counterparty risk cva - operations...

TRANSCRIPT

Counterparty Risk

CVAEduardo Canabarro

Global Head of Risk Analytics

Morgan Stanley, New York

22

Disclaimer

This presentation containsstatements and views ofthe author only.

It is not intended torepresent the views ofMorgan Stanley.

33

Introduction

OTC derivatives are efficient and effective tools to transfer financialrisks between market participants

As a byproduct of such transfer, they create credit risk between thecounterparties

They also increase the connectedness of the financial system Banks have built sophisticated frameworks to manage their

counterparty credit risks Typically, a large bank has many thousands of counterparties,

trillions of dollars of derivatives’ notional and billions of dollars ofcredit exposures to their counterparties

In this presentation we’ll cover counterparty risk pricing (aka CVA),hedging, stress testing, capital, and CCPs

44

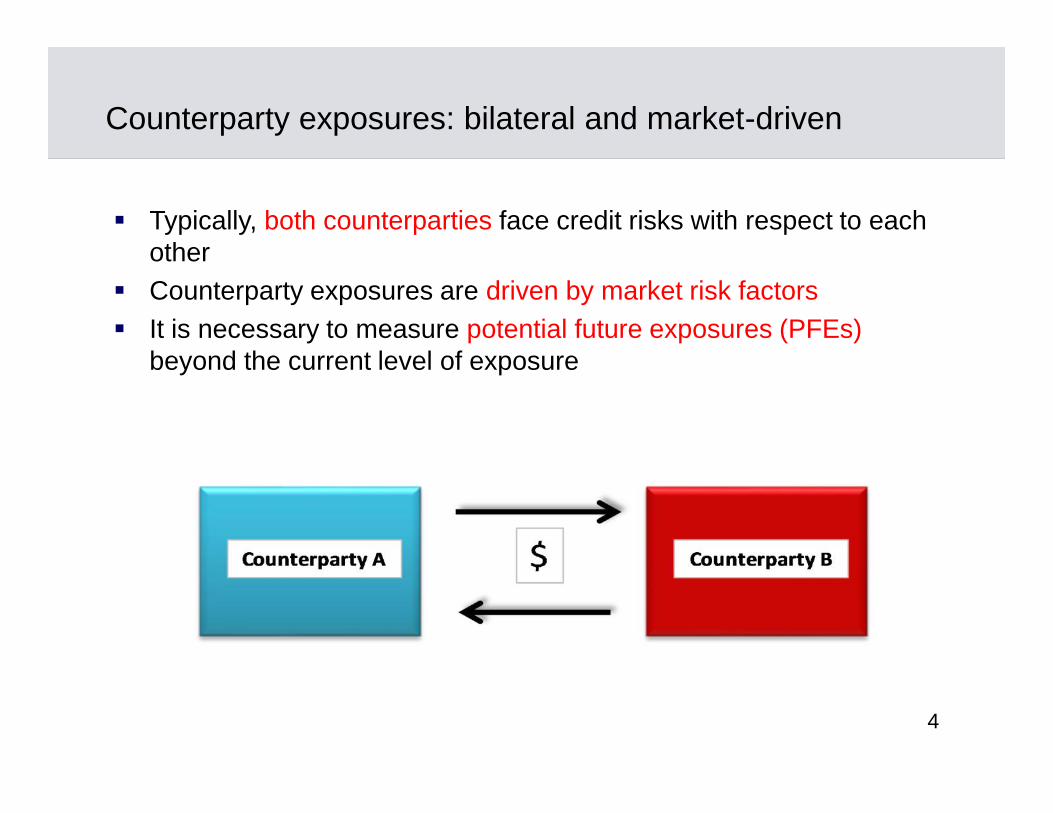

Counterparty exposures: bilateral and market-driven

Typically, both counterparties face credit risks with respect to eachother

Counterparty exposures are driven by market risk factors It is necessary to measure potential future exposures (PFEs)

