covered bond & ssa view - nord/lb · 11/2/2016 · covered bond & ssa view ... over the...

TRANSCRIPT

Please see important disclosure on the last pages.

2

Agenda Page

Market overview 2

Aaa rating awarded to Danish pool of Stadshypotek 5

Fitch publishes new rating methodology 7

NRW breaks its own benchmark maturity record 8

ECB tracker 11

Charts & Graphs 16

Publication overview 22

Contacts 23

Find us on Bloomberg: NRDR <GO>

Issue volume – Covereds Issue volume – SSA

0

5

10

15

20

25

30

11

/15

12

/15

01

/16

02

/16

03

/16

04

/16

05

/16

06

/16

07

/16

08

/16

09

/16

10

/16

EU

Rbn

AUBECACHCYCZDEDKESFIFRGBGRHUIEITLUNLNONZPLPTSESGTR

0

5

10

15

20

25

30

12

/15

01

/16

02

/16

03

/16

04

/16

05

/16

06

/16

07

/16

08

/16

09

/16

10

/16

11

/16

EU

Rb

n

Other

ES

AT

NL

FR

GE

SNAT

Source: Bloomberg, NORD/LB Fixed Income Research Source: Bloomberg, NORD/LB Fixed Income Research

Fixed Income Research

Covered Bond & SSA View 2 November 2016 43/2016

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 2 of 27

Covered Bonds Market overview

Analyst:

Kai Ebeling, CIIA

BRFkredit successfully

issues its third EUR

benchmark

Over the past five trading days, just one issuer offered its investors a euro-

denominated covered bond in benchmark format. After only issuing its inaugu-

ral bond in the euro benchmark segment earlier in the current financial year,

the Danish BRFkredit placed its third euro-denominated benchmark in 2016

on Thursday and therefore successfully completed the formation of its covered

curve. The issuer opted for a maturity of almost ten years and placed a total of

EUR 750m on the market, matching the volume of its preceding bond. With a

bid-to-cover ratio of 1.53, the bond was well-received by investors, as a result

of which the initial spread level was reduced from the guidance of ms +10bp

area to a reoffer spread of ms +8bp. At the start of the week, Caja Rural de

Navarra mandated various banks for carrying out roadshows to market a euro-

denominated green covered bond (cédula hipotecaria) with a medium maturi-

ty. The roadshow is planned for between 4 and 11 November.

Banca Popolare Emilia Issuer Country Timing ISIN Maturity Volume Spread Rating

BRFkredit DK 27.10.16 XS1514010310 9.9y € 0.75bn ms +8bp - / - / AAA

Source: Bloomberg, NORD/LB Fixed Income Research (Rating: Fitch / Moody’s / S&P)

UBS gains approval for

conversion to soft bullet

Last week, UBS gained approval from its investors to convert the structures of

some of its covered bonds from hard bullet to soft bullet. Among them are two

euro benchmark bonds included in the iBoxx EUR Covered (UBS 3 ⅞

12/02/19 and UBS 4 04/08/22). As a result, all covered bonds from Switzer-

land in the iBoxx will now feature soft bullet structures. In the case of UBS, this

changes the repayment following the activation of the defined trigger event by

up to 12 months, with the interest for this period being based on the one-

month Euribor plus a spread.

S&P has so far not carried

out any downgrades this

year

S&P recently published its Global Covered Bond Characteristics and Rating

Summary for the third quarter. In the report, the rating agency states that it

has so far not downgraded any of the covered bond programmes it rates in the

current financial year. Given the positive, albeit slow, economic growth in the

eurozone as well as the stable outlook for the majority of issuers and sover-

eigns, S&P is also anticipating that covered bonds ratings will continue to be

stable in 2017 as well. However, rating volatility for the evaluated programmes

could arise in the wake of political uncertainty or because of the susceptibility

of some banks in western Europe. The agency does not anticipate that the

revision of criteria for assessing pools of residential loans lending in Austria,

Belgium, Denmark, France, Germany and Sweden will impact the existing

ratings.

Trader’s Comment At the start of the week, market makers were almost exclusively offering bid

prices, which in turn cheapened outstanding bonds. However, this does not

appear to represent a major sell-off, but rather constant pressure that is caus-

ing spreads to widen slightly overall. Spread widening on the secondary mar-

ket has been significantly greater during such phases in the past. The slower

rate of widening now could be attributable to the only limited trading stock

levels.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 3 of 27

SSA Market overview

Analyst:

Norman Rudschuck, CIIA

Green light for Greece

The European Stability Mechanism gave the official green light for the pay-

ment of EUR 2.8bn last week. The decision is a sign that Greece is making

steady progress with its reforms, said ESM boss Klaus Regling. If the country

continues on this course, Greek economic growth will firm next year. The

tranche was linked to compliance with 15 required reforms, which led to EUR

1.1bn being released a few weeks ago. The Greek prime minister Alexis

Tsipras recently demanded a further reduction in Athens’ debt mountain. This

is of course familiar to regular readers. Even more, he is planning a govern-

ment reshuffle to demonstrate his willingness to reform according to govern-

ment insiders and Greek media.

Union faction brings the IMF

into play once more

“The Chancellor, the Minister of Finance and I have promised the faction that

the International Monetary Fund will be involved and that’s an end to it”, said

Volker Kauder. New billions for Hellas would accordingly only be released if

the IMF was involved. As long as the IMF was not on board, no additional

financial aid would be approved. The Minister of Finance was also aware of

this, he emphasised. However, other politicians in the Union faction expected

another rescue package. The dispute between the IMF and Schäuble regard-

ing aid for Greece therefore continues to smoulder.

ESM a topical issue –

voluntarily…

Kalin Anev Janse has announced that the EFSF funding for 2016 is complete.

The ESM will reach the targets it has set in November. While the prospect of

the first transaction in USD has already been held out for 2017, the funding

volume even seems to be increasing to up to EUR 50bn. Of this figure, EUR

13bn is to be issued in bills. N-bonds (private placements) will also play a

certain role again next year. The reference to the fact that the ECB’s quantita-

tive easing means that the stabilisation funds can issue bonds with negative

yields up to nine-year maturities is of interest. This remains to be seen in fu-

ture; yields have risen since then across a broad front – as is well known.

…and involuntarily Wolfgang Schäuble has wandered onto the political stage. It must therefore

be assumed that he sensed the significance of his suggestion when he de-

clared that the European Stability Mechanism should be more heavily involved

in budgetary control in the Eurozone. Schäuble is quoted as “thinking of

whether the ESM crisis fund could not gradually be developed more in this

direction”. According to his reasoning, the ESM would not assess the draft

budgets politically but strictly in accordance with the rules. The German Minis-

ter of Finance sees the necessity for differentiating the tasks of the EU Com-

mission more sharply from each other. However, a stronger political leader-

ship role for the Commission would conflict with its neutral role as guardian of

the Treaties. He again argued his position last week at a conference in Brati-

slava. A budget monitoring role as part of the stability pact is inappropriate for

the EU Commission. By contrast EU Commissioner for Economic and Finan-

cial Affairs Pierre Moscovici insisted that the Commission remains in the lead,

as it has a democratic mandate for this. The Commission will be even better

equipped for these tasks if it has a Fiscal Council at its side to provide advice,

which is to be established shortly.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 4 of 27

NRW.BANK: strong demand

for loans with long terms

In the first nine months, NRWBK provided funds of around EUR 7.8bn and

consequently increased its net new commitments by 11% (2015: EUR 7.0bn).

Of this figure, EUR 4.6bn was attributable to the “Housing & Living” field of

development and promotion, EUR 2.2bn to “Seed & Growth” and just under

EUR 1.0bn to “Development & Protection”. Demand was particularly strong, at

EUR 994.9m for its NRW.Bank.Universalkredit standardised credit programme

(2015: EUR 706.3m, +41%). According to Klaus Neuhaus, Chairman of the

Managing Board of NRW.BANK, the fact that programmes offering long terms

are particularly popular in periods of low interest rates proved to be true here.

Spanish stalemate ended The Spanish government was only in office on caretaking basis for more than

300 days but Mariano Rajoy has now officially managed to be re-elected or

tolerated. The political blockade is now finally over, as he was unable to push

through any laws, appoint anybody as minister or start any initiatives. Howev-

er, Rajoy is not going to have an easy time of it henceforth either, as he leads

a tolerated minority government. Not only the socialists but also the sepa-

ratists or proponents of secession will make life difficult for him. However, this

election is not a reason for the current rise in yields.

