cost accounting standards (()cas) · cost accounting standards (cas) what is casb? what are the...

TRANSCRIPT

COST ACCOUNTING COST ACCOUNTING

STANDARDS (CAS)( )

OFFICE OF POST AWARD FINANCIAL AWARD FINANCIAL SERVICES (OPAFS)

Course Objectives

f f d l d Increase awareness of federal and campus costing policy

Understand applicability of federal policy to campus process

Learn by example and discussion among participants

Cost Accounting Standards (CAS)

What is CASB?

What are the CAS?

Why do CAS exist?

Wh i i ? What are cost accounting practices?

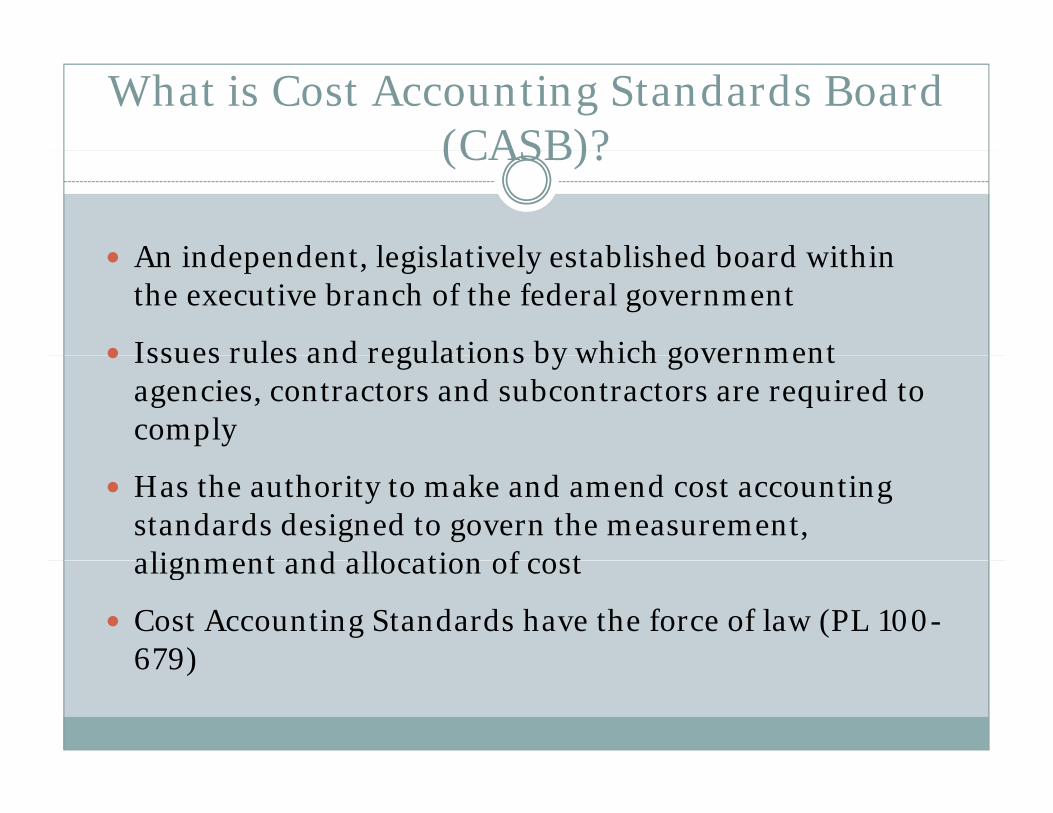

What is Cost Accounting Standards Board (CASB)?(CASB)?