beyond the current level of exposure

55

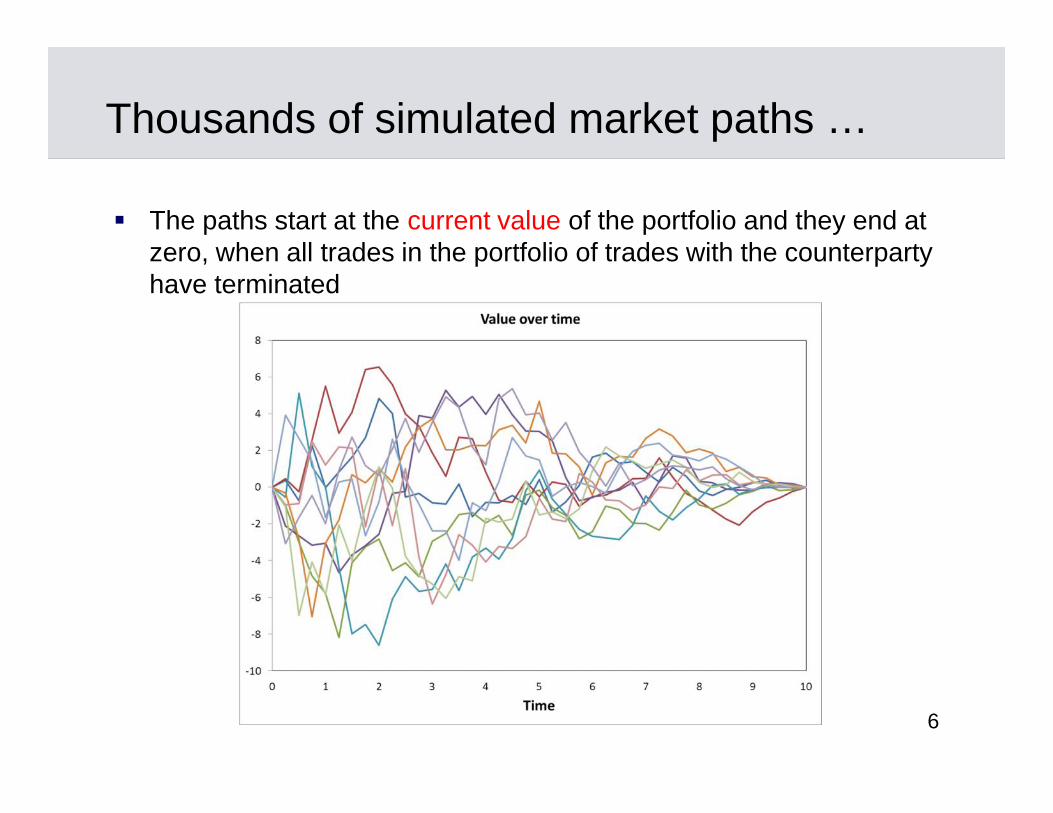

Simulation of PFEs

Banks use Monte Carlo methods to simulate the future values of theportfolio of derivatives with a counterparty

66

Thousands of simulated market paths …

The paths start at the current value of the portfolio and they end atzero, when all trades in the portfolio of trades with the counterpartyhave terminated

77

EPE and ENE

For each point in time on asimulated market path, wecalculate the exposure as themax(value of the portfolio, 0)

Expected Positive Exposure(EPE) is our averageexposure to the counterparty,across all paths, at each pointin time

Expected Negative Exposure(ENE) is the equivalent ofEPE, from the perspective ofour counterparty

88

EPE and ENE

The EPE and ENE profiles are central to the calculation of CVAs In sophisticated CVA models those profiles are calculated

conditional on the credit spreads of each counterparty

99

Credit Valuation Adjustment (CVA)

Bank A has a portfolio of OTC derivatives withCounterparty B

CVA is the adjustment to the risk-free value of theportfolio of OTC derivatives between A and B to reflectthe market value of the bilateral counterparty credit risksfaced them

Eduardo Canabarro and Darrell Duffie, Counterparty Risk: Measurement andPricing, 2003.http://www.darrellduffie.com/uploads/surveys/DuffieCanabarro2004.pdf

1010

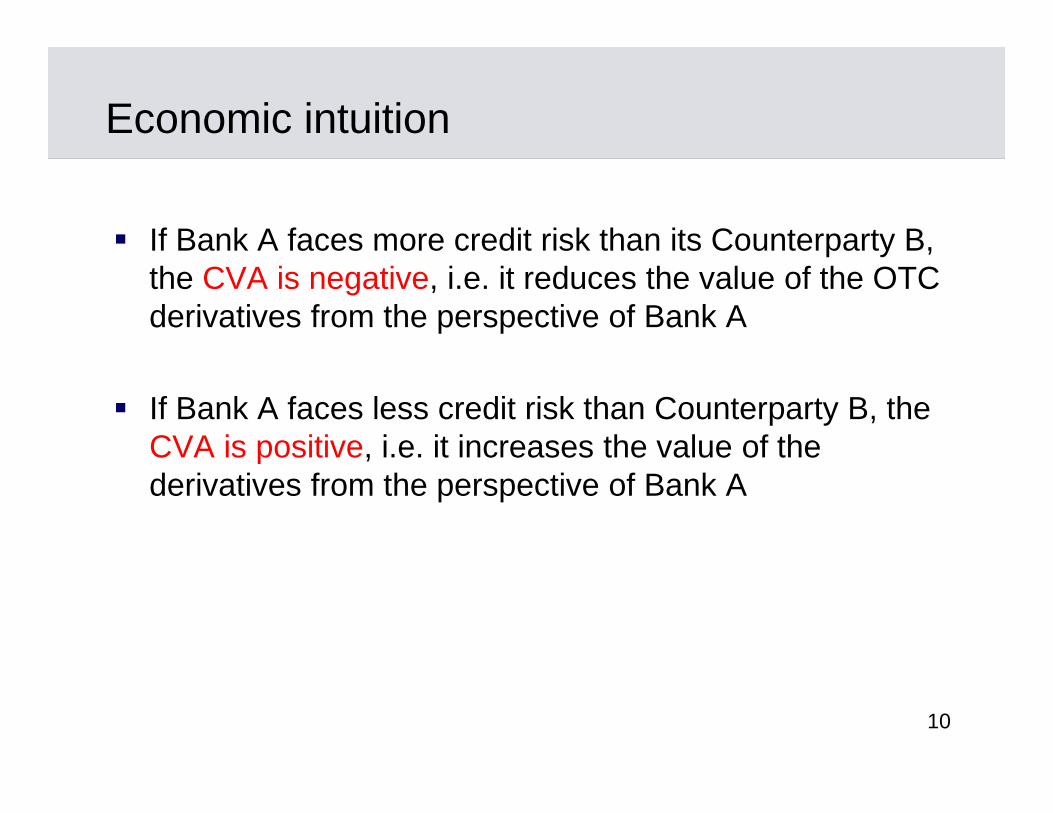

Economic intuition

If Bank A faces more credit risk than its Counterparty B,the CVA is negative, i.e. it reduces the value of the OTCderivatives from the perspective of Bank A