Primary market The federal state of NRW ventured onto the market with a new 30-year issue

last week, raising EUR 1bn at ms +18bp. This bond therefore qualifies directly

for the ECB’s PSPP and offers new opportunities at the long end. The EFSF

also put forward a tap of EUR 2bn (2026) on 26.10. RESFER also started the

IPT for a 15-year green bond on that date. This was priced as early as the

following day (ms +20bp) and amounted to EUR 900m. Meanwhile, Schles-

wig-Holstein chose banks for an eight-year benchmark, for which the most

northern Bundesland had to pay ms -20bp. Experience tells us that there will

be little activity on the primary market this week because Tuesday was a pub-

lic holiday (All Saints) in half of Europe. Many people took Monday as a bridg-

ing day. Nevertheless, two bonds (2024 and 2036) were tapped by EUR 250m

in the less catholic states of Lower Saxony and Berlin.

Issuer Country Timing ISIN Maturity Volume Spread Rating

SCHHOL GE 27.10.2016 DE000SHFM550 8.0y 0.50bn -20bp AAAe / - / -

RESFER FR 27.10.2016 XS1514051694 15.0y 0.90bn 20bp AAe / Aa2e / -

NRW GE 26.10.2016 DE000NRW0J22 29.9y 1.00bn 18bp AAAe / Aa1e / -

Source: Bloomberg, NORD/LB Fixed Income Research (Rating: Fitch/Moody’s/S&P)

Trader’s Comment On the primary market, EUR 1bn NRW 10/46 was issued at ms +18 and EUR

500m Schleswig-Holstein 11/24 at ms -20. Both bonds were well received by

the market. In the secondary market, clients increasingly requested bid prices,

even in smaller amounts. Demand from the ECB’s purchase programme fell

slightly. Spreads were stable.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 5 of 27

Covered bonds Aaa rating awarded to Danish pool of Stadshypotek

Analyst:

Kai Ebeling, CIIA

Stadshypotek already has

three cover pools

In its pre-sale report this past week, Moody’s assigned a provisional rating of

Aaa to the Danish cover pool of the Swedish Stadshypotek. So far this year,

Stadshypotek has already issued three euro-denominated covered bonds in

benchmark format, with the most recent bond being backed by the new Finn-

ish cover pool (SHBASS 0 ⅛ 10/05/26). We are taking this opportunity to more

closely examine the provisional Danish pool and compare it against the issu-

er’s other previously created cover pools.

Stadshypotek – Danish cover pool (provisional) Spread landscape – Sweden

Oustanding volume DKK 6,608.5m

-20

-15

-10

-5

0

5

10

0 2 4 6 8 10

AS

W i

n b

p

maturity

SHBASS LANSBK SEB SBAB SE

Cover pool volume DKK 6,000.0m

Overcollateralisation (committed) 2.0%

Main collateral type 100% Residential

Country 100% Denmark

Number of borrowers

3,548

Avg. exposure to borrower DKK 1,862,596

WA current LTV (Cover Pool) 65.8%

WA remaining term (Cover pool) 19.9y

CB Rating (Fitch / Moody’s / S&P) - / Aaa / -

Source: Issuer, NORD/LB Fixed Income Research Source: Bloomberg, NORD/LB Fixed Income Research

Composition of the cover

pool

According to Moody’s pre-sale report, the total value of collateral in Stadshy-

potek’s provisional cover pool is DKK 6.6bn (approximately EUR 888m; as at

reference date of 31 March 2016). This volume is made up of residential as-

sets that originate in Denmark, with 90.9% attributable to single-family houses

and 9.1% to apartments. The majority of loans are located in the Hovedstaden

region (50.6%), which also includes Copenhagen, followed by Midtjylland

(29.3%) and Syddanmark (10.2%). With around 3,548 debtors at present, the

average loan amount per borrower stands at DKK 1,862,596 (approximately

EUR 250,389). The issuer guarantees an overcollateralisation ratio of 2.0%,

which corresponds to the legally required level. In order to obtain the provi-

sional rating of Aaa, Moody’s rating methodology currently obliges the issuer

to sustain an overcollateralisation ratio of 0.0%. The average loan-to-value

(LTV) amounted to 65.8% as at the reporting date. In accordance with Swe-

dish covered bond law, residential securities and multi-family houses can ac-

count for an LTV of up to 75% of the cover pool volume. Moody’s rates the

credit quality of the assets through a collateral score, which is 9.0% for this

cover pool. As at the end of the first quarter of the year, the average collateral

score of all mortgage-backed programmes rated by Moody’s was 12.4%,

meaning that the collateral score of the Danish cover pool is above-average

by comparison. The timely payment indicator (TPI) assigned by Moody’s is

“Probable-High” and, on this basis, the TPI leeway is six notches. Potential

covered bonds therefore have a comfortable buffer against the downgrade of

the CB anchor or CR Assessment.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 6 of 27

Comparison of Stadshypotek’s cover pools

Danish

cover pool

Finnish

cover pool

Swedish

cover pool

Norwegian

cover pool

Covered bond

rating

(S&P/M/F)

-/(P)Aaa/- -/Aaa/- -/Aaa/- -/Aaa/-

Outstanding

volume EUR 0.0m EUR 500m EUR 55,715,4m EUR 2,990,4m

Cover pool

volume EUR 888.4m EUR 550.0m EUR 62,891.9m EUR 3,279.2m

OC

(committed/

current)

2.0%/ n/a 2.0%/10.0% 2.0%/12.9% 2.0%/

9.7%

Main

country 100% Denmark 100% Finland 100% Sweden

100%

Norway

Main region 50.6% Hovedsta-

den 50.2% Uusimaa

40.7% Greater

Stockholm 57.6% Östlandet

Aver. loan size EUR 232,809 EUR 86,200 EUR 65,050 EUR 404,696

Fixed interest

rate (cover pool/

CBs)

69.7%/

n/a

0%/

100%

54.2%/

92.4%

99.9%/

100.0%

Collateral score 9.0% 5.2% 5.0% 6.5%

Source: Issuer, Moody’s, NORD/LB Fixed Income Research

Comparison of various

cover pools

The greatest pool by far comprises Swedish collateral, with the issuer also

placing covered bonds through its Finnish and Norwegian programmes. An

overcollateralisation ratio of at least 2.0% is guaranteed for every pool on a

contractual basis, equating to the legal minimum requirement. The nominal

overcollateralisation for the three established pools is currently in a narrow

range of between 9.7% and 12.9%. In terms of geographic distribution, more

than 50% of the cover assets in the Danish, Finnish and Norwegian pools are

concentrated on one region in the respective country, which is in each case

the most populous region in the corresponding jurisdiction. By comparison

with the other cover pools, the collateral score of the Danish pool is slightly

higher, which generally implies that the credit quality of the securities is lower.

However, a cross-jurisdiction comparison is only to a limited extent meaningful

because the collateral score for the mortgage-backed programme also takes

into account the systemic risk. Alongside the Stadshypotek programme, in

Denmark Moody’s also rates the cover pools of Nordea Kredit (capital centre 1

and 2), which have higher collateral scores of 10.7% and 13.6%.

Conclusion With the Danish cover pool, Stadshypotek now has four cover pools. This

offers investors the opportunity to specifically invest in covered bonds backed

by the respective cover pool while at the same time evading the risks of other

jurisdictions. Despite enquiring with the issuer, neither the currency nor the

volume or timing of a potential issue have so far been determined. The cover

pool examined above is therefore only provisional and its composition could

still be subject to change. When compared with the outstanding bonds of

Stadshypotek, we expect that the spread level of a potential EUR benchmark

from the Danish pool would be insignificant higher on account of the marginal-

ly greater collateral score.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 7 of 27

Covered bonds Fitch publishes new rating methodology

Analyst:

Kai Ebeling, CIIA

Fitch concludes revision of

rating methodology

Last week, Fitch concluded the final revision of its rating criteria for covered

bonds. The first exposure draft was published in June of this year and the

agency has now adopted these criteria with a few adjustments, which will be

explored in greater detail in the following article. In addition, we will discuss

the various rating changes that have resulted from the implementation of the

adjusted methodology.

Most issuers benefit from a

higher IDR uplift

When compared with the draft of the new rating criteria that was published on

29 June 2016, Fitch has amended how an issuer default rating (IDR) uplift is

assigned as well as removing the precise definition of significant exposure

from recoveries that are denominated in a foreign currency. With regard to

ascertaining the IDR uplift, Fitch has abolished the initially set threshold value

for a minimum balance sheet total of EUR 5bn for smaller institutions and

changed its position as regards specialised covered bond issuers. A total of 72

programmes will be allocated an IDR uplift of two notches according to the

new criteria, while this was only granted to 34 programmes under the old

methodology.

Potential upgrades prevail

under the new methodology

According to Fitch’s estimate, these amendments could lead to a rating

change for 29 of the 132 programmes it rates, whereby 23 programmes would

be upgraded and 6 would be downgraded, provided that the current overcol-

lateralisation ratio of the respective issuers is not at the same time adjusted.

