©coursecollege.com 1 3 learning objectives 1. explain the concept of t-accounts and the accounting...

TRANSCRIPT

©CourseCollege.com

1

3Learning Objectives

1. Explain the concept of T-accounts and the accounting method for maintaining account balances using debits and credits

3. Describe the Chart of Accounts and its’ importance to the firm.

3. Describe the use of contra accounts.

4. Describe the separation of the 5 major types of accounts into two main categories, permanent accounts and temporary accounts.

5. Analysis: Explain and calculate a common size balance sheet

Unit 3

The Account

©CourseCollege.com

2

Objective 3.1:Debits, credits, T-accounts

These are the mechanics of maintaining account

balances. They are critical to understanding accounting

systems

O3.1

©CourseCollege.com

3

Every account has a left and a right side. Left is the debit and right is the

credit side.

Depending on where the account resides, the normal balance

will be a debitdebit or a creditcredit balance.

©CourseCollege.com

4

DEBIT side

CASH

For Example: Accounts can be

visualized as a T, with a left and right side

O3.1

CREDIT side

©CourseCollege.com

5

The normal balance depends on where the account resides(the account classification)

8 (bal)

ACCOUNTS PAYABLE

12 (bal)

CASH

ProfitDebit Credit or

Loss

Expenses

Equity

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Income

Blue areas are debit balances red areas are

credit balancesO3.1

©CourseCollege.com

6

The account classification indicates how an account is increased and

decreased

Accounts in blue areas are increased with debits accounts in red areas are

increased with credits O3.1

ProfitDebit Credit or

Loss

Expenses

Equity

BALANCE SHEET INCOME STATEMENTAssets Liabilities Revenue

+ - +

-

- + - +

- +

©CourseCollege.com

7

What is meant by normal balance?

8 (bal)

ACCOUNTS PAYABLE

12 (bal)

CASH

ProfitDebit Credit or

Loss

Expenses

Equity

BALANCE SHEET INCOME STATEMENT

Assets Liabilities Income

Answer: A positive balance.The $8 credit balance in Accounts Payable

tells us that $8 is owed to creditors for this account

O3.1

©CourseCollege.com

8

Why do you need to use left and right, debit and credit?

Answer: Using debits and credits simplifies accounting entries, reduces errors and mostimportantly insures that all changes madeto the accounting system keep the system

in balance.

DEBITS CREDITS

Total debits must always equal total

credits

O3.1

©CourseCollege.com

9

How do debits and credits work in an individual account?

1. Increase accounts by entering a normal balance entry, debit (left) or credit (right).

2. Decrease accounts by entering the opposite of a normal balance entry debit or credit.

3. At any point in time, the account balance is determined by whether there is an excess of debits or credits. Debits offset credits and visa versa, dollar for dollar. -See example on the following slide.

O3.1

©CourseCollege.com

10

150

6090

CASH

60

600

ACCOUNTS PAYABLE

In the transaction below:

•The cash account started with a $150 normal balance and accounts payable started with a $60 normal balance

•Cash is used to pay the accounts payable owed of $60 with a credit to Cash and a debit to Accounts Payable.

•The ending balances resulting in both accounts are shown.

•The change made to the accounting system involved equal debits and credits.

O3.1

©CourseCollege.com

11

Objective 3.2:Chart of accounts

The Chart of Accounts is the official list of all accounts

used by a firm. The Chart of Accounts is specially tailored

to the needs of each individual firm. (See sample

on next slide)O3.2

©CourseCollege.com

12

Chart of AccountsChung Supply

INCOME STATEMENTAssets Liabilities Revenue101 Cash 210 Accounts Payable 400 Merchandise Sales102 Petty Cash 216 Taxes Payable 410 Design Fees115 Accounts Receivable 218 Wages Payable 420 Consulting Fees116 Supplies 250 Equipment Loan117 Inventory 260 Mortgage Payable Expenses118 Prepaid Insurance 510 Cost of Goods Sold150 Store Fixtures 520 Wages Expense160 Land Equity 525 Payroll Tax Expense170 Building 300 M. Chung, Capital 528 Insurance Expense180 Equipment 310 M. Chung, Drawing 530 Supplies Expense

540 Miscellaneous Expens550 Interest Expense

ProfitDebit Credit or

Loss

BALANCE SHEET

This is the official list of accounts used by this

firm.

Notice the optional logical

numbering system

O3.2

©CourseCollege.com

13

Can accounts be removed or added to the Chart of Accounts?

Yes, whenever a new account is needed or an account is no longer needed, changescan be made to the Chart of Accounts

Controls should be in place within the firm to require proper approval to change the firm’s Chart of Accounts.

O3.2

©CourseCollege.com

14

Objective 3.3:Contra accounts

Contra accounts are “backward” accounts –their normal balances (debit or

credit) are the opposite of the normal balances of the

account(s) to which they are associated

O3.3

©CourseCollege.com

15

(4)

Net Equity 6

O3.3

A typical contra account is the Owner’s Drawing account.

Think of the contra account as a take away bucket hanging

under the regular

account to which it is attached.