If Bank A faces less credit risk than Counterparty B, theCVA is positive, i.e. it increases the value of thederivatives from the perspective of Bank A

1111

CVA is part of the valuation of derivatives

CVA is an integral component of the value of derivatives

Ideally, CVA should be part of each trade’s valuationmodel

The reason it is calculated separately is that there areportfolio effects that transcend the valuation of eachtrade (e.g. netting and margin agreements)

CVA can be attributed to each trade on a marginalcontribution basis

1212

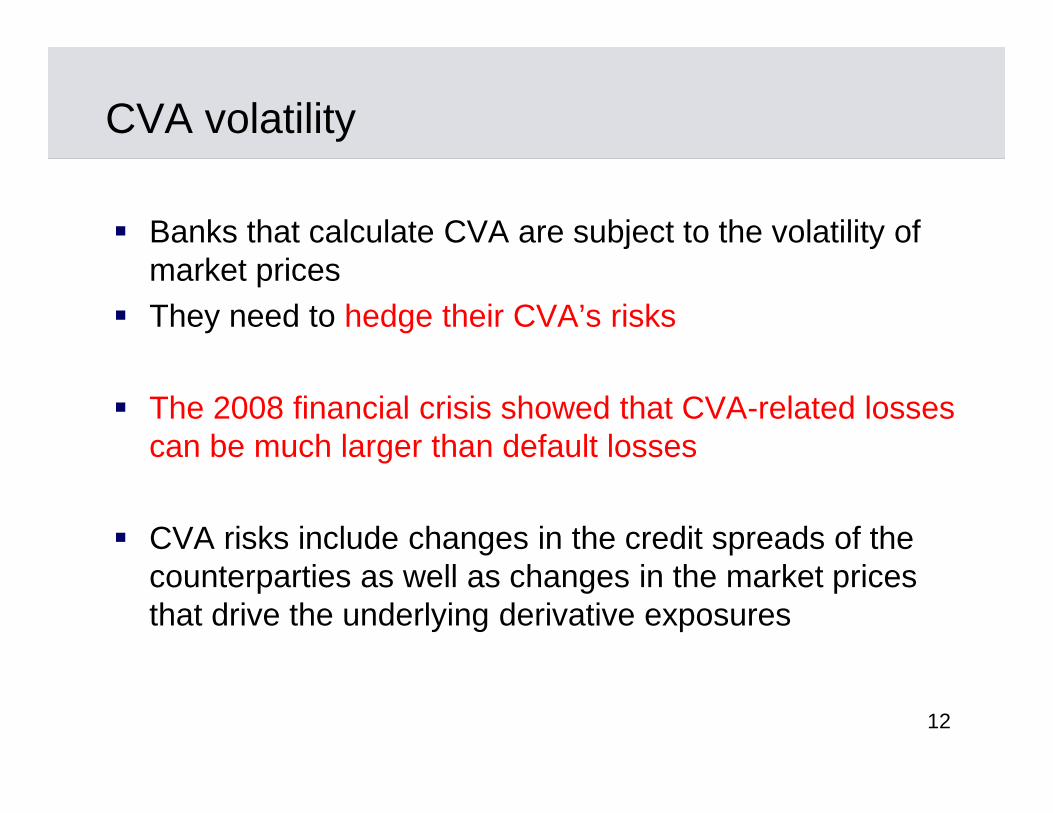

CVA volatility

Banks that calculate CVA are subject to the volatility ofmarket prices

They need to hedge their CVA’s risks

The 2008 financial crisis showed that CVA-related lossescan be much larger than default losses

CVA risks include changes in the credit spreads of thecounterparties as well as changes in the market pricesthat drive the underlying derivative exposures

1313

CVA risk management

The technology to mark to market and hedge CVA hasevolved over the last 20+ years

Investment banks started pricing and hedging CVAaround 1990 Litzenberger, R., Swaps: Plain and Fanciful, Journal of Finance, vol.47, pages

831-850, 1992. Sorensen, E., and T. Bollier, Pricing Swap Default Risk, Financial Analysts

Journal, 50, pp. 23-33, May-June 1994. Duffie, D. and M. Huang, Swap Rates and Credit Quality, Journal of Finance, v.

51, pp. 921-949, 1996

More recently, many more banks are pricing and activelyhedging their CVAs

1414

CVA calculation

In concise notation:

BBAA sEsECVA

EA is the present-valued expected exposure faced by counterparty Bwith respect to Bank A;

sA is the market loss rate (i.e. the product of risk-neutral PD and riskneutral LGD) of A

EB is the present-valued expected exposure faced by A with respectto B;

sB is the market loss rate of B.