An independent legislatively established board within An independent, legislatively established board within the executive branch of the federal government

Issues rules and regulations by which government Issues rules and regulations by which government agencies, contractors and subcontractors are required to comply

Has the authority to make and amend cost accounting standards designed to govern the measurement, alignment and allocation of cost alignment and allocation of cost

Cost Accounting Standards have the force of law (PL 100-679)679)

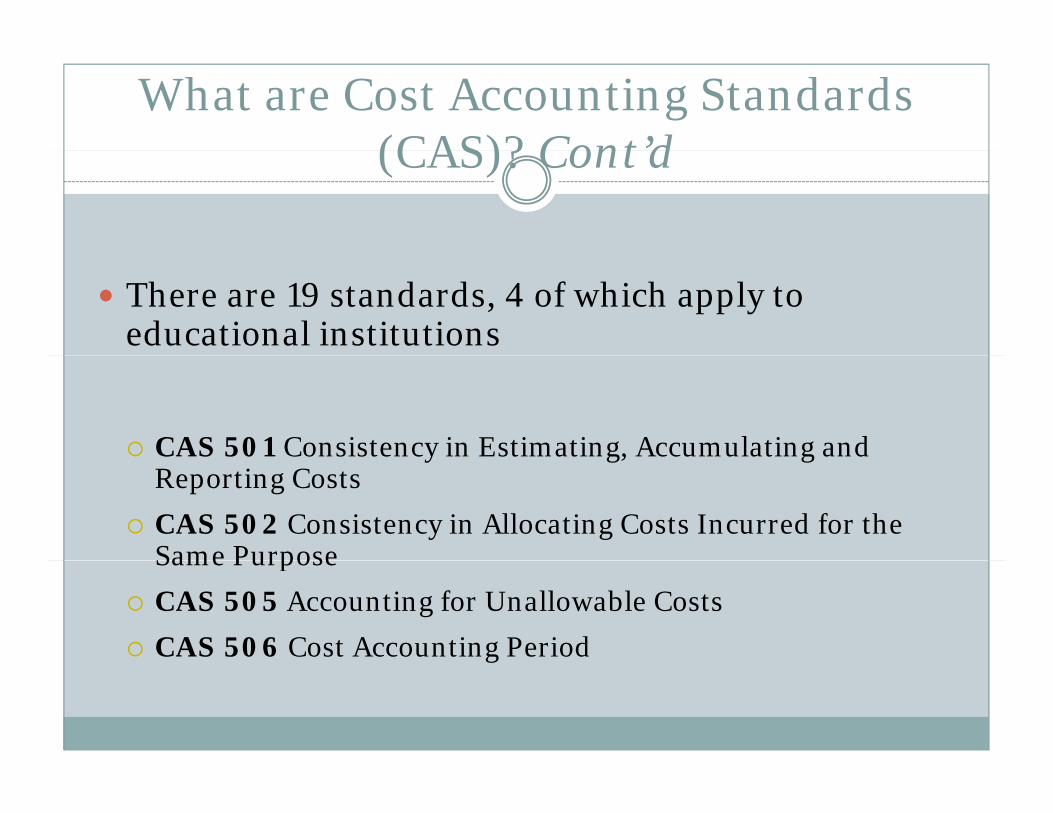

What are Cost Accounting Standards (CAS)? Cont’d(CAS)? Cont d

There are 19 standards, 4 of which apply to educational institutions

CAS 501 Consistency in Estimating, Accumulating and 5 y g, gReporting Costs

CAS 502 Consistency in Allocating Costs Incurred for the Same PurposeSame Purpose

CAS 505 Accounting for Unallowable Costs

CAS 506 Cost Accounting Period

Why does CAS exist?

T t th h i f ll bl t t To prevent the charging of unallowable costs to federal awards

T d di i i i i To standardize university costing practices

To standardize requirements for recipients of federal funds

What are Cost Accounting Practices?

