country report brazil. m&a update. spring 2013. norgestion mergers alliance

DESCRIPTION

TRANSCRIPT

Country Report - BrazilM&A update

Spring 2013

Brazil is a strategic focus forforeign corporates. Its role as hostof the 2014 FIFA World Cup and the2016 Summer Olympic Games isacting as a catalyst for a majorgovernment-led programme ofinfrastructure projects acrossthe country.

Foreign corporates are attractedto these high growth opportunitiesavailable across Brazil’s economy.Brazil attracts one of the highestlevels of FDI globally and withinvestment expected to reach arecord US$70 billion in 2013,competition for high qualityassets is increasing.

Key findings from our research:

Foreign corporates from low growtheconomies are participating in Brazil’sUS$600 billion plus investmentprogramme to upgrade infrastructureand increase energy production. Thedemand for experienced specialistproviders is creating opportunitiesacross the supply chain and drivinginbound M&A.

Brazil is forecast to be the fifth largestconsumer market globally by 2020.Both foreign corporates andinternational financial investors

are using acquisitions of leadingdomestic brands to enter the marketand establish a platform for growth.

Brazil has a complex operatingenvironment and investors typicallyenter the market via a joint venture orthrough a majority stake acquisitionwhich can include a path to fullownership.

Brazil is a corestrategic market forforeign corporateswith international

ambitions

“The increase in globalcross-border capital flowscombined with Brazil’smacro-economicfundamentals and disciplinedpolicies makes Brazil a veryattractive destination forforeign companies to invest.”Leonardo Antunes, Managing Director, BroadSpan

Major growth opportunities drivinginbound M&A

MergersAlliance20

13

Brazil M&A update

2

Foreign directinvestment to reachrecord US$70 billionin 2013Brazil is the third most attractiveinvestment destination by valueglobally with only China and theUS attracting a higher proportion ofinbound foreign direct investment (FDI).

GDP growth is forecast to exceed3% in 2013 (see Figure 1). Thedomestic economic stimulusimplemented during 2012 will supporthigher growth. Real interest rates arecurrently close to historical lows, retailsales are increasing, unemployment islow by Brazilian standards and industrialand business confidence is rising.

Higher growth means Brazil remainsattractive for inflows of FDI. FDI areexpected to increase from an estimatedUS$64 billion in 2012 to US$70 billion in2013 and US$75 billion in 2014(see Figure 2). The US, UK, Spain,Germany and China account for themajority of investment.

Mer

gers

Allia

nce

2013

Inbound FDI favoursdomestic sectors and

commodities6.1%

5.2%

-0.3%

7.5%

2.7%

0.9%

3.1%

2007 2008 2009 2010 2011 2012 2013*F

Figure 1: Gross domestic product(% growth YoY)

Source: Brazilian Statistics Bureau, *Credit Suisse

International companies have focusedon sectors linked to rising consumerspending including food products andbeverages, retail and consumerproducts, insurance and commodities(see Figure 2). Around 75% ofinvestments have been made inprojects with a value less thanUS$500 million.

Figure 2: Foreign direct investment (US$ billions)

2007 2008 2009 2010 2011 2012E* 2013F* 2014F*

34.6

45.1

25.9

48.5

66.7 64.070.0

75.080

70

60

50

40

30

20

10

0

US

$b

illio

ns

Source: Central Bank of Brazil, *Credit SuisseSource: Central Bank of Brazil

Oil & gas extraction: 4.4

Food products& beverages: 6.7

Metals: 6.5

Commerce(ex. vehicles): 5.9

Insurance: 4.4

Financial services: 4.3

Top 5 FDI by segment 2012 (US$ billions)

Brazil M&A update

3

Fifth largestconsumer marketglobally by 2020By 2020 Brazil is forecast to be thefifth largest consumer market in theworld with household consumptionof US$1.8 trillion. Foreign companiesare attracted to consumers’discretionary spending power(see Figures 3 and 4). The middleclass has grown to around 133million people in 2014 with 85% ofthe population living in urban areas.Brazilian consumers are optimisticabout the outlook for their householdincome, and fiscal initiatives have beentargeted to support consumption.

Foreign brands are taking advantageof the growth in spending on areassuch as alcohol, technology andfashion. For example, UK drinksgiant Diageo acquired the leadingpremium cachaça brand Ypióca forUS$455 million in 2012. Cachaça is thelargest spirits category in Brazil and theacquisition gives Diageo a platform forthe sale of premium international spiritsbrands in Brazil.

Mer

gers

Allia

nce

2013

Brazil is benefitingfrom high consumer

spending

11.1%

2004 2005 20072006 2008 2009 2010 2011 2012

3.1%

6.4%

13.6%

9.9%

6.8%

12.2%

6.6%

8.0%

Average growth rate

Figure 4: Broad retail sales % YoY

Source: Brazilian Institute of Geography and Statistics

10.2

USA JapanChina Germany Brazil France UK Italy

5.4

3.5

2.21.8 1.6 1.5 1.4

Figure 3: Global consumer marketin 2020 US$ trillion

Source: Exame Magazine and McKinsey

As incomes have risen, consumers arealso spending more on buying servicessuch as education and healthcare.This is leading to M&A.