1515

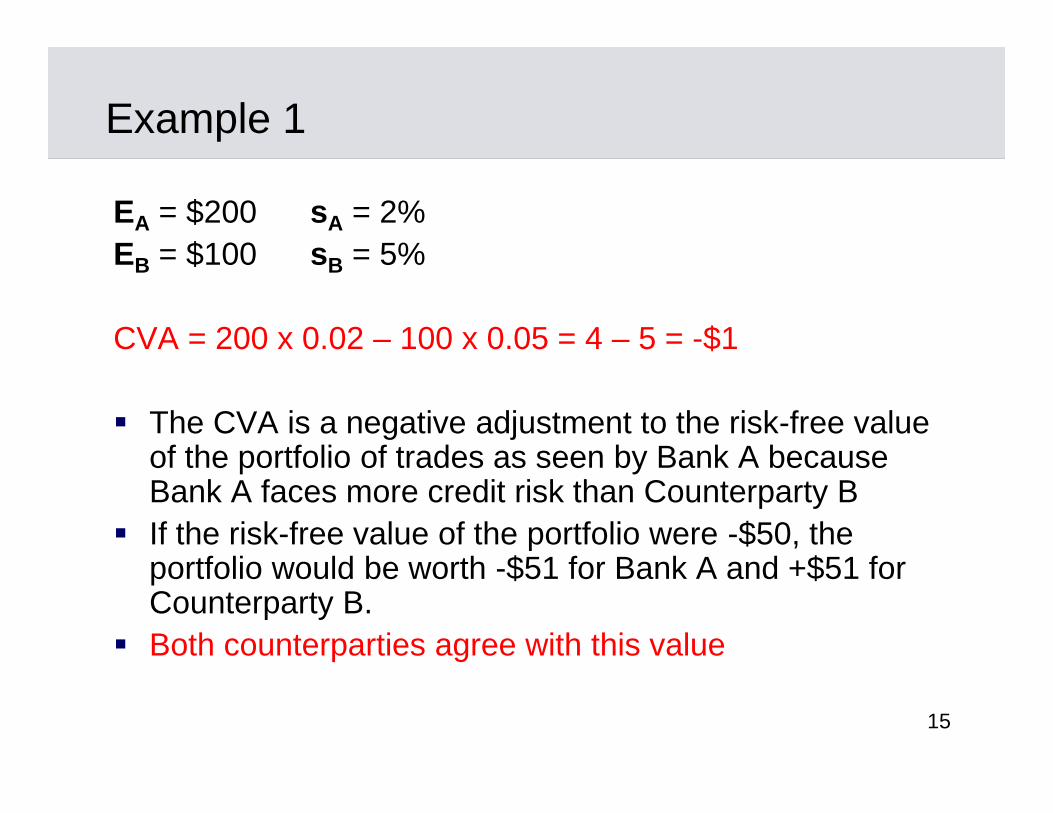

Example 1

EA = $200 sA = 2%EB = $100 sB = 5%

CVA = 200 x 0.02 – 100 x 0.05 = 4 – 5 = -$1

The CVA is a negative adjustment to the risk-free valueof the portfolio of trades as seen by Bank A becauseBank A faces more credit risk than Counterparty B

If the risk-free value of the portfolio were -$50, theportfolio would be worth -$51 for Bank A and +$51 forCounterparty B.

Both counterparties agree with this value

1616

Example 2

Now, suppose that Bank A exits the portfolio of tradeswith Counterparty B by transferring it to Bank C

C has sC = 5% and from C’s perspective:CVA = 200 x 0.05 – 100 x 0.05 = 10 – 5 = +$5

To effect the transfer, A pays +$51 to C C is a worse counterparty than A and it has to pay $6 to

B in order to compensate B for the drop in the value ofthe portfolio of trades from $51 to $45