H t d i d d ll t d How costs are measured, assigned, and allocated to final cost objectives

Either they are directly charged to individual projects and activities, or they are added as part projects and activities, or they are added as part of an overhead rate that is applied to all similar activities

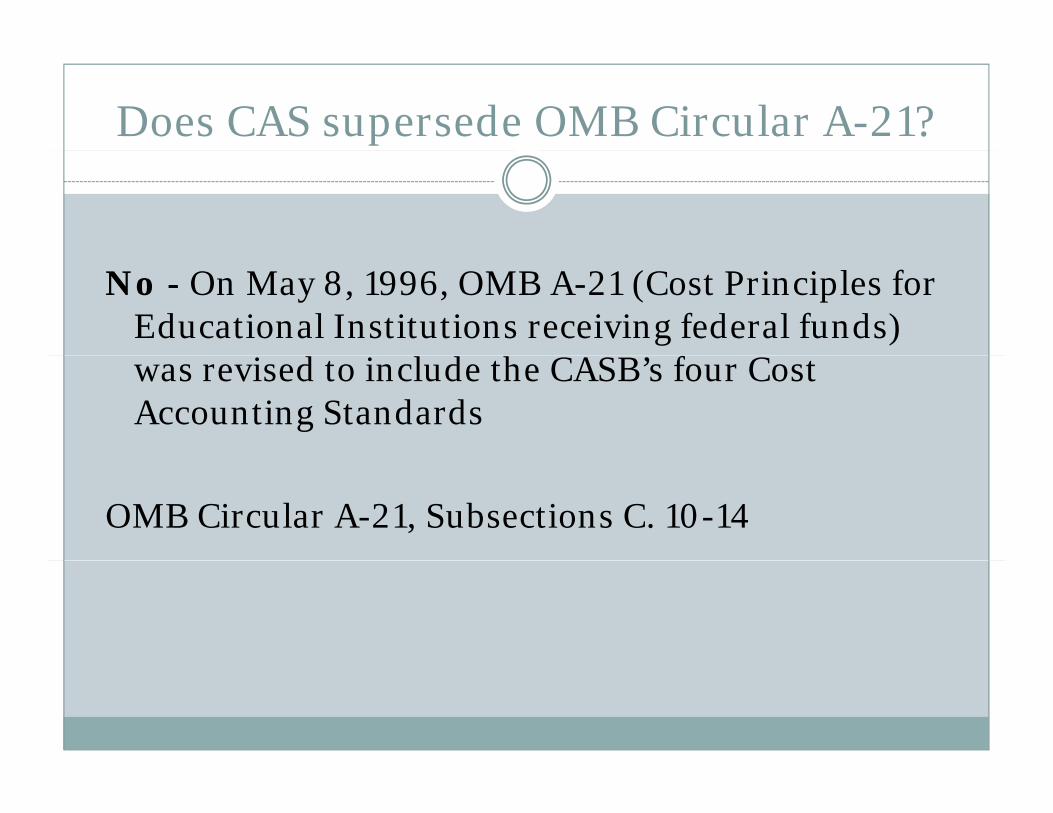

Does CAS supersede OMB Circular A-21?

No - On May 8, 1996, OMB A-21 (Cost Principles for Educational Institutions receiving federal funds)

i d i l d h ’ fwas revised to include the CASB’s four Cost Accounting Standards

OMB Circular A-21, Subsections C. 10-14

What Awards Are Covered Under CAS?

N F d l t t ft J 1 1995 New Federal contracts after Jan 1, 1995

All F d l d ( t t d t ) ft All Federal awards (contracts and grants) after May 8, 1996

