cost cutting measures

TRANSCRIPT

Cost Cutting Measures

Submitted to: Mr. Rajesh Jhamb Submitted by:Varun Sharma um10308Samdeep Soni um10305

Cost of capital

▪ Cost of capital refers to the cost of equity if the business is financed solely through equity or to the cost of debt if it is financed solely through debt.

▪ Many companies use a combination of debt and equity .

▪ The cost of various capital sources varies from company to company, and depends on factors such as its operating history, profitability, credit worthiness, etc.

▪ Debt financing has the advantage of being more tax-efficient. However, too much debt can result in dangerously high leverage, resulting in higher interest rates sought by lenders to offset the higher default risk.

Types of cost

▪ Fixed costs are expenses that do not change in proportion to the activity of a business, within the relevant period or scale of production. For example, a retailer must pay rent and utility bills irrespective of sales.

▪ Variable costs by contrast change in relation to the activity of a business such as sales or production volume. In the example of the retailer, variable costs may primarily be composed of inventory (goods purchased for sale), and the cost of goods is therefore almost entirely variable.

▪ Average cost per unit is equal to total cost divided by the number of goods produced.

▪ Marginal cost is the change in total cost that arises when the quantity produced changes by one unit.

Cost cutting measures

▪ Measures implemented by a company to reduce its expenses and improve profitability.

▪ Cost cutting measures may include laying off employees, reducing employee pay, switching to a less expensive employee health insurance program, downsizing to a smaller office, lowering monthly bills, changing hours of service and restructuring debt.

▪ E.g.- Bank of America decided to layoff 30000 employees in 2012 while RBS layed off 1000 employees in India in 2013

Tools & Technique of cost cutting

▪ Just-In-Time (JIT) System -The main aim of JIT is to produce the required items, at the required quality and quantity, at the precise time they are required. JIT purchasing requires for the items where too much carrying costs associated with holding high inventory levels. Purchasing system reduces the investment in inventories because of frequent order of small quantities.

▪ Target Costing -Target costing refers to the design of product, and the processes used to produce it, so that ultimately the product can be manufactured at a cost that will enable the firm to make profit when the product is sold at an estimated market-driven price. This estimated price is called target price.

▪ Activity Based Management (ABM) - Activity based management is the use of activity based costing to improve operations and to eliminate non-value added cost. The main goal of ABM is to identify and eliminate non-value added activities and costs.

Tools & Technique of cost cutting

▪ Life Cycle Costing - Life cycle costing estimates and accumulates costs over a product's entire life cycle in order to determine whether the profits earned during the manufacturing phase will cover the costs incurred during the pre-and-post manufacturing stage.

▪ Kaizen Costing - Kaizen costing is the process of cost reduction during the manufacturing phase of an existing product. The Japanese word 'Kaizen' refers to continual and gradual improvement through small activities, rather than large or radical improvement through innovation or large investment technology.

▪ Business Process-re-engineering - Re-engineering is a complete redesign of process with an emphasis on finding creative new ways to accomplish an objective. The aim of business process re-engineering is to improve the key business process in an organization by focusing on simplification, cost reduction, improved quality and enhanced customer satisfaction.

▪ Total Quality Management (TQM) - Under the TQM approach, all business functions are involved in a process of continuous quality improvement.

Tools & Technique of cost cutting

▪ Value chain - Value chain analysis is a means of achieving higher customer satisfaction and managing costs more effectively. The value chain is the linked set of value creating activities all the way from basic raw materials' sources, component suppliers, to the ultimate end-use product or service delivered to the customer.

▪ Bench Marketing - Bench marketing is a continual search for the most effective method of accomplishing a task by comparing the existing methods and performance levels with those of other organizations or other sub-units within the same organization.

▪ Management Audit - Management audits, also known as performance audits, can be used to facilitate cost reduction in both profit and non-profit organizations. Management audits are intended to help management to do a better job by identifying waste and inefficiency and recommending a corrective action.

Tools & Technique of cost cutting

▪ Planned value (PV) - PV is the budgeted cost for the work scheduled to be completed on an activity.

▪ Earned value (EV) - EV is the budgeted amount for the work actually completed on the schedule activity .

▪ Actual cost (AC) - AC is the actual cost incurred in accomplishing work on the schedule activity or WBS component during a given time period. This AC must correspond in definition and coverage to whatever was budgeted for the PV and the EV (e.g. direct hours only, direct cost only, or all costs including indirect costs).