All three parties break even and they agree with thetransactions

1717

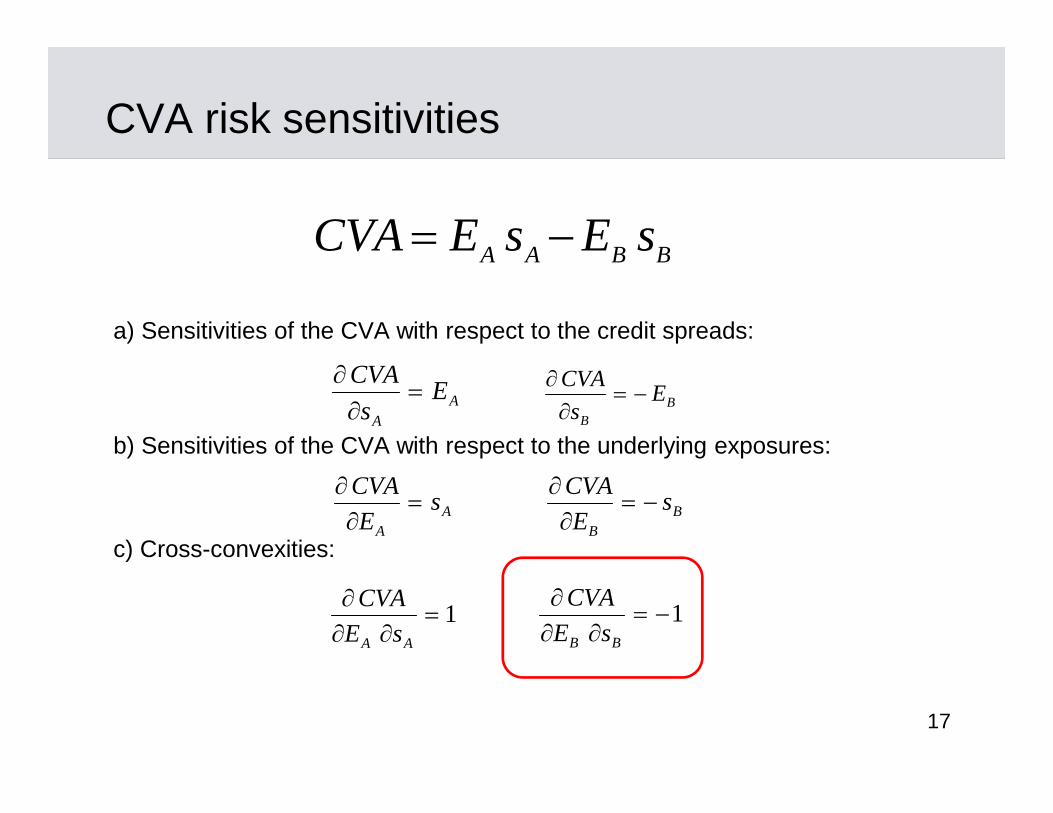

CVA risk sensitivities

a) Sensitivities of the CVA with respect to the credit spreads:

b) Sensitivities of the CVA with respect to the underlying exposures:

c) Cross-convexities:

AA

Es

CVA

BB

Es

CVA

AA

sE

CVA

BB

sE

CVA

1

AA sE

CVA1

BB sE

CVA

BBAA sEsECVA

1818

Should banks hedge their CVA?

If the bank marks to market its CVA and the bank doesnot hedge it, it will experience P&L (and earnings)variability

Importantly, in a trending and deteriorating credit marketenvironment, the bank could suffer substantialcumulative CVA losses

In the 2008 crisis, some banks lost many billions ofdollars in CVAs. This was particularly the case of banksthat did not actively hedge their CVAs

1919

CVA hedging: challenges

The hedges of the CVA include hedges of the marketrisk factors that drive the underlying exposures andhedges of the credit spreads of the counterparties

There are important cross-gammas which can be ofsubstantial size when the changes in spreads andexposures are large

During the 2008 crisis, due to the large size of the CVAsand the high volatility of markets (i.e. large ΔE and Δs),the cross-gammas created difficulties for CVA desks thatwere dynamically hedging the CVAs

Eduardo Canabarro, Pricing and Hedging Counterparty Risk: Lessons Re-Learned?, Chapter 6 in Canabarro E., editor, Counterparty Credit Risk, RiskBooks, 2010

2020

Should banks hedge their own spread?

ΔCVA / ΔEA = sAΔCVA / ΔsA = EAΔ2CVA / (ΔEA ΔsA ) = 1

Changes in the exposure EA can be hedged by takingpositions on the market risk factors that drive theexposure

Changes in Bank A’s own loss rate sA are morechallenging to hedge. The systematic risk componentcan be hedged. The bank-specific, idiosyncratic riskcomponent is more difficult to hedge

By hedging the systematic component of their own creditrisk, banks can realize the value of the liability CVA