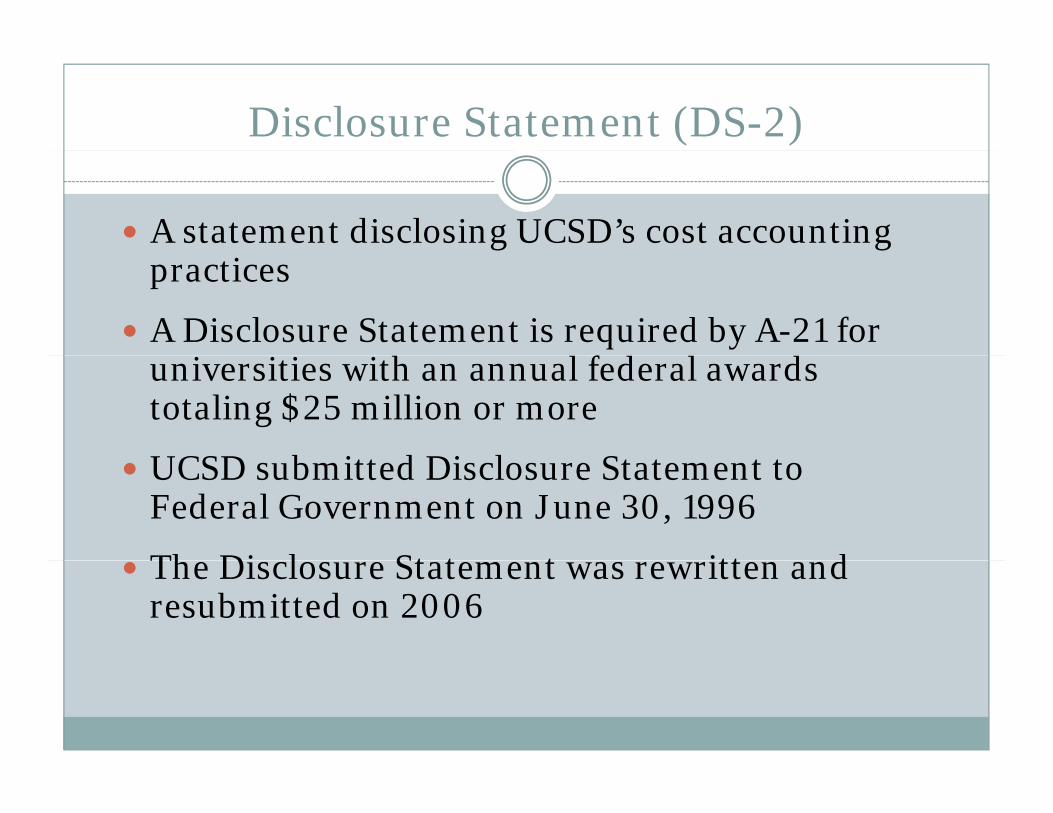

Disclosure Statement (DS-2)

A statement disclosing UCSD’s cost accounting practices

A Disclosure Statement is required by A-21 for i i i i h l f d l d universities with an annual federal awards

totaling $25 million or more

UCSD b itt d Di l St t t t UCSD submitted Disclosure Statement to Federal Government on June 30, 1996

Th Di l St t t itt d The Disclosure Statement was rewritten and resubmitted on 2006

Practices Disclosed in DS-2

The campus must disclose the specific criteria and circumstances to make distinctions between those circumstances to make distinctions between those type of costs that are sometimes accounted for as direct and sometimes as indirect.

CAS 501: Consistency in estimating, accumulating and reporting costsaccumulating and reporting costs

“To ensure that each educational institution’s ti d i ti ti t f l practices used in estimating costs for proposal are

consistent with cost accounting practices used by the institution in accumulating and reporting the institution in accumulating and reporting costs”

Cost Sharing

Definition:Definition: Commitment of University resources to supplement

externally sponsored projects

ib d b h i i i l di Resources contributed by the University including non-University resources (third party)

Type of Cost Sharing Type of Cost Sharing

Mandatory: Required by an agency as a condition of funding a sponsored projectfunding a sponsored project

Voluntary Committed: Included in proposed budget

Voluntary Uncommitted: Incurred at UCSD discretion

Formal Cost Sharing

C itt d t h i UCSD t ib ti Committed cost sharing are UCSD contributions that are included and quantified in

the proposal budget OR

the budget narrative OR

the award document

h d b k d d d These need to be tracked and reported

Formal Cost Sharing (cont’d)

Tracked on all awards after May 8, 1996y , 99

Cost Sharing System must be used for all awards after July, 1999, and may be used for awards y, 999, yprior to July 1, 1999