Tools & Technique of cost cutting

▪ Cost performance index (CPI) - A CPI value less than 1.0 indicate a cost overrun of the estimates. A CPI value greater than 1 indicates a cost under-run of the estimates. CPI equals the ratio of the EV to the AC. The CPI is the most commonly used cost-efficiency indicator.

CPI=EV/AC

▪ Cumulative CPI - The cumulative CPI is widely used to forecast project costs at completion. CPIC equals the sum of the periodic earned values divided by the sum of the individual actual costs .

SPI=EV/PV

Ways to cut cost and increase cash flow

▪ There are two primary rules, used by all properly managed companies, from one-appraiser firms to Fortune 500 companies:

1. Pay your bills only when they are due.

2. Get your income as soon as possible.

Fortunately for appraisal firms, most of the costs are variable. For example, if your work volume drops, your photo processing and appraisal fee split labour also drop.

But fixed costs, such as rent and support staff, can cause financial problems when appraisal assignments drop off quickly.

Ways to cut cost and increase cash flow

Cash management

▪ Pay no bill before its time. Don't pay any bills until they're due. See who has a late charge, and who doesn't.

▪ Exercise dormant lines of credit. Frequently business owners set up lines of credit they don't use. The bank may drop your line of credit if it is not used for a certain period of time, so be sure to check their use requirements.

▪ Closely monitor your three sources of cash:

a) Appraisals in process, not yet completed

b) Appraisals billed out, but not yet collected

c) Paid billings: cash on hand

Ways to cut cost and increase cash flow

Rent - office and storage

▪ Renegotiate your lease to a lower rent, or a temporary lower rent while business is slow. If office vacancies are high, your landlord will probably prefer reduced rent to no rent.

▪ Sublet unused office space to appraisers or non-appraisers. Or, move out of your larger office space to a smaller sublet office.

▪ If you need to move or downsize to a smaller office, but have a lease, work with your landlord. Maybe he or she will let you sublease, make a partial payment of the rest of your lease, or move to a smaller space.

▪ Shop around for low-cost storage space. We have to save our files for at least 5 years, and many of us save them for much longer. What to keep and throw out in files is an individual decision, but you can shop for a lower storage cost.

▪ Get rid of excess stored stuff, such as old office furniture. Sell it or give it away. Don't pay storage costs for things you really don't need. Don't be a packrat.

Ways to cut cost and increase cash flow

Pricing

▪ Keep close track of your competitor's costs. Don't underbid or lose work because you overbid. When fees are changing, don't get left behind and lose valuable assignments from overbidding, or income from underbidding.

▪ Don't offer lower prices to a client that isn't price sensitive. Why give away your profits?

▪ Know your costs on appraisals. The high fee jobs may not be the most profitable. It may be more profitable to set up referral alliances with appraisers in other geographic areas, rather than spend the time traveling and doing extra research on an area you're not familiar with

Ways to cut cost and increase cash flow

Personnel

▪ Cut back principals' salaries. Pay yourself last, after paying all other expenses. Although this may seem obvious, many companies have developed serious financial problems because the owners kept taking out large salaries.

▪ "Lease" your employees. Instead of laying off an experienced secretary, lease him or her to another company until business picks up again.

▪ Use temporary help whenever possible when your business substantially increases. That's how the mortgage lending industry handled the 1991 to 1993 substantial increases in lending volumes

▪ Use part-time support staff. They don't require benefits and usually have more flexible hours. Laying off a part-timer, or cutting back their hours, is much easier than a long-term loyal, full-time employee.

Ways to cut cost and increase cash flow

▪ Use an outside payroll service such as Paychex or ADP to cut bookkeeping payroll costs. Or, do it yourself by using a simple software program like Quick books. Don't use a CPA to do your bookkeeping.

▪ Broaden staff responsibilities. For example, instead of paying an outside bookkeeper, have your secretary do it. If you have to lay off a full-time secretary because your work has dropped, consider letting a less experienced associate appraiser do part-time clerical work. At least they'll have some income. Instead of having outside firms do janitorial and delivery services, have your employees do it. It's better than getting laid off, or sitting around worrying about getting laid off.

Ways to cut cost and increase cash flow

Taxes

▪ Don't overpay your income tax quarterlies. If you anticipate that your taxable income will drop this year, don't pay taxes based on last year's income. Work with your accountant to pay quarterlies based on a more accurate estimate. If you've already overpaid your quarterlies, ask your accountant about a quick refund, using Forms 4466 and 1138.