The upgrades are likely to affect issuers from the euro periphery as well as

from Norway and the UK, insofar as they have not yet been assigned an AAA

rating.

Soft bullet structures result

in a PCU of six notches

In relation to the repayment structure being used, soft bullet programmes par-

ticularly benefit from the implementation of the payment continuity uplift

(PCU). This grants the corresponding programmes an uplift of six notches on

condition that an extension option of 12 months or longer has been chosen,

which is the case for all programmes that are included in the iBoxx EUR Cov-

ered. Under the D-Cap, an uplift of only four notches had been assigned.

Rating criteria will be

implemented gradually

Fitch intends to have introduced the new rating criteria for all programmes

within the next six months, with implementation planned at jurisdiction level to

ensure it comes into effect gradually. The six issuers whose programmes will

potentially be downgraded because of the new methodology will be given the

opportunity by Fitch to improve their overcollateralisation ratio beforehand so

as to avoid being downgraded.

Conclusion The implementation of the updated rating methodology will not only lead to the

aforementioned potential upgrades and downgrades, but at the same time

reduce the overcollateralisation obligations for programmes, which, according

to Fitch, will above all apply to programmes from Portuguese and Spanish

issuers. Given the higher number of programmes that have i) a greater IDR

uplift or ii) a higher PCU on account of the soft bullet structure, the overall

stability of the covered bond ratings is likely to increase further, which means

that fewer rating amendments can be expected in the future.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 8 of 27

SSAs NRW breaks its own benchmark maturity record

Analyst:

Norman Rudschuck, CIIA

Record after record

While Rentenbank, KommuneKredit and, in particular, Austria have carried

out record-breaking transactions with their 70-year long-term bonds, North

Rhine-Westphalia would scarcely have attracted attention. Last week, the

most populous Bundesland in Germany raised EUR 1bn. It did this with a

30-year maturity. The previous record in benchmark format was, according

to relevant sources, 20 years (DE000NRW0JJ8). However, during our anal-

ysis, we identified a 25-year bond (DE000NRW0JV3), which (more than)

meets the traditional benchmark definition, at EUR 1bn. The fact that all

three long-term bonds were issued in 2016 and that NRW has consequently

secured historically low interest rates for decades is also of interest. An addi-

tional benchmark bond, which was issued with a 15-year maturity in July this

year, should also be mentioned in this context. There are also six further

EUR bonds outstanding, which firstly do not mature until after 2046 but sec-

ondly do not each in their own right even comprise an outstanding volume of

EUR 100m. Four of the bonds are also callable. We look at NRW as an is-

suer as well as the 2015 budget and the economy in the rest of the article.

NRW: the Bundesland With 17.6m inhabitants, North Rhine-Westphalia (NRW) is the most popu-

lous Bundesland in Germany. Given its area of just under 34,098 sq km, it is

the most densely populated of all the non-city federal states. At the end of

2015, the population was about 45,000 higher than a year previously. The

increase resulted from the positive balance in migratory movements: just

over 75,000 more people moved to NRW than left the Bundesland over the

same period. Approximately 755,000 companies from a vast range of sec-

tors are based in NRW, ensuring that the state’s economy is broadly based.

The federal state of NRW is also a very popular destination for foreign direct

investment, not least because of its strong economy and its well-developed

transport infrastructure. At the same time, the economy (in particular, in the

Ruhr region) has been subject to considerable structural change for dec-

ades: the proportion of gross value added attributable to manufacturing in-

dustry has fallen more sharply in NRW, at -8.4%, than in any other Land

since 1991. In contrast, the services sector’s share of the state’s gross value

added has increased. NRW has always generated a large part of national

economic output. With a GDP of EUR 645.6bn in 2015, 19.6% of German

economic output was generated in NRW. In price-adjusted terms, GDP fell

minimally by 0.01% Y/Y (Germany: +1.6% Y/Y), after the economy had in-

creased by 1.3% Y/Y in real terms (Germany: +1.6% Y/Y) in the previous

year. In 2015, NRW once again succeeded in reducing its cash deficit signif-

icantly: having stood at EUR 5.7bn in 2009, it was reduced to EUR 0.7bn in

2015. However, this figure remains the highest deficit recorded in the Bun-

desländer. Having largely been a payer in the financial equalisation system

between the federal states until 2009 (Länderfinanzausgleich, LFA), NRW

has been a consistent recipient since 2010. However, NRW still remains a

net payer in the total federal financial equalisation system.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 9 of 27

Yields of selected eurozone states (in %)

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 >2026

Foreign currencies 0 2.516 1.925 2.194 916 794 46 29 237 454 35 556

EUR other 10 110 153 56 35 0 10 80 25 175 0 1.326

EUR floating 815 2.285 2.645 1.505 4.394 929 1.065 50 1.200 750 40 772

EUR fixed 135 10.547 7.288 6.070 4.499 6.480 5.911 6.627 2.568 4.787 2.721 8.844

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000E

UR

m

Foreign currencies are converted into EUR at rates as at 1 November 2016. Source: Bloomberg, NORD/LB Fixed Income Research

Budget figures 2015 In 2015, NRW again recorded the highest deficit in absolute terms in Ger-

many (EUR 684.4m). However, the reduction of EUR 1.2bn in the deficit

meant that NRW achieved a much more significant improvement year-on-

year than any other Bundesland. Nevertheless, NRW is one of the five Bun-

desländer, which have never balanced their budget in the past ten years. Up

6.2% on 2014, the increase in total income was well above average (Bun-

desländer average: 4.7%), which also applied to tax revenue growth (+7.4%

vs. 2014). Income from the financial equalisation system rose to almost EUR

1.5bn, which meant that it represented a total of 2.3% of the budget. Alt-

hough NRW has remained a net payer in the federal financial equalisation

scheme, the total charge of EUR 0.6bn was significantly lower than in previ-

ous years (2013: EUR 1.3bn). On the expenses side, growth of 4.0% was

posted, which was primarily attributable to grants to municipalities (+9.8%

vs. 2014) that accounted for a good quarter of the budget. Hesse was the

only non-city state where these expenses rose more rapidly in the past five

years than in NRW. Personnel expenses grew by only 2.2% in 2015, repre-

senting much lower growth than in previous years (2014: +4.1% vs. 2013). A

total of 36.7% of the budget was spent on this item. Capital expenditure was

at a relatively stable level (8.3% of the budget) whereas interest expenditure

fell sharply by 7.0%, with the result that they accounted for 5.2% of the

budget. Overall, total debt fell by EUR 0.4bn to EUR 139.7bn in 2015, which

means that a net debt repayment was achieved for the first time since 2008.

The Land also forecasts its first positive budget balance for 2019. According

to NRW’s financial planning, the surplus will then be used to discharge debt.

In view of progress made with regard to reducing the portfolio, we now as-

sess the budgetary risk resulting from the loss offsetting obligation to the

EAA as lower. However, the EAA continues to represent a significant risk to

NRW’s budget, in our opinion.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 10 of 27

View of the rating agencies Bonds issued by NRW are rated AAA/Aa1/AA- by the three rating agencies

Fitch, Moody’s and S&P. Fitch justifies its rating on the basis of the principle

of federal loyalty and the federal financial equalisation system, which means

its puts the rating on the same level as that of the federal government. While

Moody’s also views its significance as the largest economic region and most

populous Bundesland positively, it rates NRW’s substantial debt negatively.

S&P also highlights the improvement in the budget situation but views the

substantial debt in relation to tax revenue, the limited budget flexibility and

contingent liabilities resulting from the winding-up agency Erste Abwicklung-

sanstalt (EAA) negatively. The rating agency also views the implicit pension

liabilities as a weakness. S&P assumes that the federal state will achieve a

balanced budget by 2020, although no net debt repayments are expected

until then.

Economy 2015 Goods and services worth around EUR 646bn were produced in North

Rhine-Westphalia in 2015. GDP was therefore at the 2014 level on a price-

adjusted basis. Economic growth of 1.7% was recorded in Germany as a

whole in 2015. NRW’s economic growth has therefore fallen to last place

among the sixteen Bundesländer last year. In nominal terms, GDP rose by

2.0% to a total of EUR 645.6bn, with the average for Germany at 3.8%.

Manufacturing industry saw a decline in economic output (-2.1%). The fed-

eral average posted growth of 1.7% for this metric. Although the service

sector was up slightly (+0.1%), growth here too was below average growth

in Germany (+1.5%). The number of persons in employment was around

9.18 million as an annual average for 2015. This means that 64,200 more

persons (+0.7%) were in employment compared to a year previously. The

average of all the Bundesländer shows an increase of 0.8% in the number of

persons in employment. In NRW’s manufacturing industry, the number of

persons in employment went down by 11,000 (-0.5%) to 2.1 million in 2015.

