cost trends - hixson architecture, engineering, interiors€¦ · the lowest average cbis were in...

TRANSCRIPT

In ThIs Issue:

The following cost trends are included in this issue.

• U.S. Construction Costs

• Leading Indicators of Construction Industry

• Construction Spending

• Construction Backlog Indicator

• Construction Employment/ Unemployment Rates

• Asphalt Pavement• Concrete• Structural Steel• Flat Rolled Steel• Stainless Steel• Copper• Pipe

For more information relating to this Cost Trends newsletter,

please contact:

Michael E. Downing, CPE, LEED AP BD+C,

Hixson ManagerCost Estimating

Page 1

What’s Changing in Construction Costs?CurrenT Trends

Welcome to the Fall 2016 issue of Cost Trends! We are seeing several factors which may affect Owners. First, while costs for most materials have remained relatively low, experiencing only slight cost increases, the potential for rising costs does exist. One indicator of this potential risk is flat-rolled steel, which has seen a 60% spike in prices during the first half of 2016. As a result, building components made from flat-rolled steel are becoming more costly to produce. Second, due to the current high construction volume and low construction unemployment, skilled labor and quality subcontractors are not as readily available as they were a few years ago, especially in the busiest regions. Also, because many contractors have sustained good backlogs of work under contract, as shown in Section 4 - Construction Backlog Indicator (CBI), they can afford to be more selective in the projects they choose to take on, will be more mindful of scheduling projects to fill any gaps in their busy schedules (or to schedule projects farther out), and may seek more opportunities to benefit their profit margins. Both of these factors indicate that it would be prudent for those planning building projects to do so proactively and procure contractors early to meet desired schedules and budgets: Those who procrastinate may have difficulty finding the necessary skilled labor and desirable subcontractors to meet tight schedules. Note too that competition for limited availability of skilled labor is resulting in labor costs creeping upwards at a potentially accelerating rate.