▪ Close to year-end, schedule a tax-planning meeting with your accountant to shift income and expenses. For example, shift income into the next year to decrease this year's taxes.

Ways to cut cost and increase cash flow

Supplies

▪ Shop for the best prices. Don't pay too much attention to percent discount. Look at the bottom line. No one pays full retail. Purchasing supplies in bulk may be worthwhile.

▪ Use office warehouse companies like Office Club. They usually offer the lowest prices. Many will deliver. Don't forget discount stores like Price Club, Wal-Mart, and Costco. Many carry some of the most-purchased office supplies, like paper, pens, and laser-jet cartridges. You don't always need to buy brand names.

▪ Keep close track of inventory so you don't have to pay someone to "run over" to the nearby high-priced office supply store.

Ways to cut cost and increase cash flow

Equipment's

▪ Sell or donate excess office furniture and equipment. Storage space is expensive. You can sell it to employees, the public, or the vendor (on consignment). Donate it to local charities or schools.

▪ When leasing equipment, get an option to cancel due to closure or consolidation. We should not get an "evergreen clause", where the contract always continues unless you give 30 days’ notice. They are difficult to cancel, as the expiration date is hard to monitor.

▪ Renegotiate your equipment leases

▪ Reduce phone lines. If you have fewer staff, you need fewer phone lines. Cancel some of the optional features you don't really need.

SBI

▪ State Bank of India (SBI) is an Indian multinational banking and financial services company. It is a government-owned corporation with its headquarters in Mumbai, Maharashtra.

▪ Initially the Imperial Bank of India became the State Bank of India. In 2008, the government of India acquired the Reserve Bank of India's stake in SBI so as to remove any conflict of interest because the RBI is the country's banking regulatory authority.

▪ As of December 2013, it had assets of US$388 billion and 17,000 branches, including 190 foreign offices, making it the largest banking and financial services company in India.

Comparison of Income & Expenditure

Description May 2013 May

2014

Difference Variance

Total Income 16798 19448 2650 16%

Total Expenses 15126 17316 2190 15%

Operating Result 1673 2109 436 26%

C.O. Int. Receivable 15829 19036 3207 20%

C.O. Int. Payable 12917 14683 1766 14%

Net Result 4585 6462 1877 41%

0

5000

10000

15000

20000

25000

Total Income TotalExpenses

OperatingResult

C.O. Int.Receivable

C.O. Int.Payable

Net Result

May-13

May-14

Movement of Earning, Expenses & Net Result for May 2013 & May 2014 of State Bank of India

0

5000

10000

15000

20000

25000

Total Income Total Expenses Operating Result C.O. Int. Receivable C.O. Int. Payable Net Result

May-13

May-14

Overheads for May 2013 & May 2014 of State Bank of India

Description May 2013 May 2014 Difference Reasons

Telephones 14 13 -1 The telephone charges have decreased because earlier

Rs. 1000 were paid to each employee but now Rs. 500

is paid for their telephone bills. Moreover, instead of

two sim cards, now only one sim card is given to each

employee.

Electricity & Gas

Charges

105 103 -2 The electricity and gas charges have decreased

because the energy consumptions measures provided

by the authority are being righty followed now by all

the branches.

Postage 29 18 -11 The postage overhead cost has decreased because now

the e-mail and other electronic services are being used,

therefore the decrement.

Repairs &

Maintenance

58 72 14 The repairs and maintenance cost has increased

because there are many branches whose maintenance

were done this year and thus there is a hike in the cost.

Figure in Crores

Overheads for May 2013 & May 2014 of State Bank of India

Description May 2013 May 2014 Difference Reasons

Stationary, Printing &

Advertising

48 41 -7 The stationary, printing and advertisement costs have decreased

because of the use of electronic services and also since the bank

has now gained a good reputation, the advertisement cost has

reduced.

Travelling Expense & Halting

Allowances

107 95 -12 Halting Allowance has decreased because it depends on the

employees for how many days they have to stay and since this

year, the period of stay was less than last year, the expense has

decreased.

Medical Expenses 37 41 4 The medical expenses have increased because from last year, the

health-issues of the employees have increased and thus we find

an increment of the cost in this particular account.

Misc. Expenses 293 43 -250 The miscellaneous expenses has decreased because earlier,

separate accounts were not maintained for each kind of expenses,

but since from this year, there has been introduction of separate

account and the miscellaneous expenses account has been done

away with, therefore we notice such a reduction in cost.

