covid-19 will intensify pre-existing recycling trends

TRANSCRIPT

COVID-19 will intensify pre-existing recycling trends

Copyright 2020 Reed Business Information Ltd. ICIS is a member of RBI and is part of RELX Group plc. ICIS accepts no liability for commercial decisions based on this content.

COVID-19 WILL INTENSIFY PRE-EXISTING RECYCLING SUPPLY/DEMAND TRENDS IN THE MID- TO LONG-TERM | 2

Although the coronavirus pandemic has seen demand for recycled material from all end-uses fall, and resulted in margin lost throughout most of the chain, in the longer-term it could intensify pre-existing fault lines in the market between packaging and non-packaging demand and deepen the structural shortage of packaging suitable material.

With consumer pressure dormant but not dissipated, and regulation likely to intensify in any post-COVID reconstruction this would heighten competition among Fast Moving Consumer Goods (FMCG) firms for high quality grades of material such as recycled high density polyethylene (PE) blow-moulding natural material, which ICIS began pricing on 21 May.

Prior to the spread of the COVID-19 pandemic high consumer and regulatory pressure resulted in a slew of FMCG brand commitments to sustainability targets of up to 50% recycled content by 2025, which has outpaced the volume of packaging-suitable material available in the market, as we’ve detailed in previous insight pieces.

This has caused a two-tier market to develop between grades suitable for packaging applications – where the need to meet sustainability targets has typically taken precedence over the need to price competitively with virgin – and non-packaging applications – which continue to purchase predominantly for cost-saving against virgin.

The result has been a weakening in the relationship between virgin and recycled polymer grades serving the packaging industry.

This is most clearly seen with R-PET where food-grade pellet prices are now almost double virgin values.

R-PET is the most established of the recycled polymer markets, and the industry where regulatory targets are most pressing, with an EU requirement that all R-PET bottle contain 25% recycled content by 2025.

It is not, however, isolated to R-PET. Blow-moulding R-HDPE natural pellet values are currently 50-65% above virgin HDPE blow-moulding spot values.

The actual difference is even more stark because virgin HDPE is priced on a free-delivered basis, while R-HDPE natural blow-moulding pellets typically trade on an ex-works basis.

Even R-HDPE injection moulding natural pellets have been trading above virgin values since the fourth quarter of 2019 due to structural shortages.

COVID-19 will intensify pre-existing recycling trends

MARK VICTORY JUNE 2020

R-PET price mid-point minus virgin PET domestic spot price mid-point

Colourless flake FD NWE Food Grade Pellet

20092010

20112012

20132014

20152016

20172018

20192020

Copyright 2020 Reed Business Information Ltd. ICIS is a member of RBI and is part of RELX Group plc. ICIS accepts no liability for commercial decisions based on this content.

COVID-19 WILL INTENSIFY PRE-EXISTING RECYCLING SUPPLY/DEMAND TRENDS IN THE MID- TO LONG-TERM | 3

With increased demand from packaging (along with more complex virgin packaging designs that have raised sorting costs) and insufficient waste supply to meet that demand, post-consumer and post-industrial waste prices have broadly risen across the past decade.

Despite this, the spread between grades of flakes and pellets most commonly used in packaging applications has broadly increased over the past decade, while conversion costs have broadly remained static (although the increased complexity of packaging has seen a rise in wastage rates), suggesting improved margins.

This is a trend that had been intensifying in the second half of 2019 – particularly for less well established recycled polymer markets – as consumer and regulatory pressure further increased and exacerbated pre-existing structural shortages.

At the same time, macroeconomic weakness in major non-packaging markets such as automotive and construction, along with global virgin polymer capacity expansions

R-HDPE price mid-point minus virgin HDPE film spot price mid-point

R-HDPE GP Black pellets R-HDPE Mixed Coloured Pellets

R-HDPE Natural Pellets

R-HDPE Pipe Grade Black Pellets

Jun 2019

Aug 2019

Dec 2019

Feb 2020

Apr 2020

Jun 2020

Oct 2019

R-HDPE pellet vs mixed-coloured HDPE post-consumer bale spread

General purpose black Natural

Mixed coloured Pipe grade black

Jun 2019

Aug 2019

Dec 2019

Feb 2020

Apr 2020

Jun 2020

Oct 2019

R-RET Food grade pellet spread vs bales

Colourless flake FD NWE Food Grade Pellet

20092008

20072010

20112012

20132014

20152016

20172018

20192020

Copyright 2020 Reed Business Information Ltd. ICIS is a member of RBI and is part of RELX Group plc. ICIS accepts no liability for commercial decisions based on this content.

