For the Year Ended June 30, 2014

Beginning Retained Earnings $17,986

Add: Net Income 14,064

Less: Dividends (3,500)

Ending Retained Earnings $28,550

c)

FlipFlop Inc.Balance Sheet

As at June 30, 2014

Assets

Current Assets

Cash $19,000

Accounts Receivable 6,100

Prepaid Insurance 3,250

Inventory 18,000

Total Current Assets $46,350

Non-Current Assets

Property, Plant & Equipment 25,000

Accumulated Depreciation (1,200)

Total Non-Current Assets 23,800

Total Assets $70,150

Liabilities

Current Liabilities

Accounts Payable $8,900

Unearned Revenue 1,700

Bank Loan - Current Portion 4,200

Total Current Liabilities $14,800

Non-Current Liabilities

Bank Loan - Non-Current Portion 16,800

Total Non-Current Liabilities 16,800

Total Liabilities 31,600

Shareholders' Equity

Common Shares 10,000

Retained Earnings 28,550

Total Shareholders’ Equity 38,550

Liabilities & Shareholders’ Equity $70,150

Chapter 16 Corporations: The Financial Statements

134

AP-18 ( 3 , 4 )

Sigmund Corporation has the following account balances. Using this information, prepare a classified balance sheet as at December 31, 2014.

Account Title BalanceAccounts Payable $56,000Accounts Receivable $47,500Accumulated Depreciation $8,600Bank Loan $110,000Cash $17,000Common Shares $42,000Inventory $65,500Preferred Shares $50,000Prepaid Rent $12,000Property, Plant & Equipment $220,000Retained Earnings $91,900Unearned Revenue $3,500

Notes:

Unlimited common shares are authorized and 2,000 have been issued.5,000 preferred shares are authorized and 500 have been issued.The bank loan is payable over 4 years and $27,500 will be paid by December 31, 2015.

Chapter 16Corporations: The Financial Statements

135

Sigmund CorporationBalance Sheet

As at December 31, 2014

Assets

Current Assets

Cash $17,000

Accounts Receivable 47,500

Prepaid Rent 12,000

Inventory 65,500

Total Current Assets $142,000

Non-Current Assets

Property, Plant & Equipment 220,000

Accumulated Depreciation (8,600)

Total Non-Current Assets 211,400

Total Assets $353,400

Liabilities

Current Liabilities

Accounts Payable $56,000

Unearned Revenue 3,500

Bank Loan - Current Portion 27,500

Total Current Liabilities $87,000

Non-Current Liabilities

Bank Loan - Non-Current Portion 82,500

Total Non-Current Liabilities 82,500

Total Liabilities 169,500

Shareholders' Equity

Common Shares 42,000

Preferred Shares 50,000

Retained Earnings 91,900

Total Shareholders' Equity 183,900

Liabilities & Shareholders’ Equity $353,400

Chapter 16 Corporations: The Financial Statements

136

AP-19 ( 3 , 4 )

Spader Inc. had the following account balances at the end of the year. Prepare a multistep income statement for December 31, 2014.

Account Title Balance

Cost of Goods Sold 234,000

Depreciation Expense 6,200

Loss on Sale of Assets from Discontinued Operations 5,700

Insurance Expense 2,700

Interest Expense 600

Income Tax Expense (Continuing Operations) 27,780

Income Tax Expense (Discontinued Operations) 2,220

Maintenance Expense 3,800

Operating Income from Discontinued Operations 16,800

Rent Expense 32,000

Salaries Expense 87,500

Sales Returns and Allowances 3,900

Sales Revenue 520,000

Telephone Expense 4,100

Travel Expense 6,300

Chapter 16Corporations: The Financial Statements

137

Spader Inc. Income Statement

For the Year Ended December 31, 2014

Sales Revenue $520,000

Less Sales Returns and Allowances (3,900)

Net Sales 516,100

Less Cost of Goods Sold (234,000)

Gross Profit 282,100

Operating Expenses

Insurance Expense $2,700

Maintenance Expense 3,800

Rent Expense 32,000

Salaries Expense 87,500

Telephone Expense 4,100

Travel Expense 6,300

Depreciation Expense 6,200

Total Operating Expenses (142,600)

Income from Operations 139,500

Other Revenue and Expenses

Interest Expense (600)

Income before Tax 138,900

Income Tax Expense 27,780

Income from Continuing Operations 111,120

Discontinued Operations

Operating Income from Discontinued Operations 16,800

Loss on Sale of Assets from Discontinued Operations (5,700)

Income Tax Expense (2,220) 8,880

Net Income 120,000

Chapter 16 Corporations: The Financial Statements

138

AP-20 ( 2 )

Aniston Corporation has the following trial balance at the end of their fiscal year. Complete the closing entries at year end, using the income summary account.

Aniston CorporationTrial Balance

For the Year Ended December 31, 2014

Account Title DR CR

Cash 51,000

Accounts Receivable 42,000

Prepaid Insurance 5,000

Accounts Payable 36,000

Unearned Revenue 4,000

Common Shares 30,000

Retained Earnings 6,300

Sales Revenue 162,000

Cost of Goods Sold 72,900

Insurance Expense 2,700

Rent Expense 16,000

Salaries and Wages Expense 38,000

Depreciation Expense 2,300

Income Tax Expense 8,400

Totals 238,300 238,300

Date Description DR CR

Dec 31 Sales Revenue $162,000

Income Summary $162,000

To close the revenue accounts

Dec 31 Income Summary $140,300

Cost of Goods Sold $72,900

Insurance Expense $2,700

Rent Expense $16,000

Salaries and Wages Expense $38,000

Depreciation Expense $2,300

Income Tax Expense $8,400

To close the expense accounts

Dec 31 Income Summary $21,700

Retained Earnings $21,700

To close the income summary account

Chapter 16Corporations: The Financial Statements

139

Exercise Questions

EX-1 ( 3 )

Black Light Environment Everyday (otherwise known as BLEE Inc.) has sales of $370,000 and expenses of $120,000 (before calculation of income tax expense). Prepare a basic income statement on June 30, 2010 for BLEE, taking into account income tax expense. Assume a tax rate of 31%.