2121

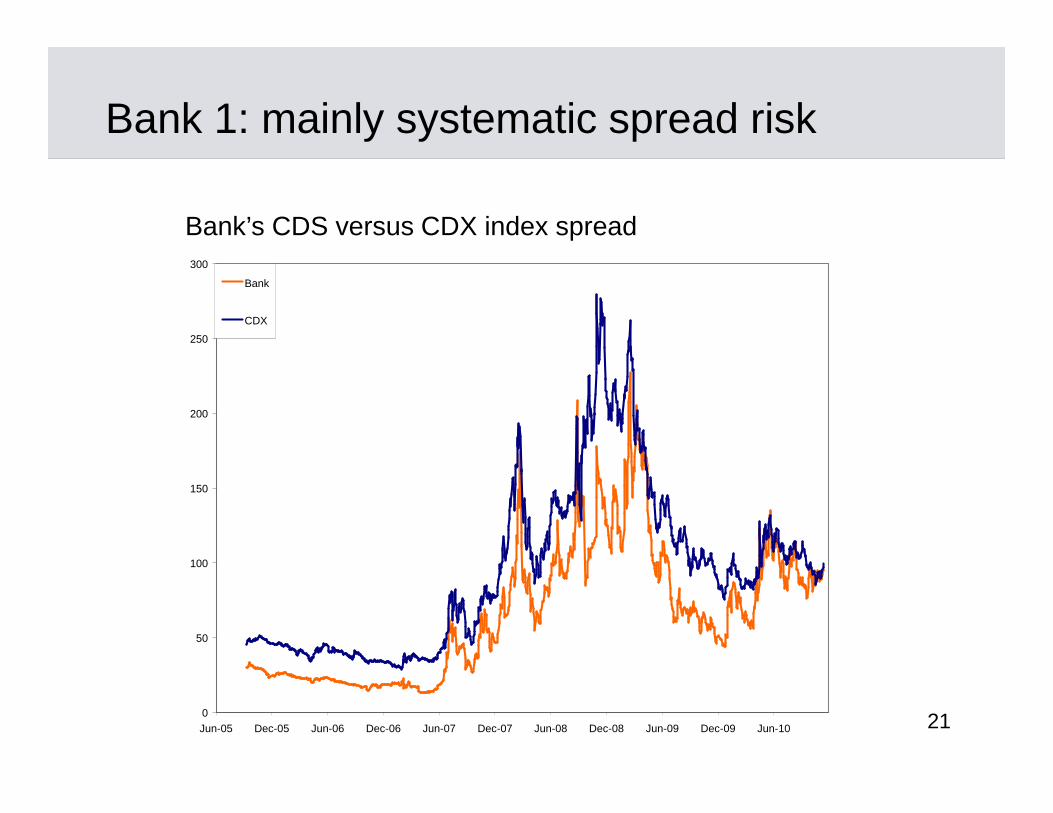

Bank 1: mainly systematic spread risk

0

50

100

150

200

250

300

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

Bank

CDX

Bank’s CDS versus CDX index spread

2222

Bank 2: some idiosyncratic spread risk

0

100

200

300

400

500

600

700

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

Bank

CDX

Bank’s CDS versus CDX index spread

2323

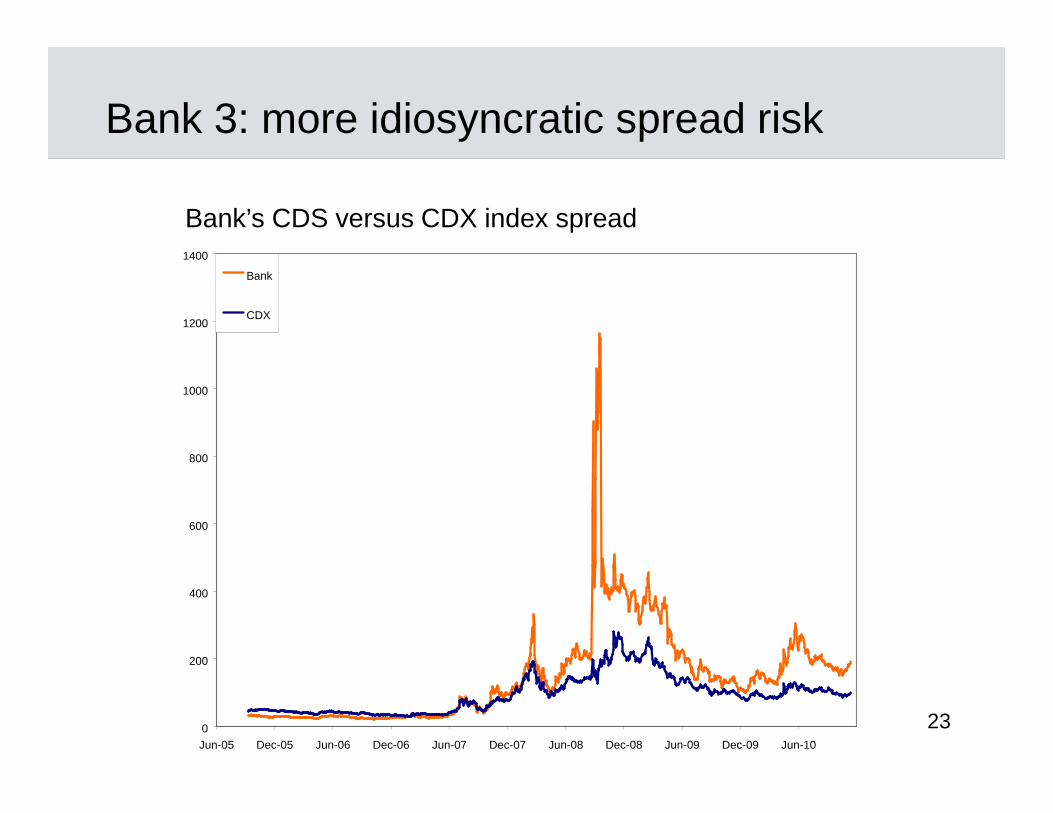

Bank 3: more idiosyncratic spread risk

0

200

400

600

800

1000

1200

1400

Jun-05 Dec-05 Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10

Bank

CDX

Bank’s CDS versus CDX index spread

2424

CVA desks

Some banks have opted for a central CVA desk Others have opted for various CVA desks deployed

within their main derivatives units CVA desks provide counterparty credit risk protection to

the derivatives trading desks They manage the risks of the CVA on an ongoing basis They are subject to market and credit risk limits and

usually do not have a revenue budget

2525

CVA risks

There are important risksthat often fall outside ofthe scope of the riskmeasurementframeworks: wrong way out of the money replacement costs dynamic hedging

“It is not what we know, butwhat we do not know whichwe must always address, toavoid major failures,catastrophes and panics.”Richard Feynman, physicist

2626

Wrong-way risks

There are wrong-risks that are specific to CVA hedging.Example: crowded counterparty risks