Tracked in the accounting recordsg

Included in project financial reports

Tracking commitments of 5% or less per person Tracking commitments of 5% or less per person per project is not required

Formal Cost Sharing

O l t th t ll bl d A 21 b Only costs that are allowable under A-21 can be cost shared

Cost Sharing on Sponsored Project PPM 150-45 http://adminrecords.ucsd.edu/ppm/docs/150-45.HTML

Allowable Costs

Reasonable It reflects what a prudent person might do

Allocable There is direct benefit to the project that paid the expense

Consistent treatmenth i i i dl f f d The accounting treatment is consistent regardless of fund

source

Allowable as defined by A-21 and/or by the Allowable as defined by A 21 and/or by the terms of the particular award

CAS 502: Consistency in Allocating Cost Incurred for the Same PurposeIncurred for the Same Purpose

To require that each type of cost is allocated only once and on only one basis to any project or

h bj iother cost objective.

h i i f d i i h ll i f The criteria for determining the allocation of costs should be the same for all similar objectives to prevent double countingto prevent double counting.

Direct and Indirect Cost

A “Direct Cost” is cost that can be identified specifically with a particular project relatively easy with a high degree of accuracy

Must be required to satisfy the project scope

Facilities and Administrative Costs

Indirect Cost is cost that are incurred for Indirect Cost is cost that are incurred for common or joint objectives, and cannot be identified with a particular project with a high degree of accuracy.

Normal Indirect Costs Specified in A-21:p Office Supplies

Postage

L l (B i ) T l h S i Local (Basic) Telephone Services

Membership Dues

Journals and Subscriptions Journals and Subscriptions

Major Projects

R i t i d i i t ti l i l Require extensive administrative or clerical support as defined by A-21

Require administrative or clerical support significantly greater than the routine level significantly greater than the routine level provided by departments

Examples of Major Projects I

L l j t Large, complex projects General Clinical Research Centers

Program Projects Program Projects

Environment Research Centers

Engineering Research Centers

Projects with extensive data accumulation, analysis, surveying cataloging and reportingsurveying, cataloging and reporting

Examples of Major Projects II

Projects with travel and meeting arrangements for j g glarge number of participants Conferences

S i Seminars

Projects with principal focus on production of Projects with principal focus on production of Manuals

Large reportsg p

Books

Monographs

E l di ti d t h i l t Excluding routine progress and technical reports

CAS 505: Accounting for Unallowable Costs

All ll bl t h ll b id tifi d d All unallowable costs shall be identified and excluded from any billing, claim, or proposal under a federal awardfederal award

Individual responsible for submitting proposals, Individual responsible for submitting proposals, classifying costs or preparing billings shall be familiar with and shall comply with the requirements imposed by CAS 505

CAS 505: Accounting for Unallowable Costs (cont’d)(cont d)

Cost of project not authorized by a sponsored agreement shall be accounted for in a manner which permits ready separation of what is authorized and what is notwhat is not

CAS 506: Cost Accounting Period

id i i f l i f i i d b Provide criteria for selection of time periods to be used as accounting period for cost estimating, accumulating and reportingaccumulating, and reporting

UCSD fiscal year July 1 – June 30 shall be used as UCSD fiscal year July 1 – June 30 shall be used as the cost accounting period

References

A-21 Cost Principles Applicable to Educational Institutionsp pp

http://www.whitehouse.gov/omb/circulars/a021/a21_2004.html

A-110 Uniform Administrative Requirements for Grants and

Agreements with Institutions of Higher Education

PPM 150-40 Cost Accounting Standards Compliance

PPM 150-42 Classification of Costs ad Direct or Facilities and PPM 150-42 Classification of Costs ad Direct or Facilities and

Administrative (Indirect)

PPM 150-43 Accounting for Unallowable Costs

PPM 150-45 Cost Sharing on Sponsored Projects

Agency Policy Statements

NIH G P li S NIH Grants Policy Statement

NSF Grants Manual

Any Questions?Any Questions?