BLEE Inc.Income Statement

For the Year Ended June 30, 2010

Sales $370,000

Expenses 120,000

Income Tax Expense 77,500 197,500

Income from Operations $172,500

EX-2 ( 3 , 4 )

The following information was taken from the accounting records of Montana Inc. at May 31, 2011. Montana Inc. is a private corporation and follows GAAP.

Assume a tax rate of 37%. During the year, no new shares were issued or redeemed.

Line Item Amount

Total dividends paid $61,000

Retained earnings, June 1, 2010 (prior to adjustment) $110,000

Net Income $156,000

Prepare a statement of retained earnings for Montana Inc. for the year ended May 31, 2011.

Montana Inc.Statement of Retained EarningsFor the Year Ended May 31, 2011

Retained Earnings, June 1, 2010 $110,000

Net Income $156,000

Dividends ‐$61,000

Retained Earnings, May 31, 2011 $205,000

Chapter 16 Corporations: The Financial Statements

140

EX-3 ( 2 )

On February 1st, Adam Enterprises declares a dividend of $4,800 to common shareholders to be paid on February 4th. Record the journal entry associated with this transaction.

Date Account Title and Explanation Debit Credit

Feb 1 Retained Earnings 4,800

Dividends Payable 4,800

Record dividend payable of $4,800

EX-4 ( 2 )

Information taken from OE Merchandising’s trial balance is shown below:

OE MerchandisingTrial Balance (Extract) September 30, 2010

Debit Credit

Sales Revenue 247,000

Cost of Goods Sold 148,200

Income Tax Expense 20,000

Rent Expense 11,000

Salaries Expense 52,000

Prepare the closing entries for OE Merchandising assuming the company uses the income summary account.

Date Account Title and Explanation Debit CreditSep 30 Sales Revenue 247,000

Income Summary 247,000To close the revenue account

Sep 30 Income Summary 231,200Cost of Goods Sold 148,200Income Tax Expense 20,000Rent Expense 11,000Salaries Expense 52,000

To close expense accounts

Sep 30 Income Summary 15,800Retained Earnings 15,800

To close income summary

Chapter 16Corporations: The Financial Statements

141

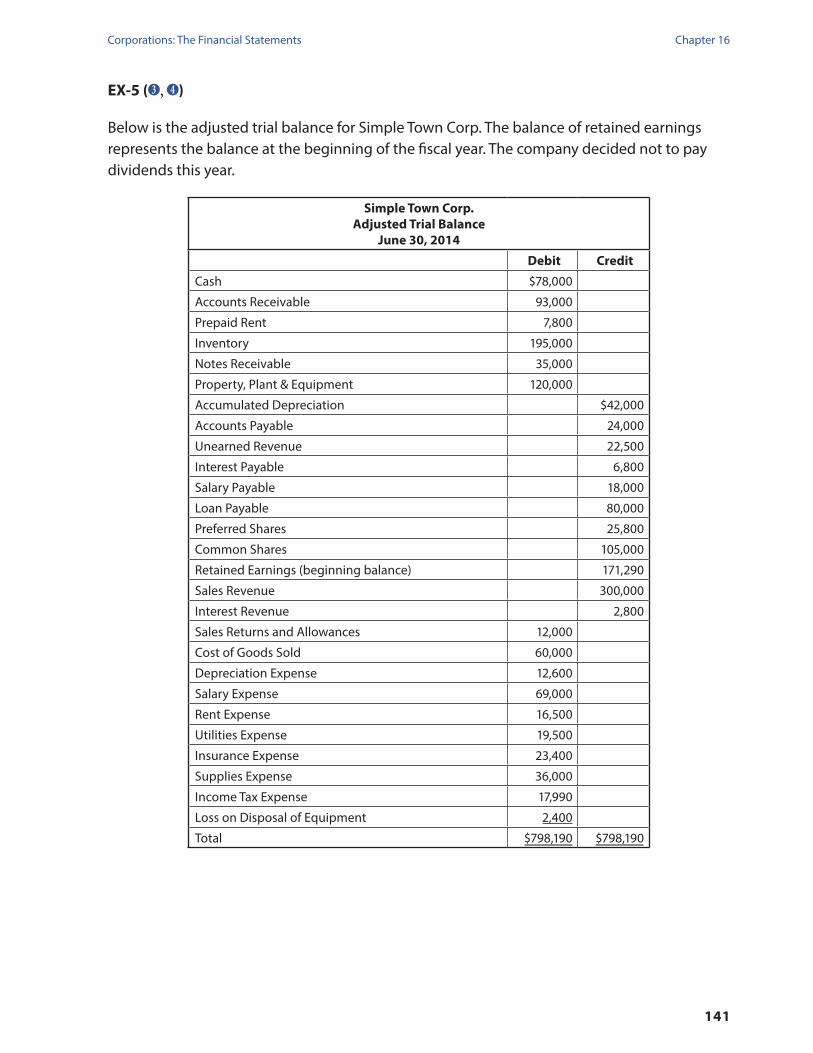

EX-5 ( 3 , 4 )

Below is the adjusted trial balance for Simple Town Corp. The balance of retained earnings represents the balance at the beginning of the fiscal year. The company decided not to pay dividends this year.