In the service sector, the number of persons in employment grew by 74,400

(+1.1%) to 7 million. The Netherlands was again the most important trading

partner in 2015. The North Rhine-Westphalian economy exported goods

worth almost EUR 18.3bn to the Netherlands, followed by France (EUR

15.5bn) and the UK (EUR 13.9bn).

Conclusion We view NRW as a core investment within a Bundesländer portfolio. We rate

its strong and well-diversified economy, which accounts for a large part of

German economic output, as a relative strength. We also view the budgetary

performance in recent years positively, as the deficit has been significantly

reduced. However, we rate the long history of deficits combined with below

average debt sustainability and interest coverage as weaknesses compared

with other Bundesländer. From our perspective, the EAA still poses a poten-

tial risk factor for the state’s budget. The pension liabilities, which we con-

sider high compared with other Bundesländer, as well as the relatively high

levels of municipal debt are other factors that could put pressure on the

budget over the next few years.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 11 of 27

Covered Bonds/SSA ECB tracker

Analysts:

Kai Ebeling, CIIA

Norman Rudschuck, CIIA

In this section, we publish weekly updates on the covered bonds, ABS, spe-

cific agencies, supranationals and sovereign bonds which the European Cen-

tral Bank (ECB) is purchasing. We provide an overview of the development of

purchases.

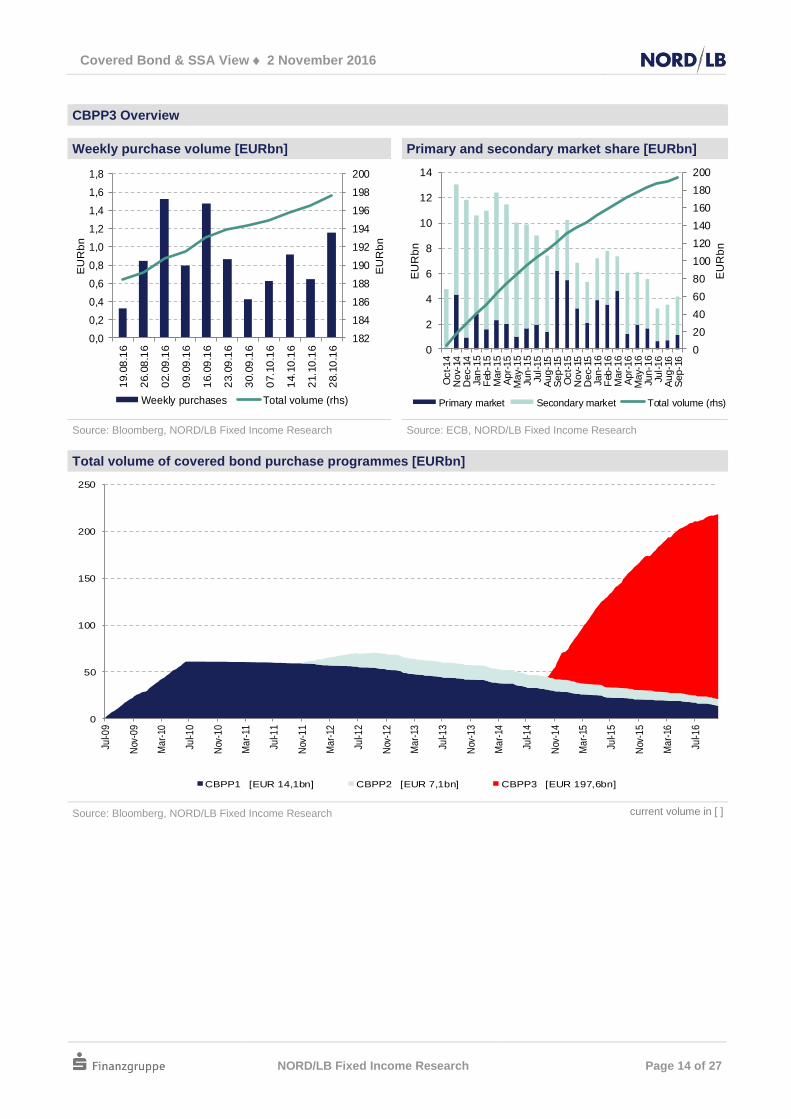

CBPP3 holdings achieve a

volume of EUR 197.646bn

As at the reference date of 28 October, the ECB reported a portfolio volume

totalling EUR 197.646bn purchased so far as part of the CBPP3. Holdings

have therefore risen by EUR 1.156bn in comparison to the previous week

(21 October: EUR 0.649bn). This development also precipitated a rise in net

inflows in the past four weeks to EUR 3.342bn (21 October: EUR 2.616bn). In

the past reporting period, net inflows consisted exclusively of purchases, with

no maturities falling due. In terms of the ABSPP, net inflows totalling EUR

184m were recorded in the central bank portfolio over the past reporting week,

meaning that the overall volume rose to EUR 21.467bn. The net inflows con-

sisted of purchases of EUR 0.6bn and maturities of EUR 0.4bn. On account of

basis effects, the volume for the rolling four week period fell to EUR 795m (21

October: EUR 1,018m). In comparison with the previous week, the volume of

the Corporate Sector Purchase Programme increased to EUR 1.929bn, bring-

ing the overall volume to EUR 37.815bn.

Weekly PSPP purchases

amount to EUR 17.2bn

As at the reference date of 28 October, the ECB reported a portfolio volume

totalling EUR 1,131.137bn purchased so far as part of the PSPP. In compari-

son with the previous week, the overall value of purchased bonds rose by an

above-average EUR 17.2bn. The average value since the programme expan-

sion to EUR 80bn per month is again EUR 16.0bn. In the previous period un-

der review, only a handful of newcomers were included on the SSA shopping

list: In the agencies segment – as was the case in the previous week – one

ISIN from RENTEN found its way into the Eurosystem’s books. The number of

RENTEN ISINs has therefore risen to 18. We watch with great interest for new

regional bonds: BRABUR and NRW (one bond each) were additions to this

segment. The overall number of German Bundesländer ISINs now amounts to

69. In addition, there are 17 bonds from the rest of the eurozone. For its re-

verse auctions on Friday, BDF’s plans are centred on two bonds each from

the EFSF and ESM. Four maturities of up to 10 years will be targeted.

Upcoming reverse auctions (Banque de France – BDF)

ISIN Bond Central bank & date

EFSF 1 1/2 01/22/20 EU000A1G0A81 Banque de France (04.11)

EFSF 0.4 05/31/26 EU000A1G0DH5 Banque de France (04.11.)

ESM 0 10/18/22 EU000A1U9985 Banque de France (04.11.)

ESM 1 09/23/25 EU000A1U9894 Banque de France (04.11.)

Total targeted size: EUR 150-250m Source: BDF, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 12 of 27

Completed reverse auctions (DeNederlandscheBank – DNB)

ISIN Bond Min. Mean Max Date

XS1022812330 NEDWBK 1 ⅛ 01/28/19 N/A N/A N/A 31.10.

XS1046410830 BNG 1 03/19/19 N/A N/A N/A 31.10.

XS0789996245 BNG 1 ⅞ 06/06/19 105.8100 105.8100 105.8100 31.10.

XS0820548716 NEDWBK 1 ⅝ 08/23/19 N/A N/A N/A 31.10.

XS0478263816 BNG 3 ¾ 01/14/20 113.1200 113.1200 113.1200 31.10.

XS0951381523 NEDWBK 1 ¾ 07/09/20 107.5500 107.5510 107.5600 31.10.

XS0537711144 BNG 2 ⅝ 09/01/20 N/A N/A N/A 31.10.

XS1315077476 BNG 0 ⅛ 11/03/20 101.5500 101.5500 101.5500 31.10.

XS1361603209 NEDWBK 0.05 02/10/21 101.2300 101.2300 101.2300 31.10.

XS0695263730 BNG 3 10/25/21 N/A N/A N/A 31.10.