When a counterparty has entered into similar and largeOTC derivatives trades with many banks, the dynamichedging programs of the banks will create wrong-wayrisk

Usually, those wrong way risks do not show up untilcredit spreads and/or exposure have grown to somelarge levels

During the 2008 crisis this occurred with respect tomonoline insurers as well as other concentratedcounterparty exposures

2727

Wrong-way risks

The CVA wrong way risks are dynamic That is, they are a feature of dynamic hedging strategies They are different from the wrong way risks as usually

defined in the Banking Book context They can be large, i.e. non-local, if there is illiquidity in

exposure or credit spread hedges

2828

Out-of-the-money risks

Potential exposure models used for CVA calculation arenot good predictors of massive market dislocations

CVA traders need to be cautious in the pricing andhedging of out-the-money counterparty exposures

The ability to hedge those exposures in the future, asthey grow, needs to be assessed prudently consideringthe overall liquidity of the market

The profitability of such trades needs to be evaluatedconsidering the potential CVA risks and dynamichedging costs

2929

Replacement costs

Potential future exposure and CVA models account forthe benefits of collateral in the calculation of counterpartyexposures

The models measure the residual exposures after theconsideration of collateral

Banks should not underestimate the all-in costs ofreplacing trades with a defaulted counterparty

Especially when that counterparty is a large marketparticipant and its default can impair the liquidity andincrease the volatility of the markets where thederivatives trade (e.g. Lehman)

3030

Dynamic hedging costs

The risk management of CVAs requires dynamic re-balancing of the hedges

When the counterparty exposures and the credit spreadsof the counterparties are large and volatile, therebalancing requirements can be intense and costly

The high cost is due to illiquidity, wide bid-ask spreadsand overall market impact of the hedging program,especially when in crowded risk situations

Dynamic hedging costs are usually not explicitlycaptured in the CVA pricing models but they can be themost relevant cost component of large, concentratedCVA risks

3131

Simulation of dynamic hedging costs

We can use Monte Carlo simulation models to assessthe size of the costs of replication over the life of theCVA hedging program

The models incorporate the market frictions and providea realistic description of the probability distribution ofpotential CVA hedging costs

During the 2008 crisis, the costs of CVA hedging provedto be quite material in some cases

Eduardo Canabarro, Dynamic Hedging Costs of CVA, in Canabarro E.and M. Pykhtin, editors, Counterparty Credit Risk, Risk Books,forthcoming 2014.

3232

CVA Stress tests

Stress testing is a fundamental component of a soundCVA risk management program

The fundamental goals of the stress test frameworkshould be:- Identification of concentrations of market and credit

risks- Identification of out-of-the-money exposures- Identification of wrong-way risks- Identification of potentially large dynamic hedging

costs of CVA

3333

Basel 3 defines CVA using the Basel 2 IMM EE profiles.The market risk of CVA is then measured by the bank’sVaR model

Capital on CVA: advanced approach

IMM exposures for risk sensitivities VaR for credit spread risk Only spread risk; no exposure risk Single name and index hedges VaR and stressed VaR, times 3 Need IMM + VaR model approvals