Simple Town Corp.Adjusted Trial Balance

June 30, 2014

Debit Credit

Cash $78,000

Accounts Receivable 93,000

Prepaid Rent 7,800

Inventory 195,000

Notes Receivable 35,000

Property, Plant & Equipment 120,000

Accumulated Depreciation $42,000

Accounts Payable 24,000

Unearned Revenue 22,500

Interest Payable 6,800

Salary Payable 18,000

Loan Payable 80,000

Preferred Shares 25,800

Common Shares 105,000

Retained Earnings (beginning balance) 171,290

Sales Revenue 300,000

Interest Revenue 2,800

Sales Returns and Allowances 12,000

Cost of Goods Sold 60,000

Depreciation Expense 12,600

Salary Expense 69,000

Rent Expense 16,500

Utilities Expense 19,500

Insurance Expense 23,400

Supplies Expense 36,000

Income Tax Expense 17,990

Loss on Disposal of Equipment 2,400

Total $798,190 $798,190

Chapter 16 Corporations: The Financial Statements

142

a) Prepare an income statement for the year ended June 30, 2014.

Simple Town Corp.Income Statement

For the year ended June 30, 2014

Sales Revenue $300,000

Less: Sales Returns and Allowances $12,000

Net Sales 288,000

Cost of Goods Sold 60,000

Gross Profit 228,000

Operating Expenses

Depreciation Expense 12,600

Salary Expense 69,000

Rent Expense 16,500

Utilities Expense 19,500

Insurance Expense 23,400

Supplies Expense 36,000 177,000

Income from Operations 51,000

Other Revenue and Expenses

Interest Revenue 2,800

Loss on Disposal of Equipment (2,400) 400

Income Before Tax 51,400

Income Tax Expense 17,990

Net Income $33,410

b) Prepare the statement of retained earnings for Simple Town Corp.

Simple Town Corp.Statement of Retained Earnings

For the year ended June 30, 2014

Retained Earnings, July 1, 2013 $171,290

Add: Net income 33,410

Less: Dividends 0

Retained Earnings, June 30, 2014 $204,700

Chapter 16Corporations: The Financial Statements

143

EX-6 ( 3 , 4 )

Below is the adjusted trial balance for Del Ray Inc. Dividends paid during the year was $7,800.

Del Ray Inc.Adjusted Trial Balance

March 31, 2014

Debit Credit

Cash $33,800

Accounts Receivable 40,300

Prepaid Insurance 5,070

Supplies 84,500

Property, Plant & Equipment 65,000

Accumulated Depreciation $22,750

Accounts Payable 10,400

Unearned Revenue 9,750

Interest Payable 2,250

Loan Payable 25,000

Preferred Shares 14,500

Common Shares 21,700

Retained Earnings (after dividends) 116,110

Sales Revenue 130,000

Gain on Disposal of Equipment 5,200

Sales Discounts 650

Sales Returns and Allowances 1,950

Cost of Goods Sold 26,000

Depreciation Expense 7,150

Salary Expense 29,900

Rent Expense 7,150

Utilities Expense 8,450

Insurance Expense 10,400

Supplies Expense 15,600

Interest Expense 1,250

Income Tax Expense (Continuing Operations) 8,010

Income Tax Expense (Discontinued Operations) 2,880

Income from Discontinued Operations 8,100

Gain on Sale of Assets from Discontinued Operations 1,500

Total $357,660 $357,660

Chapter 16 Corporations: The Financial Statements

144

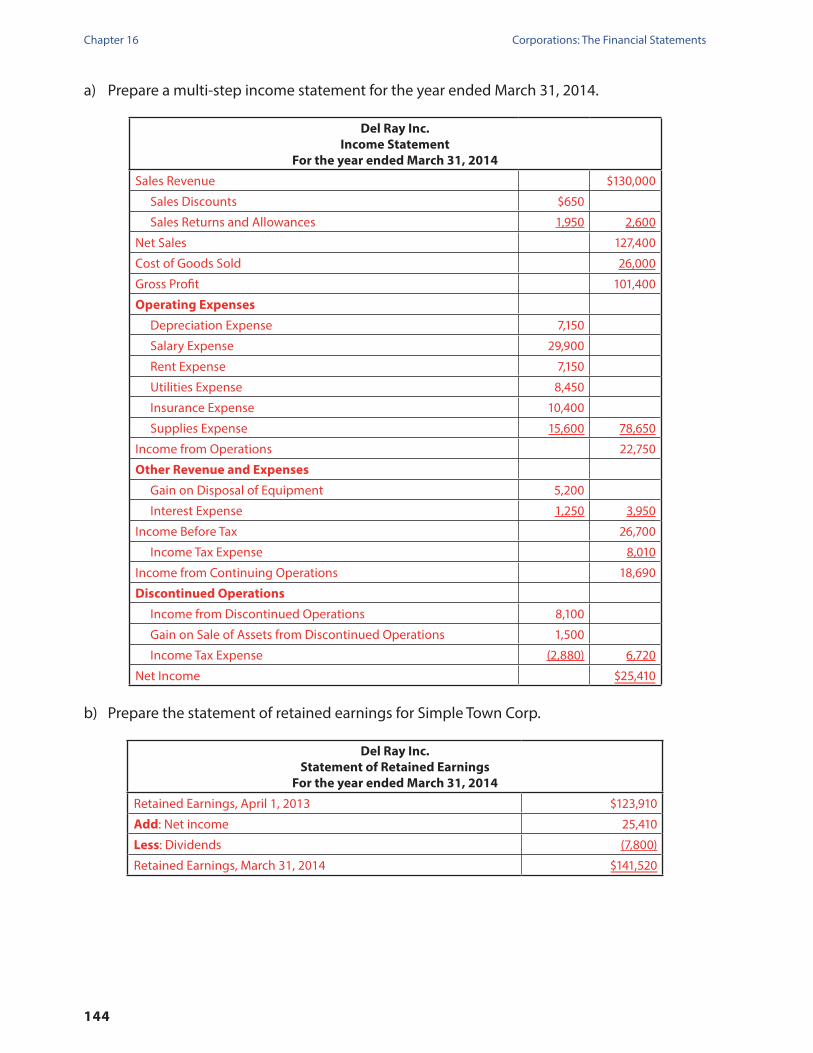

a) Prepare a multi-step income statement for the year ended March 31, 2014.