Total Amount Offered EUR 90m

Total Amount Allocated EUR 50m

Source: DNB, NORD/LB Fixed Income Research

ECB purchase list for PSPP – regional issuers

Issuer Jurisdiction ISINs already purchased

BADWUR GE 3

BAYERN GE -

BERGER GE 10

BREMEN GE 5

BRABUR GE 3

HESSEN GE 10

HAMBRG GE 2

NIESA GE 4

MECVOR GE -

NRW GE 23

RHIPAL GE 4

SAARLD GE -

SCHHOL GE -

SAXONY GE -

SACHAN GE -

THRGN GE -

LAENDER GE 5

IDF FR 2

VDP FR 1

MADRID ES 6

CASTIL ES 1

BASQUE ES 1

ARAGON ES 1

WALLOO BE 2

FLEMSH BE 2

LCFB BE 1

Source: ECB, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 13 of 27

ECB purchase list for PSPP

Issuer Jurisdiction ISINs already purchased

EIB SNAT 53

EFSF SNAT 32

ESM SNAT 15

EU SNAT 20

COE SNAT 7

NIB SNAT 1

EURAT SNAT -

KFW DE 40

RENTEN DE 18

NRWBK DE 25

LBANK DE 6

CADES FR 18

RESFER FR 14

UNEDIC FR 17

AGFRNC FR 14

OSEOFI FR 11

CDCEPS FR 3

CNA FR 2

ACOSS FR -

BNG NL 23

NEDWBK NL 18

NEDFIN NL 2

OBND AT 8

ASFING AT 8

FINNVE FI 4

TVRFIN FI 2

ICO ES 9

ADIFAL ES 3

CDEP IT 3

IP (REFER / ESTPOR) PT -

SEDABI SI 1

DARSDD SI -

FADE ES 4

KUNTA FI 1

PARPUB PT 1

CASDEL IT -

AFLBNK FR 2

APHP FR -

GDCHU FR -

SPABSS FR -

HSGFIN IE -

FRBRTC BE -

SOCWAL BE -

FONWAL BE -

SWLBEL BE -

Source: ECB, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 14 of 27

CBPP3 Overview

Weekly purchase volume [EURbn] Primary and secondary market share [EURbn]

182

184

186

188

190

192

194

196

198

200

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

19.0

8.1

6

26.0

8.1

6

02.0

9.1

6

09.0

9.1

6

16.0

9.1

6

23.0

9.1

6

30.0

9.1

6

07.1

0.1

6

14.1

0.1

6

21.1

0.1

6

28.1

0.1

6

EU

Rb

n

EU

Rb

n

Weekly purchases Total volume (rhs)

0

20

40

60

80

100

120

140

160

180

200

0

2

4

6

8

10

12

14

Oct-14

Nov-

14D

ec-

14Ja

n-1

5F

eb-1

5M

ar-

15

Apr-

15

May-

15

Jun-1

5Ju

l-15

Aug-1

5S

ep-1

5O

ct-15

Nov-

15D

ec-

15Ja

n-1

6F

eb-1

6M

ar-

16

Apr-

16

May-

16

Jun-1

6Ju

l-16

Aug-1

6S

ep-1

6

EU

Rb

n

EU

Rb

nPrimary market Secondary market Total volume (rhs)

Source: Bloomberg, NORD/LB Fixed Income Research Source: ECB, NORD/LB Fixed Income Research

Total volume of covered bond purchase programmes [EURbn]

0

50

100

150

200

250

Jul-0

9

Nov

-09

Ma

r-10

Jul-1

0

Nov

-10

Ma

r-11

Jul-1

1

Nov

-11

Ma

r-12

Jul-1

2

Nov

-12

Ma

r-13

Jul-1

3

Nov

-13

Ma

r-14

Jul-1

4

Nov

-14

Ma

r-15

Jul-1

5

Nov

-15

Ma

r-16

Jul-1

6

CBPP1 [EUR 14,1bn] CBPP2 [EUR 7,1bn] CBPP3 [EUR 197,6bn]

Source: Bloomberg, NORD/LB Fixed Income Research current volume in [ ]

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 15 of 27

PSPP overview

Weekly purchase volume [EUR bn] Distribution by country at month-end [EUR bn]

800

850

900

950

1000

1050

1100

1150

5

7

9

11

13

15

17

19

19.0

8.1

6

26.0

8.1

6

02.0

9.1

6

09.0

9.1

6

16.0

9.1

6

23.0

9.1

6

30.0

9.1

6

07.1

0.1

6

14.1

0.1

6

21.1

0.1

6

28.1

0.1

6

Weekly purchases Total volume (rhs)

0

20

40

60

80

100

120

140

160

180

200

220

240

EU

Rb

n

Source: Bloomberg, NORD/LB Fixed Income Research Source: ECB, NORD/LB Fixed Income Research

Overall distribution of PSPP buying at month-end (EURbn)

Country Adjusted

distribution key1

Purchases (EUR m)

Expected purchases (EUR m)

2

Difference (EUR m)

Average time to maturity in

years

Market average in years

3

Difference in years

DE 26.3% 237,884 241,469 -3,585 7.69 13.75 -6.1

FR 20.7% 188,929 191,370 -2,441 7.70 11.27 -3.6

IT 18.0% 164,352 165,499 -1,147 9.20 7.17 2.0

SNAT 0.0% 114,275 116,537 -2,262 7.12 11.13 -4.0

ES 12.9% 117,900 118,702 -802 9.64 7.24 2.4

NE 5.9% 53,114 53,726 -612 7.76 12.30 -4.5

BE 3.6% 32,742 33,225 -483 9.92 14.42 -4.5

AT 2.9% 25,984 26,364 -380 9.23 12.38 -3.1

PT 2.6% 20,818 22,552 -1,734 9.91 7.18 2.7

FI 1.8% 16,683 16,888 -205 7.56 10.42 -2.9

IE 1.7% 14,934 15,396 -462 9.25 11.23 -2.0

SK 1.1% 7,413 8,986 -1,573 7.85 9.25 -1.4

SI 0.5% 4,105 4,437 -332 8.25 8.86 -0.6

LU 0.3% 1,621 2,154 -533 5.81 13.88 -8.1

LV 0.4% 1,122 1,718 -596 6.59 6.90 -0.3

LT 0.6% 1,892 2,817 -925 6.42 6.60 -0.2

MT 0.1% 609 729 -120 10.75 9.69 1.1

CY 0.2% 269 1,607 -1,338 5.10 6.10 -1.0

EE 0.3% 66 603 -537 1.87 0.00 1.9

GR 0.0% 0 0

0.00 13.06 -

Total / average

100.0% 1.004.712 - - 8.28 9.35 -1.1

1 Based on the ECB capital key, adjusted to include supras and the disqualification of Greece

.

2 Based on the adjusted distribution key.

3 Weighted average time to maturity of the bonds eligible for purchasing under the PSPP.

Source: ECB, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 16 of 27

Covered Bonds Charts & Graphs

Outstanding volume (Bmk.) Top 10 countries (Bmk.)

20,7%

19,8%

11,6%8,1%

4,9%

4,9%

4,4%

4,3%

3,1%

2,8%

15,3%

EUR 1062,8bn

FR

ES

DE

IT

GB

NL

CA

NO

SE

AT

Others

Country Vol. (€bn) No. of CBs ØVol. (€bn) Vol. weight.

ØMod. Duration

FR 219,5 168 1,3 4,2

ES 210,8 161 1,3 3,0

DE 123,2 188 0,7 3,9

IT 86,4 90 1,0 3,5

GB 52,3 44 1,2 3,7

NL 51,7 41 1,3 4,5

CA 47,1 38 1,2 3,6

NO 46,2 45 1,0 3,3

SE 33,2 33 1,0 3,7

AT 29,5 48 0,6 3,2

Issue volume by year (Bmk.) Maturities next 12 months (Bmk.)

0

50

100

150

200

250

300

350

2011 2012 2013 2014 2015 2016

EU

Rb

n

ATAUBECACHCYCZDEDKESFIFRGBGRHUIEITLUNLNONZPLPTSESGTR

0

5

10

15

20

25

30

35

40

11/1

6

12/1

6

01/1

7

02/1

7

03/1

7

04/1

7

05/1

7

06/1

7

07/1

7

08/1

7

09/1

7

10/1

7

EU

Rb

n

AUBECACHCYCZDEDKESFIFRGBGRHUIEITLUNLNONZPLPTSESGTR

Avg. mod. duration by country (vol. weighted) Rating distribution (vol. weighted)

0

1

2

3

4

5

6

AT

AU

BE

CA

CH

CZ

DE

DK

ES FI

FR

GB IE IT LU

NL

NO

NZ

PL

PT

SE

SG

67,9%

4,3%11,5%

0,8%

5,4%

3,8%0,2% 3,4%

2,2%

0,6%0,0%

6,1%

AAA/Aaa

AA+/Aa1

AA/Aa2

AA-/Aa3

A+/A1

A/A2

A-/A3

BBB+/Baa1

BBB/Baa2

BBB-/Baa3

BB+/Ba1

BB/Ba2

BB-/Ba3

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 17 of 27

Covered Bonds Charts & Graphs

Spread development (last 15 issues)