- H.I.G. Capital acquired Cel LepIdiomas, a leading premium EnglishLanguage Teaching network, in 2012

- Italian global medical devicemanufacturer Sorin Group recentlyacquired Alcard Industria Mecanica,a manufacturer of medical devices forcardiac surgery

- Canada-based Valeant is a serialacquirer and has established a strongpresence in dermatology and thesports food supplement marketwith the acquisitions of InstitutoTerapêutico Delta, Bunker IndustriaFarmacêutica and Probiotica

- US-based Agfa HealthCare acquiredhealthcare IT company WPD,enabling Agfa to increase its marketshare for imaging and IT systems forradiology in Brazil

4

Brazil M&A update

Foreign companieswill bid in 2013infrastructure

concession auctions

Bottlenecks drivingmajor infrastructurespendThe 2014 FIFA World Cup and 2016Summer Olympic Games are actingas a catalyst for public and privateinvestment to upgrade Brazil’sinfrastructure, which is runningat overcapacity and slowingeconomic growth.

The Government will spendUS$33 billion on preparations tohost the World Cup and Olympicsincluding building stadiums, watersports venues, hotels, roads,subways and airports. This will besupplemented by investment from thecorporate sector in the supply chainrelated to the events.

Brazil is auctioning concessions formajor airports, railways and toll roads.Auctions, which will typically be wonon price, are open to internationalcompetition. Foreign corporates areattracted to companies withconcessions. For example, in 2012US-based Brookfield Infrastructureestablished a joint venture with AbertisInfraestructuras to acquire a majoritystake in Arteris for US$1.7 billion.Arteris is one of the largest ownersand operators of toll road concessionsin Brazil

Foreign corporates are using theirtechnical expertise to supplementBrazil’s less mature infrastructurecapabilities. Companies from theUK are particularly active:

- Balfour Beatty entered the marketvia a partnership with leadingconstruction company CamargoCorrêa and is working on rail linksto the mining industry based innorth Brazil

Mer

gers

Allia

nce

2013

20

70

80

90

50

60

30

40

10

100

0

Fiat

Ford

Rena

ultHo

nda

Niss

an

Othe

rs

Market Share %21.7%

9.0%

6.5%

4.9%4.3% 3.6%

Citro

en

2.7%

6.7%

GM

18.2%

Hyun

dai

VW

20.6%

Toyo

ta

2.0%

Figure 5: Foreign brands dominatecar sales (2012 sales units 10k)

Source: KARI, Mirae Asset Research

Demand for automobiles is increasing,but with light vehicle density just 137per 1,000 people compared to morethan 640 cars in the US, the potentialfor growth is significant. Brazil’s autosales hit a record high in 2012, growingby over 6% from 2011 to reach over3.6 million vehicles (excluding trucksand buses).

Demand is being boosted by reducedindustrial products tax and an increasein financed car purchases. As shownin Figure 5, a range of foreignmanufacturers including Fiat andVolkswagen have a significant marketshare for their locally-produced vehiclesand are investing heavily to developlocal production capabilities.

5

Brazil M&A update

Mer

gers

Allia

nce

2013

US$ billion

Electricitygeneration

Housing

Airports

Highways

Water andsanitation

Railroads

Telecommunications

Energy includingPetrobras

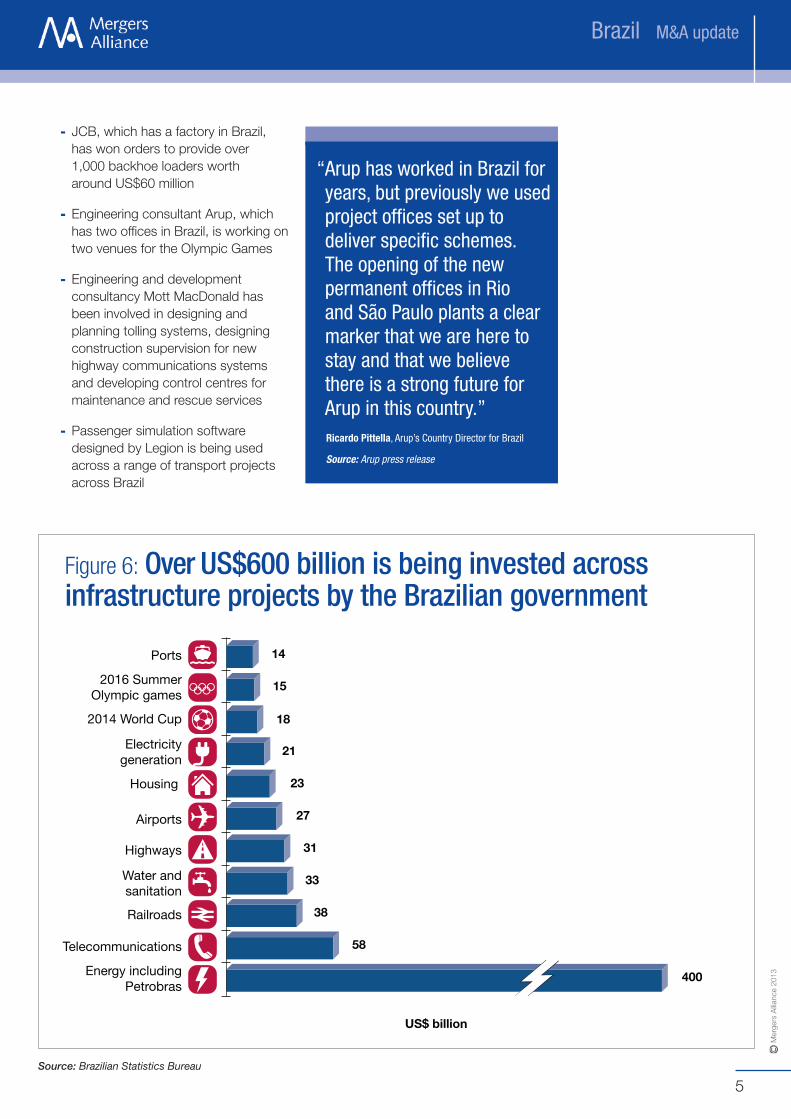

21

23

27

31

33

38

58

400

2016 SummerOlympic games

15

2014 World Cup 18

Ports 14

Figure 6: Over US$600 billion is being invested acrossinfrastructure projects by the Brazilian government