Del Ray Inc.Income Statement

For the year ended March 31, 2014

Sales Revenue $130,000

Sales Discounts $650

Sales Returns and Allowances 1,950 2,600

Net Sales 127,400

Cost of Goods Sold 26,000

Gross Profit 101,400

Operating Expenses

Depreciation Expense 7,150

Salary Expense 29,900

Rent Expense 7,150

Utilities Expense 8,450

Insurance Expense 10,400

Supplies Expense 15,600 78,650

Income from Operations 22,750

Other Revenue and Expenses

Gain on Disposal of Equipment 5,200

Interest Expense 1,250 3,950

Income Before Tax 26,700

Income Tax Expense 8,010

Income from Continuing Operations 18,690

Discontinued Operations

Income from Discontinued Operations 8,100

Gain on Sale of Assets from Discontinued Operations 1,500

Income Tax Expense (2,880) 6,720

Net Income $25,410

b) Prepare the statement of retained earnings for Simple Town Corp.

Del Ray Inc.Statement of Retained Earnings

For the year ended March 31, 2014

Retained Earnings, April 1, 2013 $123,910

Add: Net income 25,410

Less: Dividends (7,800)

Retained Earnings, March 31, 2014 $141,520

Chapter 16Corporations: The Financial Statements

145

EX-7 ( 4 )

Below is the adjusted trial balance for Connection Communications Inc. for the month of September 2014. Dividends of $5,800 were declared and paid in the month.

Connection Communications Inc.Adjusted Trial Balance

September 30, 2014

Debit Credit

Accounts Payable $5,176

Accounts Receivable $20,057

Accumulated Depreciation 11,325

Cash 16,822

Common Shares 11,600

Cost of Goods Sold 12,940

Depreciation Expense 3,395

Insurance Expense 1,545

Interest Expense 1,225

Interest Payable 2,083

Loan Payable 24,500

Preferred Shares 4,500

Prepaid Insurance 1,850

Property, Plant & Equipment 32,350

Rent Expense 3,550

Retained Earnings (after dividends) 23,300

Salary Expense 8,160

Salary Payable 3,882

Sales Revenue 64,700

Supplies 42,055

Supplies Expense 7,764

Unearned Revenue 4,852

Utilities Expense 4,205

Total $155,918 $155,918

Prepare a statement of retained earnings for the month ended September 30, 2014.

Connection Communications Inc.Statement of Retained Earnings

For the month ended September 30, 2014

Retained Earnings, September 1, 2014 $29,100

Add: Net income 21,916

Less: Dividends (5,800)

Retained Earnings, September 30, 2014 $45,216

Chapter 16 Corporations: The Financial Statements

146

EX-8 ( 4 )

Top Cuisine Inc. has a March 31 year end. Retained earnings at March 31, 2012 had a credit balance of $54,700. During the 2013 fiscal year net income was $24,615 and dividends of $12,600 were declared and paid. During the 2014 fiscal year Top Cuisine had a net loss of $16,680 and dividends of $10,400 were declared but not yet paid.

Calculate Top Cuisine’s retained earnings as at March 31, 2014 by completing the following statements:

Top Cuisine Inc.Statement of Retained Earnings

For the year ended March 31, 2013

Retained Earnings, March 31, 2012 $54,700

Add: Net Income 24,615

Less: Dividends (12,600)

Retained Earnings, March 31, 2013 $66,715

Top Cuisine Inc.Statement of Retained Earnings

For the year ended March 31, 2014

Retained Earnings, March 31, 2013 $66,715

Less: Net Loss (16,680)

Less: Dividends (10,400)

Retained Earnings, March 31, 2014 $39,635

EX-9 ( 4 , 5 )

Kensington Inc. has a December 31 year end. Retained earnings as at December 31, 2012 had a debit balance of $15,450. During the 2013 fiscal year net income was $91,550 and dividends of $34,500 were declared and paid.

Complete Kensington Corp.’s statement of retained earnings for 2013.

Kensington Inc.Statement of Retained Earnings

For the year ended December 31, 2013

Retained Earnings, December 31, 2012 ($15,450)

Add: Net income 91,550

Less: Dividends (34,500)

Retained Earnings, December 31, 2013 $41,600

During the 2014 fiscal year Kensington had a net income of $32,100 and dividends of $28,000 were declared and paid. An audit revealed that the 2013 net income was understated by a net value of $5,200. A new engine was recorded as an expense when it should have been recorded as an asset.

Chapter 16Corporations: The Financial Statements

147

Complete Kensington Corp.’s statement of retained earnings for 2014.

Kensington Inc.Statement of Retained Earnings

For the year ended December 31, 2014

Retained Earnings, December 31, 2013 $41,600

Add: Prior Year Adjustment 5,200

Add: Net Income 32,100

Less: Dividends (28,000)

Retained Earnings, December 31, 2014 $50,900

EX-10 ( 6 )

Below is the adjusted trial balance for Home Care Solutions Inc.:

Home Care Solutions Inc.Adjusted Trial Balance

June 30, 2014

Debit Credit

Accounts Payable $71,200

Accounts Receivable $80,000

Accumulated Depreciation 28,000

Cash 63,850

Common Shares 10,400

Cost of Goods Sold 96,000

Depreciation Expense 35,200

Insurance Expense 36,000

Interest Expense 21,120

Interest Payable 14,960

Inventory 90,000

Loan Payable 176,000

Preferred Shares 7,200

Prepaid Rent 28,000

Property, Plant & Equipment 176,000

Rent Expense 66,000

Retained Earnings (after dividends) 40,810

Salary Expense 72,000

Salary Payable 34,000

Sales Returns 12,000

Sales Revenue 400,000

Unearned Revenue 49,600

Utilities Expense 56,000

Total $832,170 $832,170

Chapter 16 Corporations: The Financial Statements

148

Additional information:• Netincomefortheyearwas$5,680andtheretainedearningsatJuly1,2013was

$44,960. Dividends of $4,150 were declared and paid in the year. • HomeCareSolutionshasaloanpayableduein8years.Theprincipalpaymentsare

$2,800 per month. • 1,440$2,cumulativepreferredshareshavebeenissuedand15,000havebeen

authorized. 3,000 common shares have been issued and 45,000 have been authorized.