BR

F 0

1/2

10/0

1/2

6

DG

HY

P 0.0

5 1

2/0

6/2

4

ND

B 0

1/4

10/2

8/2

6

AC

AS

CF 0

1/4

10/3

1/2

6

PK

OB

HB

0 1

/8 0

6/2

4/2

2

SN

SB

NK

0 3

/4 1

0/2

4/3

1

FB

AV

P 0

10/2

4/2

3

BM

O 0

.1 1

0/2

0/2

3

SA

BS

M 0

1/8

10/2

0/2

3

CA

ZA

R 0

1/4

10/1

8/2

3

CA

RPP 1 0

9/3

0/3

1

CA

RPP 0 1

/4 0

9/3

0/2

4

AS

BB

NK

0 1

/8 1

0/1

8/2

3

SH

BA

SS

0 1

/8 1

0/0

5/2

6

NA

CN

0 0

9/2

9/2

3

-20

-10

0

10

20

30

40

50

bp

Reoffer Spread Current ASW

Bid-to-Cover (last 15 issues)

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0,0

0,5

1,0

1,5

2,0

2,5

BR

F 0

1/2

10/0

1/2

6

DG

HY

P 0

.05 1

2/0

6/2

4

ND

B 0

1/4

10/2

8/2

6

AC

AS

CF 0

1/4

10/3

1/2

6

PK

OB

HB

0 1

/8 0

6/2

4/2

2

SN

SB

NK

0 3

/4 1

0/2

4/3

1

FB

AV

P 0

10/2

4/2

3

BM

O 0

.1 1

0/2

0/2

3

SA

BS

M 0

1/8

10/2

0/2

3

CA

ZA

R 0

1/4

10/1

8/2

3

CA

RP

P 1

09/3

0/3

1

CA

RP

P 0

1/4

09/3

0/2

4

AS

BB

NK

0 1

/8 1

0/1

8/2

3

SH

BA

SS

0 1

/8 1

0/0

5/2

6

NA

CN

0 0

9/2

9/2

3

EU

Rb

n

Amt. Issued Order Book Bid-to-Cover (rhs)

Spread development by country Performance (total return)

-40 -30 -20 -10 0 10 20

TRSGSEPTNZNONLITIE

GBFRFI

ES - SingleES - Multi

DKDECHCABEAU

bpΔ 3 Months Δ Week Δ Month

0% 5% 10% 15% 20%

Overall

1-3Y

3-5Y

5-7Y

7-10Y

2016 ytd

2015

2014

2013

2012

2011

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 18 of 27

Covered Bonds Charts & Graphs

Germany & Austria France

-30

-20

-10

0

10

20

30

40

50

0 1 2 3 4 5 6 7 8 9 10

AS

W in b

p

years to maturity

AT DE - Öpfe DE - Hypfe DE - Others

-30

-25

-20

-15

-10

-5

0

0 1 2 3 4 5 6 7 8 9 10

AS

W in b

p

years to maturityOF OH Structured

Nordics Other Core

-20

-15

-10

-5

0

5

10

0 1 2 3 4 5 6 7 8 9 10

AS

W in b

p

years to maturityDK FI NO SE

-20

-15

-10

-5

0

5

10

15

0 1 2 3 4 5 6 7 8 9 10

AS

W in b

p

years to maturityBE CH GB LU NL

Overseas & Others Periphery

0

50

100

150

200

250

300

-15

-10

-5

0

5

10

15

20

25

0 1 2 3 4 5 6 7 8 9 10

AS

W in p

b

AS

W in b

p

years to maturityAU CA NZ SG TR (rhs.)

-30

-10

10

30

50

70

90

110

0 1 2 3 4 5 6 7 8 9 10

AS

W in b

p

years to maturity

ES - Single ES - Multi IE IT PT

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 19 of 27

SSA Charts & Graphs

Outstanding volume (Bmk.) Top 10 countries (Bmk.)

38,2%

37,4%

11,2%

4,2%

4,1%1,5%

1,0%

0,7%

0,3%

0,3%

1,0%

4,9%

EUR 1454,1bn GE

SNAT

FR

NE

SP

AS

CA

IT

PO

FI

Others

Country Vol. (€bn) No. of bonds

ØVol. (€bn) Vol. weight.

ØMod. Duration

GE 555,2 476 1,2 4,3

SNAT 543,5 128 4,2 6,9

FR 163,5 105 1,6 5,5

NE 60,4 56 1,1 4,7

SP 60,1 60 1,0 3,4

AS 22,4 22 1,0 6,9

CA 15,1 11 1,4 5,1

IT 9,9 10 1,0 8,5

PO 4,8 8 0,6 4,0

FI 4,3 5 0,9 5,9

Issue volume by year (Bmk.) Maturities next 12 months (Bmk.)

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2016e

EU

Rb

n

Other

ES

AT

NL

FR

GE

SNAT

0

5

10

15

20

25

3011

/16

12

/16

01

/17

02

/17

03

/17

04

/17

05

/17

06

/17

07

/17

08

/17

09

/17

10

/17

EU

Rb

n

Other

ES

AT

NL

FR

GE

SNAT

Avg. mod. duration by country (vol. weighted) Rating distribution (vol. weighted)

0

1

2

3

4

5

6

7

8

9

GE

SN

AT

FR

NE

SP

AS

CA IT

PO FI

44,2%

12,7%

28,4%

7,6%

0,4%2,8%

0,9%

0,4%0,2%

1,0%

2,8%

AAA/Aaa

AA+/Aa1

AA/Aa2

AA-/Aa3

A+/A1

A/A2

A-/A3

BBB+/Baa1

BBB/Baa2

BBB-/Baa3

BB+/Ba1

BB/Ba2

BB-/Ba3

B+/B1

B/B2

B-/B3

NR

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 20 of 27

SSA Charts & Graphs

Spread development (last 15 issues) S

CH

HO

L 0

.05 1

1/0

4/2

4

(fix

ed

)

RE

SF

ER

1 1

1/0

9/3

1

(fix

ed

)

NR

W 1

10/1

6/4

6 (

fixed)

KO

MM

UN

0 7

/8 1

1/0

3/3

6

(fix

ed

)

RE

NTE

N 0

5/8

10/3

1/3

6

(fix

ed

)

EIB

0 0

3/1

3/2

6 (

fix

ed

)

IBR

D 0

5/8

01/1

2/3

3

(fix

ed

)

TH

RG

N 0

.2 1

0/2

6/2

6

(fix

ed

)

BN

G 0

7/8

10/2

4/3

6 (

fixed)

IBB

SH

0 1

0/2

0/2

0

(flo

atin

g)

SA

GE

SS

0 5

/8 1

0/2

0/2

8

(fix

ed

)

FM

SW

ER

0 1

0/2

0/2

0

(fix

ed

)

BR

AB

UR

0 1

/4 1

0/1

9/2

6

(fix

ed

)

SF

ILF

R 0

1/8

10/1

8/2

4

(fix

ed

)

ES

M 0

10/1

8/2

2 (

fixed)

-40

-30

-20

-10

0

10

20

30

bp

Reoffer Spread / DM Current ASW / DM

Spread development by country Performance (total return)

-30 -25 -20 -15 -10 -5 0 5

GE

SNAT

FR

SP

NE

AS

bp1W 1M 3M

-5% 0% 5% 10% 15% 20% 25% 30%

Overall

1-3

3-5

5-7

7-10

10+

YTD

2015

2014

2013

2012

2011

Performance (total return) – 2015 Performance (total return) – 2015

-2% -1% 0% 1% 2% 3% 4% 5%

Supras

Agencies

Public Banks

Regions

Bundesländer

Periphery

Non-Periphery

1W

1M

3M

6M

12M

YTD

-2% -1% 0% 1% 2% 3% 4% 5% 6%

Overall

AAA

AA

A

BBB

1W

1M

3M

6M

12M

YTD

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 21 of 27

SSA Charts & Graphs

Germany (by segments) France (by risk weight)

-60

-50

-40

-30

-20

-10

0

0 1 2 3 4 5 6 7 8 9 10

AS

W in

bp

years to maturity

National agencies Bundesländer Regional agencies Bunds

-50

-40

-30

-20

-10

0

10

20

30

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

AS

W in

bp

years to maturity

RW: 0% RW: 20% OATs

Netherlands & Austria Supranationals

-60

-50

-40

-30

-20

-10

0

10

20

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

AS

W in

bp

years to maturity

Dutch agencies DSLs Austria Austrian agencies

-60

-50

-40

-30

-20

-10

0

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

AS

W in

bp

years to maturity

Supranationals Supranationals Bunds OATs

Core Periphery

-40

-30

-20

-10

0

10

0 1 2 3 4 5 6 7 8 9 10

AS

W in

bp

years to maturityGerman nat. agencies Bundesländer

German reg. agencies French RW: 0%

French RW: 20% Dutch agencies

Austrian agencies Supras

-50

0

50

100

150

200

250

300

350

400

0 1 2 3 4 5 6 7 8 9 10

AS

W in

bp

years to maturity

Spanish agencies Spanish regions Italian agencies

Portuguese agencies Bonos BTPs

Portugal

Source: Bloomberg, NORD/LB Fixed Income Research

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 22 of 27

Appendix Publication overview

Publication Topics

42/2016 26 October Market overview

Nowotny believes CBPP3 limits have been reached

Public Sector Programmes from Austria

ECB Meeting of the Governing Council in the aftermath

ECB Tracker

41/2016 19 October Market overview

Moody’s concludes rating review following HETA deal

DEPFA ACS and DEPFA PBI reduce outstanding issuance and

cover pool volumes

Agreement reached on the Federal Financial Equalisation System

ECB Tracker

40/2016 12 October Market overview

BNP Paribas Fortis is about to launch its first EUR benchmark

SNS Bank is renamed “de Volksbank”

PSPP holdings – an overview

ECB Tracker

39/2016 05 October Market overview

Deutsche Bank Pfandbriefe could face higher volatility in the short term

Nordea restructuring forges ahead

ESM and EFSF present funding plan for Q4

ECB Tracker

38/2016 28 September Market overview

PKO Bank to issue its first EUR benchmark shortly?