Source: Brazilian Statistics Bureau

- JCB, which has a factory in Brazil,has won orders to provide over1,000 backhoe loaders wortharound US$60 million

- Engineering consultant Arup, whichhas two offices in Brazil, is working ontwo venues for the Olympic Games

- Engineering and developmentconsultancy Mott MacDonald hasbeen involved in designing andplanning tolling systems, designingconstruction supervision for newhighway communications systemsand developing control centres formaintenance and rescue services

- Passenger simulation softwaredesigned by Legion is being usedacross a range of transport projectsacross Brazil

“Arup has worked in Brazil foryears, but previously we usedproject offices set up todeliver specific schemes.The opening of the newpermanent offices in Rioand São Paulo plants a clearmarker that we are here tostay and that we believethere is a strong future forArup in this country.”Ricardo Pittella, Arup’s Country Director for Brazil

Source: Arup press release

6

Brazil M&A update

Mer

gers

Allia

nce

2013

BroadSpan is the Brazilian partnerof Mergers Alliance. LeonardoAntunes, BroadSpan’s ManagingDirector has completed deals,capital raising and project

finance worth over US$15 billion in South America.He discusses M&A trends and provides insightsinto how foreign companies are entering Brazil.

BroadSpan is helping a range of investors accessopportunities in Brazil

We are currently working with both public and privateforeign companies, as well as private equity whorecognise that they need to supplement their expertisewith local specialists who have significant strategic andtransaction experience. Most inbound interest is currentlycoming from the US, UK, France and Spain.

M&A activity is focused on three key areas

Companies based in the low growth developedeconomies are being forced to look to faster growingcountries like Brazil for opportunities. Developedeconomies have mature industrial sectors, sophisticatedbusiness services providers and leading consumerbrands. Companies in these areas are taking advantageof the scale of investment being made across Brazil’sinfrastructure and energy supply chain, and the spendingpower of the rapidly increasing middle class. This is beingreflected in M&A activity (see page 8).

While the mega deals grab the headlines, there is a lot ofactivity by large and mid-sized foreign players acquiringsmaller niche players such UK-based Intertek, whichrecently acquired an 85% stake in Brazilian toy andconsumer products testing laboratory E-Test forUS$9.9 million.

Using a local advisor is critical to developing andimplementing the right market entry strategy

The operating environment for businesses in Brazil iscomplex and poor advice will lead to costly delays andmissed opportunities. It’s vital that companies work with alocal advisor who is able to use their market insight andpersonal relationships with companies and thegovernment to help formulate the right entry

strategy, use their expertise to evaluate the best localopportunities and deliver a transaction successfully.

Potential acquirers need to consider issuesspecific to Brazil

Around 90% of businesses in Brazil are family-ownedand many will not have considered an exit strategy.This presents challenges to potential overseas acquirers.It is common for these businesses to maintain two setsof books and for results to be unaudited. High taxesbased on revenue rather than profit mean owner-managers are careful about what they declare to thetax authorities. But this often creates a valuation gapwith an overseas buyer because of the differencebetween the declared profit and the actual profit.

BroadSpan has significant experience of creatingdeal structures which recognise fair value andmeet the governance standards demandedby overseas buyers.

Different sectors have specific legislationand tax rules

Foreign corporates need to be aware of the specificrequirements associated with operating in Brazil whichgovern a range of issues including the level of foreignownership permitted, local content and licensingrequirements and taxation and employment practices.

For example, Brazil has multiple taxation regimes withdifferent levels of taxing authorities. Tax laws changefrequently, so it’s not unusual for companies andtheir advisors to work with more than one tax specialist.

The status of employees can also raise issues, especiallyin the business services sector and consulting inparticular. For example, to reduce employment taxesmany employees in the service sector are contractors butif an acquirer wants to make employees permanent post-deal, this may trigger historic payroll tax and socialsecurity liabilities (see Case study on page 7).

To protect overseas acquirers from claims, Sale &Purchase Agreements tend to include a higher numberof indemnification clauses than an overseas acquirermight be used to.

A perspective on M&A trends and market entry strategies

7

Brazil M&A update

Mer

gers

Allia

nce

2013

Undertaking rigorous due diligence is especiallyimportant in Brazil

We always try to identify and qualify potential issues forour clients in advance of commencing full diligence toavoid surprises and gain early visibility of those areaswhich may have a significant impact on the value andthe transaction process.

Should a client wish to proceed and given the issuesdiscussed earlier, due diligence is critical and can uncoverissues such as liabilities associated with existing litigationand potential claims, which affect the valuation of a targetand potentially negotiations.

