cost accounting

DESCRIPTION

Cost Accounting. Dr. Baldwin University of Arkansas – Fort Smith Fall 2010. CHAPTER 1. The Accountant’s Role in the Organization. Accounting Disciplines. Financial Accounting focus on external users and GAAP rules Managerial Accounting – - PowerPoint PPT PresentationTRANSCRIPT

Cost Accounting

Dr. BaldwinUniversity of Arkansas – Fort

SmithFall 2010

CHAPTER 1

The Accountant’s Role in the Organization

Accounting Disciplines

• Financial Accounting – focus on external users and GAAP

rules• Managerial Accounting –

– focus on internal users and is not necessarily GAAP-driven. Also provides data for financial accounting. This includes:• Cost Accounting• Cost Management

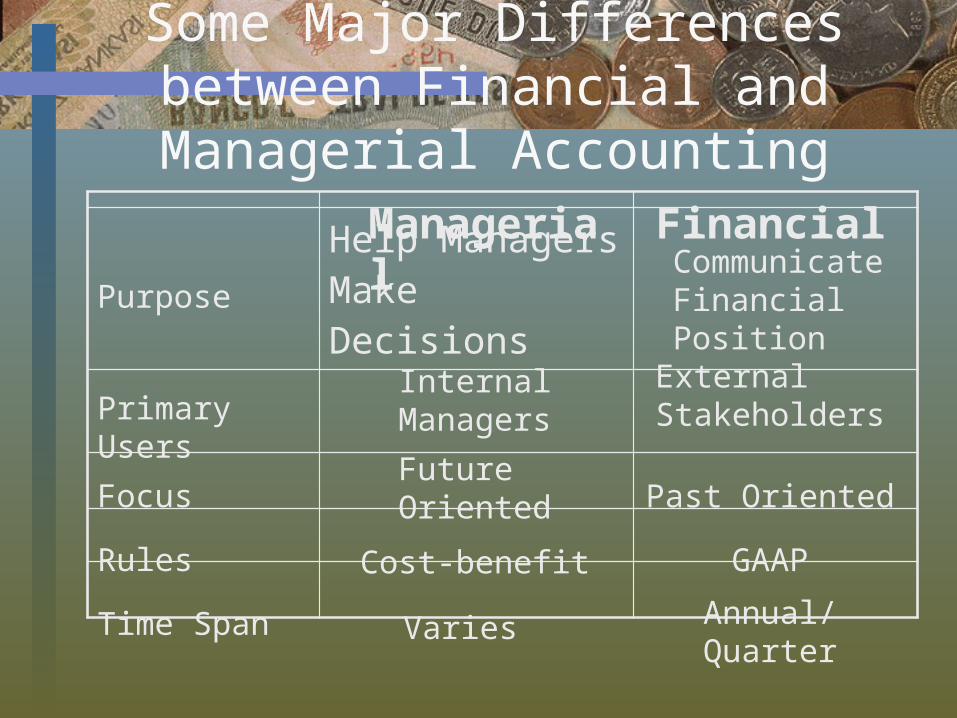

Some Major Differences between Financial and Managerial Accounting

Help Managers Make Decisions

Managerial Financial

Purpose

Primary Users

Focus

Rules

Time Span

Communicate Financial Position

Internal ManagersExternal Stakeholders

Future Oriented Past Oriented

Cost-benefit GAAP

Varies Annual/Quarter

Strategy and Management Accounting

• Strategy – specifies how an organization

matches its own capabilities with the opportunities in the marketplace to accomplish its objectives

• Strategic Cost Management – focuses specifically on the cost

dimension within the overall strategy

Strategy and Management Accounting

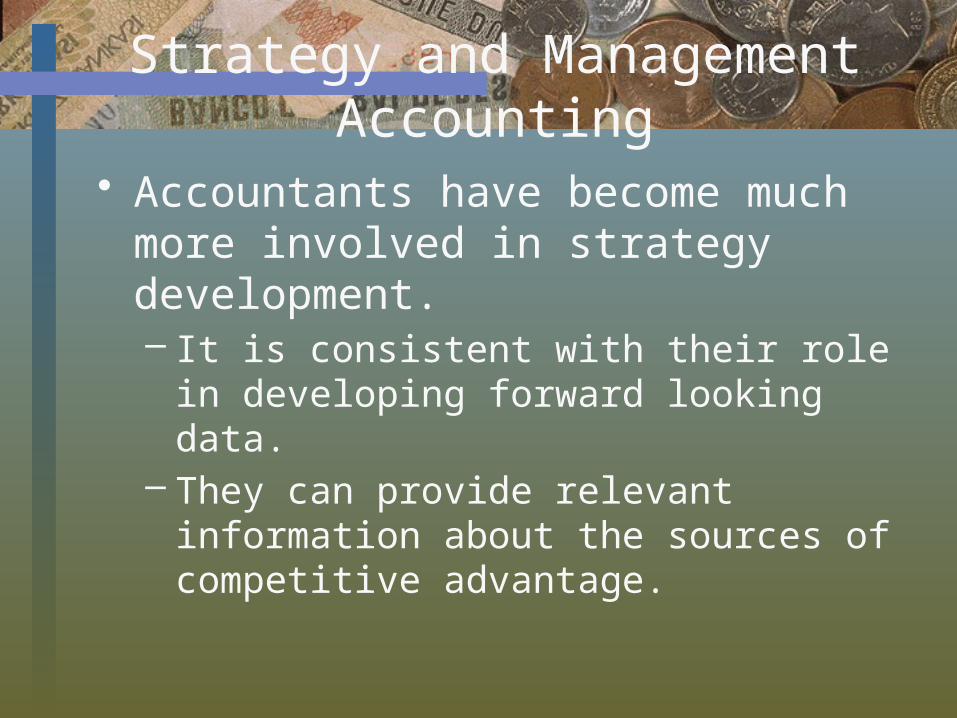

• Accountants have become much more involved in strategy development.– It is consistent with their role in

developing forward looking data.– They can provide relevant information

about the sources of competitive advantage.