Will regional elections in Spain bring an movement to the political deadlock?

ECB Tracker

38/2016 28 September Market overview

PKO Bank to issue its first EUR benchmark shortly?

Will regional elections in Spain bring an movement to the political deadlock?

ECB Tracker

37/2016 21 September Market overview

DBS Bank issues inaugural covered bond in euro

Belgian regions as an investment alternative?

ECB Tracker

36/2016 14 September Market overview

Repayment structures in the covered bond market

Municipal Schuldscheindarlehen (SSDs) trending

ECB Tracker

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 23 of 27

Appendix Contacts

Fixed Income Research

Michael Schulz Head +49 511 361-5309 [email protected]

Kai Ebeling Covered Bonds +49 511 361-9713 [email protected]

Mario Gruppe Public Issuers +49 511 361-9787 [email protected]

Michaela Hessmert Banks +49 511 361-6915 [email protected]

Melanie Kiene Banks +49 511 361-4108 [email protected]

Jörg Kuypers Corporates / Retail Products +49 511 361-9552 [email protected]

Matthias Melms Covered Bonds +49 511 361-5427 [email protected]

Sascha Remus Corporates / Retail Products +49 511 361-2722 [email protected]

Norman Rudschuck Public Issuers +49 511 361-6627 [email protected]

Thomas Scholz Corporates / Retail Products +49 511 361-4710 [email protected]

Martin Strohmeier Corporates / Retail Products +49 511 361-4712 [email protected]

Kai Witt Corporates / Retail Products +49 511 361-4639 [email protected]

Markets Sales

Carsten Demmler Head +49 511 361-5587 [email protected]

Institutional Sales (+49 511 9818-9440)

Daniel Gutschka (Head) [email protected] Gabriele Schneider [email protected]

Thorsten Bock [email protected] Dirk Scholden [email protected]

Uwe Kollster [email protected] Uwe Tacke [email protected]

Daniel Novotny-Farkas [email protected]

Sales Savings Banks / Regional Banks (+49 511 9818-9400)

Christian Schneider (Head) [email protected] Martin Koch [email protected]

Oliver Bickel [email protected] Bernd Lehmann [email protected]

Tobias Bohr [email protected] Jörn Meißner [email protected]

Kai-Ulrich Dörries [email protected] Lutz Schimanski [email protected]

Jan Dröge [email protected] Ralf Schirrling [email protected]

Sascha Goetz [email protected] Brian Zander [email protected]

Stefan Krilcic [email protected]

Sales Asia (+65 64 203136)

Jefferson Ko [email protected] Muhammad Peter Shepherd

Fixed Income / Structured Products Sales Europe (+352 452211-515)

René Rindert (Head) [email protected] Toni Martikainen [email protected]

Morgan Kermel [email protected] Laurence Payet [email protected]

Patricia Lamas [email protected]

Corporate Sales

Shipping / Aircraft +49 511 9818-8150 Corporate Clients +49 511 9818-4003

Real Estate / Structured Finance

+49 511 9818-8150 FX/MM +49 511 9818-4006

Syndicate / DCM (+49 511 9818-6600)

Thomas Cohrs (Head) [email protected] Wlada Pesotska [email protected]

Axel Hinzmann [email protected] Andreas Raimchen [email protected]

Thomas Höfermann [email protected] Udo A. Schacht [email protected]

Alexander Malitsky [email protected] Marco da Silva [email protected]

Julien Marchand [email protected]

Financial Markets Trading

Corporates +49 511 9818-9690 Collat. Mgmt / Repos +49 511 9818-9200

Covereds / SSAs +49 511 9818-8040 Cust. Exec. & Trading +49 511 9818-9480

Financials +49 511 9818-9490 Frequent Issuers +49 511 9818-9640

Governments +49 511 9818-9660 Structured Products +49 511 9818-9670

Länder & Regionen +49 511 9818-9550

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 24 of 27

Disclaimer

This investment recommendation/investment strategy recommendation (hereinafter the „Investment Recommendation”) was drawn up

by NORDDEUTSCHE LANDESBANK GIROZENTRALE („NORD/LB“). The supervisory authorities in charge of NORD/LB are the Euro-

pean Central Bank („ECB“), Sonnemannstraße 20, D-60314 Frankfurt am Main, and the Federal Financial Supervisory Authority (Bun-

desanstalt für Finanzdienstleitungsaufsicht - „BaFin“), Graurheindorfer Str. 108, D-53117 Bonn, and Marie-Curie-Str. 24-28, D-60439

Frankfurt am Main. Details about the extent of NORD/LB´s regulation by the respective authorities are available on request. Generally,

this Investment Recommendation or the products or services described therein have not been reviewed or approved by the competent

supervisory authority.

This Investment Recommendation is addressed exclusively to recipients which are professional and institutional clients in Germany, the

United Kingdom, Austria, Belgium, Italy, Spain, Denmark, Finland, Estonia, France, Greece, Ireland, Luxembourg, the Netherlands,

Poland, Portugal, Sweden, the Czech Republic, Canada, Switzerland and Cyprus (hereinafter the „Relevant Persons” or „Recipients”).

The contents of this Investment Recommendation are disclosed to the Recipients on a strictly confidential basis and, by accepting this

Investment Recommendation, the Recipients agree that they will not forward to third parties, copy and/or reproduce this Investment

Recommendation without NORD/LB’s prior written consent. The figures discussed in this Investment Recommendation are only ad-

dressed to the Relevant Persons and any persons other than the Relevant Persons must not rely on this Investment Recommendation.

In particular, neither this Investment Recommendation nor any copy thereof must be forwarded or transmitted to the United States of

America or its territories or possessions or distributed to any employees or affiliates of Recipients resident in these jurisdictions.

This Investment Recommendation was drawn up in compliance with the applicable provisions of the German Securities Trading Act

(Wertpapierhandelsgesetz) and the Regulation Governing the Analysis of Financial Instruments (Verordnung über die Analyse von

Finanzinstrumenten). In organizational, hierarchical, functional and local terms, the Research Division of NORD/LB is independent of any

divisions responsible for the issuance of securities and investment banking activities, for trading (including proprietary trading) in and

sales of securities as well as for lending activities.

This Investment Recommendation and the information contained herein have been compiled and are provided exclusively for information

purposes. This Investment Recommendation is not intended as an investment incentive. It is provided for the Recipient’s personal infor-

mation, subject to the express understanding, which is acknowledged by the Recipient, that it does not constitute any direct or indirect

offer, individual recommendation, solicitation to purchase, hold or sell or to subscribe for or acquire any securities or other financial

instruments nor any measure by which financial instruments might be offered or sold.

All actual details, information and statements contained herein were derived from sources considered reliable by NORD/LB. However,

since these sources are not verified independently, NORD/LB cannot give any assurance as to or assume responsibility for the accuracy

and completeness of the information contained herein. The opinions and prognoses given herein on the basis of these sources consti-

tute a non-binding evaluation by the analysts of NORD/LB. Any changes in the underlying premises may have a material impact on the

developments described herein. Neither NORD/LB nor its governing bodies or employees can give any assurance as to or assume any

responsibility or liability for the accuracy, adequacy and completeness of this Investment Recommendation or any loss of return, any

indirect, consequential or other damage which may be suffered by persons relying on the information or any statements or opinions set

forth in this Investment Recommendation (irrespective of whether such losses are incurred due to any negligence on the part of these

persons or otherwise).

Past performances are not a reliable indicator of future performances. Exchange rates, price fluctuations of the financial instruments and

similar factors may have a negative impact on the value and price of and return on the financial instruments referred to herein or any

instruments linked thereto. An evaluation made on the basis of the historical performance of any security does not necessarily give an

indication of its future performance.