COVID-19 WILL INTENSIFY PRE-EXISTING RECYCLING SUPPLY/DEMAND TRENDS IN THE MID- TO LONG-TERM | 4

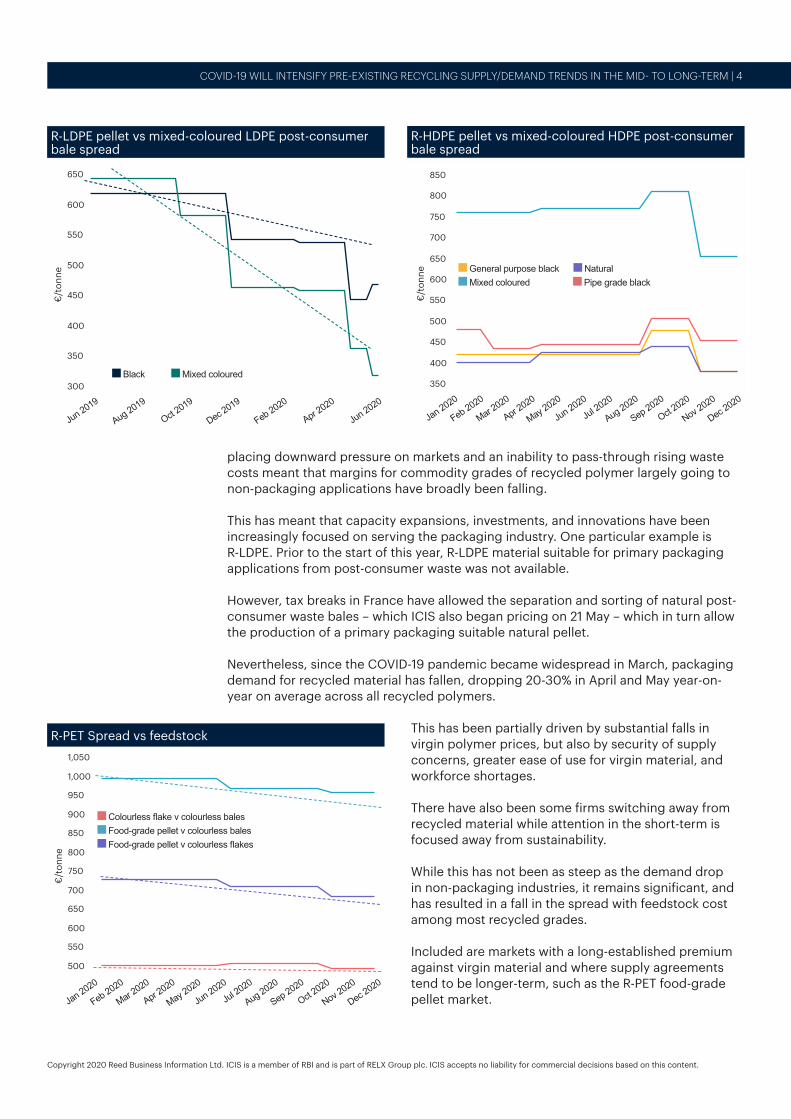

placing downward pressure on markets and an inability to pass-through rising waste costs meant that margins for commodity grades of recycled polymer largely going to non-packaging applications have broadly been falling.

This has meant that capacity expansions, investments, and innovations have been increasingly focused on serving the packaging industry. One particular example is R-LDPE. Prior to the start of this year, R-LDPE material suitable for primary packaging applications from post-consumer waste was not available.

However, tax breaks in France have allowed the separation and sorting of natural post-consumer waste bales – which ICIS also began pricing on 21 May – which in turn allow the production of a primary packaging suitable natural pellet.

Nevertheless, since the COVID-19 pandemic became widespread in March, packaging demand for recycled material has fallen, dropping 20-30% in April and May year-on-year on average across all recycled polymers.