Prepare a classified balance sheet as at June 30, 2014.

Home Care Solutions Inc.Balance Sheet

As at June 30, 2014Assets Current Assets

Cash $63,850 Accounts Receivable 80,000 Prepaid Rent 28,000 Inventory 90,000

Total Current Assets $261,850 Non-Current Assets

Property, Plant & Equipment 176,000 Less: Accumulated Depreciation (28,000) 148,000

Total Assets $409,850 Liabilities Current Liabilities

Accounts Payable $71,200 Unearned Revenue 49,600 Interest Payable 14,960 Salary Payable 34,000 Current portion of Bank Loan 33,600

Total Current Liabilities $203,360 Non-Current Liabilities

Long-term portion of Bank Loan 142,400 Total Liabilities 345,760 Shareholders’ Equity Contributed Capital

Preferred shares, $2, cumulative, 15,000 shares authorized, 1,440 shares issued and outstanding 7,200

Common shares, 45,000 shares authorized, 3,000 shares issued and outstanding 10,400

Total Contributed Capital 17,600 Retained Earnings 46,490 Total Shareholders’ Equity 64,090 Total Liabilities and Shareholders’ Equity $409,850

Chapter 16Corporations: The Financial Statements

149

EX-11 ( 6 )

Below is the adjusted trial balance for Busy Town Inc.:

Busy Town Inc.Adjusted Trial Balance

December 31, 2014

Debit Credit

Accounts Payable $69,420

Accounts Receivable $78,000

Accumulated Depreciation 27,300

Cash 66,300

Common Shares 147,500

Cost of Goods Sold 93,600

Depreciation Expense 34,320

Insurance Expense 35,100

Interest Payable 936

Interest Receivable 1,560

Interest Revenue 10,400

Inventory 87,750

Long term Debt 46,800

Loss on Sale of Equipment 1,800

Notes Receivable 130,000

Preferred Shares 148,530

Prepaid Insurance 27,300

Property, Plant & Equipment 171,600

Rent Expense 64,350

Retained Earnings 5,784

Salary Expense 70,200

Salary Payable 33,150

Sales Returns 11,700

Sales Revenue 390,000

Unearned Revenue 48,360

Utilities Expense 54,600

Total $928,180 $928,180

Additional information:• Net income for the year was $34,730 and retained earnings at January 1, 2014 was

$70,484. Dividends of $64,700 were declared and paid in the year.• BusyTownhasanotereceivablethatmaturesinDecember2017,withno

installment payments received until maturity. Busy Town also has long term debt that is due in 4 years. The principal payments are $975 per month.

• Preferredsharesare$1,non-cumulative,95,000shareshavebeenauthorizedand24,700 shares are issued and outstanding. For common shares, 200,000 shares have been authorized and 29,800 shares have been issued.

Chapter 16 Corporations: The Financial Statements

150

Prepare a classified balance sheet as at December 31, 2014.

Busy Town Inc.Balance Sheet

As at December 31, 2014

Assets

Current Assets

Cash $66,300

Accounts Receivable 78,000

Interest Receivable 1,560

Prepaid Insurance 27,300

Inventory 87,750

Total Current Assets $260,910

Non-Current Assets

Notes Receivable 130,000

Property, Plant & Equipment 171,600

Less: Accumulated Depreciation (27,300)