Ensure the acquisition structure is tax efficient

Acquirers need to engage early with tax and legalspecialists to ensure a transaction is structured torepatriate dividends and earnings in the most tax efficientway possible. Brazil has signed double tax treaties withonly a handful of countries and so holding companies andinvestment vehicles are often located in jurisdictionslike the Netherlands.

New pre-merger review requirement affectstransaction planning

New competition laws introduced in 2012 are potentially asignificant hurdle for cross-border transactions. Under theprevious notification process, transactions could becompleted before CADE (Administrative Council forEconomic Defense) had given its approval. Now reportabletransactions (one party has turnover in Brazil ofapproximately US$400 million and the other US$40 million)need to receive CADE’s approval before a transaction cancomplete. The waiting period for a reportable transaction

to be reviewed can be up to 330 days. As yet there isno fast track process, although to date “non-complex”transactions have been cleared in around 18 days.Although this creates uncertainty for the vendor andacquirer, the new process removes the possibility ofpost-merger remedial action.

The new notification and approvals process needs tobe factored into the timetable planning for a transaction,especially as the information required in a notificationform for a complex transaction is considerable.

Companies prefer to create joint ventures oracquire a majority position

Most companies prefer to enter the market via a jointventure or through a majority stake acquisition. Dealstructures range from 50% to 80% and can include a pathto full ownership over a two to four year period. The scaleof a foreign company’s first acquisition varies with somepreferring to make smaller acquisitions in order tounderstand the market better before making a largermove. Our experience suggests that a staggeredapproach to full ownership helps to align the interestsof a company’s founder or shareholders.

Outlook for foreign investors over the next12 months is positive

The upcoming World Cup and Olympics, rising purchasingpower of the middle class and range of government-supported growth measures means Brazil has theattention of global corporates and investors looking forstrategic growth. This will drive increasing competition forhigh quality assets and stimulate inbound, outbound anddomestic M&A.

Case study: Accenture’s acquisition of RiskControlBroadSpan advised RiskControl, a privately heldrisk consulting company based in Rio de Janeiro,on its recent sale to US consulting and technologyservices company Accenture.

Reason for acquisition

The acquisition complemented and expandedAccenture’s risk service in the rapidly growingBrazilian market. It also gave Accenture access to the

end-to-end software tool RiskControl, a softwareplatform that helps companies manage, monitor andevaluate risks throughout their business.

How the deal was transacted

BroadSpan navigated through complex deal structureswhich addressed issues associated with contingentworkers including contractors and permanentemployees in order to maximize RiskControl's value.

8

Brazil M&A update

180

160

140

120

100

80

60

40

20

60,000

50,000

40,000

30,000

20,000

10,000

00

Num

ber

of

dea

ls

Dis

clo

sed

valu

e(B

RL

mill

ion)

Indus

trials

Infor

mat

ionTe

chno

logy

Real E

state

Finan

cials

Food

&Drin

k

Health

care

Busine

ssSer

vices

Consu

mer

Produc

ts

Utilitie

s

Natur

alre

sour

ces

Energ

y

Constr

uctio

n

DealsDisclosed Value (RHS)