This has been partially driven by substantial falls in virgin polymer prices, but also by security of supply concerns, greater ease of use for virgin material, and workforce shortages.

There have also been some firms switching away from recycled material while attention in the short-term is focused away from sustainability.

While this has not been as steep as the demand drop in non-packaging industries, it remains significant, and has resulted in a fall in the spread with feedstock cost among most recycled grades.

Included are markets with a long-established premium against virgin material and where supply agreements tend to be longer-term, such as the R-PET food-grade pellet market.

R-LDPE pellet vs mixed-coloured LDPE post-consumer bale spread

Black Mixed coloured

Jun 2019

Aug 2019

Dec 2019

Feb 2020

Apr 2020

Jun 2020

Oct 2019

R-HDPE pellet vs mixed-coloured HDPE post-consumer bale spread

General purpose black Natural

Mixed coloured Pipe grade black

Jan 2020

Feb 2020

Mar 2020

Apr 2020

Jun 2020

Aug 2020

Oct 2020

Jul 2

020

Sep 2020

Nov 2020

Dec 2020

May 2020

R-PET Spread vs feedstock

Colourless flake v colourless bales

Food-grade pellet v colourless bales

Food-grade pellet v colourless flakes

Jan 2020

Feb 2020

Mar 2020

Apr 2020

Jun 2020

Aug 2020

Oct 2020

Jul 2

020

Sep 2020

Nov 2020

Dec 2020

May 2020

Copyright 2020 Reed Business Information Ltd. ICIS is a member of RBI and is part of RELX Group plc. ICIS accepts no liability for commercial decisions based on this content.

COVID-19 WILL INTENSIFY PRE-EXISTING RECYCLING SUPPLY/DEMAND TRENDS IN THE MID- TO LONG-TERM | 5

Mark VictorySenior Markets Editor

Mark Victory is one of the Senior Editors for recycling at ICIS (the Independent Commodities Intelligence Service), and is dedicated to expanding its coverage across this vital and growing sector. Mark has been with ICIS since 2008, covering recycling, petrochemical and fertilizer markets – including 8 years as the editor of the R-PET report. Mark is currently the editor of the R-PE and R-PP reports, which he launched in 2019.Prior to joining ICIS, Mark covered international bond, commercial paper and structured product markets.

As the first in our industry to offer a R-LDPE natural waste quotes, ICIS can now provide relevant cost quotes to the nascent R-LDPE primary packaging sector.

Gain an unprecedented holistic view of the R-PE market with new pricing assessments

GET AN UNMATCHED VIEW OF THE MARKET TODAY

The substitution back to virgin caused by COVID-19 resulted in the first fall in R-PET food-grade pellet prices since February 2016.

Uncertainty has also resulted in delays to new project start-ups. This is particularly significant for recycled polyolefin markets where long 18-month testing cycles from the cosmetic and household goods packaging sector were due to complete in the second and third quarters of 2020 and had been expected to result in substantial increases in demand.

While COVID-19 disruption is ongoing there is a deep unwillingness to open new supply routes. There is also an unwillingness to make fresh investments.

This has placed recycling manufacturers under significant pressure. Non-integrated recycling producers typically have lower cash reserves than petrochemical firms and a positive demand outlook led to heavy investment in the build up to the COVID-19 outbreak creating large-scale debts that need to be serviced.

There has been talk across the recycled markets of impending bankruptcies, although there have yet to be any declared.

Nevertheless, the background pressures that existed pre-COVID remain in place. While consumer pressure is not as sharp in current circumstances, it is likely to return as soon as the current crisis is over. Similarly, legislation is likely to build in the post-COVID-19 recovery.

Legislators will be keen to recoup money spent on suring up the economy during the crisis, ‘social’ taxes unlikely to result in much consumer pushback such as recycling legislation are likely to be attractive to Governments.

At the same time, delayed investments, delayed projects and bankruptcies will make it even more difficult to hit 2025 targets and are likely to sharpen the supply/demand imbalance in the mid-to-long term for packaging favoured material, while upstream markets remain pressured by any post-Covid recession that emerges.

COVID-19 might have reversed some of the trends we had been seeing in recycling markets in the short-term, but in the longer term it will have served to entrench them further.