3434

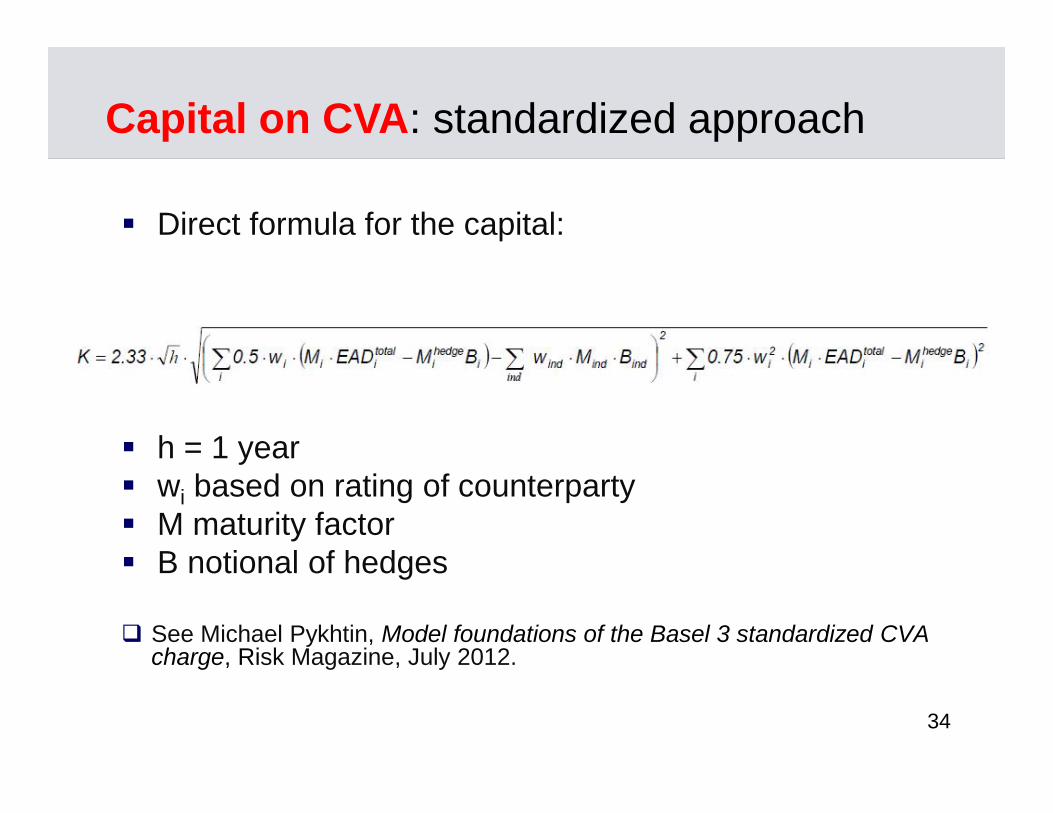

Capital on CVA: standardized approach

h = 1 year wi based on rating of counterparty M maturity factor B notional of hedges

See Michael Pykhtin, Model foundations of the Basel 3 standardized CVAcharge, Risk Magazine, July 2012.

Direct formula for the capital:

3535

Computational effort

Data Sourcing

Typically 2-10M trades, 2-10k netting sets and margin

agreements, market data

Trade Pricing

Typically 2-10M trades,over 1-2k paths at each of

100 dates

Simulation of Markets

Typically 1-2k paths of 2-5krisk factors over 100 future

dates per path

Exposure and CVAcalculations

Typically 10k nettingnodes

Back of envelope numbers: 2M trades x 2k paths x 100 dates/path = 400B pricings 400B pricings x 0.00001 sec/pricing = 400k secs = 111 CPU hours

This is just for one calculation … we need many more calculations toobtain CVA risk sensitivities.

3636

CVA systems

CVA systems are complex and computationallydemanding

Banks with large OTC derivatives franchises haveinvested large resources to build up these systems overthe last 10-15 years

3737

CVA systems

It is important to engineer the CVA system and modelsfor computational efficiency and speed

Various techniques have evolved to enable fastcalculations

Data storage strategies for trade and netting set dataand parallel processing are key elements

3838

The banks that implemented the most successful CVAsystems were the ones that pursued:

– Modularization– Parallel processing capability– Scalability– Pragmatic analytics

“… as simple as possible; but not simpler.”- Einstein

CVA systems

3939

Central Counterparties (CCPs)

Clearing Members (CMs)face a CPP instead offacing each other directly

Multilateral netting, marginrequirements, capitalbuffers, and highoperational standardsreduce the connectednessof the financial system

There will be trades leftoutside of the CCPs

4040

CCPs are critical components of the global financial andpayments systems

They are vital to financial stability They enable multilateral netting and collateralization They promote transparence and standardization of

trades They provide capital buffers to absorb counterparty

default losses They reduce connectedness and systemic risk

CCPs – favorable aspects

4141

Since 2009, inter-dealer clearing of OTC derivatives hasaccelerated

It is expected to continue increasing The largest counterparty risks faced banks are rapidly

shifting from peer banks to CCPs A typical large bank is a clearing member of tens of

CCPs and it is likely that its top 5-10 counterpartyexposures are already to CCPs today

CCPs – becoming large exposures

4242

Basel 2 did not charge regulatory capital on CCPs Basel 3 charges capital on exposures to CCPs: about

20% EAD, IMM based

Initial margin for OTC is typically at 95-99% confidencelevel, 5-day market move

Margin may also consider liquidity characteristics, riskconcentration and product-specific features

CCPs – capital and margin

4343

Defaulting CM margin Defaulting CM’s guarantee fund CCP’s equity capital (small) Guarantee funds of non-defaulting CMs Additional calls for capital on non-defaulting CMs

(unlimited liability)

CCPs – loss waterfall

4444

CCPs - concerns

Specialization Fragmentation Competition Too big to fail

This book describes the methods and practices used to manage OTCderivative counterparty risk and the performance of those methodsduring the 2008 financial crisis. It covers topics in counterparty riskmeasurement, CVA, CVA hedging, credit derivatives, collateralization,stress testing, back testing and integration of counterparty credit riskinto economic capital frameworks. Experiences and new ideas onmodels are discussed by a group of world-class experts. The contentof the book is particularly relevant in light of the Basel 3 rules on theregulatory capital on counterparty risks. The book contains a wealth ofinsights that can be useful for practitioners, regulators, consultants,accountants, lawmakers, auditors and researchers to understand thesubstantive, and often technical, issues related to counterparty riskmanagement.

Chapters by: Aaron Brown • Eduardo Canabarro • Guanghua Cao •Patrick Chen • Eduardo Epperlein • Jon Gregory • Andrew Hollings •Gregory Hopper • Sean Hrabak • Phillip Koop • Darren Measures •Shankar Mukherjee • Evan Picoult • Michael Pykhtin • Dan Rosen •David Rowe • David Saunders • Alan Smillie • Svein Stokke • Yi Tang •Lauren Teigland-Hunt • Dan Travers • Katsuichiro Uchiyama • AndrewWilliams • Wei Zhu

Counterparty Credit RiskMeasurement, Pricing and Hedging

Edited by Eduardo Canabarro

Online: riskbooks.com/counterparty-credit-risk-2ISBN: 978-1-906348-34-2