Figure in Crores

Overheads for May 2013 & May 2014 of State Bank of India

Description May 2013 May 2014 Difference Reasons

Controllable Overheads 692 426 -266 The controllable overheads cost have decreased because in most

branches, the norms were followed and therefore we find a

reduction in the total cost.

Non Controllable

Overheads

171 245 74 Non controllable overheads have increased because most of

them are fixed in nature and therefore the cost cannot be

decreased.

Total Overheads 863 671 -192 Total overheads cost has decreased due to the effective use

of the measures lay by the authority and adapted efficiently

to gain cost reduction.

Figure in Crores

Comparison of Overheads for May 2013 & May 2014 of State Bank of India

0

100

200

300

400

500

600

700

800

900

1000

May-13

May-14

Figure in Crores

Movement of Overheads for May 2013 & May 2014 of State Bank of India

0

100

200

300

400

500

600

700

800

900

1000

May-13

May-14

Figure in Crores

PUNJAB NATIONAL BANK

▪ Punjab National Bank (PNB) is an Indian financial services company based in New Delhi, India. Founded in 1894, the bank has over 5,800 branches and over 6,000 ATMs across 764 cities. It serves over 80 million customers.

▪ PNB has the distinction of being the first Indian bank to have been started solely with Indian capital that has survived to the present.

▪ The Government of India (GOI) nationalized PNB and 13 other major commercial banks, on 19 July 1969.

PUNJAB NATIONAL BANK Income & Expenditure

Parameters Mar’09 Mar’10 Mar’11 Mar’12 Mar’13 Mar’14 CAGR (%)