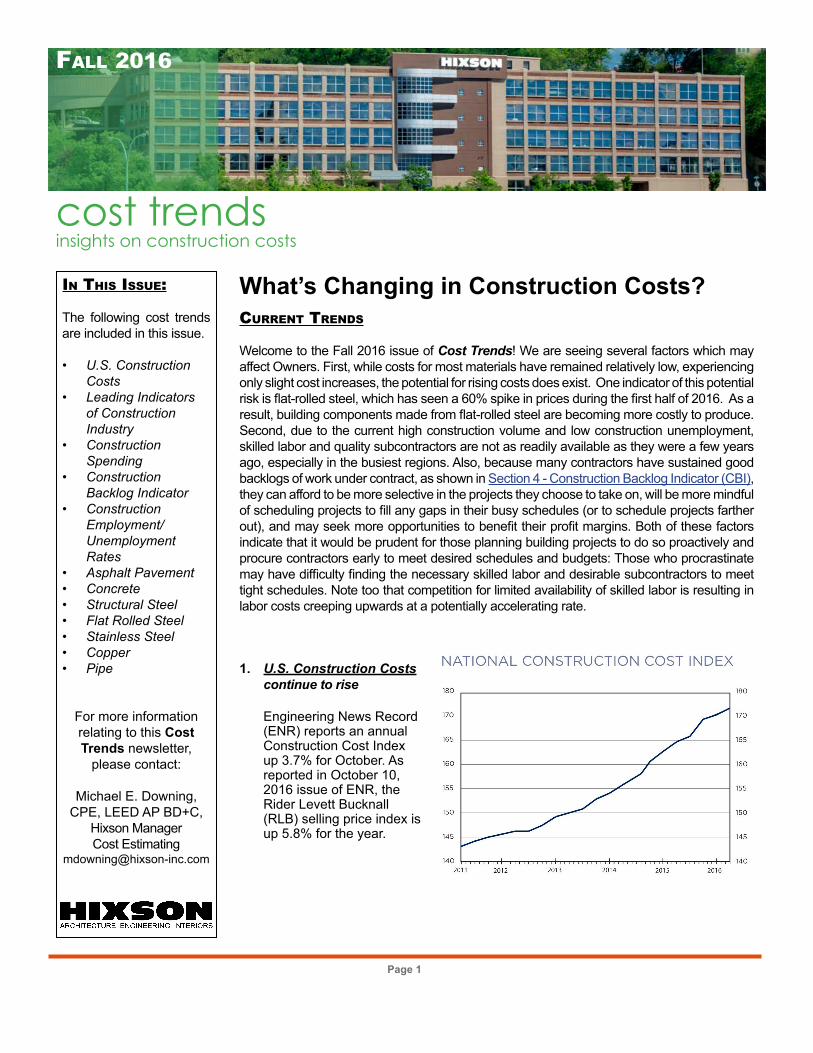

1. U.S. Construction Costs continue to rise

Engineering News Record (ENR) reports an annual Construction Cost Index up 3.7% for October. As reported in October 10, 2016 issue of ENR, the Rider Levett Bucknall (RLB) selling price index is up 5.8% for the year.

Fall 2016

cost trendsinsights on construction costs

Page 2

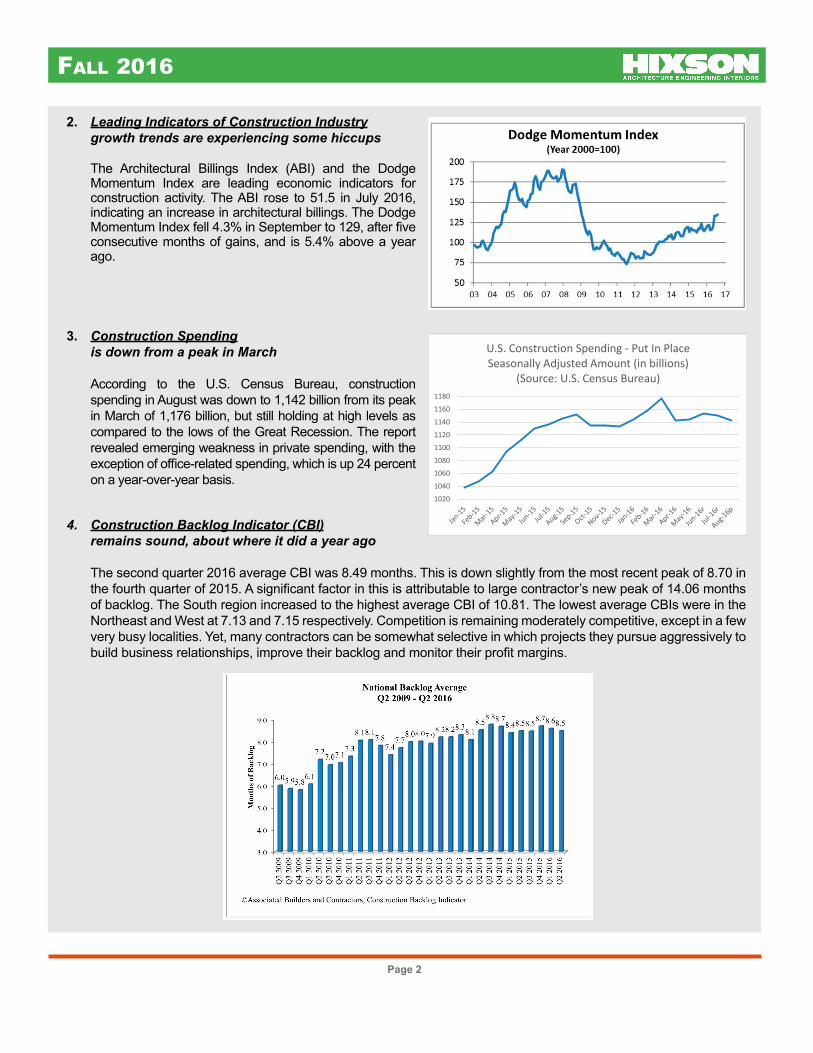

2. Leading Indicators of Construction Industry growth trends are experiencing some hiccups The Architectural Billings Index (ABI) and the Dodge