Strategy and Management Accounting

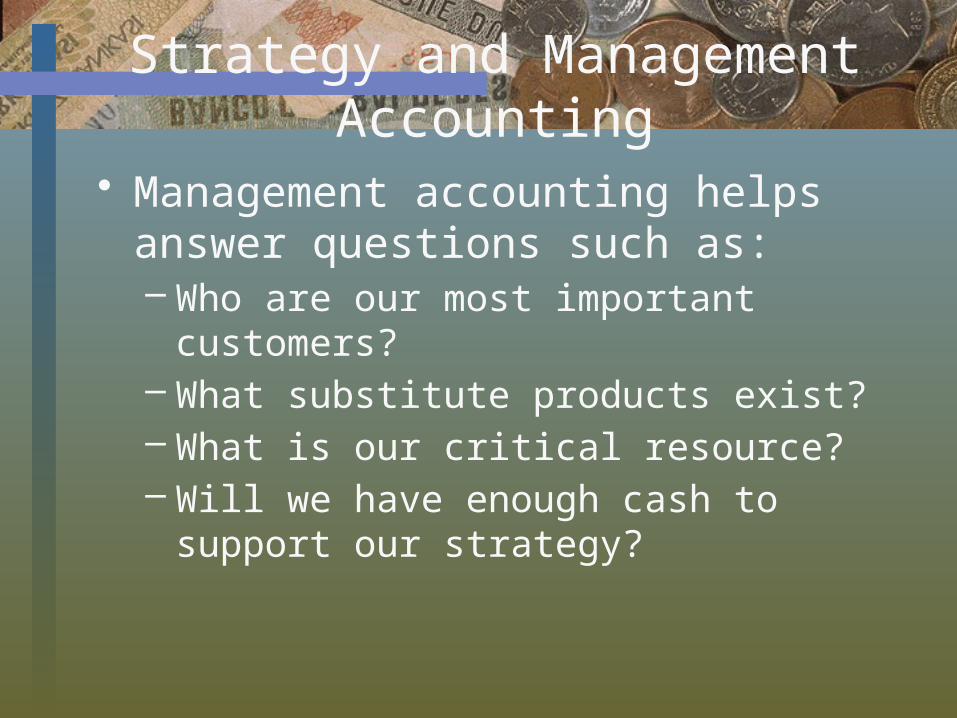

• Management accounting helps answer questions such as:– Who are our most important

customers?– What substitute products exist?– What is our critical resource?– Will we have enough cash to support

our strategy?

Course Themes

• Customer Focus• Key success factors

– Cost and efficiency– Quality (TQM)– Time– Innovation

• Continuous improvement• Value Chain & Supply Chain

Management Accounting and Value

• Creating value is an important part of planning and implementing strategy

• Value – is the usefulness a customer gains

from a company’s product or service• Value Chain

– is the sequence of business functions in which customer usefulness is added to products or services

Management Accounting and Value

• The Value Chain:– Research and Development– Design– Production– Marketing– Distribution– Customer Service

• Management accounting can provide information in each of these areas

• Analysis can also include the supply chain

Supply Chain

• Describes the flow of goods, services, and information from cradle to grave. – At the extreme, this can include the mining

of raw materials to disposal of recycled products.

• The supply chain may be spread out over many entities.

• See page 8 for an example.

Key Success Factors

• The dimensions of performance that customers expect, and that are key to the success of a company include:– Cost and efficiency– Quality– Time– Innovation

Planning and Control Systems

• Planning – selects goals, predicts results, decides

how to attain goals, and communicates this to the organization

– Budget – the most important planning tool

• Control – takes actions that implement the

planning decision, decides how to evaluate performance, and provides feedback to the organization

Cost Accounting

Management Decisions: 5-Step Process

• An accounting system must enable managers to work through issues to make decisions– Planning phase

• Identify problems and uncertainties• Obtain information• Make predictions about the future• Choosing among alternatives

– Control phase• Implement plans, Evaluate performance

(scorekeeping and attention directing), and Provide feedback

• Feedback is necessary to link the two types of activities

Management Accounting Guidelines

• Cost – benefit approach is commonly used: benefits generally must exceed costs as a basic decision rule

• Behavioral and Technical Considerations – people are involved in decisions, not

just dollars and cents• Different definitions of cost may be

used for different applications

Management Accounting Roles

• Problem Solver• Scorekeeper• Attention Director

Organizational Structure and the Management Accountant• A typical structure might include:

– CEO• CFO

– Controller – responsible for managerial and financial accounting

– Treasury– Risk Management– Taxation– Internal Audit

Cost Accounting

CFO• oversees all financial

operations–Controllership–Treasury–Risk management–Taxation– Investor relations– Internal audit

Cost Accounting

Controller• The controller is primarily

responsible for the financial and managerial accounting and reporting of information.

• Requires – Technical and analytical competence– Behavioral and interpersonal skills

Professional Ethics

• The four standards of ethical conduct for management accountants as advanced by the Institute of Management Accountants:– Competence– Confidentiality– Integrity– Objectivity

Cost Accounting

Resolution Of Ethical Conflict

• Discuss problem with supervisor and up the chain of command

• If issue is still unresolved, discuss with an objective advisor.

• Consult an attorney if necessary.• If unresolved, may need to resign

End of Chapter 1

• Just a review of things you already learned in Managerial Accounting.

• Now, let’s move forward!