Operating Profit 5690 7326 9056 10614 10907 11384 14.88%

Net Profit 3091 3905 4433 4884 4745 3343 1.58%

Deposit 209760 249330 312899 379588 391560 451397 16.56%

Advance 154703 186601 242107 293775 308796 349269 17.69%

Total Business 364463 435931 555005 673366 700356 800666 17.05%

Figure in Crores

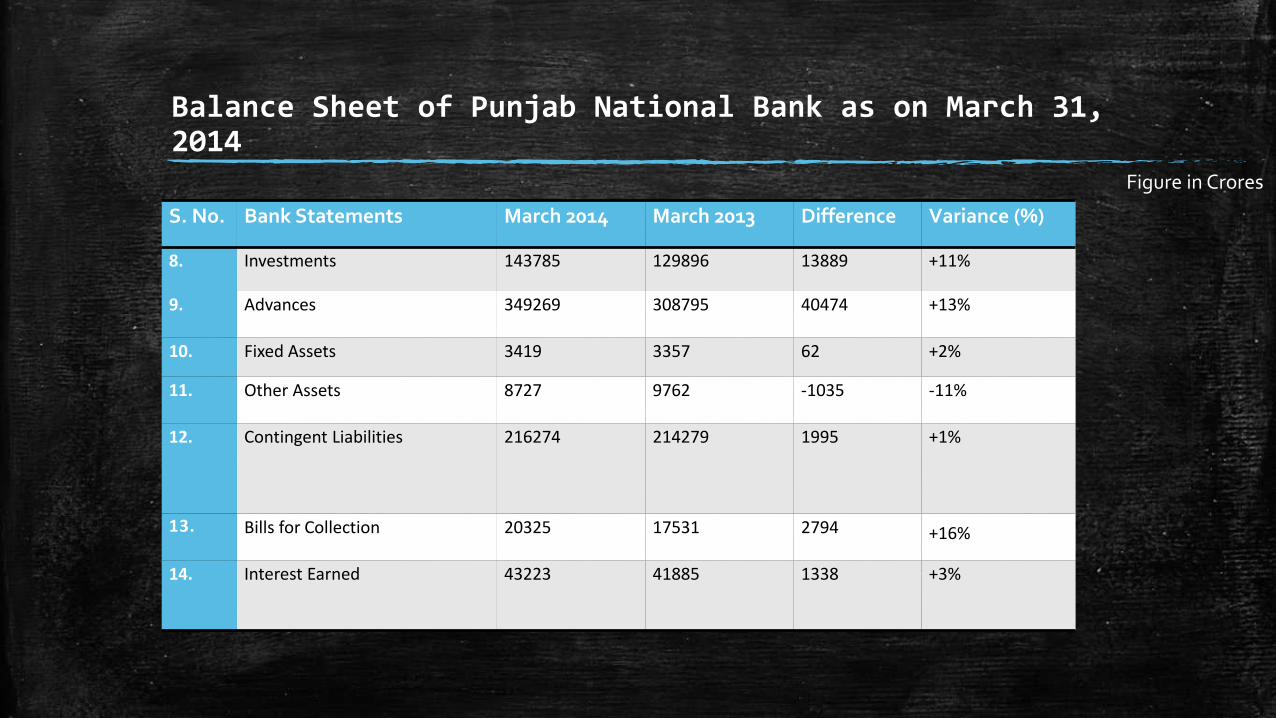

Balance Sheet of Punjab National Bank as on March 31, 2014

S. No Bank Statements March 2014 March 2013 Difference Variance (%)

1. Capital 362 353 9 +3%

2. Reserves & Surplus 35533 32323 3210 +10%

3. Deposits 451396 391560 59836 +13%

4. Borrowings 48034 39620 8414 +21%

5. Other Liabilities and Provisions 15093 15089 4 +0.02%

6. Cash & Balances With RBI 22245 17886 4359 +23%

7. Balances with Banks & Money at

Call & Short notice

22972 9249 13723 +15%

Figure in Crores

Balance Sheet of Punjab National Bank as on March 31, 2014

S. No. Bank Statements March 2014 March 2013 Difference Variance (%)

8. Investments 143785 129896 13889 +11%

9. Advances 349269 308795 40474 +13%

10. Fixed Assets 3419 3357 62 +2%

11. Other Assets 8727 9762 -1035 -11%

12. Contingent Liabilities 216274 214279 1995 +1%

13. Bills for Collection 20325 17531 2794 +16%

14. Interest Earned 43223 41885 1338 +3%

Figure in Crores

Balance Sheet of Punjab National Bank as on March 31, 2014

S.

No.

Bank Statements March 2014 March 2013 Difference Variance (%)

15. Other Income 4576 4223 353 +8%

16. Interest Expended 27077 27036 41 +0.15%

17. Operational Expenses 9338 8165 1173 +14%

18. Provisions & Contingencies 8041 6159 1882 +31%

Comparison of Balance Sheet of Punjab National Bank for March’13 & March’14

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Series1

Series2

Figure in Crores

Movement of Balance Sheet of Punjab National Bank for March’13 & March’14

Capital

Reserves & Surplus

Deposits

Borrowings

Other Liabilities and Provisions

Cash & Balances With RBI

Balances with Banks & Money at Call & Short notice

Investments

Advances

Fixed Assets

Other Assests

Contingent Liabilitites

Bills for Collection

Interest Earned

Other Income

Interest Expended

Operational Expenses

Provisions & Contingencies

NPA

NPA (Non-Performing Asset) is an industrial phenomenon which indicates industrial sickness. The national growth of a country particularly country like India depends upon the growth and health of SME’s. The so called banking reform are targeted towards killing the Sick units rather than curing them.

Effect of NPA on Bank• The day to day operating the account becomes difficult as Bank starts

adjusting money deposited against their dues.• The reputation of the borrower in the market is adversely affected.• The Bankers attitude towards the borrower becomes more arrogant,

authoritative and threatening, instead of extending helping hand to them to get out of the situation.

• This leads to demoralization of the borrower who has been working with the Bank for number of years and as customer has contributed in the profit of the Bank.

• The principle of customer care is neglected and customer torture begins. This brings the borrower in a helpless situation and at the mercy of the Bank

NPA

• Banks interest income can fall down and accounted on the basis of receipt.

• Profitability of Banks is caused harmfully due to offering of doubtful debts and ensuing contain it as terrible debts.

• ROI (Return on investments) is decreased.• The adequacy ratios of capital are termed as NPAs and are following into

its estimation.• Maximizes the capital price.• Variance of liability and assets will expand.• EVA (The economic value addition) by banks get trouble for the reason

that EVA is similar to the profit of net functioning less capital cost and

• It margins funds recycling.

Reasons for NPA

▪ Economic slowdown in the National and International Sectors. Here, bank just can't do much.

▪ Default by So called Ultra High worth Corporates and Individuals SBI, the leader of the consortium of banks that have lent funds to Kingfisher Airlines, has an exposure of Rs 1,457.78 crore to the struggling firm. SBI's exposure is the highest among any of the lenders to the airline, followed by IDBI Bank (Rs 727.63 crore), Punjab National Bank (Rs 710.33 crore), Bank of India (Rs 575.27 crore) and Bank of Baroda (Rs 537.51 crore).