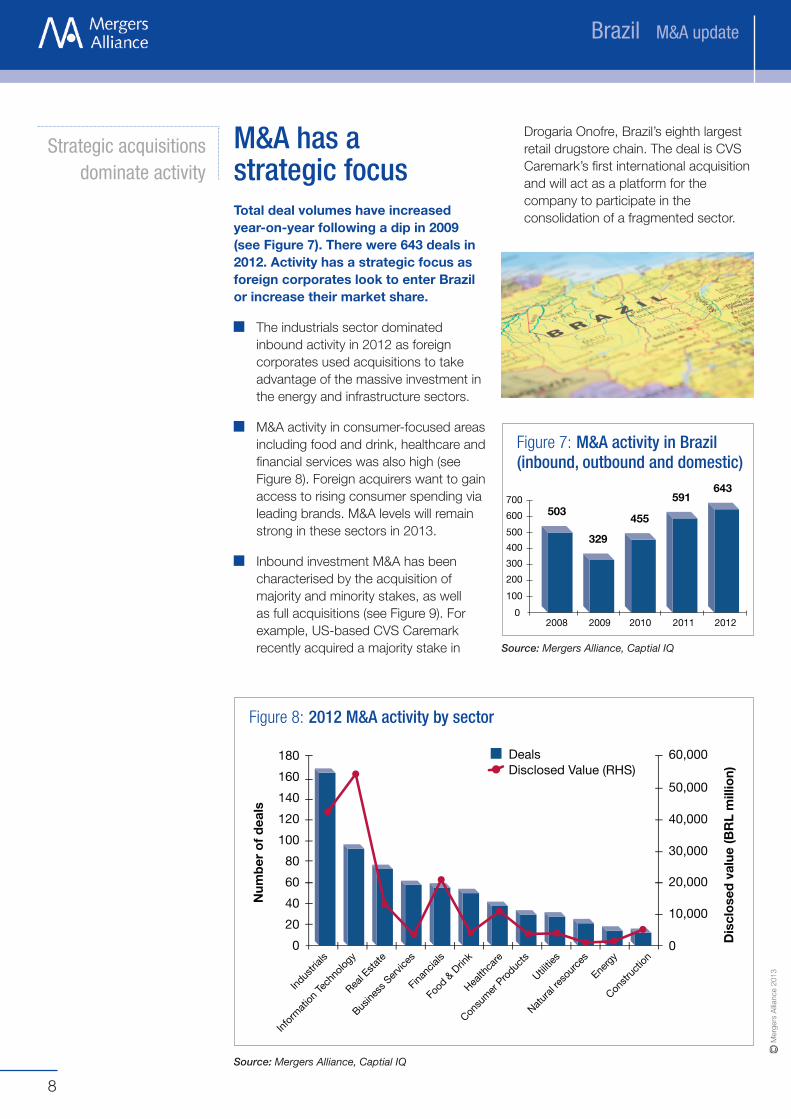

Figure 8: 2012 M&A activity by sector

Source: Mergers Alliance, Captial IQ

Strategic acquisitionsdominate activity

M&A has astrategic focusTotal deal volumes have increasedyear-on-year following a dip in 2009(see Figure 7). There were 643 deals in2012. Activity has a strategic focus asforeign corporates look to enter Brazilor increase their market share.

The industrials sector dominatedinbound activity in 2012 as foreigncorporates used acquisitions to takeadvantage of the massive investment inthe energy and infrastructure sectors.

M&A activity in consumer-focused areasincluding food and drink, healthcare andfinancial services was also high (seeFigure 8). Foreign acquirers want to gainaccess to rising consumer spending vialeading brands. M&A levels will remainstrong in these sectors in 2013.

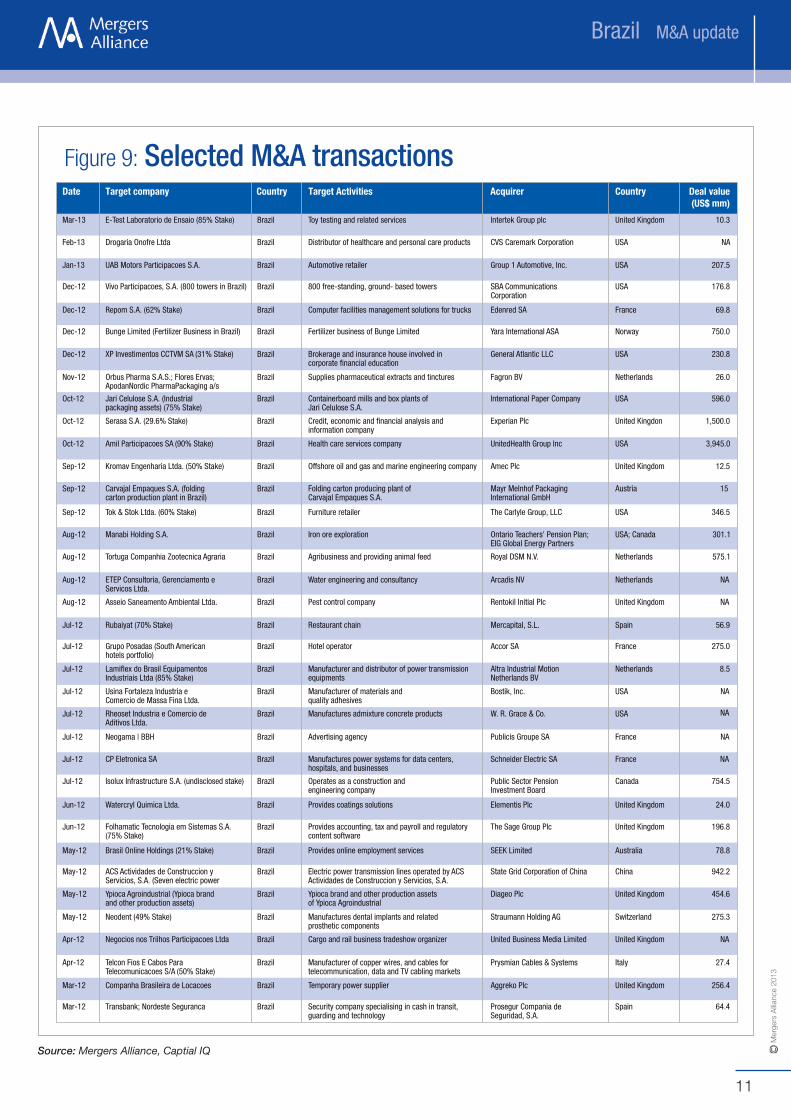

Inbound investment M&A has beencharacterised by the acquisition ofmajority and minority stakes, as wellas full acquisitions (see Figure 9). Forexample, US-based CVS Caremarkrecently acquired a majority stake in

Drogaria Onofre, Brazil’s eighth largestretail drugstore chain. The deal is CVSCaremark’s first international acquisitionand will act as a platform for thecompany to participate in theconsolidation of a fragmented sector.