This Investment Recommendation neither constitutes any investment, legal, accounting or tax advice nor any representation that an

investment or strategy is suitable or appropriate in the light a Recipient’s individual circumstances, and nothing in this Investment Rec-

ommendation constitutes a personal recommendation to the Recipient thereof. The securities or other financial instruments referred to

herein may not be suitable for the Recipient’s personal investment strategies and objectives, financial situation or individual needs.

Also this Investment Recommendation as a whole or any part thereof is not a sales or other prospectus. Correspondingly, the infor-

mation contained herein merely constitutes an overview and does not form the basis for an investor‘s potential decision to buy or sell. A

full description of the details relating to the financial instruments or transactions which may relate to the subject matter of this Investment

Recommendation is set forth in the relevant (financing) documentation. To the extent that the financial instruments described herein are

NORD/LB’s own issues and subject to the requirement to publish a prospectus, the conditions of issue applicable to any individual finan-

cial instrument and the relevant prospectus published with respect thereto as well NORD/LB’s relevant registration form, all of which are

available for downloading at www.nordlb.de and may be obtained, free of charge, from NORD/LB, Georgsplatz 1, 30159 Hanover, shall

be solely binding. Any potential investment decision should at any rate be made exclusively on the basis of such (financing) documenta-

tion. This Investment Recommendation cannot replace personal advice. Before making an investment decision, each Recipient should

consult an independent investment adviser for individual investment advice with respect to the appropriateness of an investment in

financial instruments or investment strategies as contemplated herein as well as for other and more recent information on certain in-

vestment opportunities.

Each of the financial instruments referred to herein may involve substantial risks, including capital, interest, index, currency and credit

risks, political, fair value, commodity and market risks. The financial instruments could experience a sudden substantial deterioration in

value, including a total loss of the capital invested. Each transaction should only be entered into on the basis of the relevant investor’s

assessment of its individual financial situation as well as of the suitability and risks of the investment.

NORD/LB and its affiliates may, for their own account or for the account of third parties, participate in transactions involving the financial

instruments described herein or any underlying assets, issue further financial instruments having terms that are the same as or similar to

those governing the financial instruments referred to herein as well as enter into transactions to hedge positions. Such actions may affect

the price of the financial instruments described in this Investment Recommendation.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 25 of 27

To the extent the financial instruments referred to herein are derivatives, they may involve an initial negative market value from the

customer’s point of view, depending on the terms and conditions prevailing as of the transaction date. Furthermore, NORD/LB reserves

the right to pass on its economic risk from any derivative transaction it has entered into to third parties in the market by way of a mirror

image counter-transaction.

Further information on any fees which may be included in the sales price is set forth in the brochure „Customer Information Relating to

Securities Transactions“ which is available at www.nordlb.de.The information set forth in this Investment Recommendation shal l super-

sede all previous versions of any relevant Investment Recommendation and refer exclusively to the date as of which this Investment

Recommendation has been drawn up. Any future versions of this Investment Recommendation shall supersede this present version.

NORD/LB shall not be under any obligation to update and/or review this Investment Recommendation at regular intervals. Therefore, no

assurance can be given as to its currentness and continued accuracy.

By making use of this Investment Recommendation, the Recipient shall accept the foregoing terms and conditions.

NORD/LB is a member of the protection scheme of Deutsche Sparkassen-Finanzgruppe. Further information for the Recipient is set

forth in clause 28 of the General Terms and Conditions of NORD/LB or at www.dsgv.de/sicherungssystem.

Additional information for recipients in the UK

NORD/LB subject to limited regulation by the Financial Conduct Authority (“FCA”) und Prudential Regulation Authority (“PRA”). Details

about the extent of our regulation by the FCA and PRA are available from NORD/LB on request.

This Investment Recommendation is a financial promotion. Relevant Persons in the UK should contact NORD/LB’s London Branch,

Investment Banking Department, Telephone: 0044 / 2079725400 with any queries.

Investing in financial instruments referred to in this Investment Recommendation may expose an investor to a significant risk of losing all

of the amount invested.

Additional information for recipients in France

NORD/LB is partially regulated by the Autorité des Marchés Financiers for the conduct of French business. Details about the extent of

our regulation by the respective authorities are available from us on request.

This Investment Recommendation constitutes investment research within the meaning of Article 24(1) Directive 2006/73/EC, Article

L.544-1 and R.621-30-1 of the French Monetary and Financial Code and does qualify as research recommendation under Directive

2003/6/EC and Directive 2003/125/EC.

Additional information for recipients in Austria

None of the information contained in this Investment Recommendation constitutes a solicitation or offer by NORD/LB or its affiliates to

buy or sell any securities, futures, options or other financial instruments or to participate in any other strategy. Only the published pro-

spectus pursuant to the Austrian Capital Market Act should be the basis for any investment decision of the Recipient.

For regulatory reasons, products mentioned in this Investment Recommendation may not being offered into Austria and are not available

to investors in Austria. Therefore, NORD/LB might not be able to sell or issue these products, nor shall it accept any request to sell or

issues these products, to investors located in Austria or to intermediaries acting on behalf of any such investors.

Additional information for recipients in Belgium

Evaluations of individual financial instruments on the basis of past performance are not necessarily indicative of future results. It should

be noted that the reported figures relate to past years.

Additional information for recipients in Cyprus

This Investment Recommendation constitutes investment research within the meaning of the definition section of the Cyprus Directive

D1444-2007-01(No 426/07). Furthermore, this material is provided for informational and advertising purposes only and does not consti-

tute an invitation or offer to sell or buy or subscribe any investment product.

Additional information for recipients in Denmark

This Investment Recommendation does not constitute a prospectus under Danish securities law and consequently is not required to be

nor has been filed with or approved by the Danish Financial Supervisory Authority as this Investment Recommendation either (i) has not

been prepared in the context of a public offering of securities in Denmark or the admission of securities to trading on a regulated market

within the meaning of the Danish Securities Trading Act or any executive orders issued pursuant thereto, or (ii) has been prepared in the

context of a public offering of securities in Denmark or the admission of securities to trading on a regulated market in reliance on one or

more of the exemptions from the requirement to prepare and publish a prospectus in the Danish Securities Trading Act or any executive

orders issued pursuant thereto.

Additional information for recipients in Greece

The information contained herein describes the view of the author at the time of its publication and it must not be used by its Recipient

unless having first confirmed that it remains accurate and up to date at the time of its use.

Past performance, simulations or forecasts are therefore not a reliable indicator of future results. Mutual funds have no guaranteed

performance and past returns do not guarantee future performance.

Additional information for recipients in Ireland

This Investment Recommendation has not been prepared in accordance with Directive 2003/71/EC, as amended, on prospectuses (the

“Prospectus Directive”) or any measures made under the Prospectus Directive or the laws of any Member State or EEA treaty adherent

state that implement the Prospectus Directive or those measures and therefore may not contain all the information required where a

document is prepared pursuant to the Prospectus Directive or those laws.

Additional information for recipients in Luxembourg

Under no circumstances shall this Investment recommendation constitute an offer to sell, or issue or the solicitation of an offer to buy or

subscribe for Products or Services in Luxembourg.

Covered Bond & SSA View 2 November 2016

NORD/LB Fixed Income Research

Page 26 of 27

Additional information for recipients in Netherlands

The value of your investments may fluctuate. Results achieved in the past do not offer any guarantee for the future (De waarde van uw

belegging kan fluctueren. In het verleden behaalde resultaten bieden geen garantie voor de toekomst).

Additional information for recipients in Poland

This Investment Recommendation does not constitute a recommendation within the meaning of the Regulation of the Polish Minister of

Finance Regarding Information Constituting Recommendations Concerning Financial Instruments or Issuers thereof dated 19 October

2005.

Additional information for recipients in Portugal

This Investment Recommendation is intended only for institutional clients and may not be (i) used by, (ii) copied by any means or (iii)

distributed to any other kind of investor, in particular not to retail clients. This Investment Recommendation does not constitute or form

part of an offer to buy or sell any of the securities covered by the report nor can be understood as a request to buy or sell securities

where that practise may be deemed unlawful. This Investment Recommendation is based on information obtained from sources which

we believe to be reliable, but is not guaranteed as to accuracy or completeness. Unless otherwise stated, all views herein contained are

solely expression of our research and analysis and subject to change without notice.

Additional information for recipients in Sweden

This Investment Recommendation does not constitute or form part of, and should not be construed as a prospectus or offering memo-

randum or an offer or invitation to acquire, sell, subscribe for or otherwise trade in shares, subscription rights or other securities nor shall

it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. This Investment Recom-