Total Non-Current Assets 274,300

Total Assets $535,210

Liabilities

Current Liabilities

Accounts Payable $69,420

Unearned Revenue 48,360

Interest Payable 936

Salary Payable 33,150

Current Portion of Long Term Debt 11,700

Total Current Liabilities $163,566

Non-Current Liabilities

Long Term Debt 35,100

Total Liabilities 198,666

Shareholders’ Equity

Contributed Capital

Preferred shares, $1, non-cumulative, 95,000 shares

authorized, 24,700 shares issued and outstanding 148,530

Common shares, 200,000 shares authorized, 29,800

shares issued and outstanding 147,500

Total Contributed Capital 296,030

Retained Earnings 40,514

Total Shareholders’ Equity 336,544

Total Liabilities and Shareholders’ Equity $535,210

Chapter 16Corporations: The Financial Statements

151

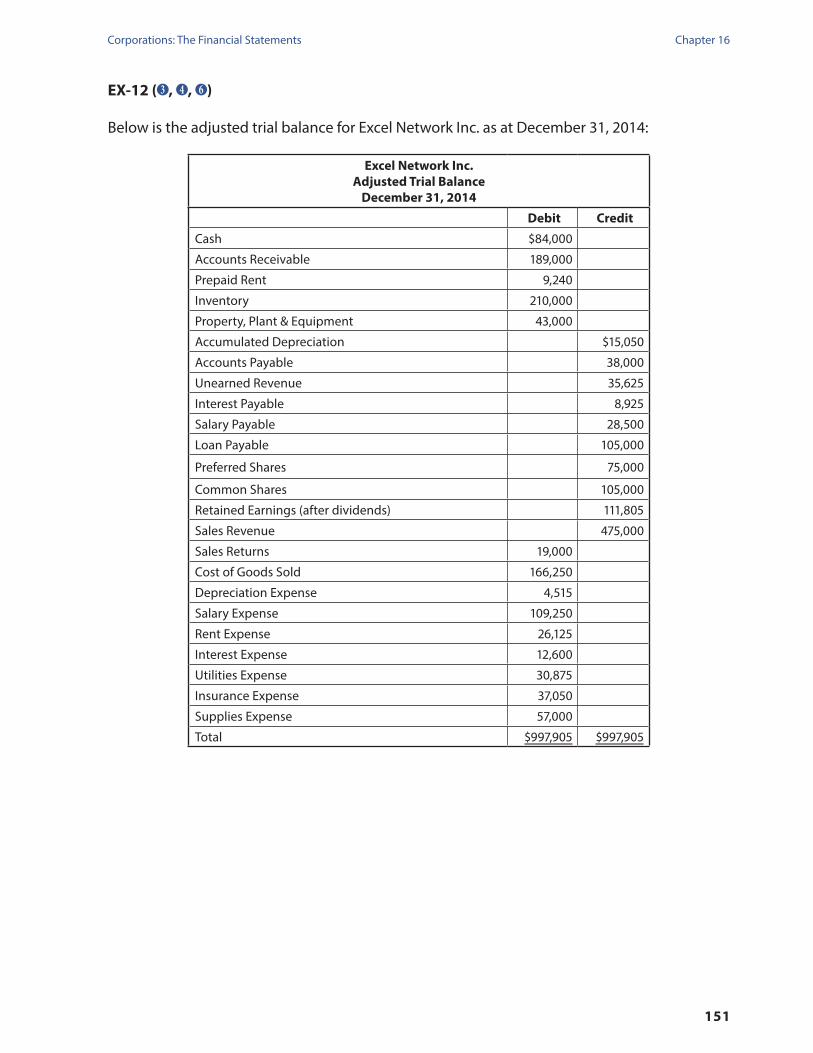

EX-12 ( 3 , 4 , 6 )

Below is the adjusted trial balance for Excel Network Inc. as at December 31, 2014:

Excel Network Inc.Adjusted Trial Balance

December 31, 2014

Debit Credit

Cash $84,000

Accounts Receivable 189,000

Prepaid Rent 9,240

Inventory 210,000

Property, Plant & Equipment 43,000

Accumulated Depreciation $15,050

Accounts Payable 38,000

Unearned Revenue 35,625

Interest Payable 8,925

Salary Payable 28,500

Loan Payable 105,000

Preferred Shares 75,000

Common Shares 105,000

Retained Earnings (after dividends) 111,805

Sales Revenue 475,000

Sales Returns 19,000

Cost of Goods Sold 166,250

Depreciation Expense 4,515

Salary Expense 109,250

Rent Expense 26,125

Interest Expense 12,600

Utilities Expense 30,875

Insurance Expense 37,050

Supplies Expense 57,000

Total $997,905 $997,905

Chapter 16 Corporations: The Financial Statements

152

a) Prepare a multi-step income statement for the year ended December 31, 2014. Ignore income taxes.

Excel Network Inc.Income Statement

For the year ended December 31, 2014

Sales Revenue $475,000

Less: Sales Returns (19,000)

Net Sales 456,000

Cost of Goods Sold 166,250

Gross Profit 289,750

Operating Expenses

Depreciation Expense $4,515

Salary Expense 109,250

Rent Expense 26,125

Utilities Expense 30,875

Insurance Expense 37,050

Supplies Expense 57,000 264,815

Income from Operations 24,935

Other Revenue and Expenses

Interest Expense 12,600

Total Other Revenue and Expenses 12,600

Net Income $12,335

b) The retained earnings at January 1, 2014 were $160,305 and dividends of $48,500 were declared in the year. Prepare a statement of retained earnings for the year ended December 31, 2014.

Excel Network Inc.Statement of Retained Earnings

For the year ended December 31, 2014

Retained Earnings, January 1, 2014 $160,305

Add: Net income 12,335

Less: Dividends (48,500)

Retained Earnings, December 31, 2014 $124,140

c) Prepare a classified balance sheet as at December 31, 2014. Additional information as of December 31, 2014 is as follows:

• The loan payable is due over 5 years. The principal payments are $1,000 for each month.

• Preferredshares:$8,cumulative,100,000sharesauthorizedand25,000havebeenissued and are outstanding.

• Commonshares:unlimitednumberofsharesauthorized,46,000shareshavebeenissue and are outstanding.

Chapter 16Corporations: The Financial Statements

153

Excel Network Inc.Balance Sheet

As at December 31, 2014

Assets

Current Assets

Cash $84,000

Accounts Receivable 189,000

Prepaid Rent 9,240

Inventory 210,000

Total Current Assets $492,240

Non-Current Assets

Property, Plant & Equipment 43,000

Less Accumulated Depreciation (15,050)

Total Non-Current Assets 27,950

Total Assets $520,190

Liabilities

Current Liabilities

Accounts Payable $38,000

Unearned Revenue 35,625

Interest Payable 8,925

Salary Payable 28,500

Current Portion of Bank Loan 12,000

Total Current Liabilities $123,050

Non-Current Liabilities

Long-Term Portion of Bank Loan 93,000

Total Liabilities 216,050

Shareholders’ Equity

Contributed Capital

Preferred shares, $8, cumulative, 100,000

authorized, 25,000 issued and outstanding 75,000

Common shares, unlimited authorized, 46,000

issued and outstanding 105,000

Total Contributed Capital 180,000

Retained Earnings 124,140

Total Shareholders’ Equity 304,140

Total Liabilities and Shareholders’ Equity $520,190

Chapter 16 Corporations: The Financial Statements

154

EX-13 ( 3 , 4 , 6 )

Below is the adjusted trial balance for SandStone Corp. as at September 30, 2014:

SandStone Corp.Adjusted Trial Balance

September 30, 2014

Debit Credit

Accounts Payable $20,470

Accounts Receivable $23,000

Accumulated Depreciation 8,050

Cash 19,550

Common Shares 8,750

Cost of Goods Sold 40,250

Depreciation Expense 10,120

Gain on Disposal of Equipment 2,530

Gain on Sale of Assets from Discontinued Operations 13,400

Income Tax Benefit (Continuing Operations) 10,788

Income Tax Benefit (Discontinued Operations) 6,240

Insurance Expense 10,350

Interest Expense 5,520

Interest Payable 3,910

Inventory 25,875

Loan Payable 46,000

Loss from Discontinued Operations 29,000

Preferred Shares 5,890

Prepaid Insurance 8,050

Property, Plant & Equipment 50,600

Rent Expense 19,550

Retained Earnings 35,512

Sales Discounts 11,060

Salary Expense 20,700

Salary Payable 9,775

Sales Returns and Allowances 3,450

Sales Revenue 115,000

Supplies Expense 7,400

Unearned Revenue 14,260

Utilities Expense 16,100

Total $300,575 $300,575

Chapter 16Corporations: The Financial Statements

155

a) Prepare a multi-step income statement for the year ended September 30, 2014.