Momentum Index are leading economic indicators for construction activity. The ABI rose to 51.5 in July 2016, indicating an increase in architectural billings. The Dodge Momentum Index fell 4.3% in September to 129, after five consecutive months of gains, and is 5.4% above a year ago.

3. Construction Spending is down from a peak in March

According to the U.S. Census Bureau, construction spending in August was down to 1,142 billion from its peak in March of 1,176 billion, but still holding at high levels as compared to the lows of the Great Recession. The report revealed emerging weakness in private spending, with the exception of office-related spending, which is up 24 percent on a year-over-year basis.

4. Construction Backlog Indicator (CBI) remains sound, about where it did a year ago

The second quarter 2016 average CBI was 8.49 months. This is down slightly from the most recent peak of 8.70 in the fourth quarter of 2015. A significant factor in this is attributable to large contractor’s new peak of 14.06 months of backlog. The South region increased to the highest average CBI of 10.81. The lowest average CBIs were in the Northeast and West at 7.13 and 7.15 respectively. Competition is remaining moderately competitive, except in a few very busy localities. Yet, many contractors can be somewhat selective in which projects they pursue aggressively to build business relationships, improve their backlog and monitor their profit margins.

Fall 2016

1020

1040

1060

1080

1100

1120

1140

1160

1180

U.S. Construction Spending - Put In PlaceSeasonally Adjusted Amount (in billions)

(Source: U.S. Census Bureau)