2008 2009 2010 2011 2012

503700

600

500

400

300

200

100

0

329

455

591643

Figure 7: M&A activity in Brazil(inbound, outbound and domestic)

Source: Mergers Alliance, Captial IQ

Mer

gers

Allia

nce

2013

9

Brazil M&A update

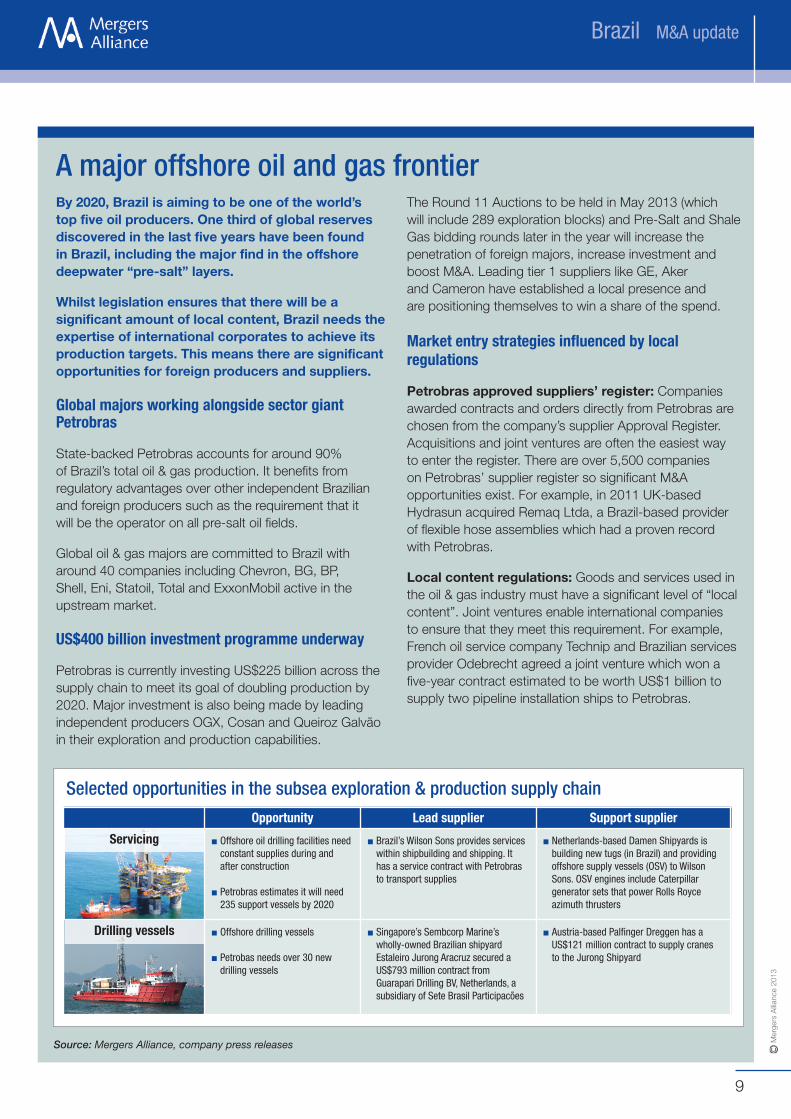

By 2020, Brazil is aiming to be one of the world’stop five oil producers. One third of global reservesdiscovered in the last five years have been foundin Brazil, including the major find in the offshoredeepwater “pre-salt” layers.

Whilst legislation ensures that there will be asignificant amount of local content, Brazil needs theexpertise of international corporates to achieve itsproduction targets. This means there are significantopportunities for foreign producers and suppliers.

Global majors working alongside sector giantPetrobras

State-backed Petrobras accounts for around 90%of Brazil’s total oil & gas production. It benefits fromregulatory advantages over other independent Brazilianand foreign producers such as the requirement that itwill be the operator on all pre-salt oil fields.

Global oil & gas majors are committed to Brazil witharound 40 companies including Chevron, BG, BP,Shell, Eni, Statoil, Total and ExxonMobil active in theupstream market.

US$400 billion investment programme underway

Petrobras is currently investing US$225 billion across thesupply chain to meet its goal of doubling production by2020. Major investment is also being made by leadingindependent producers OGX, Cosan and Queiroz Galvãoin their exploration and production capabilities.

The Round 11 Auctions to be held in May 2013 (whichwill include 289 exploration blocks) and Pre-Salt and ShaleGas bidding rounds later in the year will increase thepenetration of foreign majors, increase investment andboost M&A. Leading tier 1 suppliers like GE, Akerand Cameron have established a local presence andare positioning themselves to win a share of the spend.

Market entry strategies influenced by localregulations

Petrobras approved suppliers’ register: Companiesawarded contracts and orders directly from Petrobras arechosen from the company’s supplier Approval Register.Acquisitions and joint ventures are often the easiest wayto enter the register. There are over 5,500 companieson Petrobras’ supplier register so significant M&Aopportunities exist. For example, in 2011 UK-basedHydrasun acquired Remaq Ltda, a Brazil-based providerof flexible hose assemblies which had a proven recordwith Petrobras.

Local content regulations: Goods and services used inthe oil & gas industry must have a significant level of “localcontent”. Joint ventures enable international companiesto ensure that they meet this requirement. For example,French oil service company Technip and Brazilian servicesprovider Odebrecht agreed a joint venture which won afive-year contract estimated to be worth US$1 billion tosupply two pipeline installation ships to Petrobras.