SandStone Corp.Income Statement

For the year ended September 30, 2014

Sales Revenue $115,000

Sales Discounts $11,060

Sales Returns and Allowances 3,450 14,510

Net Sales 100,490

Cost of Goods Sold 40,250

Gross Profit 60,240

Operating Expenses

Depreciation Expense 10,120

Salary Expense 20,700

Rent Expense 19,550

Supplies Expense 7,400

Utilities Expense 16,100

Insurance Expense 10,350 84,220

Income (Loss) from Operations (23,980)

Other Revenue and Expenses

Gain on disposal of equipment 2,530

Interest Expense (5,520) (2,990)

Income (Loss) Before Tax (26,970)

Income Tax Benefit 10,788

Income from Continuing Operations (16,182)

Discontinued Operations

Gain on Sale of Assets from Discontinued Operations 13,400

Loss from Discontinued Operations (29,000)

Income Tax Benefit 6,240 (9,360)

Net Income (Loss) ($25,542)

b) The balance of retained earnings in the adjusted trial balance represents the beginning balance at October 1, 2013. No dividends were declared during the year. Prepare a statement of retained earnings for the year ended September 30, 2014.

SandStone Corp.Statement of Retained Earnings

September 30, 2014

Retained Earnings, October 1, 2013 $35,512

Less: Net Loss (25,542)

Less: Dividends 0

Retained Earnings, September 30, 2014 $9,970

Chapter 16 Corporations: The Financial Statements

156

c) Prepare a classified balance sheet as at September 30, 2013. Additional information is as follows:

• Theloanpayableisdueover4years.Theprincipalpaymentsare$1,050eachmonth• Preferredshares:$1,cumulative,55,000authorized,7,800issuedandoutstanding• Commonshares:100,000authorized,15,900issuedandoutstanding

SandStone Corp.Balance Sheet

As at September 30, 2014

Assets

Current Assets

Cash $19,550

Accounts Receivable 23,000

Prepaid Insurance 8,050

Inventory 25,875

Total Current Assets $76,475

Non-Current Assets

Property, Plant & Equipment 50,600

Less Accumulated Depreciation (8,050)

Total Non-Current Assets 42,550

Total Assets $119,025

Liabilities

Current Liabilities

Accounts Payable $20,470

Unearned Revenue 14,260

Interest Payable 3,910

Salary Payable 9,775

Current portion of Bank Loan 12,600

Total Current Liabilities $61,015

Non-Current Liabilities

Long-term portion of Bank Loan 33,400

Total Liabilities 94,415

Shareholders’ Equity

Contributed Capital

Preferred shares, $1, cumulative, 55,000 shares

authorized, 7,800 shares issued and outstanding 5,890

Common shares, 100,000 shares authorized, 15,900

shares issued and outstanding 8,750

Total Contributed Capital 14,640

Retained Earnings 9,970

Total Shareholders’ Equity 24,610

Total Liabilities and Shareholders’ Equity $119,025

Chapter 16Corporations: The Financial Statements

157

EX-14 ( 3 , 4 , 6 )

Below is the adjusted trial balance for Elements Inc. as at March 31, 2014:

Elements Inc.Adjusted Trial Balance

March 31, 2014

Debit Credit

Accounts Payable $19,580

Accounts Receivable $22,000

Accumulated Depreciation 7,700

Cash 18,700

Common Shares 21,500

Cost of Goods Sold 37,400

Depreciation Expense 9,900

Insurance Expense 9,900

Interest Payable 660

Interest Receivable 1,320

Interest Revenue 2,640

Inventory 24,750

Long Term Debt 13,200

Loss on Disposal of Machinery 1,485

Notes Receivable 33,000

Preferred Shares 19,850

Prepaid Insurance 7,700

Property, Plant & Equipment 49,500

Rent Expense 18,150

Retained Earnings (after dividends) 54,185

Salary Expense 19,800

Salary Payable 9,350

Sales Returns and Allowances 3,300

Sales Revenue 110,000

Unearned Revenue 13,640

Utilities Expense 15,400

Total $272,305 $272,305

Chapter 16 Corporations: The Financial Statements

158

a) Prepare a multi-step income statement for the year ended March 31, 2014. Ignore taxes for this question.

Elements Inc.Income Statement

For the Year Ended March 31, 2014

Sales Revenue $110,000

Less: Sales Returns and Allowances 3,300

Net Sales 106,700

Cost of Goods Sold 37,400

Gross Profit 69,300

Operating Expenses

Depreciation Expense 9,900

Salary Expense 19,800

Rent Expense 18,150

Utilities Expense 15,400

Insurance Expense 9,900

Total Operating Expenses 73,150

Income (Loss) from Operations (3,850)

Other Revenue and Expenses

Interest Revenue 2,640

Loss on Disposal of Equipment 1,485

Total Other Revenue and Expenses 1,155

Net Loss ($2,695)

b) Retained earnings at April 1, 2013 had a credit balance of $68,335 and dividends of $14,150 were declared and paid in the year. Prepare a statement of retained earnings for the year ended March 31, 2014.

Elements Corp.Statement of Retained Earnings

For the Year Ended March 31, 2014

Retained Earnings, April 1, 2013 $68,335

Less: Net Loss (2,695)

Less: Dividends (14,150)

Retained Earnings, March 31, 2014 $51,490

c) Prepare a classified balance sheet as at March 31, 2014. Additional information as of March 31, 2014 is as follows:

• Thelongtermdebtisdueover4years.Theprincipalpaymentsare$275eachmonth.