▪ Credit Management is not a thing of FOCUS for the present leadership of SBI. They are busy in playing the game for Individual Margins through SBI Life and SBI Mutual Fund. The focus of the Higher Management has been shifted to earning more PERSONAL Commissions through cross selling of the policies of SBI Life and SBI Mutual Fund

Energy consumption in Banks (RBI Guidelines)

It will be beneficial if lights and fans are switched-off before leaving the seat or during lunch hours.

It will be better for the energy saving purpose if monitors are switched-off when not in use.

Scheduling switching on and off of lights and A.Cs on by 10:00 AM and switched off by 5:00 PM at offices/branches except Air conditioners of server room can be used in order to decrease the cost of electricity.

24 deg. C or above temperature in AC area shall be maintained as reducing the temperature further by over 1 deg. C can consume approximately 3% more power. Therefore this will help in electricity saving.

Display/showcases can be turned off at night to save electricity consumption.

The reduction of the number of lifts operating during non-peak hours at offices/branches (i.e. 11:00AM to 1:00 PM and 3:00 PM to 4:30 PM) and residential buildings (i.e. 11:00 AM to 5:00 PM) can save the cost.

Suggestions for cost cutting

▪ The bank has 14 stationery departments to supply A4 size papers, ball pens, pins and clips to 14 circles of the bank. These departments employ several hundred workers. Does a bank need such a division when a Flipkart.com can take care of such needs? Similarly, it has 14 processing centres to scrutinize new depositors’ forms, employing at least a couple of thousand people. It’s a mystery why SBI needs data processing centres for every circle when most foreign and new private banks run one centre to process such data across India.

▪ Yet another cost centre is the currency chests that SBI has historically been managing on behalf of the Reserve Bank of India. Of the 4,200 currency chests across India, SBI runs 2,200 or 52% of them while its market share in loans and deposits is around 17%. Assuming that each currency chest on average needs about six armed guards, more than 13,000 such armed guards are on the payroll of the bank. While cash management is a critical activity for the banker to the nation, surely there are modern cash replenishment and logistics alternatives that can minimize use of guards and space.

▪ Another area where the bank must look into is its 41,000-odd ATM network for the group. In November, the SBI group roughly accounted for 41% of the 380 million outstanding debit cards (and 45% of the total 530 million transactions) but its share in the ATM network was far less, at 30%. As a result, the bank’s customers use other banks’ ATMs for withdrawal of money. Under norms, up to five such transactions are free. While the customers make free transaction at other banks’ ATMs, SBI needs to pay Rs.18 per transaction. Indeed, SBI also makes some money while other banks’ customers use its ATMs but that’s far less than what it pays to other banks. It possibly needs to take a look at the locations of its ATMs to increase the footfalls. It can also explore whether it can charge on its ATM use. There are roughly 8 million ATM transactions a day and even if it charges Rs.1 per transaction, it can earn Rs.300 crore a year.

Suggestions for cost cutting

▪ The biggest challenge before the bank, at this point, is monitoring its bad assets, about 60% of which originate from mid-corporates and relatively large among the small and medium enterprises (SMEs), the companies which are not diversified, and another 25% from low-ticket accounts from retail, agriculture and small businesses. The bank must give up its traditional model of focusing on manual supervision which is almost impossible when one needs to track millions of accounts. Apparently, sometime back it had set up an account tracking and monitoring platform, called ATM, for real time monitoring of stressed accounts, but it has not been put to proper use.

Loss through ATM

▪ According to SBI’s data, its employees transact about 280,000 ATM card-swipes in other banks’ cash machines per month. This costs the bank about Rs. 42 lakh plus taxes. Every card swiped at other banks’ ATM makes that branch richer by Rs. 15. For SBI, this is reducing profits by a staggering Rs. 5 Crore a year.

▪ Bank can thus ask the employees to use their own bank’s ATM to carry out the transaction; this will help the bank to have stronger relationship with employees. This step is an addition to the slew of measures being taken by the bank to reduce expenditure.

▪ At present the first five transactions in the non- parent bank are free of cost, and the parent bank has to pay the cost. This would mean that each bank would have to foot the bill for these transactions. It has been found out that ATM interchange fees also increased to Rs 273 Crore, a 29% increase, at the end of December 2013. Further it has been discovered that bank will go slow on hiring of employees as well, because the bank has noticed an upsurge of 35% in the expenses of the staff within a couple of years.