Opportunity Lead supplier Support supplier

Offshore oil drilling facilities needconstant supplies during andafter construction

Petrobras estimates it will need235 support vessels by 2020

Brazil’s Wilson Sons provides serviceswithin shipbuilding and shipping. Ithas a service contract with Petrobrasto transport supplies

Netherlands-based Damen Shipyards isbuilding new tugs (in Brazil) and providingoffshore supply vessels (OSV) to WilsonSons. OSV engines include Caterpillargenerator sets that power Rolls Royceazimuth thrusters

Offshore drilling vessels

Petrobas needs over 30 newdrilling vessels

Singapore’s Sembcorp Marine’swholly-owned Brazilian shipyardEstaleiro Jurong Aracruz secured aUS$793 million contract fromGuarapari Drilling BV, Netherlands, asubsidiary of Sete Brasil Participacões

Austria-based Palfinger Dreggen has aUS$121 million contract to supply cranesto the Jurong Shipyard

Selected opportunities in the subsea exploration & production supply chain

Source: Mergers Alliance, company press releases

Servicing

Drilling vessels

A major offshore oil and gas frontier

Mer

gers

Allia

nce

2013

10

Brazil M&A update

Find out moreSpecialist advice on call…For information on Brazil

Leonardo AntunesManaging Director, BroadSpan CapitalLocation: Rio de Janeiro

Telephone: +55 21 2543 5409Email: [email protected]

Leonardo is Managing Director of BroadSpan.His experience covers a range of sectors includingpower, oil & gas, mining, technology and healthcare.He has executed over 30 advisory transactions with avalue in excess of US$10 billion and over US$5 billionin fund raising and project finance transactions.

Prior to joining BroadSpan, Leonardo was responsible forM&A, capital markets and project finance transactions inBanco Modal and Vice Preside Corporate Finance andStructured Finance for Latin America at ABN AMRO.

Languages spoken: English, Portuguese and Spanish

Michael GerrardManaging Director, BroadSpan CapitalLocation: Miami

Telephone: +1 (305) 424 3400Email: [email protected]

Michael is a founder and Managing Director of BroadSpanCapital. He has overseen a variety of M&A and restructuringassignments and taken an active role in the development ofBroadSpan Asset Management LLC, the firm's assetmanagement subsidiary.

Before founding BroadSpan, Michael headed the LatinAmerican Capital Markets division at Barclays Capital where hewas responsible for capital markets origination and executionfor a range of products. While with Barclays, Michael executedover US$3.5 billion of international capital markets financingsfor Latin American issuers.

Languages spoken: English, Portuguese and Spanish

Private equityinvestmentPrivate equity is an important driverof M&A in Brazil with deal volume overthe last ten years worth aroundUS$22 billion.

Both domestic and international PE arefocusing on companies benefiting fromthe growing spending power of themiddle class. For example, in 2012Brazil’s BTG Pactual acquired clothingretail store Leader Magazine forUS$274 million in 2012, US-basedCarlyle Group acquired furniture storeTok & Stok for US$348 million andUK-based 3i Group has recently led aconsortium which has acquired ÓticasCarol, Brazil’s second largest eyewearretailer, for US$54 million. Activity willcontinue to be strong in 2013.

Large foreign institutional investorsare also attracted to investmentopportunities. For example, OntarioTeachers’ Pension Plan holds a 12.5%stake in Brazilian iron-ore companyManabi Holding and Canada’s PublicSector Pension Investment Board hasacquired a stake in Isolux Infrastructurefor US$402 million.

Exit activity includes trade sales,secondary buyouts and initial publicoffering. Stratus Group, a Brazilianmid-market private equity investor,listed technology service providerSenior Solution in 2012 and car rentalcompany Locamerica, backed by theprivate equity arm of Banco Votorantim,floated in April 2012.

Private equity has asuccessful record

in Brazil

Mer

gers

Allia

nce

2013

11

Brazil M&A update

Date Target company Country Target Activities Acquirer Country Deal value(US$ mm)

Mar-13 E-Test Laboratorio de Ensaio (85% Stake) Brazil Toy testing and related services Intertek Group plc United Kingdom 10.3

Feb-13 Drogaria Onofre Ltda Brazil Distributor of healthcare and personal care products CVS Caremark Corporation USA NA

Jan-13 UAB Motors Participacoes S.A. Brazil Automotive retailer Group 1 Automotive, Inc. USA 207.5

Dec-12 Vivo Participacoes, S.A. (800 towers in Brazil) Brazil 800 free-standing, ground- based towers SBA CommunicationsCorporation

USA 176.8

Dec-12 Repom S.A. (62% Stake) Brazil Computer facilities management solutions for trucks Edenred SA France 69.8

Dec-12 Bunge Limited (Fertilizer Business in Brazil) Brazil Fertilizer business of Bunge Limited Yara International ASA Norway 750.0

Dec-12 XP Investimentos CCTVM SA (31% Stake) Brazil Brokerage and insurance house involved incorporate financial education

General Atlantic LLC USA 230.8

Nov-12 Orbus Pharma S.A.S.; Flores Ervas;ApodanNordic PharmaPackaging a/s

Brazil Supplies pharmaceutical extracts and tinctures Fagron BV Netherlands 26.0

Oct-12 Jari Celulose S.A. (Industrialpackaging assets) (75% Stake)

Brazil Containerboard mills and box plants ofJari Celulose S.A.

International Paper Company USA 596.0

Oct-12 Serasa S.A. (29.6% Stake) Brazil Credit, economic and financial analysis andinformation company

Experian Plc United Kingdon 1,500.0

Oct-12 Amil Participacoes SA (90% Stake) Brazil Health care services company UnitedHealth Group Inc USA 3,945.0

Sep-12 Kromav Engenharia Ltda. (50% Stake) Brazil Offshore oil and gas and marine engineering company Amec Plc United Kingdom 12.5

Sep-12 Carvajal Empaques S.A. (foldingcarton production plant in Brazil)

Brazil Folding carton producing plant ofCarvajal Empaques S.A.