Page 3

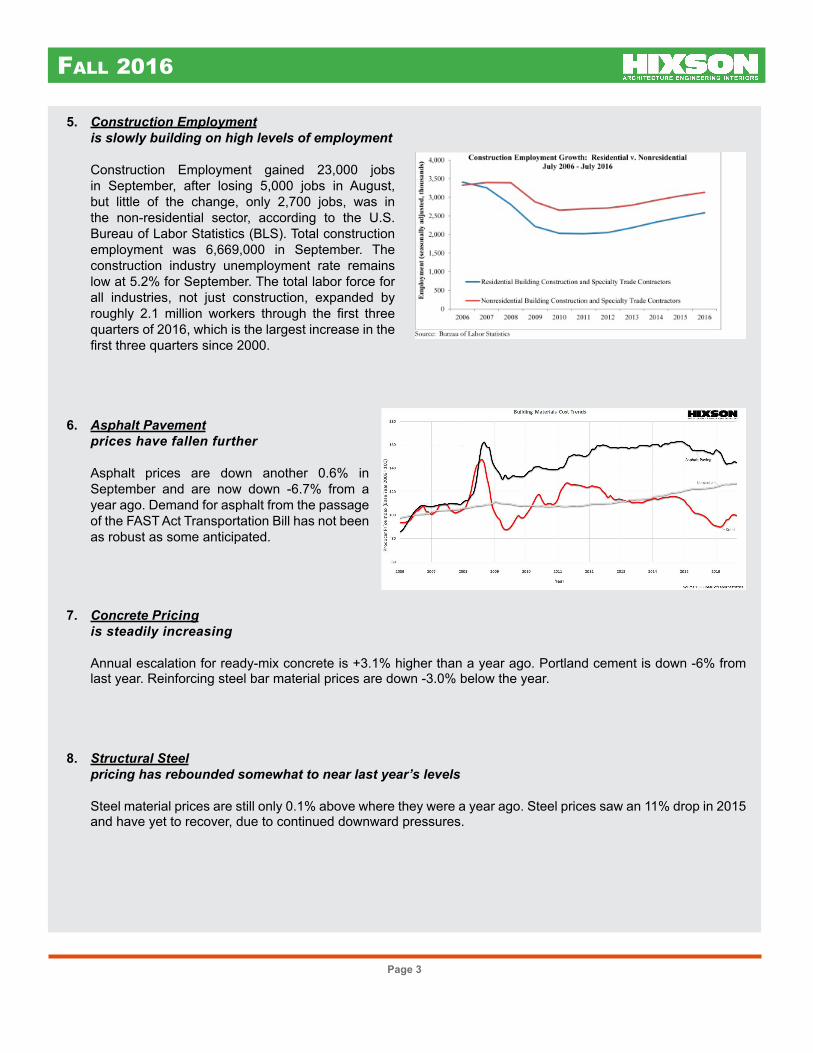

5. Construction Employment is slowly building on high levels of employment

Construction Employment gained 23,000 jobs in September, after losing 5,000 jobs in August, but little of the change, only 2,700 jobs, was in the non-residential sector, according to the U.S. Bureau of Labor Statistics (BLS). Total construction employment was 6,669,000 in September. The construction industry unemployment rate remains low at 5.2% for September. The total labor force for all industries, not just construction, expanded by roughly 2.1 million workers through the first three quarters of 2016, which is the largest increase in the first three quarters since 2000.

6. Asphalt Pavement prices have fallen further

Asphalt prices are down another 0.6% in September and are now down -6.7% from a year ago. Demand for asphalt from the passage of the FAST Act Transportation Bill has not been as robust as some anticipated.

7. Concrete Pricing is steadily increasing

Annual escalation for ready-mix concrete is +3.1% higher than a year ago. Portland cement is down -6% from last year. Reinforcing steel bar material prices are down -3.0% below the year.

8. Structural Steel pricing has rebounded somewhat to near last year’s levels

Steel material prices are still only 0.1% above where they were a year ago. Steel prices saw an 11% drop in 2015 and have yet to recover, due to continued downward pressures.