• Preferredshares:$0.50,non-cumulative,15,000sharesauthorized,13,233sharesissued and outstanding.

• Commonshares:21,000sharesauthorized,19,550sharesissuedandoutstanding.• The note receivable will not be paid until December 2015.

Chapter 16Corporations: The Financial Statements

159

Elements Inc.Balance Sheet

As at March 31, 2014

Assets

Current Assets

Cash $18,700

Accounts Receivable 22,000

Interest Receivable 1,320

Prepaid Insurance 7,700

Inventory 24,750

Total Current Assets $74,470

Non-Current Assets

Notes Receivable 33,000

Property, Plant & Equipment 49,500

Less: Accumulated Depreciation (7,700)

Total Non-Current Assets 74,800

Total Assets $149,270

Liabilities

Current Liabilities

Accounts Payable $19,580

Unearned Revenue 13,640

Interest Payable 660

Salary Payable 9,350

Current Portion of Long Term Debt 3,300

Total Current Liabilities $46,530

Non-Current Liabilities

Long Term Debt 9,900

Total Liabilities 56,430

Shareholders’ Equity

Contributed Capital

Preferred shares, $0.50, non-cumulative, 15,000

authorized, 13,233 issued and outstanding 19,850

Common shares, 20,000 authorized, 19,550

issued and outstanding 21,500

Total Contributed Capital 41,350

Retained Earnings 51,490

Total Shareholders’ Equity 92,840

Total Liabilities and Shareholders’ Equity $149,270

Chapter 16 Corporations: The Financial Statements

160

Case Study

CS-1 ( 7 )

Obtain the current financial statements of a large capitalization company (i.e. > $5 Billion), and answer the following questions.

The details for Kroger’s January 31, 2009 financial statements have been included as an example.

a) Name of company Kroger Co.

b) Capitalization of the company $14.85B

c) Industry in which the company is engaged Food Market

d) Contributed capital amount $955m

e) Retained earnings amount $7,489m

f ) Total Liabilities $17,940m

g) Total shareholders' equity $5,176m

h) Debt-to-Equity Ratio 17,940 ÷ 5,176 = 3.47

i) Earnings per share (basic) $1.92

j) Dividend per share $0.36

k) Dividend payout ratio 0.19

l) Book value per share (show calculation) 5176 ÷ [(955 + 947) ÷ 2] = $5.44

m) Current market price per share (note the date) $22.82 (Nov 19, 2009)

Chapter 16Corporations: The Financial Statements

161

Critical Thinking

CT-1 ( 7 )

In this chapter, you have learned how to calculate earnings per share. Often, a corporation’s annual report will report earnings per share as calculated by the corporation. Rarely do the corporation’s reported earnings per share agree with a financial analyst’s calculation of this number. Discuss why these two calculations may differ.

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

______________________________________________________________________________

Since these calculations per share involve only two numbers, the earnings and average

number of shares, the difference in the values must result from a difference in either of the

two numbers involved in the calculations. Since earnings are fixed, the differences arise from

the calculation of average number of shares. The average number of shares can be calculated

in several ways – daily, weekly, month-end or year-end. The calculation described in this

chapter uses year-end figures to calculate EPS. The corporation may use one of the other

methods in order to increase the accuracy of the calculations. This is easy for the corporation

because it has access to detailed share holding records. Financial analysts, however, only have

access to the year-end numbers.

Chapter 16 Corporations: The Financial Statements

162

CT-2 ( 3 , 4 )

The following information was taken from the accounting records of Splinter Inc. at December 31, 2014. Splinter Inc. is a public corporation and follows IFRS.

Line Item Amount

Common shares, 50,000 outstanding on January 1, 2014 $350,000

Common shares, 70,000 outstanding on December 31, 2014 120,000

Cost of Goods Sold 468,000

Dividends paid 50,000

Gain on Sale of Assets 6,200

General operating expenses 210,000

Income tax expense on continuing operations 29,850

Income tax expense on operating income from discontinued operations 18,600

Interest Expense 8,700

Operating income from discontinued operations 62,000

Prior year error – debit to Retained Earnings 6,000

Retained Earnings, January 1, 2014 (prior to adjustment) 410,000

Sales revenue 780,000

Required:

a) Prepare the statement of comprehensive income for the year ended December 31, 2014.

b) Prepare the statement of changes in equity for the year ended December 31, 2014 showing the changes in contributed capital and retained earnings.

Chapter 16Corporations: The Financial Statements

163

a) Statement of Comprehensive Income

Splinter Inc.Statement of Comprehensive Income

For the Year Ended December 31, 2014

Sales Revenue $780,000

Cost of Goods Sold 468,000

Gross Profit 312,000

Operating Expenses

General Operating Expense 210,000

Results from Operating Activities 102,000

Other Revenue and Expenses

Gain on Sale of Assets 6,200

Interest Expense (8,700) (2,500)

Income before Tax 99,500

Income Tax Expense 29,850

Income from Continuing Operations 69,650

Discontinued Operations

Operating Income from Discontinued Operations 62,000

Less: Income Tax Expense (18,600) 43,400

Total Comprehensive Income for the Period $113,050

b) Statement of Changes in Equity

Splinter Inc.Statement of Changes in Equity

For the Year Ended December 31, 2014

Contributed

CapitalRetained Earnings Total

Balance at January 1, 2014 350,000 410,000 760,000

Adjustment to Correct Error from 2013 (6,000)

Total Comprehensive Income for the Period 113,050 113,050

Contributions by and Distributions to Owners

Issued Common Shares 120,000 120,000

Dividends to Shareholders (50,000) (50,000)

Total Contributions by and Distributions to Owners 120,000 (50,000) 70,000

Balance at December 31, 2014 470,000 467,050 937,050

164

Notes

Chapter 16 Corporations: The Financial Statements