Mayr Melnhof PackagingInternational GmbH

Austria 15

Sep-12 Tok & Stok Ltda. (60% Stake) Brazil Furniture retailer The Carlyle Group, LLC USA 346.5

Aug-12 Manabi Holding S.A. Brazil Iron ore exploration Ontario Teachers' Pension Plan;EIG Global Energy Partners

USA; Canada 301.1

Aug-12 Tortuga Companhia Zootecnica Agraria Brazil Agribusiness and providing animal feed Royal DSM N.V. Netherlands 575.1

Aug-12 ETEP Consultoria, Gerenciamento eServicos Ltda.

Brazil Water engineering and consultancy Arcadis NV Netherlands NA

Aug-12 Asseio Saneamento Ambiental Ltda. Brazil Pest control company Rentokil Initial Plc United Kingdom NA

Jul-12 Rubaiyat (70% Stake) Brazil Restaurant chain Mercapital, S.L. Spain 56.9

Jul-12 Grupo Posadas (South Americanhotels portfolio)

Brazil Hotel operator Accor SA France 275.0

Jul-12 Lamiflex do Brasil EquipamentosIndustriais Ltda (85% Stake)

Brazil Manufacturer and distributor of power transmissionequipments

Altra Industrial MotionNetherlands BV

Netherlands 8.5

Jul-12 Usina Fortaleza Industria eComercio de Massa Fina Ltda.

Brazil Manufacturer of materials andquality adhesives

Bostik, Inc. USA NA

Jul-12 Rheoset Industria e Comercio deAditivos Ltda.

Brazil Manufactures admixture concrete products W. R. Grace & Co. USA NA

Jul-12 Neogama | BBH Brazil Advertising agency Publicis Groupe SA France NA

Jul-12 CP Eletronica SA Brazil Manufactures power systems for data centers,hospitals, and businesses

Schneider Electric SA France NA

Jul-12 Isolux Infrastructure S.A. (undisclosed stake) Brazil Operates as a construction andengineering company

Public Sector PensionInvestment Board

Canada 754.5

Jun-12 Watercryl Quimica Ltda. Brazil Provides coatings solutions Elementis Plc United Kingdom 24.0

Jun-12 Folhamatic Tecnologia em Sistemas S.A.(75% Stake)

Brazil Provides accounting, tax and payroll and regulatorycontent software

The Sage Group Plc United Kingdom 196.8

May-12 Brasil Online Holdings (21% Stake) Brazil Provides online employment services SEEK Limited Australia 78.8

May-12 ACS Actividades de Construccion yServicios, S.A. (Seven electric power

Brazil Electric power transmission lines operated by ACSActividades de Construccion y Servicios, S.A.

State Grid Corporation of China China 942.2

May-12 Ypioca Agroindustrial (Ypioca brandand other production assets)

Brazil Ypioca brand and other production assetsof Ypioca Agroindustrial

Diageo Plc United Kingdom 454.6

May-12 Neodent (49% Stake) Brazil Manufactures dental implants and relatedprosthetic components

Straumann Holding AG Switzerland 275.3

Apr-12 Negocios nos Trilhos Participacoes Ltda Brazil Cargo and rail business tradeshow organizer United Business Media Limited United Kingdom NA

Apr-12 Telcon Fios E Cabos ParaTelecomunicacoes S/A (50% Stake)

Brazil Manufacturer of copper wires, and cables fortelecommunication, data and TV cabling markets

Prysmian Cables & Systems Italy 27.4

Temporary power supplierMar-12 Companha Brasileira de Locacoes Brazil Aggreko Plc United Kingdom 256.4

64.4Mar-12 Transbank; Nordeste Seguranca Brazil Security company specialising in cash in transit,guarding and technology

Prosegur Compania deSeguridad, S.A.

Spain

Figure 9: Selected M&A transactions

Source: Mergers Alliance, Captial IQ

Mer

gers

Allia

nce

2013

www.mergers-alliance.com

Mer

gers

Allia

nce

2013

BroadSpan and the Mergers Alliance partners are expertly placedto offer advice.In particular, we offer:

Advice on structuring and completing deals in Brazil

Identifying acquisition opportunities around the world

Information on sector trends and valuations

Access to corporate decision-makers and owners

Join in the mergers and acquisitions discussion

Australia

Austria

Belgium

Brazil

Bulgaria

Canada

China

Colombia

Czech Republic

Denmark

Finland

France

Germany

India

Italy

Japan

Luxembourg

Mexico

Netherlands

Norway

Poland

Russia

Singapore

South Africa

Spain

Sweden

Switzerland

Turkey

UK

USA

Mergers Alliance is a group of award-winning corporate finance specialistswho provide high quality advice to organisations who require reach fortheir International M&A strategies.

Global coverage

Leonardo AntunesManaging Director, Rio de Janeiro

Contact: +55 21 2543 [email protected]

Felipe MonacoDirector, São Paulo

Contact: +55 11 4114 [email protected]

Ricardo SirotskyManaging Director, Rio de Janeiro

Contact: +55 21 2543 [email protected]

Michael GerrardManaging Director, Miami

Contact: +1 (305) 424 [email protected]

Derek GalloDirector, São Paulo

Contact: +55 11 4114 [email protected]

Horacio Moreira Piedras JrDirector, Rio de Janeiro

Contact: +55 21 2543 [email protected]