Fall 2016

Page 4

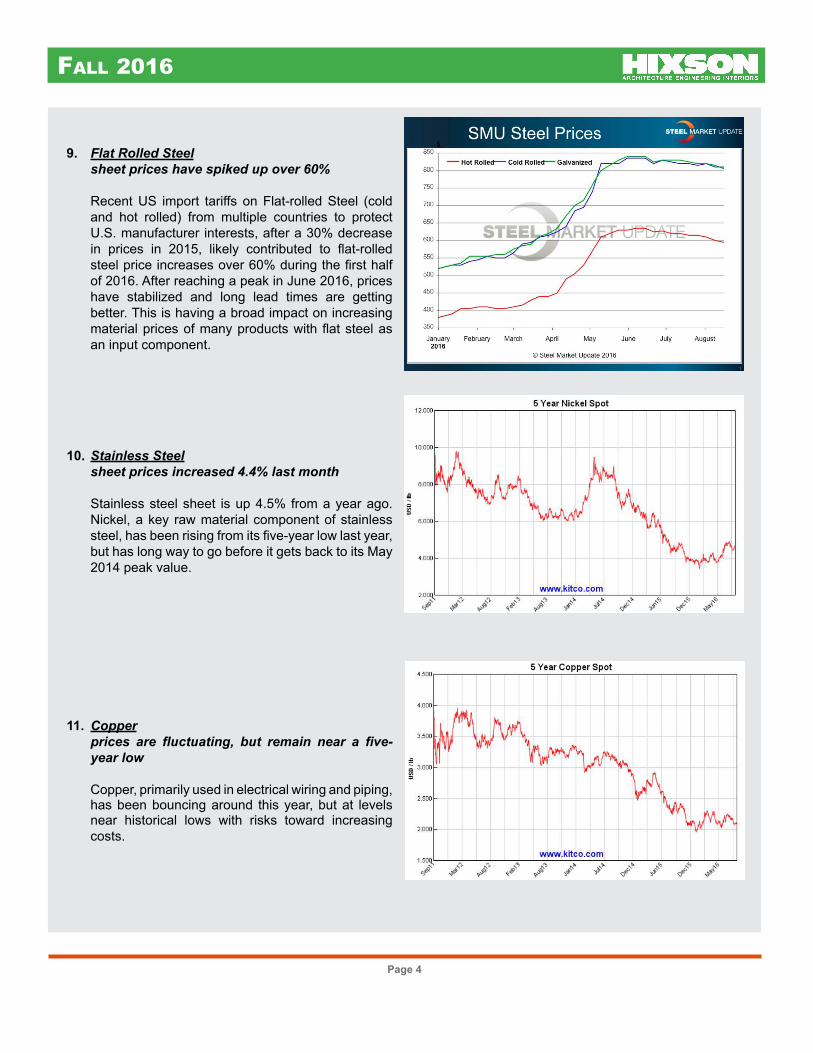

9. Flat Rolled Steel sheet prices have spiked up over 60%

Recent US import tariffs on Flat-rolled Steel (cold and hot rolled) from multiple countries to protect U.S. manufacturer interests, after a 30% decrease in prices in 2015, likely contributed to flat-rolled steel price increases over 60% during the first half of 2016. After reaching a peak in June 2016, prices have stabilized and long lead times are getting better. This is having a broad impact on increasing material prices of many products with flat steel as an input component.

10. Stainless Steel sheet prices increased 4.4% last month

Stainless steel sheet is up 4.5% from a year ago. Nickel, a key raw material component of stainless steel, has been rising from its five-year low last year, but has long way to go before it gets back to its May 2014 peak value.

11. Copper prices are fluctuating, but remain near a five-

year low

Copper, primarily used in electrical wiring and piping, has been bouncing around this year, but at levels near historical lows with risks toward increasing costs.

Fall 2016

Page 5

12. Pipe prices have increased, for the most part across the board this year, except for PVC pipe which is about

the same

Corrugated steel pipe is 4.2% above October 2015. Ductile iron pipe is up 5% above 2015. Reinforced concrete pipe is up 14.4% this year. PVC water pipe has increased only 0.1% this year.

About This Newsletter

Cost Trends is a publication created by the Hixson Cost Estimating department. Having a professional in-house estimating department is uncommon in design/engineering firms, but enables Hixson to fulfill our commitments to design/engineer a project to an agreed-upon cost, by knowing our clients, their projects, and the areas where those projects are built.

Because Hixson consistently works on projects throughout North America, we therefore have up-to-date information on prices and conditions that affect our work. Sources used to compile this edition of Cost Trends include:

• American Institute of Architects• Associated Builders & Contractors, Inc.• Associated General Contractors of America• Compass International Reports• Commodity Online• Construction Data Company• Dodge Data & Analytics• Engineering News Record

Hixson associates regularly participate in continuing professional education events across the country.Recent events attended by Hixson’s Cost Estimating Group include:

• ASPE Chapter Monthly Meetings

• AACE Section Monthly Meetings

Fall 2016

• Gilbane Construction Economics• IHS Global Insight• Kitco• Portland Cement Association• Rider Levett Bucknall Consultants• R.S. Means, Quarterly Cost Round-up• Turner Building Cost Index• U.S. Bureau of Labor Statistics

Advocacy:Hixsonisa“No-Bias”Company

At Hixson, we seek to serve as extended team members of our clients’ organizations, not as representatives of companies with outside concerns. Therefore, we do not accept income or incentives – or sell/represent products – from equipment suppliers, contractors or any company that could improperly influence our opinion. Because of this,

Hixson ensures that the information we present is unbiased and has been developed in the best interests of our clients.

659 Van Meter Street . Cincinnati, OH 45202P: 513.241.1230 F: 513.241.1287

www.hixson-inc.com