ContraAccount

P. Wills, Drawing

P. Wills, Capital 10

©CourseCollege.com

16

Why are contra accounts necessary?

At times, it is important to accumulate separately all the reductions recorded to an account rather

than simply make the reductions directly

O3.3

This gives us additional information. For example,“Equity is $4,000” is not as informative as

“Equity started the year at $15,000, however$11,000 was withdrawn by the owner and

$4,000 remains”.

©CourseCollege.com

17

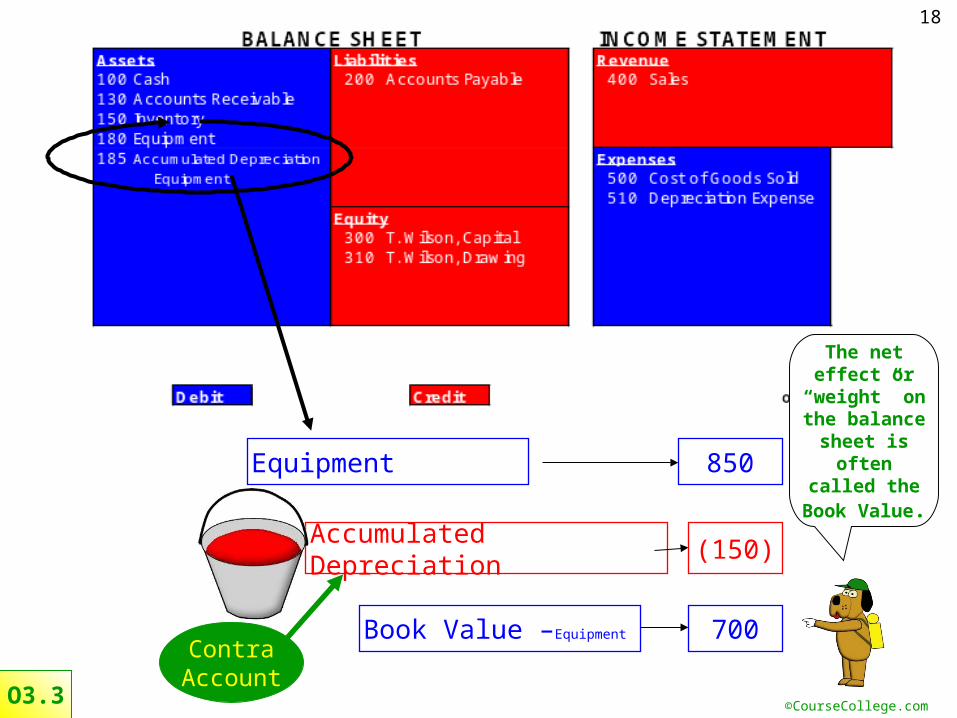

What is another contra account?

O3.3

Accumulated Depreciation is a contra account thatgathers all of the reductions in value recorded fordepreciable assets since their acquisition by the

firm.

©CourseCollege.com

18

O3.3

Accumulated Depreciation

(150)

Book Value –Equipment 700

Equipment 850

ContraAccount

The net effect or

“weight” on the balance

sheet is often called

the Book Value.

©CourseCollege.com

19

Objective 3.4:Permanent and Temporary

Accounts

In general, Balance Sheet accounts are permanent and Income Statement accounts

are temporary

O3.4

©CourseCollege.com

20

Remember the five broad classes of accounts,–Assets, Liabilities, Equity, Revenue and Expenses.

As such, the Income Statement accounts are considered temporary accounts and the Balance Sheet accounts* are considered permanent accounts. The income statement accounts are considered temporary because they are

regularly closed (every fiscal period).

Closing an account sets the balances back to zero and causes the net effect of these accounts to be formally updated (moved)

to the equity accounts.

O3.4

Also remember that revenue and expenses are temporary accumulations of

eventual changes to the equity account.

©CourseCollege.com

21

ProfitDebit Credit or

Loss

Expenses

Equity

BALANCE SHEET INCOME STATEMENTAssets Liabilities Revenue

TEMPORARY ACCOUNTS

PERMANENT ACCOUNTS

All the activity from income and expenses is summarized in profit or loss. Closing the temporary income statement accounts will

formally bring this result to the equity section.

O3.4

©CourseCollege.com

22

Objective 3.5:Common size Balance

Sheet

By expressing individual items on a balance sheet in terms of their percentage of

total assets, valuable additional information is

obtained

O3.5

©CourseCollege.com

23

Assets % Liabilities %

Cash 150 20.4% Accounts Payable 225 30.5%

Accounts Receiv. 322 43.7%

Inventory 190 25.8% EquityEquipment 75 10.2% Owner, Capital 512 69.5%

Total assets 737 100.0% Total liab & equity 737 100.0%

Balance SheetAs of 12/31/08

(Common Size)

For Example: This is calculated as 75/737 = 10.2%

With common size percentages, balance sheet items can be

compared from one period to the next and from one firm to the

next.

©CourseCollege.com

24

End of Unit 3